The future realities and innovations for a sustainable energy value chain - Paul Vermeulen Manager DSM and SSM City Power Johannesburg 8 March ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The future realities and innovations for a sustainable energy value chain Paul Vermeulen Manager DSM and SSM City Power Johannesburg 8 March 2018

Presentation theme

Municipal revenues are declining due

to unaffordability of electricity, system

inefficiencies, technology advancement

and slow economic growth - negatively

impacting service delivery.

How can this be turned around and

how does the energy transition provide

opportunities for municipalities to

explore other sources of income and

ensure revenue sustainability? What does our future hold?

2

What’s wrong with the cash cow?

By 2014, it became apparent that electricity’s

Structural core business was unable to generate a surplus

changes to without including grants and subsidies.....

the energy

Sustained

system –

economic Projected demand growth

uptake of

downturn

alternatives

?

from 2008

Energy ~ 25 TWh

Spiralling tariff demand

increases, Peak

unprecedented ~ 12.5 2

demand

TWh 6000 MW

customer

Peak

investments in EE demand 1

2800 MW

2014 time (2034)

(years)

Affordability issues Traditional EDI planning is based on

continuous demand growth – perhaps

a thing of the past? 3

‘As is’ Municipal Distributor Value Chain

Provide Procure Transport Dispense and Collect

Distribution energy via networks Record Revenues

Infrastructure

• Maintain • Procure energy • Operate • Operate and • Vend to pre-

distribution from Eskom networks maintain pre-paid paid customers

infrastructure • (Procure energy • Monitor and metering systems • Bill and collect

• Build new from IPPs e.g. Control power • Operate and revenues from

infrastructure Kelvin) flows maintain post post-paid

• Refurbish aged • Restore outages paid metering customers

infrastructure systems

4

Just how ‘dead’ is the traditional electricity business model?

The NERSA benchmark regulatory methodology excludes any effects related to:

• Cross-subsidies from commercial sector to residential sector as per the Electricity Pricing

Policy

• Insurance and the actual costs of vandalism and theft (particularly copper theft)

5

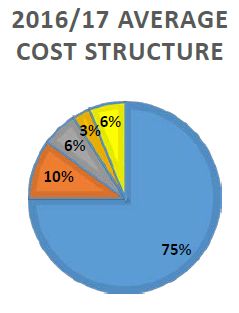

Shrinking Gross Revenue Margins

Breakdown of key figures within the NERSA 'municipal benchmark' regulatory methodology

R million R million

NERSA regulated sales margin 1.62 Regulated Revenue Allowed R million 1620 This

ss

Hypothetical Bulk Purchases 1000 Total Regulated Costs 1250 busine

is

Total regulated costs 1250 Gross Revenue Potential 370 model

Regulated Cost Breakdown Allowed losses in

s

Purchases, 75% of total 1000 Permitted System Losses Technical, 10% R million 162

distres

Salaries and Wages, 10% 125 Permitted System Losses non Technical, 5% R million 81

Repairs, 6% 75 Actual Surplus -Gross revenue less 'allowed losses' 127

Capital Charges, 3% 37.5 Gross surplus permitted by NERSA, 15% - R million 243

Other Costs, 6% 75 But this includes allowed losses?

Every 1% increase in non-technical losses above the allowed 5%, destroys 12,75% of the surplus!

As the cost of ‘Eskom product’ has increased, so has the cost of cross-subsidy to the poor. This erosion of surplus is not factored into the NERSA

benchmarking model.

The theft of copper cannot be considered as part of the repairs and maintenance allocation – we cannot consider this business as usual, with ‘an

allocation’ for these syndicates.

A transition from benchmark regulation to proper cost based regulation is needed

6

There’s no room for any inefficiencies in the system!

Provide Procure Transport Dispense and Collect

Distribution energy via networks Record Revenues

Infrastructure

• Inadequate substation and • Non-verification of bulk • Excessive unplanned • Illegal service connections • Unbilled customers

network maintenance purchases with check outages • Unmetered Customers • Billing estimation issues

• Continuous recovery from theft metering • Network reliability issues • Bypassed meters • Incorrect customer data

and vandalism • Unnecessary NMD - overloading • Incorrectly metered • Incorrect PoD technical data

• Backlog in refurbishment of penalties • Unmanaged technical customers • Account tampering

aged networks • Increasing peak period losses and reactive • Incorrect tariff migrations • Unending customer Queries

• CAPEX – Delays in build of new energy volumes energy losses • Meter tampering • Legal Queries

bulk supply networks • Unmanaged evening peak • Inadequate monitoring • Incorrect reversals

• CAPEX – INEP delays to demand and control systems

reticulate townships • Effectively a prohibition • Ineffective fault

on alternative, cheaper reporting and restoration

bulk energy purchases - systems

IPPs

These are presently by far the greater threats to business

7

Declining sales volumes vs. increasing customer numbers

The issue of tariff decoupling -

Since 2009, City Power has seen a full 10% reduction in

kWh sales, from 13 100 GWh down to 11 780 GWh per

annum.

Since 2002, City Power has connected up 60 000 new

customers (largely in the low income residential sector)

Tariffs that are based purely on

Individual customers are becoming energy efficient but

energy (R/kWh charges) will result in

still rely on the convenience of the grid for their energy

declining revenues

needs

f

Tariffs that include a defined (fixed) Tarif s

The metro economy is becoming less energy ture

charge component to be connected Struc t

intensive while businesses still need mus

to the grid and a separate energy ge

a reliable grid to prosper chan

component are sustainable

8

The New Cousin – Distributed Generation

Distributed, particularly PV generation, is blamed for the demise while in reality

Embedded Generation has many unseen benefits –

ly

False of • Behind the meter commercial PV systems do reduce utility sales volumes to

ed

accus part these customers - but they provide a way for customers to reduce their energy

being e

of th costs, thereby gain a competitive edge and stay in Jo’burg

!

Gang

• Residential PV systems reduce day time kwh volumes but also export valuable

day time energy into the grid, available for sale to neighbors

• Distributed energy sources include peaking plant and energy storage that will

reduce overload at intake points and congested distribution networks

• All distributed energy sources reduce distribution technical losses and can at the

same time alleviate capacity bottlenecks

• Customers want to use the grid to ‘wheel’ and trade energy and are willing to

pay for the service

This is where new business and revenues lie

9

Energy storage – Another New Cousin

City Power

Electrification

• Each year a greater proportion of peaky residential load and self- completed over the

dispatched renewable energy is being connected to our grids. Year years

2013/14 2,151

• The effect is a deteriorating load factor, leading to a higher cost of Eskom 2014/15 2,238

supply. 2015/16 5,438

2016/17 4,850

• DSM tools are needed to contain these costs 2017/18 850

• We require 2 key ‘behind the Eskom meter’ grid management tools to do

this: City Power has to date

– Access to ‘dispatchable’ generation authorized over 15 MW

of private PV power

– Control of flexible loads connected to its grids.

• Energy storage fits the bill as both a flexible load and as a generation

source.

• Where the storage facilities are located is almost irrelevant. As long

as the municipal distributor is able to control the charge and

discharge cycles, the benefits will be realized.

10Municipal C&I Customers - Taxed to death, three times

Municipalities demand a surplus from the Municipal Electricity Distribution Industry to fund other

municipal services.

(Note – Where Eskom distributes for the City of Joburg in Sandton and Soweto – about 25% of the total

power distributed - they are not required to make a surplus contribution to the City)

The Electricity Pricing Policy requires distributors to protect the poor by creating subsidies for low income

residential customers from the commercial and industrial tariffs, the customer segment that is the only

source of any operating surplus

Eskom levies an ‘urban low voltage subsidy’ of R 12,48 per kVA per month on all customers taking power at

above 66kV, including municipal distributors, to meet their own EPP cross-subsidy obligations

Municipal Business Tariff = Eskom base cost + Municipal Surplus + Subsidy for poor + Eskom subsidy for poor

This is taxing the input to the City’s economy rather than the output. Something needs to change!

11An unsustainable SA Electricity Industry Structure

Eskom Generation -

Large coal fleet, one

REIPPP – Green COGTA

Energy nuclear, some hydro

Department of

DPE Cooperative Governance

Department of NERSA Regulates Eskom Transmission

this part of the and Traditional Affairs

Public (Incorporates the System

*Required to

industry using Operator and Single Buyer

Enterprises . generate a

Eskom Retail Tariff Office )

surplus for SALGA

Control over and Structural South African Local Government

SoEs such as Eskom Distribution municipalities.

Adjustment Association

Eskom Methodology Retail Sales

National *170

Eskom C&I Smaller

Treasury PFMA *8 other

Customers Eskom *City Power Munics NERSA Regulates

Compact with Metro s this part of the

Residential Metro (SoC)

Eskom Customers Distributor industry using a

municipal

City of Johannesburg benchmarking

methodology

National Municipal Municipal

Not required to generate

Nuclear a surplus for the City Residential C&I

Regulator Customer Customers

DoE – Department of Energy has oversight over the whole industry 12Reassessing the value of the grid

g r id Instant load balancing services

The Night time backup service for natural energy systems

can ly A marketplace for distributed generation investors to sell surpluses

le ss

seam ide: Enhanced security of supply where islanding facilities are combined with

prov energy storage

Is our future a transition from a commodity sales based business to a commodity transport based

business, or somewhere in between?

How much of the business is there to provide product – just energy in the form of kWhs?

How much of the business is there to provide network services – access into or out of an energy

highway?

The weighting and ratio of fixed network charges to variable charges of future

tariffs will depend on how these questions are answered

13Right-sizing the businesses

We have 177 municipal electricity distributors ranging from small – less than 20 MW of load to large

metros distributing 1000+ MW

The smaller municipalities do not have a sufficiently large revenue base to employ the necessary

engineering skills to operate, maintain and expand their networks as they should

Some municipalities do not have a favorable customer mix – too few Commercial and Industrial

customers with a large proportion of Low Income Residential customers simply leads to higher

prices all around and migration of businesses

The distribution industry needs to be consolidated into distribution companies

that are big enough to be regional players, including Eskom distribution.

These companies can pay servitude rentals to municipalities (Portland example)

14Small Scale Embedded Generation tariff and cost of PV

NERSA Approved for City

Power, 2017/18 on an Those willing to invest

must be on the

interim basis residential TOU tariff

Cannot be on a pre-

paid tariff

Those willing to ‘Net Billing’ applies Surplus energy put to

invest must be on a 15 MW already the grid is credited at

conventional tariff commissioned 43,77 c/kWh The Levelized Cost

Cannot be on a pre- Of Energy (LCOE)

paid tariff of rooftop PV

Surplus energy put to systems is around

the grid is credited at R1,12 per kWh

36,96 c/kWh The present average cost of

Eskom power is R0,90 per and will stay fixed

kWh and is likely to escalate at that price for

at above inflation rates the next 20 years

*Energy only = R0,71 per kWh

15The changing, but stuck energy mix

• SSEG tariffs allow City Power to

TREASURY procure surplus residential PV

!

Eskom Generation -

Large coal fleet, one Provides tax incentives for energy at 43 cents per kWh

REIPPP – Green

nuclear, some hydro EE and RE

Energy • Eskom energy now costs 90 cents

SALGA and CITIES per kWh (2018/19 may be R1,08)

½! Eskom Transmission

(Incorporates the System ! Recognize climate change issues • The margin of selling surplus PV

Operator and Single Buyer energy is 27 c/kWh better than

Office ) selling Eskom power

NERSA

Eskom Distribution

Retail Sales

! Approved SSEG tariffs for several

municipalities

• Without storage, 100 000 affluent

residential PV customers could

contribute 700 MWh of cheap

energy towards the 29 000 MWh

û

*170

Smaller

the city requires each day.

Eskom C&I

! Customers Eskom *City Power

*8 other

Metro s

Munics • This would be a fair contribution

û

Residential Metro (SoC) to the cross-subsidy needed to

Customers Distributor support the poorer residential

le

Doub o n sector

City of Johannesburg

i s ru pti

D • Munics have been told not to

Municipal Municipal for bother applying for generating

Residential C&I

u n ics! licenses for their own PV farms, as

Customer Customers M the Minister has not made a

! !

determination on the matter

• Is a determination necessary? 16New service offerings where the grid is key

New value proposition from grid operators is to provide

backup supply and seamless load balancing services

From a national While storage cost

systems point of Grid provides the DG investor a marketplace to trade is still relatively

view, the most their surplus energy and optimize their investment. Low high, the EDI has a

efficient green cost surplus alleviates cross-subsidy burden small window of

energy solution opportunity to

includes the Grid enables Green Energy trading and new municipal convince customers

existing grid – AC revenues from the ‘transport’ of energy of the value of the

or DC An element of storage added to a grid tied renewable grid

energy system is of benefit to the investor as well as the

municipal distributor

Avail the grid as a market for all forms of energy

Support for trading or energy offsetting across the grid

Introduce time dependent use of system charges

Include the low income sector in the PV revolution (e.g. Mauritius)

Apply storage to effect enhanced security of supply

Deliberate islanding to secure supply

Offsetting energy from home to office for EVs

17De-dumb ‘Smart’ systems – drive appropriate technology

What is smart about meters if they cannot support new tariff structures we need, like -

• Fixed charge (network) and variable (energy) charges on a pre-paid basis?

• Support for time of use tariffs on a pre paid metering basis?

• Support for FBE energy packages with ‘top-up’ options in the case of the low income sector?

The South African EDI was instrumental in pioneering the original pre-

paid metering systems

We now need more sophisticated pre-paid systems and must define

the market once again

18Conclusion - some likely additions and changes

Provide

Distribution &

Procure Transport Dispense and Collect

Generation

energy via networks Record Revenues

Infrastructure

• Add energy

• Focus on Eskom • Avail the grid for • Offer new ‘top- • Modernize

storage

role as supplier of energy trading up’ tariff revenue

facilities

last resort • Create super packages for low collection

• Venture into

• Accommodate secure key income systems

DC distribution

“prosumer” customer zones residential sector • Utilize block-

and micro-grids

surpluses with islanded • Enhance chain

• Build a portfolio of storage facilities metering to technology for

partner IPPs • Promote the support trading trading

• Invest in own value of the grid • Convert

renewable energy to customers residential sector

plant to TOU tariffs,

with home

automation 19Thank you, from the City of Johannesburg

20You can also read