Samsung: Why the Stock Could Soar - Barron's Cover

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

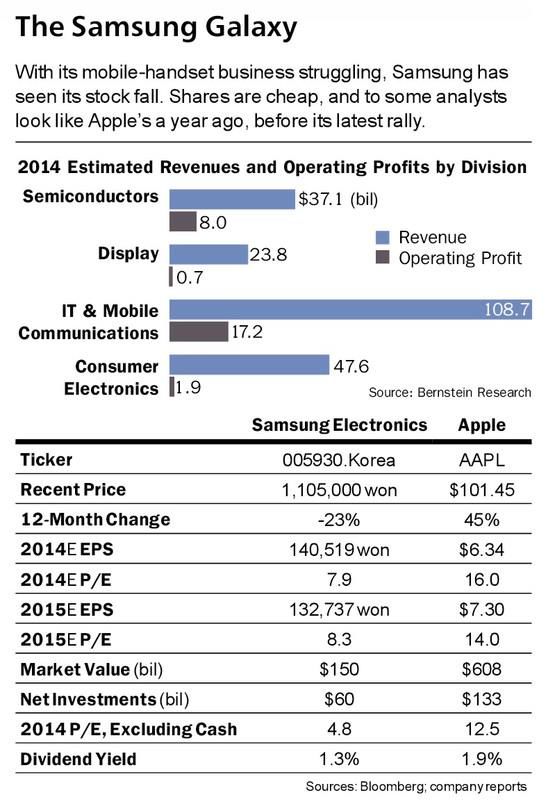

Barron's Cover Samsung: Why the Stock Could Soar It’s hard to think of another huge company with a stock as cheap as South Korea’s Samsung Electronics. Its shares could rally 50%. By Andrew Bary Barron’s, October 11, 2014 http://online.barrons.com/articles/samsung-why-the-stock-could-jump-50-1413005581 Samsung Electronics could be the world’s cheapest mega-cap stock. Just don’t expect it to stay that way. The South Korean maker of cellphones, tablets, memory chips, and big-screen TVs trades for eight times estimated 2014 earnings, and just five times projected profit excluding its massive stash of net cash and investments, which totaled $60 billion at the end of the second quarter. Then again, Samsung itself is a colossus, with $200 billion in expected annual revenue—more than enough to qualify as the largest technology company in the world. It boasts a market value of $150 billion, and accounts for 15% of Korea’s Kospi index. It’s also the biggest company in key developing-country equity indexes.

Lately, Samsung (ticker: 005930.Korea) is very much out of favor with investors, due to plunging profit in its largest business, mobile phones. That has led to fears the company could become the next major casualty in a brutal market that already has claimed former heavyweights Nokia and Motorola, and dashed the fortunes of Canada’s BlackBerry (BBRY). Viewed differently, however, Samsung looks more like the Apple (AAPL) of a year ago. Apple’s shares briefly fell below $60 last year, and traded for about 10 times future earnings, or 6.5 times, excluding cash. Carl Icahn and other shrewd buyers loaded up on the stock, which has rallied 70% since, to $101. Samsung’s upside might not be quite as large, but some bulls think the shares could gain 50%. “The semiconductor division and the cash are worth more than the current market cap,” says Mark Newman, an analyst with Bernstein Research. “That means investors are getting for free the world’s largest maker of handsets, the leading display business, and the biggest and most profitable TV producer.” Newman carries a price target of 1.65 million Korean won, 50% above the current share price of KRW1.1 million. Each Samsung share is worth about $1,030 based on the current exchange rate of KRW1,070 to the dollar. Samsung shares are down 19% this year and hit a new 52-week low this past Friday after the company released disappointing third-quarter profit news. We wrote a favorable story about Samsung in February when the shares were KRW1,275,000 (“Samsung: Ready to Rebound,” Feb. 10). SAMSUNG ALSO HAS preferred shares, which are less liquid than but economically equivalent to the common, and pay a slightly higher dividend. Lacking voting rights, they trade for around KRW824,000, a 25% discount to the common. The Samsung preferred offers an even cheaper way to play an already inexpensive stock. Many Korean companies have preferred shares that trade at a steep discount to their common. Rob Taylor, co-manager of the Oakmark International Fund, a Samsung holder, is bullish on the company’s long-term prospects. Samsung, he notes, has “a strong No. 1 or No. 2 position in all its major markets. Management has been good at looking out over the long term to maintain or improve market position.” Downside in the shares seems limited, as the memory-chip business could generate operating profit of $10 billion next year, up from $8 billion this year, adding even more money to the company’s growing pile of cash. Put a multiple of 10 on next year’s projected semiconductor operating profit, and add the cash and investments, and you’ve exceeded Samsung’s current market value. Net cash and investments now equal 40% of Samsung’s market value.

Samsung trades for just a 5% premium to book value, a level that historically has been a floor for the stock. Book value mostly reflects cash and factories, not intangible items. The company is valued at 50% of annual sales, based on its enterprise value (equity-market value less net cash and investments). Apple is valued at 2.5 times sales. It is possible that an activist investor could surface who would press the company to boost its dividend, which now equates to a 1.3% yield, or repurchase shares, which it hasn’t done since 2007. In this way, too, Samsung resembles the Apple of the past, which was returning none of its cash to shareholders in the form of dividends or buybacks. It isn’t easy, however, to pressure family-controlled Korean companies like Samsung. The insular Lee family, which controls the stock, is unlikely to engage an activist the way Apple did Icahn.

SAMSUNG’S SHARPLY lower cellphone profit is weighing on overall earnings and scaring away investors. In its preliminary financial report for the third quarter, released last week, the company reported operating earnings of about $3.8 billion, below already reduced expectations, and down 60% from the year-earlier period. Estimated cellphone profit plunged by nearly two- thirds, to $1.5 billion. Samsung is being squeezed from above by Apple, and from below by Chinese manufacturers. Apple’s introduction of the larger- screen iPhone 6 could put further pressure on Samsung’s high-end Galaxy S5 and Note 4, which had benefited from a bigger screen than the iPhone 5. Samsung’s smartphones and tablets use Google ’s (GOOGL) Android operating system, which gives phone makers less flexibility than Apple’s iOS. Apple’s biggest bull, Icahn, who owns more than $5 billion of its shares, essentially wrote off Samsung in a letter last week to Apple CEO Tim Cook. He called the iPhone 6 a “superior product” and wrote that a comparison between top-of-the-line Samsung and Apple phones is “analogous to the choice of a Volkswagen over a Mercedes at the same price.” That sounds far too harsh an assessment to Galaxy and Note fans, not to mention some Samsung analysts and investors. “It is ludicrous to compare Samsung to Nokia, BlackBerry, or Motorola,” says Shaun Cochran, the head of Korean research for CLSA in Seoul. “Samsung has a history of reinventing itself time and time again. There is an institutional paranoia, a constant sense of crisis that has helped make Samsung so great.” Cochran says Samsung’s cellphone lineup is far more diversified than Nokia or BlackBerry. He argues that Samsung shares are “close to a bottom,” given support from book value. CLSA has a Buy rating on the stock and a price target of KRW1.5 million. Samsung was the world’s largest maker of cellphones last year, with a 30% share. It is the largest and most profitable maker of memory chips. With a 40% market share in DRAMs, it is the leader of a lucrative oligopoly that includes Micron Technology (MU) and Korea’s SK Hynix (000660.Korea). Samsung also is a top producer of NAND, or solid-state memory, which is replacing disk drives in many technology applications. Samsung is the leading maker globally of displays, which has helped it become No. 1 in TVs, including curved-screen TVs and ultrasize sets with screens of 60 inches or more. Samsung’s next major innovation in cellphones is expected to be foldable screens using its best-in-class OLED display technology, which relies on plastic rather than glass. The OLED screens provide their own light, a big advantage over most existing technology. This could allow the creation of screens that bend or roll, as well as handsets that open into tablets. Expect these Samsung products in 2016. Some of this display technology should be available soon in the new Samsung Galaxy Note Edge “phablet,” a large-size phone whose screen curves around one edge. A demonstration of Samsung’s foldable technology, called YOUM, wowed an audience at last year’s CES (Consumer Electronics Show). A video of the Samsung presentation is available on YouTube.

AS SOUTH KOREA’S most prestigious company, Samsung attracts the best and brightest engineers from the country’s top universities. They work tirelessly in what’s described as a flexible hierarchy, in which each operating business must succeed on its own without help from other parts of the company. This strategy has helped Samsung trump its Japanese rivals, including a now-struggling Sony (SNE). Samsung’s ailing chairman, Lee Kun-hee, 72, once inspired employees with a speech that included a line to “change everything except the wife and kids.” The Lee family, which controls a sprawling Samsung empire, including construction and insurance, might have little interest in seeing a higher stock price, in order to minimize estate taxes when the patriarch’s 3% stake gets passed on to his children. That also could account for the puny dividend and lack of a stock-buyback program. Samsung has returned less than 10% of its net income to shareholders in recent years in the form of dividends. Succession speculation has heated up this year because Lee has been hospitalized in Seoul since a heart attack in May and reportedly has lost cognitive functions. The company said last week that he is “making a steady recovery.” When Lee dies, the family will probably want to get greater income from its Samsung Electronics holdings in order to pay estate taxes, and that might prompt a sharply higher dividend. Korean estate taxes are punitive at around 50%, and Lee’s heirs could face a bill of $4 billion, payable over five years. A higher dividend would enable the family to settle estate taxes without having to liquidate sizable chunks of the Samsung empire, including its 4% stake in the crown jewel, Samsung Electronics. Some investors tell Barron’s that investors could pile into the stock after Lee’s death, in the expectation the family will have an incentive to take shareholder- friendly steps that would boost the stock price. THE FAMILY APPEARS to be moving toward a restructuring of the complex web of Samsung entities, with two initial public offerings expected in the next few months. It plans to sell shares in the family-controlled holding company, Cheil Industries, which owns 19% of Samsung Life Insurance (032830.Korea). The insurer in turn holds a 7.6% interest in Samsung Electronics, the single largest stake. Samsung is the biggest and most powerful of South Korea’s “chaebols,” or family-controlled conglomerates that have dominated its economy for decades. The top chaebol families are treated like royalty in South Korea, and like British aristocrats, often marry among themselves.

Lee Jae-yong, left, is the heir apparent to his ailing father, Samsung Chairman Lee Kun-hee. In June, CLSA’s Cochran, a longtime student of the chaebols, wrote a nearly 200-page report, “Chaebolaction: How Samsung will put the pieces together,” outlining the series of steps the Lee family might take to restructure the Samsung group. His view: The family will move to simplify the web of Samsung companies to solidify its control of Samsung Electronics. It will be simpler to achieve that goal by having publicly traded securities in Cheil and Samsung SDS, a technology-services company due to go public next month. Cochran also has written that the family needs a high dividend yield of 6% on its Samsung holding to finance likely estate taxes. A substantial increase in the dividend also could influence other Korean companies, which generally have puny payouts. Samsung heir apparent Lee Jae-yong, 46, is Lee Kun-hee’s son. He serves as co-vice chairman and the company’s emissary to the global technology world. He was invited to Steve Jobs’ memorial service in 2011. The Korean media refer to him as the “crown prince of Samsung.” The younger Lee, whose education included several years of post-graduate study at Harvard, is fluent in Japanese and English, and keeps a low profile. Like most Korean companies, Samsung usually doesn’t make executives available to talk to investors. None of the top leadership, for instance, is involved in quarterly earnings calls, and none spoke with Barron’s. The dangers of investing in insular Korean companies were apparent recently when Hyundai Motor (005380.Korea), the auto company, agreed to pay a stunning $10 billion for a 20-acre property in Seoul’s desirable Gangnam neighborhood to build a new headquarters. That price was about three times what many thought the property was worth, and the dubious deal sent Hyundai shares down by nearly 10%. Samsung reportedly was the second-highest bidder. SAMSUNG SHARES aren’t listed in the U.S., which also might account for the stock’s depressed valuation. While institutional investors can buy shares in Korea with some ease, it is difficult for U.S. retail investors to access the Korean market, since buyers often need a registration certificate from Korean regulatory authorities. Many U.S. brokerage firms don’t allow retail clients to buy Korean stocks. Merrill Lynch and Fidelity are exceptions—and even there it can take some work. Morgan Stanley and UBS wealth-management clients, on the other hand, can’t purchase Korean shares.

Samsung has dollar-denominated shares that trade in London, currently around $515 apiece. (Each share is equal to half a Korean share.) These global depository receipts (GDRs) also are tough for U.S. retail investors to purchase, since they are geared toward American institutional buyers. Non-U.S. buyers, however, face few restrictions on buying the London-listed shares. Samsung has no plans to list American depositary receipts, and analysts don’t see a U.S. listing until after the Lee family restructures its Samsung holdings. Investors can get exposure to Samsung through exchange-traded funds, notably the iShares MSCI South Korea Capped fund (EWY), which has a 20% weighting in Samsung. The closed- end Korea Fund (KF) has a similar Samsung weighting and trades at an 8% discount to its net asset value. It has a higher fee than the iShares ETF. The broader Korean market looks appealing. Korean stocks have lagged behind the Standard & Poor’s 500 index in recent years, with the Kospi unchanged since late 2010. The market trades for about 12 times forward earnings, a historically low multiple. Fixing the cellphone business is a top priority at Samsung. In recent years, Samsung and Apple have accounted for all the profits in the global handset business, but the profit pool is shifting toward Apple. Samsung is moving to introduce low- and midprice handsets in order to blunt the impact of Chinese and other low-cost manufacturers. Samsung’s strong position in cellphone components and global distribution give it an advantage, and most analysts see the handset business remaining profitable. “Samsung has to get better in software,” said tech maven Walt Mossberg last week on CNBC. He said the company has “too many models. Samsung makes things for carriers in different markets while Apple makes things for users, and carriers have to take them.” Making major improvements to the software in its Android phones might be tough, but Samsung could score in 2016 with foldable displays. SAMSUNG’S LEADING position in memory chips looks unassailable. The company’s announcement recently of plans to construct a $14 billion semiconductor factory in South Korea, to be completed by 2018, underscored its financial strength and the moat around that business. Samsung profit estimates continue to fall. The current consensus for 2015 earnings is about KRW133,000 per share, down from KRW200,000 at the start of this year. The forward multiple is eight. Barring a complete evaporation of handset profits, earnings should hold above KRW100,000. Investors note that Apple shares bottomed last year when earnings estimates stopped coming down, and the same could happen soon to Samsung. The Samsung story may require some investor patience. Yet the shares look promising, given the company’s leading brand, fortress-like balance sheet, still-ample earnings, and a controlling family that sooner or later will align itself with outside shareholders.

You can also read