The March 2020 episode of market turmoil and lessons for future financial stability

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The March 2020 episode of market turmoil and

lessons for future financial stability

Anil Kashyap

University of Chicago Booth School of Business

July 7, 2020

The views here are my own and not necessarily shared by the Bank of England’s

Financial Policy Committee. Thanks to Geoff Coppins, Lee Foulger and Bernat Gaul-

Ricart for helpful conversations on these matters.

Outline • Dislocations during March • Interlinkages across markets • Policy implications

The speed and size of sales of US Treasuries challenged dealers’

intermediation capacity…

US equity prices and bond yields Primary dealer net inventories of US Treasuries

Per cent UST 10y yield (RHS) Basis

S&P 500 (LHS) points

9 Mar 15 Mar

5 10

0 -10

-5 -30

-10 -50

-15 -70

-20 -90

-25 -110

-30 -130

-35 -150

Jan 20 Feb 20 Mar 20 Apr 20 May 20 Jun 20

Sources: Bloomberg Finance L.P. and Bank calculations. Displayed as changes year to date. The aggregate net inventory (long minus short) of primary dealers, maturity weighted by multiplying the

net position in dollars by the number of years to the centre of each reported maturity class, to roughly

reflect the sensitivity of market values to changes in yields.

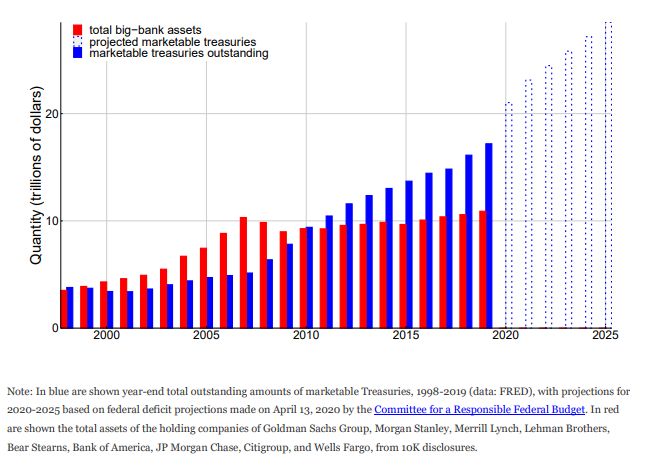

Source: Federal Reserve Bank of New YorkThe stock of marketable Treasuries has grown significantly relative to dealer balance sheets Source: Duffie (2020) Still the World’s Safe Haven? Redesigning the U.S. Treasury Market After the COVID-19 Crisis

…and impaired UST market functioning, which only normalised

after Fed action

Basis Basis

UST 30y bid/offer spread (RHS) UST 2y cash-futures basis (LHS)

points points

140.00 15 Mar: USD swapline rate and 3.2

maturity enhanced

120.00 23 Mar: Federal 2.8

100.00 Reserve 2.4

announces further

80.00 measures 2

60.00 1.6

40.00 1.2

20.00 0.8

0.00 0.4

-20.00 0

Jan 20 Feb 20 Mar 20 Apr 20 May 20 Jun 20

Sources: Bloomberg Finance L.P, Eikon by Refinitiv. and Bank calculations

Note: The bid/offer spread is a 5-day moving average.

Latest observation: 18 Jun 2020 (27 May 2020 UST 10y cash-futures basis)Funding costs in USD increased, and only fell back once the Fed

introduced central bank swap lines

Dollar swaps outstanding

Onshore and offshore rates for 3m dollar funding

Other Bank of Canada

OIS +[25bps to 50bps] Swiss National Bank Bank of England $ bns

Central bank USD swapline rate Bank of Japan European Central Bank 700

Onshore via USD LIBOR Per cent

Total

3.5 600

15 Mar:

20 Mar: Swapline

Swapline rate and 3.0 frequency 500

maturity enhanced 20 Mar: Swapline

2.5 increased 400

frequency increased

2.0

300

15 Mar:

1.5 Swapline rate

and maturity 200

1.0 enhanced

9 Mar 100

0.5

0

0.0 2007 2009 2011 2013 Mar 20 Apr 20 May Jun 20

Feb 20 Mar 20 Apr 20 May 20 Jun 20 20

Sources: Bloomberg Finance L.P. and Bank calculations

Note: Offshore funding calculations use FX swaps referencing 3 month Libor. The dotted light blue

line indicates that prior to the 15 March 2020, swap lines were only offered at a 1-week, not 3 Sources: Bloomberg Finance L.P. , Federal Reserve and Bank calculations

month, maturity. Note: Other includes the Reserve Bank of Australia, the Banco Central do Brasil, the

Latest observation: 18 June 2020 Danmarks Nationalbank, the Bank of Korea, the Banco de Mexico, the Norges Bank, the

Reserve Bank of New Zealand, the Monetary Authority of Singapore, and the Sveriges

Riksbank.

Latest observation: 11 Jun 2020A similar dynamic was seen in the UK gilt market, which also

became impaired, and normalised after the BoE’s QE…

Gilt yields Bid-offer spreads on gilts

5 year 10 year 30 year Per cent 5 year 10 year

Basis

30 year points

1.6 4

19 Mar: BoE package 19 Mar: BoE

1.4 package 3.6

(Bank rate cut 15bps

and additional £200bn 1.2 3.2

asset purchases) 1 2.8

0.8 2.4

2

0.6

1.6

0.4

1.2

0.2 0.8

0 0.4

-0.2 0

Jan 20 Feb 20 Mar 20 Apr 20 May 20 Jun 20 Jan 20 Feb 20 Mar 20 Apr 20 May 20 Jun 20

Source: Bloomberg Finance L.P., TradeWeb and Bank calculations Source: Eikon by Refinitiv

Latest observation: 18 June 2020 Data up to: 18 June 2020…and in sterling money markets, which became stressed and only

stabilised when the BoE launched QE and liquidity support

Sterling money market spreads MMF outflows and assets

Overnight reverse repo - Bank rate spread Basis £ Per

3-month reverse repo-OIS spread ‘Dash for cash’

points billions cent

3-month £LIBOR-OIS spread 24 Mar: CTRF

270 4

announced 100

19 Mar: Further BoE 260 3

package 31 Mar: 80

2

Quarter- 250

60

end 1

40 240

0

20 230

-1

0 220 -2

-20 210 -3

Jan 20 Feb 20 Mar 20 Apr 20 May 20 Jun 20 Mar 20 Apr 20 May 20

Source: Bank of England Sterling Money Market data collection and Bank calculations. Sources: Crane Data LLC and Bank calculations

Notes: The overnight reverse repo rate is for cleared DBV (Delivery by Value) transactions. The 3-

month reverse repo rate uses only transactions estimated to be non-nettable (under leverage ratio

rules). Both rates are volume-weighted and are stated from the perspective of dealers.

Last observation: 18 June 2020During the market stress in March, ‘flight to safety’ movements

widened the spread between IG bonds and government bonds…

Basis

points

Non-financial corporate investment-grade spreads

500

400

300

200

100

0

1/1/2020 2/1/2020 3/1/2020 4/1/2020 5/1/2020 6/1/2020 7/1/2020

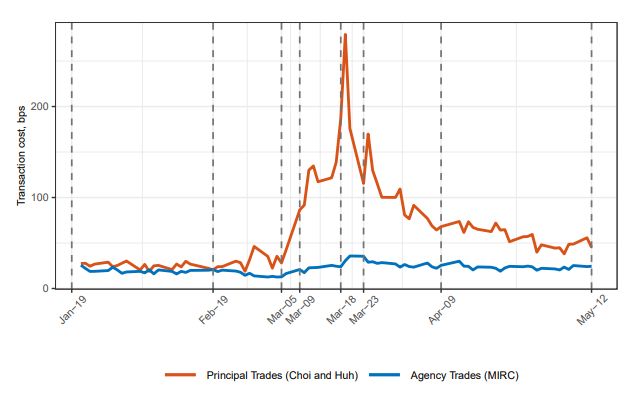

GBP IG USD IG EUR IG…and dealers stopped absorbing US corporate bonds, and shed

some of their inventory, leading to higher trading costs

Cumulative inventory change (USD billions) in the

Transaction costs in the US corporate bond market

dealer sector and as a fraction of total supply

Primary Dealer

Credit Facility

announced

Primary and Secondary Market

Corporate Credit Facilities announced

Source: Corporate Bond Liquidity During the COVID-19 Crisis (Kargar et al)Interlinkages across markets

What were the market interlinkages in March’s ‘dash for cash’?

Large margin calls on derivatives forced funds and …and withdrawals from money market funds and

insurers to raise cash through repo or bond sales… other open-ended funds added selling pressure to

asset markets and money markets.

Bond liquidation

The usual stabilisers in government bond markets did not work as leveraged

investors were forced to sell, and dealers became overwhelmed by selling

pressure.

Bond market illiquidity Funding illiquidity puts

spreads to funding pressure on bond markets

markets

As bond prices fell and became …which forced more of the

volatile, it became difficult and investors trying to raise cash to

expensive to repo… sell bonds.Policy implications

What could be the policy implications of March’s ‘dash for cash’? • If central banks step in during stress to backstop financial markets, is greater resilience in markets need (via regulation or market reform)? Which markets should be covered? • How should the financial system best adapt to a world where markets may not be able to rely on dealers to maintain levels of liquidity at all times and other intermediaries are involved in market making? • If even sovereign bonds can become illiquid, what does that mean for banks' liquidity regulation? • Do we need to change MMMF regulation to ensure that MMMFs retain cash like properties even in stress?

Further reading

Further reading on March’s ‘dash for cash’ • BoE – Interim Financial Stability Report May 2020 • Jon Cunliffe, Deputy Governor, Financial Stability, BoE – • “Financial System Resilience: Lessons from a real stress” • Andrew Hauser, Executive Director, Markets, BoE “Seven Moments in Spring: Covid-19, financial markets and the Bank of England’s balance sheet operations” • BIS – Annual Economic Report 2020

You can also read