The European Commission's science and knowledge service - Joint Research Centre - Smart Specialisation Platform

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The European Commission’s science

and knowledge service

Joint Research Centre

Financing Energy Efficiency

Paolo Bertoldi

CAUSE OF FINANCING BARRIERS • Problem not caused by a lack of available funding capacity in many/most local markets. • Caused by an inability of Energy Efficiency Projects (EEPs) to access existing funds due to a “disconnect” between traditional Asset-based lending to corporations versus Cash Flow-based project financing to EEPs. • The solution to the problem is difficult because energy efficiency markets are not developed enough to motivate local banks to invest in setting up an EEP lending infrastructure.

BARRIERS • The most frequently cited reason for local governments not engaging in comprehensive building retrofit and energy efficiency activities is a perceived "lack of capital". • The truth of the matter is that even cash starved local governments can take advantage of different financing methodologies to get the work done from pre-feasibility analysis to monitoring and verification of energy savings. • It is simply a matter of knowing where to look for the capital- and how to structure the form that the capital will take in the transaction that will best suit your own unique needs.

CAPITAL STRUCTURE Local Financing Institutions (LFIs) typically: • Are accustomed to providing “asset-based” lending at 70%-80% of the market value of assets being financed, or other collateral. • Do not recognize the Cash Flow generated by EEPs as a new asset to be valued in the financing structure (credit enhancement). • Are not familiar with the intricacies of financing EEPs - creating a perceived high-risk lending profile for EEPs. Hence De-Risking • Do not have the internal capacity to properly evaluate EEP risks/benefits nor to structure their financing in market-acceptable ways. • Are unwilling to invest the time and resources needed to develop lending infrastructure due to relatively small size of each EEP. Role for Aggregators • Experience market conditions that preclude commercially-viable financing to EEPs (high interest rates and short repayment terms).

Energy Services Companies: Status and

Related Projects

Why is access difficult ?

• Lending from Local Financial Institutions (“LFIs”) - EEP not traditional business

- Corporate Lending – generally Asset based

- Energy Efficiency investment risks not understood –

- Risks perceived too high

- Interest Rates too high

- Repayment Term too Short

• Lending from International “IFIs” not applicable:

- Size of Projects too small

- Due diligence too cumbersome

FINANCING OPTIONS Municipality have several options before them in terms of how they seek to finance energy efficiency projects. These include: • Own Source Revenues; • Direct Borrowing; • Third Party Financing; • Innovations and Future Options;

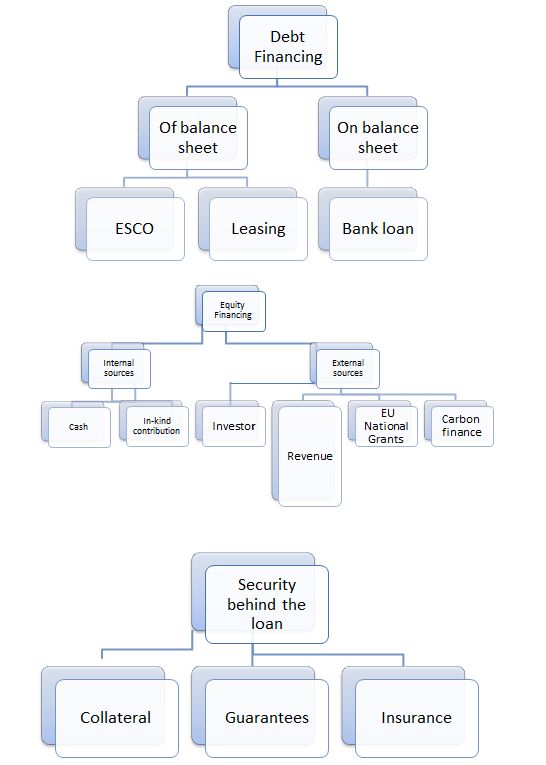

CAPITAL STRUCTURE

Debt Financing Equity Financing

On-balance-sheet Off-balance-sheet Internal sources External sources

In-kind

Bank loan ESCO Leasing Cash Investor Revenue

contribution

EU

Security behind the loan funding

Carbon

Collateral Guarantees Insurance finance

1. OWN SOURCE REVENUES

I

• Municipalities have several sources of capital to tap for efficiency retrofits. The first is their

Operating Budget of which energy or utility bills constitute only 1%-2%. However, in a large

city, which still maintains a budget in excess of 1 Billion Euro, this equates to roughly 10 Million

Euro which is spent annually. If the city can save only 20% on its owned buildings, it would

save about 2 Million Euro annually!

• The Operating Budget however, may not be the most practical place to look for substantial

funds to retrofit municipal building stocks. In fact, most municipalities typically allocate small

amounts of capital depending on their size, but often as little as up to 100000 Euro per year

which enables facility managers to do very little that is meaningful (e.g. lighting upgrades in

one building).

1. OWN SOURCE REVENUES

II

• The Capital Budget makes slightly more sense to use in that energy efficiency can become a

"line item" in the budget on an on-going basis. This would obviate the need to seek funding for

energy efficiency work on an annual basis. Unfortunately, the capital budget is usually seen as

the "hard infrastructure" funding method for roads, sewers and bridges, schools etc. to be

maintained and upgraded. This means that it typically does not fit into the Budget and

Administration Office's list of "vital" projects compared to more immediate needs.

• A strong bias against using internal revenues comes from the economic perspective. Using

either operating or capital budgeting for energy efficiency leads to a "crowding out" effect of

scarce internal capital when it could go to more pressing issues with more obvious political

rewards.1. OWN SOURCE REVENUES

III

• Another problem with internal budget allocations or using reserves, has to do with a

typical approach evident in local government; if any department saves money as a

result of energy efficiency upgrades, it will often be penalized with a reduced

budget at the sole discretion of the budget chief or comptroller. This does not

result in any motivation for that department to pursue strategic long-term savings since

the savings go directly to the comptroller's office! More thought should be spent on how

best to set up revolving-style funds that are capitalized with state or utility incentives or

internal seed capital that is replenished with energy savings.2. DIRECT BORROWING • Local governments can usually obtain long-term debt through the issuance of General Obligation Bonds (GOs). GOs represent the "full faith obligation" of the borrower, which can be the municipality, province, or region. The risk associated with GOs is that the issuer is at financial risk, it affects the balance sheet directly, and there is a chance that the proceeds of the bond issuance could go "stale" while a program lags in development. Finally, a GO bond issuance will take long lead time, and is costly for issuance fees, legal and financial advice, etc. • Loans are an obvious method for which municipalities could draw on available funds from eager financial institutions. Funders would look at the credit risk of the municipality and offer a rate of interest reflecting the cost of capital, swap costs to hedge interest risk, and a profit margin which varies depending on the lending institution, the municipal client, and the perceived risk. Loans are far more costly to local governments, and they put the municipal corporation directly at risk.

DEBT FINANCING

On balance sheet financing – corporate obligation appearing on the balance sheet

of the company’s financial statements

• Components of the cost of debt capital

• Base rate - the cost of capital to the bank to which a spread is added for the profit and risks to come up with a total lending rate for

the borrower.

• Spread - The difference between the costs of funds to the lending bank and the interest charged to borrowers.

• Handling fee – regular fee payable for the handling of the accounts

• Evaluation fee – fee payable for the initial evaluation of loan application

• Hold for available fee – fee for retaining the availability of the credit line.

• Grace period – period without any principal repayment obligation.

• Financial risks

• Country risks - General level of political, financial and economic uncertainty in a country affecting the value of loans or investments

in that country.

• Credit risks - The risk that an issuer of debt securities or a borrower may default on his obligations, or that the payment may not be

made on a negotiable instrument.

• Exchange rate risks - Also called currency risk, the risk of an investments value changing because of currency exchange rates.

• Interest rate risks - The risk that a security´s value changes due to a change in interest rates.

• Inflation risks - Also called purchasing-power risk, the risk that changes in the real return the investor will realize after adjusting for

inflation will be negative.

• Operating risk - the inherent or fundamental risk of a firm, without regard to financial risk. The risk that is created by operating

leverage.SECURITY BEHIND THE LOAN

• Collateral - Assets pledged as security under a loan to assure repayment of debt

obligations.

• Loan guarantee – partial guarantee facility with the objective of credit enhancement.

• Bank guarantees – A guarantee issued by one bank (Issuing Bank) to another bank

(Beneficiary) as security for general banking facilities given by the latter to a mutual

customer.

• Sovereign Guarantee - A governmental guarantee for fulfillment of obligations.

• Insurance

• In cashing rights - right for reclaiming repayments through access to bank accountsTHIRD PARTY FINANCING Perhaps the easiest way for municipalities to undertake energy efficiency projects (e.g. building energy retrofits) is to allow someone else to provide the capital and to take the financial risk (or guarantee the technical risk). With these alternative methods of financing, one can expect a higher cost to reflect the fact that the debt resides on someone else's balance sheet. Nonetheless, as it should become clear, the interest rate is only one factor among many that should be considered in determining the suitability of a project financing vehicle.

OFF BALANCE SHEET FINANCING

A corporate obligation that does not appear as a liability on the company’s

balance sheet

• Operational leasing – Rental in which the period of contract is less than the life of the equipment and

the lessor pays all maintenance and servicing costs.

• ESCO – Energy Service Company taking charge of (i) project identification, (ii) engineering, design, and

permitting, (iii) construction, (iv) operation and maintenance, (v) administration of billing, (vi) and

organization of financing for the above.

• Forfeiting - In case of forfeiting the supplier forgoes its accounts receivable to the benefit of the bank or

financial institute, which in return does assume all associated risks, and passes up its right of reclaims.

Forfeiting is used for medium and long term outstanding receivables or annuities.

• Public Private Partnership

• BOO(T) - Build, Own, Operate and Transfer of infrastructure projects, promoted and financed by the private sector, whereby

the promoter builds, owns and operates the project and only after a specified number of years does it transfers it the

ownership back to the public sector.

• Concession - An understanding between a company and the host government that specifies the rules under which the

company can provide service locally.FINANCING MECHANISM PUBLIC INTERNAL PERFORMANCE COMMITMENTS Besides the large private ESCO sector, Public Internal Performance Commitments (PICO) provide a department in the public administration who acts as a unit similar to an ESCO in function for another department. The ESCO department organises, finances and implements energy-efficiency improvements mostly through a fund made up of municipal money, and using existing know-how. This allows larger cost savings and implementation of less profitable projects, which would be ignored by a private ESCO. However, these projects lack the energy savings guarantee, because there are no sanction mechanisms within a single organisation (even though PICO includes saving targets). This model has been mainly implemented in Germany.

LEASE Leasing can be an attractive alternative to borrowing because the lease payments tend to be lower than the loan payments; it is commonly used for industrial equipment. The client (lessee) makes payments of principal and interest; the frequency of payments depends on the contract. The stream of income from the cost savings covers the lease payment. The ESCO can bid out and arrange an equipment lease-purchase agreement with a financing institution. If the ESCO is not affiliated to an equipment manufacturer or supplier, it can bid out, make suppliers competitive analysis and arrange the equipment. There are two major types of leases: capital and operating. Capital leases are instalment purchases of equipment. In a capital lease, the lessee owns and depreciates the equipment and may benefit from associated tax benefits. A capital asset and associated liability appears on the balance sheet. In operating lease the owner of the asset (lessor – the ESCO) owns the equipment and essentially rents it to the lessee for a fixed monthly fee; this is off-balance sheet financing source. It shifts the risk from the lessee to the lessor, but tends to be more expensive to the lessor. Unlike in capital lease, the lessor claims any tax benefits associated with the depreciation of the equipment. The non-appropriation clause means that the financing is not seen as debt.

FINANCING MECHANISM PUBLIC-PRIVATE PARTNERSHIPS I Cooperation between the municipality, local investors, and local citizens are deemed to be vital factors of success for realizing energy efficiency projects. The leadership of local governments usually have a crucial role in forging partnerships and pooling resources across the public and private sectors. As an enabler, municipalities have the capacity to steer policies in support of niche innovations that are new to the market as well as technologies that offer multiple social benefits, In this case the local authority uses a concession scheme under certain obligations. Public administration promotes the project and allows a private company to run it revolving the profits on the initial investment. This kind of contract are usually flexible.

FINANCING MECHANISM PUBLIC-PRIVATE PARTNERSHIPS II Bioenergy system – Enköping, Sweden A successful private–public partnership which grew from small scale operations to medium scale decentralized production system. A small scale wood chip boilers in 1979 for experiential learning purposes was built. This learning phase continued through the 1980s resulting in knowledge and skills build up for local energy companies. The growing concern of climate change resulted in the introduction of a number of policies to support bioenergy development including a carbon tax in the 1990s, which played a pivotal role in the commissioning of Enköping’s biofuels only medium scale CHP plant in 1994. About 40% of the total investment costs were subsidised by the Swedish Government. The plant had a capacity of 45MW of heat and 24 MW of electricity. The Enköping local government formed a company, which managed the plant in collaboration with another local private energy company.

FINANCING MECHANISM ENERGY COOPERATIVES Energy cooperatives play an important role for consumers who want to take action but are not confident or interested in acting alone. Different types of energy cooperatives exist. Some operate their own generation assets (such as wind or solar parks), others can act as aggregators or intermediaries, ensuring optimal operation and management of their members’ generation installations (such as roof-top PVs on houses), others can act as financial actors, helping to fund low-carbon renovation/construction works. They contribute to decarbonising electricity generation, they involve citizens who can easily understand and, hence, play a role in the energy market and help the energy transition.

EQUITY FINANCING

I

Cash or assets contributed by the project sponsors

• Own equity

• Cash and cash equivalents

• In kind contribution – Transfer of non-cash input like tangible or intangible assets into a venture

which can be given a cash value.

• Goodwill - Excess of the purchase price over the fair market value of the net assets acquired under

the purchase method of accounting.

• Components of the cost of equity capital

• Risk free rate - The yield on long-term government bonds.

• The market risk premium - represents the amount by which returns from equity investments in

publicly traded markets, represented by a market proxy, have exceeded risk free returns.

• Small stock risk premium - Historical smaller companies have been viewed as riskier than larger

companies. Investors are compensated for taking on this additional risk by higher returns

provided by small companies over the long term.

• Company specific risk premium - Additional risk for which investors are compensated.

Country risk premium represents the additional risk for which investors must be compensated when investing

in a developing country.EQUITY FINANCING

II

• External equity by investors

• Private equity in form of venture capital

• Exit – Sale of equity interest in a company to management, or other external

investor.

• Management buy out - Leveraged buyout whereby the acquiring group is led by

the firms management.

• Preferred shares - Preferred shares give investors a fixed dividend from the

company's earnings. And more importantly: preferred shareholders get paid

before common shareholders.

• Vendor Finance - Debt provided by a supplier of equipment or services to

the project company.

• Mezzanine financing - A hybrid of debt and equity financing generally

used to finance the expansion of existing companies. The debt element is

subordinated to other loans without any pledges on assets, while it is also

holding a conversion-to-equity element.OTHER FINANCING MECHANISMS

Developing EE financial products and creating demand for EE finance

• Vendor financing

• Energy Efficient Mortgage

• On-bill financingOTHER FINANCING MECHANISMS VENDOR FINANCING Vendor financing occurs when a financier provides a vendor with capital to enable them to offer "point of sale" financing for their equipment. Under a vendor financing scheme there are two types of arrangements: one between the vendor and the financier; and the other between the vendor and the customer. The former defines the terms that can be offered to the customer such as rates, length of term and necessary documentation. The vendor/customer agreement defines the repayment terms of the loan. For EE equipment these agreements can be structured such as that the customer payments are lower than the value of energy savings associated with the new equipment.

OTHER FINANCING MECHANISMS ENERGY EFFICIENCY MORTGAGE An EEM is a reduced rate mortgage that credits the energy efficiency of the building in the mortgage itself. There are two types of energy mortgages: Energy Improvement Mortgage (EIM) - finances the energy upgrades of an existing home in the mortgage loan using monthly energy savings, and Energy Efficient Mortgage (EEM) - uses the energy savings from a new energy efficient home to increase the home buying power of consumers and capitalizes the energy savings in the appraisal. An EIM is used to purchase existing homes that will have an energy efficiency improvement made. In the US both EEMs and EIMs require a home energy rating to provide the lender with the estimated energy savings.

OTHER FINANCING MECHANISMS ON BILL FINANCING Integrating loan payments with energy bills and allowing utilities to cut off energy supply to defaulting customers has the potential to both lower collection costs and enhance credit quality of the financing scheme, thereby lowering financing costs. Payment via utility bill reduces risk of credit default and lowers collection risk. Energy suppliers collect the repayment of a loan through energy bills. It leverages the relationship, which exists between a utility and its customer in order to facilitate access to funding for sustainable energy investments

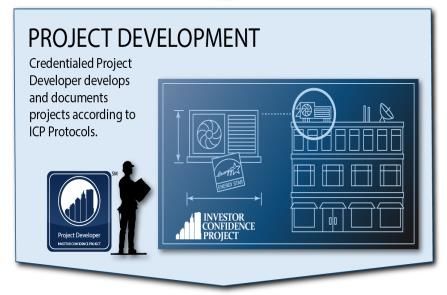

CREATING BANKABLE PROJECTS What is a “bankable” project? • it is a clearly documented economically viable project. Building a bankable project starts with sorting out the pieces that make a project economically attractive. • The first step is to examine the key components and make sure each aspect is properly assessed and the plan to effectively manage that aspect is clearly presented. Each component carries a risk factor, and each risk factor carries a price tag. • ESCOs know how to assess the components e.g. customer pre-qualification, audit quality, equipment selection and installation, and savings verification, and how to package them into a project that can be financed.

ENERGY AUDIT QUALITY A stand and energy audit with its “snap shot” of current conditions in not good enough for performance contracting. These audits typically assume present conditions will prevail for the life of the project. When an ESCO bets money on predicted future savings, these assumptions must be tested through an careful risk assessment procedure. Only an investment grade audit that adds specific risk appraisals to the standard nameplate/run calculations will meet performance contracting needs. In recent years, energy engineers have learned to look at facility and mechanical conditions and determine the ability of the remaining equipment and energy consuming subsystems to accept the recommended measures. An investment grade audit (IGA) goes beyond these engineering skills and requires the art of assessing people; the level of commitment of management to the project, the extent to which the occupants are informed and supportive as well as the O”&M staff’s abilities, manpower depth and attitude. A key aspect of quality IGA is a carefully detailed base year with the average energy consumed over several years and the current operating conditions, which affect that consumption. The ESCO that consistently delivers a quality IGA, which in turn accurately predicts potential savings, builds a track record that financiers find very heart warming. A good IGA is at the heart of the bankable project. When the total project plan is wrapped around a quality IGA and delivered by an ESCO, who can back its predictions with a solid history of successful projects, financiers have every reason to smile.

SAVINGS VERIFICATION When money changes hands based on the level of savings achieved, all parties should be comfortable with how the achieved savings are verified and attributed to the work performed by the ESCO. Under the financiers’ general guidance, the ESCO and owner should jointly decide on the level of verification and attribution necessary. It id basically a case of cost vs. accuracy, and it is possible to reach the point of diminishing returns rather quickly. With the verification burden becoming so great that a measure is no longer economically viable. The financier wants some sense that the projects benefits are measurable and they are measured through accepted protocols. Too often verification procedures are basically passive, a negative drain on the cash flow, and the investors are not interested in funding a gold plated M&V approach that offers little or no return on investment.

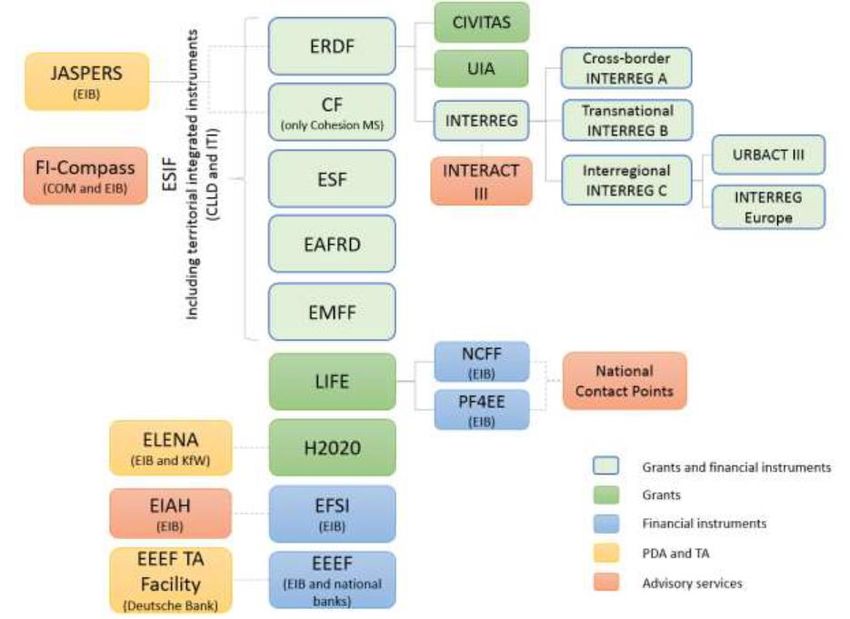

FINANCING SOURCES

Some of existing climate and energy

efficiency finance instruments available

in the EU are:

• ELENA KfW

• EEEF

• HORIZON 2020FINANCING SOURCES ELENA KfW ELENA KfW is a financial scheme that supports local and regional authorities and other public bodies. The focus areas are energy efficiency in public and private buildings and street lighting, integrated renewable energy sources (RES), energy efficiency and integrated RES in urban transport including freight logistics in urban areas, local infrastructures for energy efficiency and municipal waste-to-energy projects. KfW-ELENA consists of two elements, ELENA grant from the European Commission for Project Development Services and global loans to local participating financial intermediaries (PFIs) in order to target smaller investments (volume up to EUR 50 million).

FINANCING SOURCES European energy efficiency fund (EEEF) Following the European Commission’s technical assistance facility managed by the European Energy Efficiency Fund (EEEF), the Fund has now set up a new assistance scheme to support ambitious public beneficiaries in developing bankable sustainable energy investment programmes. These projects shall relate to the energy efficiency sector, small-scale renewable energy and/or urban public transport. The technical assistance facility aims to bridge the gap between sustainable energy plans and real investments through supporting all activities necessary to prepare investments into sustainable energy projects.

FINANCING SOURCES European energy efficiency fund (EEEF) Eligible applicants: regions, city councils, universities, public hospitals and other public entities located in the Member States of the European Union. Sectors covered: energy efficiency, small-scale renewable energy and/or public urban transport. While the supported activities are: feasibility studies, energy audits, evaluation of the economic viability of the investments and legal support.

THE BUY-IN; THE BUY-DOWN As a final cornerstone to this financing business, owner should not overlook the value of taking an equity position in the project. It is a way to get non–energy related projects incorporated, and/or reduce ESCO and financiers risks. A little owner equity can be a powerful leveraging force and make a bigger project possible. Financier’s guidance should be available to the ESCO and owner as they develop a project. The financier’s due diligence, in the end, is the ESCO’s and owner’s best guarantee that they have a double project. In today’s market, if an energy efficiency project can’t get financed, the first step is to rethink the project!

Joint Research Centre (JRC)

FINANCING MECHANISMS

Most common financing mechanisms used to finance

investments mainly in RES and EE:

• Soft loans

• Leasing

• Energy service company (ESCO)

• Public Internal Performance

Commitment (PICO)

• Public-Private Partnerships

• Energy cooperatives

• Third party financing schemesFINANCING MECHANISM SOFT LOANS Soft loan schemes which offer below market rates and longer payback periods, and loan guarantees, which provides buffer by first losses of non-payment, are mechanisms whereby public funding facilitates/triggers investments in EPC. They give long-term financial coverage to help bridge the pre-commercialisation financing gap for EE projects by direct subsidies on interest payments, by risk premiums (e.g. an IFI or a state can guarantee a certain amount of loans), or by capital gains to a revolving fund. They are commonly used for energy efficiency measures.

FINANCING MECHANISM LEASING The common way of the market of dealing with the barrier of initial cost is the leasing. Leasing is a way of obtaining the right to use an asset (rather than the possession of this asset). In many markets finance leasing can be used for EE equipment, even when the equipment lacks collateral value. There are two major types of leases: capital and operating. The former usually concerns shorter term leases, the latter transfer the risk to the lessee. Capital leases are instalment purchases of equipment. A capital asset and associated liability appears on the balance sheet. In operating leases the owner of the asset owns the equipment and essentially rents it to the lessee for a fixed monthly fee. This is an off-balance sheet financing source.

FINANCING MECHANISM ENERGY SERVICE COMPANY (ESCO) I Energy Services Companies (ESCO) usually finance the energy-saving projects without any up- front investment costs for the local authority. The investment costs are recovered and a profit is made from the energy savings achieved during the contract period. Often, the ESCO offers a performance guarantee which can be shaped in several forms. The guarantee can revolve around the actual flow of energy savings from a retrofit project. Alternatively, the guarantee can stipulate that the energy savings will be sufficient to repay monthly debt service costs. The key benefit to the building owner is the removal of project non-performance risk, while keeping the operating costs at an affordable level.

FINANCING MECHANISM ENERGY SERVICE COMPANY (ESCO) II Energy Performance Contracting (EPC) is a contractual arrangement between a beneficiary and an Energy Service Company (ESCO) about energy efficiency improvements or renewables installations. Normally an ESCO implements the measures and offers the know-how and monitoring during the whole term of the contract. Essentially the ESCO will not receive its payment unless the project delivers energy savings/production as expected. Financing is arranged so that the energy savings cover the cost of the contractor's services and the investment cost of the new and more energy efficient equipment. The repayment options are negotiable. Measurements and verification of the energy and savings produced are a critical point.

FINANCING SOURCES Horizon 2020 (Call EE22 – PDA) The beneficiaries of the program are local and regional authorities, public bodies, private infrastructure operators, ESCOs and SMEs. The program focuses on areas regarding public and private building stocks, public lighting, district heating and cooling networks, urban transport, energy efficiency in industries and services and investments in RES. It supports programs above 7,5 to 50 million euros maximum.

No shortage of money

Mechanisms for financing EE

• Own capital

• Loans/mortgages – residential/commercial buildings

• Leasing

• Specialised energy efficiency Funds

• Property funds specialising in energy efficient buildings

• Financing of energy service contracts through ESCOs and Super ESCOs

• EPC / Chauffage / ESA / MESA / MEETS / LaaS / P4P

• On Bill Recovery (OBR)

• Property Assessed Clean Energy (PACE)

• Guarantee funds

• Forfaiting funds

• Green bonds

• YieldCosChallenges to financing energy efficiency • Small projects • Lack of well developed bankable projects • Lack of standardisation • Hard to measure • Uncertain results – the design gap • Hard to meter • Hard to monetize • Complex contract forms • Lack of capacity in the financial sector / demand side / supply side • Split incentives • Low energy prices • Institutional barriers • etc etc. These apply to all sources of finance including balance sheet self-funding

The project life cycle

Development Underwriting Invest Performance

Period Period Period

High Risk

Low

Risk

Development finance Implementation finance

- Equity - Debt

- Grant (PDA)

Scarce AbundantStandardisation

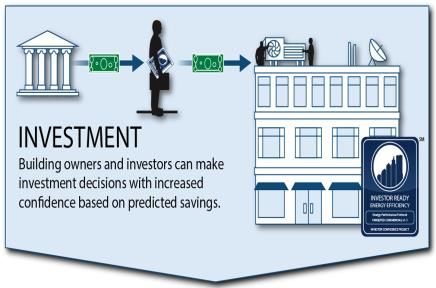

An international framework for reducing owner and

investor risk, lowering due diligence costs, increasing

certainty of savings achievement and enabling

aggregation.

Investor Ready Energy Efficiency™ is the

quality mark like BREEAM or LEED but

for an ENERGY EFFICIENCY Standardisation

RETROFIT PROJECT

Ensures transparency, consistency and trust-worthiness through best

practice and independent verification.

Available across EU for buildings, industry, street lighting and

district energy projects.

These projects have received funding from the European Union’s Horizon 2020 research and innovation programme under grant agreements No 649836 and No. 754056.

The sole responsibility for the content of this presentation lies with the authors. It does not necessarily reflect the opinion of the European Union. Neither the EASME nor the European Commission are responsible for any use that may be made of the information contained therein .The Investor Ready Energy EfficiencyTM

process

Development Underwriting Invest Performance

Period Period PeriodYou can also read