Sustainable Finance Policy Engagement - An Analysis of Lobbying on EU Sustainable Finance Policy September 2020 - Politico.eu

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Sustainable Finance Policy Engagement An Analysis of Lobbying on EU Sustainable Finance Policy September 2020

Sustainable Finance Policy Engagement An Analysis of Lobbying on EU Sustainable Finance Policy September 2020 Table of Contents Executive Summary 2 Glossary 4 Introduction 5 Methodology 7 Results 9 Ranking Tables 21 Sustainable Finance Policy Engagement. September 2020 1

Executive Summary

This research has mapped out intensive lobbying on European sustainable finance policy, led by industry

groups representing the finance and corporate (real economy) sectors. Whilst a small number of financial

institutions have pushed for ambitious policy, the majority have remained silent or stated only high-level

support. Meanwhile, all but one of the 20 powerful industry associations analyzed have lobbied to dilute

and delay key regulations designed to align Europe's financial system with the Paris Agreement.

The lobbying comes at a critical moment with the European Commission currently deciding a Renewed

Sustainable Finance Strategy, considering both the European Green Deal and the need to recover from the

impact of COVID-19. Having consulted on possible next steps over the summer, a proposal is expected

from the Department for Financial Stability and Capital Markets (DG FISMA) in the fourth quarter of 2020.

This will build on the current EU's Action Plan on Sustainable Finance, originally launched in 2018, to

deliver on a High-Level Expert Group on Sustainable Finance (HLEG) recommendation for “no less than a

transformation of the entire financial system”.

InfluenceMap's research covers 75 financial companies belonging to 63 of the largest financial institutions

in Europe, 12 finance sector industry associations and 8 corporate industry associations. The methodology

drew on InfluenceMap's established methodology for assessing corporate influence on key policy areas,

scoring over 2000 evidence pieces across the 83 entities involved to derive metrics indicative of policy

engagement behavior towards sustainable finance policy. InfluenceMap consulted extensively with these

industry groups and individual financial institutions on the methodology and their scores prior to release.

BNP Paribas, Aviva and Groupe BPCE stand out as being actively engaged in promoting progressive

sustainable finance policy. However, there is also a small group of individual financial institutions including

BlackRock, BNY Mellon, Invesco and UBS that appear to be resistant towards stringent regulation.

The quadrant chart below plots the results of InfluenceMap's analysis for the financial institutions and

industry associations included in the analysis. Engagement Intensity refers to how actively the entity is

engaging, while Organization Score measures the degree of support/opposition to policy.

Most financial institutions (bottom-right quadrant, in blue) have shown caution and, despite having made

some high-level supportive comments, have tended not to engage in a detailed or intensive manner. A

small number of financial institutions (top-right quadrant, blue) have been actively engaged in promoting

sustainable finance policy. A few financial institutions (center-left of the diagram, blue) appear to be more

cautious about sustainable finance policy. See section on Key Finding 1 for more detail.

Finance industry associations (center-left of the diagram, yellow) appear to have positions that are

misaligned from most of their members and have tended to state high-level support for policies whilst

lobbying on detailed regulation to weaken their stringency. See section on Key Finding 2 for more detail.

The research highlights the importance for active progressive lobbying by finance, with a battle emerging

with corporate industry associations (bottom-left quadrant, green) that have been highly engaged on

certain strands of sustainable finance regulation and appear to be a significant barrier to progressive

sustainable finance policy. See section on Key Finding 3 for more detail.

Sustainable Finance Policy Engagement. September 2020 2

The chart below plots the results of InfluenceMap's analysis for the financial institutions and industry associations included in the analysis. Engagement Intensity refers to how actively the entity is engaging, while Organization Score measures the degree of support/opposition to policy. Sustainable Finance Policy Engagement. September 2020 3

Glossary AFME Association for Financial Markets in Europe AIMA Alternative Investment Management Association CEFIC European Chemical Industry Council EBF European Banking Federation EFAMA European Fund and Asset Management Association HLEG High-Level Expert Group IDD Insurance Distribution Directive IIGCC The Institutional Investors Group on Climate Change IOGP International Association of Oil & Gas Producers MiFID Markets in Financial Instruments Directive SFDR Regulation on sustainability-related disclosures in the financial services sector TEG Technical Expert Group Sustainable Finance Policy Engagement. September 2020 4

Introduction

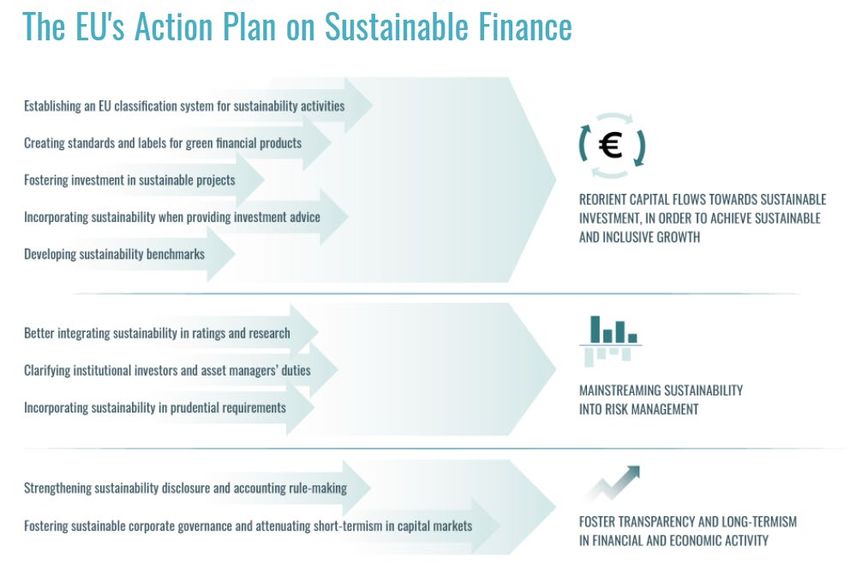

The EU's Sustainable Finance Action Plan

Launched in March 2018, the EU's Action Plan on Sustainable Finance is seen as critically important in

achieving the EU's climate goals, through reorienting capital flows towards a more sustainable economy and

mainstreaming sustainability issues into financial decision-making. The Action Plan followed the

recommendations of the High-Level Expert Group on Sustainable Finance (HLEG) which highlighted the need

for “no less than a transformation of the entire financial system” to deal with the challenges raised by climate

change.

Since 2018, the European Commission has made progress on many of the policies under the Action Plan,

visualized below. The Action Plan includes new regulations and directives as well as amendments to existing

legislation. Although the framework legislation is now in place for some of the policies, such as the taxonomy,

climate benchmarks and investors' ESG disclosure, in most cases the technical details are still under

consideration. Other policy areas, such as incorporating sustainability into prudential requirements and

investors' duty to integrate ESG are yet to be meaningfully progressed.

Source: European Commission

The Commission also set up the Technical Expert Group on Sustainable Finance (TEG) to assist in developing a

number of these policies, including the taxonomy, an EU Green Bond Standard and climate benchmarks.

In 2020, in light of both the agreement on the European Green Deal and the need to recover from the impact

of COVID-19, the Commission announced a Renewed Sustainable Finance Strategy which will build on the

current workstream and is expected to be launched in the fourth quarter of 2020.

Sustainable Finance Policy Engagement. September 2020 5

Influencing of the EU’s Sustainable Finance Plan Research has shown the scale of lobbying apparatus the financial sector has in play in Europe. In 2012, UK- based investigative researchers The Bureau of Investigative Journalism found 129 finance sector organizations actively engaged in the UK policymaking processes. In 2014, Corporate European Observatory (CEO) found that the post-financial-crisis EU regulatory framework had been lobbied by over 700 organizations linked to the financial sector. Subsequent research by CEO has tracked a string of European policy outcomes that have been shaped by EU financial industry association lobbying. InfluenceMap's research on the lobbying of the EU’s Sustainable Finance Taxonomy, published in December 2019, found intense lobbying activity on this key policy by both the financial and corporate sectors, including engagement from the fossil fuel value chain. Although many important aspects of the taxonomy were maintained against external pressure (at least partially due to positive lobbying forces), coverage of environmentally damaging activities was excluded due to significant negative lobbying. Lobbying to weaken the technical thresholds to be defined 'green' under the taxonomy is still ongoing. Based on existing studies of finance sector lobbying, and InfluenceMap's research on the taxonomy, finance and corporate sector influencing is likely to play a crucial role in determining the success of the wider action plan and other sustainable finance policies across Europe. In 2015, InfluenceMap established a systematic platform for tracking, assessing and scoring corporate and industry engagement on climate change policy. In 2019-2020, InfluenceMap expanded this platform to assess the financial sector’s influence over emerging sustainable finance policy streams. This report is companied by the release of an online platform detailing the positions and engagement of 63 of the largest financial institutions in Europe, along with their key industry associations and relevant corporate industry associations. Many of the links in this report lead to evidence pieces stored in InfluenceMap’s online platform. This research covers the period from 2017 to July 2020, following the High-Level Expert Group on Sustainable Finance and the first stage of the EU's Action Plan on Sustainable Finance. Although most of the engagement found focuses on the EU's Action Plan, this analysis also contains engagement on other relevant developments in Europe, including the UK Department for Work and Pension's update to trustees' investment duties and the development of the UK's 2020 Stewardship Code. InfluenceMap's platform provides a snapshot of policy engagement so far and will be continually updated to cover future engagement, including on the EU's Renewed Strategy on Sustainable Finance. Additionally, InfluenceMap plans to expand this analysis to cover relevant sustainable finance policy streams globally. Sustainable Finance Policy Engagement. September 2020 6

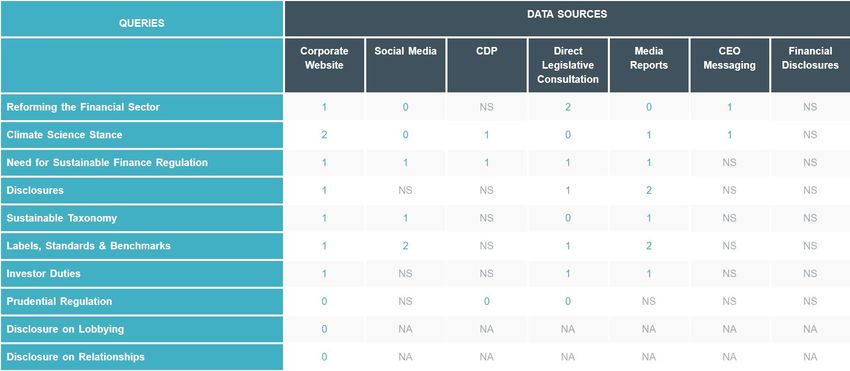

Methodology InfluenceMap’s methodology covers seven publicly available data sources, searching for evidence of engagement and corporate positioning since 2017. To determine the policy issues within the scope of the analysis, InfluenceMap breaks down sustainable finance policy engagement into a series of subcategories, or 'queries'. These are designed to cover high-level issues relating to the importance of sustainable finance, as well as more specific areas of sustainable finance policy making. InfluenceMap’s research process searches for evidence of an organization's engagement with each sustainable finance policy issue, across each of the data sources. This process can generate hundreds of evidence pieces which are stored in InfluenceMap’s data-content management system, shown in the image below. InfluenceMap's scoring process is policy neutral. It does not assess the quality of governmental policy but rather the positions of companies and industry groups relative to this policy. This is achieved by using the statements and ambitions of government-mandated bodies tasked to propose or implement sustainable finance policy as the benchmarks against which corporate and industry association policy positions are scored. For this analysis, the recommendations of the European Commission’s High-Level Expert Group and its Action Plan on Sustainable Finance were relied on heavily as benchmarks. This was supplemented in places with the statements and recommendations of UN-backed scientific enquiry, such as the findings of the Intergovernmental Panel on Climate Change (IPCC). InfluenceMap recognizes that while some areas of EU sustainable finance policy are well-developed, others are less so. This is the case for integrating ESG into prudential regulation, for example. InfluenceMap has therefore taken a cautious approach to benchmarking positions on this policy stream. While InfluenceMap’s system continues to search for and log evidence of engagement with ESG integration with prudential regulation, this evidence is not currently scored and will therefore not contribute to the overall analysis of an organization. As this policy stream develops, InfluenceMap will update its analysis. Scored evidence is coded by InfluenceMap as: ‘strongly supporting’, ‘supporting’, ‘no position/mixed position’, ‘not supporting/supporting with exceptions’, or ‘opposing’ with reference to the benchmarks explained above. These categories correspond to a numerical five-point scale between +2 and -2, where +2 indicates strong Sustainable Finance Policy Engagement. September 2020 7

support and -2 indicates opposition. InfluenceMap’s data-content management system then calculates four

core metrics from the scored evidence with weightings to factor in the relative importance of the different

data sources and queries. These metrics are:

Organization Score: A measure of an organization’s engagement with policy. Above 75 indicates support,

below 50 indicates increasing opposition towards 0.

Relationship Score: A measure of a financial institution’s industry association's sustainable finance policy

engagement. Above 75 indicates broad support, below 50 indicates increasing opposition towards 0

(financial institutions only).

Performance Band: A full measure of a financial institution's sustainable finance policy engagement

accounting for both its and its own industry associations' activity on an A through to F scale. For industry

associations, the performance band is based on the organization score only.

Engagement Intensity: Describes the level of engagement on sustainable finance policy, whether positive

or negative. Above 12 indicates active engagement, above 25 indicates highly active or strategic

engagement. In this research, financial institutions with an engagement below 8 were excluded from

most of the analysis as a clear position could not be determined.

This methodology is closely based on InfluenceMap’s existing methodology for assessing lobbying on climate

change policy, the results of which are used by numerous partners including the Climate Action 100+ investor

engagement process.

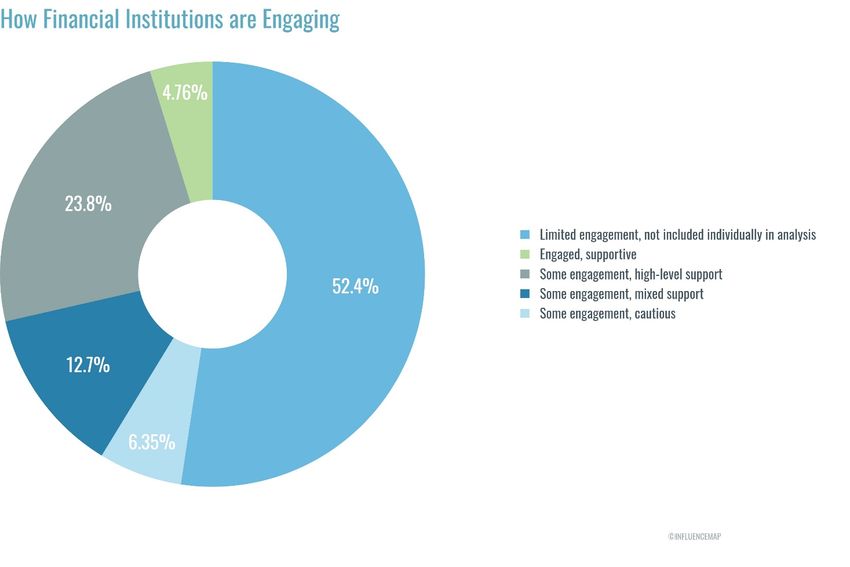

Sustainable Finance Policy Engagement. September 2020 8Results Key Finding 1: Most financial institutions are not strategically engaged Individual financial institutions mostly limit their support to top line statements Most financial institutions do not appear to be strategically engaged on sustainable finance policy, keeping largely to high-level statements in their own policy engagement and communications. More than 50% of the financial institutions researched have had such limited engagement that a clear position on sustainable finance policy could not be ascertained. These financial institutions are therefore not given scores and do not feature at an individual level in the remainder of the analysis. The individual scores for the 30 financial institutions who do have at least some significant policy engagement can be found in the ranking tables at the end of this report, with links to their profiles in InfluenceMap's online platform. Although most financial institutions have been enthusiastic in their support for the Paris Agreement and the need to scale up green investments, they appear to be reluctant to discuss curtailing damaging activities. Of more than 500 comments InfluenceMap found relating to action on climate change, only 3% referred to the need to reduce finance to environmentally harmful activities. Sustainable Finance Policy Engagement. September 2020 9

A small number of financial institutions have actively supported progressive sustainable

finance policy

BNP Paribas, Aviva and Groupe BPCE (primarily through subsidiaries Mirova and Natixis) stand out as being

very positively engaged on sustainable finance policy, as seen in the quadrant diagram. A larger group have

taken similarly supportive positions but do not appear to be as strategically engaged. This includes Legal &

General, who rank at the top of the overall scoring (see ranking tables) and have been engaged on UK policy

but do not appear to be as engaged as the leading three financial institutions on EU policy, where the majority

of evidence has been found. Other very supportive financial institutions include Nordea, Rabobank, Unipol and

Aegon.

The three leading financial institutions have all been consistent in their support for key sustainable finance

policies and have gone beyond high-level supportive statements to engage on regulations in detail. All three

have been members of one of the European Commission's expert groups - representatives of Aviva Investors

and Mirova were on the HLEG and representatives of BNP Paribas Asset Management and Mirova were on the

TEG. All three are also active in promoting and supporting policies in the media. The table below provides

some examples of engagement from leading financial institutions. To view all evidence for the financial

institutions, follow the links in the ranking tables to the profiles on InfluenceMap's online platform.

Based on their own individual policy engagement as financial institutions, BNP Paribas, Aviva, and Groupe BPCE

stand out as being both highly active and highly positive (all scoring over 80 on a 0 to 100 scale) on ambitious

sustainable finance policy for Europe. Under InfluenceMap's scoring system, their overall Performance Bands

are lower due to their memberships in negatively positioned industry associations which appear to be

misaligned with these financial institutions' sustainable finance policy positions.

Financial Institution Examples of engagement

Advocated for regulation on sustainable finance since at least 2014,

regularly putting out position papers with policy suggestions, many

of which have since been taken up by the European Commission

Vocal in its support for clarifying that fiduciary duty should cover

ESG issues and for policies to mandate engagement

with clients and beneficiaries about their ESG preferences. Aviva

further advocated for ambitious policy in this area in consultation

Performance

B- responses to the European Commission and the UK's Department for

Band

Work and Pensions in 2018

Organization Supportive of the creation of an EU Green Bond Standard,

84

Score advocating for a stringent approach to verification and suggesting

Engagement that policymakers should "expedite plans"

35

Intensity

Sustainable Finance Policy Engagement. September 2020 10 Mirova and Natixis have been particularly engaged in promoting the

taxonomy, with Mirova supporting the policy in newsletters,

on social media, and in consultations. Natixis has also supported the

policy on its website, in consultations and in media interviews,

including clear support for rigorous science-based criteria and

support for the expansion of the taxonomy to cover environmentally

harmful activities

Actively supporting incorporating ESG factors into fiduciary duty and

Performance

C+ has strongly supported related policies including the investors'

Band

disclosures regulation, on social media and in interviews, and the

Organization integration of ESG preferences in the advice investment firms give to

82

Score clients, in consultation responses

Engagement

40

Intensity

BNP Paribas Asset Management has been actively engaged on

promoting the taxonomy on its website, in social media posts

and media interviews. According to minutes accessed through a

Freedom of Information request, BNP Paribas advocated for a

rigorous science-based taxonomy in a meeting with the European

Commission, expressing concern that a Member-State-based expert

group could open the taxonomy to undue political influence

Performance BNP Paribas Asset Management has supported clarifying investor

C+ duties to include ESG issues and has also strongly advocated for

Band

policies which would implement this including ESG investor

Organization

81 disclosure and integrating ESG preferences into suitability

Score

assessments

Engagement

40

Intensity

A small number of financial institutions appear to have pushed for less stringent

regulatory intervention

A few financial institutions appear to be more resistant towards sustainable finance regulation and have

pushed back against more stringent requirements. This includes BlackRock, Invesco, UBS and BNY Mellon.

These groups have tended towards arguing in favor of policy focused on transparency rather than regulatory

mandates for the financial sector. The positions of these financial institutions most closely resemble the

positions of finance sector industry associations, discussed in the next section. Within this group, BlackRock

appears to be the most strategically engaged.

The table below provides some examples of engagement from these more skeptical financial institutions. To

view all evidence for the financial institutions, follow the links in the ranking tables to the profiles on

InfluenceMap's online platform.

Sustainable Finance Policy Engagement. September 2020 11Financial Institution Examples of engagement

Stated broad support for the taxonomy whilst arguing for an less

rigorous approach based on facilitating investor choice over strict

science-based thresholds

Argued against the creation of green labels at the EU level in 2017

and since has pushed for a weaker approach to the EU's Ecolabel, for

example arguing in January 2019 for unambitious thresholds of 25%

green activities to be considered green at portfolio or company level

(this position was revised in May 2019 to 70%, in line with the EU

Joint Research Centre's suggested threshold)

Opposed updating fiduciary duties to include ESG issues in 2017 and

Performance since has argued for a weaker approach to related updates to MiFID

D

Band II to integrate ESG preferences into the advice investment firms give

Organization to clients and, in response to a Financial Conduct Authority

48 consultation on the UK's Stewardship Code, appeared to push for a

Score

Engagement definition of stewardship with less emphasis on long-term benefits

22 for society and economy

Intensity

UBS Asset Management appears to be cautious about stringent,

science-based regulatory intervention on sustainable

finance, emphasizing in a 2019 whitepaper that the EU's Sustainable

Finance Action Plan "must serve investors’ needs" and be

“compatible with clients’ investment objectives”.

Performance UBS Asset Management appears to support a less stringent

D approach to the EU's taxonomy, raising concerns that the taxonomy

Band

Organization was too narrow and possibly supporting the inclusion of certain oil

49 and gas activities in a green taxonomy

Score

Engagement

10

Intensity

In consultations in 2017-18, BNY Mellon appeared to take a

cautious positions on the taxonomy and green labelling and updates

Performance to investor duties

D More recently BNY Mellon has expressed more positive positions on

Band

Organization these policy streams in articles on its website but does not appear to

44 have continued to engage with policymakers through more recent

Score

consultations

Engagement

15

Intensity

Released a report with Danske Bank in 2018 which argued that

transparency and choice were more likely to achieve long-term

benefits than mandatory requirements

Commented on the taxonomy to argue that the proposed 'green'

thresholds were too stringent in a media article in 2019 and

in feedback to the European Commission in 2020

Performance In feedback to the TEG in 2019, supported the EU Green Bond

D

Band Standard with a number of exceptions including arguing against

Organization mandatory external review and alignment with the taxonomy and

44 argued against the TEG's proposed criteria for climate benchmarks,

Score

suggesting that minimum requirements should be "principles-based"

Engagement

15

Intensity

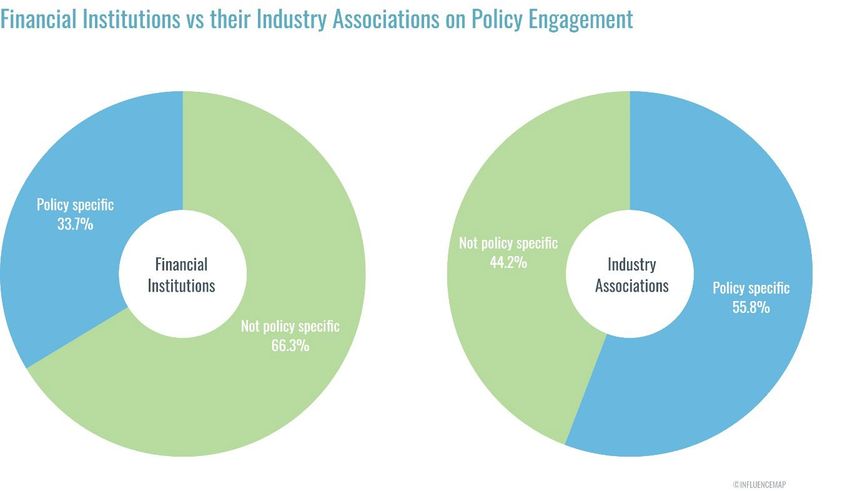

Sustainable Finance Policy Engagement. September 2020 12Key Finding 2: Finance industry associations are misaligned from their members Finance industry associations are more engaged on detailed regulation The finance industry associations considered in this analysis are: Alternative Investment Management Association (AIMA), Association for Financial Markets in Europe (AFME), European Federation of Insurance Intermediaries (BIPAR), European Fund and Asset Management Association (EFAMA), European Association of Co-operative Banks (EACB), European Banking Federation (EBF), Institutional Investors Group on Climate Change (IIGCC), Insurance Europe, Invest Europe, Managed Funds Association (MFA), PensionsEurope and The Institute of International Finance (IIF). In contrast to the financial institutions they represent, finance sector industry association engagement has focused on commenting on detailed regulation through position papers and consultation responses. More than 50% of engagement from finance industry associations focused on specific policies, compared to a third of engagement from financial institutions themselves. Finance industry associations are misaligned from most of their members Most finance industry associations have stated broad support for sustainable finance policy whilst lobbying to weaken the details of key regulatory strands. As a result, their organization scores are significantly lower than the financial institutions they represent. This analysis highlights at least two potential causes of this misalignment: Sustainable Finance Policy Engagement. September 2020 13

'Lowest common denominator': Industry associations may be adopting the most cautious positions

amongst their members when there are conflicting positions within the association

Public vs private positions of financial institutions: Financial institutions may be issuing positive high-level

statements on sustainable finance policy whilst channelling their concerns around the details of

regulations through finance industry associations, potentially to avoid public scrutiny of less positive

positions

61 of the 63 (97%) financial institutions analyzed in this research have links to industry associations that have

lobbied to weaken regulation. The following graphic represents the misalignment between finance industry

associations and most of their members, with the industry association's organization score indicated by a

yellow circle and its members by blue circles. The exception to the trend is IIGCC which, whilst having a very

similar set of members to other industry associations, appears to promote the most positive positions of its

membership.

Sustainable Finance Policy Engagement. September 2020 14Finance industry associations appear to be supportive of green finance incentives but

skeptical of the regulation of harmful activities

Finance industry associations have taken the most positive positions on policies which focus solely on scaling

up green finance, for example the EU Green Bond Standard. In line with the finding on high-level messaging

from financial institutions avoiding focus on the need to curtail damaging activities, the greatest pushback

from finance industry associations appears to be in areas that would either increase transparency of financing

of damaging activities (e.g. the expansion of the taxonomy to cover environmentally harmful activities) or

require consideration of ESG factors in mainstream financial decision-making (e.g. updating investor duties to

incorporate ESG issues). These are also the areas where the least progress has been made in the Action Plan.

The following table highlights some examples of pushback from finance industry associations. To see all

evidence for industry associations, follow the links in the ranking tables to the profiles on InfluenceMap's

online platform.

Policy Themes of Engagement Examples

AFME, EBF, EFAMA, Insurance Europe, PensionsEurope

have pushed back against the expansion of the taxonomy

to cover environmentally harmful activities

AFME, EBF, EFAMA, AIMA all argued for the taxonomy to

be restricted to financial products marketed as

Lobbying to restrict the sustainable, rather than applicable to all financial

scope of the taxonomy; products

arguing against a IIF, EFAMA, Invest Europe, AIMA have argued that

Taxonomy 1 rigorous approach to disclosure in line with the taxonomy should be voluntary

classification or to IIF, EACB, EBF have all suggested that a simpler or less

weaken specific 'green' rigorous approach to classification would be preferable to

thresholds the proposed science-based thresholds

AFME, EBF, EACB, EFAMA, IIF have argued for weaker

thresholds for specific economic activities to be

considered 'green', for example the relaxing of the

electricity generation threshold to accommodate

unabated natural gas

EFAMA has argued for weaker green criteria and weaker

exclusion thresholds for environmentally harmful

Lobbying for weaker activities

EU Ecolabel 'green' thresholds and EACB supported the Ecolabel with a number of exceptions

for Financial exclusion criteria based including arguing for some criteria to be weakened and

Products on expanding the suggesting that some of the compliance and verification

investment universe requirements were too onerous

Insurance Europe has argued that the criteria are too

stringent

Broad support but some Insurance Europe has supported the EU Green Bond

disagreement over Standard including legislation to introduce a centralized

EU Green

whether legislation to accreditation regime for external green bond verifiers

Bond

introduce a centralized EBF has supported the EU Green Bond Standard but not

Standard

accreditation scheme is an ESMA-led supervision of external review providers that

required would require a legislative approach

1 For more detail on lobbying on the taxonomy, please see InfluenceMap's December 2019 report The EU’s Sustainable Finance Taxonomy

Sustainable Finance Policy Engagement. September 2020 15 AFME argued for weaker requirements including

suggesting consideration of scope 3 emissions should be

Lobbying on exclusion

optional and supporting flexibility in choice of exclusion

thresholds for

Benchmarks criteria and supported weaker ESG disclosure for all

environmentally harmful

benchmarks

activities

EFAMA argued for weaker exclusion thresholds for fossil

fuels

EBF, PensionsEurope, BIPAR and AIMA have all argued for

the regulation to be restricted to financial products

marketed as sustainable, rather than apply to all financial

Lobbying to restrict the products

scope to products Insurance Europe, AFME, AIMA, EACB, EBF, EFAMA and

SFDR marketed as sustainable; PensionsEurope signed a joint letter calling for the

lobbying to delay timeline of the regulation to be changed over concerns

implementation the technical details would not be in place before the

regulation came into force

PensionsEurope pushed for a delay again in April 2020,

citing disruption caused by the COVID-19 pandemic

Updates to AFME, BIPAR, EFAMA, Invest Europe, AIMA have argued

MiFID II and for phrases such as "where relevant" and "if any" to be

IDD to Lobbying for weaker inserted into the regulation, reducing the stringency of

integrate ESG wording in the the requirement to take into account all clients' ESG

preferences regulation which would preferences when giving investment advice

into deprioritise ESG

suitability preferences

assessments

for clients

EFAMA, EACB, MFA, AIMA, Invest Europe have all opposed

the idea of updating the legal frameworks for investor

Clarifying Opposition to clarifying duties to incorporate ESG factors

investor investor duties regarding PensionsEurope opposed measures to incorporate ESG

duties 2 sustainability issues into the 'prudent person rule' in IORP II

2 Not a currently active policy area, although the above two regulations are relevant, but it is instructive to recognize that this has faced

significant opposition when proposed in the past. The Commission has indicated that it may be included in the Renewed Sustainable

Finance Strategy

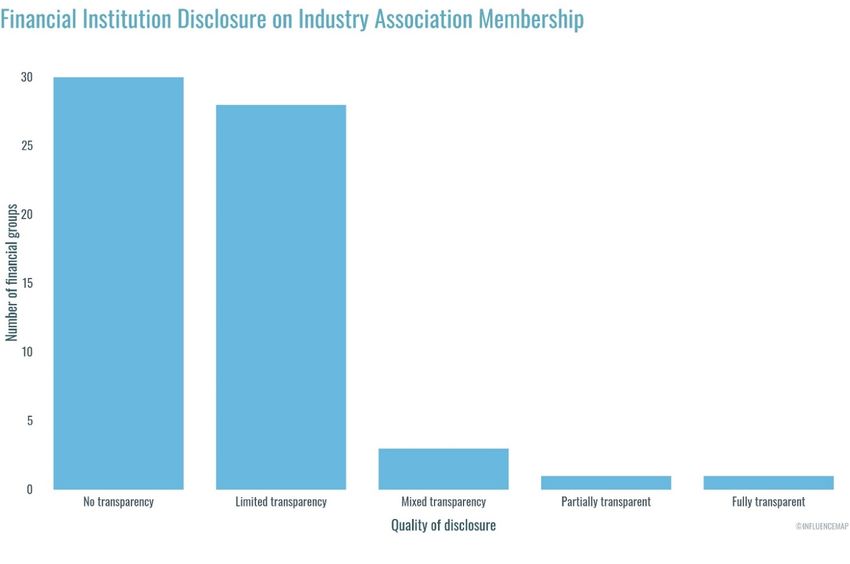

Sustainable Finance Policy Engagement. September 2020 16Disclosure of Indirect Policy Engagement Activities is Generally Poor

Investors are increasingly demanding that the companies they invest in disclose and address misalignments

between their lobbying practices and those of the industry associations through initiatives such as CERES and

CA100+. Despite this, most financial institutions analyzed have either no or limited transparency on their

indirect policy engagement through industry associations

Description Examples of disclosure

Has clearly described industry association memberships, with

Fully transparent positions taken by company within the industry associations and

ability to shape policy positions

Has disclosed memberships to third party organisations with

details of on these organisations sustainable finance lobbying

Partially transparent

positions and has indicated whether they are consistent with

own.

Has described how it is able to shape a industry association's

Mixed transparency policy positions on sustainable finance, but not what outcomes it

is seeking

Has disclosed memberships to third party organisations but has

Limited transparency not given details on the sustainable finance policy positions of

these organisations, or actions taken to address misalignments

InfluenceMap has not been able to find any disclosures from

No transparency company on their third-party memberships, or related

governance

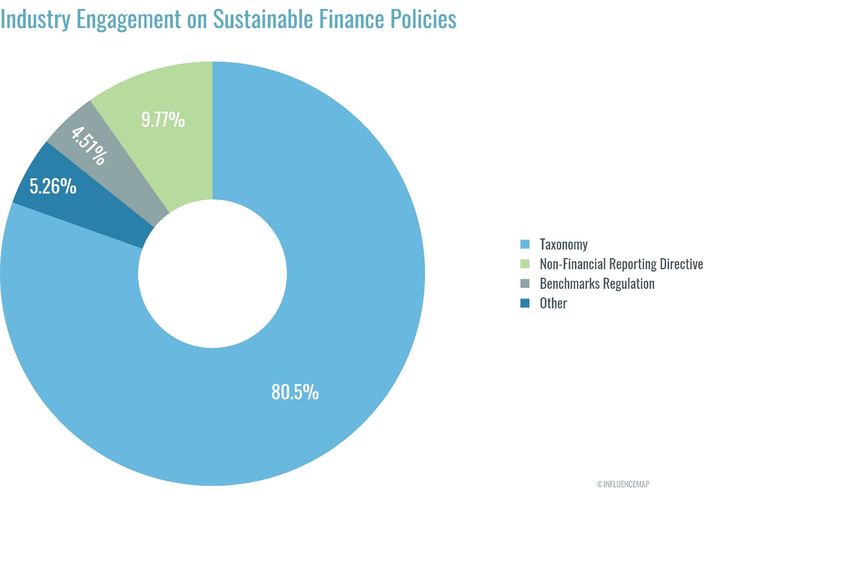

Sustainable Finance Policy Engagement. September 2020 17Key Finding 3: Corporate industry associations are an obstacle to progressive sustainable finance policy Corporate (real economy) industry associations have been highly engaged on some streams of sustainable finance policy The corporate (real economy) industry associations considered in this analysis are: BusinessEurope, Eurelectric, European Chemical Industry Council (CEFIC), European Steel Association (Eurofer), EuropeanIssuers, FORATOM, FuelsEurope and International Association of Oil and Gas Producers (IOGP). Industry associations representing the corporate sector have been highly engaged on certain sustainable finance policy streams that directly impact their activities and their engagement has been more overtly oppositional to progressive policy than that from financial institutions and finance industry associations. Over 80% of all engagement from corporate industry associations has focused on the taxonomy, reflecting the potential ramifications of this policy for powerful vested interests who have sought to either restrict the taxonomy's coverage of their activities or to ensure their inclusion in what is defined as 'green'. 3 3 For more detail on lobbying on the taxonomy, please see InfluenceMap's December 2019 report The EU’s Sustainable Finance Taxonomy Sustainable Finance Policy Engagement. September 2020 18

Groups Involved Theme of engagement Examples of engagement

BusinessEurope and EuropeanIssuers both argued for a

less stringent approach to determining what can be

considered 'green' under the taxonomy, opposed the

application of the taxonomy beyond products explicitly

marketed as sustainable, opposed the expansion of the

Lobbying to weaken the

Cross-sector taxonomy to cover environmentally harmful activities

framework of the

groups and opposed disclosure requirements for investee

taxonomy

companies.

BusinessEurope and EuropeanIssuers were reportedly

successful in blocking "any ambitious proposals" when

the taxonomy regulation was debated at the European

Parliament.

IOGP and FuelsEurope have argued for the threshold for

electricity generation to be weakened to accommodate

natural gas and for a more lenient approach to blended

fuels, in line with RED II.

Eurofer has pushed back against the use of strict

thresholds, arguing instead for a qualitative approach

based on relative improvement. Eurofer has argued

against the proposed used of EU ETS benchmarks for

steel production.

Lobbying to weaken

CEFIC has suggested that the thresholds proposed by

Sector-specific specific ‘green’

the TEG risk undermining transitional efforts and has

groups thresholds to include

argued for the reconsideration of plastics in the

sector’s activities

taxonomy based on their use in products that can

facilitate the transition to a low-carbon economy.

FORATOM pushed back against the initial exclusion of

nuclear energy by the TEG under the 'do no significant

harm' criteria.

Eurelectric called for weaker thresholds for electricity

generation to include natural gas, supported the

inclusion of nuclear energy and a more lenient

approach to bioenergy in line with RED II.

There is an emerging battle between the finance and corporate sectors on non-financial

reporting

With the upcoming revision of the EU's Non-Financial Reporting Directive (NFRD), corporate industry

associations are becoming increasingly engaged on this policy stream and have strongly contrasting demands

to the financial sector.

Parts of the financial sector were cautious on proposals for improved regulated corporate reporting when

responding to the 2019 TEG consultation on updating the non-binding guidelines on reporting climate-related

information. However, in the June 2020 consultation on the update to the NFRD, the financial sector was

almost universally supportive of increased ambition, at least partially reflecting the increased reporting

requirements on the sector brought on by the taxonomy and the SFDR which will require increased disclosure

from investee companies.

Sustainable Finance Policy Engagement. September 2020 19Issue Finance sector demands Corporate sector demands

The 'Joint Statement on the Revision of BusinessEurope has argued against

the Non-Financial Reporting Directive in expansion of the scope to a wider set of

the Context of Covid-19' 4 called for the companies including SMEs, non-listed

expansion of companies falling under companies and companies not established

Which companies the scope of the NFRD. AFME, in the EU that are listed in EU markets.

should disclose Insurance Europe, PensionsEurope, EuropeanIssuers has opposed expansion to

EACB, EFAMA and IIGCC have all argued SMEs but supported expansion to non-EU

for the expansion of applicability of the companies operating in the EU.

NFRD to SMEs (in a simplified manner)

and/or unlisted companies.

The Joint Statement called for minimum BusinessEurope has argued that the lack of

mandatory reporting requirements. comparability and relevance of non-financial

Standardization AFME, Insurance Europe, EBF, EFAMA, information is not a problem.

of non-financial IIGCC, PensionsEurope have all called BusinessEurope has opposed a possible

information and for at least some mandatory requirement for companies reporting under

how companies standardized reporting requirements the NFRD to disclose their materiality

determine what and materiality assessments. assessment process. EuropeanIssuers has

is 'material' also opposed this requirement. IOGP has

also called for corporates to be able to

decide what is 'material'.

AFME, Insurance Europe, EBF and IIGCC BusinessEurope has opposed greater

Assurance and

have all supported the need for greater assurance and verification of non-financial

verification of

assurance and verification of non- information. EuropeanIssuers, however,

non-financial

financial information. appears to be more supportive of phasing in

information

verification requirements.

AFME, EACB, EBF and EFAMA have all EuropeanIssuers has argued against the

Digitalization of emphasized the importance of the digitalization of ESG data on the basis that

non-financial digitalization of non-financial non-financial information is not "mature

information information. enough to be processed in an automated

way".

The Joint Statement supports the BusinessEurope has argued against possible

inclusion of material non-financial requirements to publish non-financial

Location of non- information in the management report. information in the management report.

financial EACB and PensionsEurope have also EuropeanIssuers has argued for flexibility

information suggested that ideally non-financial over the location of non-financial

information should be included in the information.

management report.

Some of the financial institutions have links to powerful cross-sector corporate industry

associations opposing sustainable finance policy

Some of the financial institutions analyzed are represented by EuropeanIssuers in their corporate functions.

This includes Aegon, BNP Paribas, Generali, Santander and Intesa Sanpaolo. The positions taken by

EuropeanIssuers are clearly highly misaligned from the individual positions of these financial institutions and

even from their finance sector industry associations.

4 The Joint Statement was issued by European Fund and Asset Management Association (EFAMA), Association of Chartered Certified

Accountants (ACCA), Accountancy Europe, Association of German Banks (BdB), Climate Disclosure Standards Board (CDSB), Frank Bold,

Institutional Investors Group on Climate Change (IIGCC), Schroders, ShareAction and World Wide Fund for Nature (WWF), with confirmed

support from BNP Paribas Asset Management and Candriam.

Sustainable Finance Policy Engagement. September 2020 20Ranking Tables

The metrics given in the following ranking tables are noted below.

Organization Score: A measure of an organization’s engagement with policy. Above 75 indicates support,

below 50 indicates increasing opposition towards 0.

Relationship Score: A measure of a financial institution’s industry association's sustainable finance policy

engagement. Above 75 indicates support, below 50 indicates increasing opposition towards 0 (financial

institutions only).

Performance Band: A full measure of a financial institution's sustainable finance policy engagement

accounting for both its and its own industry associations' activity on an A through to F scale. For industry

associations, the performance band is based on the organization score only. The performance bands are

measured against absolute benchmarks, as described in the methodology.

Engagement Intensity: Describes the level of engagement on sustainable finance policy, whether positive

or negative. Above 12 indicates active engagement, above 25 indicates highly active or strategic

engagement. In this research, financial institutions with an engagement below 8 were excluded from

most of the analysis as a clear position could not be determined.

Performance Organization Relationship Engagement

Financial institution

Band Score Score Intensity

Aviva B- 84 51 35

Legal & General B- 79 55 19

Groupe BPCE C+ 82 46 40

BNP Paribas C+ 81 49 40

Rabobank C+ 77 47 9

Unipol C+ 74 41 15

Nordea C+ 74 54 22

Aegon C+ 73 47 13

Deutsche Bank C 70 52 19

AXA C 70 50 18

Barclays C 69 47 8

BBVA C 67 48 19

Swiss Re C 67 49 11

Royal Bank of Scotland Group C 66 48 8

Danske Bank C 65 55 11

ABN AMRO C- 63 49 12

Allianz C- 63 51 29

Société Generale C- 63 47 13

Commerzbank C- 61 50 8

Zurich Insurance C- 59 48 11

Sustainable Finance Policy Engagement. September 2020 21HSBC D+ 59 50 24

Standard Life Aberdeen D+ 58 47 17

Standard Chartered D+ 54 49 10

Credit Agricole D+ 51 50 20

State Street D 52 43 13

Schroders D 51 43 25

UBS D 49 49 10

BlackRock D 48 51 22

BNY Mellon D 44 51 15

Invesco D 44 54 15

Performance Organization Engagement

Finance Industry Association

Band Score Intensity

Institutional Investors Group on Climate

B 80 27

Change (IIGCC)

The Institute of International Finance (IIF) D+ 51 15

PensionsEurope D+ 51 28

Association for Financial Markets in

D+ 51 29

Europe (AFME)

Insurance Europe D 49 24

European Banking Federation (EBF) D 47 24

BIPAR D 46 13

Managed Funds Association (MFA) D 45 8

European Association of Co-operative Banks

D- 43 24

(EACB)

European Fund and Asset Management

E+ 39 34

Association (EFAMA)

Invest Europe E+ 37 14

Alternative Investment Management

E 33 17

Association (AIMA)

Performance Organization Engagement

Corporate Industry Association

Band Score Intensity

Eurelectric D 50 17

European Chemical Industry Council (CEFIC) D- 41 6

European Steel Association (Eurofer) E+ 37 7

FORATOM E 34 12

EuropeanIssuers E- 27 27

BusinessEurope E- 25 18

FuelsEurope F 18 12

International Association of Oil and Gas

Producers (IOGP) F 18 16

Sustainable Finance Policy Engagement. September 2020 22You can also read