THE SIG DIGEST - Singapore University of Social Sciences

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SUSS INVESTMENT GROUP | SEPTEMBER 2020 | ISSUE #1

THE SIG DIGEST

FOREWORD GREEN FINANCE

By Dr Tan Eng Joo, Senior Lecturer,

Singapore University of Social Sciences

Faculty Advisor, SUSS Investment

Group

Bittersweet; deafening silence; open secret; humane

slaughter.

Is “green finance” also an oxymoron? After all, the term

“finance” often evokes an image of the callous,

calculating banker, a jarring contrast to the passionate,

empathetic environmentalist associated with the term

“green”. Indeed, protecting the environment, a global

public good, is a costly activity that seems to be at odds

with value maximization for an individual business. Green finance is defined as the use of financial products to

achieve both financial returns and sustainable outcomes. The

Yet, firms are becoming cognizant that environmental term has exploded in popularity in recent years. From “green

sustainability is increasingly intertwined with business bonds” that finance climate and environmental projects to the

sustainability. For some, it will be an existential concern stocks of socially responsible companies to Environmental,

in the near future. An unsustainable business cannot Social and Governance (ESG) Exchange Traded Funds, the

continue to create value. As policymakers realize that number of avenues available for green investors has

finance is a powerful force that can be leveraged in skyrocketed, with the trend showing no signs of slowing.

fighting climate change and put money where the mouth

is, businesses will better appreciate the alignment between Traditional energy companies are facing mounting pressure to

environmental sustainability and value maximization. transition away from fossil fuel production amidst investor

activism and rising competition from renewable energy

Rare is the breed of students who care about companies. Some companies such as Shell and BP have

environmental sustainability. Even rarer is the breed of proactively made concrete steps toward a greener future, while

finance students who do. As a step in this direction, the others such as ExxonMobil and Chevron have lagged behind.

SUSS Investment Group (SIG) has chosen to dedicate the In this inaugural issue of the SIG Digest, we explore what the

inaugural issue of its newsletter to covering companies future holds for green finance.

that are making an environmental impact.

In our Equity Research column, we analyse Bonheur ASA, a

The SIG was formed in 2017 by a few passionate Norway-based holding company specialising in the marine and

individuals and has grown to a 21-strong group. The renewable energy sector. We examine past and upcoming

group has assisted in organizing the My Money @ events that influence Bonheur’s profitability and market

Campus talk and the CFA Research Challenge internal valuation.

selection. Its members have represented the university for

the CFA Ethics Challenge, CFA Research Challenge, In our Global Macro Research column, we discuss renewable

Eurasia Asset Management Challenge, GIC Stock Pitch energy trends and the prospects of green investing. We also

Challenge, and the McGill International Portfolio explore a case study of the transition of a traditional Oil & Gas

Challenge. company, British Petroleum, towards clean energy.

Disclaimer: Information in this newsletter is for educational purposes only

This newsletter is the SIG’s latest initiative. I hope you and do not constitute investment advice.

will enjoy reading it and look forward to more exciting

Editor

initiatives from the group. Chia Rui Yang

For enquiries on collaboration or partnership VP (External Relations)

opportunities, please contact sussinvest@gmail.com. rychia001@suss.edu.sg

Page | 1

SUSS INVESTMENT GROUP | SEPTEMBER 2020 | ISSUE #1 Equity Research

Bonheur ASA (OB: BON) | Industry: Industrial Conglomerates

A rising star in global energy transformation: SIG initiates coverage with a Buy Basic Information

recommendation on Bonheur ASA, with a target price of NOK 287.89, Recommendation BUY

representing an upside of 26.0%. Current Price NOK 228.00

12 Mth Target Price NOK 287.89

Business Summary Upside 26.0%

Headquartered in Oslo, Bonheur ASA is listed on the Oslo Stock Exchange and

1 Year Price vs OSLO OBX (Rebased)

has long-term investments in three main industries – shipping, energy, and leisure.

The group’s key business activities, wind energy generation, wind turbine 1.40

installations, and cruise are carried out by Fred. Olsen Renewables (FORAS),

Fred. Olsen Ocean (FOO), and First Olsen Holding AS. Bonheur’s wind energy 1.20

business has entered its growth stage with new technology and business 1.00

opportunities in North America and Asia. With a premium branding, FOCL is

approaching maturity. In 1Q20, the group’s four business segments generated 0.80

NOK 492 million in revenue. Offshore wind installation contributed the most to 0.60

the group’s revenue (32%), followed by Renewable energy (29%), Cruise line Volume Bonheur ASA

(25%), and other investments (14%). OSLO OBX

Source: Yahoo Finance, Team

Highlights of the year:

Key Financials

FOWIC clinched another Taiwanese offshore wind project in March 2020.

The group is commissioned to transport and install wind turbines for the 600MW Market Cap (NOK, mm) 9612.2

Shares Out. (mm) 42.5

Changfang and Xidao offshore wind complex.

Avg 3M Daily Vlm 0.07

Dividend payout in 2019 increased from NOK 2 per share to NOK 4 per Float % 46.7%

share, a 100% jump. For several years, Bonheur ASA’s annual dividend has Enterprise Value 14,137.6

remained stagnant at NOK 2 per share. A NOK 4 per share dividend payout last P/E Ratio -

year reflects outstanding management, while the declared forward dividend of Dividend Yield % 1.9%

52 Wk High/Low 232/134

NOK 4.30 per share is a sign of the group’s confidence for growth.

Our take on Bonheur: Major Shareholders

Bonheur can anticipate revenue growth alongside the burgeoning renewable INVENTO AS 28.99%

QUANTRO A/S 20.54%

energy sector. According to our research, renewable energy generation and

FOLKETRYGDFONDET 4.31%

consumption is looking positive in regions that renewable energy and offshore

Other shareholders 46.16%

wind installations have set foot in – Europe, North America and Asia. We see that

the renewable energy industry has a very positive outlook with renewable energy

Full report: bit.ly/34aF3ek

generation forecasted to double in the current decade.

Strong customer loyalty and innovative programs can bring further growth to Analysts

the Cruise Business. Cruise line remains competitive with its longstanding

Cassandra Tan Tung Yan

customer loyalty. The cruise line found opportunities amidst COVID-19 with its

cassandratan003@suss.edu.sg

innovative virtual cruising programs that makes its name unforgettable.

Charlton Koh Yong En

Valuation. We derived a 12M target price of NOK 289.89 through blended DCF

VP (Global Macro Research)

valuation and SotP relative valuation.

charltonkoh001@suss.edu.sg

Financial Valuation and Key Metrics:

Daniel Nyau Zhi Mo

Year FY19A FY20E FY21E FY22E FY23E FY24E President; VP (Equity)

danielnyau001@suss.edu.sg

Revenue (mm) 7,834.7 6,314.7 8,921.7 9,822.1 10,866.1 12,027.5

Rev. Growth 15.5% -19.4% 41.3% 10.1% 10.6% 10.7%

Net income (mm) (343.1) (40,.4) (319.8) (315.9) (11.7) 19.4 Dione Goh Wen Hui

ROA (%) -174.7% -20.6% -162.8% -160.8% -6.0% 9.9% dionegoh001@suss.edu.sg

ROE (%) -2.9% -0.3% -2.8% -2.9% -0.1% 0.2%

EV/EBITDA 11.8x 11.1x 4.2x 4.6x 3.8x 3.4x

EV/REVENUE 1.6x 2.3x 0.6x 0.7x 0.7x 0.6x Song Bing Heng

Dividend Yield 12.6% 11.8% 12.7% 13.7% 14.7% 15.8%

bhsong001@suss.edu.sg

Page | 2

SUSS INVESTMENT GROUP | SEPTEMBER 2020 | ISSUE #1 Global Macro Research

Market Outlook: The Green Recovery

Summary In contrast, Europe’s clean energy investments peaked in

2011 [Figure 5], with no signs of growth for 8 years. In

As a vital resource in our lives, energy has spurred many modern Europe, Wind energy is sub categorised into onshore, with

advancements. Still, with rising concerns about global warming and wind turbines installed on land, and offshore, with wind

sustainability, traditional energy companies are pressured to find turbines situated in water bodies. The popularity of

alternative energy sources to avoid obsolescence. In this article, we offshore wind has skyrocketed in recent years with

analyse renewable energy trends and a case study of the transition technological advancements as offshore wind speeds are

towards renewable energy in a traditional oil & gas (O&G) known to be higher and more consistent. By harnessing

company, British Petroleum. We also examine the benefits and the 3 sea basins surrounding Europe (the Baltic, the North

drawbacks from the adoption of clean energy. Sea and part of the Atlantic), Europe is poised to increase

its clean energy investments through offshore wind. Data

from the IEA indicates that the increasingly competitive

Background Information offshore wind projects are on course to attract trillions of

A survey conducted by the Pew Research Center in November 2019 dollars in investments till 2040.

revealed that 77% of Americans believe that developing “alternative With the COVID-19 pandemic devastating the global

energy” is of utmost importance. A separate survey by economy, governments have passed massive bills and

BloombergNEF observed an exponential trend in clean energy over stimulus packages, rivalling those seen in the Global

the past 10 years, where a cumulative 59.5 GW have been purchased Financial Crisis (GFC) of 2008. The ongoing crisis

representing a CAGR of 51.8%. Interestingly, the major players are presents an opportune moment for a strategic ‘Green

tech companies such as Facebook, Google and Amazon, followed by Recovery’. Back in 2008 after the GFC, 16% of global

traditional O&G companies. We believe that large tech companies are stimulus was spent on green recovery with governments

aggressively pursuing renewable energy agreements due to investors’ giving subsidies for renewable energy and funding for

rising ESG concerns. Traditional O&G companies are also shifting R&D of clean tech (e.g. electric vehicles). Although

towards cleaner energy by utilising solar/wind energy to power oil renewable electricity capacity is forecasted by the IEA to

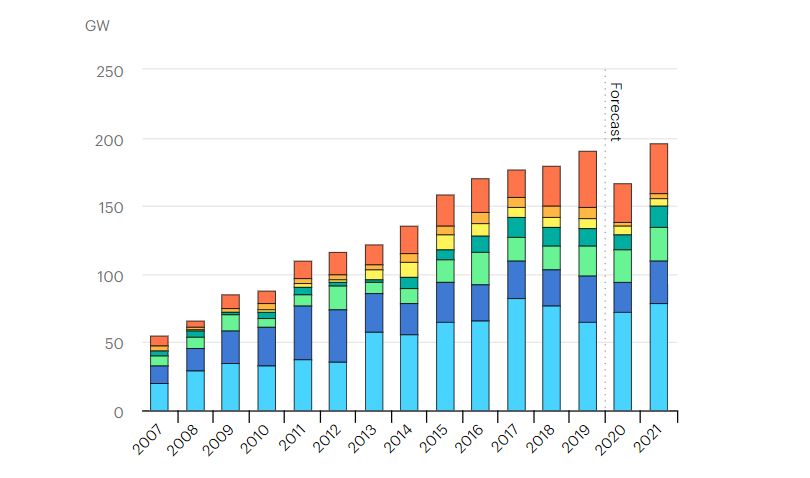

mining operations with investor sentiment in mind and to diversify decline by 13% in 2020 [Figure 6], we attribute the

their individual exposure from unsystematic energy disasters. Overall, decline to systematic factors such as policy uncertainty

from 2006-2019, new clean energy investments across the globe are and market developments.

experiencing a steady upward trend, with no signs of slowing down in

the coming years [Figure 2]. Many countries still relate falling emissions with a

faltering economy, although it has been proven to not be

the case. Work is still needed to educate and ensure that

Clean Investments Trends by Region people see a clear path to high quality alternatives so as to

achieve a sustainable future.

APAC has outpaced the world in renewable energy dollar

investments, with a CAGR of 10.7% from 2009-2019 compared to *Refer to Appendix for figures

0.46% and 7.8% in EMEA and America respectively [Figure 3].

To illustrate its magnitude, BlackRock's global Head of Renewable

Analysts

Power David Giordano highlighted that for every $10 spent

globally on new renewables capacity, $4 goes towards APAC. Aaron Luke Devarajan

Contributing to APAC’s popularity among green investors are the VP (Global Macro Research)

attractive 20 year feed-in-tariffs – payments to consumers for kxdeverajan001@suss.edu.sg

supplying excess clean energy to the grid – for the wind and solar

markets in Taiwan, South Korea and Japan. Countries with high Bryan Lim Bei En

renewable energy subsidies would likewise have high feed-in- bryanlim006@suss.edu.sg

tariffs and the opposite holds true as well. Charlton Koh Yong En

In other regions, the US and Europe appear to diverge on clean VP (Global Macro Research)

charltonkoh001@suss.edu.sg

energy investments [Figure 4 & Figure 5]. The US exhibits a

positive trend over the past 10 years, indicating increasing clean Shane Joachim

energy investments. Investments in wind have eclipsed investments shanejoachim001@suss.edu.sg

in solar since 2014, a likely result of wind turbines being generally

more efficient – a single wind turbine can generate the same Quek Guang Xuan, Bryan

amount of kWh as a thousand solar panels. bryanquek002@suss.edu.sg

Page | 3SUSS INVESTMENT GROUP | SEPTEMBER 2020 | ISSUE #1 Global Macro Research

Figure 1: Renewables share of

A Case Study: British Petroleum (BP)

power generation by BP

In this case study, we analyse British Petroleum (BP), best chronicled as one of the

largest publicly traded oil companies in the world and a pioneer among titans, first

adopting clean energy into renewable energy sources as early as 1995 [Figure 1]. This

acceleration towards clean energy generation is largely due to immense public pressure

and scrutiny.

For example, in 2010, BP experienced the Deepwater Horizon oil spill. The oil spill

covered more than 112,000km2 of the ocean's surface with currents spreading the

spillage across 2,100km. This resulted in catastrophic effects on the environment with

the deaths of countless wildlife.

Figure 2: BP Share Price in 2010

The financial consequences were tremendous to BP. With 130 lawsuits filed against

them, BP’s share price plummeted [Figure 2]. Reportedly, US$11.6 billion was paid out

in reparations to coastal states with projected losses estimated at US$22.7 billion. In

addition, BP had to set up a US$2.3 billion fund for seafood & fishery business for the

job losses incurred by oil spill.

The Deepwater oil spill served as an expensive catalyst for BP to review their energy

sources and diversify their energy provisions. 10 years after the worst oil spill in human

history, it has taught large oil companies that ESG investing is not just a public relations

move, but also a growing market [Figure 3].

More recently, BP plans on cutting up to $17.5 billion from the value of their oil and

Figure 3: BP’s Renewable Share of

gas assets after their in-house research predicted that the pandemic may affect the Power Generation by Region

global oil demand for the next 30 years. This big move had to be executed to illustrate

the impact of the COVID-19 outbreak on the global economy as well as the increased

effort to build a better environment to be in line with the goals of the Paris Agreement,

as said by the CEO of BP, Bernard Looney.

Such traditional energy companies are constantly pressured by shareholders who want

to see ESG compliance and the practicing of responsible and sustainable operations.

The growing importance is also seen when Bloomberg announced the launch of the US

equity benchmark capabilities which aims to act as a basis for the Bloomberg SASB

ESG Index family. This product would also focus on realising the SASB’s vision of

“materiality-based ESG”. This materiality-based ESG by SASB aims to identify

financially material issues – issues which are more likely to make an impact on the

financial condition or operating performance of a company.

With renewables being the fastest-growing energy sector, BP has established a portfolio of renewable fuels, power and products.

Currently, they are also developing new business models in sectors such as the low carbon power and digital energy. These are

strategic efforts made by BP as it aims for net zero emissions by 2050 or earlier:

• Partnerships to maintain adherence to ESG criteria and • Led Series A funding in Grid Edge (Oct 2019), whose

permit use of alternative sources of energy. software predicts, controls and optimises a building’s energy

profile reducing carbon emissions by 10-15% on average.

• Invested in joint venture with DuPont (Apr 2017) producing

alternative fuel sources (bio-isobutanol) from corn. • Invested in joint venture with Bunge (Dec 2019) that

produces renewable energy from its biofuels manufacturing

• Increased stake in Lightsource BP, which aims to develop sites. Venture is now 2nd largest operator by effective crushing

10GW of solar projects by 2023. capacity in Brazil’s bioethanol market.

With the diversified portfolio illustrated above, BP aims to become an industry leader in clean energy. By bringing together the

expertise and assets of the partnerships and ventures, BP has a clear direction to improve and innovate more options for a better

environment, and also to prevent future energy disasters from crippling their operations. Overall, BP has a promising macro outlook

in terms of contributing towards the green recovery and providing a more sustainable future.

Page | 4SUSS INVESTMENT GROUP | SEPTEMBER 2020 | ISSUE #1 Appendix

Figure 1: Global Corporate Buying Clean Energy Power Purchase Agreements (PPA)

Source: BloombergNEF, U.S. Global Investors

Figure 2: Global New Investment in Clean Energy (2006-2019)

Source: BloombergNEF

Figure 3: Global New Investment in Clean Energy by Region (2006-2019)

Source: BloombergNEF

Page | A1SUSS INVESTMENT GROUP | SEPTEMBER 2020 | ISSUE #1 Appendix

Figure 4: United States New Investment in Clean Energy by Sector (2006-2019)

Source: BloombergNEF

Figure 5: Europe New Investment in Clean Energy by Sector (2006-2019)

Source: BloombergNEF

Figure 6: Renewable Electricity Capacity Additions, 2007-2021, Updated IEA Forecast

Source: International Energy Agency, 2020

Page | A2You can also read