The Maven Letter: April 21, 2021 - Resource Maven

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Maven Letter: April 21, 2021

Mailbox: Sorry for the Frustration…Not Sorry for What I’ve Said. Maven Buys: Newrange Gold (TSXV: NRG;

USOTC: NRGOF). Mid-Month Free Trade Date Table. Full Portfolio Table & Portfolio Updates from Banyan,

Benchmark, Empress, Kodiak, Montage, Northern Vertex, Outcrop, Silver Tiger, Vizsla.

I got an email from a subscriber who feels I fed false promises over the last two years about gold’s upside. The

response ended up an entire article, with a long title that summarizes my sentiment: Sorry for the

Frustration…Not Sorry for What I’ve Said.

It’s exciting for me to find out that a company has changed into something more than the market sees. I

learned about one such transformation this week when I talked to Robert Archer, CEO of Newrange Gold. I

knew Newrange as trying, without major success, to turn the high-grade vein showings and old adits at the

Pamlico project in Nevada into something significant. But last year the team realized the need for a new

approach – and the pivot has created three good and essentially new targets at Pamlico (that do not involve

high-grade veins!) plus a never-drilled target at a new project in Ontario that looks promising. Four good

targets that will get drilled this year, under the expert geologic guidance of Archer and his Newrange partner

Robert Carrington (yes, it’s the Robert and Robert show), makes for odds I want to bet on.

The mid-month Free Trade Date Table appears this week. Following that is the Full Portfolio Table and

Portfolio Updates from Banyan, Benchmark, Empress-Telson, Kodiak, Montage, Northern Vertex, Outcrop,

Silver Tiger, and Vizsla.

-------------------------------------------------------------------------------------------------------------------

Sorry for the Frustration…Not Sorry for What I’ve Said

"... gold will be a bit late to the party" ....

All the time that I have been following you (2 years) and going to the Metals Investor Forum, gold has

been about to rocket off into the cosmos. Then last September gold has gone sideways; and now

"...gold will be a bit late to the party".

Not happy. Please explain.

Reader NM

In the last 2.5 years gold has done this:

Gold miners as a whole have done this, using the GDX as a proxy:

There really is no good proxy for junior gold explorers. The TSX Venture Composite Index used to be a

reasonable representation but now, with virtual currencies and pot stocks and other tech items, it really isn’t

any more. So I can’t show what juniors have done. I would say they’ve followed a similar pattern, albeit with

smaller gains (explorers don’t enjoy the same leverage to a rising metal price as miners enjoy because they

don’t actually produce, or often even have in the ground, any gold) and a lot more volatility stemming from

results.

So my first response is that gold has done darn well.

My second response is that I do not ever see gold going like a rocket into the cosmos, and as such I certainly

don’t say so. Others who take the stage at the Metals Investor Forum (MIF) perhaps do. I am not a gold bug. I

don’t believe fiat currencies are going to explode; I don’t think all the mega money printing the central banks

around the world are going will send gold to the moon. I don’t even own any physical, aside from a few pieces

of jewelry.

I think history is being made as governments and central banks abandon long-held ideas (like that debts

should ever be repaid) in favour of Modern Monetary Theory. And I don’t know how it will all play out. No one

2

does. And because of that, I think gold – a long standing safe haven of value – will play an important role in the

coming years.

I try to convey the twists and turns in that process in my editorials. I try to caution when I see near term risk. I

try to encourage when I see opportunity. I act on those forecasts myself (and my portfolio has multiplied

threefold since I started The Maven Letter in 2015, for what it’s worth).

Don’t get me wrong: I share your frustration. I started a business based on the idea that metals would turn

from bear to bull – and that was six years ago! As the charts above show, the premise has been correct, even if

the scale of success has left all of us wanting more.

I want the gold market to take off tomorrow and not turn back. But I am a realist. Even well-established bull

markets don’t simply go straight up. And gold is a complicated beast, its performance impacted by growth and

inflation and confidence and the all-important bond market. So I watch those things and try to understand

how they might influence gold in the near and medium term.

Last fall I swallowed my pride and sold a set of stocks I had entered in August because I realized that I’d let

gold’s rapid rise from June to August get me overexcited. In that excitement, I let down my guard, letting

myself neglect that even fully established gold bull markets take a step back for every two or three steps

forward, whether because of macroeconomic shifts or straight seasonality. When gold started coming off its

peak, I remembered. I sold at a loss (about 30% on average, if memory serves) and commented that I should

have kept a more level head.

Since then, the gold market has been aggravating. Believe me, I know – I focus on it every day. But I still

believe the fundamentals are in place for it to work well in the medium term. And because I hold that outlook,

I have to try to predict the near term as well, because it’s whether we are at an interim peak or valley that

helps determine when to move on opportunities.

It would be a heck of a lot easier to just stick with my medium-term confidence and say, always, that gold is

about to go. But that would not be true or helpful.

So. I’m sorry for getting overexcited last August. I very much understand the frustration in having to wait,

more, for the gangbuster gold bull market that we all want. But I am not sorry for conveying how and why my

near-term outlook shifts, within a bullish medium-term perspective.

And finally: I know that gains got last year feel pretty distant. But they happened. We did well.

And we will again.

---------------------------------------------------------------------------------------------------------------------

Mid-Month Feature: Free Trade Date Table

On the third Wednesday of each month I publish a table with which stocks have financing stock under hold

and when those holds end. Based on the difference between the financing price and the current price, the

amount of stock issued in the raise and the daily trading volume, the type of stock (flow through vs hard), and

any other factors that matter (like if a long-time supporter took a big chunk of the raise or if key news is

expected), I rate the risk each free trade date appears to pose to the stock. Note that these ratings will change

month to month as the story progress and the share price rises or eases.

Red means high risk (strong likelihood the free trade date will lead to a significant share price decline)

3

Yellow means moderate (free trade date could have some negative share price impact but not dramatic)

Green means negligible (free trade date not likely to impact share price)

Amount Financing Financi Warran Current Free Comment

raised shares ng t? price trade

($M) (shares out) price date

IsoEnergy $4.0 2.7M (94M) $1.48 no $2.50 22-Apr

Nevada $3.3 26M $0.13 full $0.15 28-Apr Drills will be turning on

Exploration (130M) key program

Generation $3.3 4.2M $0.77 no $0.91 30-AprFT (higher odds of selling);

Mining (139M) E Sprott bought half

(lower odds)

Rokmaster $9.1 23.4M $0.32 full $0.43 30-Apr half FT (higher odds of

(98M) selling); insider funds took

more than half

Banyan $2.5 8.4M $0.26 no $0.23 30-Apr Charity FT but Banyan

(172M) placed stock (I give the

estimated hard price)

Norseman $1.8 7M (37M) $0.25 full $0.39 14-May I would not buy until this

Silver risk passes

Edgemont $2.0 8.8M (22M) $0.20 half $0.16 17-Jun Drills should be turning…

Gold

Vangold $17.0 56.5M $0.30 half $0.61 10-Jul Sprott, insiders, and

(189M) named funds took ~half

Brigadier $1.0 5M (71M) $0.20 full $0.17 16-Jul Too far out to comment…

Telson $10 50.4M $0.20 half $0.36 30-Jul

Mining (183M)

Outcrop $9.20 21.4M $0.43 half $0.26 26-Jul

Gold (110M)

-------------------------------------------------------------------------------------------------------------------

Maven Buys: Newrange Gold (TSXV: NRG, USOTC: NRGOF)

I was compiling a list of topics for a video series I’m going to do about what metals and mining investors

should know. I went through the usual topics: start from a bullish macroeconomic thesis, shape your portfolio

according to your risk tolerance and time commitment, when to buy a stock, how long to hold a stock, how

and why you have to manage risk, and the litany of forces (many not related to rocks!) that push junior share

prices around.

Then I started to think about how to discuss how to choose the junior co’s upon which you will bet…and

another entire list emerged. Number of targets, the strength of the exploration thesis, access to funding,

4

clarity of plan, permitting hurdles and timelines, share structure, valuation, communication – it really goes go

on.

But when I sit back and think for a moment…it’s all about people.

Leading a junior explorer is not easy. The requirements list is very long. You need capital markets savvy –

connections for raising capital, knowledge of how it all functions, experience with poor structures and deals

and shareholders and markets and projects, a clear grasp of metal macroeconomics and investment trends,

and the good accounting abilities that are part of leading a company. But you also have to have technical

knowledge – whether or not a CEO drives the geology side of the business, he or she needs to understand it

and question it and explain it and calculate the odds that a geologist’s ideas will create value for shareholders.

It’s a very hard list to cover. And so I keep tabs on the people I think manage it.

Robert Archer is one. Archer co-founded Great Panther Silver in 2004, which in hindsight was a great move but

at the time required guts and macroeconomic conviction. Great Panther now operates three mines and is

building a fourth while exploring several other projects. Its share price performed very well in the last bull

market (which sparked that ‘hindsight’ comment) and it’s been free of controversy, whether sociopolitical or

technical.

After stepping down as CEO of Great Panther a few years ago Archer thought about retiring, but retirement

just didn’t stick. And so in early 2019 he joined Newrange Gold as CEO.

It made sense. Newrange’s Pamlico project was an interesting, promising piece of ground in Nevada but the

company had struggled to advance it apace largely because NRG lacked capital markets savvy. Archer brought

that, while also complementing the geologic knowledge of president Robert Carrington.

OK, fast forward 2+ years. Archer and Carrington have pursued the high-grade veins that stick out of the

ground or have been small-scale mined at Pamlico but without great luck. Archer realized the need for two

things: a new approach and a second story.

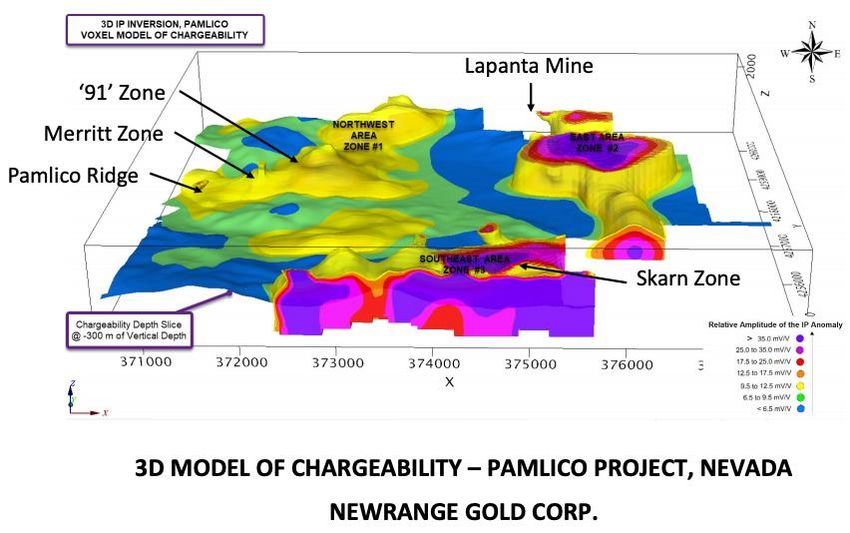

The new approach at Pamlico started with an IP survey that greatly expanded coverage compared to a

previous survey. Think of this in two ways: NRG needed to step back and see if they could find an overall

geologic explanation for the high-grade gold at Pamlico and they needed to see if IP could help them track

those high-grade veins better. The gold at Pamlico is associated with sulphides, which are oxidized and so not

trackable by geophysics at surface but are preserved below the oxidation level.

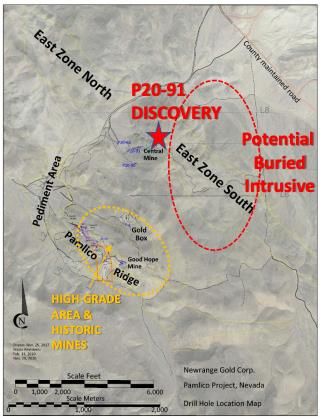

The work outlined three target areas. The Northwest Area encompasses Pamlico Ridge (where much of the

historic mining took place) and the high-grade Merritt Area as well as a newer area called the 91 Zone; the IP

depth slice below doesn’t capture it well but the survey outlined a chargeability anomaly east of the 91 Zone

that just might be a mineralized intrusion. The Southeast Area covers what NRG had already dubbed the Skarn

zone. And the East Area is a new target, potentially related to the Southeast anomaly.

5

There are a few important takeaways here.

First, NRG had focused at Pamlico Ridge

because old adits made for clear high-grade

targets that, if they grew into something, could

have complemented the small but well-

mineralized Merritt area they drilled in 2017.

But the corridor of increasing chargeability

from Pamlico Ridge to 91 supports NRG’s

recent shift in focus eastward.

91 is called such because late last year hole

P20-091 returned 0.4 g/t gold over 52 metres

from the western edge of the IP anomaly as

NRG understood it then (before the expanded

survey). NRG followed up with another four

holes; all returned gold starting about 110

metres downhole and continuing to end of

hole. The zone is currently defined across 200

metres east-west and only 50 metres north-

south and grades seem to be increasing to the

east, coincident with higher chargeability

readings.

This zone doesn’t sound particularly exciting

but details matter. There are high-grade hits

scattered in the lower-grade horizon. And it sits

near the base of oxidation; the fresh rock below

carries at least 1% pyrite.

6

It leads to a working theory that the volcanic tuff-hosted layer of gold at 91 could have come from an intrusive

body to the east, which is where the IP survey defined a large chargeability anomaly.

NRG is keen to return and test the main chargeability anomaly with a diamond drill that can go beyond the

reach of the RC rigs, to see if it does indicate . the presence of a mineralized buried intrusive.

And there’s another target that also deserves work: in February hole 115 returned 4.4 g/t gold over 13.7

metres from 15 metres downhole, 5.5 g/t gold over 7.6 metres from 93 metres, and 13 g/t gold over 1.5

metres from 123 metres. Importantly, the rocks between these intercepts were variably mineralized such that

the full 124-metre interval averaged 1.13 g/t gold, in oxide rock within 120 metres of surface.

The hit came 85 metres east of the Merritt zone, which is an area of shallow, fairly high-grade oxide gold

mineralization. Merritt has returned some good hits, like 37 metres of 3.6 g/t gold and 34 metres of 1.1 g/t

gold, but the zone hadn’t developed scale as yet. This new hit to the east adds precisely that potential.

OK, so hole 115 needs follow up for its long interval of good-grade, near-surface, oxide gold. 91 Area needs

follow up to see if this consistent-if-low-grade body of mineralization sitting ~110 metres below surface stems

from a mineralized intrusion to the east, where they now know a large, strong chargeability anomaly sits.

Those are good targets. But the target I’m most excited about is the Skarn Area.

NRG had prospected the Skarn Area before and dubbed it such after seeing chalcopyrite on surface along with

skarn alteration (garnets and hornfels). The IP survey, though, has made the target suddenly more exciting. It

returned very strong chargeability readings over an area 3 km by 2 km (and still open). The shape of the

anomaly, coincident low resistivity, the intensity of the chargeability readings, and the evidence of skarn

mineralization on surface make it a darn good skarn target. And helpfully the target sits less than 100 metres

below surface in places, while deeper readings may be indicating an underlying porphyry.

Pamlico summary: in 2020 NRG was struggling to pull a story together at Pamlico. Good geologists they are,

they tried another approach, testing different targets east-northeast of Pamlico Ridge and running a property-

wide IP survey.

Both angles worked. The IP targets are very interesting: the Skarn Area has all the signs you would want for a

skarn deposit and potential buried porphyry, while the big chargeability anomaly east-northeast of the new 91

discovery area deserves a test. And hole 115 returned that wide, near-surface oxide intercept close to the

Merritt zone.

NRG will kick off a new drill program shortly. Besides additional RC drilling to follow up hole 115, the five

planned diamond drill holes will test the chargeability targets beside 91 and at Skarn. Archer says they won’t

stop at 5 holes if they hit something good.

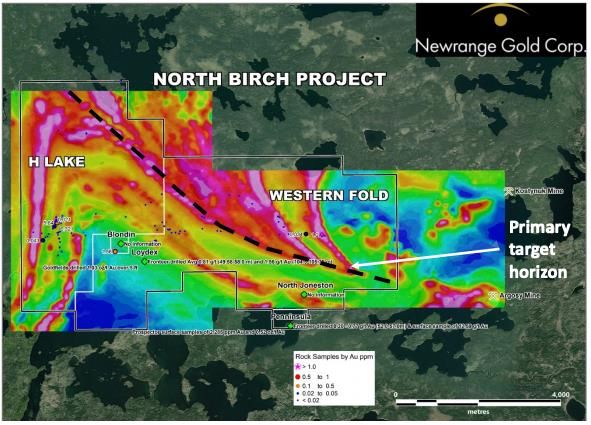

The North Birch Project

When Archer called me the other day, it was to tell me about a financing. When he mentioned a flow-through

component I immediately asked: why are you raising flow? Flow-through funds can only be used to explore

projects in Canada and I didn’t know NRG had a project outside of Pamlico.

Turns out they do – and the North Birch project in Ontario is pretty darn interesting and is drill-ready.

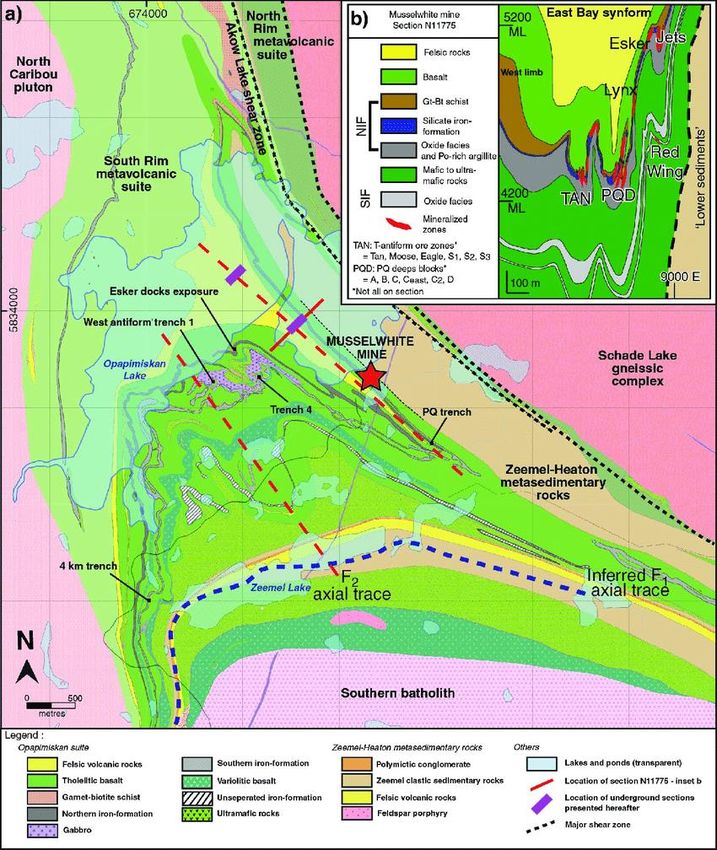

North Birch is an iron formation gold target. IF gold deposits are well known; the closest large one hosts the

Musselwhite mine about 190 km to the north, which has produced or still offers in reserves over 8 million gold

ounces.

Interesting backstory: Archer worked on the prefeasibility study for Musselwhite and re-wrote the geologic

model for the deposit for Placer Dome in 1994. That work got him interested in IF opportunities, which led him

7

to stake the North Birch project in 2002. He optioned it to an Australian junior who did some good work but

then got distracted and gave it back. That happened just as Archer was starting Great Panther so North Birch

got ignored, with the claims lapsing.

A Canadian junior called AurCrest re-staked the project in recent years. AurCrest flew a great mag survey but

did no ground work. NRG optioned it from AurCrest in late 2019. The terms are easy - $200,000 in cash and 1

million shares over two years to earn 100%, with Aurcrest retaining a 2% NSR half of which NRG can

repurchase for $1 million – and between Archer’s experience at Musselwhite and Carrington’s previous long

experience at Springpole (the 4.7M oz deposit just 12 km to the east that First Mining Gold is advancing) the

NRG team is well suited to explore this area and target.

The target horizon is obvious in the magnetics map below.

The 8-km long target horizon is recessive (sunk down into the ground) so it is not exposed at surface. As such it

has not been sampled or trenched directly. But IF rock samples that made it to the surface have been

collected and returned grades as high as 5.6 g/t gold. And the rocks south of the IF horizon host multiple gold

showings, which suggests a strong mineralizing event and potential across stratigraphies.

For interest, below is a geological map of the Musselwhite mine area. Iron formations are in grey, but note the

similarity in overall shape.

8

Newrange wanted to explore North Birch last summer but COVID slowed new exploration permits to a crawl in

some parts of Ontario, which meant the company didn’t get its permits until the fall. They recently ran a

ground IP survey to complement the airborne mag data and have applied for a drill permit.

Summary

A year ago, Newrange was chasing high-grade veins at Pamlico Ridge. The project (which I’ve visited) certainly

gives the sense of a potential for scale, with old adits and veins scattered across the hills for literally miles. But

several years in, Newrange hadn’t managed to pull the potential together into something of significance.

So Archer and Carrington tried a new approach: test different areas and run a property-wide IP survey to

hopefully help with the overall geologic framework.

Both worked. As a result, Pamlico now has three interesting targets:

The Merritt-to-hole 115 area, where potential lurks for a body of good grade oxide gold at surface

9

The chargeability anomaly east of Area 91, which could be a mineralized intrusion that created the low

grade but nicely continuous gold zone that NRG has recently identified (and that strengthens heading

towards the potential intrusion)

The Skarn Area, where NRG just identified coincident strong high chargeability and low resistivity

anomalies close to surface and right underneath surface showings of chalcopyrite and skarn alteration.

Archer and Carrington also added a second project to the company. North Birch saw good historic work, offers

up gold in iron formation rock samples, and has the exact geophysical signatures you want to see in an iron

formation gold target.

I often say I want companies to have more than one target because odds of scoring a goal are higher if you can

take multiple shots. NRG has transitioned from a one target company (I’m simplifying when I describe Pamlico

Ridge as one target, but it’s still valid) to a company about to test four good targets.

That NRG’s share price is essentially unchanged since last fall says that the market hasn’t understood this

transition yet.

Newrange has 127 million shares outstanding and very few warrants. At today’s close of $0.13 it carries a

$16.5-million market cap.

I don’t know how soon the market will see this opportunity but I’m keen to enter now, because:

Newrange just financed. It was popular, which means Archer told the new story to lots of interested

parties.

IP results from North Birch should be out shortly. This release isn’t likely to impact the market but an IP

map that helps illustrate cross-cutting structures and similarities to Musselwhite will help tell the story.

With cash now in hand NRG will head to Pamlico to drill in the next few weeks.

10Drill results from Pamlico are still months out and NRG doesn’t yet have a drill permit for North Birch (though

those shouldn’t take long, as long as COVID doesn’t slow First Nations approval dramatically), so there isn’t

any real pressure to buy now. But I like the story and the targets they will test over the next 6-12 months. If

that’s the case, I figure I’ll buy now, ahead of any potential price creep as the new Newrange story gets out.

------------------------------------------------------------------------------------------------------------------

Full Portfolio Table

Stocks shaded in green are expected to issue notable news soon

Stocks in bold and marked with an asterisk (*) I am currently buying (adding to my position)

Entry Entry % Price

Company Ticker Cost base Change

Date price position today

Mine Developers

NEE.V,

18-Feb-20 $0.75 100 $0.42 -44%

NHVCF.OTC

Northern

Strong Nevada exploration team with pre-discovery project merged with Northern Vertex to

Vertex

bring exploration prowess to underexplored Moss mine. Move took market by surprise but it

does make sense

ORE.V,

13-Jun-18 $0.81 100 $0.97 20%

Orezone ORZCF.OTC

Gold * Under construction gold project with scale and strong economics, and a team that has

successfully built many mines. Value gains ahead whether ORE builds or gets bought

TSN.V 24-Feb-21 $0.30 100 $0.36 20%

Telson Turnaround story: new finance package and people will allow Telson (which market had

Mining * written off bcs of debts) to finish building gold mine, turn zinc mine around, and make $.

Should re-rate significantly

UEC.NYSE 21-Jun-15 $1.72 100 $2.74 59%

Uranium

Energy Ready to ramp up low-cost output into developing uranium bull market that will likely offer a

premium for US output. One of few clear bets for uranium

Feasibility-Stage Projects

ERD.T, $0.36 (add @ $0.24,

08-Jan-17 $0.86 200 $0.37 3%

Erdene ERDCF.OCT COVID)

Resources Advancing dual tracks: develop BK (first gold by late 2021) and keep exploring. Exploration

ongoing and returning new high-grade zones!

Advanced Assets (PEA or Pre-feasibility)

ADZN.V;

Adventus 07-Apr-21 $1.00 100 $1.07 7%

ADVZF.OTC

Mining *

11-$0.57 (sold half $1.67;

FWZ.V 01-Jun-17 $0.80 25 $0.80

COVID)

Fireweed

Zinc Mac Pass is a standout zinc project. Summer drilling returned long intercepts from Boundary

zone, which is now dramatically increasing the scale of any Mac Pass mine. 2021 will see

Boundary fleshed out (good odds of major resource boost plus testing new targets

GENM.V 20-Nov-19 $0.19 $0.10 50 $0.91 810%

Generation Unique PGM asset: large resource in great location with grade and scale upside. Feasibilty

Mining * returned robust numbers. Exploration too. Price rising as investors rotate back to PGEs

after COVID scare

ITR.V; $2.58 (COVID;

Integra 06-Nov-17 $0.90 100 $4.03 56%

ITGR.NYSE rollback)

Resources

PEA outlined good, large mine already. Favoured jurisdiction, strong treasury, exploring for

*

high grade, updating PEA with much bigger mine plan

KORE.V,

27-Mar-19 $0.23 $0.29 (COVID) 100 $0.84 190%

KORE KOREF.OTC

Mining Advanced heap leach Imperial project (permitting story) plus PEA-stage Long Valley project

with exciting potential. Fundamental value, potential for splash, lots of news

KUYA.C 08-Oct-20 $1.42 33 $2.66 87%

Kuya Silver New company pushing the Bethania mine in Peru back into production, with plans to expand.

Low cost, near term silver producer; strong team; tight stock.

MAU.T 27-Jan-21 $0.97 100 $0.77 -21%

Montage

3M oz open pit deposit in Cote d'Ivoire being advanced rapidly to development by high

Gold

caliber team. New deal, undervalued, catalyst rich 2021.

27-May-

NCAU.V $0.36 $0.61 (tranches) 100 $0.62 2%

20

Newcore

Advancing the PEA-level Enchi gold project in Ghana: resource growth, testing new targets,

Gold

updating economics and mine plan. Neglected asset getting focused attention for first time.

Top tier management.

RVG.V,

30-Oct-19 $0.51 100 $0.68 33%

RVLGF.OTC

Revival

Strong team advancing historic asset to production in Idaho. Tight structure, strong capital

Gold

markets capacity, looking for additional acquisitions. Upsized summer exploration plans after

raising $13M - potential to demonstrate scale if raft of targets work.

RKR.V 29-Dec-20 $0.45 100 $0.43 -4%

Rokmaster

2M oz resource in east-central BC. High grade, growing, and metallurgical issues now

Resources

addressed. Market hesitant on balloon payment and met plans but I think both are fine

*

and stock will shine once that realization catches on

TSG.V,

24-Jun-20 $0.30 100 $0.26 -13%

TSGZF.OTC

Tristar

PEA outlines a robust low-cost open pit mine with 43% IRR at $1250 gold and pre-feas due

Gold

out in late 2021 will be markedly better. Renewed exploration effort very likely to find more

of the same mineralization (1 g/t average) and could find a high-grade zone.

12TLG.T;

19-Jun-19 $0.69 $0.765 (COVDI) 100 $1.16 52%

Troilus CHXMF.OTC

Gold Large open pittable gold resource at historic mine. PEA captured value; now keep expanding

resource and testing regionally for additional discoveries.

VGLD.V,

17-Dec-20 $0.28 100 $0.61 122%

VGLDF.OCT

Vangold El Pinguico mine was uber high grade but abandoned 70 years ago; no exploration since.

Mining Opportunity to chase known shoots to depth, find additional shoots, test other structures.

Also significant stockpiled ore on surface and underground; Vangold dealt to buy neighouring

El Cubo mill so will start producing in 2021.

Exploration

BYN.V 17-Dec-20 $0.25 100 $0.23 -10%

Banyan 1M oz resource growing steadily at AurMac, a road-accessible project between two

Gold operating mines in Yukon. Inexpensive entry on expectation this team will double this open

pittable resource by 2022.

BNCH.V,

29-Dec-20 $1.07 $0.60 50 $1.50 150%

Benchmark BNCHF.OTC

Metals Huge drill effort to prove up signficant gold resource at Lawyers project in BC. First resource

due end Q1, PEA to follow, $25M exploration effort in 2021 will test long list of targets.

Blue Lagoon 17-Dec-20 $0.69 100 0.63 -9%

Blue Small scale production imminent from previous operator's work and focus. High potential to

Lagoon find high-grade mineralization on multiple veins on very underexplored, road accessible

project in BC.

BRG.V,

12-Aug-20 $0.39 100 $0.17 -56%

Brigadier BGADF.OTC

Gold Picachos project in between GRSL's Plomosas and VZLA's Panuco. Similar: high-grade historic

mines, underexplored. Area play and project potential for splash.

CLZ.V 13-Jul-20 $0.15 100 $0.10 -33%

Canasil

Resources First results from Candy vein a technical success; market wanted more. Ongoing work could

provide. Now drilling LA Esperanza to expand discovery from years ago.

CVB.V 10-Apr-19 $0.34 $0.355 (COVID) 100 $0.21 -38%

Compass

Gold Cashed up to drill test slew of targets backed by a few seasons of data. Seeking open pittable

1-2 g/t gold in Mali. Could be 'boring' until that become apparent and then…

EDGM.CSE 20-Jan-21 $0.25 100 $0.16 -38%

Edgemont Exploring the Dungate project in central BC for a porphyry. Two good targets (via one historic

Gold hole with no assays but promising drill logs, geophysics, sampling, soils) on property road

accessible, workable year round, gentle terrain. Low market cap at entry

GFG.V 18-Oct-19 $0.18 $0.21 100 $0.17 -21%

GFG

Resources Multiple gold hits in a few drill programs at Pen project. Systematic approach to grassroots

exploration. Holding through results from late 2020 program at least

GGL

GGL.V 08-Oct-20 $0.18 100 $0.16 -11%

Resources

13Getting set to start drilling the high-grade oxide gold zone at Gold Point in Nevada.

Opportunity to extend known high-grade shoots, explore around old stopes,and test other

veins/areas. Strong technical team, tight share structure.

GXX.CSE 07-Apr-21 $0.33 100 $0.43 30%

Gold Basin

Under the radar company drilling with Gold Basin project in Arizona to confirm JORC

Resources

resource and grow it. Good odds to define at least 1M oxide gold ounces in short order.

GBR.V, $0.48 (sold half to $0,

11-Dec-17 $0.29 50 $14.62 2946%

Great Bear GTBAF.OCT COVID)

Resources GBR doing 300-hole program to define first resource at LP Fault as fast as possible. 10M oz. is

likely. Race to resource before getting taken out

HSTR.V 30-Jul-20 $0.09 $1.35 (rollback) 100 $1.20 -11%

Unga project in Alaska has four strong targets (high-grade vein with expansion potential,

Heliostar high-grade veins on surface ignored for 40 years because bad drilling gave bad results, drill-

Metals * tested high-grade beneath old gold mine left behind bcs polymetallic, and flat-lying surface

oxide gold zone). New management advancing with focus & funding; also brought in 3

promising Mexican projects

HIGH.V; Spinout or

$0.45 $0.41 (COVID) 100 $1.39 239%

HGGOF.OTC $0.45

HighGold

Mining Drilled multiple targets at JT project. Goal: show there's significantly more potential than the

current resource, through expansion AND multiple new zones. Strong contender for standout

drill results (already some). Also drilling in ON throug winter

ISO.V,

12-Dec-18 $0.40 $0.44 (COVID) 100 $2.50 468%

ISENF.OTC

IsoEnergy

Only junior with a high grade U discovery as uranium bull market gathers momentum. Tight

structure amplifies response to news. Hitting high grade ahead of maiden resource

KDK.V 18-Dec-19 $0.35 $0 50 $1.67

Kodiak Major gold-copper porphyry discovery in second drill program at MPD. Will soon start

Copper 30,000-metre follow up program aimed at expanding high-grade core south plus testing

other very similar targets on property

LGD.V,

Liberty 13-Apr-20 $1.15 100 $1.55 35%

LGDTF.OTC

Gold

Rapidly growing a good oxide gold resource in Idaho. Well capitalized, good momentum

NGE.V,

11-Oct-17 $0.33 $0.30 (COVID) 100 $0.15 -52%

Nevada NVDEF.OTC

Exploration Stalking big gold under cover in Nevada. Have found what looks like a massive system; need

to find the hot spot therein. Drilling now underway

NORA.V 08-Oct-20 $0.18 100 $0.08 -56%

Norra

Will soon start drilling around and under the Bleikvassli mine in Norway to verify and expand

Metals

historic resource. Moderate success would garner a market cap well above current $9M

OROX.V 08-Oct-20 $0.80 100 $0.69 -14%

Oro X Merging with Latitude Silver to become Silver X, focused on Nueva Recuperada mine in Peru.

Mining Operating zinc-silver mine with exploration upside and expansion potential. Corporate goal:

add more silver assets. Paul Matysek involved.

14OSI.V 13-Apr-20 $0.69 -0.03 50 $1.39

Osino

Resources Gold discovery in Namibia under till. Potential for deposit of scale essentially at surface.

Strong shareholder registry and team.

OCG.V,

12-Feb-20 $0.11 0 75 $0.26 160%

MRDDF.OTC

Outcrop

Hammering the vein system at Santa Ana with holes; great success thus far hitting repeating

high-grade shoots along 14 km vein extent.

NOC.V 20-Jan-21 $0.39 25 $0.39 0%

Norseman Emerging silver company with three exploration projects I west-central BC…but investment

Silver thesis is that this team will acquire one or more additional, more advanced silver assets.

Small position for exposure to potential for this to become more

PGZ.V,

18-Feb-21 $0.48 100 $0.52 8%

Pan Global PGNRF.OTC

Resources advancing a strong and potentially large VMS discovery at the Escacena project in Spain.

* Lots of room to grow, multiple similar untested targets (and VMS's occur in clusters), and

surrounded by operating mines. Standout copper explorer

PRG.V 25-Sep-19 $0.16 $0.135 (COVID) 100 $0.18 33%

Precipitate

Gold Optioned flagship PG project to Barrick (strong deal if it indeed hosts a discovery). Pivoted to

explore nearby Ponton project; targets look good.

RSLV.V 23-Sep-20 $1.05 100 $1.03 -2%

Reyna

Silver * Top tier technical and markets team with portfolio of Mexican silver assets. Two projects

will be drilled 2021; potential for big success

RDG.V 17-Aug-20 $0.55 100 $0.47 -15%

Ridgeline New company with three high potential Nevada gold projects. Selena showing promise for

Minerals surface oxide silver-gold; Swift and Carlin East are deep, high-grade targets. Well funded,

strong backers, tight structure, cheap drill contract

SASY.C 08-Oct-20 $1.08 100 $0.36 -67%

Sassy

Resources Foremore project in BC has multiple strong targets. New Newfoundland land position gives

exposure to another hot district.

SLVR.V,

29-Dec-20 $0.51 100 $0.75 47%

SLVTF.OTC

Silver Tiger

* Serially successful team in finding & developing deposits in Mexico. El Tigre mine was very

rich; remnant halo hosts 1M heap leachable gold eq. ounces. This will grow; PEA pending.

Splash potential: exploring the rest of the vein system. 5 rigs turning

PEAK.V 17-Aug-20 $0.90 100 $0.41 -54%

Sun Peak Portfolio of VMS projects in Ethiopia being explored by a team that has made two major VMS

Metals discoveries in the same rocks in neighbouring Eritrea. Tight structure, strong backing, cashed

up, many strong targets. Violent unrest has project on pause…

TRG.V 08-Oct-20 $0.40 100 $0.26 -35%

Tarachi

Gold Mexico gold-silver explorer that just bought the Magistral tailings and process plant - path to

near term production, to create cash flow. Right team for the task

VLZ.V 20-Jan-21 $0.18 25 $0.16 -14%

15Well structured & managed company diving into gold potential of Wyoming, which is littered

Visionary

with historic gold mines but has been ignored by modern explorers. Dipped a toe into this

Gold

stock for its potential to become much bigger

Vizsla VZLA.V 09-Oct-19 $0.41 100 $1.85 351%

Resources Exciting high-grade silver discovery underway at Panuco project in Mexico. Multiple veins

* to test. Strong team, cashed up, momentum, 4 drills means constant news.

Royalty Companies

EMPR.V;

30-Dec-20 $0.54 0.13 66 $0.42 223%

Empress EMPYF.OTC

Royalty * New royalty co with strategy focused on buying new royalties, in deals engineered by three

strategic partners. Impressive management.

EMX.V,

14-Nov-14 $0.86 $0.98 100 $3.97 305%

EMX NYSE

Royalty Using cash to constantly build the portfolio: royalties, properties to prep and option out,

strategic investments. Cash flows cover operations. Tight shareholder registry.

Portfolio Updates

Banyan Gold (TSXV: BYN; USOTC: BYAGF)

BYN released assays for the last of the holes it drilled on AurMac in 2020. This last batch included a north-

south fence of holes drilled 125 metres east of prior work on the Powerline deposit. The results continued to

show a largely consistent area of mineralization with medium-to-long widths of mineable grade stuff (e.g.,

41.7 metres of 1.4 g/t in Hole 59 and 122 metres over 0.77 g/t in Hole 63) along with one narrow, high-grade

interval (35.3 g/t over 1.2 metres within 6.8 g/t over 7.0 metres in Hole 64). The target remains open in all

directions.

16Remember that the investment thesis here is that BYN looks likely to define two million oz. of open-pittable

gold at AurMac over the next year. This would be a resource that’s in a great location – it’s road accessible and

almost adjacent to the operating Eagle mine, where the head grade of 0.8 g/t gold could benefit from a

higher-grade satellite deposit. Success outlining a resource of this size at AurMac should make BYN worth

notably more than the $35 million it is valued at today. Oh, and there’s another benefit to AurMac’s location:

BYN started its 2021 drill program a month ago and is already 20 holes in!

Benchmark Metals (TSXV: BNCH; USOTC: BNCHF)

BNCH is turning its attention to readying drill targets on the Marmot and Marmot East areas within its Lawyers

project. With the resources at Cliff Creek, Duke and AGB anchoring the project’s near-term value, BNCH’s

analysis of geochem and drilling data collected on these targets, which together span two kilometres by three

kilometres and include a 2020 discovery hole grading 0.82 g/t gold-equivalent over 101 metres, will support a

planned 10,000-metre drill program to test their potential to host satellite deposits. If BNCH indeed defines

resources at these new areas, they would be added to later versions of the mine plan, the first version of

which will come out as a PEA this year.

The market isn’t going to care about this piece of news but majors, some of which are undoubtedly already

assessing the potential at Lawyers, will be interested in additional potential at the project.

Empress Royalty (TSXV: EMPR; USOTC: EMPYF) & Telson Mining (TSXV: TSN)

Empress and Telson announced the close of the Taheuheuto stream agreement. The deal gives Empress a

stream of 100% of Tahuehueto’s silver until 1.25 million oz. have been delivered and 20% thereafter. For the

stream, EMPR is paying US$2M now and will pay another US$3M once Telson closes the other key part of the

Tahuehueto build finance package, which is its lending facility with Accedno Banco.

That should close in a few weeks, at which time Tahuehueto construction should ramp right up. Given work

done already, the mine should be complete before the end of the year.

For Empress: Tahuehueto should produce 1.8M oz silver a year, which is a strong flow that means this deal

generates a good IRR for Empress at current silver prices. That they got the deal shows how important their

relationship with Accendo Banco.

For Telson: the streaming deal is great for EMPR but it’s still good for Telson. Telson needed a complete

finance package to get Tahuehueto built, big enough and with enough players of merit to convince Trafigura,

to whom TSN owes a lot of money, to restructure those debts. Accendo Banco is key to that, but Empress

helps. I realize EMPR is still a new company but management has deep connections in the mining space and

the company has demonstrated that it has access to cash and deals. Moreover, the silver stream is simply an

important chunk of money as part of the overall package; Accendo didn’t want to offer up all the needed

capital. But with the US$5 million from the stream, the finance package should certainly be enough to get

Tahuehueto built, repay bits of and restructure the rest of the debt, and start down the new path as a two-

mine operator. Given this was the way to get to that end point, TSN wasn’t in a position to push back too hard

against Empress; as such the stream isn’t great, but is fine, for Empress.

17Empress released another piece of news just this morning: the close and funding of the Manica gold project

royalty. this is a relatively small deal, with EMPR providing US$2M to get 2.25% of gold revenues from the

project until 95,000 oz. From there the royalty drops to 0.75%.

Manica, by way of reminder, is a project in Mozambique with four deposits. Only one of those deposits has a

compliant resource estimate that Empress can report: Fair Bride hosts 13 million measured and indicated

tonnes grading 1.8 g/t gold for 755,500 oz. in an open pit shell. The plan is to mine and process the oxide and

transitional ore with a carbon-in-leach plant with 42,000 tonnes per month capacity.

Those initial 92,000 oz. will more than cover the US$2 million Empress is paying for the royalty and should

come in the first two years of production. And production should kick off before the end of the year. Empress

hasn’t given that timeframe but he crushing and grinding circuits are already in place; this stream was basically

to finance the last piece of the puzzle, which is the CIL circuit to recover the gold. EMPR does also describe

Manica as the first resource in its portfolio that will be cash flowing.

Tahuehueto should come online not long after Manica. As such, these two pieces of news are pretty darn

significant, despite being ‘just’ the closings of already-announced deals. Investors in the royalty space are very

focused on near-term revenues and clear revenue growth ahead. Closing these deals should let Empress

actually discuss revenue projections and timelines, soon, something the company has not been able to do to

date.

Near-term revenue and clear revenue growth should appeal to investors. Finding more deals to enhance both

of those would amplify the appeal; boosting cash flows would also give EMPR the option to finance additional

deals with cash and debt, rather than equity,

which is what royalty investors really want to

see. And Empress makes clear that they are

close to closing on a few other deals.

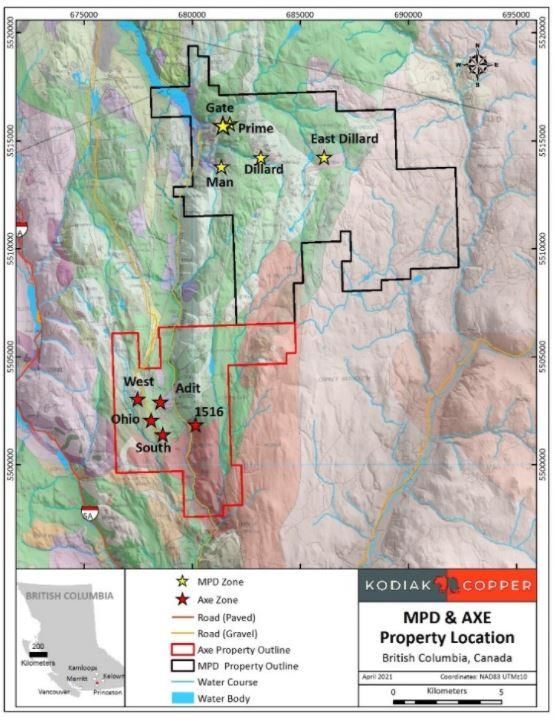

Kodiak Copper (TSXV: KDK; USOTC: KDKCF)

By announcing a deal with Orogen Royalties

to take a 100% interest in that company’s Axe

property, KDK has added another ~5,000

hectares of property on the south side of

MPD.

The move adds to the number of “Gate-like”

copper-porphyry centres for KDK to test along

southern BC’s Quesnel Trough. Axe comes

with four zones of known porphyry-style

mineralization and includes almost 25,000

metres of historic drilling from work going

back more than five decades.

Highlights from that work include 49.5 metres

of 0.31% copper and 1.3 g/t gold and 124

metres of 0.38% copper and 0.22 g/t gold.

Those aren’t exciting intercepts but neither

were the shallow hits at MPD before Kodiak

came along and, based on alteration

18vectoring and geophysical targets, drilled deeper and hit much better grades. As at MPD, most of the historic

drilling at Axe was shallow. In addition, Axe contains the underexplored 1516 zone, which appears to have a

very similar geologic footprint to Gate.

Under the deal, KDK will issue Orogen 950,000 shares and make small payments, in either cash or shares, for

hitting the milestones from 5,000 metres of drilling to issuing a feasibility study on the project. It’s a cheap

deal and one that grows KDK’s overall footprint and kicks at the can to find another strong copper-gold

porphyry considerably.

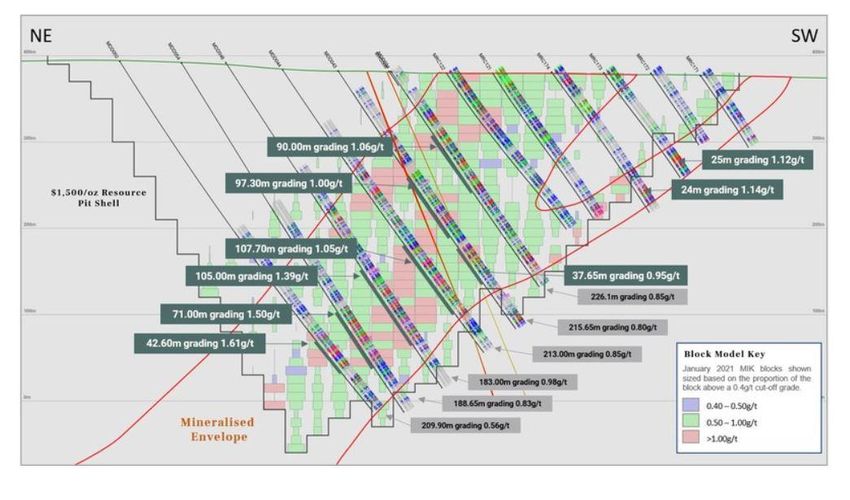

Montage Gold (TSXV: MAU; USOTC: MAUTF)

Fully 60% of MAU’s infill drilling program at Kone is now complete, and the company recently reported assays

from another 13 holes from this effort. The cross-section below shows some of the holes drilled on Kone’s

section 4950.

As you can see, they include some grades above the resource grades (e.g., 183 metres of 0.98 g/t, 105 metres

of 1.4 g/t, 71.0 metres of 1.5 g/t within 188.7 metres of 0.83 g/t, and 110.7 metres of 1.1 g/t.)

Infill results aren’t ever exciting, but these manage to hold a bit of splash with slightly better grades than the

resource average. MAU keeps marching ahead, pushing this project towards a build decision as quickly as

possible.

Northern Vertex Mining (TSXV: NEE; USOTC: NVHCF)

The Moss operation is getting efficient, as the table of operating results below shows. Relative to last year

they are mining more and producing more, even though grades are down because mine sequencing means

they don’t have access to some of the better ore right now.

19In all, Moss produced just shy of 10,000 gold-equivalent oz. in Q1 2021, a total that benefited from large

production benches now available on its West Pit. The stripping there is mostly done, which means head

grades may improve in coming quarters, although the ore at West is, on average, lower grade than the Center

Pit NEE was mining previously.

It’s great to see so much drilling at Moss (more than 15,000 metres of infill and exploration)! I’m particularly

keen to see the results from the work that targeted the intersection of the Moss and Ruth veins, targets where

NEE concentrated roughly half of that metreage. Drilling below the West, Center, and East pits will continue

later this quarter.

Meanwhile, at the Hercules project , the company completed some useful geophysical surveys that highlight

elevated silica alteration (higher resistivity) and zones of intense clay alteration (lower resistivity). These

identified at least 45 new targets on the project. When either of these types of alteration are also associated

with elevated potassium and low magnetic response (mineralizing fluids in these environments usually cause

magnetite destruction), the area is worth a look for gold.

NEE will certainly keep exploring Hercules, but even with this work done they have not laid out a drill plan as

yet. It’s not surprising, as there is more than enough reserve delineation and exploration work at the Moss

mine to keep them busy.

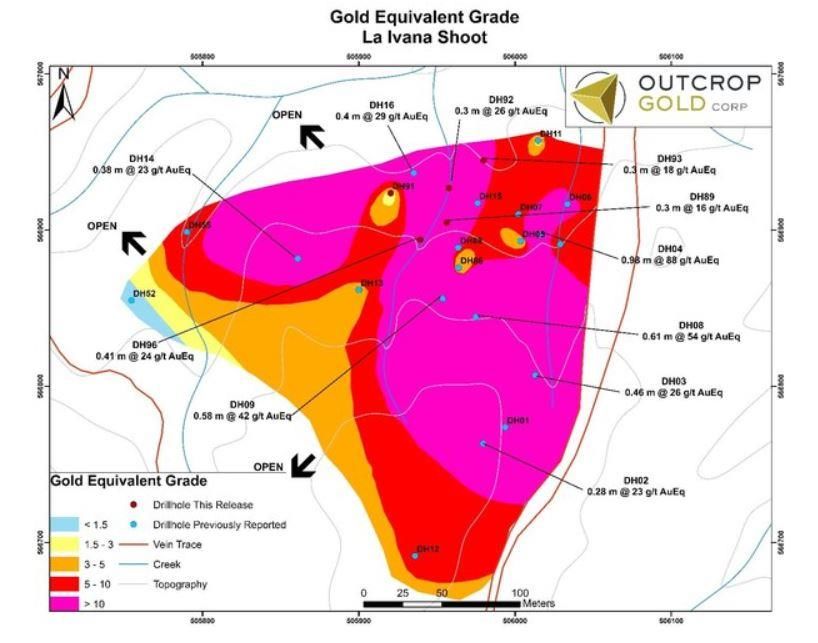

Outcrop Gold (TSXV: OCG; USOTC: OCGSF)

With the latest assays from Santa Ana’s La Ivana oreshoot, OCG has now traced the target for 320 metres at

surface and 310 metres down dip. The best result from this batch came from Hole 96, which cut 0.41 metres

of 24.4 g/t gold equivalent (1,785 g/t silver equivalent), part of a group of five holes that managed to extend

La Ivana another 50 metres to the north. Hole 92 hit two vein-shoot segments separated by 25 metres (0.46

metres of 3.2 g/t gold equivalent and 0.3 metres of 26.2 g/t gold equivalent). Yes, the intercepts at La Ivana

are narrow, but a stacked vein set can compensate for narrow widths and that’s what seems to be emerging

here.

20Initial exploration drilling on the Prias, Culebra and Paloma targets outlined predicted vein structures on each

target. At Prias, drilling turned up a shallow, 0.48-metre interval of 1.6 g/t gold equivalent. Not a high-grade

hit, to be sure, but indicative of the tenor of mineralization that helped OCG vector in on higher grade shoots

elsewhere at Santa Ana, so this is the potentially the start of something interesting. Remember that it takes

time and holes to find new high-grade shoots along known structures.

All that said…OCG’s share price has sucked of late, even as other silver stocks have gained. I talked to

management today about it and they don’t understand exactly what’s going on. One theory is that one or

several funds in the stock got perturbed when it took Outcrop six weeks to close its recent financing.

It’s fair enough to worry if a financing stays open for ages, as the most common reason is that the company

can’t find enough investors to fill the book. With Outcrop that was not the case. Rather, it was that the

Securities Commission told Outcrop – after they had announced the raise – that the technical report on Santa

Ana was insufficient and they needed to complete a new one.

The Commission doesn’t assess the state of technical reports for regular financings but Outcrop raised via a

prospectus offering, in order to avoid the four-month hold period. They thought it worth the extra hassle of

doing a prospectus because lots of funds shy away from hold periods; prospectus offerings therefore just

avoid that barrier.

Of course, it takes some time to write a technical report, and then for the Commission to review and stamp it.

That’s why the financing took so long to close.

For a fund manager to start selling because they see a financing not close quickly without calling the company

to find out why is pretty annoying. Even more annoying is that selling begets selling, so what might have

started as one fund manager exiting for a dumb reason seems to have become several.

21I can’t know this is the reason…but I can’t really come up with anything else. Today’s results were good, and

they came out on great day for silver, and yet OCG lost $0.02.

Bottom line: I can’t see any reason based in exploration results for Outcrop’s share price to have performed as

it has, in particular in the last few weeks. I can only hope that OCG’s steady stream of results – and generally

pretty good ones – can turn the tide.

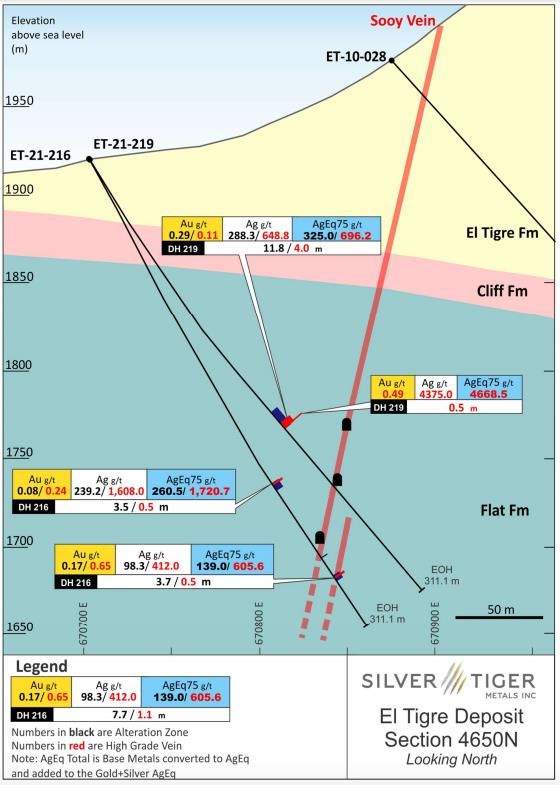

Silver Tiger Metals (TSXV: SLVR; USOTC: SLVTF)

Silver Tiger released another set of results from the Sooy vein area. The results looked good at first glance;

they looked significantly better after the company answered a series of questions I sent their way.

That process was a good reminder that it’s harder than it might seen to convey drill results, especially when

the target is a vein.

The Sooy vein is parallel to the main El

Tigre vein. It was close enough to the

old mine that it also saw some mining,

though like at El Tigre the old miners

took only the very highest grade

material from the middle of the vein.

Silver Tiger started drilling Sooy to see

how it evolved along strike and at

depth, below the old workings. And

they have been rewarded for their

efforts.

Sooy had returned some nice numbers

before yesterday’s news, showing a

system that certainly carried grade.

Yesterday’s results added clear scale

to the story of grade. Hole 219 was

drilled 250 metres south along strike

from the Sooy vein discovery hole

(hole 202, announced in early

February) and returned 11.8 metres

grading 325 g/t silver equivalent,

including 0.5 metres carrying 4,668.5

g/t silver equivalent. That’s a heck of a

hit. And interestingly it did not come

in the main Sooy vein but in a

hangingwall vein that Silver Tiger has

intercepted in three drill sections.

(Hole 219 did not return an intercept

from Sooy itself because it hit old

workings.)

22Hole 216 was also in the latest batch of results. It also ran into old workings on Sooy itself but returned hits

from the hangingwall and footwall veins – nothing too splashy but evidence of continued mineralization in

these veins.

Hole 217 stepped another 775 metres south o hole 219 and returned 7.3 metres of 221.1 g/t silver equivalent,

including 0.5 metres of 2,693.6 g/t silver equivalent, from the main Sooy vein.

(I should also note: Silver Tiger reports in silver equivalent grades because the veins carry silver, gold, copper,

and zinc, but the majority of the value – almost always better than 90% - is in silver, with a few more percent

from gold. The base metals contribute only slightly.)

The plan map below helps with context.

23Red lines are veins. Black lines are old workings, which means veins mined to 400 metres depth or so. You can

see the Silver Tiger drilled a set of holes around Sooy discovery hole 202 (the majority of the boxes on the left)

and is now working its way south. Hole 217 is a big step.

The biggest takeaways from yesterday’s news are:

Hitting such a strong intercept on a 1-km stepout is impressive. It adds to the evidence that El Tigre is

an extensively mineralized system, as opposed to one where value is really only present in high-grade

ore shoots (as is the case in most vein systems). At El Tigre, grade certainly fluctuates but to hit 2.7 g/t

silver equivalent in a 1-km step out is either very lucky (they blindly drilled right into a high-grade

shoot) or evidence that the vein carries good to great grade over major distance. From hole 217 to the

drilling at Benjamin to the north, the system strikes 2.2 km.

o Yesterday’s step out result is by no means the first indication of consisnte mineralization along

impressive strike extents. The old miners figured that out; their shallow workings cover almost

a kilometre of strike right around El Tigre and Sooy. But to keep drilling into good or great

grades along 2+ km of strike hammers home the point

Sooy is not a single vein. This is a point I needed explained better, as for the sake of simplicity and

clarity Silver Tiger did not include all intercepts from each drill hole on all cross sections. Had they done

so, it would have been visually apparent that drills are consistently hitting veins in both the

hangingwall and footwall as well.

It’s also important to note that halo mineralization around the veins creates intercepts 7 to 10 metres wide.

That’s wide enough to enable some kind of mechanized mining, rather than less efficient stoping. Of course

we need much more drilling and then a resource estimate and model before we can know this for sure, but

intercepts in the 7 to 10-metre range are becoming the norm.

Finally: look again at the plan map. The Silver Tiger team is really excited about the vein field to the north

(Fundadora, Protectora, Aguila, and whatever else might be up there. They have been drilling in this area and

have released some results, including some strong intercepts. I’m keen to see what they uncover.

This system has scale and strength. This team is phenomenal at exploring systems like this, as their track

record attests.

Vizsla Silver (TSXV: VZLA; USOTC: VIZSF)

VZLA has elected to move ahead with a spin-out of its copper assets in BC into Vizsla Copper. Existing Vizsla

Silver shareholders will receive one Vizsla Copper share for every three shares of VZLA held. The deal is

conditional on shareholder, provincial, and Venture Exchange approval and on the newco completing a $3.5

million private placement. With the shareholder meeting slated for June 15, the spinout should occur

sometime thereafter, subject to those other stipulations.

I really don’t think VZLA gets any credit for these assets, which if I’m right should mean VZLA shouldn’t lose

value by spinning these out. But the team wouldn’t be spinning them out unless they thought these assets

worthy of some attention, so there is upside potential in the new company. Free money!

----------------------------------------------------------------------------------------------------------------------

24EDITORIAL POLICY AND COPYRIGHT: Companies are selected based solely on merit; fees are not paid. This

document is protected by copyright laws and may not be reproduced in any form for other than personal use without prior

written consent from the publisher.

DISCLAIMER: The information in this publication is not intended to be, nor shall constitute, an offer to sell or solicit any

offer to buy any security. The information presented on this website is subject to change without notice, and neither

Resource Maven (Maven) nor its affiliates assume any responsibility to update this information. Maven is not registered as

a securities broker-dealer or an investment adviser in any jurisdiction. Additionally, it is not intended to be a complete

description of the securities, markets, or developments referred to in the material. Maven cannot and does not assess,

verify or guarantee the adequacy, accuracy or completeness of any information, the suitability or profitability of any

particular investment, or the potential value of any investment or informational source. Additionally, Maven in no way

warrants the solvency, financial condition, or investment advisability of any of the securities mentioned. Furthermore,

Maven accepts no liability whatsoever for any direct or consequential loss arising from any use of our product, website, or

other content. The reader bears responsibility for his/her own investment research and decisions and should seek the

advice of a qualified investment advisor and investigate and fully understand any and all risks before investing.

Information and statistical data contained in this website were obtained or derived from sources believed to be reliable.

However, Maven does not represent that any such information, opinion or statistical data is accurate or complete and

should not be relied upon as such. This publication may provide addresses of, or contain hyperlinks to, Internet websites.

Maven has not reviewed the Internet website of any third party and takes no responsibility for the contents thereof. Each

such address or hyperlink is provided solely for the convenience and information of this website's users, and the content

of linked third-party websites is not in any way incorporated into this website. Those who choose to access such third-

party websites or follow such hyperlinks do so at their own risk. The publisher, owner, writer or their affiliates may own

securities of or may have participated in the financings of some or all of the companies mentioned in this publication.

25You can also read