Regional and Local Governments (RLGs) Moody's Approach - JUNE, 2018 - salga

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Regional and Local Governments (RLGs) Moody’s Approach SALGA – Municipal Innovative Infrastructure Financing Conference JUNE, 2018

Agenda

1. Moody’s Sub-Sovereign Group

2. List of rated RLGs in South Africa

3. List of Metros and secondary cities

4. Moody’s RLGs Rating Approach

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 3

Moody’s Sub-Sovereign Group

Sub-Sovereign – A global presence

49 analysts/associates located in 17 offices, serving 44 countries

16 different nationalities speaking 17+ languages

USD 1.51 trillion rated debt

Stockholm

Moscow

Toronto London

Paris Prague

New York Frankfurt

Madrid Beijing

Milan

Tokyo

Shanghai

Mexico City

Sao Paulo

Johannesburg Sydney

Buenos Aires

Sources: CSS data, AWT, Moody’s Database Rated debt (excluding US)

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 5Rating Universe: A Wide Array of Public

Entities

Two big families: 337 RLGs, 162 GRIs

Regions

Provinces

RLGs States

337 Cities

Transportation

Higher Education

Water

Housing Association

GRIs Utilities

Healthcare

162

Specialized Lenders

Financial Institutions

Not for Profit

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 6RLG Ratings Universe by Geography

Credits spread over 44 countries

Australia

» Strong presence in Canada and Mexico,

South

and Asia America

W.Europe & CEE/CIS

Africa

Western

» Issuer ratings dominant vs. debt ratings,

Europe

capital mkt activity limited in many countries

» National Scale Ratings widely used in

Mexico, CEE/CIS, South Africa and Turkey

North » Africa coverage is limited to South Africa

America

Eastern

Europe

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 7List of rated RLGs in South Africa

South African Rated Sub-Sovereigns

(as at March 2018)

Outlook Global Scale National Scale Rating

METROPOLITAN MUNICIPALITIES

City of Cape Town Negative Baa3/P-3 Aaa.za/P1-za [1]

Ekurhuleni Metro Stable Baa3/P-3 Aaa.za/P-1.za [1]

Johannesburg Stable Baa3/P-3 Aa1.za/P-1.za [1]

Nelson Mandela Metro Stable Baa3 Aaa.za

City of Tshwane Stable Ba2/NP A1.za/ P-1.za

Mangaung Stable Ba2/NP A1.za/P-1.za

LOCAL MUNICIPALITIES

Rustenburg Stable Ba2 A1.za

Bergrivier Stable Ba3/NP Baa1.za/P-2.za

Breede Valley Stable Ba2/NP A2.za/P-1.za

City of Umhlathuze Stable Ba2 A1.za

DISTRICT MUNICIPALITIES

Amathole District Stable Ba1 A2.za

GOVERNMENT RELATED ISSUERS (GRI’S)

City Power Johannesburg Stable Baa3 Aa1.za

East Rand Water Care Company (ERWAT) Stable Ba1 Aa3.za

Ratings Under

South African National Roads (SANRAL) Ba1/NP Aa3.za/P-1.za

Review

Notes: [1] Issuer and debt ratings.

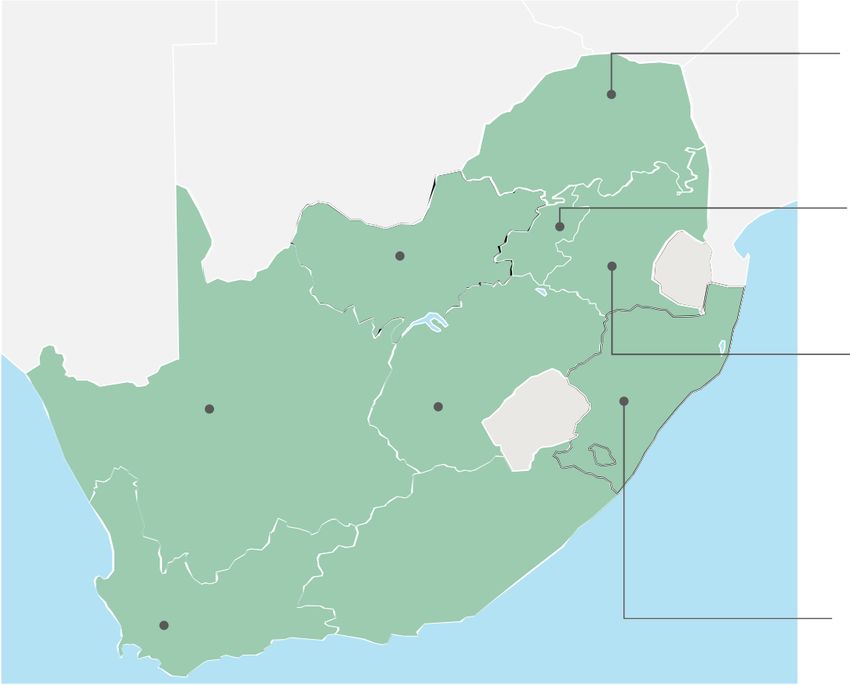

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 9List of Metros and Secondary Cities

Metropolitan municipalities have large

revenue base

Total Revenue - 2017 Total Revenue - 2017

Metropolitan Municipalities Province (ZAR million) ($ million)

Buffalo City Metropolitan Municipality Easter Cape 6,276 483

City of Cape Town Western Cape 38,404 2,954

City of Ekurhuleni Gauteng 31,457 2,420

City of Johannesburg Gauteng 45,422 3,494

City of Tshwane Gauteng 30,401 2,339

Ethekwini Metropolitan Municipality Kwazulu Natal 33,539 2,580

Mangaung Metropolitan Municipality Free State 5,767 444

Nelson Mandela Bay Metropolitan Municipality Easter Cape 9,802 754

Source: National Treasury & issuers’ financials

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 11Metros’ population growth rate from

2011 – 2016 continue to exert spending

pressure

FREE STATE: GAUTENG:

Mangaung 2% Ekurhuleni 6%

Johannesburg 12%

Tshwane 12%

KWAZULU NATAL:

eThekwini 6%

EASTERN CAPE:

WESTERN CAPE:

Buffalo City 7%

Cape Town 7% Nelson Mandela

Bay 10%

Source: Statistics South Africa

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 12Secondary cities largely depend on

transfers for capital infrastructure

Total revenue - 2017 Total revenue- 2017

Secondary cities Province (ZAR million) ($ million)

Emfuleni Gauteng 5,584 429

Msunduzi Kwazulu Natal 4,576 352

Rustenburg North West 4,277 329

Polokwane Limpopo 3,114 240

uMhlathuze Kwazulu Natal 3,007 231

Mogale City Gauteng 2,585 199

Mbombela Mpumalanga 2,587 199

Emalahleni Mpumalanga 2,470 190

Matlosana North West 2,402 185

Matjhabeng Free State 2,254 173

Sol Plaatje Northern Cape 1,905 147

Madibeng North West 1,879 145

Drakenstein Western Cape 1,883 145

Newcastle Kwazulu Natal 1,750 135

Govan Mbeki Mpumalanga 1,665 128

George Western Cape 1,643 126

Steve Tshwete Mpumalanga 1,449 111

Stellenbosch Western Cape 1,519 117

Tlokwe North West (2016 AFS) 1,270 98

Source: National Treasury, issuers’ financials

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 13Population growth rate from 2011 –

2016 also exert spending pressure for

secondary cities

NORTH-WEST: LIMPOPO:

Rustenburg 14%

Polokwane 12%

Matlosana 5%

Tlokwe 10% GAUTENG:

Madibeng 12% Emfuleni 2%

Mogale City 6%

NORTHERN CAPE:

MPUMALANGA:

Sol Plaatje 3%

Mbombela 6%

Emalahleni 15%

WESTERN CAPE:

Drakenstein 12% Govan Mbeki 15%

George 7% Steve Tshwete 21%

Stellenbosch 11% KWAZULU NATAL:

Msunduzi 10%

FREE STATE: uMhlathuze 11%

Matjhabeng 6% Newcastle 7%

Source: Statistics South Africa

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 14Moody’s RLGs Rating Approach

RLGs: The Approach

RLGs are “enduringly linked” to their respective sovereign.

1 The sovereign’s credit quality will to some extent anchor the

credit quality of the RLG

Sovereign and Sub-Sovereigns are likely to be affected by

2 similar external factors. Sub-Sovereigns do not posses

special autonomous characteristics that insulate them from

sovereign-related risks

Sub-sovereign issuers tend to be highly exposed to the same

3 macroeconomic and financial sectors pressures which affect

the central government.

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 16How sovereign credit quality affects

other ratings

Slower economy

Slowing or contracting economic Austerity measures

activity can have wide-ranging

consequences Defensive sovereign actions may include

austerity measures which reduce or delay

government payments

Financing costs

Liquidity constraints and higher Exchange and interest rates

financing costs resulting from Unfavourable changes to exchange rates, interest rates

diminished investor confidence or price levels

Regulation Political uncertainty

Government interference or

Increased risk of political uncertainty and

changes in regulation

civil or labour unrest

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 17Rating Approach:

BCA and Extraordinary Support

F1. Economic Fundamentals

F2. Institutional Framework

Operating Environment Extraordinary

F3. Financial performance & Debt profile (typically reflected in

Support Range

F4. Governance & Management Sovereign bond rating)

Assessment of Assessment of

idiosyncratic risk systemic risk

Baseline Credit Assessment

RLG Rating

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 18Assessing Idiosyncratic Risk

Financial performance Governance

Economic Institutional

& &

Strength Strength Debt profile Management

Idiosyncratic Risk

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 19Assessing Idiosyncratic Risk

Financial performance Governance

Economic Institutional

& &

Strength Strength

Debt profile Management

Why it matters

An RLG's ability to service its debt depends on, among other factors, the sufficiency

and reliability of its future revenues. Relative economic performance will likely impact

an RLG’s ability to generate own-source revenues and its dependence on fiscal

transfers. In general, a relatively wealthier region would have a more productive tax

base and could therefore generate necessary own-source revenues more readily.

How it’s measured in the scorecard

» Regional GDP per capita as a percentage of national GDP per capita

» Economic volatility is assessed by evaluating an RLG’s economic diversity

Idiosyncratic Risk

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 20Assessing Idiosyncratic Risk

Financial performance Governance

Economic Institutional

& &

Strength Strength

Debt profile Management

Why it matters

The institutional framework encompasses the arrangements that determine intergovernmental

relations and shape RLG powers and responsibilities. This factor addresses the RLG's public-

policy responsibilities and the adequacy of its fiscal powers to meet them. It also addresses

the way in which these responsibilities and powers may be altered, whether by a higher tier

entity or by the RLG itself.

How it’s measured in the scorecard

» We gauge predictability, stability and responsiveness by assessing whether and how RLG

powers and responsibilities may be altered in response to changing circumstances.

» We gauge financial flexibility by evaluating own-source revenue flexibility and the RLG

sector's spending flexibility

Idiosyncratic Risk

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 21Assessing Idiosyncratic Risk

Financial performance Governance

Economic Institutional

& &

Strength Strength

Debt profile Management

Why it matters

Financial performance is the product of accumulated decisions of policy makers regarding an

RLG’s revenue structure and expenditure base, as well as the economic environment in

which the government operates. The government's debt profile includes the amount of debt,

the burden it poses, its structure and composition, as well as past trends and future

borrowing needs – all important determinants of credit quality.

How it’s measured in the scorecard

» Ratio of gross operating balance to operating revenue

» Ratio of interest payments to operating revenue

» Cash and liquidity management

» Debt burden

» Debt structure

Idiosyncratic Risk

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 22Assessing Idiosyncratic Risk

Financial performance Governance

Economic Institutional

& &

Strength Strength

Debt profile Management

Why it matters

Our assessment of a government's credit standing includes an assessment of the

quality of financial decision-making and execution with a review of the government

structure, financial management practices and the transparency of financial

disclosures.

How it’s measured in the scorecard

We evaluate each RLG’s:

» Risk controls and financial management practices.

» Investment and debt management policies and practices

» Transparency and disclosure practices

Idiosyncratic Risk

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 23Assessing Extraordinary Support

Baseline Credit Assessment Extraordinary Support

Extraordinary support is defined as the likelihood that a higher-tier government would

aid an RLG in the event that it faced acute liquidity stress or act in such as way as to

help avoid a default of its debt obligations. Support could take different forms, for

example, a one-time cash infusion or any action facilitating negotiations with lenders

that enhances access to interim financing for the RLG.

RLG Rating

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 24Introduction of Ranges for Support

» Consistent with the support ranges for government-related issuers, we

have refined our support classifications into five ranges: low (0% -

30%), moderate (31% - 50%), strong (51% - 70%), high (71% - 90%)

and very high (91% - 100%).

» To arrive at a decision concerning the degree of support, we consider

factors within three main areas:

– Institutional framework;

– Historical behaviour; and

– Individual characteristics.

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 25Summary Idiosyncratic Risk Scorecard

and Weights

Scorecard Sub-factor weighting Factor weighting

1. Economic fundamentals 20%

1.1 Economic strength 70%

1.2 Economic volatility 30%

2. Institutional framework 20%

2.1 Legislative background 50%

2.2 Financial flexibility 50%

3. Financial performance and debt profile 30%

3.1 Operating margin 12.5%

3.2 Interest burden 12.5%

3.3 Liquidity 25%

3.4 Debt burden 25%

3.5. Debt structure 25%

4. Governance and management MAX 30%

4.1 Risk controls and financial management

4.2 Investment and debt management

4.3 Transparency and disclosure

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 26Rating process: in five steps to the first

time rating

Moody’s provides agenda and

1. Informal talk with 2. Formalisation of the information requirements for

face-to-face meeting

Moody’s rating mandate

3. Formal rating meeting

with Moody’s

5. Issuer notification on 4. Analysis and rating

assigned rating and decision on the basis of Feedback in advance of

potential publication the committee vote the Rating Committee

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 27Daniel Mazibuko Sebastien Hay Mauro Crisafulli

Associate Lead Analyst Senior Vice President / Manager Associate Managing Director

+271.1217.5481 +349.1768.8222 +3902.9148.1105

daniel.mazibuko@moodys.com sebastien.hay@moodys.com mauro.crisafulli@moodys.com

moodys.comThis publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action

information and rating history.

© 2018 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors

affiliates (collectively, “MOODY’S”). All rights reserved. and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity,

including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that,

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control

ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from

COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE or in connection with the information contained herein or the use of or inability to use any such information.

MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT

COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT

AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS,

ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER

RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS

OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-

BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”),

ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes

INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of

DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees

NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to

INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that

MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have

WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at

CONSIDERATION FOR PURCHASE, HOLDING, OR SALE. www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder

Affiliation Policy.”

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian

INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL

MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document

IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act

2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent

COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section

REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt

OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail

OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN investors. It would be reckless and inappropriate for retail investors to use MOODY’S credit ratings or publications

CONSENT. when making an investment decision. If in doubt you should contact your financial or other professional adviser.

CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A

BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of

WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK. Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of

MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are

Because of the possibility of human or mechanical error as well as other factors, however, all information contained Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and,

herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are

information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA

reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and Commissioner (Ratings) No. 2 and 3 respectively.

cannot in every instance independently verify or validate information received in the rating process or in preparing

the Moody’s publications. MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and

municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and

and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

damages whatsoever arising from or in connection with the information contained herein or the use of or inability to

use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to:

(a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial

instrument is not the subject of a particular credit rating assigned

by MOODY’S.

Regional and Local Governments (RLGs) Moody’s Approach, June 2018 29You can also read