Standard Chartered - Publicised tax avoidance strategy

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Standard Chartered –

Publicised tax avoidance strategy

January 2015

Summary

Standard Chartered is a UK FTSE-100 listed Mozambique it would theoretically reduce Capital

bank with an extensive presence across Gains Tax from 32 percent to 0 percent. Among

Africa, Asia and the Middle East. The bank other countries potentially affected are Nigeria,

Kenya, Uganda, and Zimbabwe depending on

offers a wide-range of banking services in

the specifics of their taxation treaties with Mauritius.

15 African countries1. It has operated on

the continent for 150 years and is a well- Although it does not endorse the strategy, by

recognised brand both in African business publishing it Standard Chartered contributed to a

circles and among consumers. conversation among companies about how to

avoid tax in some very poor countries. According to

The bank plays an important role in ActionAid International research, almost half of all

providing financial services for growing investment into developing countries goes through

tax havens3. Meanwhile the OECD estimates that

economies on the continent. In its report

developing countries lose three times more to tax

“Impact on Africa” it states it supports 1.9 havens than the amount they receive in aid each

million jobs in Sub-Saharan Africa and in year4. This is money that could otherwise be used

2013 supported trade worth USD7.2 billion2. to pay for schools, hospitals and transport

infrastructure and to reduce aid-dependency.

Evidence seen by ActionAid International shows the

bank published an article by a Mauritius-based The need for African nations to improve revenue

financial firm describing a tax avoidance strategy in collection is widely recognised. For example, a

its publication Standard Chartered Insights major report by the High Level Panel on Illicit

2013/2014: Maximising Business Opportunities Financial Flows for the African Union chaired by

in Asia, Africa and the Middle East – a former President of South Africa Thabo Mbeki will

Treasury Guide. The strategy can be used to examine how African nations can prevent the loss

legally avoid tax in some of the poorest countries in of billions of dollars of tax revenue – which could

the world and was contained within an article otherwise be invested in vital services. To be clear,

authored by Cim Tax Services managing director ActionAid International is not suggesting that the

Gary Gowrea. use of the investment structure described in the

Cim article is unlawful or would constitute an “illicit

The article highlights the tax benefits of structuring financial flow”.

investments through Mauritius in order to legally

avoid capital gains tax and withholding tax. This Standard Chartered states that the Cim article does

strategy could be used by companies to legally not constitute the Bank’s own advice or opinion,

avoid potentially hundreds of millions of dollars of and that it does not itself promote tax avoidance

tax on a single deal. In the example of products to its customers.

ActionAid International Report January 2015The evidence The ActionAid International allegation relates to and opinion. The tax avoidance strategy appeared a tax avoidance strategy published in the journal in an article entitled “Mauritius: An Investment “Standard Chartered Investment Insight Gateway to Africa” and was written by Mauritius- 2013/14”. This publication consists of articles written based financial company Cim Tax Services. by external contributors offering investor information ActionAid International Report January 2015

The article explains that tax can be avoided The key advantages of the tax avoidance

by structuring investments through Mauritius- structure described in the article, which

based holding companies in order to take uses the example of Mozambique, are:

advantage of the island’s network of tax

treaties (referred to in the strategy as Double 1. Capital Gains Tax

Taxation Avoidance Agreements (DTAAs).)

Using the structure, a company could reduce its

There is no suggestion that the structure included capital gains tax from 32 percent to no tax at all.

by CIM in the article is particularly innovative or

This single tax avoidance strategy could potentially

unusual, or that its use by any given taxpayer is

be worth hundreds of millions of dollars to a

unlawful. In fact ActionAid International has found

company. As an example of the amount of money

a previous instance where a very similar structure

potentially involved – in 2014 the oil and gas

was advised by a major accountancy firm5.

company Anadarko was reported to have paid

The authors of the article advise investors Mozambique US$520 million in capital gains tax at

that “adequate substance and commercial the standard rate of 32% following a transaction

rationale be included in the structure to avoid which yielded a capital gain of US$1,625,000,0007.

any potential challenge by tax authorities”.

The report describes the capital gains tax advantages

However ActionAid International believes for companies operating in Africa as follows:

that the structure could be used where

“An increasing number of African states

there is little or no commercial rationale

are starting to impose capital gains tax.

for doing so other than to avoid tax.

However the DTAAs [tax treaties] in force

The article states that: in Mauritius restrict taxing rights of capital

gains to the country of the seller of the

“an essential ingredient [of Mauritian assets. Since there is no capital gains tax

investment] beyond the commercial rationale in Mauritius, the potential tax savings

is the tax arbitrage a company can benefit for a Mauritius registered company are

from”. Expanding on the taxation advantages of significant.”

Mauritius, the article goes on to say:

2. Withholding Tax

“Based on the beneficial withholding tax

rate that the treaties provide as well as the Using the structure advised in the strategy could

flexible Income Tax Act provisions, various potentially lead to a 60 percent saving in withholding

structuring possibilities are available, such tax. In Mozambique, the rate of withholding tax

as an investment holding platform or on dividends and interest is 20 percent. But

regional treasury, or a structure holding by using a holding company incorporated in

intellectual properly rights.” Mauritius this rate can be reduced to 8 percent.

The strategy is designed to be used in different The report describes the overall benefits

ways in a range of countries which have tax treaties of this form of tax avoidance to companies

with Mauritius. Mauritius has recently embarked operating in Africa as follows.

on a significant expansion of its network of tax

treaties with African nations and currently has “The majority of African states impose

more than 40 either agreed, signed or awaiting some withholding tax on dividends paid

ratification with countries including Mozambique, out to non-residents. These vary between

Kenya, Zambia, Uganda, Zimbabwe, and 10 percent and 20 percent. The DTAAs

Nigeria6. The amount of money that can be [tax treaties] in force in Mauritius limit

avoided using a similar strategy will vary depending withholding taxes on dividend[s]”.

on the specifics of individual tax treaties.

ActionAid International Report January 2015What the companies told us: Cim Tax Services Ltd Statement:

We wrote to both Standard Chartered and Cim Tax “The article in question makes mention

Services asking them to respond to our allegation. of a wide range of benefits for companies

Below is the text of the statements they sent us. and investors seeking to use Mauritius as

an investment and trading hub for Africa;

Standard Chartered Statement: the tax treatment of certain financial

receipts could be just one of these benefits.

“Standard Chartered does not consider this

Mauritius and other developing African

article to be the advice of the bank. There

countries have entered into mutually

is a clear disclaimer on the back of the

beneficial bi-lateral agreements designed

report that says ‘The opinions expressed in

to promote and increase the flow of

this publication are not necessarily those

Foreign Direct Investment to support the

of either the publisher, Standard Chartered

sustainable development of these countries.”

Bank nor the institutions for which the

contributing authors work or by which they Conclusion

have been commissioned”.

Standard Chartered clearly provide developing

“Standard Chartered is one of the largest economies with high-quality financial services

corporate tax payers in Africa. In 2013, that in turn generate jobs and reduce poverty.

across our 15 Sub-Saharan businesses

we paid US$182m in Corporation tax. An But by publishing this strategy – Standard Chartered

independent report, ‘Banking on Africa’, contributed to a culture whereby companies are

found that Standard Chartered’s support exploring ways to pay minimal tax on their profits in

for our clients underpins $1.8 billion of very poor countries. Tax avoidance costs developing

annual tax payments in Sub Saharan Africa, countries billions of dollars a year in lost revenues..

equivalent to 1.1% of the entire tax receipts

received by governments in the region.” Taxation treaties remain a key tool currently in

use by large companies wishing to avoid paying

“Our tax position is very clear. We do tax on their operations in Africa. Mauritius is in

not enter into transactions whose sole the process of rapidly expanding its network of

purpose is to minimise or reduce tax cost. taxation treaties – and there remain risks that

Similarly, we do not promote tax avoidance these treaties will continue to expose developing

products to our customers. We set out countries to further loss of tax revenues.

country-by-country tax information in

respect of the year ended 31 December By Richard Grange

2013 on our website.” With assistance from Nadia Harrison

1. h

ttps://www.sc.com/en/sustainability/performance- 5. http://www.actionaid.org.uk/sites/default/files/

and-policies/impact-reports/africa-day.html publications/deloitte_in_africa_1.pdfN

2. https://www.sc.com/en/sustainability/performance-and- 6. http://www.lowtax.net/information/mauritius/

policies/impact-reports/sub-saharan-africa-report.html mauritius-tax-treaty-introduction.html

3. http://www.actionaid.org.uk/sites/default/files/publications/ 7. http://allafrica.com/stories/201404150130.html

how_tax_havens_plunder_the_poor_2.pdf

4. http://www.theguardian.com/commentisfree/2008/

nov/27/comment-aid-development-tax-havens

ActionAid International

Postnet Suite 248

Private Bag X31

Saxonwold 2132

Johannesburg

South Africa

ActionAid is a registered charity no. 27264198

ActionAid International Report January 2015The key pages from the documents which are referred to in this report are attached below. They are the copyright of PPP

Company Limited, Standard Chartered Bank and contributors. They are drawn from the publication Standard Chartered

Insights 2013/2014: Maximising Business Opportunities in Asia, Africa and the Middle East – a Treasury Guide.

Mauritius:

An Investment Gateway to Africa

Based on Investment Promotion and companies, these are deemed to

Protection Agreements be a foreign source and get the

the beneficial As an African nation, Mauritius $3*%

*

%(

$*.( *

has signed Investment mechanism.

withholding tax Promotion and Protection

rate that the Agreements (IPPAs) with

15 African member states.

Figure 4 depicts a typical

holding structure that can be

treaties provide The IPPA typically offers set up in Mauritius. We have

the following guarantees to taken an example of a Chinese

as well as the investors from contracting Investor wishing to invest in the

flexible Income states:

1 ((&*( * %$%

emerging coal and gas sector in

%0# '+

3$$ $

%

Tax Act provisions, investment capital and the Mozambique Company can

returns;; be done either through debt or

various structuring 1 +($*

$)* equity.

possibilities are expropriation;;

1%)*

,%+($* %$(+" i) The Chinese Investor can

available, such with respect to the treatment invest in equity in the Mauritius

of investment, compensation Holding Company, which in

as an investment for losses in case of war, turn invests in the Mozambique

holding platform or (#%$4 *( %*)*$

1(($

#$*

%()**"#$*

Company.

The advantages of this

regional treasury, of disputes between investors structure are:

and the contracting states. 1)&(*

*.*(*/*-$

or a structure Mauritius and Mozambique,

holding intellectual )%$*

$3 "

withholding tax rate that the

dividend paid to the Mauritius

Holding Company will

property or rights. treaties provide as well as be subject to a reduced

*

4. "$%#.* withholding tax rate of 8% in

provisions, various structuring Mozambique.

possibilities are available, 1 *

*

&&" * %$%

*

such as an investment holding foreign tax credit mechanism,

platform or regional treasury, or the effective tax for the

a structure holding intellectual Mauritius Holding Company

property or rights. will be reduced to nil.

1+( * +)

)*

."+) ,

The Finance Act 2012 has right to tax any gains derived

amended the Financial Services by the Mauritius Holding

Act 2007 to add two activities to Company on the sale of shares

*

+( * +)%

( $

2

"%" held in the Mozambique

headquarters administration Company.

and global treasury activities. 1)%&&%)*%%*

(

Schedule 2 part II and part III tax treaties signed by

sets out that that at least three Mozambique, Mauritius has

services must be performed for exclusive rights to tax capital

three related entities, be it in gains on the sale of shares

the treasury or administrative held in the Mozambique

3" ,$

*

* , * )( Company even if the assets

provided to global business of the Mozambique Company

260 Standard Chartered Insights 2013/14The key pages from the documents which are referred to in this report are attached below. They are the copyright of PPP

Company Limited, Standard Chartered Bank and contributors. They are drawn from the publication Standard Chartered

Insights 2013/2014: Maximising Business Opportunities in Asia, Africa and the Middle East – a Treasury Guide.

Mauritius:

An Investment Gateway to Africa

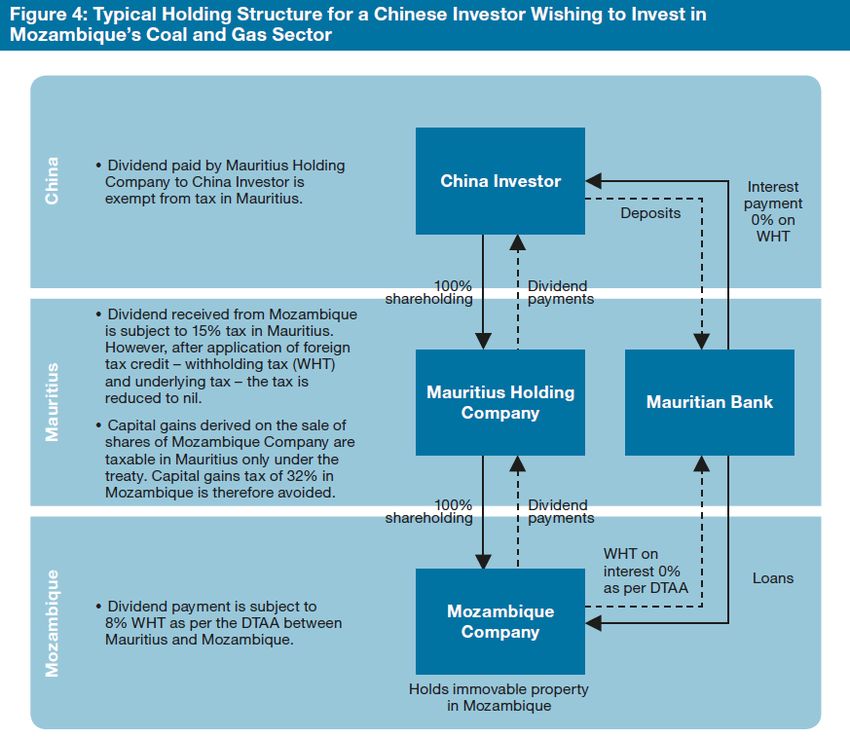

Figure 4: Typical Holding Structure for a Chinese Investor Wishing to Invest in

Mozambique’s Coal and Gas Sector

1Dividend paid by Mauritius Holding

China

Company to China Investor is China Investor Interest

exempt from tax in Mauritius. payment

Deposits 0% on

WHT

100% Dividend

shareholding payments

1Dividend received from Mozambique

is subject to 15% tax in Mauritius.

However, after application of foreign

tax credit – withholding tax (WHT)

Mauritius

and underlying tax – the tax is

reduced to nil. Mauritius Holding

Mauritian Bank

Company

1Capital gains derived on the sale of

shares of Mozambique Company are

taxable in Mauritius only under the

treaty. Capital gains tax of 32% in

Mozambique is therefore avoided.

100% Dividend

shareholding payments

WHT on

interest 0% Loans

Mozambique

as per DTAA

1Dividend payment is subject to Mozambique

8% WHT as per the DTAA between

Mauritius and Mozambique. Company

Holds immovable property

in Mozambique

Source: Taxand

consist principally of between Mauritius and 1$(*

*(*/ $*()*&

immovable property. Mozambique. by the Mozambique Company

1)*

( )$%& *"

$) to the Mauritian Bank is free

tax in Mauritius, gains are not ii) The Chinese Investor can of any withholding tax.

taxed at all. ")%3$$*

%0# '+ 1"*($* ,"/*

)#()+"*

1 , $)& /*

Company partly through a can be achieved if the Chinese

Mauritius Company to the back-to-back loan. Investor invests the money

Chinese Investor will be 1

$) %#&$/ as equity in the Mauritian

exempt from tax in Mauritius. deposits money in a Mauritian Company, which then deposits

1$,$&( $

(#$* Bank. the money in the Mauritian

can be obtained from the 1

+( * $$!&(%, Bank.

Mauritius Revenue Authority a loan to the Mozambique 1$*()*( ,/*

under Article 25 of the treaty Company. Mauritius Company from

Maximising Business Opportunities in Asia, Africa and the Middle East – a Treasury Guide

261The key pages from the documents which are referred to in this report are attached below. They are the copyright of PPP

Company Limited, Standard Chartered Bank and contributors. They are drawn from the publication Standard Chartered

Insights 2013/2014: Maximising Business Opportunities in Asia, Africa and the Middle East – a Treasury Guide.

Mauritius:

An Investment Gateway to Africa

the Mauritian Bank will be provided by the Mauritius- Conclusion

exempt from tax in Mauritius. Mozambique tax treaty are Mauritius continues to be used

1%-,(%0# '+%) not available under the South as a platform for investment

have thin capitalisation rules Africa-Mozambique or India- into Africa and Asia and to

which provide that loans from Mozambique tax treaty. reinforce its reputation as

related foreign corporations a jurisdiction of substance

must not exceed twice the Caution must be taken in through its network of IPPAs,

corresponding equity in light of greater convergence DTAAs and other such

the borrowing Mozambican toward the adoption of anti- agreements. A testimony to this

corporation. avoidance rules by developed is the December 2012 visit from

1"*

%+

*

"%$ )

(%# and emerging nations. It is International Monetary Fund

the Mauritian Bank, which strongly advised that adequate Managing Director Christine

is a non-related party, it is substance and commercial Lagarde, which resulted in

advisable to keep a debt to rationale be included in the the signing of a memorandum

equity ratio of 2:1. structure to avoid any potential with the Government of

While we have taken the challenge by tax authorities. Mauritius to locate the Africa

example of an investor from a In many cases, the returns on Training Institute in Mauritius.

country that does not have a investment will be yielded in the As reported in the press,

tax treaty with Mozambique, future. However, it is important the Australian Agency for

the structure can also be to provide substance to the International Development and

used by investors from treaty Mauritius Company well before the Chinese authorities have

countries like India and South there is any claim for treaty also pledged support for this

Africa, as the advantages $3*) initiative.

About the Author

Gary Gowrea

Gary Gowrea is Managing Director at Cim Tax Services. He has more than 15 years of

experience in international tax and advises on tax structures set up by multinational

corporations, fund managers and high net worth individuals. He is also a member

of the operational committee of Global Institutional Investors Forum and sits on

agreements. He has been a speaker at several local and international conferences and

is a Member of the Society of Trust and Estate Practitioners (UK) and the International

and holds a Diploma in International Taxation. He completed his MSc in Accounting from De Monfort

University in Leicester, UK.

262 Standard Chartered Insights 2013/14You can also read