SOUTH AFRICA'S CREDIT OUTLOOK - 30 MARCH 2020 ADRIAAN PASK, PHD PSG WEALTH: CHIEF INVESTMENT OFFICER

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

South Africa’s credit outlook

30 March 2020

Adriaan Pask, PhD

PSG Wealth: Chief Investment Officer

The world is constantly turning. We know how important

it is to keep up. That’s why we continually expand our

insurance and investment offerings, that’s how we keep

your best interests at heart.

Copyright © PSG

Contents

1. Review of recent ratings

2. Rating factors

3. Our base case

4. Relative ratings – emerging market (EM) peers

5. Market and currency movements

6. Bottom line

7. Frequently asked questions

2

Copyright © PSG1 Review of recent ratings 3 Copyright © PSG

Fitch – 26 July 2019

• Fitch kept South Africa’s long-term foreign and local currency debt on BB+. This is the

first notch of sub-investment grade.

• However, the ratings agency downgraded the country’s outlook from stable to negative.

• Rationale:

- The agency cited concerns over the government’s financial support of state-owned

enterprises, particularly Eskom.

“While South Africa’s worsening debt forecasts don’t include the threats posed by the state taking

on any of the embattled power utility’s R450 billion ($30 billion) of debt, any risks posed by this

are reflected in the nation’s current credit assessment.”

- Low economic growth

“Failure to stabilize the debt-to-GDP ratio over the medium term is a negative rating sensitivity,”

commented Fitch.

Source: Fitch analytics

4

Copyright © PSGS&P – 22 November 2019

• S&P Global Ratings cut South Africa’s credit outlook from stable to negative.

• However, the country’s long-term foreign currency rating remains at BB, which is two notches

below investment grade and our long-term local currency rating remains at BB+.

• S&P warned that it could still lower these ratings if it observed continued fiscal deterioration

and if the economy failed to improve.

• Rationale:

“The negative outlook indicates that South Africa’s debt metrics are rapidly worsening as a

result of the country’s low GDP growth and high fiscal deficits,” said S&P.

- Low GDP growth and high fiscal deficits are causing an unsustainable debt trajectory.

- Poor economic performance is a result of weak investor sentiment and investment,

power shortages, and sluggish reform momentum.

Source: S&P Global Ratings

5

Copyright © PSGMoody’s – 27 March 2020

• Moody’s Investors Service (Moody’s) downgraded South Africa to junk status.

• The ratings agency dropped South Africa’s long-term foreign and local currency ratings to BA1

with a negative outlook. This is the fist rung below investment grade.

• Rationale:

- “Unreliable electricity supply, persistent weak business confidence and investment as well as long-

standing structural labour market rigidities continue to constrain South Africa’s economic growth. As

a result, South Africa is entering a period of much lower global growth in an economically vulnerable

position,” said Moody’s.

- “The unprecedented deterioration in the global economic outlook caused by the rapid spread of the

coronavirus outbreak will exacerbate South Africa’s economic and fiscal challenges and will

complicate the emergence of effective policy responses.” Moody’s

• This changes was widely expected, and priced in to some regard.

• Although a rating upgrade is unlikely in the near future, they could upgrade the rating should

they see “a gradual reduction in South Africa's primary deficit in the next few years, with

increasing assurance that government debt will stabilize comfortably below 90% of GDP”.

Source: Moody’s analytics

6

Copyright © PSGRatings in context

When is it prime or non-investment grade

7 PSG Wealth research team

Copyright © PSGFrom an economic perspective

…the following happens when a sovereign a downgraded to ‘non-IG’

• Government may struggle to raise funding for projects

• Yields on bonds should move higher to compensate investors for additional

sovereign risks

• This increases government’s cost of capital

• Added pressure on national budget, and ultimately taxes

• Corporate financing cost will also increase

• This places pressure on earnings and growth

• The rand already weakened sharply on downgrade news

• Further rand volatility likely to continue

8

Copyright © PSG2 Ratings factors 9 Copyright © PSG

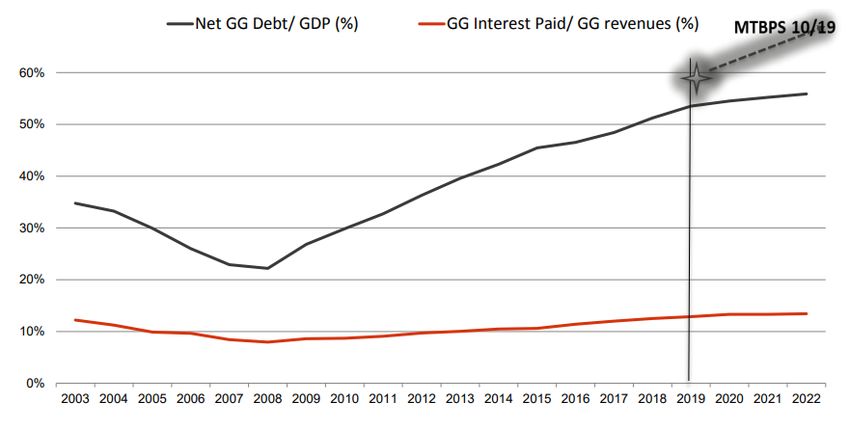

Debt burden Debt levels have been rising substantially post-crisis 10 Source: S&P Global Copyright © PSG

Low growth

Annual GDP since 2013

3,0

2,5

2,5

2,0

1,8

1,5 1,4

1,2

1,0

0,8

0,5 0,4

0,20

0,0

2013 2014 2015 2016 2017 2018 2019

Sources: Trading Economics and PSG Wealth research team

11

Copyright © PSGMacroeconomic pressures

• Covid-19’s adverse economic effect both on a local and global scale

• Instability at Eskom and other state-owned enterprises

• High unemployment rate

12

Copyright © PSG3 Our base case 13 Copyright © PSG

Our base case

• Short-term volatility should persist and could well place pressure on bond yields as

well as the currency.

• However, when looking at Brazil’s economy after Finch, S&P and Moody’s

downgraded it, bond and exchanges rates recovered substantially.

• Although South Africa has to face the added pressure of fighting the effects of

COVID-19, we feel that the market has already priced in the downgrade and that

rates should normalize over the medium term.

14

Copyright © PSGHow does South Africa compare to its EM peers? 4 15 Copyright © PSG

Debts and deficits of EM peers

SA government debt at 62.2% of GDP

Government debt (as % of GDP)

0,00% 10,00% 20,00% 30,00% 40,00% 50,00% 60,00% 70,00% 80,00% 90,00%

3,00%

2,00% Russia

1,00%

0,00%

Governmebt deficit / GDP (%)

-1,00%

-2,00% Turkey Hungary

-3,00%

India

-4,00%

Romania South Africa

-5,00%

-6,00%

-7,00% Brazil

-8,00%

16 Sources: Trading Economics and PSG Wealth research team

Copyright © PSGSouth Africa’s credit risk premium based on the S&P

Local currency lowered to BB

17

Copyright © PSG

Source: PSG Wealth research team5 Market and currency movements 18 Copyright © PSG

Currency moves after the downgrade

As demonstrated by the USD/ZAR exchange rate and JSE All Share

graph, both the local 18,00 46 000

market and currency took

a knock after the Moody’s 17,60

44 000

announcement; pressure

that might remain during 42 000

the short term. However, 17,20

we feel that it will recover, 40 000

at least to some degree, 16,80

once the dust has settled 38 000

with regards to the

16,40

downgrade decision. 36 000

16,00 34 000

Mar-13 Mar-15 Mar-17 Mar-19 Mar-21 Mar-23 Mar-25 Mar-27

USD/ZAR JSE ALSI (J203)

19

Copyright © PSGOther bond market responses to earlier downgrades

Yield recover

20

Sources: PSG Wealth research team, S&P Global Ratings, Bloomberg

Copyright © PSG6 Bottom line 21 Copyright © PSG

Bottom line

From an economic perspective

• A lot of work ahead (ratings just affirm what is known)

Employment

Education

Investment

Revenue/revenue productivity

Commodity prices and agriculture

Financing costs

Contingent liabilities

Spending for growth

22

Copyright © PSGBottom line

From an investment perspective

• Don’t make emotional investment decisions. It rarely ends well for investors.

• Review your financial plan and your risk appetite.

• If your financial plan makes sense and your investments are allocated to reflect your

risk appetite and long-term objectives, leave the rest to the guys who work with

markets daily.

• Clients should take comfort in the fact that:

- Their financial planning is done by the best financial planners available in South

Africa.

- We have award-winning processes and products.

- Our investment partners are rated amongst the top nationally and internationally.

23

Copyright © PSG7 Frequently asked questions 24 Copyright © PSG

Frequently asked questions and answers

1. Now that SA has been downgraded, what is the likely impact on the local economy?

From an economic perspective the government may struggle to raise funding for projects. Yields on bonds will have to move higher in order

to compensate investors for the additional sovereign risks, which increases the government’s cost of capital, which will place additional

pressure on the national budget, and ultimately taxes. In addition, corporate financing cost will increase, which places pressure on earnings

and growth. From a market perspective, bond yields have already moved higher to price in the sovereign risk increase.

2. What does junk status really mean?

It means that the perceived probability of defaulting on the capital loan repayment is higher than that of investment grade bonds. In return of

taking additional risk, investors will demand greater compensation, i.e. higher yields. This cost will be directly borne by government and

corporates, but ultimately passed on to consumers and shareholders.

3. Who would be able to invest in SA now that we’ve reached junk status?

The country remains open for investment to anyone who is unaffected by investment mandate constraints. Some mandates of pension funds

or unit trust portfolios are required to invest in investment grade instruments only. These investment vehicles will no longer be able to invest

in these bonds, and finance will have to be obtained through other investors with more liberal mandates.

25

Copyright © PSG4. What type of investors are we likely to see enter our local bond market?

Investors with higher risk appetites willing to take on additional sovereign risk in return they’ll receive additional

compensation.

5. Would a junk status rating affect consumers/everyday South Africans?

Yes, most definitely. Yields on bonds will have to move higher in order to compensate investors for the additional

sovereign risks, which increases the government’s cost of capital. This will place additional pressure on the national

budget, and ultimately taxes. In addition, corporate financing cost will increase, placing pressure on corporate earnings

and economic growth.

6. Did you anticipate that SA will reach junk status?

We previously communicated that “the market is currently pricing in a strong possibly of a downgrade.”

26

Copyright © PSG7. How could SA improve its rating from here?

Our two main concerns are the current account and the fiscal budget. We need to improve our relative attractiveness in order to attract

investment. We need to increase our export to import ratio and get a firmer grip on our fiscal spending. Economic growth will go a long way

towards increasing spending power. Ultimately we will have to cut spending and increase revenue simultaneously in order to make swift work

of recovering investment-grade status.

8. Is it the end of the world now that SA reached junk status?

It has serious implications for both investors and consumers, and it poses a massive challenge to all South Africans. We cannot afford to be

complacent regarding the impact, nor lacklustre in our efforts to turn things around.

At the same time, a diversified portfolio of assets will deliver mixed results in reaction to the downgrade. Bonds’ capital value will be under

pressure, but at the same time, more attractive yields will be on offer. Offshore investments will benefit from a weaker currency, offsetting

some the losses in bank, retailers, and property investments.

Our product positioning was well diversified in anticipation of tougher, both political and economic, investment climate. We anticipate that

weak sentiment will dominate markets over the short term, which may offer some attractive investment opportunities.

27

Copyright © PSGWant to talk to us?

Or register for PSG Wealth newsletters?

• Please visit https://beta.psg.co.za/secure/comms-ui/manage-subscriptions to sign

up for our PSG Wealth newsletters.

• Follow us on social media:

- https://www.facebook.com/PSG.Wealth.platform

- https://twitter.com/PSGWealth

- https://www.linkedin.com/company/psg-wealth/

- https://www.youtube.com/user/PSGKonsultLtd

28

Copyright © PSGDisclaimer

The content and information provided are owned by PSG Wealth Financial Planning (“PSG") and are protected by copyright and other

intellectual property laws. All rights not expressly granted are reserved. The content and information may not be reproduced or distributed

without the prior written consent of PSG.

The content of this presentation is provided by PSG as general information about the company and its products and services.

PSG does not guarantee the suitability or potential value of any information shared in this document.

The information provided is not intended nor does it constitute financial, tax, legal, investment, or other advice. Before making any decision

or taking any action regarding your finances, you should consult a licensed financial adviser.

Nothing contained in the presentation constitutes a solicitation, recommendation, endorsement or offer by PSG, but shall merely be deemed

to be an invitation to do business.

PSG has taken and will continue to take care that all information provided, in so far as this is under its control, is true and correct. However,

PSG shall not be responsible for and therefore disclaims any liability for any loss, liability, damage (whether direct or consequential) or

expense of any nature whatsoever which may be suffered as a result of or which may be attributable, directly or indirectly, to the use of or

reliance upon any information provided.

FAIS affiliates of the PSG Konsult Group are authorised financial services providers.

29

Copyright © PSGFAIS Affiliates of the PSG Konsult Group are authorised financial services providers. Copyright © PSG

You can also read