SUSTAINABLE FINANCE & CONSUMER PROTECTION - A program by - 2 Degrees ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SUSTAINABLE FINANCE &

CONSUMER PROTECTION

A program by

Dec 2019

1 OVERVIEW

A principal-agent problem

The transition to a low carbon economy requires the mobilization of providers of capital to steer

investment decisions in a direction compatible with the objectives of the Paris Agreement and

Sustainable Development Goals. As the ultimate asset owners and beneficiaries, consumers play an

important role in this evolution towards a more ‘sustainable’ financial system. However, the current

situation suggests a major principal-agent problem:

• According to surveys, in most countries, a large majority of retail clients and beneficiaries expect their

savings to contribute to social and environmental objectives (see examples page 5).

• On the other hand, the integration of these objectives in investment strategies by intermediaries is both

marginal and superficial (see page 7 and 9).

A better alignment of investment strategies with consumer expectations is prevented by several barriers,

including: the systematic ignorance of client’s social and environmental objectives by financial advisors,

the lack of suitable products, and the lack of a level playing field regarding green marketing.

Objectives of the program

Building on the 2° Investing Initiative’s research findings*, the European Commission is currently

introducing a series of reform to address this problem, including an obligation for financial advisors to

ask about and take into account social and environmental ‘preferences’, and an obligation for product

manufacturers with social and environmental features to disclose relevant information. Given the

magnitude of the gap between offer and demand suggested by market research (see page 3), we expect

these reforms to eventually lead to a major transformation of the retail market and inspire similar reforms

in other jurisdictions. The objective of our program is to support and accelerate this transformation in

Europe and beyond via a multi-disciplinary approach including consumer research, behavioral finance,

legal and regulatory analysis, policy work, methodological and data work, and software development.

Knowledge of Identification of Responsible Reform of the Unbiased, free

retail clients’ relevant marketing suitability online advisor

expectations and investment framework based questionnaire acting as a

behavior techniques and on scientific impact and process benchmark for

suitable products assessment the industry

Scope of the activities

Following a first pilot conducted in Germany, in partnership with the Ministry of the

Environment (2018-2020), we will deploy the program in France (2020-2025) in

partnership with the environmental agency and the supervisory authorities, with funding

from the European Commission. Our objective over the next five years is to replicate the

program in key EU member States, the UK and beyond Europe. We envision doing so in

partnership with both public authorities and the private sector.

*Non-financial message in a bottle, how the environmental objectives of retail investors are overlooked in MIFID II and PRIIPS implementation

(2Dii, 2017)

2

1 OVERVIEW

Retail clients and beneficiaries are individuals who buy and sell securities, save money via financial products,

such as ETFs, mutual funds, DC pension plans, insurance products and savings accounts and/or benefit from

DB pensions plans. In Europe, they are the largest holders of financial assets. At the end of 2017, European

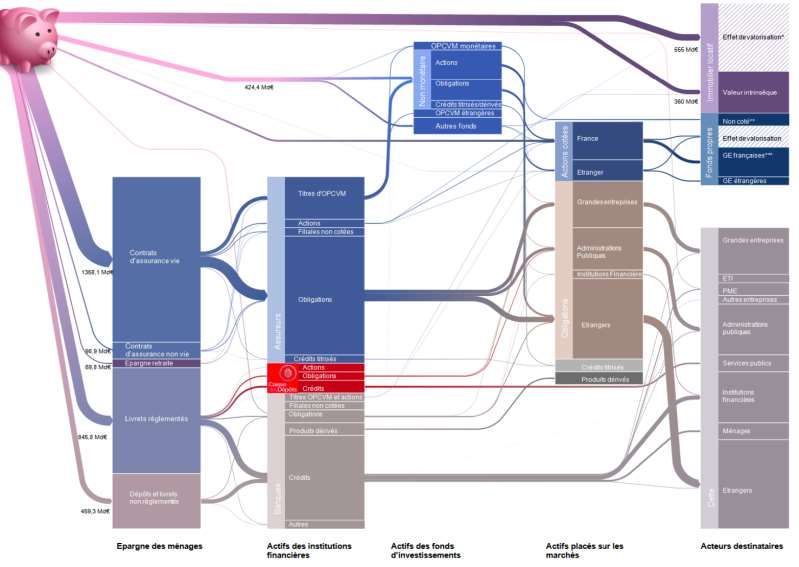

households held just under €30 trillion of liquid financial assets, representing 30% of total financial assets in

Europe (fig 1). Most retail investments being intermediated (fig 3), the ability of clients to integrate social and

environmental objectives primarily relies on product design and marketing. As far as these objectives are

concerned, our analysis suggests a major gap between client’s expectations and products sold to them (fig 2).

Retail investment by type of asset Funds profiles vs clients’ profiles – France*

(EFAMA 2019)

100% No ESG criteria

Debt securities

80%

Quoted shares Soft integration of ESG

60%

Investment funds Best-in-class/universe

40%

Currency and deposits Exclusion/thematic

20%

Insurance and pension… Impact (real economy)

0%

0% 10% 20% 30% 40% 50% Funds Clients

profiles profiles

*Figures based on AFG data for asset management in general (including institutional and retail) in France (2018) and 2Dii retail clients profiling

based on the results of consumer surveys (France, 2019) - see details page 9.

Link between household savings and the real economy in France

(2Dii/France Strategy 2015)

31 MARKET RESEARCH

The ‘non-financial’ investment objectives of retail clients and their related behaviors are

complex to understand. Our objective is to consolidate and develop further knowledge

on the topic in order to equip industry and regulator with scientific evidence. In parallel

we review how the product offer can address these needs and how it can be improved.

Quantitative consumer surveys

We design and implement quantitative consumer surveys to explore a range of topics related

to the purchase of a green financial products, including: the expected outcomes, the

motivations, the willingness to accept trade-offs, the interpretation of marketing claims, etc.

The outputs are public studies (see 1 below) as are the questionnaire themselves.

Qualitative research

The surveys are completed with qualitative interviews and focus group with consumers to

further explore the perceptions and motivations. The outputs are integrated in the public

studies and made available as short videos.

Literature review

Our research is completed by an ongoing review of new surveys and publications on the

topic. The outputs are integrated in our publications.

Behavioral finance field experiments

We support our academic and industry partners in the development of behavioral finance

experiments aimed at understanding if consumers ’walk the talk’ in real-life decision making.

Products and techniques benchmarking

Our team analyzed the offer of products and their suitability to the needs identified, with a

focus on investment strategies aiming at delivering environmental impacts. Our work

specifically focuses on assessing the effectiveness of different investment techniques

(engagement, divestment, targeted investments, earmarking, etc.) and the methods available

to substantiate impact claims related to the mobilization of these techniques. To date, we

conclude that there is a lack of methodological framework to produce evidence and

substantiate impact claims made by fund managers.

1 2

Main implementation partners

Publication Q1-2020

41 MARKET RESEARCH

How would you respond to ethical, social or environmental concerns with your investments?*

■ Having an impact in the real economy (43%)

”Because other shareholders might vote like me, and we can eventually improve things”

100% 15% “Because I want to send a message to these companies by boycotting them”

90%

80%

do not ■ Avoid guilt by association (33%)

“Because I don’t want to be associated with these practices in any way”; “Because, even if

70% we do not reach a majority and the resolution is rejected, I’ll have done the right thing”

60% ■ Optimize returns on investments (20%)

50% ”To avoid losing money if the controversies turn into a crisis for the company”

40% 85%

30% Take NB: the total is not 100% due to empty fields / no response

20% Action

10%

0%

Take Action Vote for firing top Vote in favour of Sell some shares Sell all shares

manager resolutions to reform the

companies policy on the

mater

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Which product would you prefer?*

Assuming that it is recommended for reaching your financial objectives to invest a part of your savings in this category.

Pension Fund 30% 39% 10% 3% 17%

The following products (see table) are equal from a financial risk and returns perspective, only the environmental characteristics are different.

Equity Fund 34% 29% 26% 2% 8%

Real Estate Fund 41% 30% 17% 1% 11%

Brown portfolio Green portfolio with Best-in-class

with proven impact no proven impact strategy with no None of the above

proven impact I don’t understand

20% you accept a -5% trade off on your total pension to integrate your ESG objectives?*

Would

18%

Percentage of 64%

respondents

16% accept the suggested -5% trade-off

14%

12%

10% 6% reject the suggested

15% reject the suggested trade-off trade off and then accept

8% but then accept a lower trade-off a higher impact

6%

4%

2%

0%

Not interested in 0-1% 2-3% 4-5% 5-6% >10%

the first place

Percentage of trade-off accepted on the total amount of savings available at retirement age

*Surveys conducted on 4,000 German and French consumers 2Dii/Splendid research 2019. Upcoming publication Q1-2019

52 RESPONSIBLE MARKETING & DISTRIBUTION

Our actions on marketing and distribution aim to prevent mis-selling of unsuitable

financial products to consumers who want to have an environmental impact

Environmental impact assessment

Building on our research on methodologies, we support coalitions of investors, banks, and

fund managers in the assessment of the impact of their climate actions. In its first stage (Q1-

2 2020) the program focuses on assessing the results of engagement and voting activities.

The program will then be extended to other types of actions (divestment, sustainability

improvement loans, etc.)

Environmental impact claims review

Our legal team analyses the compliance of environmental claims made by fund managers,

investors and banks (see paper 1). The analysis includes a review of the claims and the

evidence available to substantiate the claims. The legal analysis is completed by testing the

interpretation of misleading claims through a consumer survey and interviews.

Mystery shopping visits

The purpose of mystery shopping visits is to assess the ability of financial advisors to comply

with general regulatory requirements and integrate non-financial objectives into the suitability

assessment test. Our visits are based on a protocol built in collaboration with supervisory

authorities. Our program targets the main distribution channels of retail investment products

in a country and include 50 to 100 visits per country/year. The output is a report assessing

the level of compliance (see paper 2 and 3) as well as short videos (actors performing)

illustrating good and bad practices.

Policy work: green labels

Our team supports the development of environmental labels on financial products, through

technical analysis, legal analysis, as well as market research on products, data and

consumer preferences. We notably contributed to the development of the TEEC label in

France and currently contribute to the work on the EU Ecolabel (see paper 4).

Policy work: greening tax incentives

In partnership with the French PM think tank, we have analyzed the effectiveness of current

tax breaks related to savings products and explored options to better align them with

environmental policy goals (see paper 5).

1 2 3 4 5

Publication Q1-2020 Publication Q2-2020

62 RESPONSIBLE MARKETING & DISTRIBUTION

How do French retail banks advise clients seeking environmental impact?

(mystery shopping visits in France*)

Spontaneously, it is part Only after heavy Never, even after heavy and

of the procedure and repeated signs repeated signs of interests

The financial advisor asks questions

Q3

about sustainability objectives

He/she admits that the product is He/she tries to convince the

In the absence of suitable product Yes not suitable but still tries to sell it client that the product is suitable

(i.e. associated with evidence of

environmental impact), the advisor

Q1

recommends to search elsewhere

Frequency of product-specific Impact claims compliance, Funds categorized based on

environmental impact claims* by type of regulatory criteria* the compliance of impact

Analysis of 250 funds available in Europe (in % of total AuM) claims* (in % of total AuM)

100% 80%

False claim 9%

80% 60%

60%

40%

40% Misleading

claim 58%

20% 20%

0% 0%

Ambiguous

SRI Green Green Deceptive Unclear Claims too 33%

claim

funds funds bonds claims claims broad

funds

Interpretation of false and misleading claims by consumers Survey of 2,000 French and Germans, 2019

“The Green Bond fund allows you to finance the “The Green Equity Fund allows investors to have a real impact on climate

energy transition. You assess your actual impact via change. The design of the fund aims at generating a real impact on the

the tons of CO2 avoided or reduced. The proceeds of environment and create solutions for climate change: For example, a 5

the bonds are earmarked to finance specific million Euro investment in the fund, for one year would reduce polluting

environmental projects with a positive emissions by 4,200 tons of CO2, which is equivalent to taking 1,900 cars off

environmental impact”. the road for a year. These figures are reported every year and audited.”

55% Mislead 68% Mislead 12%

13%

46% 43%

41% 45%

20% Other wrong product Nonsensical

14% answer Feel mislead

Right Don’t see the difference

31% product Right product

25% identified Blame themselves

identified

*Preliminary results based on a limited sample, before quality review and re-calibration of categories.

The final results will be published in Q1 2020.

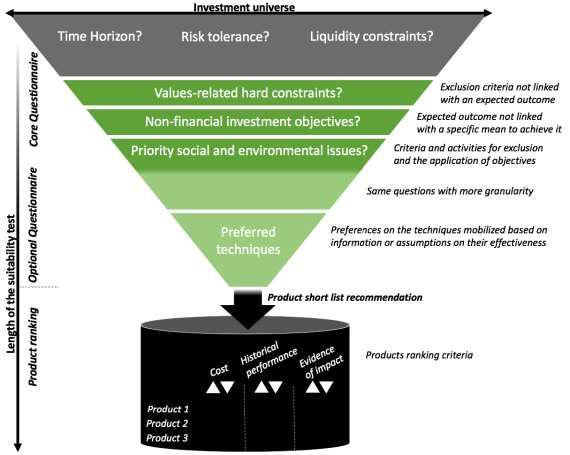

73 SUITABILITY ASSESSMENT

The framing of questions to consumers about their expectations, and the way their

answers are turned into criteria for recommending products is critical to prevent mis-

selling and greenwashing.

Policy work: reform of MIFID/IDD

Building on our findings from mystery shopping visits (see paper 2 page 6) and our legal

analysis, the EC High Level Expert Group (HLEG) recommended the integration of

sustainability into financial advice (see paper 1 below) and the EC decided to reform the

related regulation accordingly (MIFID/IDD). Our policy work on the topic focuses on: i)

supporting the adaptation of guidance (ESMA) and national regulations, ii) exporting the

reform to other jurisdictions, iii) exploring how the shareholder voting preferences of clients

and beneficiaries can be reflected into funds design and management (see 4 below).

Suitability questionnaire

Our research on consumer preferences (page 4) and the results of mystery shopping visits

(page 6) suggest that the design of an unbiased ‘suitability questionnaire’ is complex

technically and unlikely to take place spontaneously given the incentive financial institutions

have to frame the questions in a way that supports the sales of existing products. Our work in

this field aims at setting the bar in terms evidence-based questionnaire, building on the

outputs of consumer research, behavioral finance and methodological developments on

environmental impact measurement. Concretely, we produce suitability questionnaires that

can be used as default option by the industry and the ‘gold standard’ by regulators, as well

as guidance on how to design such questionnaires (see upcoming paper 3 below).

Product database

To help consumers and advisors identify suitable products for impact-seeking consumers,

we support the development of free and non-commercial databases comparing retail

products on financial and non-financial criteria, with a focus on environmental impact

measurement. Our first partners include InfluenceMap (see website 2 below), LITA (France),

the German and the French governments. The first products will be launched in Q1-2020

Online financial advisor

Our mid-term goal (2021-22) is to combine our questionnaire, our product database and an

asset-liability management calculator to provide a free, unbiased, non-commercial online

financial advisor. The product will be launched in partnership with governments.

1 2 3 4

Publication Q2-2020 Publication Q4-2019

83 SUITABILITY ASSESSMENT

Recommended steps to integrate non-financial objectives and preferences into the suitability

assessment questionnaire and process

We recommend to

disentangle:

• Values–related

hard constraints

(e.g. no exposure

to alcohol

production is a

prerequisite),

• Green

investment

objectives (e.g. the

product is

expected to have

an impact in the

real economy) and

related priorities,

• Potential

preferences for

certain techniques

(e.g. divestment) if

the client is

informed enough

to form such

preferences.

Consumers’ main objectives and suitable products based on survey results (France, Germany 2019)

ENVIRONMENTAL/SOCIAL IMPACT SYMBOLIC ACTIONS TO AVOID OPTIMIZE RETURNS NO INTEREST

OF THE INVESTMENT STRATEGY GUILT / DO NO HARM VIA ESG IN ESG

Investment strategies with Thematic funds, exclusion and norm- Products with Standard

environmental impact management based screening, best-in-class and ESG integration investment

engagement strategies focused on focus on products with

NO PRODUCT financially

social and environmental outcomes no significant

IDENTIFIED material issues ESG integration

94 ABOUT US

In order to avoid conflicts of interest, our approach is implemented on a non-commercial

basis. We partner with multiple stakeholders to help them integrate the outputs of our

research and development activities into their activities and products.

2° Investing initiative

The 2° Investing Initiative is a multi-stakeholder think tank working to align the financial sector with

sustainability policy goals. The organization is not-for-profit and non-commercial. It helps develop the

regulatory frameworks, performance metrics, data and tools to support this evolution.

The organization is composed of three not-for-profit entities incorporated in France, Germany and US.

Our +40 staff operates in Europe, North and South America and Japan.

Thanks to its EU-funded research programs, 2° Investing Initiative has introduced the climate scenario

analysis of investment and lending portfolios into regulatory frameworks (France, EU, California),

investors and banks practices (for more than 600 users and €60Tn of assets) and supervisory practices

(UK, EU, California, Japan).

2° Investing Initiative’s research on the suitability assessment test in Europe triggered, via the HLEG, the

reform of MIFID and IDD introduced by the EC regulatory package on sustainable finance.

About the program team

The above-described program on household savings mobilize experts from different fields including:

legal, regulatory, behavioral science, marketing, software and data engineering.

Lead Software & database development

Stan Dupre Klaus Hagedorn Nicola Koch Constanze Bayer

CEO Senior Analyst Project Manager Analyst

New York City Berlin Berlin Berlin

Legal & regulatory Consumer research & behavioral finance

Pablo Felmer Roa David Cooke Bo van Grindven, PhD Thierry Santacruz

Senior Legal Advisor Policy Manager Consultant Analyst

Barcelona Paris Utrecht Paris

105 PARTNERSHIPS

In order to avoid conflicts of interest, our approach is implemented on a non-commercial

basis. We partner with multiple stakeholders to help them integrate the outputs of our

research and development activities into their activities and products.

Supervisory authorities

Financial supervisors such as Market Authorities are in charge of ensuring consumer

protection, including the integrity of suitability assessments and fair competition. By sharing

our research findings we prevent an asymmetry of information with the finance sector on

consumer preferences. In parallel, we support the design of guidance and enforcement

mechanisms. Following informal collaboration with the European and German authorities, we

partnered with the French authorities on the full scope of the above described program for

the period 2020-2025.

Policy makers and standard setters

Our research has triggered the upcoming integration of sustainability into financial advice.

We continue to support the related regulation design. Our work also focuses on product

labelling and disclosure, through our involvement in related EU and French working groups.

Financial institutions

The program is relevant to financial institutions in their capacity as retail product

manufacturers (product design, marketing and substantiation of claims) and distributors

(design of the suitability assessment test, point-of-sale marketing, product selection).

Building on our existing memberships and partnerships with banks and investors on portfolio

climate analysis*, we have organized seminars and workshops to share our findings and

coordinate policy positions. Moving forward, we will develop bilateral partnerships to support

the implementation of the above-mentioned reforms.

Multi-stakeholder working groups

Given the novelty and complexity of the issues at stake, we believe that engagement

between supervisors, regulated entities, academia and other stakeholders (environmental

NGOs, consumer associations) is necessary to inform the development of best practices on

the various topics. We help initiate ad hoc working groups. Our first pilot took place in

Germany in 2018-19, the second will start in France in 2020.

Implementation partners in France

In France, our team has partnered with the

authorities and the industry association to

support the implementation of the above

described program. The activities have

started in 2019 for a period of 5 years.

2Dii designed the program and raised the

related funds for all partners (EU Life grant).

*Examples of partners include Axa, Aviva, Blackrock, Barclays, BBVA, BNP Paribas, BPCE, Citi, ING, KBC, SocGen, Santander, UBS, etc.

11Contact us at Retail@2Dii.org

Download our papers on 2Dii.org

A program supported by

LIFE IP grant AFFAPYou can also read