The Wall Street Consensus - Daniela Gabor (UWE Bristol) - OSF

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Wall Street Consensus

Daniela Gabor (UWE Bristol)

Abstract: The Wall Street Consensus (WSC) is an elaborate effort to reorganize

development interventions around selling development finance to the market. The

Billions to Trillions agenda, the World Bank’s Maximizing Finance for Development

or the G20’s Infrastructure as an Asset Class all call on international development

institutions and governments of poor countries to ‘escort capital’ – the trillions of

institutional investors – into ‘investable development bonds’, preferably in local

currency. For this, the 10 WSC commandments aim to simultaneously reorganize

local financial systems around bond market-based finance and forge the de-risking

state. The state derisks bond finance for institutional investors by extending

guarantees and subsidies to cover (i) demand risks attached to user-fees for (PPP)

infrastructure, (ii) political risk attached to policies such as nationalization, higher

minimum wages and climate regulation, (iii) climate risks that may become part of

regulatory frameworks as material credit risks and (iv) bond market (liquidity) risks

that complicate foreign investors’ exit from development assets. The WSC narrows

the scope for a green developmental state that could design a just transition to low-

carbon economies.

1

INTRODUCTION

‘….we have to start by asking routinely whether private capital,

rather than government funding or donor aid, can finance a

project. If the conditions are not right for private investment,

we need to work with our partners to de-risk projects, sectors,

and entire countries’.

Jim Yong Kim, World Bank Group President (2017)

The international development literature made two notable predictions over the past

twenty years. It announced the (overdue) death of the Washington Consensus

paradigm (Gore, 2000; Rodrik 2006). The Washington Consensus, anchored in the

work of John Williamson (1990, 1993), outlined ten policy areas that would set poor

countries’ economies on firm market foundations, under a ‘holly Trinity’ of

macroeconomic stabilization through lower inflation and fiscal discipline;

liberalization of trade and capital flows, of domestic product and factor markets; and

privatization of state companies. After the East Asian crisis, the poor performance of

countries closely wedded to the Washington Consensus prescriptions (Rodrik, 2006;

Fischer, 2019) and the revolt of notable insiders such as Joseph Stiglitz, Gore (2000)

predicted that the holy Trinity would make room for an Asian developmental model,

updated to the ‘age of global money’ (Yanagihara and Sambommatsu, 1996). The

collapse of Lehman Brothers brought the second notable prediction: the end of the age

of global money and its ‘foreign finance fetish’ (Birsdall and Fukuyama, 2011).

Both predictions turned out wrong. Financial globalization is alive and well, and sets

the particular context in which ‘international development’ is pursued in the

21st century. As Lord Stern, of the influential G20 Eminent Persons Group, put it: ‘the

challenge of achieving the SDG is in large measure that challenge, of fostering the

right kind of sustainable infrastructure’, for which, ‘you have to have good finance,

2

the right kind of finance, at the right scale, at the right time’1. The ambition is spelled

out in the Billions to Trillions agenda, the World Bank’s new Maximising Finance for

Development (MFD) agenda, or the G20 Infrastructure as an Asset Class agenda,

which aim to create investable opportunities in poor countries that can attract the

trillions of global institutional investors and orient them to the SDG ambitions. For

instance, the MFD promises global institutional investors $12 trillion in market

opportunities that include “transportation, infrastructure, health, welfare, education’,

to be minted into investable securities via Public-Private Partnerships2.

This shift in the development agenda is here conceptualized as the Wall Street

Consensus, an emerging policy paradigm that reframes the (Post) Washington

Consensus (Öniş and Senses, 2005) in the language of the Sustainable Development

Goals, and identifies global finance as the actor critical to achieving the SDG. To

explore its contours, the article draws on previous scholarly accounts of the

financialisation of development, understood as strategies to ‘escort’ (speculative)

capital to poor countries into derisked asset classes (Carroll and Jarvis, 2014; Baker

2015; Mawdlsey, 2018). While these micro-level accounts emphasize the role that

MDBs or donor agencies play in derisking, the role of the state and its macro-

financial policies is largely ignored. To fill in this gap, the article draws on a critical

macrofinance (CMF) approach concerned with the co-evolution of global finance and

the macro-institutions of the state (Gabor, 2020). This co-evolution reflects deeply

political processes through which private finance seeks protection from systemic risks

and accommodation for new asset classes (Dafermos et al, 2020). CMF takes as

analytical starting point the transformation of global finance, and fleshes out its

consequences for our understanding of credit creation, macroeconomic policies, and

of development strategies in the age of financial capitalism.

Through this lens, the WSC is an attempt to re-orient the institutional mechanisms of

the state towards protecting the political order of financial capitalism against climate

justice movements and Green New Deal initiatives (Wainwright and Mann, 2018). It

1 http://live.worldbank.org/implenting-SDGs-changing-

world?CID=ECR_TT_worldbank_EN_EXT_AM2018-sdgs

2

The World Bank’s first Head for Maximising Finance for Development was previously Practice

Manager for PPPs at the World Bank https://www.worldbank.org/en/about/people/c/clive-harris.

3is an organized attempt to forge what conceptually can be conceived as the de-risking

state that ‘escorts’ global finance to investible assets in the Global South.

The creation of investable assets requires a two-pronged strategy: (a) enlist the ‘de-

risking’ state into de-risking new ‘SDG’ bond classes created via Public-Private

Partnerships in infrastructure projects, and (b) re-engineer local financial systems in

the image of US market-based finance to allow global investors’ easy entry into, and

exit from, new SDG bonds (see also Mawdlsey, 2018). This is what lies behind the

World Bank’s ambitions to crowd in private investors and create new markets, coded

into what institutional investors describe as ‘a cultural shift to a broader de-risking

philosophy’ (Deau, 2019: 259). Thus, Wall Street Consensus marks a new moment in

capitalist accumulation, from what David Harvey (2003) termed ‘accumulation by

dispossession’ to accumulation by de-risking.

The de-risking state does not break with the (Post-)Washington Consensus state, a

state complicit in pushing the holy trinity since Margaret Thatcher (Bruff, 2014).

Rather, it builds on the Post-Washington Consensus acceptance that the state is

necessary to correct market failures, through regulation and poverty alleviation (Öniş

and Senses, 2005). The WSC asks the state to compensate global finance confronted

with complex risk landscapes in SDG assets: (i) demand risks attached to user-fees for

PPP infrastructure, (ii) political risk attached to policies that would threaten profits

such as nationalization, higher minimum wages and climate regulation, (iii) climate

risks that may become part of regulatory frameworks as material credit risks and (iv)

bond market and currency risks that complicate foreign investors’ exit.

The practice of de-risking goes back to the developmental state, but its politics

changed. The developmental state de-risked for domestic manufacturing companies in

priority, mainly export, sectors (Wade, 2018). It was successful where it had the

capacity to discipline local capital (Öniş, 1991), to govern market failures through

evolving institutional structures (Haggard 1990, 2018) and to generate elite support

for the developmental state as a political project (Mkandawire, 2001). In contrast, the

WSC state de-risks for global institutional investors without the embedded autonomy

of the developmental state (Evans, 1991). It lacks an autonomous strategic vision,

4unless ‘more infrastructure’ can be described as such, and has fewer tools to

discipline the global captains of finance industry.

The content of structural transformation also changes through subtle norm

substitution processes à la Washington Consensus (Kentikelenis and Babb, 2019).

WSC proponents, from MDBs to states in the Global North and South, seek to

normalize the appropriateness of a market-based financial structure in technocratic

forums away from public scrutiny. Structural policies shift from the manufacturing

sector, as in the traditional developmental states (Wade, 2018), to the local financial

system. The WSC consolidates several global initiatives to restructure financial

systems in developing and emerging economies (DEE) towards securities market-

based finance or shadow banking (IMF and World Bank, 2020; also Gabor, 2018),

where global and domestic institutional investors can easily purchase local bonds

(securities), including infrastructure-backed securities, and finance as well as hedge

their securities positions via repos and derivative markets. In pushing for financial

structure change, institutional investors seek to preserve their ability to divest from

local (SDG) securities, an implicit recognition of the limits of the de-risking state. De-

risking capacity can be quickly eroded by shocks such as climatic or pandemic events.

For this, the WSC aims to re-orient the central bank into tackling bond market risks

and currency markets.

The emerging WSC is a template, but not a straightjacket. It requires local political

coalitions to consolidate around the de-risking state, to deliver on its demands or to

diffuse political contestation. Indeed, the WSC downplays the costs and risks of the

macro-financial order it seeks to impose. It engineers financial globalization that

comes with increasing vulnerability to volatile capital flows (Rey, 2015) and also

threatens developmental policy space, by narrowing the scope for a green

developmental state that could design a just transition to low-carbon economies,

where the burden of structural change does not disproportionately fall on the poor.

To trace these reconfigurations, the paper explores the policy documents produced by

WSC institutions (World Bank, other MDBs, the IMF) and private finance. The WB

intends to mainstream the MFD/Cascade approach across its operations, using as pilot

the infrastructure sector, broadly understood. By 2020, it had introduced a new tool

5for the MFD approach, entitled Infrastructure Sector Assessment Programs

(InfraSAP) and produced InfraSAPs for several MFD pilot countries: Egypt, Nepal

Sri Lanka and Vietnam (for the energy sector in the last two)3. The paper finally

provides a short reflection on the possible trajectories of the Wall Street Consensus

during and after the COVID19 pandemic.

THE WALL STREET CONSENSUS: A BRIEF TIMELINE

The Wall Street Consensus has its origins in the 1980s, when donor governments

turned to ‘de-risking’ seeking to realign policies with the Washington Consensus. One

such pioneer, the German development bank Kreditanstalt für Wiederaufbau (KfW),

persuaded German politicians that traditional lending to recipient governments should

be repurposed to finance high-risk tranches of new financial instruments. This would

circumvent local institutions vulnerable to capture, increase KfW’s ability to closely

control development interventions and eventually involve private finance more

systematically (Volberding, 2018). This logic remains dominant, as for instance in

Germany’s Compact with Africa (see Banse, 2019).

In parallel, Germany pushed the local bond markets agenda within the G8 (Gabor,

2018), recommending the elimination of capital controls that hamstrung portfolio

inflows into local bond markets, and promoting local resource mobilization. The latter

measure called for privatizing segments of the welfare state to create a domestic

institutional investor base, including private pension funds, mutual funds and

insurance companies, later conceptualized as shadow banking or market-based

finance (Pozsar, 2013; Storm, 2018).

At first, the global financial crisis stopped the Wall Street Consensus it its tracks.

Rich and poor countries alike abandoned the celebratory narrative of free capital

flows for a new vocabulary of shadow banking, global financial cycles, carry-trade

speculation, interconnectedness on the balance sheet of global banks (Rey, 2014;

3

The publication of InfraSAP for Indonesia, one of the keenest supporters of the MFD approach,

initially expected in January 2019, was delayed after public outcry over a leaked draft.

6Gallagher 2015; Bortz and Kaltenbrunner, 2018). As the IMF dropped its notorious

opposition, scholars celebrated the normalization of capital controls as the ‘the single

most important way in which policy space for development has widened in several

decades’ (Grabel, 2011:806). One after another, DEEs imposed controls on portfolio

flows into local securities markets, upending an international development discourse

focused on selling development finance to institutional investors via portfolio inflows.

However by 2015, the WSC was back on track. The crisis narrative became gradually

sensationalized along ‘greedy bankers’ lines, downplaying the structural roots that

would have required significant reform, particularly of shadow banking (Gabor,

2019). Indeed, shadow banks – global asset managers, hedge funds and other

institutional investors – are crucial actors in the political alliances backing the WSC,

alongside MDBs, global regulators, elite technocrats (see the Eminent Persons Group

2018) and governments of high-income countries. The world largest financial

institution, Blackrock, relied on ‘ferocious lobbying’ to successfully fight the

Financial Stablity Board’s (FSB) attempts to regulate asset managers as systemic

shadow banks in 2014-2015. As a result, the FSB announced that it would shift its

approach to transforming shadow banking into resilient market-based finance.

The resilience of market-based finance reflects the limited institutional incentives that

either central banks or politicians have to pursue deep structural reforms. Post 2008,

central banks protected their powerful position in the macrofinancial architecture by

unconventional monetary policies such that stabilized market-based finance without

reforming it (Hannoun, 2012; Gabor, 2016). Equally important is that central banks

buried one important political aspect in technocratic discussions: market-based

finance entangles monetary, fiscal, and financial stability policies. Sovereign debt is

“vital to the functioning of the financial system, analogous to the function of money

in the real economy,” stressed the ECB’s Benoît Cœuré (2016:3). But if sovereign

debt is core to market-based finance, then central banks’ financial stability mandates

structurally require them to protect governments from volatility in sovereign bond

markets (Gelpern and Gerding, 2016). Paradoxically, it hardwires austerity into policy

frameworks: caught between ‘independent’ central banks reluctant to intervene and

‘bond vigilantes’ threatening higher financing costs should structural reforms of

finance be enacted, elected politicians embrace ‘fiscal discipline’. Austerity reinforces

7market-based finance: hesitant taxation of big capital, asset-based welfare and passive

index investment all feed into institutional investment in the age of asset management

(Haldane, 2014).

The Wall Street, rather than the Frankfurt or London, Consensus reflects the structural

importance of US-based institutional investors and their asset managers, the ‘new

powerbrokers of modern capital markets (Fisch et al, 2018). The ‘hidden power’ of

the new ‘captains of finance industry’ extends from their influence over corporations

as majority shareholders (Fichtner et al. 2017), to partnerships in global development

initiatives such as the G20 Infrastructure as an Asset Class initiative 4 , and their

growing involvement in national infrastructure, such as Blackrock in Mexico, for

some a case of corporate colonialism5.

THE TEN COMMANDMENTS OF THE WALL STREET CONSENSUS

The Washington Consensus proposed 10 policy lines guided by the holy trinity of

stabilization, privatization, and liberalization. These reimagined development for the

international liberal order, attributing policy failures to domestic factors rather than

global structures, and shifting the overarching ambition from long-run structural

transformations to a more efficient distribution of resources (Gore, 2000). A similar

set of policies can be traced into the emerging WSC (see Table 1).

4 See Blackrock (2015).

5 Between 2012 and 2018, Blackrock was a prime beneficiary of president Pena Nieto’s PPP-

driven infrastructural projects, acquiring infrastructure assets through revolving door

relationships. In his campaign, the left-wing Lopez Obrador denounced Blackrock as white-

collar financial mafia, but gave up the campaign promise to review Blackrock PPP contracts

once he won the presidency in 2019 (Blackrock Transparency Project, 2019).

8Table 1: The 10 commandments of the Wall Street Consensus

Washington Consensus Wall Street Consensus

1. Fiscal discipline, Central bank 1. Fiscal discipline, central bank independence

independence

2. Public spending: primary education, 2. Public spending: de-risk new asset classes in

primary health, public infrastructure education, health, transport, energy

‘Infrastructure as an asset class’

3. Tax reform: lower marginal rate, broader 3. Sustainability reform: ESG criteria

base

4. Macro-finance policy: replace 4. Sustainable local currency bond finance: engineer

developmental banking with market-based market-based finance, prioritize securitization, support

interest rates securities prices (market-maker of last resort)

5. Exchange rate: either market-determined 5. Hedger/swapper of last resort to de-risk currencies for

or ‘competitive’ according to equilibrium (institutional) investors

theories, capital account liberalization

6. Trade liberalization 6. Financial globalization (no capital controls)

7. FDI promotion 7. Portfolio flows promotion

8. Privatization 8. Privatization of pension funds for domestic resource

mobilization

(Privatization) PPPs for ‘infrastructure as an asset class’

9. Competitiveness-enhancing deregulation 9. Removal of regulatory barriers to foreign-financed

PPPs

10. Property rights 10. Surveillance capitalism/Screen New Deal

The WSC revives the old developmental concerns with long-run structural

transformation, now framed through questions of ‘how to grow in an age of global

money’ that cannot move large pools of capital into small projects. This is no longer

the world of vulgar ‘efficiency gains will deliver growth’ neoliberalism (Rodrik,

2006), but neither is it a return to developmental states (Haggard, 2018). Rather,

structural transformation means policy-engineering SDG assets and a new market-

based local financial system that can attract global money, i.e. the money of global

9institutional investors, with specific mandates and practices of investment that need to

be accommodated.

The fiscal-monetary architecture

The WSC preserves the basic institutional macro-architecture of the Washington

Consensus: an independent central bank targeting inflation and a fiscally disciplined

Ministry of Finance. The separation matters in two ways. First, this macro-

architecture confers ‘infrastructural power’ to finance, since central banks rely on the

financial system to implement inflation targeting (Braun and Gabor, 2019). The

transmission mechanism of monetary policy becomes a stick to discipline advocates

of ‘shrinking to size’ financial regulation. Reforming (shadow) banks, it is argued,

will disrupt inflation targeting regimes.

Second, the ‘game of chicken’ between an independent central bank and the treasury

keeps at bay a developmentalist model that requires the central bank to work closely

with the developmentalist technocracy in charge of strategic industrial policy (Öniş,

1991). Such a developmentalist model further requires the central bank to impose

extensive capital controls in order to insulate the strategic industries, and the banking

sector financing them, from financial instability (Wade, 2018).

The focus on fiscal rectitude dictates the mechanisms for creating SDG asset classes:

user-pay/concession Public-Private Partnerships are framed as a strategic necessity

(Bull and Milkian 2019, also Foster 2017, World Bank 2018a, p13). PPPs are

functional to the de-risking state because their coding into law and public finances

allows a clandestine reorienting of public resources to private investors while

maintaining the ideological commitment to ‘fiscal responsibility’. PPPs are more

expensive than traditional public investment, but the illusion of fiscal effectiveness is

useful for governments and MDBs because it allows them to circumvent budgetary

restrictions and spend off-balance (Bayliss and van Waeyenberge, 2018), often in the

guise of progressive infrastructure policies, as ‘affordable housing’ PPP projects in

Brazil and Colombia suggest (Santoro, 2019). The state’s PPP commitments are

recorded as contingent liabilities, and do not count as public debt. PPPs become a ‘get

10out of jail’ card for politicians who can promise large infrastructure projects financed

by foreign institutional investors without increasing debt/GDP levels – at least in the

beginning.

Infrastructure is the hook for orienting institutional investors towards SDGs. While

institutional investors have long treated infrastructure as an asset class, they often

argue that large-scale infrastructure investments face significant hurdles. Around 60%

of infrastructure projects in emerging countries are not investible because their risk

architecture does not create the cash flow characteristics that institutional investors

prefer or are inscribed in their mandates6. Governments and MDBs are urged to plug

in those risk gaps through global policy initiatives such as the G20 Infrastructure as

an asset class (G20, 2018).

Behind the rhetoric of independent central banks and fiscal discipline, the Wall Street

Consensus imagines a new kind of state. The de-risking state puts its fiscal and

monetary arm in the service of de-risking bond finance for global institutional

investors.

Public spending: de-risking for institutional investors

The Washington Consensus codified what Williamson (1993) described as ‘belief in

fiscal discipline’, in direct opposition to ‘left-wing believers in Keynesian stimulation

via large budget deficits’, a perspective that became ‘almost an extinct species’ in the

1990s. Fiscal discipline meant cuts to subsidies for state-owned companies and for

basic consumption goods (e.g. gasoline, food). It prescribed spending on primary

education, primary health rather than high-tech hospitals in the capital, and on public

infrastructure investment.

6 For instance, a common rule of thumb is that pension funds need a minimum 4% return plus

inflation. See https://realassets.ipe.com/reports/infrastructure-as-asset-class-a-brief-

history/realassets.ipe.com/reports/infrastructure-as-asset-class-a-brief-

history/10026752.fullarticle

11The Wall Street Consensus similarly celebrates fiscal restraint. The MFD’s

operational tool, the Cascade Approach7, stresses that scarce fiscal resources cannot

deliver the SDGs 8 (World Bank, 2017). Instead it sets out a series of steps for

producing investible projects (see Figure 1), a theoretical armour for state

interventions in the guise of de-risking.

The Cascade Approach systematizes earlier efforts to promote renewable energy

markets in Africa through de-risking political technologies (Sweerts et al 2019;

Müller, 2020). Emerging out of a partnership between Deutsche Bank (DB, 2011) and

the UNDP, suggestively entitled ‘De-risking clean energy business models in a

developing country context’, the Global Energy Transfer Feed-in Tariffs (Get FiT)

Program proposed an innovative public-private de-risking partnership that absorbed

some of the risks faced by private renewable companies in developing countries. It

built on the UNDP’s work on regulatory barriers, including vertically integrated,

state-owned energy monopoly utilities, subsidised energy tariffs, to political risks or

lack of local financing. A better distribution of risks, DB argued, would see host

governments introduces tariffs and prioritise renewable energy in regulatory

framework, whereas the public sector in high-income countries and MDBs would

absorb counterparty credit risk (affecting agreements between state-owned wholesale

electricity purchaser and the private renewable energy suppliers) and other political

risks.

Somewhat paradoxically, the DB report did not discuss renewable energy markets

through the ‘infrastructure as an asset class’ lens, nor did it make reference to the

trillions of institutional investors. Instead, it identified the limited lending capacity of

local banking systems as a constraint, and green bonds as a mechanism for financing

MDBs. However, the UNDP (2013) report frames de-risking as the instrument for

escorting the trillions of global institutional investors to the Global South,

distinguishing between policy de-risking instruments (energy market regulations,

7 MFD complements the IFC’s strategy to “Create Markets” and MIGA’s 2020 strategy by

strengthening regulatory or policy frameworks, promoting competition, and achieving

demonstration effects, as well as a cross-WBG program to develop local capital markets (“J-

CAP”). (World Bank, 2017).

8

The World Bank’s (2018a) InfraSAP for Vietnam claims that the existing model for

financing energy infrastructure – state lending to state companies – is no longer viable

because of statutory public debt limits.

12institutional capacity etc.) and financial de-risking instruments (loan guarantees,

political risk insurance or public equity co-investments that would transfer the risks

that investors face to public actors, such as development banks).

The Cascade Approach simplifies the UNDP recommendations into a three-step

blueprint for de-risking SDG assets created via PPPs. It recommends lifting

regulatory or policy barriers to improve the risk-return profile, by for instance,

allowing user fees on highways. If reforms are insufficient to attract investors, then

subsidies and guarantees to de-risk the project might do so. Only when these

measures fail, it is suggested to opt for a fully public solution. Furthermore it has to

be ensured that SDG assets become investible, by identifying MFD-enabling projects,

i.e. those projects that support financial or capital market reform to unlock additional

sources of private financing (see IMF and World Bank, 2020).

Figure 1 The Cascade Approach in the WB’s Maximising Finance for Development

Source: Own representation of data from World Bank (2017)

13The revival of the PPPs in the age of institutional investors does little to address the

old criticisms of PPP models: extra demands on fiscal resources, concentration of PPP

activity in areas already benefiting from public investment, dubious effects on

poverty, access and inequality (Bayliss and van Waeyenberge, 2018), regulatory and

technical capacities hardly available to poor countries (Romero, 2018 9 ). But the

renewed PPP push in the Wall Street Consensus incorporates lessons drawn from the

early 2000s on how to systemically enlist the state in de-risking infrastructure assets.

In the early 2000s, infrastructure as asset class projects typically involved the

privatization of urban infrastructure in high-income countries, de-risking via complex

financial instruments, and global interlinking in the portfolio of global institutional

investors (Pryke and Allen, 2017). Yet local political contestation of contract terms

often threatened cash flows (Morag Torrance, 2008). Where new asset classes involve

uncertain flows of value, as Carruthers and Stinchcombe (1999) show for the US

mortgage market, the state can step in to generate predictability by first rendering

assets knowable and then ‘deriskable’. State agencies Fannie Mae and Freddie Mac

assembled mortgage loans for delivery to shadow banks, which in turn resorted to

securitization in order to create tranches with different risk profiles. Legal processes

code into law the new asset classes a la Pistor (2018).

The WSC takes these lessons to construct a broad range of techniques and

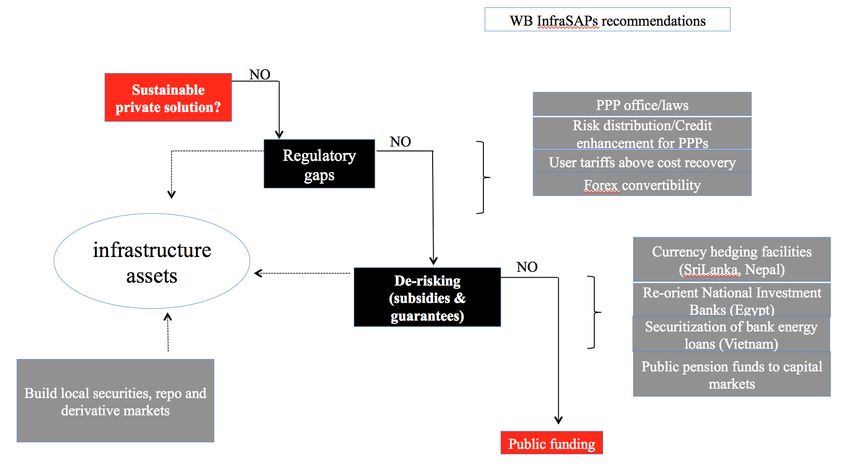

institutional mechanisms for de-risking. Indeed, the four InfraSAPs – for Egypt,

Nepal, Vietnam and Sri Lanka - identify PPPs as the key priority for the infrastructure

strategy and map a set of derisking avenues (World Bank 2018a,b; 2019a,b).

The WSC targets demand risk in PPP, user-fee based (social) infrastructure and

political risk that future governments might (re-)nationalize commodified

infrastructure or introduce tighter regulations, of for instance climate exposures or

labour markets.

Demand risks are a critical feature of PPP infrastructure because the WSC advises

transitioning from taxpayer funding to user fees, set above cost recovery. While this

9

https://www.devex.com/news/opinion-public-private-partnerships-don-t-work-it-s-time-for-

the-world-bank-to-take-action-92585

14remains the price liberalization agenda of the Washington Consensus, user fees do not

ensure predicable cash flows. Where the poor cannot afford the social infrastructure,

the de-risking state is expected to guarantee the cash flows that service the interest

payments on securities sold to institutional investors.

Such guarantees are written into PPP laws under the heading ‘risk distribution’. The

WB Egypt InfraSAP advises the Egyptian Electricity Holding Company (EEHC), the

national electricity utility, that PPP contracts should include Payment Security

Mechanisms that effectively guarantee payment flows against low demand. Similarly,

the Vietnam InfraSAP applauds the PPP law that commits public resources to cover

Vietnam risks, including offtake 10 and supply risks, currency convertibility and

inflation adjustment, and termination payment obligations, across social infrastructure

in ‘transportation; street lighting; water supply; waste treatment; power plants and

transmission; commercial infrastructure; social infrastructure facilities for health care,

culture, sports, industry, and agriculture’ (World Bank, 2018b: 23).

Figure 2 InfraSAPs recommendations: the Cascade Approach in practice

Source: Own representation of data from WB InfraSAPs.

10

In poor countries, the standard institutional arrangement in power infrastructure relies on a

state-owned utility as the main project counterparty responsible for purchasing the power

output produced by PPP companies, at a pre-agreed price. The offtake risks are those risks of

not getting paid for output.

15The mechanics of demand de-risking can be gleaned from Nigeria. At the World

Bank’s Maximizing finance for the development of infrastructure in Nigeria workshop

in September 2019, the Minister of Finance noted that ‘Nigeria no doubt lacks the

fiscal space to self-finance’ the estimated USD 100 billion a year infrastructure gap.

Instead, she promised to continue its collaboration with the World Bank to leverage

private investment, building on previous success stories in ‘transport, energy and

power sectors using PPP models’ 11 . Among those, the World Bank representative

identified the Azura power plant ‘as an example of how we have attracted private

sector investment in the power sector’, the first privately-financed power project in

Nigeria. While Azura was set up as the de-risking PPP template for ‘lighting up

Africa’12, it is hardly a success story. Similar to other private operators, Azura sells

power to state-owned Nigeria Bulk Electricity Trading (NBET), who would pass it to

distributors to recover costs and pay Azura. Once Azura started operating in 2018,

demand risks materialized as its installed capacity could not be absorbed by the

dilapidated Nigerian grid energy infrastructure. The PPP contract shifted demand

risks to either NBET or failing, that, to the World Bank, whose partial risk guarantee

promised to pay Azura if the Nigerian state failed to do so. Thus, MDB guarantees

trap the de-risking state into a lose-lose situation, since a triggered risk guarantee

becomes a WB loan to Nigeria (the de-risking state always pays!). Under pressure

from the World Bank, the Nigerian federal government mandated its central bank to

pay Azura from an existing USD 2.3 billion fund destined to cover NBET payment

shortfalls. In doing so, the Nigerian central bank reallocated funds destined to other

private providers, who responded with a legal case against the Nigerian government

and Azura13.

11

See https://nairametrics.com/2019/09/24/nigeria-needs-100-billion-annually-to-fix-

infrastructural-deficit-finance-minister/

12 https://www.institutionalinvestor.com/article/b14z9q8pv7zzdb/is-new-nigerian-power-

plant-a-template-for-lighting-up-africa

13 https://uk.reuters.com/article/uk-nigeria-power-exclusive/exclusive-nigerian-energy-

sectors-crippling-debts-delay-next-power-plant-idUKKCN1OK1J4. While the ensuing

scandal prompted the government to suspend other PPP initiatives, the September event

suggests continued political commitment to the Wall Street Consensus.

16While the Nigerian case is indicative of how the WSC works in practice, the range of

demand risks that the state is expected to assume varies across countries. The Sri

Lankan InfraSAP (WB and IFC, 2019) recommends a government-sponsored

currency hedging facility that protects foreign investors from currency volatility. It

also advises the state to pass the costs of de-risking to end-users via periodic

adjustments of tariffs, and in case of severe disruptive events, to absorb those costs (p.

63). The InfraSAPs for Egypt (World, Bank 2018a), Vietnam (World Bank, 2018b)

and Nepal (2019b) similarly call for the state to facilitate the development of hedging

facilities. Furthermore, the Egyptian InfraSAP targets the relics of the traditional

developmental state. Its National Investment Bank, it argues, should stop direct

lending for public projects and instead embrace a more catalytic role for commercial

financing of infrastructure, following the KfW business model (World Bank, 2018a).

Equally important, the climate crisis gives rise to a series of political and demand

risks that institutional investors need de-risking for.

Sustainability reform: the turn to ESG ratings

The 2011 DB/UNDP report on renewable energy was written at a time when green

bonds were still a niche area for impact investors. By 2020, green finance moved into

mainstream investment practice through the framework of Environmental, Social and

Governance (ESG), a private sector approach that, it is increasingly argued, could be

guided by the SDGs14.

The ESG ratings system started as a corporation-focused, equity-tailored, sustainable

impact investor system of aggregating into a rating a set of environmental, social and

governance practices, as identified by the ESG provider. Once central banks in the

Network for Greening the Financial System identified climate risks as material risks

for financial stability, global finance embraced ESG as a private taxonomy for green

finance.

14 https://www.pimco.co.uk/en-gb/insights/viewpoints/esg-investing-and-fixed-income-the-

next-new-normal/

17Initially, ESG data were used to encourage corporations to engage more

systematically in ESG disclosure. More recently, private providers have issued ESG

ratings for countries. This is another step towards the extension of ESG ratings to

securities (bonds, securitization tranches etc.), as institutional investors recognize that

ESG is no longer simply about impact investment but about credit risks to portfolios

with carbon equities and securities (Inderst and Stuart, 2018). Thus, the ESG

framework is morphing into a private taxonomy for green/dirty15 finance: high ESG

ratings are interpreted to signal a ‘green’ financial instrument, and vice-versa.

For institutional investors, ESG ratings are a strategic necessity in the Wall Street

Consensus.

First, in mapping ESG ratings against the SDGs, institutional investors strive to

become credible development partners to the de-risking state and MDBs, and more

importantly, epistemic guardians of green taxonomies. Such new partnerships around

ESG are emerging rapidly. The Asian Infrastructure Investment Bank’s Asia ESG

Enhanced Credit Managed Portfolio includes an ESG Markets Initiative in

partnership with asset managers, to demonstrate ‘an AIIB ESG Framework that is

consistent with the spirit and vision of the AIIB’s Environmental and Social

Framework’ 16 (AIIB, 2019: 3). The AIIB ESG framework would allow the asset

manager to design, monitor and enforce ESG criteria, delegating rule making and

enforcement to private finance. The World Bank’s updated Environmental and Social

Framework17 similarly embraces the ESG status-quo. Long seen as ‘gold standard in

development finance’18, the mandatory safeguards have recently been replaced with a

‘risk-based, outcome focused, tailored and proportionate approach’. The World Bank

accepts the use of borrowers’ E&S frameworks that are ‘materially’ close to the WB’s

15 the standard climate finance language distinguishes between green and ‘brown’ assets,

disregarding the racist connotations embedded in conceptualizing dirty finance as ‘brown’

(see https://www.commondreams.org/views/2020/06/26/language-brown-finance-climate-

finance-racist). In this paper, dirty finance replaces the standard ‘brown’ term.

16

https://www.aiib.org/en/projects/approved/2018/_download/regional/ESG-enhanced-credit-

managed-portfolio.pdf

17 Other MDBs use a similar framework, with varying degrees of credible commitment to the

E&S principles (see for example https://thediplomat.com/2017/08/is-the-aiib-really-lean-

clean-and-green/ for AIIB)

18 http://archive.bankinformationcenter.org/world-banks-updated-safeguards-a-missed-

opportunity-to-raise-the-bar-for-development-policy/

18own, without clearly defining either ‘materially close’ in terms of thresholds or

mechanisms for monitoring changes in borrowers’ frameworks19.

Second, the turn to ESG raises the distinct possibility of SDG/green washing. ESG

providers use bespoke screening to eliminate issuers whose business lines are

inconsistent with certain investment policies or social norms. For instance, the

financial service firm MSCI provides bespoke screening for 'Catholic values' like

anti-abortion legislation 20 . This would allow institutional investors to claim SDG

outcomes when their investment decisions actively undermine women's rights

agendas.

Beyond SDG washing, the private ESG status-quo is functional to the Wall Street

Consensus. A private ESG metric for SDG asset classes allows investors to shop

around for high ESG ratings for their ‘sustainable’ portfolios, and for asset managers

to boost their climate warrior credentials. In one instructive example, Blackrock

pioneered ESG ETFs (passive investment vehicles), while wielding its shareholder

21

power to block climate measures against high-carbon companies. Even as

institutional investors divest from coal assets, large asset managers insulate

companies from sustainability pressures through index investment, potentially

becoming holders of last resort of high-carbon, potentially stranded, assets (Jancke

2019).

Such climate hypocrisy is accommodated by private providers – such as MSCI, FTSE

or Sustainalytics - who quantify the ESG performance on a large number of criteria,

chosen and assessed on discretionary basis. Hence, ratings often conflict: Tesla’s

global auto ESG ratings vary from very good (MSCI) to very bad (FTSE) and mid-

range (Sustainalytics)22. ESG providers face similar disincentives to those of credit

rating agencies before 2008. These responded to ratings shopping by awarding high

19

https://consultations.worldbank.org/Data/hub/files/oxfam_comments_on_second_draft_wb_

environmental_and_social_framework.pdf

20

http://documents.worldbank.org/curated/en/913961524150628959/pdf/125442-REPL-

PUBLIC-Incorporating-ESG-Factors-into-Fixed-Income-Investment-Final-April26-

LowRes.pdf

21

https://bit.ly/2zzTZ5f

22 https://ftalphaville.ft.com/2018/12/06/1544076001000/Lies--damned-lies-and-ESG-rating-

methodologies/

19ratings to issuers of complex financial products without due diligence into the credit

quality of the underlying loans. In turn, weak ESG standards perpetuate the failure of

financial markets to price climate risks adequately23.

The WSC creates mechanisms to protect investors from climate-related losses. In

promising to assume demand risks via PPP contracts, the state would absorb the

physical risks of extreme climate events or global pandemics that would strand

infrastructure assets. SDG-led development thus becomes a strategy of green

financialisation through which private finance manages the environmental crisis, a

step further in the financialization of nature that once focused on risk instruments

such as catastrophe bonds (Keucheyan, 2018).

The WSC also protects investors against political risks arising from the potential

emergence of green developmental states. The green developmental state would

prioritise the reorientation of finance towards low carbon activities. This requires a

public taxonomy of ‘green’ and ‘dirty’ assets that overcomes the shortcomings of

private ESG ratings, and policies to penalize dirty assets (through capital

requirements or haircuts) 24 . Yet in the Wall Street Consensus framework, such

policies would classify as political risks to SDG assets.

In its strategy to mutate climate risks into political and demand risks, private finance

may have found an important ally. Central banks in the Network on Greening the

Financial System conceptualize the immediate impact of tighter climate rules as

transition risks25. Realigning portfolios through ESG ratings, it is often argued, would

improve their resilience to physical risks that climate events would strand high-

carbon/dirty assets (Christophers, 2019), and to transition risks, those financial

stability risks arising from climate regulation that accelerate the transition to low-

carbon economies. These are risks that the transition to a low-carbon economy would

23 Blackrock calculated that several US asset classes that do not price in extreme climate

events would experience significant losses over a long horizon. See

https://www.ft.com/content/2350de58-7236-3593-ad79-16bfa6ecea8d

24 Such initiatives already exist. The European Commission announced a public taxonomy in

June 2019 that it expects to become the benchmark for European finance.

https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance_en

25 See https://www.bankofengland.co.uk/knowledgebank/climate-change-what-are-the-risks-

to-financial-stability

20increase the cost of funding or dramatically change asset values, affecting

profitability. The faster the low-carbon transition, the higher the potential that

transition risks affect financial stability, thus binding central banks in political trade-

offs that privilege incremental green regulatory regimes, however urgent the climate

crisis.

In seeking to enlist central banks in the political coalitions against biting climate

regulation, the Wall Street Consensus would tie the hands of green developmental

states directly, by making it liable for transition risks that can be framed as political

and demand risks, and indirectly, by reducing the public resources and central bank

support for Green New Deal programs that can effectively manage transition risks.

The de-risking state and the green developmental state can hardly co-exist,

particularly within market-based financial structures.

Structural reforms: the turn to sustainable bond finance (formerly known as

shadow banking)

The turn to private finance as vehicle for sustainable development requires a change

in financial structures. Bank-dominated financial systems would transform into

market-based financial systems. This project of transforming shadow banking into

resilient market based finance accommodates the entry of global and domestic

institutional investors into local (SDG) securities and allows them to finance and

hedge their securities positions via repos and derivative markets. In this push for

structural transformation, the Wall Street Consensus assigns a de-risking role to the

central bank as market-maker of last resort that reduces liquidity and currency risks

for global investors.

The MFD agenda converges with several other global initiatives to restructure

financial systems towards market-based finance (see Figure 3). The Local Currency

Bond Market Initiative seeks to Americanise the local currency securities markets of

DEE countries by creating the ‘plumbing’ – derivatives and repo markets – necessary

for their increased liquidity (Gabor, 2018). It was originally introduced under the

leadership of the German Central Bank, the Bundesbank, in cooperation with the

21World Bank and the IMF, at the G8 meeting in Germany in 2007, as part of a broader

push for selling development finance to the market. The 2011 G20 Action Plan noted

that well-developed local securities markets would reduce dependency on external

financing and improve DEE countries’ ability to withstand volatile capital inflows.

While acknowledging capital flow volatility, the Action Plan called for carefully

phasing out capital controls, eliminating first those capital controls that hamstrung

local securities markets (such as withholding taxes on foreign investors’ bond

earnings). Domestic institutional investors were also to be encouraged, by privatizing

pension funds and ‘enabling mutual funds and insurance companies’. Similarly, the

Financial Stability Board announced in 2015 its new priority, to transform shadow

banking into resilient market-based finance, understood as the development of

securities, derivatives and repo markets that would allow the real economy to tap

credit from institutional investors.

Figure 3 The turn to securities markets/market-based finance in international development

Source: own representation.

In another illustration of the implicit WSC promotion of shadow banking, the push for

market-based finance brings back securitization as an important de-risking instrument

to crowd in private (institutional) investors and scale up sustainable assets.

Securitization features prominently in the OECD’s low-carbon infrastructure push,

22the MDBs plans to optimize balance sheets, or the G20 plans26 for Infrastructure as

an Asset Class.

Securitization – shadow banking instrument par excellence - is promoted as a de-

risking instrument that transforms non-tradable loans, extended by MDBs or private

banks, into a range of tradable securities with distinctive risk/return profiles that can

be sold to institutional investors (Gabor, 2019). The securitisation of infrastructure

loans would create both highly-rated, low-return tranches suitable for conservative

pension funds/asset managers and lower-rated, higher return tranches suitable for

investors with higher risk appetite. It would also accelerate lending to infrastructure

projects, constrained by Basel III rules for banks. As the Vietnam InfraSAP suggests,

bank energy loans could be securitized to make room for additional lending. Banks

could also sell infrastructure loans to platforms such as the AIIB’s Infrastructure

Private Capital Mobilization Platform, which in turn would package and securitize

them for distribution through capital markets to ‘build infrastructure as an asset class’

(AIIB, 2019:1).

The promotion of securitization and domestic capital markets that are deep and liquid

downplays the systemic risks characteristic to market-based finance. While reducing

dependency on foreign currency debt (Berensmann et al, 2015), the shift to market-

based finance comes with systemic, shadow banking type instabilities that turned

Lehman into a global systemic event.

The WSC template for liquid securities markets calls for importing the fragile

liquidity structures of US financial markets (Brunnermeier and Pedersen, 2009). It

asks countries to redesign repo (securities financing) markets and derivative markets

according to the US template so that foreign (institutional) investors can easily

finance and short securities. This ‘Americanization’ of local financial systems

involves liberalising repo markets to enable legal transfer of title to collateral

securities, to allow mark to market and shorting, and the development of onshore

derivative markets. Yet it was precisely this type of collateral-based financing

26 See the Eminent Persons Group proposals to the G20

https://g20.org/sites/default/files/media/epg_chairs_update_for_the_g20_fmcbgs_meeting_in

_buenos_aires_march_2018.pdf

23markets that fed, through shadow banking, cycles of liquidity and leverage before

Lehman. When the crisis came, it manifested in fire sales of securities, evaporating

market liquidity and wholesale funding runs. The FSB’s repo collateral rules and

Basel III do not go far enough to contain such dynamics (Gabor, 2018), and may be

rolled back in response to the global COVID pandemic.

The structural transformation of financial systems does not protect institutional

investors against liquidity risks in the bond markets that are used as collateral for

financing. This is why the central bank becomes an important anchor of the de-risking

state through bond market-maker of last resort (MMLR) that institutionalizes a

commitment to preserve collateral liquidity through outright purchases when market-

based finance comes under pressure (Mehrling, 2012). Such interventions, introduced

through (often clandestine) extensions of formal mandates after Lehman’s collapse,

derisk bond markets by creating an asymmetric regime where the central bank puts

floors but not ceilings on securities prices (Gabor, 2016).

Before the COVID19 pandemic, bond derisking only occurred in high-income

countries. In some polities like the Eurozone, it gave rise to significant contestation

because most interventions to stabilise the plumbing of market-based finance requires

outright purchases of government bonds, for conservative voices a revival of the

monetary financing of governments. Similarly, the notion of market maker of last

resort was taboo in emerging and poor countries, denounced as a pathological capture

of the central bank by populist governments. Instead, the WSC celebrated the growing

presence of non-resident investors in local currency bond markets as a victory of its

mantra ‘development aid is dead, long-live private finance!’. Portfolio inflows would

improve the liquidity of government bond markets, and with it, DEEs dependence on

external debt. The vulnerabilities associated with the global dollar financial cycle

were set aside (see Gevorkyan and Kvangraven, 2016), as if borrowing from foreign

investors automatically generates policy autonomy. But elsewhere, the IMF

recognized that local securities and equity markets, capital flows and credit cycles

increasingly move together, all in the shadow of the US dollar (Adrian, 2019).

Increasingly popular Exchange Traded Funds (ETFs) - that package equities or bonds

and issue ETF shares against them - sharpen this dependency: while emerging market

ETFs are traded on the exchanges of high-income countries, their issuance and

24redemption requires the purchase/sale of the underlying shares/bonds, thus generating

capital flows. As Converse et al (2020) document, ETFs amplify the global financial

cycle for DEEs. Thus, direct and indirect (via ETFs) inflows into local currency bond

markets move with dollar financing conditions, while exchange rate volatility

amplifiesof portfolio flow pro-cyclicality: currency depreciation accelerates capital

flight (Hördahl and Shim, 2020).

Indeed, currency risk has long been identified as a significant obstacle to attracting

foreign institutional investors in large-scale infrastructure assets (see Baker, 2015 for

renewable energy in South Africa). In response, the WSC outlines three currency

derisking strategies (see Hördahl and Shim, 2020). As the World Bank’s InfraSAPs

recommend, state development banks could provide hedging facilities through which

institutional investors transfer currency risk to the state. Second, central banks can

undertake regular derivative operations to derisk exchange rates for foreign holders of

local currency bonds (Macalos, 2017). Finally, central banks can become swappers of

last resort, supplying financial institutions with foreign liquidity during periods of

instability, thus reducing exchange rate volatility (Gonzales et al, 2019). Note that

these strategies are designed to minimize recourse on capital controls, further

entrenching Rey’s (2015) dilemma: free portfolio flows into local (SDG) securities

markets comes with loss of monetary policy independence and of influence over local

credit conditions.

The critical de-risking role assigned to central banks in part reflects that the journey to

infrastructure as a bond asset class is long and fraught with institutional complexity.

As Klagge and Nweke-Eze (2020) document, complex risk structures deter

institutional investors from participating in Keyna’s renewable energy projects,

leaving MDBs, governments and renewable industry investors to finance and derisk.

In other words, the derisking of PPP infrastructure and its financing via securities sold

to institutional investors may proceed at different pace, constrained by the pace of

structural transformation of local financial systems.

25Surveillance capitalism in the WSC

Finally, WSC aims to leverage the model of surveillance capitalism (Zubhoff, 2019)

already deployed via the trope of digital financial inclusion in overlapping networks

of state institutions, international development organisations and ‘philanthropic

investment’ fintech companies (Gabor and Brooks, 2017). The aim was to map,

harvest and monetize digital footprints via behavioural analytics to render the poor

‘investible’ through an ‘all data is credit data’ approach.

Surveillance capitalism increasingly overlaps with the Wall Street Consensus, as

illustrated by the turn to private/PPP healthcare in African countries. In the wake of

the Washington Consensus, African countries privatized health through different

methods, from user fees on public health services to encouraging private healthcare

and promoting insurance schemes (Baloyi, 2019). Across SubSaharan Africa, 50% of

healthcare is provided by the private sector, with financing provided by investment

platforms and fund managers promoting the development of healthcare asset classes

(Hunter and Murray, 2019). Enter digital healthcare, with its promise of better

diagnostics through advanced technologies, and a complex ecosystem ripe for ‘health

as an asset class’ initiatives.

PharmAccess Group, for instance, operates both on the supply side and the demand

side of private healthcare. It provides financing to small-scale private health

companies in Tanzania, Kenya, Ghana and Nigeria, from healthcare SMEs to

specialist care providers and other businesses catering to health facilities, through the

Medical Credit Fund. PharmAccess’ partners include AfDB, the World Bank and

most official development aid agencies, alongside foundation involved in the financial

inclusion project. On the demand side, it has received ODA funding for the

Safaricom-backed healthcare app M-Tiba, where users save for medical care, pay and

manage their insurance policies and support their dependants.

Digital healthcare can morph into surveillance devices whereby insurance companies

can adjust premiums via data delivered to doctors. For instance, MTiba launched a

new hypertension and care app for low-income patients in 2018, that allows them to

monitor blood pressure and blood glucose levels, digitally sending the results to

26You can also read