Monetary policy challenges in Colombia - Ana Fernanda Maiguashca* Board Member Santander - 9th Annual Latin America European Forum. September 9th ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Monetary policy challenges in

Colombia

Ana Fernanda Maiguashca*

Board Member

Santander - 9th Annual Latin America European Forum. September 9th 2020

1

*The opinions presented here do not represent the position of the Board of DirectorsTHE SHOCKS

Content POLICY RESPONSES AND RESULTS

ECONOMIC FORECASTS

POLICY CHALLENGES• The Colombian economy is facing an unprecedented shock because of

containment measures and the drop of international commodity prices

Google Mobility Trend – Colombia Commodity prices

(percental change from baseline) (January 2020 = 100)

20 140

120

0

Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20

100

-20

80

-40

60

-60

40 Coal

Carbón

-80 Coffee

Café

20

Entertainment and retail

Oil

Petróleo

Grocery and Pharmacy 0

-100

Workplaces Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20

Source: Bloomberg y Google

3• Colombia and Latam will suffer a severe recession. A contraction of real GDP

of more than 7,4% is expected.

% Real GDP

15 (annual growth)

10 8,7

3,3 4,2

4,9 5,2 4,4 4,1 4,2

5 3,4 3,7 3,0

1,1 2,2 2,2

1,1 0,2 0,1

0

-0,3 0,0

-5 -2,2 -2,8 -2,3

-3,9

-6,1 -6,6 -5,8 -5,8

-10 -8,6

-9,3

-11,3 -11,7

-15

-20

-25 -21,9

2019 2020 2021

-30

-30,6

-35

Chile Mexico Argentina Brazil Paraguay Uruguay Venezuela Bolivia Colombia Ecuador Peru

Source: Latin American Consensus Forecast- August 2020

4• Major effects on the labor market. The economic rebound expected for 2021 won’t

be enough to recover the employment levels observed in 2019

Unemployment Rate

20

18 17,3

16 14,6 14,013,6 13,5

14 12,5

11,9 11,3

12 11,2 11,2

10,5

9,8 9,4 9,9 9,5 9,4 9,2

10 9,1 8,9

%

7,2

7,8

8 6,6

5,7 6,0

6 5,4

3,8 3,5

4

2

0

Colombia Brazil Argentina Peru Chile Uruguay Paraguay Ecuador Mexico

2019 2020 2021

Source: Latin American Consensus Forecast- July 2020

5• The monetary policy and other institutional frameworks in

the Colombian economy provided a strong base to

confront this crisis:

1. The Colombian economy has a fully-fledged inflation targeting regime

with exchange rate flexibility with high credibility

2. Fiscal policy is anchored in the medium term

3. Adequate level of external buffers

4. Adequate financial supervision

5. Contained currency mismatches

6THE SHOCKS

Content POLICY RESPONSES AND RESULTS

ECONOMIC FORECASTS

POLICY CHALLENGESThe central bank is using its toolbox to support the economy by:

• Providing liquidity to avoid disruptions in the payment systems and

contribute to the credit supply by financial institutions

• Helping stabilize key financial markets suffering liquidity problems

• Maintaining external buffers to facilitate external payments of the

economy

• Supporting the economy through interest rates

• No QE in Colombia. Liquidity measures had the purpose of

improving the conditions of key financial markets

8Central Bank Response

Protecting the Preserve the Stabilizing key Provide an

Objectives payments supply of credit financial economic

Actions system markets stimulus

Temporary liquidity

(repo operations):

Increase in the allotment X X X

counterparties, collaterals and

maturities

Outright purchases of public and

private securities X X X

Reduction of banks’ reserve

requirements X X X

Auction of FX Non-delivery

forwards X

Auction of FX swaps

X X X

Reduction of the interest rates

X X 9• These policies improved conditions in local financial markets.

Bid-Ask Spread for the Colombian peso Bid-Ask Spread for 10-year sovereigns in local currency*

14 (basis points, 10-day moving average)

12 40

Mexico

35

10 Brazil

30

Colombia

Colombian pesos

8 25

6 20

15

4

10

2

5

0 0

3-Jul 3-Aug 3-Sep 3-Oct 3-Nov 3-Dec 3-Jan 3-Feb 3-Mar 3-Apr 3-May 3-Jun

Source: Banco de la República. *For Colombia TES 2028, Brazil 2029 and Mexico 2029.

10• Reductions in the monetary policy rate will contribute to relieve the financial

burden of debtors and reduce the cost of credit. However transmission channels

have been affected.

Policy Rate

10%

9%

8% 7,75%

7%

6%

5% 4,50% 4,25%

4%

3%

2%

1% 2,00%

0%

11

Source: Banco de la RepúblicaTHE SHOCKS

Content POLICY RESPONSES AND RESULTS

ECONOMIC FORECASTS

POLICY CHALLENGES• The staff estimates a contraction of between 6% and 10% this year,

consistent with a more negative output gap.

% Annual GDP growth Annual Output Gap

9 2

8%

6

0

3 3%

0 -2 -2

%

-3

-4

-6 -5 -5

-6%

-6

-9

-10%

-7

-12 -8

2015 2016 2017 2018 2019 2020 2021 2015 2016 2017 2018 2019 2020 2021

13

Source: Banco de la República – Monetary Policy Report. *Difference between the observed GDP and the potential GDP obtained from the 4GM model.• Headline inflation will most probably close the year below target.

Headline Inflation

7

6

5

4

%

3 3%

2

2% 2%

1

1%

0

2015 2016 2017 2018 2019 2020 2021

14

Source: Banco de la República – Monetary Policy Report• The future of the external deficit is highly uncertain, but a contraction is expected. CB´s

estimate is that the domestic demand contraction effect will prevail over the ToT shock, and

we will see a lower CAD. The number for Q2 (3%) indicates this will be the case.

Current Account

% (% of GDP)

0

-1

-2,0 -2,0

-2

-3

-4 -3,3 -3,3

-3,9 -3,7 -3,8

-5 -4,2 -4,3

-5,0

-6 -5,2 -5,5

-7 -6,3

2013 2014 2015 2016 2017 2018 2019 (pr) 2020 2021

(proy) (proy)

(pr): preliminary.

(proy): proyection 15

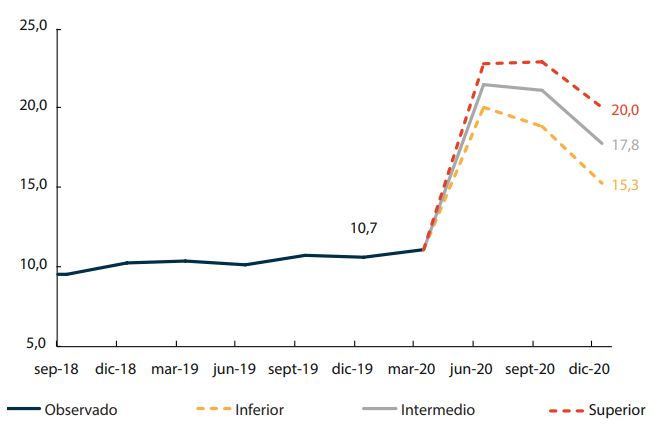

Source: Banco de la República – Monetary Policy Report• A slow normalization of employment is expected. The rigidities in the labor market

partially explain the speed of the adjustment. The gender gap has widened to highly

concerning levels.

Simulations for the National Unemployment Rate

%

Observed Lower Intermediate Higher

16

Note: seasonally adjusted series

Source: DANE. Calculations by Banco de la RepúblicaTHE SHOCKS

Content POLICY RESPONSE AND RESULTS

ECONOMIC FORECASTS

POLICY CHALLENGES• Inflation expectations remain close to the target, and the rate of reduction of expectations

seems be declining. Transmission mechanisms have been affected and there is still high

uncertainty about how they will evolve, stemming from the evolution of the pandemic itself.

10% Headline inflation and inflation expectations

9%

1-year ahead inflation expectations

8%

2-year ahead inflation expectations

7%

Inflation target

6%

Headline inflation

5%

3,0%

4%

3%

2% 2,83%

1% 1,97%

0%

Jul-09 Jul-10 Jul-11 Jul-12 Jul-13 Jul-14 Jul-15 Jul-16 Jul-17 Jul-18 Jul-19 Jul-20

Source: Banco de la Repúlblica and DANE

18• BR has taken a gradual approach to its monetary easing, seeking a sustainable level of

stimulus to support the recovery. There is uncertainty surrounding i) effects of the shocks on

supply and demand, ii) international financial conditions, iii) public debt dynamics, iv) effects

of the shocks on financial stability.

Foreign participation in the local public debt market

(Non-resident holdings as a % of outstanding securities)

60%

50%

40%

30%

20%

10%

0%

Mar-13 Dec-13 Sep-14 Jun-15 Mar-16 Dec-16 Sep-17 Jun-18 Mar-19 Dec-19

Brazil Chile Colombia Peru

Perú

Source: Arslanalp and Tsuda (2014)

19• The financial sector, faces these shocks with high levels of liquidity and solvency. The length of

the recovery period poses challenges to profits and business cases.

• Risk has increased and credit supply (and demand) and prices will continue to reveal this.

Liquidity risk indicator of credit establishment Solvency ratio of credit establishments

400

18

350 17 14,8

16

300

210,4 15

250 14

13

200

12

Liquidity risk indicator (IRL) 11 Total Solvency Ratio

150

10 Regulatory limit

Regulatory limit

100

9

50 8

jun-14 jun-16 jun-18 jun-20 may-10 may-12 may-14 may-16 may-18 may-20

20

Source: Superintendencia Financiera and Banco de la RepúblicaYou can also read