The global lithium-ion battery race and Europe's role in it - Presentation at ITIF, Washington DC, 7 Nov 2018 Tobias S Schmidt, Energy Politics ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The global lithium-ion battery race and Europe’s role in it Presentation at ITIF, Washington DC, 7 Nov 2018 Tobias S Schmidt, Energy Politics Group, ETH Zurich

D GESS

Agenda

▪ Why is it a race to lithium-ion?

▪ What is Europe’s position in this race?

EPG | Energy Politics Group | 2

D GESS

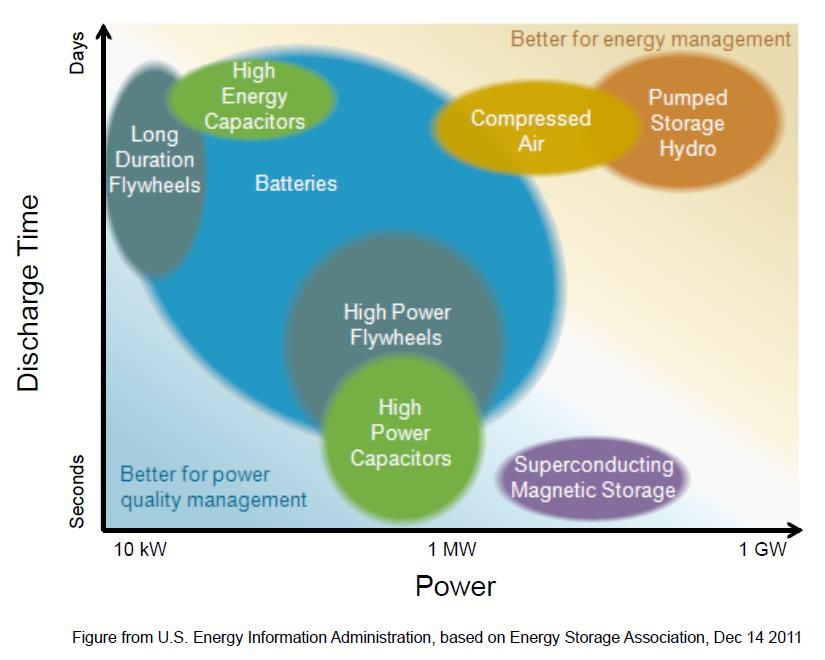

Why lithium-ion (as opposed to other storage techs)?

Source: Kalhammer et al. 2007

+ high round-trip efficiency + government support (US, Japan, Korea, China)

+ low-temperature

+ relatively safe

EPG | Energy Politics Group | 3

D GESS

Historic demand for and innovation in lithium-ion batteries

Historic

Hist Source: Battke, Schmidt, Stollenwerk, Hoffmann. Research Policy (2016)

http://dx.doi.org/10.1016/j.respol.2015.06.014

oric

EPG | Energy Politics Group | 4

D GESS

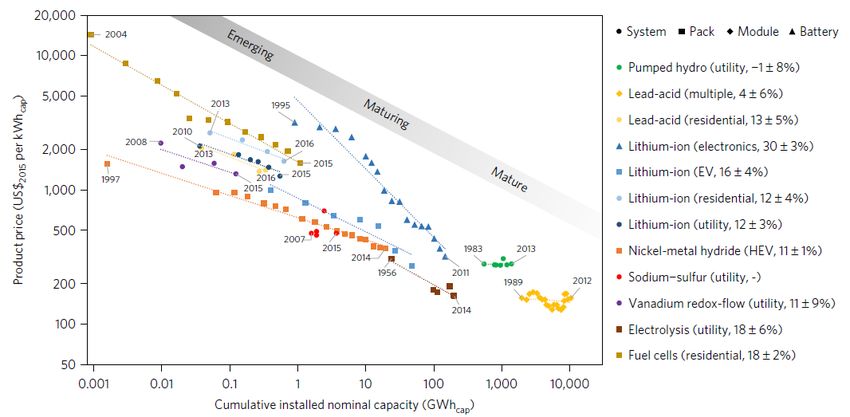

Lithium-ion batteries have experienced massive cost reductions and will see more

in the future

Source: O. Schmidt et al. (2017), Nature Energy http://dx.doi.org/10.1038/nenergy.2017.110

EPG | Energy Politics Group | 5

D GESS

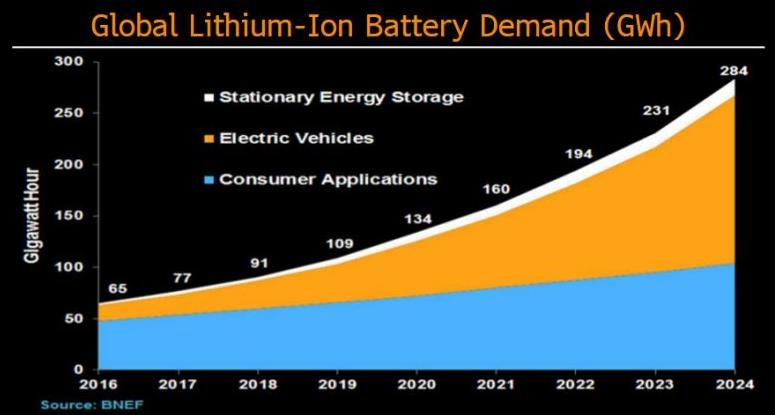

Future demand for Lithium-ion batteries will come from three main markets

EPG | Energy Politics Group | 6

D GESS

Rough cost composition of an EV and its battery pack (as of 2017)

100%

Pack: 40% 60%

Cell: 30%

10%

12%

8% 8%

2%

Cathode Anode other Cell Packaging Integration, EV

materials Manufacturing rest of vehicle

Source: EPG/ETH Zurich, based on 2017 market numbers

EPG | Energy Politics Group | 7

D GESS

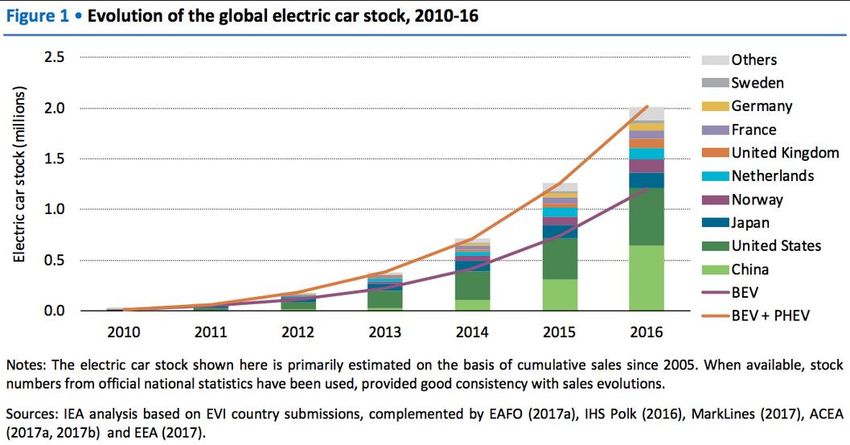

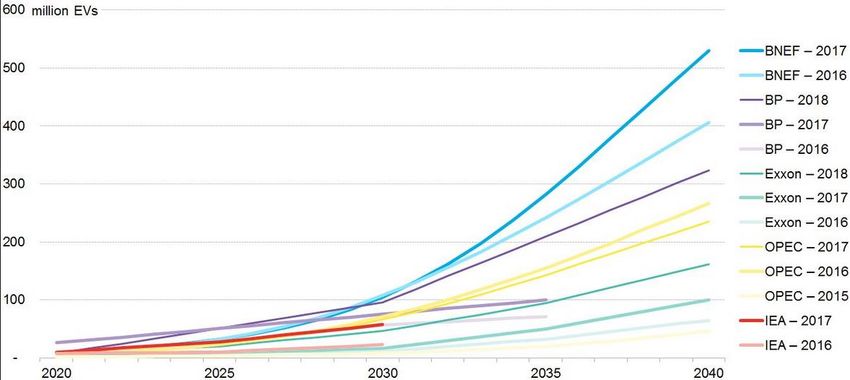

The market for BEVs (past and outlook)

Electric vehicle sales (millions)

Source: BNEF

EPG | Energy Politics Group | 8

D GESS

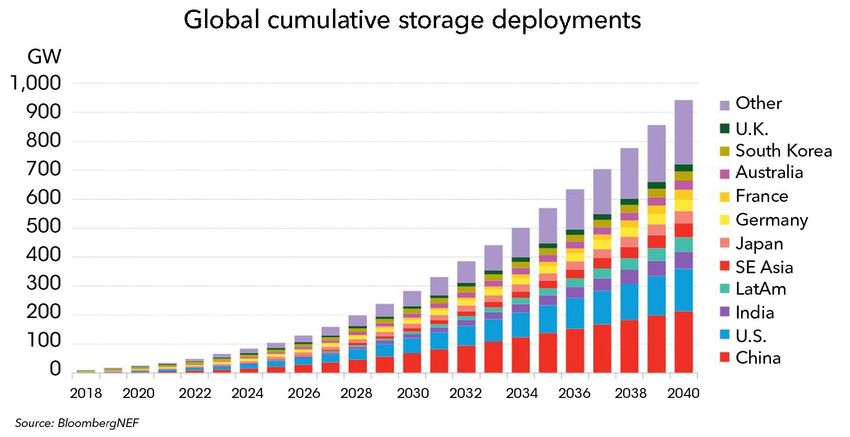

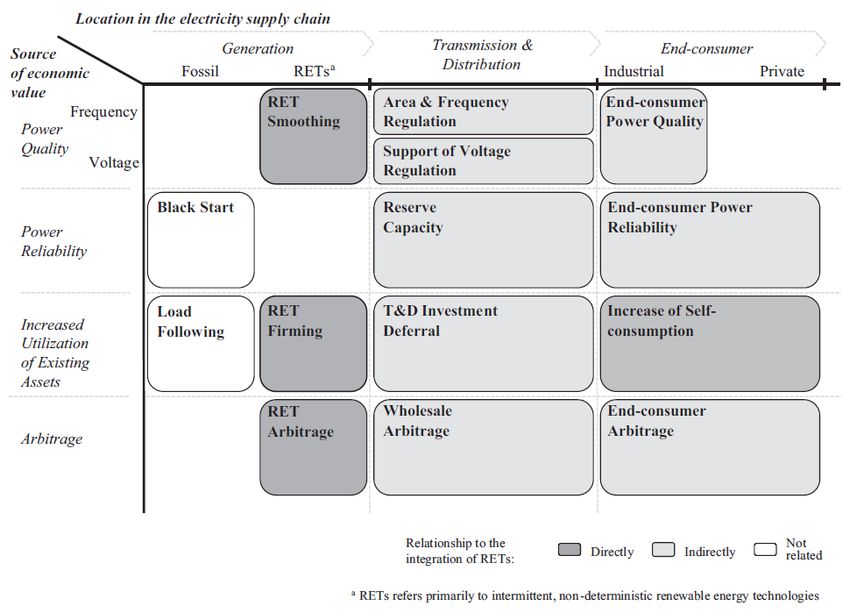

Also stationary storage market is expected to grow massively, where it can create

value in many applications

Stationary storage applications along electricity supply chain and by type of value creation

BNEF: stationary storage (without PHS) is

a USD 1.2 trillion market till 2040

Source: Battke & Schmidt, Applied Energy (2015)

Source: BNEF 2018, https://about.bnef.com/blog/energy-storage-1-2-trillion- http://dx.doi.org/10.1016/j.apenergy.2015.06.010

investment-opportunit§y-2040/?sf94588529=1

EPG | Energy Politics Group | 9

D GESS

Lithium-ion batteries “eat into” stationary storage market

Preliminary results – do not cite or distribute

Technology market shares

[Newly-built electricity storage projects]

Low EV demand (5% CAGR) High EV demand (32% CAGR)

100% 100%

8h duration –

1 cycle/day

50% 50%

Utility-scale

0% 0%

2018 2022 2026 2030 2018 2022 2026 2030

100% 100%

1.75 cycle/day

4h duration –

50% 50%

0% 0%

2018 2022 2026 2030 2018 2022 2026 2030

Li-ion (NMC) Li-ion (NCA) Li-ion (LFP) VRLA Flow Battery PHS

Source: EPG/ETH Zurich

EPG | Energy Politics Group | 10D GESS

Agenda

▪ Why is it a race to lithium-ion?

▪ What is Europe’s position in this race?

EPG | Energy Politics Group | 11D GESS

Europe’s current position: pieces of the puzzle do not (yet) match

• Market share in cell manufacturing thus far attempts have failed (TerraE) or are faring; buy in from car industry only picking up now (it seems)

Source: Beuse, Schmidt, Wood, Science (2018) EPG | Energy Politics Group | 12D GESS

Three questions need to be asked (and answered)

1) Is a battery cell a commodity- 2) Is it possible to leapfrog? 3) How to catch up?

like component, to simply

source on the market?

Our opinion: Our opinion: Our opinion:

• Core component (strong • Hard if not impossible, as next • Generally it is possible to catch

influence on vehicle design) generation requires a lot of tacit up (see Korea/China from Japan)

• Strategic component (better cell knowledge in design and • Waiting only widens gap

makes a better EV) production • Airbus is not a good role model

• Complex component, requiring • Gaining tacit knowledge requires • We recommend a “technology-

tacit knowledge to design experience with design, smart” policy

• Market power might not be as production and use of the

clear as with other car technology

component suppliers • Complex industry value chains

involved, with strong need for

interaction

Source: Beuse, Schmidt, Wood, Science (2018)

EPG | Energy Politics Group | 13D GESS

Our research aims to understand technology differences.

Policy should be “technology-smart” in order to be cost effective

What are elements of a “technology-smart” ...complex to design technologies:

catching

100%

up strategy?

80%

Wind 1) Interactions with downstream

60%

Wind 40%

Product

High activities

Process

1. Make production in Europe and partnerships

20%

0%

2) TransferWind turbines

of human capital Lithium- ion batteries

1991 1992 1995 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

with European firms attractive 3) Stable home market (to get

100% constant user feedback and new

80%

60%

PV Product Design users)

Solar PV

2. Create

40%

a large and predictable home

Combination

market complexity

20% Process

...complex to manufacture

(EV targets; more stringent caps of fleet

0%

technologies:

emission standards)

100% 1) Interactions with upstream

80%

60%

Li-ion Product Micro hydro plants activities Solar PV

Lithium-ion Combination Low

3. Only 40%

if enough learning and catching-up Process

has 2) Transfer of capital goods and

20%

(tacit) integration knowledge

taken place, create incentive for a “European

0%

3) Increasing (global) demand

cell”

Low High

Manufacturing

complexity

Relevant factors for catching up in…

Sources: Beuse, Schmidt, Wood, Science (2018); Schmidt & Huenteler, Global Env. Change

EPG | Energy Politics Group (2016); Malhotra, Schmidt, Huenteler; AAAS conference (2017) | 14D GESS

Thanks for your attention!

web: www.epg.ethz.ch

twitter: ETH_EPG

EPG | Energy Politics Group | 15You can also read