Shared Ownership - Savills

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

UK Residential – 2019

S P OT L I G H T

Savills Research

Shared Ownership

Profiling costs and buyers Jump-starting supply Investing in the future

Introduction

The end of Help to Buy could increase Shared

Ownership demand by over 15,000 homes per year

Shared Ownership

An established fixture on the housing landscape, Shared Ownership offers

its residents an affordable route to home ownership

Shared Ownership (SO) has come a long initial deposit can be as low as 1.25% of It could also have implications for

way. Since its inception four decades the total property value. institutional investors, whose demand

ago it has become an established fixture Due to these similarities, there is for long-term, inflation-linked income

in the housing landscape. Now, more significant overlap in the target markets makes Shared Ownership a natural fit.

than 200,000 households live in the for Shared Ownership and Help to Buy. We believe that recent deals by Heylo,

tenure. There were over 13,400 Shared This has helped suppress take-up of Shared Sage, and ReSI are the first of many such

Ownership completions in 2018, and Ownership over the last five years. Once private investments into this sector. This

Rightmove listed around 2,500 second- Help to Buy ends, as Government states it could drive opportunities for housing

hand Shared Ownership properties in will in 2023, Shared Ownership will become associations to unlock capital for more

Q4 2018: 69% more than in Q4 2010. the main route to home ownership for those housing development.

Those households represent a broad unable to access the market. This could The sector is not without its problems.

swathe of the population. Yes, Shared increase demand for Shared Ownership For housing associations, taking on

Ownership has helped many thousands of homes by over 15,000 homes per year. sales risk leaves them more exposed to

households to become first time buyers. This has implications for fluctuations in the housing market, while

It has also helped growing families, housebuilders, who will look to Shared for residents, contracted rent increases

downsizers, divorcees, and people Ownership when Help to Buy comes to could mean their housing costs rise faster

moving regions for work into secure and an end. By providing alternative routes than the open market.

affordable homes. to market, either through bulk deals Despite these issues, Shared Ownership

As it stands now, Shared Ownership or individual sales, Shared Ownership gives housebuilders a new route to market

occupies a similar but much smaller helps increase sales rates and helps and helps them recover their capital

place in the market to the Help to Buy housebuilders recycle their capital faster. quicker, provides investors with a long-

equity loan (HtB). Our analysis shows The first step to achieving this must term income stream, and gets Government

that, given the same deposit, monthly be educating new homes sales staff, so closer to its aim of delivering 300,000 new

costs for the two schemes are similar. they’re able to offer Shared Ownership homes per year. Most fundamentally, it

Shared Ownership offers lower barriers to potential buyers as part of a range of offers its residents an affordable route to

to potential homeowners, however, as the options where appropriate. home ownership.

Figure 1 Ongoing costs of home ownership options

Full Ownership PRS HtB

SO 50% SO 25%

£2,000

£1,800

£1,600

Monthly cost

£1,400

£1,200

£1,000

£800

£600

Jan-43

Jan-19

Jan-21

Jan-31

Jan-41

Jan-20

Jan-22

Jan-23

Jan-24

Jan-25

Jan-26

Jan-27

Jan-28

Jan-29

Jan-30

Jan-32

Jan-33

Jan-34

Jan-35

Jan-36

Jan-37

Jan-38

Jan-39

Jan-40

Jan-42

Assumptions for Figure 1 chart: Deposit is 5% of full property value, long-term house price inflation in line with RPI Includes

repair & maintenance at 1% of property value per year Source Savills Research using Oxford Economics, Bank of England

2Shared Ownership

The heir apparent?

Shared Ownership is Help to Buy’s natural successor, which will lead

to opportunities for housebuilders and investors

Profiling the costs

Given the same initial deposit and the Help to Buy equity loan scheme For example, rental growth in the North

the same property, the monthly costs ends in 2023. East was just 6.4 % between 2008 and

for Shared Ownership are substantially However, as the rent portion of 2018 according to the ONS. RPI over

cheaper than full ownership. The costs Shared Ownership costs rises at a that period was 31.1%. Applying that

for 50% Shared Ownership are in line premium to inf lation, monthly costs inf lation plus a premium to Shared

with Help to Buy, and 25% Shared will rise faster than for full ownership. Ownership rents results in rental

Ownership is cheaper still (See Fig 1). This ultimately leads to Shared growth far in excess of the market.

The costs for 50% Shared Ownership Ownership becoming more expensive It’s possible that households will use

remain aligned to Help to Buy for than full home ownership by the end this initial period of lower housing

the first decade of ownership. This of the mortgage term. costs to save up and purchase a greater

means that while the Help to Buy This point could come earlier in share in their home. However, since

equity loan remains, buyers are likely some parts of the country. While rental households living in Shared Ownership

to favour it over Shared Ownership growth at a national level is roughly in tend to have lower incomes, their

as it gives them a higher proportion line with RPI, this hides a great deal of capacity to save up may be limited. To

of their home’s equity. However, we regional variation. In many parts date, evidence from Shared Ownership

expect that Shared Ownership will of England, private rents have shown portfolios suggests staircasing is

service the gap left behind when little growth over the last decade. relatively rare (see Page 11).

Figure 2 Minimum deposit and income requirements for a £230,000 home

■ Deposit ■ Mortgage ■ Equity loan ■ Retained equity

Full ownership Help to Buy 50% Shared 25% Shared

5% of full value 5% of full value Ownership Ownership

£11,500 £11,500 5% of 50% 5% of 25%

share £5,750 share £2,875

Minimum income required

£48,600 £38,800 £27,600 £21,600

Source Savills Research

3Shared Ownership

Minimum deposit required for Shared

1.25% Ownership, as proportion of property value

Figure 3 Monthly home ownership costs in Year 1*

London Horsham England Burnley

Full ownership £2,286 £2,125 £1,238 £444

50% Shared Ownership £1,672 £1,555 £906 £325

*See Figure 1 footnote for assumptions

Source Savills Research

The pattern of housing costs is Buy loan in London in the year to The lower deposit requirement

largely the same across England. The September 2018. for Shared Ownership significantly

exception is London, where the higher One advantage of Shared Ownership reduces the barriers to home

equity loan allowance brings the initial is that it enables households to access ownership for households without

cost of Help to Buy below that of 25% home ownership with a much lower existing savings, and the lower

Shared Ownership. Help to Buy remains deposit: 5% of the share, which could mortgage borrowing requirements

the cheapest option in London for most be as low as 1.25% of the full property and discounted rent open it up to

of the 25-year mortgage term. Just over value. Help to Buy, by contrast, requires a households on lower incomes.

5,000 households took up a Help to minimum 5% of the full value as deposit.

Figure 4 Distribution of Shared Ownership and Help to Buy users by income

Proportion of SO purchasers Proportion of HtB purchasers

35%

30%

25%

Proportion of households

20%

15%

10%

5%

0%

£0 – £20,001 - £30,001 - £40,001 - £50,001 - £60,001 - £80,001 - Greater than

£20,000 £30,000 £40,000 £50,000 £60,000 £80,000 £100,000 £100,000

Source CORE 2016/17, Evaluation of the Help to Buy Equity Loan Scheme 2017 (Whitehead & Williams, 2018)

4Shared Ownership

of Help to Buy users have incomes

10% above the Shared Ownership limits

Profiling the buyers Ownership simply by having incomes the North or the outer parts of the East

Despite similarities in entry and ongoing above the cap. of England. Help to Buy take-up is much

costs, there are significant differences More than half of all Shared higher in the North, but less prevalent

in the types of households taking up Ownership sales in 2016/17 were to in London and south of the capital.

Shared Ownership and Help to Buy. single person households, a far higher However, take-up in London is increasing

Shared Ownership is more popular proportion than for Help to Buy. as more buyers take advantage of the

with those on lower incomes. The However, the profile of Heylo’s buyers more generous equity loan there.

scheme is only available to households is weighted more towards families, After April 2021, each region bar

with incomes below £80,000 demonstrating how Shared Ownership London will be subject to a new, lower

(£90,000 in London), and buyers must can appeal to different demographics Help to Buy value cap. In some local

demonstrate they couldn’t afford to buy depending on how it is marketed. authorities average Help to Buy property

a home without support. By contrast, There are substantial parts of the values already exceed these caps, so

Help to Buy users have a wider variety country where take-up of Shared housebuilders will need to build cheaper

of buyer incomes, as the scheme has no Ownership and Help to Buy don’t homes if they want to continue using the

income restrictions. overlap. Shared Ownership is more scheme. Where this isn’t possible, we

More than 10% of those using Help to prevalent in the South, Midlands, could see more of these homes coming

Buy are currently excluded from Shared and London, with limited take-up in to market as Shared Ownership.

Figure 5 Household characteristics using Shared Ownership and Help to Buy

■ SO ■ Heylo SO ■ HtB FTB ■ SO ■ Heylo SO ■ HtB FTB

60% 60%

50% 50%

40% 40%

Proportion of buyers

30% 30%

20% 20%

10% 10%

0% 0%

1 Person 2 People 3 People 4+ People 16-24 25-34 35-44 45+

Source CORE 2016/17, Heylo via Outra, Evaluation of the Help to Buy Equity Loan Scheme 2017 (Whitehead & Williams, 2018)

5Shared Ownership

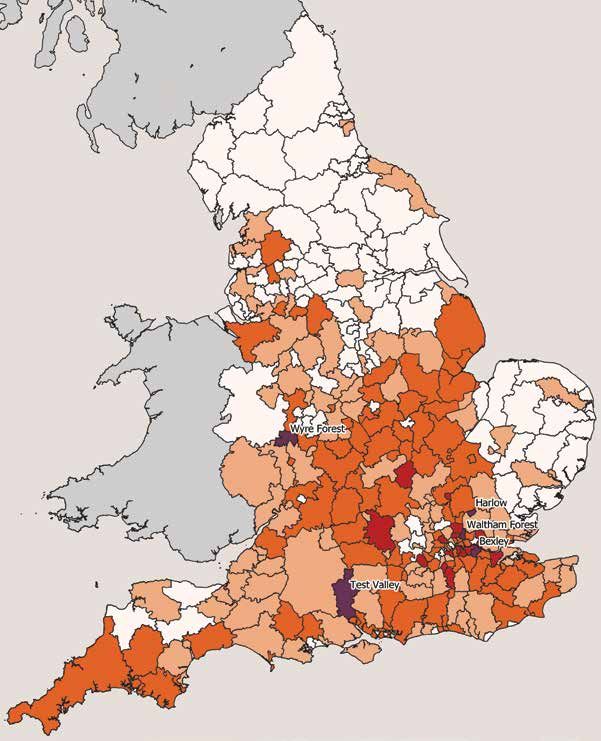

Shared Ownership accounted for 5% of

5% new housing delivery between 2013 and 2018

Figure 6 Shared Ownership as a proportion of new homes

Number of Shared Ownership

sales as proportion of new homes

■ Under 2.5%

■ 2.5% - 5.0%

■ 5.0% - 10.0%

■ 10.0% - 15.0%

■ Over 15% (labeled)

Wyre Forest

Harlow

Waltham Forest

Bexley

Test Valley

Source Savills Research using Homes England, MHCLG

6Shared Ownership

proposed end date for the

2023 Help to Buy equity loan scheme

Death (of HtB) and taxes Figure 7 Eligibility criteria for home ownership schemes

Until recently, Shared Ownership buyers had

a substantial disadvantage relative to Help

Requirements Shared Help to Buy Help to Buy

to Buy users: Shared Ownership buyers were Ownership Equity Loan Post-2021

excluded from first time buyers’ stamp duty Current

relief. The 2018 Autumn Budget brought

Shared Ownership into line with other first

time buyers. This should help bolster Shared Household LondonSupply

Residents win

Saving in monthly housing costs for 50%

27% Shared Ownership versus full ownership

of the same property

Housebuilders win

By selling at discounts up to 15%,

15% housebuilders can recycle capital

and move to the next site faster

Government wins

Shared Ownership supported more

15% than 15% of new homes in five local

authorities

Jump-starting supply

Shared Ownership offers developers an alternative to selling

their homes on the open market. This drives higher sales rates

and accelerates housing delivery

We’ve seen in the previous section

how Shared Ownership appeals to a

different market from open market

rise over the next five years. Shared

Ownership offers access to the same

property with lower monthly housing

2 Housebuilders win

Shared Ownership offers

housebuilders a way to broaden the

sale. Developers can sell homes in bulk costs, lowering that affordability range of products they bring to the

to registered providers or investors, barrier for households who can’t market. That’s attractive at a time of

who then sell the equity stakes on to afford to buy outright. slowing sales rates. Our analysis shows

individual households. Alternatively, households could that sales rates have levelled off for the

This is a win-win scenario. Aspiring use Shared Ownership to purchase eight largest UK housebuilders since

homeowners will enjoy a broader range a larger home than they could afford 2016, with falls over the last three

of housing options to choose from. to buy outright. This is similar to months of 2018.

Housebuilders benefit from freeing how many households currently We’ve seen developers announce

up their capital faster. Government use the Help to Buy equity loan a flurry of bulk deals for Shared

will come a step closer to achieving its scheme. This approach will grow in Ownership over the last six months,

housing delivery ambitions. popularity as the equity loan scheme including Taylor Wimpey and Bovis.

wraps up, particularly from April Some of these deals represent a

1 Residents win

Our modelling shows that the

monthly cost of buying a 50% Shared

2023 when Government intends to

end it entirely.

Around 40,000 households

discount to gross development value

of up to 15%.

Part of this discount reflects the

Ownership property could be 27% become first time buyers each year finance and marketing cost savings

lower than using the same deposit to through the Help to Buy equity loan. the developer makes by selling

buy outright. This widens the range Of those, 38% or around 15,300 in bulk, which will become even

of households who can afford to buy. purchasers, could not have bought a more important as interest rates

Increasingly, affordability stress home without the scheme. rise over the next few years. But

testing is limiting the number of If all this demand were to switch it also demonstrates the scale of

households able to access home to Shared Ownership homes after housebuilders’ appetite to recycle

ownership. Unless those stress tests the equity loan scheme ends in 2023, their capital and move onto the next

are relaxed or removed, they will only Shared Ownership supply would have site quickly. Whether selling in bulk

get more restrictive as interest rates to increase by more than 150%. to housing associations or directly to

8Supply

Increase in Shared Ownership supply

150% needed to meet demand after HtB ends

Figure 8 Housebuilder sales rates and buyer confidence

Average sales rate Buyer confidence

3.4 0

3.2 10

Proportion of households considering

buyer confidence a major constraint

Average sales rate per outlet per month

3.0 20

2.8 30

of eight housebuilders

2.6 40

2.4 50

2.2 60

2.0 70

1.8 80

1.6 90

1.4 100

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source Housebuilder trading updates and HBF

buyers, Shared Ownership can help Programme: over £4 billion to fund this proportion is far higher: in the

housebuilders increase their rate of 135,000 new Shared Ownership home Test Valley first tranche Shared

housing delivery. starts by 2021. Ownership sales accounted for 19%

As well as purchasing Section of new home EPC registrations.

3 Government wins

Government remains committed

to delivering 300,000 homes per year

106 stock, registered providers

are developing their own Shared

Ownership homes on land-led

Shared Ownership supported more

than 15% of new homes in a further

four local authorities.

in England by the mid-2020s. Energy schemes. The receipts from these Shared Ownership can also

Performance Certificate registrations first tranche sales can help them help support the Letwin Review’s

suggest that 238,200 new homes were cross-subsidise other affordable recommendations through increasing

completed in England in 2018, a 12% housing tenures. the supply of housing for older people.

increase on the previous year. Private investors are already Shared Ownership for Older People is

These figures are encouraging, involved, acquiring both Section a distinct scheme offering homes for

but it’s difficult to see how delivery 106 stock and doing bulk deals with the over-55s.

can accelerate much further without housebuilders to build portfolios Our previous research has shown

developing a broader range of housing of scale. With Government inviting there are 150,000 older households

tenures and types, as suggested in proposals for how to unlock more who own some housing equity but

the Letwin Review. Shared Ownership development could not afford to buy a purpose-

First tranche Shared Ownership through private investment, this built retirement apartment outright.

sales have averaged just under 10,000 trend is set to continue. Shared Ownership, whether

per year over the last three years. Our analysis suggests that specifically for older people or not,

That’s a substantial increase on Shared Ownership sales supported could unlock this market, releasing

the 2012-15 average, 7,700, reflecting just under 5% of new housing the equity stored in their former

the scale of Government support delivery between Q2 2013 and homes and freeing up family housing

in the 2016-21 Affordable Homes Q1 2018. In some local authorities for younger households.

9Investment

Investing in the future

Shared Ownership is an attractive long-term investment proposition,

but investors face challenges building portfolios at scale

Whoever acquires the unsold equity in housing associations (HAs). Shared These sources of income come with

a Shared Ownership scheme can expect Ownership sales have added a total of relatively little risk. The repossession

to see a steady, secure rental income £5.9 billion to HA turnover since 2016. rate for Shared Ownership properties

rising above inflation. It’s the kind of First tranche Shared Ownership was just 0.02%, less than half the level

long-term investment you’d expect sales delivered over £1.2 billion to for general owner occupation at 0.05%,

to see pension funds and institutions HA turnover in 2018 alone. according to UK Finance.

taking serious interest in. On top of that, the unsold equity To date, HAs have shown little

To date, private sector involvement on these Shared Ownership homes interest in selling the retained equity

in this asset class has been driven delivers a rental income. While the in their Shared Ownership homes.

by a handful of entrepreneurial initial yield may appear low at up But the low-yield, low-risk nature of

investors such as Heylo, Blackstone, to 2.75%, it looks more attractive these income streams may be better

and ReSI. Housing associations develop considering this is net income, suited to long-term income investors,

and retain the vast bulk of Shared residents being responsible for any such as pension funds, than HAs with

Ownership homes, using any profits repair and maintenance costs, and development aspirations: especially

it may generate to cross-subsidise other that this rent grows at or above RPI. if the vendor retains management of

affordable housing delivery. Evidence from the National Sales the scheme.

As Shared Ownership matures into Group suggests 39% of staircasing There may be an opportunity for

an established housing tenure, voices in 2018 was partial, meaning those HAs to unlock the value of these

across Government, the housing sector residents still pay rent on the rest of income streams to enable more

and private investors have started their property value. affordable housing development.

calling for a different approach. The remaining 61% of staircasing

was to full ownership, which means Government

Housing associations those residents are no longer required Currently, Government supports the

Shared Ownership is big money for to pay rent. majority of Shared Ownership housing:

Figure 9 Shared Ownership supply and staircasing volumes

■ Staircasing to 100% (left axis) ■ First tranche sales

Staircasing to 100% as proportion of all shared owners (right axis)

19,250 5.5%

17,500 5.0%

15,750 4.5%

Number of 100% staircasing events

100% staircasing as a proportion

14,000 4.0%

or first tranche sales

of all shared owners

12,250 3.5%

10,500 3.0%

8,750 2.5%

7,000 2.0%

5,250 1.5%

3,500 1.0%

1,750 0.5%

0 0.0%

2017-18

2007-08

2008-09

2002-03

2005-06

2006-07

2013-14

2015-16

2016-17

2009-10

2010-11

2012-13

2001-02

2003-04

2004-05

2014-15

2011-12

Source Savills Research using Homes England SDR and TSA RSR with data before 2008-09 from ‘Understanding the second-hand market for shared

ownership properties’ by Anna Clarke and Andrew Heywood, 2012, Cambridge Centre for Housing & Planning Research, University of Cambridge

10Investment

households used an

83,000 equity release loan in 2018

either through grant funding

or imposing Section 106 contributions

on developers. This could be set

to change.

For years, private investors and

developers have been able to hold a

long-term interest in Shared Ownership

housing. And now Government is

assessing the proposals for privately

funded Shared Ownership that it called

for in the 2018 Budget.

These measures pave the way for

private investors to fund the

development of Shared Ownership

homes and retain the unsold equity,

with the associated rental income

stream, for the long term.

Descending the staircase

Most discussion of staircasing in Shared Ownership

is around households buying more of their home.

It’s far less common for registered providers to offer

the reverse: buying back shares of the property from

the resident.

Currently, this is only allowed for households in

financial difficulties who are struggling to meet

their mortgage obligations and maintenance costs.

However, as the market for Shared Ownership matures,

one demographic group in particular looks like it could

benefit from downward staircasing: older people.

83,000 households used an equity release loan in

2018, according to the Equity Release Council. This

demonstrates the demand from older people to

release some of the wealth tied up in their homes.

Registered providers could offer a similar scheme

to their older Shared Ownership residents, whether

or not they live specifically in Older People’s Shared

Ownership. This would help their residents release

cash while retaining the homes within the same tenure.

And by designing and marketing Shared Ownership

homes specifically to older people, providers can help

older owner occupiers unlock their housing equity.

11Savills Research

We’re a dedicated team with an unrivalled reputation for producing well-informed

and accurate analysis, research and commentary across all sectors of the UK property market.

Research

Lawrence Bowles Ed Hampson Chris Buckle Josh Rose-Nokes Lydia McLaren

020 7299 3024 020 3107 5460 020 7016 3881 020 7409 5907 020 3428 2939

lbowles@savills.com ed.hampson@savills.com cbuckle@savills.com josh.rosenokes@savills.com lydia.mclaren@savills.com

Shared Ownership

Helen Collins Piers de Winton Patrick Eve

Head of Housing Consultancy Director, Capital Markets Head of Regional Development

020 7409 8154 020 7016 3816 018 6526 9071

hcollins@savills.com pdewinton@savills.com peve@savills.com

Savills plc is a global real estate services provider listed on the London Stock Exchange. We have an international network of more than 600 offices and associates throughout the Americas, UK, Europe,

Asia Pacific, Africa and the Middle East, offering a broad range of specialist advisory, management and transactional services to clients all over the world. This report is for general informative purposes only. It may

not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every effort has been made to

ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is

prohibited without written permission from Savills Research.You can also read