Sixt Leasing SE Capital Markets Day 2019 - 16 April 2019 - The site can't be ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Sixt Leasing SE

Capital Markets Day 2019

16 April 2019

Disclaimer

This presentation contains certain forward-looking statements relating to the business, financial performance and results of the Sixt Leasing SE (together with its

subsidiaries, the “Company”) and/or the industry in which the Company operates. Forward-looking statements, regardless if made orally or in writing, concern future

circumstances and results and other statements that are not historical facts, sometimes identified by the words “believes,” “expects,” “predicts,” “intends,” “projects,”

“plans,” “estimates,” “aims,” “foresees,” “anticipates,” “targets,” and similar expressions. Forward-looking statements, including assumptions, opinions and views of

the Company or cited from third party sources, are solely opinions and forecasts which are uncertain and subject to risks. Actual events may differ significantly from

any anticipated development due to a number of factors, including without limitation, changes in general economic conditions, in particular economic conditions in

the Company’s target markets, changes affecting interest rate levels, changes in competition levels, changes in laws and regulations, environmental damages, the

potential impact of legal proceedings and actions and the Group’s ability to achieve operational synergies from past or future acquisitions. The Company does not

guarantee that the assumptions underlying forward-looking statements, regardless if made orally or in writing, are free from errors nor does it accept any

responsibility for the future accuracy of opinions or any obligation to update the statements in this presentation to reflect subsequent events. Forward-looking

statements are made only as of the date hereof. Neither the delivery of this presentation nor any further discussions of the Company with any of the recipients

thereof shall, under any circumstances, create any implication that there has been no change in the affairs of the Company since such date. Consequently, the

Company does not undertake any obligation to review, update or confirm investors' expectations or estimates or to release publicly any revisions to any forward-

looking statements to reflect events that occur or circumstances that arise in relation to the content of the presentation.

Furthermore, a totally different performance can ensue from an unexpected slump in demand or economic stagnation in our key market Germany and/or in other

Western European markets. The actual development can differ materially from the forecasts made in this presentation, in case one of the aforementioned risks or

other risks not mentioned here should materialize and/or the assumption on which we have based our forecasts and prospects turn out to be wrong.

This presentation contains summary information only and does not purport to be comprehensive and is not intended to be (and should not be used as) the basis of

any analysis or other evaluation. In addition, the information in this presentation is subject to change. No representation or warranty (express or implied) is made as

to, and no reliance should be placed on, any information, including projections, estimates, targets and opinions, contained herein, and no liability whatsoever is

accepted as to any errors, omissions or misstatements contained herein.

The presentation is furnished to you solely for your information and may not be reproduced or redistributed, in whole or in part, to any other person.

By accepting this presentation you acknowledge the foregoing.

2 2

Introducing Michael Ruhl, CEO Sixt Leasing SE

▪ Since 1 January 2019: CEO of Sixt Leasing SE

▪ 2013 – 2018: Managing Director of Hannover Leasing

GmbH & Co. KG

▪ Hannover Leasing manages more than 200

investments and mutual funds with a total asset value

of around 10 billion euros

▪ 1997 – 2013: DaimlerChrysler Services Structured

Finance GmbH and DFH Deutsche Fonds Holding AG,

among others as Member of the Board

▪ Before 1997: Various positions at Commerzbank

3 3

Agenda

A INTRODUCTION 04

B HIGHLIGHTS & FINANCIALS FY 2018 // GUIDANCE – BJÖRN WALDOW 06

C GROUP STRATEGY & OUTLOOK – MICHAEL RUHL 18

D FLEET LEASING – MICHAEL RUHL 27

E ONLINE RETAIL – DR. FELIX FRANK 31

F FLEET MANAGEMENT – CHRISTOPH V. TSCHIRSCHNITZ 43

4 4

Agenda

A INTRODUCTION 04

B HIGHLIGHTS & FINANCIALS FY 2018 // GUIDANCE – BJÖRN WALDOW 06

C GROUP STRATEGY & OUTLOOK – MICHAEL RUHL 18

D FLEET LEASING – MICHAEL RUHL 27

E ONLINE RETAIL – DR. FELIX FRANK 31

F FLEET MANAGEMENT – CHRISTOPH V. TSCHIRSCHNITZ 43

5 5

Introducing Björn Waldow, CFO Sixt Leasing SE

▪ Since 1 April 2015: CFO of Sixt Leasing SE

▪ 2010 – 2015: Sixt SE, Managing Director

Corporate Development, Strategy,

Mergers & Acquisitions, Sales Controlling and

Corporate Risk Management

▪ 2002 – 2010: Roland Berger Strategy Consultants,

Principal

▪ 1995 – 2001: Various positions at Deutsche Bank

▪ Degree in Business Studies and training as a banker

6 6

Online Retail became largest business field of Sixt Leasing Group in

the financial year 2018

STRONG CONTRACT GROWTH SINCE 2011 WELL DIVERSIFIED CONTRACT PORTFOLIO

[# contracts in ‘000]

100%

132.9 129.7

2011: Establishment of

113.6 – Online Retail

103.2 ▪ Private and commercial customers

97.4

35% ▪ Classic leasing and vario-financing + services

76.2

▪ One-stop online shop with ~35 brands at choice

62.2

56.3 44,700*

2012: Establishment of

– Fleet Management

2011 2012 2013 2014 2015 2016 2017 2018 ▪ Mid-sized and large corporates

32%

▪ Fleet management and consulting

INCREASING ONLINE SHARE IN NEW BUSINESS ▪ Optimisation of total cost of ownership

42,000*

54%

48% 49%

36% 39% – Fleet Leasing

33% ▪ SMEs + large corporates

▪ Full-service leasing

2014 2015 2016 2017 2018

▪ Optimisation of total cost of ownership

43,000*

[Share of Online Retail new contracts out of total Leasing new contracts; excluding 1&1/Peugeot Portfolio Q4 2018

campaign in 2017]

*Number of contracts

7 7

FY 2018: Growth of revenue and earnings – contract portfolio and

operating return on revenue at around previous year’s levels

2018 Change vs. 2017 Guidance

Group contract portfolio 129,700 -2.4% Around previous year

▪ Online Retail 44,7001) -1.6% 10,000-12,000 new contracts

▪ Fleet Management 42,000 6.6% Slight increase

▪ Fleet Leasing 43,000 -10.5% ~43,000

Financials

Operating revenue EUR 480.5 m 5.7% Slight increase

EBITDA EUR 240.8 m 2.8% Slight increase

EBT EUR 30.5 m 2.8% Around previous year

Operating return on revenue 6.4% -0.1pp In line with 6% target

Equity ratio 15.6% 1.4pp At least 14%

Dividend [pay-out ratio]2) EUR 0.48 [45%] - 30-60% pay-out ratio

1) Slightly more than 10,000 new contracts

2) Pay-out ratio based on consolidated profit of EUR 22.0 m

8 8

DRIVE>2021 highlights 2018: Focus on improving risk-return profile

and enabling future growth

DIGITALISATION RISK REDUCTION DIESEL REMARKETING

Online Retail became Number of Euro-5/4 non- Proportion of NBB diesel International used

largest business field buyback (NBB) diesel cars cars in new business car sales successfully

of the Group in Germany halved significantly reduced established

LOCATIONS EXPANSION GROWTH FUNDING FINANCING

First own used car sales Experienced Managing EUR 1 bn debt issuance Fully independent

and delivery/return station Directors for Online Retail programme set up financing structure

opened near Frankfurt and Fleet Mgmt. hired achieved

9 9

Robust risk profile through low stock of older diesel vehicles,

significant buyback share and diversified remarketing approach

DECREASING STOCK OF OLDER DIESEL CARS DIVERSIFIED REMARKETING APPROACH

[Number of Euro 5/4 diesel vehicles in Germany without buyback agreement in ‘000] [Based on total remarketed vehicles in FY 2018 in Germany; including Fleet Management]

TOTAL REMARKETED VEHICLES

12.2

8.9 ~55% ~45%

5.6

Buyback agreement No buyback agreement

2.8

~85%

‘Cherrypicking’

1

2015 2016 2017 2018 ~15%

Sale to

OEM/dealer

SIGNIFICANT SHARE OF BUYBACK AGREEMENTS

Non-Buyback (NBB) ~20% ~30% ~50%

2 3 4

42%

Sale to B2B auction B2C used car

Buyback (BB) 58% customer platform locations

[Based on number of vehicles of Sixt Leasing SE as of 31 December 2018]

10 10Operating revenue and EBT increased in FY 2018 despite slow-down

in contract growth

Sixt Leasing Group – Key performance indicators 2014 – 20181)

CONTRACT PORTFOLIO [‘000]2) REVENUE [EUR m] EBT [EUR m]4)

Operating

return on 6.0 7.0 7.3 6.5 6.4

revenue [%]4)

CAGR

CAGR EBITDA5) 207.0 230.1 228.6 234.3 240.8

+7%

132.9 129.7 +9% 805.8

744.0

113.6 713.9

665.4 CAGR

103.2 48.1 43.0 +4%

97.4 325.3

575.0 289.6

47.5 235.6 283.9 31.6

Sales 30.3 29.7 30.5

48.3 revenue

147.1

50.2 25.6

39.4 42.0

Fleet

38.7 27.4 28.0 25.6 26.1

Leasing Operating 480.5

33.8 427.9 429.8 430.0 454.4 23.5

Fleet 31.4 Revenue3) Leasing

Mgmt. 45.4 44.7

21.1 27.4 Fleet

Online 15.8 Mgmt. 2.8 3.5 4.1 4.4

2.2

Retail

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

1) 2014: Figures derived from combined financial statements; due to rounding, individual figures may not always add up to the total figure

2) Including leasing contracts, fleet management contracts, service contracts and order book (contracts for which the leased vehicle has not yet been delivered to the customer)

3) The sum of leasing revenue (i.e. the finance rate, being the financing portion, consisting of interest and depreciation, of the agreed lease instalment) and other revenue from leasing business of the

Leasing business unit as well as fleet management revenue from the Fleet Management business unit

4) The ratio of earnings before taxes (EBT) to operating revenue

5) Earnings before interest, taxes, depreciation and amortisation

11 11Both business units contributed to increase of EBT in FY 2018

EBT development of Sixt Leasing Group and business units 2014 – 20181)

GROUP [EUR m] LEASING [EUR m] FLEET MANAGEMENT [EUR m]

Operating Operating Operating

return on 6.0 7.0 7.3 6.5 6.4 return on 6.1 6.9 7.1 6.3 6.1 return on 5.3 8.7 9.4 8.6 8.0

revenue [%]2) revenue [%] revenue [%]

EBITDA3) 207.0 230.1 228.6 234.3 240.8 EBITDA 200.9 2019.9 224.8 230.0 236.4 EBITDA 2.5 3.1 3.8 4.3 4.5

CAGR

+4%

CAGR

31.6 +3%

30.3 29.7 30.5

25.6 27.4 28.0

25.6 26.1

23.5

CAGR

+19%

4.1 4.4

3.5

2.8

2.2

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

1) 2014 figures derived from combined financial statements; due to rounding, individual figures may not always add up to the total figure

2) Ratio of EBT to operating revenue

3) EBITDA = Earnings before interest, taxes, depreciation and amortisation

12 12Lease assets of more than EUR 1.2 bn – Solid equity ratio of 16.4%

Sixt Leasing Group – Development of key balance sheet figures 2015 – Q1 20191)

TOTAL ASSETS [EUR m] FINANCIAL LIABILITIES [EUR m]2) EQUITY [EUR m]

Net debt Equity

[EUR m] 781 844 1,054 1,020 975 ratio [%] 16.0 16.6 14.2 15.6 16.4

1,443

1,393 1,359

224 188 1,060

1,172 207 1,026

1,113 976

151 848 201

Other 155 800 173

472

Current 32 222.6

207 216.8

194.7 205.1

178.3

1,219 1,204 1,152

Lease 1,021

assets

958 768 826 803

641 587

Non-

current

2015 2016 2017 2018 Q1/19 2015 2016 2017 2018 Q1/19 2015 2016 2017 2018 Q1/19

1) 2014 figures derived from combined financial statements; due to rounding, individual figures may not always add up to the total figure

2) Including liabilities to related parties until 2017

13 13Fully independent financing structure of Sixt Leasing Group after

repayment of EUR 190 m to Sixt SE achieved in June 2018

Sixt Leasing Group – Maturities of financial liabilities as of 31 December 2018 [EUR m]

FINANCIAL LIABILITIES1) 2019 2020 2021 2022 2023 Total FINANCING INSTRUMENTS

Asset backed securities

154 154 96 37 2 443 ▪ EUR 500 m ABS programme

(ABS) programme

Bank loans 37 - - - - 37 ▪ > EUR 400 m bilateral credit lines

Bonds2) - - 250 250 - 500 ▪ EUR 1 bn debt issuance programme

Borrower's note loans

- 30 - - - 30

(Schuldscheindarlehen)

Finance leases 4 8 3 - - 15 FINANCING STRATEGY

Total 195 192 349 287 2 1,026 ▪ Balancing out fleet growth and

equity ratio

Bank balances / cash 6

▪ Dividend pay-out ratio of 30-60%

Net debt 1,020 of consolidated profit

1) Nominal repayment amounts; excluding future accrued interest; due to rounding it is possible that individual figures may not exactly add up to the total amount

2) Bond 2017/2021 is a stand-alone bond; Bond 2018/22 is first bond under the debt issuance programme

14 14Attractive dividend policy supported by successful significant

reduction of average refinancing rate since IPO

DIVIDEND PER SHARE [IN EUR] AVERAGE REFINANCING RATE

Net interest

37% 40% 47% 45% Pay-out ratio 21.2 19.5 16.2 13.2 payments

[in EUR m]

4.2%

2.5%

2.4%

2.7% Dividend yield1)

2.5%

2.1%

1.7%

0.48 0.48 0.48 1.3%

0.40

Dividend policy:

Pay-out of 30-60%

of consolidated profit

2015 2016 2017 2018 2015 2016 2017 2018

[Calculated as net interest payments/average net debt; net interest payments = financial

result without result from at-equity measured investments]

1) Based on the Xetra year-end price

15 152019 forecast and medium-term outlook – Strong growth of contract

portfolio, operating revenue and EBT expected by FY 2021

2019 2021 Change 2021 vs. 2018

Contract portfolio

Group Slight increase ~ 200,000 ~ 50%

Financials

Operating revenue Around previous year ~ EUR 650 m ~ 35%

EBT Around previous year EUR 40-45 m ~ 40%

For H1-2019, business

development is expected to be

significantly weaker than in

H1-2018 as well as the expected

business development in

H2-2019.

16 16Agenda

A INTRODUCTION 04

B HIGHLIGHTS & FINANCIALS FY 2018 // GUIDANCE – BJÖRN WALDOW 06

C GROUP STRATEGY & OUTLOOK – MICHAEL RUHL 18

D FLEET LEASING – MICHAEL RUHL 27

E ONLINE RETAIL – DR. FELIX FRANK 31

F FLEET MANAGEMENT – CHRISTOPH V. TSCHIRSCHNITZ 43

17 17Sixt Leasing has a strong market position and crucial capabilities

inhouse to benefit from various megatrends

MEGATRENDS MARKET POSITION CAPABILITIES

▪ Mobility #1 mobility brand 2 well-known online platforms

for new vehicles

▪ Using instead of owning

#3 independent full-service car

▪ Car-as-a-service leasing provider in Germany 360°proprietary developed IT

platforms and products

▪ Digitalisation

3 unique business fields with

▪ E-commerce individual strengths, leveraging >70 in-house IT developers

on a common core and project managers

▪ Outsourcing

>4,000 service partners in Well diversified

▪ Smart data Germany customer base and contract

portfolio

18 18Rising demand for mobility – Cars will continue to play key role –

New mobility solutions will increase in importance

Development of mobility demand by transport mode (EU-28) [trillion passenger km]1)

FORECAST CAGR CAGR

HISTORICAL

‘10-‘16 ‘16-‘25

6.6 6.7 0.7% 1.3%

6.3 6.5

6.0 6.2

5.7 5.7 5.8 5.8 5.7 5.8 19% 19% 19% 0.8% 1.3%

5.4 5.5 19% 19%

19%

18% 18% 18% 18% 18% 18% 7% 9%

18% 2% 4% 5% 1.4% 21.9%

Public transport 19% 1% 2% 2%

1% 1% 1% 1%

Shared car 1% 1%

81% 81% 81% 81% 80% 79% 79% 77% 76% 74% 72% 0.7% 0.2%

Exclusive car 80% 81% 81%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2025

1) Source: Roland Berger, Embracing the Car-as-a-Service model – The European leasing and fleet management market, 2018

19 19carefree

VISION multi-brand

flat rates

flexible offerings

usage models

We aim to become the automated

processes

convenient

online processes

full-service

packages

leading provider of digital

car sales

fast online

longer-term auto mobility autonomous

configuring and

ordering

driving AUTOMATED

in Europe. cost-saving

outsourcing of

fleet management

complex MISSION

offline

long-term

processes

ownership

We facilitate the

longer-term auto mobility

time-consuming analogue

purchasing car sales

traditional

cost-intensive

dealers of our customers with

internal fleet

management single-service

agreements

best-in-class individualised

brand

loyalty solutions.

20DRIVE>2021 programme continues to provide framework for

strategic progress over the coming years

D igitalisation R isk-return profile I nternationalisation V olume &

▪ Build scalable ▪ Further diversify ▪ Strengthen position ▪ Increase contract

platforms/back-ends customer structure in home market portfolio to

▪ Further digitalise via increasing share ▪ Better exploit ~ 200,000 contracts

internal, customer of smaller customers potential of existing ▪ Increase operating

and servicing ▪ Reduce share of Fleet Management revenue to

processes older diesel vehicles foreign subsidiaries ~ EUR 650 m

▪ Improve digital ▪ Open own used car ▪ Enter new markets

customer experience remarketing stations in Fleet

Management

▪ Develop digital

products

▪ Increase number of

international dealers ▪ Internationalise

E arnings growth

connected to B2B Online Retail

remarketing platform business beginning ▪ Increase EBT to

from 2020 EUR 40-45 m

21 21In 2019 we are addressing 10 action fields to further develop our

business model in line with our vision (I)

TODAY TOMORROW

Car leasing with fixed term & mileage Flexible car usage/subscription

PRODUCTS New cars only Used car leasing

Service products as part of leasing contract Service products stand-alone & on-demand

Customer service largely via call centre App-supported self-service functions

CUSTOMER

EXPERIENCE

Delivery/return via third party Delivery/return also via self-operated stations

22 22In 2019 we are addressing 10 action fields to further develop our

business model in line with our vision (II)

TODAY TOMORROW

Focus on mid-sized and large fleets Target smaller fleets with dedicated approach

SEGMENTS

Fleet management Corporate mobility management

& MARKETS

Focus on Germany Gradual international expansion

Still several manual and analogue processes Digital processes for customers and internally

PROCESSES

Business field-centric mentality Leverage more synergies across business fields

23 23Strategic measures intend to support domestic fleet and service

growth accompanied by international expansion

Schematic representation of operating revenue and contract bridge until 2021 ~ 200,000

contracts

INT.

~ EUR

GROWTH

650 m

▪ Better exploit potential

SERVICE

in existing foreign

GROWTH subsidiaries (sales

activities, knowledge

DOMESTIC ▪ Service penetration transfer)

▪ Stand-alone services ▪ Follow existing

129,700 FLEET ▪ On-demand service customers abroad

contracts GROWTH upselling ▪ Establish hubs

▪ New service products ▪ Enter new markets

▪ Sales & Marketing ▪ Fleet Management ▪ Opportunistic M&A

EUR ▪ New products ▪ New tools

481 m ▪ Customer experience ▪ Cooperations

▪ Retention rate

▪ Campaigns/

cooperations

▪ Opportunistic M&A

2018 2021

24 24Operational optimisation measures aim to complement fleet and

service growth to lift EBT to EUR 40-45 m until 2021

Schematic representation of EBT bridge until 2021

EUR 40-45 m

OPERATIONAL

OPTIMISATION

▪ Digitalisation

SERVICE ▪ Customer self-service

GROWTH ▪ Cost optimisation

▪ More efficient

processes

▪ Synergies across

EUR 30.5 m business fields

▪ Improved

FLEET time-to-market

MARKETING GROWTH ▪ Product and pricing

IT differentiation

PERSONNEL ▪ Economies of scale

2018 2021

25 25Agenda

A INTRODUCTION 04

B HIGHLIGHTS & FINANCIALS FY 2018 // GUIDANCE – BJÖRN WALDOW 06

C GROUP STRATEGY & OUTLOOK – MICHAEL RUHL 18

D FLEET LEASING – MICHAEL RUHL 27

E ONLINE RETAIL – DR. FELIX FRANK 31

F FLEET MANAGEMENT – CHRISTOPH V. TSCHIRSCHNITZ 43

26 26Future growth of full-service fleet market is expected to primarily

come from the smaller fleet segment

NEW VEHICLE REGISTRATIONS IN GERMANY1) RISING MARKET POTENTIAL IN SME SEGMENT

[Forecasted car-as-a-service market development in EU-18 in EUR bn]2)

Manufacturers Private

& car dealers customers CAGR

FORECAST ‘16-‘25

28% 34%

86.3 5.0%

3.7 m vehicles 79.6

14.1 7.4%

71.2 13.1

> EUR 100 bn

65.1 7.8 51.2%

market 60.4 11.7 5.1

11%

55.5 10.4 2.3

15% 9.0 1.0

Rental 12% Private 7.5 0.5 24.0 6.4%

22.8

cars Small Mobility providers 0.2 20.1

15.9 17.8

business SME 14.0

Corporate

fleets customers

35.9 37.1 38.7 39.8 1.8%

~ 450,000 vehicles p.a. Corporate 33.8 35.0

- thereof 47%: smaller fleets (100 vehicles)

2016 2018 2020 2022 2024 2025

1) Source: Dataforce 2018/2017, Statista.com

2) Source: Roland Berger, Embracing the Car-as-a-Service model – The European leasing and fleet management market, 2018

27 27Long-lasting relationships with key customers – moderate customer

concentration

FLEET LEASING CUSTOMER TYPE FLEET LEASING CUSTOMER STRUCTURE1)

[as of 31 December 2018]

Duration of relationship with top 10 customers

20 years

5% 18% 39% 38%

Multi Supply Single Supply Average length of relationship = 18 years

44% Customer concentration

47%

Top

Customers 2-10 Other customers

customer

42% 47%

11%

9% Top 10 customers = 53%

Dual Supply

Contract expiration

2019 2020 2021 2022+

42% 28% 22% 8%

Average term = 39 months

1) Based on Fleet Leasing contracts in Germany as of 31 December 2018 (except order book and service contracts); average term incl. foreign countries

28 28With the establishment of Sixt Leasing’s local sales activities a new

customer group with an attractive margin potential is targeted

CUSTOMERS WITH 20-80 VEHICLE FLEET

ANCHORING BUSINESS

BOOST SALES ▪ Further strong

contract growth

▪ Promising lead

SET UP TEAM pipeline ▪ Anchoring small fleet

customer segment as

▪ Local sales team set ▪ Ambitious new further mainstay and

PILOTING PHASE

up in five regions business targets growth area within

▪ Development of offer across Germany Fleet Leasing

▪ Substantial increase business field

calculator & technical

▪ Significant increase of contracts expected

standard profile

of customer base ▪ Further diversification

▪ Finalising of product of Sixt Leasing’s

▪ First customers won

standardisation customer portfolio

2017 2018 2019 2020+

29Agenda

A INTRODUCTION 04

B HIGHLIGHTS & FINANCIALS FY 2018 // GUIDANCE – BJÖRN WALDOW 06

C GROUP STRATEGY & OUTLOOK – MICHAEL RUHL 18

D FLEET LEASING – MICHAEL RUHL 27

E ONLINE RETAIL – DR. FELIX FRANK 31

F FLEET MANAGEMENT – CHRISTOPH V. TSCHIRSCHNITZ 43

30 30Introducing Dr. Felix Frank, Managing Director Online Retail

▪ Since 1 January 2019: Chief Digital Officer (CDO) and

Managing Director Online Retail

▪ 2012 – 2018: Vice President Customer Product and

Marketing at the Scout24 Group, heading the operational

management of the digital marketplace AutoScout24 as well

as the marketing and product strategy for the dealer,

manufacturer and private seller business

▪ More than ten years of professional experience in the fields of

e-business, innovation management and pricing

▪ 2006 – 2012: Boston Consulting Group, core member of

technology, media and telecommunication practice

▪ Doctorate in technology marketing and customer relationship

management

▪ Degree in international computer science

31 31Two important secular market trends in our favour

SHIFT TO ONLINE USING INSTEAD OF OWNING

[Online share of direct sales in selected industries; Germany]1) [Increasing demand for subscription models]

38%

29%

26%

16%

12%

2%

New Living/ Jewellery/ Fashion Consumer Travel

cars furniture watches Electronics

New car sales just at the beginning of (All-inclusive) subscriptions becoming

digitalisation wave preferred paradigm

1) Sources: DAT-Report 2019; own estimates; HDE, Online Monitor 2018; FUR, ReiseAnalyse 2018

32 32Significant pent-up potential for online sales

INFORMATION BEHAVIOUR DEALER VISITS ONLINE SALES DEMAND

[Share of new car buyers using the internet as [Average dealer visits of new car buyers; Germany]2) [Readiness to order a car online; Germany]3)

information source; Germany]1)

+29% -45%

81% 3.3 Online

ready

63% Not online 34%

ready

1.8

66%

2013 2018 2015 2018

Information phase already Almost two thirds of car

happening almost purely Only 0.8 additional dealers buyers are ready to order the

online visited for car purchases next car online

1) DAT-Report 2014; DAT-Report 2019

2) Sources: DAT-Report 2019; own estimates; HDE, Online Monitor 2018; FUR, ReiseAnalyse 2018

3) Source: MHP, Online Car Sales 2018

33 33Usage based models catalyst for online sales

NEW CAR COST IN COMPARISON DEMAND FOR CAR SUBSCRIPTION ROCKETING

[in EUR]1) [Google search volume ‘auto abo’]

Average

e-commerce basket

72

Skoda Citigo

(48/10 leasing rate)

75

Average maximum

online spend

1,353

Skoda Citigo

(Min leasing 1,414

commitment)

Skoda Citigo

(Cash purchase)

9,870

08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19

Leasing rate in line with typical Subscription category for cars seeing strong

e-commerce spending amounts demand growth

1) Sources: IntelliAd, E-Commerce Branchenindex; Skoda Citigo leasing rate and list price based on prices on sixt-neuwagen.de

34 34Sixt Neuwagen ideally positioned against these trends: #1 new car

sales and fully fledged fleet operations at scale

STRONG BRAND AWARENESS LARGE USER BASE FLEET OPERATIONS AT SCALE

[Supported brand awareness of online vehicle platforms]1) [Example: Sixt Leasing service & dealer network in Germany]

1,379,000

AutoScout24 87,3

mobile.de 85,5

Sixt-Neuwagen.de 53,7 260,700

Meinauto.de35 39,5

+ many other key

functions already

autohaus24.de 35,5

44,700 at scale:

- Procurement

12neuwagen.de 27,3 - Remarketing

Contract Registered Website - Customer service

carneoo.de 7,5 portfolio users visits/ -…

month Workshop/garage Dealer

Sixt Neuwagen is strongest Sixt Neuwagen has a very Sixt Neuwagen already has the

online new vehicles brand in large addressable user infrastructure to run an all-

Germany base inclusive subscription model

1) Own survey

35 35Our way forward

1

Establish a digital culture and organisation ▪ Time to market

Digital culture and as basis to effectively develop best-in-class ▪ Effectiveness

organisation digital products and services ▪ Talent acquisition

2

Step up website UX and operational ▪ Retention rate

Best customer experience processes in order to deliver a best-in-class ▪ Repurchase rate

customer experience both on- and offline 36 ▪ Cost per sale

3

More user group-specific differentiation in ▪ Addressable

Customer specific proposition and go-to-market to better audience

propositions address user needs ▪ Conversion rate

x Deep dive in following

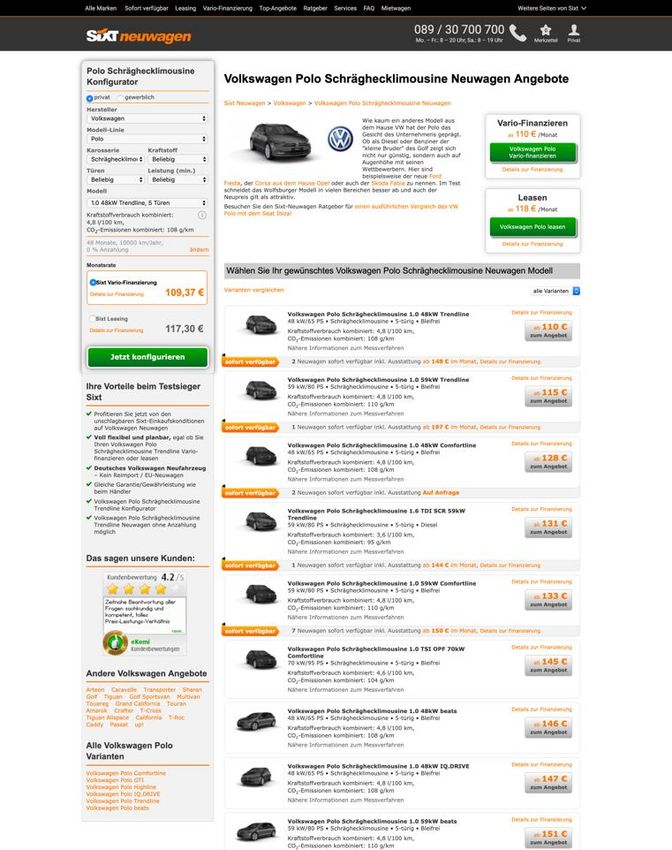

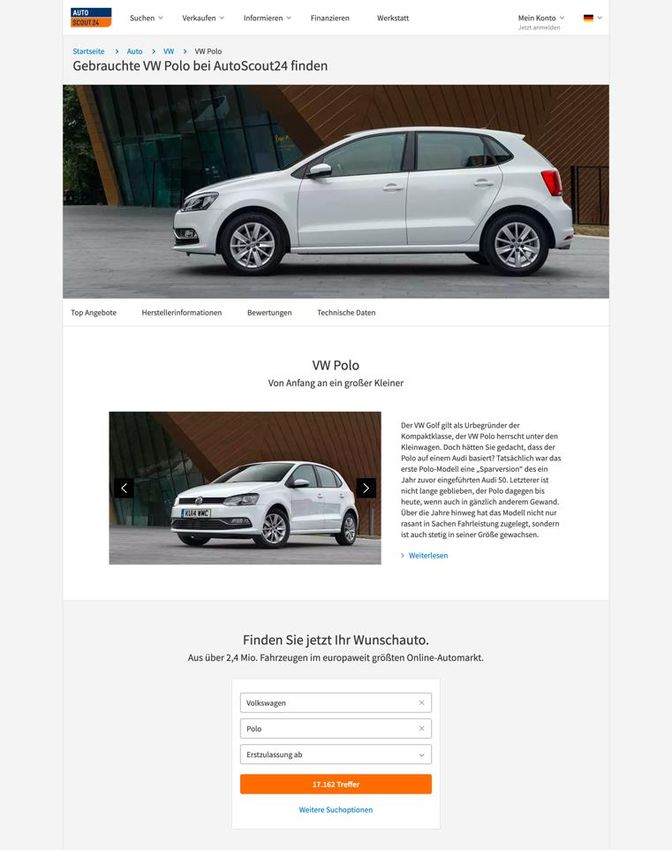

36 362 Best customer experience: Ordering process with headroom for

improvement… and we already proved what is possible

LEADS PER FTE1) CREDIT CHECKS PER FTE1) CONVERSION TIME2)

+56% x4.5 -33%

Regular Fully digital Regular Fully digital Regular Fully digital

Fully digital sales and ordering Number of processed credit Time to close sales was

process and pre-defined product checks was increased significantly significantly reduced, leading to

enable handling of significantly due to pre-registration by the client higher customer satisfaction and

more leads per FTE and automated preliminary checks conversion rates

1) Regular: 2017 except March and April; Digital: March 2017 2) Regular: All 2017 new contracts without 1&1 campaign; Digital: 1&1 contracts

37 372 Best customer experience:

Significant improvement potential in UX

CURRENT SIXT-NEUWAGEN LANDING PAGES EXAMPLE: AUTOSCOUT24 LANDING PAGE

38 383 Customer group-specific propositions: clear user groups help to

build targeted propositions

Buying criteria importance

CHARACTERISTIC Choice Price Convenience OUR PROPOSITION

Emotional approach to ▪ Build-to-order cars with best-in-

car buying and very class configurator & competent

specific and detailed sales consultants

preferences on make, Detailed Flexible on Perfect

configu- budget for buying ▪ Leasing/ Vario-financing as

Car Fan model and extras ration dream car experience means to afford dream car

Classic smart shopper

who is triggered by Special campaign offers with no/

discounts rather than low customization at very

concrete models Flexible on Fully deal- Simplicity in attractive rates

model driven decision-

Deal Maker making key

Utilitarian view on cars; Worry free with all-inclusive

high aversion of package, potentially with lower

potential unplanned cost Brand as Flexible on Peace-of- commitment requirements

and long commitment ‘insurance‘ model to mind key (currently in development)

Security Seeker for quality match budget

39 393 Customer group-specific propositions: Sixt Leasing ideally

positioned for worry-free proposition (with growing demand)

OEMs Marketplaces Startups Captives Sixt Leasing

Strong brand, no

CONSUMER REACH ~ direct contact ✓ ✓

Car variety/ configuration ~ ✓ ~ 10-20 models ✓ ✓

PROPOSITION

Subscription pricing ✓ ✓ ~ Deferentfacto,positioning

but dif-

Flexibility/ low committment ✓

Several add-on

Worry-free package ✓ ✓ ~ services

Sourcing ✓ ✓ ✓ ✓

Handover logistics ✓ ~ Via 3rd party Potentially

dealers

via

✓ Already at

OPERATIONS

scale with

Service operations ✓ ~ Via 3rd party Potentially

dealers

via

✓ high margins

Customer service Potentially

dealers

via

✓ Not at scale ✓ ✓

Remarketing Potentially

dealers

via

~ Via 3rd party ✓ ✓

Financing Potentially

captives

via

~ Via 3rd party ✓ ✓

Sixt Leasing with fully fledged operations at scale –

and opportunity to expand service penetration as additional margin source

Analysis based on AIM group classified intelligence report Vol 19 No 23a, Dec 2018

40 40Our plan

3

Rocketing

2

Fixing

&

Innovating

1 ✓

Analysed

41 41Agenda

A INTRODUCTION 04

B HIGHLIGHTS & FINANCIALS FY 2018 // GUIDANCE – BJÖRN WALDOW 06

C GROUP STRATEGY & OUTLOOK – MICHAEL RUHL 18

D FLEET LEASING – MICHAEL RUHL 27

E ONLINE RETAIL – DR. FELIX FRANK 31

F FLEET MANAGEMENT – CHRISTOPH V. TSCHIRSCHNITZ 43

42 42Page 43

Introducing Christoph v. Tschirschnitz, Managing Director

Sixt Mobility Consulting

▪ Since 1 November 2018: Managing Director

Sixt Mobility Consulting GmbH

▪ 2014 – 2018: President and CEO of the BMW Group

Region Central & Southeastern Europe

▪ 2008-2014: Member of the BMW Group Germany

management, leading the Corporate & Direct Sales

business segment

▪ 2014 – 2008: Director Sales & Marketing for the BMW

sales region Asia, Pacific, Africa and Eastern Europe

▪ Further management positions at BMW Group in the

fields Corporate Control/M&A, Distribution Channels

Strategy and at BMW MotorradPage 44

Business model and scope of service

We manage corporate fleets on behalf of companies with a broad range

of services.

We add value to the business of our corporate customers by using

our vast experience & technologies in managing fleets and our

purchasing power to buy car-related technical services.

We consult companies on corporate mobility options with the aim

to provide attractive and efficient individual mobility for their employees.

Beyond managing the traditional company car we offer

innovative and more modular means of individual mobility to corporates.Page 45

Sixt Mobility Consulting acts as intermediary between its

corporate customers, their mobility users and suppliers

CORPORATE CUSTOMER

▪ Consulting ▪ Mandate for fleet

▪ Reporting management

▪ Invoicing ▪ Budget for employees

Full range of corporate mobility

solutions for employees

Employee 1 Employee 2 Employee 3

− Car sharing budget − Classic company car − Mobility budget

− Public transport allowance − Ride-hailing budget − Company bikePage 46

We do have a strong base for serving our corporate

customers across Europe

COMPANY STRENGTHS CUSTOMER PROPOSITION

✓ Very strong mobility brand ✓ Consulting based on decades-long

creates trust and attractiveness fleet management experience

✓ 42,000 vehicles under management ✓ Adding value for our customers through

optimisation of total cost of ownership

✓ Vast experience and knowledge

of fleet management ✓ We offer modular individual solutions

✓ Strong track record of cost-efficient ✓ Supplier-neutral sourcing and consulting

operations

✓ Simplification of fleet management processes

✓ We cooperate with any leasing

company or supplier ✓ Full-service car user support

✓ Comprehensive range of services 2 stakeholders

within company

✓ Deep integration with customer

(both in terms of mobility and IT) FLEET MANAGER CAR USERPage 47

Future growth is especially supported by three developments

1

MARKET 2

DIGITALISATION 3

▪ >12 million fleet cars in

INNOVATIONS

Europe

▪ We re-shape our business

▪ Strong trend to outsourcing model by digitalising of our

corporate fleets operations until the end of ▪ Rising demand for modular

▪ Growing demand for 2019 corporate mobility due to

additional types of changing customer needs

▪ Growing scalability of our

individual corporate mobility resources ▪ We have access to all kinds

▪ Our European scope and ▪ Company growth will of innovative modular

growing presence disconnect from labour mobility serviced by all

costs kinds of suppliers

▪ Rising profitabilityPage 48

1

Sixt Mobility Consulting targets a huge market in Europe

LARGE MARKET POTENTIAL HIGH CONCENTRATION ATTRACTIVENESS OF SME

[Cars under management in EU-18 in million]1) [Cars under management in EU-6]1) [Subdivision of vehicles in corporate fleets in DE]2)

3.1 1.000+

Light commercial

vehicles (LCV) LCV 0.6 16%

2.4 2.4 500-999

2.3 6% 20-99

0.5 Germany

0.8 300-499 6% 52%

1.7

>12m cars 0.2

20%

in Europe PV 2.5

0.9 100-299

1.9 0.1 0.7

1.6 1.5

10.4 0.1

0.8 0.6 ~ 450 fleets

Passenger

vehicles (PV) DE FR UK IT NE ES ~ 1,700 fleets

~ 17,500 fleets

More than 12 million company cars ~ 11 million serviced company cars in Large untapped potential in the

are serviced in Europe only six European countries < 300 vehicle fleet segment

1) Source: Roland Berger, Embracing the Car-as-a-Service model – The European leasing and fleet management market, 2018

2) Dataforce 2017Page 49

1

Sixt Mobility Consulting expands in Europe

WHY INTERNATIONALISING

▪ Making use of further large

market potential in Europe

▪ Serving transnationally

operating companies UK OUR EXPANSION PLAN

NL

demanding transnational fleet NL

management services DE ▪ Boost French business in a

▪ Leveraging synergies market with large fleets

across countries FR CH AT

AT ▪ Re-establish our Dutch

operations

▪ Expand our Swiss operations

IT

▪ Establish SMC Austria as hub

ES

for Eastern Europe

▪ Prepare new market entries

in UK, Italy and Spain

▪ Opportunistic M&A

Home market Existing foreign subsidiaries New target countries (acquire local competitors)Page 50

Sixt Mobility Consulting strengthens the operating model 2

with the aim to grow fast and profitably

TOMORROW

DIGITAL OPERATIONS

TODAY

SCALABILITY OF

CALL-CENTRE BASED RESOURCES

USER SERVICES DIGITALISING

▪ Labour-intensive services ATTRACTIVE SERVICES

THE OPERATING

24/7 TO USERS

▪ Costly MODEL OF SMC

▪ Analogue

IN 2019 REDUCE COST

▪ Cumbersome

PER SERVICE

INCREASING

PROFITABILITYPage 51

Our new app is the core of our future business operations – 2

starting in June 2019

Our All-New Fleet Management App

‘THE COMPANION’

Shifting service operations from employees to digital self-service

CORE FUNCTIONALITIES OF THE APP

▪ Fleet users are able to carry out entire company

car-related tasks by themselves

▪ Messenger service for communication between

fleet manager and car user

▪ The app is customizable to specific company

needs, e.g. car policy, sourcing, etc.

THE COMPANION will become the new all-in-one touch point for corporate car usersPage 52

Our new app aims to further improve service levels, user 2

experience and easy-of-use for corporate car users

TOP FEATURES OF 1.0 VERSION

▪ Dynamic start page reminds users

of upcoming tasks, e.g. book a

workshop appointment

▪ Workshop online appointment tool

to easily arrange online workshop

appointments

▪ Appointment overview

▪ Workshop finder map

▪ FAQ pages for accident and

breakdown situations

▪ ‘Click to Call’ function –

Sixt Assistance hotline numberPage 53

3

We shape the future of corporate mobility

TRADITIONAL CHANGING MOBILITY FUTURE OF

CORPORATE MOBILITY CORPORATE MOBILITY

NEEDS OF EMPLOYEES

Employee receives or demands ▪ Especially employees working in Mobility demands of employees

company car larger cities increasingly use vary significantly

alternative mobility solutions

instead of a car

▪ Company car loses motivational

Employer provides company car to character for some employees Employer wants to keep pace with

employee ▪ Alternative and innovative mobility talent requirements

concepts (like mobility budgets, car

sharing, ride-hailing, company

bikes, etc.) find their way into

Car is managed by internal or corporations Companies look for a full-range

external fleet manager corporate mobility provider/manager

with digital servicesPage 54

Summary

1

MARKET 2

DIGITALISATION 3

✓ >12 million serviced INNOVATIONS

company cars in Europe

✓ Introduction of

✓ Increasing market ‘THE COMPANION’ app

potential ✓ We address the changing

✓ User self-service adds customer needs

✓ Clear international value for customers and

expansion roadmap investors ✓ SMC is best positioned to

benefit from this trend

✓ Scalable platform will

support further growth ✓ Product innovations will

support growthHighlights

Ten action fields identified on the Group level to achieve significant

1 growth of contract portfolio, operating revenue and EBT until 2021

Favourable market trends and customer segmentation open up

2 further potential on top of underlying growth in Online Retail

Digitalisation and internationalisation deliver substantial value and

3 growth upsides in Fleet Management

Smaller fleets present attractive margin potential within competitive

4 Fleet Leasing market and support diversified customer base

Attractive dividend policy backed by resilient risk-return profile

5 and significant reduction of refinancing rate since IPO

55 55Q&A 56 56

Contact details

ADDRESS INVESTOR RELATIONS

Sixt Leasing SE Stefan Kraus

Zugspitzstrasse 1 Sixt Leasing SE

82049 Pullach T: +49 89 74444 4518

Germany F: +49 89 74444 84518

Email: stefan.kraus@sixt-leasing.com

57 57Appendix 58 58

Sixt Leasing Group: Revenue and earnings performance FY 2018

in EUR million 2018 2017 Change in %

Operating revenue 480.5 454.4 5.7

Sales revenue 325.3 289.6 12.3

Consolidated revenue 805.8 744.0 8.3

thereof Leasing business unit 705.0 637.8 10.5

thereof Fleet Management business unit 100.8 106.1 -5.0

Fleet expenses and cost of lease assets -508.0 -460.7 10.3

Personnel expenses -36.5 -33.0 10.4

Net other operating income/expense -20.4 -16.0 -28.0

EBITDA 240.8 234.3 2.8

Depreciation and amortisation -197.1 -188.3 4.7

Net finance costs -13.2 -16.2 18.6

EBT 30.5 29.7 2.8

Operating return on revenue1) 6.4 6.5 -0.1 points

Income tax -8.6 -8.8 -2.6

Consolidated profit 22.0 20.9 5.1

Earnings per share (in EUR) 1.07 1.01 -

1) Ratio of EBT to operating revenue

59 59Sixt Leasing Group: Further KPIs FY 2018

31 Dec 2018 31 Dec 2017 Change in %

Group contract portfolio 129,700 132,900 -2.4

thereof Online Retail 44,700 45,400 -1.6

thereof Fleet Leasing 43,000 48,100 -10.5

thereof Fleet Management 42,000 39,400 6.6

in EUR million

Total equity and liabilities 1,392.7 1,442.8 -3.5

Lease assets 1,204.4 1,219.2 -1.2

Financial liabilities1) 1,026.1 1,059.8 -3.2

Equity 216.8 205.1 5.7

Equity ratio (%) 15.6 14.2 1.4 points

2018 2017

Gross cash flow 247.8 216.7 14.3

Investments in lease assets 475.7 619.2 -23.2

1) Current and non-current financial liabilities; as of 31 December 2017 including EUR 190.0 m Core Loan and EUR 3.9 million other liabilities to related parties

60 60You can also read