TAPER TANTRUM IN 2021-22: BEWARE OF THE TUCKANS - Euler Hermes

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Photo on Shutterstock ALLIANZ RESEARCH TAPER TANTRUM IN 2021-22: BEWARE OF THE TUCKANS 12 April 2021 04 Could the Fed start to normalize monetary policy earlier than expected and unsettle financial markets? 06 Emerging Market initial conditions are more favorable than in 2013, with exceptions 11 Which countries are most at risk? 12 What could this mean for markets?

Allianz Research

Could the Fed start to normalize its monetary policy earlier than expected? With

the USD1.9trn fiscal stimulus package and a new USD2.3trn infrastructure pro-

EXECUTIVE gram, we have raised our US GDP growth forecasts to +5.3% in 2021 and +3.8%

in 2022. As a consequence, tightening labor market conditions along with higher

commodity prices should also lift consumer price inflation to 2.5% in 2021 and 2%

SUMMARY in 2022. But we continue to believe that the US Fed will only consider tapering its

bond purchases starting in H2 2022 and increasing the Fed Funds Target rate

only from H2 2023 onward. And because monetary tightening in the US will cer-

tainly generate financial pressures worldwide, we think that the Fed will com-

municate on its future moves better than it did in 2013, when its announcements

surprised markets and caused the taper tantrum. Yet, there is a risk that the Fed

may be tempted to normalize its monetary policy earlier, and perhaps again sur-

prise markets due to miscommunication, so Emerging Markets (EMs) may be

faced with another potential taper tantrum. Our pattern recognition model con-

firms that this risk cannot be entirely ruled out.

Emerging Market initial conditions are more favorable than in 2013, with excep-

Alexis Garatti, Head of Economic Research tions. Current account deficits are lower today, credit growth is at more sustaina-

alexis.garatti@eulerhermes.com ble levels and we expect inflation to remain under control, by and large. EM cur-

rencies are likely to remain volatile but we do not forecast a broad-based repeat

of the substantial depreciations experienced in 2013-2014, also because real

effective exchange rates are currently less strained as currencies already took

large hits in 2020. Moreover, monetary policy is currently ultra-loose in many EMs

and it should remain accommodative overall in the near future even though a

moderate tightening is likely in those countries where inflation exceeds the cen-

tral banks’ target ranges. Increases in inflation expectations could put pressure

on central banks as the need of adapting the monetary policy clashes with the

Pablo Espinosa Uriel, Capital Markets need to support the Covid-19 recovery.

Research Analyst

pablo.espinosa-uriel@allianz.com However, external financing requirements and the steady rise in sovereign debt

reveal some weak spots. In six countries, the external debt payments falling due

in the next 12 months significantly exceed the level of official foreign exchange

reserves (Turkey, Argentina, Ukraine, South Africa, Romania, Chile). Moreover, the

steady rise in sovereign debt over the past decade poses a significant risk, in par-

ticular for those EMs where the share of non-residents’ holdings of public debt

has increased over the last seven years.

Overall we identify seven EMs particularly vulnerable to the eventual Fed taper-

ing, especially if it is not well communicated, the TUCKANS: Turkey, Ukraine,

Manfred Stamer, Senior Economist for

Emerging Europe and the Middle East

Chile, Kenya, Argentina, Nigeria, South Africa. A stabilization of the money flows

manfred.stamer@eulerhermes.com

after a complicated 2020 would be crucial, but a pattern of relatively steady in-

flows into EMs is not yet visible, at least not in a generalized way.

EMs, in particular some of the TUCKANS, are already experiencing generalized

rises in the interest rates of their local currency bonds. In the short term, this is a

sign of upcoming volatility. If sustained, it could pose severe threats to debt sus-

tainability, which was already an issue for some of the countries before. However,

this spike could be at least partially a consequence of high growth expectations,

which would make it less risky than one solely based on US tapering.

2

12 April 2021

Photo on Unsplash

7

Emerging Markets particularly vulnerable to

an eventual tapering of monetary policy by the US Fed.

3

Allianz Research

COULD THE FED START TO NORMALIZE

MONETARY POLICY EARLIER THAN EXPECTED

AND UNSETTLE FINANCIAL MARKETS?

The interdependence of financial mar- end of 2022 compared with 6.2% in confirms that the US central bank could

kets, and the predominant position of February 2021. Fiscal incentives to in- be tempted to normalize monetary

the US and the USD, make the rest of crease the minimum wage (we inte- policy much earlier. However, we conti-

the world – especially Emerging Mar- grate a scenario leading us to USD11 nue to think that the Fed will only consi-

kets (EMs) – sensitive to any financial per hour by end-2022 compared with der tapering starting in H2 2022 and

event that takes place in the US, not to USD7.25 today) will add further infla- increasing the Fed Funds Target rate

mention any changes in the Federal tionary pressures alongside the rapid only from H2 2023 onward. The proxi-

Reserve’s monetary policy. This was last diminution of the US job market’s de- mity between the Funds target rate

seen in 2013, when just the announce- gree of slack. As a result of these upco- and the natural rate of interest rate

ment of future tapering by the Fed go- ming tightening job market conditions tells us that the current stance of the US

vernor unchained a generalized spike and the positive pass-through of recent monetary policy can be deemed as

in US sovereign yields, the appreciation energy and commodity prices (the im- being only moderately accommodative

of the USD and capital outflows from pacts of which are already visible at the in the current circumstances. In this

fragile EMs. level of input prices), we have revised case, the Fed will have the luxury to

Taking into account President Joe on the upside our US CPI inflation sce- wait and see before really envisaging a

Biden’s USD1.9trn fiscal package and nario, with 2.5% y/y expected in 2021, normalization in its monetary policy.

the USD2.3trn infrastructure investment 2% in 2022 and 2.1% y/y in 2023. The But despite this forecast, and due to the

plan, we now expect US GDP to grow two-year average CPI yearly increase message conveyed by the mechanical

by +5.3% y/y in 2021 and +3.8% y/y in will reach 2% y/y in early H2 2022 ins- approach of the Fed’s reaction func-

2022, with risks tilted on the upside1. As tead of late H2 2022 in our previous tion, episodes of stress and volatility will

a result, the level of slack of the US job scenario. be visible if the market considers at one

market in particular will diminish more Our Fed reaction function, estimated in point that the Fed is behind the curve.

rapidly than expected before (full em- function of the spread of inflation bet- In such circumstances, we need to anti-

ployment end-2022). We expect the US ween observed data and the target of cipate the consequences of another

unemployment rate to hit 4.3% at the 2%, and in function of the NAIRU gap, potential taper tantrum.

Figures 1 and 2: Job market conditions in the US

16 NAIRU 10

Average Hourly Earnings (%, y/y)

US unemployment rate

14 15$ end of 2022

8 Average 15$ end 2022

12 11$ end of 2022

Average 11$ end 2022

10 6

8

4

6

2

4

2 0

10 11 12 13 14 15 16 17 18 19 20 21 22 10 11 12 13 14 15 16 17 18 19 20 21 22

Sources: National statistics, IMF, Allianz Research forecasts

1

For more details on our outlook for the US economy, refer to our recent report Race to the post Covid-19 recovery: Seven obstacles to overcome.

4

12 April 2021

Figure 3: Fed’s theoretical reaction function Figure 4: Fed Funds target rate (%)

8 7

6

6

4

5

2

4

0

3

-2

2

-4

1

-6

-8 0

95 98 01 04 07 10 13 16 19 22

00 02 04 06 08 10 12 14 16 18 20 22 24

FFR Expected new Expected old Effective Fed Funds Rate US natural rate of interest

Sources: : National statistics, IMF, Allianz Research forecasts Sources: National statistics, IMF, Allianz Research

What do the markets tell us about the larities between the current situation These results show that the current situ-

proximity to a taper tantrum-like and our pattern of interest (early 2013). ation is more similar to relatively calm

situation? moments than to severe crisis-like situa-

In our case, we use a very large sample

tions. However, as experienced sailors

of ETFs – cross asset classes and cross

One year after Covid-19 shook up the know, it is important to distinguish real

geographies – and measure their rela-

financial markets, the waters are calm- calm from apparent calm. Compared

tive strength against the MSCI World,

er but volatility and risks remain, trans- to 2013, the framework of today’s situa-

our benchmark. By doing that, we do

lating into some market movements, tion is not very different (nor the clos-

not limit ourselves to a particular mar-

including in the US yield curve2 and est) so some kind of taper tantrum is

ket or asset but aim to capture the gen-

commodities markets3, both of which not something that can be excluded.

eral trend. After comparing today’s

EMs are very sensitive to. In order to

strength with the weekly positioning

analyze the global situation of financial

since late 2008 by ETFs, we aggregate

markets, and how close we are to the

the square of the differences and the

taper tantrum situation seen in 2013,

results are shown in Figure 5.

we use a pattern recognition frame-

work to identify whether there are simi-

Figure 5: Pattern recognition – relative strength of financial indicators against the MSCI World

40 000 400

35 000 350

30 000 300

25 000 250

20 000 200

15 000 150

10 000 100

5 000 50

0 0

-5 000 -50

2008 2010 2012 2014 2016 2018 2020

Distance to current markets performance (LHS)

US Curve Steepness (bps) (RHS)

Sources: : Bloomberg, Refinitiv, BofA, Allianz Research.

2

To understand the tensions at the short-end of the curve, refer to U.S. Yield curve: Let’s twist again?

3

Find our latest analysis on commodities Higher demand, supply bottlenecks, but no speculation (yet). 5Allianz Research

EMERGING MARKET INITIAL CONDITIONS ARE

MORE FAVORABLE THAN IN 2013,

WITH EXCEPTIONS

Higher yields in the US and Europe section, we compare the current situa- eight years ago, including the large

create competition for capital and can tion to that of 2013 for 16 selected economies of India, Brazil, Mexico,

make financing EM imbalances more comparatively fragile EMs, the Fragile Turkey and South Africa. Only two

difficult. Previous EM crises have 164 , with a focus on these key risk indi- countries, Kenya and Romania, are

showed that a slow policy response to cators. projected to post shortfalls of more

rising imbalances can indeed lead to a than -4% of GDP in 2021, a value often

sharp deterioration in market confi- Current account deficits have signifi- used as the threshold between critical

dence. The key indicators that identify cantly declined and adequate deficits (see Figure 6). In

EM vulnerabilities and also differen- 2013, five out of the Fragile 16 ex-

tiate between economies are the cur- The external balances of major EMs ceeded this threshold. This suggests

rent account balance, credit growth, are currently more favorable than back that these EMs are currently overall less

inflation, currencies, policy interest in 2013. Most of the 16 EMs in our dependent on foreign capital inflows

rates, foreign exchange reserves, sove- sample are forecast to record a smaller than in 2013 – at least for now – bo-

reign debt and bonds. In the following current account deficit in 2021 than ding well for the eventual Fed tapering.

Figure 6: Current account balances (% of GDP) of selected EMs

Kenya

Romania

Nigeria

Colombia

South Africa

Chile

Turkey

Indonesia

Mexico

Argentina

India

Philippines

Hungary

Brazil

Ukraine

Russia High risk

-10% -8% -6% -4% -2% 0% 2% 4%

2013 2021f

Sources: National statistics, IMF, Allianz Research forecasts

4

The 16 selected “comparatively fragile EMs” – the Fragile 16 – comprise the 10 EMs we identified as fragile in 2013 and the 13 most fragile EMs we have identified in early 2021, both

6 out of a larger group of 28 economies. There is an overlap of seven countries between these samples from 2013 and 2021.12 April 2021

Credit growth is more sustainable monetary policy style, including lower- tion below the 5% mark and within the

ing interest rates to levels that will in- individual target ranges of their nation-

Also positive from a risk point of view, crease rather than decrease economic al central banks in 2021, which is an

credit growth to the private sector was imbalances. improvement compared to 2013 (see

more moderate in our sample of EMs in Figure 8).

2020 than it was in 2013, despite the Inflation to remain in check in most EMs

massive monetary easing that was im- Another traditional indicator for infla-

plemented to mitigate the impact of A view on consumer price inflation rates tion expectations are inflation-linked

the Covid-19 pandemic on economies. provides a more differentiated picture. bonds, both in terms of the amount

This may reflect less demand for credit In 2013, Argentina was the only country issued and in terms of breakeven infla-

amid the crisis and will reduce growth with double-digit inflation (10.6%) in our tion. Although these bonds are not

prospects in the near term but it also sample of 16 EMs. In 2021, we forecast available for all the countries in our

indicates lower liquidity risk than during Argentina, Nigeria and Turkey to post sample, for the countries that do have

the taper tantrum period in 2013-2014. average annual inflation rates well them, the picture is very similar to our

This is particularly the case for Brazil, above 10% (45% in the case of Argenti- forecasts in terms of countries at risk of

Colombia, Russia, India, the Philippines na), which will also be clearly higher higher inflation (see Figure 9). Among

and Indonesia, countries where credit than the rates recorded eight years the countries in the selection, Turkey

growth was at or above our 15% thresh- ago. Ukraine (6.6% forecast in 2021 vs. has been one of the most volatile, with

old in 2013, indicating elevated risk5. -0.3% in 2013) and Kenya (5.1% vs. break-even inflation above 15%. It was

However, rapid credit growth still flash- 1.1%) should also post significantly accentuated because of the financial

es warning signals in Turkey, Argentina higher inflation this year than eight turmoil that has taken place after the

and Nigeria, where it rose by well years ago, with Ukraine’s projected rate latest events around the central bank.

above 20% y/y on average in 2020, as to exceed the central bank’s 5% ± 1pp Apart from Turkey, other countries such

well as in Hungary (17% y/y, see Figure inflation target range. South Africa, as Brazil, Russia and Ukraine have re-

7). At the time of writing, a clear down- Hungary, Chile, the Philippines and Co- cently increased their respective inter-

ward trend in credit expansion was only lombia are also expected to record est rates. These moves confirm that

visible in Argentina. Meanwhile, the higher inflation in 2021 compared to some Emerging Economies are already

expected transmission of sharp interest 2013, but the price changes should be fighting these expectations.

rate hikes in Q4 in Turkey into slower kept in check, i.e. remain below 5%, and To summarize, we expect inflation to

credit growth has yet to materialize. In within the central banks’ respective tar- remain under control across major EMs

fact, this may not happen at all after get ranges. In Russia, average annual in 2021, excluding a few vulnerable

the dismissal in mid-March 2021 of inflation is forecast to increase from economies that already experienced

Central Bank governor Agbal who had 3.4% in 2020 to 5.1% in 2021, thus ex- crises prior to the Covid-19 pandemic.

been in office for just four months and ceeding the 4% inflation target, but it This offers room for central banks to

was responsible for the appropriate will be lower than the 6.8% posted in provide support to their domestic econ-

rate hikes. Markets now fear that Tur- 2013. India, Brazil and Indonesia are omies, and perhaps governments, in

key will revert to its known unorthodox expected to experience moderate infla- the event that foreign credit dries up.

Figure 7: Private sector credit growth (%) of selected EMs Figure 8: Average annual inflation (%) in selected EMs

Turkey Argentina 45%

Argentina Turkey

Nigeria Nigeria

Hungary Ukraine

Brazil Kenya

Chile Russia

Colombia India

Russia Brazil

Kenya South Africa

India Romania

Mexico Hungary

Philippines Chile

Romania Mexico

South Africa Philippines

Indonesia Colombia

Ukraine Rising risk Indonesia

0% 2% 4% 6% 8% 10% 12% 14%

-10% 0% 10% 20% 30% 40%

2013 2020 2013 2021f

Sources: National statistics, IMF, Allianz Research Sources: National statistics, IMF, Allianz Research forecasts

5

The threshold is given as 150% of the long-term average of the monthly medians (of private sector credit growth) of approximately 160 EMs.

6

Here it is calculated as the difference between the nominal bonds yield and the inflation-linked bond yield. It is the level of inflation that would provide equal real yield in both type of 7

bonds.Allianz Research

Figure 9: Inflation-linked bonds across selected EMs Figure 10: Exchange rates of selected EMs

Growth IXL bonds outs. 2018 (LHS) Growth IXL bonds outs. 2019 (LHS)

Growth IXL bonds outs. 2020 (LHS) Growth IXL bonds outs. 2021 (LHS)

B/Even Inflation 2018 (RHS) B/Even Inflation 2019 (RHS)

B/Even Inflation 2020 (RHS) B/Even Inflation 2021 (RHS)

45% 18%

30% 12%

15% 6%

0% 0%

-15% -6%

BRA CHL MEX COL RUS POL THA TUR ZAR

Sources: Refinitiv, BofA, Allianz Research Sources: IHS Markit, Allianz Research

Currencies to remain volatile but no gure 10 shows the largest movements Russia, Brazil), interest rates should re-

broad-based repeat of the deep slides in the FX Market since the end of 2020. main low in the EM world, by and large,

in 2020 Looking ahead, our internal calcula- and continue to support the recovery in

tions show that some currencies may 2021-2022. And even if rates are hiked

When looking at the evolution of cur- have depreciated too much, and there moderately in a few other countries

rencies, 2020 was a year of generalized could be room for some reversal, al- over the next 12 months, as will likely be

depreciations of EM currencies, if we though still not enough to reach 2019 the case, we expect the overall moneta-

exclude some strong Asian economies levels. On the other hand, there are ry policy stance in EMs to remain loose.

(China, South Korea and Malaysia), currencies that could still depreciate This will continue to provide space for

Chile and the Eastern European curren- further, such as the Mexican peso, alleviating any impact of the eventual

cies highly correlated with the euro. South African rand or the Thai baht. The Fed tapering on EMs without putting

There were different intensities, ranging Argentinian peso and the Turkish lira the recovery path at risk.

from the small movements of the rest of seem to position themselves as the

the APAC currencies such as the Thai most volatile currencies among the se- External financing requirement reveals

baht (almost flat) or the Indonesian lection. weak spots

rupiah (-1.2%) to the strong deprecia- However, the pace of the Covid-19

tions in Brazil (-29%) or Argentina (- shock recovery, the high risk of policy With regard to the foreign exchange

40%). mistakes – as idiosyncratic features – (FX) reserves coverage of maturing

The common denominator of 2021 has and the evolution of the US economy short-term external debt, the situation

been volatility – much of it also im- and global financial markets – as syste- has worsened since 2013. In six coun-

ported from the US – but the first quar- mic risks – could dramatically change tries, the external debt payments falling

ter indicates further strengthening of the outlook. due in the next 12 months significantly

the USD, mainly against the euro- exceed the level of official FX reserves

centric Eastern Europe and APAC cur- Monetary policy to remain accommo- held at the respective central banks,

rencies. In Latin America, the deprecia- dative overall despite an expected mo- notably in Turkey where the debt is

tions have deepened – now including derate tightening more than four times higher than re-

the Colombian peso. Meanwhile, the serves (see Figure 12). Four of the six

Monetary policy interest rates are cur- countries (Turkey, Argentina, South Afri-

Turkish lira slumped at the end of rently lower for most EMs than in 2013,

March after the firing of the central ca, Chile) have been through one or

except for countries that have suffered several crises over the past few years.

bank governor Agbal who had calmed from the aftermath of a recent crisis,

financial markets prior through appro- As a result, the economies experienced

such as Argentina, Mexico, Turkey and net capital outflows and currency pres-

priate monetary tightening during his Nigeria (see Figure 11). In most cases,

short term in office. Markets now fear sures. Mostly unsuccessful FX interven-

policy rates were already on a down- tions by the respective central banks to

that Turkey may reverse that policy ward path prior to 2020 as a result of

course too quickly which could maneu- mitigate the financial turbulence have

easing inflationary pressures and were led to a drawdown of FX reserves. On

ver the economy once again close to cut further during the pandemic in or-

the next currency crisis. Meanwhile, as the other hand, a majority of EMs inclu-

der to mitigate the impact of the crisis. ding India, Brazil, Russia and Mexico

other main currencies such as the euro Even if some central banks raised policy

or the Japanese yen are losing ground have ample reserves, which strengthen

rates in March 2021 in response to their central banks’ policy options in the

against the USD as well, the impact on above-target inflation (Ukraine, Turkey,

those exchange rates is lessened. Fi- event of external shocks.

812 April 2021

Figure 11: Key monetary policy interest rates in selected EMs

16% 90% 8% 30%

14% 80% 7%

25%

70%

12% 6%

60% 20%

10% 5%

50%

8% 4% 15%

40%

6% 3%

30% 10%

4% 20% 2%

5%

2% 10% 1%

0% 0% 0% 0%

12 13 14 15 16 17 18 19 20 21 12 13 14 15 16 17 18 19 20 21

Brazil Chile Colombia Mexico Argentina (rhs) Hungary Romania Ukraine (rhs) Russia (rhs) Turkey (rhs)

9% 20%

8% 18%

7% 16%

14%

6%

12%

5%

10%

4%

8%

3%

6%

2% 4%

1% 2%

0% 0%

12 13 14 15 16 17 18 19 20 21 12 13 14 15 16 17 18 19 20 21

India Indonesia Philippines South Africa Nigeria Kenya

Sources: National statistics, IHS Markit, Allianz Research

Figure 12: Maturing external debt over the next year in relation to FX reserves (%) in selected EMs

Turkey 454%

Argentina

Ukraine

South Africa

Romania

Chile

Hungary

Indonesia

Mexico

Colombia

Kenya

Philippines

Russia

Brazil

India

High risk

Nigeria

0% 50% 100% 150% 200% 250%

2013 2021f

Sources: National statistics, IMF, Allianz Research forecasts

9Allianz Research

Risks with regard to sovereign debt On the other hand, this risk has decli- We conclude from this analysis of cru-

ned since 2013 in Hungary, Mexico, the cial vulnerability indicators that, by and

On a negative note, the share of non- Philippines and Brazil because the large, major EMs are in a better posi-

residents’ holdings of public debt has share of nonresident holdings of public tion to withstand the impact of even-

increased in many EMs over the last debt has markedly fallen in these mar- tual US Fed tapering than they were in

seven years. In Indonesia, Ukraine, Ke- kets. 2013. Yet, the risk of widespread finan-

nya, Romania, Argentina, Turkey, Chile cial market turmoil is not negligible,

and South Africa, it currently exceeds Meanwhile, the spreads of hard curren- especially if the Fed tapering is badly

35% of total public debt (see Figure 13). cy sovereign bonds present two diffe- communicated. Moreover, a few mar-

This increases the risk of a sudden capi- rent trends. The main EMs in Asia and kets are currently more vulnerable than

tal reallocation from EMs to the US and Central and Eastern Europe now have others, mostly due to macroeconomic

financial market turbulence in EMs in narrower spreads than they did in April imbalances or a lack of economic poli-

the event that the Fed tapers and hikes 2013, so in case of a future spike the cy leeway to counter cyclical weak-

rates earlier than currently announced starting point is lower. The opposite nesses. In the next section we will iden-

and without appropriate advance com- situation is visible in Turkey and the tify the weak spots by combining the

munication. This will make financing main Latin American and African advanced indicators for financial ten-

more expensive for EMs, also for the economies in our sample (see Figure sions in EMs in a scoring model.

private sector (notably corporates), so 14).

that payment behavior could deterio-

rate and insolvencies may increase.

Figure 13: Non-resident holding of total public debt (%) Figure 14: EM hard currency sovereign bond spreads (bps)

Argentina

Indonesia

Ukraine*

Ukraine

Turkey

Kenya Nigeria

Romania Egypt

Argentina Kenya

Turkey

South Africa

Brazil

Chile

Colombia

South Africa Mexico

Hungary Russia

Colombia Romania*

Mexico Indonesia

Philippines

Russia

Chile

Philippines Croatia*

Brazil Malaysia

Higher risk

India Poland*

0% 10% 20% 30% 40% 50% 60% 0 200 400 600 800 1000

2013 2020 Current Apr 2013

Sources: IIF, IHS Markit, Allianz Research estimates Note: * indicates that the hard currency is EUR, otherwise USD.

Sources: Refinitiv, BofA, Allianz Research

1012 April 2021

WHICH COUNTRIES ARE

MOST AT RISK?

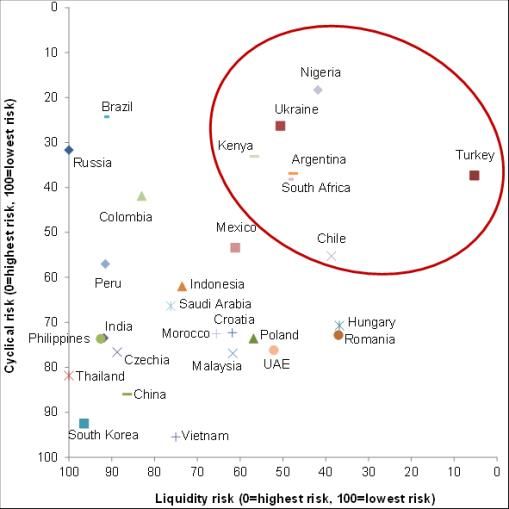

Even if we expect this time to be differ- We have undertaken a reality check Seven EMs are particularly fragile to a

ent from 2013 with regard to the US and identified the most fragile EMs with potential repeat of the 2013 taper tan-

Fed policy announcements, financial regard to : trum over the next two years or so ac-

market reactions and the pre- Liquidity risk (current account bal- cording to our analysis, the TUCKANS:

conditions in many major EMs, there ance, short-term external debt due, Turkey, Ukraine, Chile, Kenya, Argenti-

will be some among the latter that are import cover, private sector credit na, Nigeria and South Africa. Less vul-

more vulnerable than others to a taper growth) and nerable but not fail-safe are Brazil,

tantrum, especially if the Fed’s actions Cyclical risk (currency risk, inflation, Mexico, Colombia, Hungary, Russia and

are not well communicated. commodity dependence, equities, Romania, which should thus also be

bonds). monitored closely.

The result is summarized in Figure 15.

Figure 15: Advanced indicators for financial tensions in major EMs

Source: Allianz Research

11Allianz Research

WHAT COULD THIS MEAN

FOR MARKETS?

The Fed has committed to keep rates As we have seen lately, the movements tries in Figure 16, Argentina and

low and the consensus is that the first in the US bond markets have had cor- Ukraine deserve a special mention, with

rate hikes would take place in 2023, responding aftershocks in local curren- interest rates in the local currency

with the tapering starting in 2022. cy bond yields in developing countries. bonds above 40% and 10%, respective-

However, stress in the US bond markets In terms of hard currency bonds, the ly. Their curves have flattened in the last

or rising inflation expectations bring the movements in the US bond market couple of months, with decreases in the

question of what could happen if some have not yet caused generalized long end (from 50.8% to 46.6% in the

measures need to be anticipated. As it spread widening in EMs (with the ex- Argentinian 7Y), and increases in the

was the case in 2013, and has been at ception of Turkey), which could have short end. In those two countries, the

other occasions, a (mis)calculated made things harder. idiosyncratic pressures of both countries

speech by a central banker could be and the situation that they had already

enough to unchain the reaction, even if Figure 16 shows the latest volatility in at the beginning of the year play an

the words materialize into actions only sovereign bonds issued in local curren- important role. The fact that

months or years afterwards. Although cy. In broad terms, the figure also corro- movements in their bond markets may

tightening in the US will certainly gene- borates the findings of the taper tan- go in the opposite direction as the rest

rate pressures worldwide, the Fed trum risk indicator: the largest moves so of EM countries is not necessarily a

claims to have learnt its lesson. Whe- far took place in the TUCKANS. As men- good signal.

ther the announcements, the tapering tioned in previous sections, the events

and the hikes are somehow predictable at the Central Bank of Turkey have

and relatively structured will determine created turmoil in Turkish financial mar-

the impact and will prove whether the kets, which exacerbates the trend seen

lesson was really understood. in other regions. In addition to the coun-

Figure 16: Changes in the LC sovereign yields since 01.02.2021 (in bps) – 1Y and 10Y

Turkey

Brazil

Nigeria

Mexico

Colombia

Philippines

Russia

South Africa

Chile

Czechia

Thailand

Kenya

Malaysia

Romania

Poland

-200 0 200 400 600 800

10Y 1Y

Note: The graph shows only a sample of the countries analyzed, that corresponds with the countries with the highest increases in the 10Y bonds.

Sources: Refinitiv, BofA, Allianz Research

1212 April 2021

Figure 17: Differential between past economic growth and current cost of Figure 18: Volatility in the FX market – selected currencies against the

debt (measured as the average coupon of the sovereign debt) USD

14% 24

TRY +2

12% +1 x=y

10%

8% 18

BRL

As of 31.03.2021

6%

4%

12

2% MXN

0%

-2%

6

-4%

ARS

-6%

BRA

UKR

RUS

TUR

THA

CZE

ZAF

MEX

IDN

IND

POL

NGA

KEN

COL

MYS

PHL

CHN

PER

HUN

ROU

0

0 6 12 18 24

Differential Avg Coupon Avg YoY Nom. Growth 2015-2019

As of Feb19

Note: Argentina’s not shown as the picture would not contain the defaulted bonds Note: The volatility of the Turkish lira was already one of the highest before 15

in 2020. March.

Sources: Refinitiv, national statistics, Allianz Research Sources: Refinitiv, Allianz Research

Although the concept of a taper tan- Most of the TUCKANS are again at risk rise as well, including the potential ta-

trum is linked to volatility in the short when looking at the interest rate- per tantrum.

term, should the increase in the interest growth differential: Nigeria, Ukraine,

rates remain; it could have harming Turkey, Kenya and South Africa Even if a proper taper tantrum does not

effects on debt sustainability. Low inter- (Argentina as well, refer to the note on finally materialize in generalized out-

est rates are key for sustaining current Figure 17). In addition, some of the flows from EMs and generalized spikes

levels of indebtedness, especially when countries that appeared in the second in sovereign yields and spreads, the

the programs to fight Covid-19 and its group regarding their taper tantrum struggle to overcome the Covid-19 cri-

lasting effects may require more financ- risk (Brazil, Russia, Colombia) could sis (both from sanitary and economic

ing. face severe debt sustainability issues, perspectives), rising inflation expecta-

given the already high differential be- tions and the eventual Fed tightening

To analyze that, in addition to the tween payable coupons and economic are elements that will increase volatility

changes shown in Figure 16, we have growth. In terms of maturity, among the across EMs, at least to higher levels

performed an analysis of the differen- countries more at risk, Turkey and Brazil than seen in the period preceding the

tial between the interest rates and are the ones with the shortest term, Covid-19 shock. In fact, since the trough

growth rates. This is a common meas- which adds more uncertainty as they of the oil crisis in 2015, and with the

ure of debt sustainability, as the cost of would have more redemptions in 2021. exception of local instabilities, EMs had

debt is compared with the returns it On the opposite side, we find the Asian performed relatively well.

provides. For the calculation, we use the economies and Central and Eastern

average coupon that EM countries are Europe (with the exception of Russia Will higher volatility become the norm

paying for their sovereign debt and the and Ukraine). Their reasons, however, in the coming years? We cannot answer

average nominal yearly growth be- are different: while the Eastern Europe- the question yet, but we have already

tween 2015-2019. The countries that in an countries are characterized by low seen how the volatility that came after

Figure 17 show a positive difference interest rates and moderate economic Covid-19 has not fully disappeared.

between average coupon and past growth, some of the Asian economies One example is the FX market.

economic growth could have problems like India, Indonesia and Philippines are

in the coming years if they do not man- characterized by strong economic To observe this, we compare moving

age to change one or both variables. As growth that makes up for interest rates standard deviations on exchange rate

the starting point of GDP in 2020 is low, above 5%. changes at different points in time. In-

the potential growth is higher. But will it stead of taking the values around the

be enough to offset the cost of debt? As In any case, the figure uses pre-crisis volatility peak in March 2020 – which

of today, we have been observing some economic growth, so the perspectives could be considered one-offs - we take

increases in the interest rates that could could change for some countries, either the situation one year before and one

make it harder, a situation that could because they are not able to go back to year after (current). We observe in Fig-

worsen in the event of a taper tantrum. pre-crisis growth rates, or because they ure 18 how the volatility is generally

Figure 17, read from left to right, shows manage to recover quickly and strong- higher, with currencies such the Turkish

the countries with the largest imbalanc- ly. In terms of how the interest rates lira, Brazilian real and Mexican peso

es. could change in the future, there are being the most affected.

some risks that indicate that they could

13Allianz Research

Yet another proof of volatility, both in At this point, it is important to note the mark an important distinction from the

the US and in the EMs, is the flow of interdependency of financial markets. situation in May 2013, when Bernanke’s

capital from/to these markets. After a One should not forget that central arguments for tapering were more on

2020 of net outflows in most of the local banks, by tampering the risk perception the line of exhausted effectiveness of

bond markets, the flows in Q1 2021 in their intent to contain idiosyncratic some monetary tools. It is not only the

depict an erratic trajectory. In principle, risks, have increased interdependence fact that interest rates rise, but also the

we expect the cumulative balance to be between different asset classes7. For the reason why they rise.

positive, with net inflows to EMs in 2021, case of this paper, this means that in

but at the same time with high volatility the case of negative developments, the All in all, we expected a bumpy 2021,

in both size and direction of the net improvements of a country’s situation which by definition includes some vola-

flows. would not be enough to avoid the con- tility in expectations through the year.

tagion, although it is always preferable As of today, with the mentioned excep-

The situation differs considerably across to have low idiosyncratic pressures. tions of particular countries, the current

countries. Figure 19 shows the standar- Taking into account that the departure developments fit into the turbulence

dized cumulative flows to local bond points are the Covid-19 levels, the narrative. Whether the turbulence re-

markets since 2018 in a selection of growth expectations look better now mains manageable will depend on ma-

countries. While Q4 2020 was positive than they did in 2013-2015. Further- ny factors, one of them being the indi-

in terms of inflows for most of the coun- more, there are signs of rising inflation rect effects of US tapering, but it is defi-

tries, Q1 2021 is much more hetero- expectations that in general will remain nitely not the only one.

geneous. under control. These two elements

Figure 19: Cumulative flows since 31.12.2018 in the local bond markets, standardized

1.8

1.6

1.4

1.2

1

0.8

0.6

Dec-18 Jun-19 Dec-19 Jun-20 Dec-20 Jun-21

Brazil Poland South Korea Mexico Thailand India Turkey

Sources: Refinitiv, Allianz Research

7

To deepen into the topic of QE and diversification, refer to one of our latest papers QE and the bull market in everything but diversification.

14OUR TEAM

15RECENT PUBLICATIONS

07/04/2021 Unleashing excess foreign exchange reserves to boost growth in Latin America

06/04/2021 Joe Biden's infrastructure plan: defying gravity

01/04/2021 Race to the post Covid-19 recovery: 7 obstacles to overcome

26/03/2021 The Suez Canal ship isn't the only thing clogging global trade

23/03/2021 The Hotel California effect: How the European hospitality sector is looking for people

who stay

22/03/2021 China's policy mix: "proactive" and "prudent" in name, tightening in practice

17/03/2021 Show me the money: debunking a couple of myths about excess liquidity

15/03/2021 The irony of Biden's super stimulus: USD360bn for exporters around the world

11/03/2021 Commodities: higher demand, supply bottlenecks, but no speculation (yet)

08/03/2021 US yield: Let's twist again?

05/03/2021 Tourism: Europe will be at the frontline of the recovery, but only in 2024

03/03/2021 The not so merry adventures of the Robin Hood generation in financial markets

25/02/2021 Covid-19 one year on: 1.8 million additional long-term unemployed in Europe

24/02/2021 European corportaes: (active) cash is king

23/02/2021 QE and the bull market in everything but diversification

18/02/2021 Risk literacy and choices - Stubbing toes in the dark

17/02/2021 Digital-enabling countries proved more resilient to the Covid-19 economic shock

15/02/2021 Italy: Draghinomics FAQ

11/02/2021 Is the Chinese ox reflating the world, one container at a time?

09/02/2021 China: Riding the silicon ox?

08/02/2021 Big Oil: At risk of becoming fossil firms?

04/02/2021 Covid-19 vaccines: a USD40bn revenue windfall for pharmaceuticals

03/02/2021 Vaccination delay to cost Europe EUR90bn in 2021

27/01/2021 Allianz Regional Pension Report 2021: Asia

26/01/2021 EU vs. U.S. vs. China: The hot race for green tech dominance to cool the global cli-

mate

20/01/2021 President Biden's inauguration: 100 days to save America?

19/01/2021 Allianz Risk Barometer 2021

18/01/2021 The world is moving East, fast

Discover all our publications on our websites: Allianz Research and Euler Hermes Economic Research

16Director of Publications: Ludovic Subran, Chief Economist

Allianz and Euler Hermes

Phone +33 1 84 11 35 64

Allianz Research Euler Hermes Economic Research

https://www.allianz.com/en/ http://www.eulerhermes.com/economic-

economic_research research

Königinstraße 28 | 80802 Munich | 1 Place des Saisons | 92048 Paris-La-Défense

Germany Cedex | France

allianz.research@allianz.com research@eulerhermes.com

allianz euler-hermes

@allianz @eulerhermes

FORWARD-LOOKING STATEMENTS

The statements contained herein may include prospects, statements of future expectations and other forward -looking

statements that are based on management's current views and assumptions and involve known and unknown risks and

uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such forward -

looking statements.

Such deviations may arise due to, without limitation, (i) changes of the general economic conditions and competitive situa-

tion, particularly in the Allianz Group's core business and core markets, (ii) performance of financial markets (particularly

market volatility, liquidity and credit events), (iii) frequency and severity of insured loss events, including from natural ca-

tastrophes, and the development of loss expenses, (iv) mortality and morbidity levels and trends, (v) persistency levels, (vi )

particularly in the banking business, the extent of credit defaults, (vii) interest rate levels, (viii) currency exchange rat es

including the EUR/USD exchange rate, (ix) changes in laws and regulations, including tax regulations, (x) the impact of

acquisitions, including related integration issues, and reorganization measures, and (xi) general competitive factors, in

each case on a local, regional, national and/or global basis. Many of these factors may be more likely to occur, or more

pronounced, as a result of terrorist activities and their consequences.

NO DUTY TO UPDATE

The company assumes no obligation to update any information or forward -looking statement contained herein, save for

any information required to be disclosed by law.

17You can also read