TONY'S VIEW - Tony Alexander

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

TONY’S VIEW

Input to your Strategy for Adapting to Challenges

Feel free to pass on to friends and clients wanting independent economic commentary

ISSN: 2703-2825 Thursday 14 May 2020

To subscribe click this link https://forms.gle/qW9avCbaSiKcTnBQA

Speaking enquiries tony@tonyalexander.nz

Back issues at www.tonyalexander.nz

My Aim

To help Kiwis make better decisions for their businesses, investments, home purchases, and people by

writing about the economy in an easy to understand manner.

“Gizza Job. I can do that.” Just as an aside, this website from MBIE needs an

update, but it contains something I’d not seen before.

It describes how you can download an app called

We Kiwis are shy. The Americans find us not “Occupation Outlook” which will help you with a

emotive enough. Asians consider us too trusting. choice of potential new career, the relative expense

Australians think we are not assertive enough – all of training, and likely end-demand. The end-demand

these comments based on research undertaken a piece clearly needs updating. But if you are

few years ago by NZTE and which I used to discuss undertaking a course of study lasting maybe a

in my Brain Gain publication. couple of years the current state of the labour market

is not all that important.

What does that mean in the context of the Covid-19 https://occupationoutlook.mbie.govt.nz/

crisis? It means that if you’ve just been laid off or

you’re going to be, you’ll look for work on sites like

Seek and Trademe, and ask around a bit. But you’re Uniqueness

almost certain not to stand on the corner with a sign

saying you’re out of work and you’ll do anything. I was asked during a webinar this week to describe

how this recession is unique compared with others

You’re almost certain not to work your LinkedIn in recent decades. The unique aspect is that this is

contacts saying you’re up for a go at something new. a temporary voluntary crushing of the economy

undertaken in order to save the lives and long-term

You’ll basically keep your head down and try to do health and happiness of tens of thousands of people.

your best. Blow that. The world belongs to those who

put themselves out there, take a risk of having others This recession does not result from a collapse in our

laugh at or look down at them, and plough on export prices for which we tend to see a 12-month

regardless. Meaning what? lag before it hits the cities, then extended urban

weakness while the farming sector eventually starts

If you’re laid off or about to be and want to advertise coming back up again assisted by a belated

your skills and what you have to offer, email me. I weakening of the NZD and falls in interest rates.

don’t want a CV, I don’t want your life story, I don’t

want details of your experience. You’ve got 100 This recession does not result from a global financial

words to sell yourself to the now 10,000 people who system shock in response to excessively bad lending

directly receive Tony’s View each week and the and excess construction of houses in many

many more who receive it second hand or access it countries, as was the case with the GFC. The unique

from one of the many links people place on their aspect of that downturn was the seizing up for some

websites or in their social media posts. 6 weeks of the global credit system and deep worries

that many banks might collapse around the world.

I will publish your blurb as an add-on to my weekly Worries about a repeat of the Great Depression

for the following week. caused weakness in share prices and sustained

declines in house prices, household wealth

You choose what to write, but make sure to include destroyed and willingness to spend along with it, and

your location and whatever form of contact you want sustained lending restraint by banks rebuilding their

to share so people can get in touch with you directly balance sheets.

if they want, rather than going through me. What

have you got to lose? Your job? Too late. This recession is not because of entrenched high

inflation necessitating sustained high interest rates

(Ref. = Yosser Hughes, Boys from the Blackstuff.) to crush inflation and inflation expectations – as

happened in New Zealand in the late-1980s. Such

Tony’s View

inflation fights are often of long duration and much

hope of better times is lost by consumers and Then there is the other structural factor driving higher

businesses, and this can weaken willingness to unemployment. We have entered my predicted

spend and willingness to hire and invest. period of “weeding out’ of businesses across all

sectors, challenged by new technologies, social

Which brings us back to this downturn. It does not pressures, finance shortages etc. The restructuring I

come about through an income shock or a financial figured would take 2-3 years will probably all happen

shock or a need to fight high inflation. Only for a short before the end of this year.

time will it affect the willingness of you and I to spend,

and of businesses to hire and undertake capital Finally, there is the new structural element of

expenditure. That perhaps is the big difference, more decreased capital costs associated with sustained

so than the short-term depth of this downturn and the low interest rates. In recent years businesses have

unique shocks to inbound tourism and hospitality. facilitated their growth by hiring people. Now, with

the hurdle rate for undertaking capital spending so

Because the worst of this downturn is hitting now and low, some will embrace greater labour-saving

in the next few months, and job losses are radically production techniques.

front-loaded, the recovery will appear much sooner

than in previous downturns. The willingness of A quick reduction in our unemployment rate will

people to spend and businesses to hire is going to happen later this year. But it will still leave a new pool

return earlier than in previous recessions, with of potentially long-term unemployed people. How

assistance from the biggest set of fiscal and depressed should we be about this? Maybe not as

monetary stimuli that we have ever seen. much as in earlier years when work structures and

roles were more rigidly defined.

In the words of former Federal Reserve Board

Chairman and student of the Great Depression Ben As mentioned here before, young people may not

Bernanke, “The expected duration is much less, and have much resilience (though they are getting some

the causes are very different.” The US economy now), but they are highly adaptable. They know

shrank for 43 months in a row from 1929-33. This nothing other than the new. New technologies, new

time shrinkage will be limited to just a few months. ways of shopping, new ways of working. They will

The IMF predicts that the world economy will shrink willingly embrace new roles, set up new businesses

about 3% this year versus 10% shrinkage during the from home with minimal overheads, and perhaps

1930s downturn, with growth resuming around the ultimately disrupt existing operators in a way we

world over 2021. have not seen before.

Ultimately then the unique aspect of this recession So that then becomes a warning to existing

may not be its magnitude or even the speed with companies getting through this okay. You are about

which it has struck. Instead it may be the focus right to be challenged with the greatest wave of people

from the start on recovery – which sectors first, which having a go perhaps in your sector, that you have

last. ever seen. If you want to keep up with the ways they

will undermine your business model, it would

My gut feel is that we will individually reach for the probably be a good idea to hire them or buy out their

light at the end of the tunnel far earlier than in past start-ups as quickly as possible. There is ultimately

recessions. That ultimately will drive consumption, one thing we know which always emerges from

new hiring and investment, and that will produce crises. A sharp acceleration in innovation. Next year

growth through 2021 and quite possibly from the through 2022 will be fascinating.

early part of the December quarter.

And just to finish off with the issue of how unique this

However, this is not to say that underlying downturn is. In every previous recession I have lived

unemployment will disappear quickly. That is through people have talked about New Zealand

something different. The inbound tourism sector has being stuffed and that we should leave and the last

gone and unless businesses believe Kiwis will one out turn off the light. For this recession we are

undertake a huge surge in domestic travel, there is happy to be here, intend staying, expect many Kiwis

no point keeping staff on. The hospitality sector is offshore to eventually return, and anticipate a wave

also experiencing a structural reduction in customer of foreigners wanting to get in.

flows with many people likely to avoid crowded

locations for potentially years rather than just the

next few weeks. That factor, added to the generally

high turnover rate of hospitality businesses, will see

many closures and many people displaced from the

sector.

Page | 2

Tony’s View

US 14.7% Unemployment Not Confidence Measures

What It Seems You might have noticed that in contrast to my normal

practice over the years I’ve not been reporting on all

On Friday night we learnt that the United States relevant economic indicators, including the business

unemployment rate jumped in April to the highest and consumer confidence gauges. That is because

level since the 1930s at 14.7% from a low of 3.5% in in the short-term they cannot yield useful information

February. This resulted from 20.5 million people for my purposes which is gauging likely changes in

losing their jobs in April. spending, hiring, and capital spending and

conveying those thoughts to yourselves.

The news is bad and it is expected that in May the

unemployment rate will exceed 20%. However, there We all know the economy is extremely weak at the

is something important to note regarding labour moment. But my commentary will not be altered by

market dynamics in the US. In New Zealand during a measure falling 60% rather than 40%. These

times of demand weakness companies tend to changes do not reflect true underlying trends in what

reduce work hours of employees. In the US they we are doing with our money but the effects of a

place them on furlough. That means that they are temporary health scare and actions taken on a

unemployed but there is an expectation that temporary basis to fight it.

conditions will allow them to be rehired down the

track. This also means that very shortly, as we receive high

frequency data showing big bounces upward in

And that is the key characteristic of this jump in many measures, I will ignore them as well. But it gets

unemployment in the US and around the world. worse. At the same time as we soon will receive

Soaring job losses have not come about because these positive measures reflecting the transitions to

companies believe customer demand has Levels 3 then 2, we will also receive the more usual

permanently declined and they have to become data released with a lag showing the extreme

smaller businesses (though there are elements of weakness of lockdown. Plus, we will have data

this in aviation, tourism, and hospitality). releases showing what happened in the March

quarter just before lockdown started on March 26 –

Job losses do not reflect unaffordability of such as last week’s employment numbers.

employees because of legislated high pay rates, a

sudden escalation in debt servicing costs, loss of Focus on the underlying trends, not the contradictory

markets to competitors in other countries, the economic data and its massive volatility for the

development of completely new products stripping remainder of this year.

away demand for existing outputs, or a collapse in

bank financing requiring drastic action to try and

reduce debt.

Buying NZ-Made

The job losses arise because governments forced

businesses to close in order to stop the spread of I have mentioned that it would be in our best

Covid-19. When that spread is contained interests to support NZ producers of goods and

employment growth will soar as furloughed people services as much as possible when we re-engage

get re-employed and new businesses start up to take with the retail sector. Business NZ own the New

the place of those without sufficient capital to make Zealand Made trademark registration process (I

it through the period of shutdown. believe), and if you want to get their much-

recognised sticker of a Kiwi within a curved triangle

The economic impact of shutdowns will be severe you can commence the process to do so here.

and will negatively affect levels of economic activity https://buynz.org.nz/

for a long time. But the sustained impact will be

nowhere near the short-term outcome of soaring This website will show you goods produced by those

unemployment and closed businesses. who have registered for the New Zealand Made

trademark and have goods to sell online.

So be careful not to get overly depressed by http://www.buynzmarket.org.nz/

comparing these sorts of numbers with those from

the 1930s. This is a short, sharp shock with a long

tail rather than the extended collapse back then.

Page | 3

Tony’s View

Will taxes need to rise? Not necessarily. In 1972 the ratio of government net

debt to GDP was 6%. It soared to 55% in 1992. It

then fell to 6% in 2008, rose to 26% in 2013, and a

You’ll all have seen the Budget details by now, the few months back was below 20%. Under Budget

media and your in-boxes will be awash with projections the ratio will exceed 50% very shortly.

descriptions of what was in it and dissection of the Will taxes need to go up in order to get the ratio back

financial details. As per my tradition the past couple down to a low level in readiness for the next crisis

of decades I will limit Budget reporting to a summary such as an earthquake in a major NZ city or new

of the high-level details and some comment on likely health scare?

impact.

Not necessarily. Over the 16-year period from 1992

As regards the Budget highlights we have the to 2008 when the ratio fell from 55% to 6% the rate

following. of GST was unchanged at 12.5%. The top marginal

income tax rate was raised by Labour

• A $50bn fund has been created to fight (unnecessarily) in 2000 from 33% to 39%. But core

economic effects of Covid-19. $14bn has Crown revenue as a proportion of GDP fell from near

already been spent, the Budget allocates 36% in 1992 to 33% in 2008.

$16bn, leaving $20bn to be spent on other https://www.wgtn.ac.nz/sacl/centres-and-

unannounced initiatives as the government chairs/cpf/publications/pdfs/2016/WP_04_2016_Th

sees fit. e_Changing_Role_of_the_State.pdf

• The $16bn new spending announced today

includes $3.2 for the wage subsidy extension, The government did not have to boost its tax receipts

$3bn on infrastructure, $1.6bn for fees-free in order to get the net debt ratio down. Instead they

trades training, more students, and retention of exercised restraint in spending over a long period of

current apprentices, $1.1bn for “green” jobs in time. That is what needs to happen this time around,

the regions, $5bn for an extra 8,000 state although on current projections Labour may not be

houses, $0.6bn rent subsidies, $0.4bn tourism the government capable of doing it.

recovery fund, and miscellaneous other things

like school lunches.

•

Recent Publications

There are no changes in tax rates or tax reform

of any kind, and no changes in welfare

payments.

• Budget deficits are predicted for 7 years What real estate agents are seeing.

http://tonyalexander.nz/resources/Tony's%20View%20Real%20

through to 2028 with this year’s deficit to be Estate%20Survey%20May%202020.pdf

almost 10% of GDP at $28bn, then $30bn over

2020/21 and $27bn over 2021/22. Kiwi consumer plans for spending.

• The net debt to GDP ratio will rise from 20% to http://tonyalexander.nz/resources/TV%20Spending%20Plans%2

peak at 54% in 2023/24 then ease to 42% come 0Survey%20May%202020.pdf

2034.

• However, because some announcements Things which might be better as a result of this crisis.

differed from what Treasury was led to believe http://tonyalexander.nz/resources/TV%20Covid-

19%20No.8%20Supplement.pdf

at the cut-off date for making their forecasts, the

numbers if they generated them now would be

Things which will slightly limit housing weakness.

slightly worse. https://www.stuff.co.nz/life-style/homed/121227636/heres-why-

• The spending by the government will provide a house-prices-may-not-fall-as-far-as-you-expect

6.5% boost to the economy this year, offsetting

direct weakness related to Covid-19 and Recession elders passing on their knowledge to

producing growth in the year to June 2020 newbies of what to do when these bad times arrive.

expected at -4.6% then -1.0% to June 2021 http://tonyalexander.nz/resources/TV%20Covid-

19%20No.7%20Supplement.pdf

before +8.6% to June 2022 and +4.6% to June

2023. There are both upside and downside

risks to these growth forecasts.

• The unemployment rate is seen peaking just

below 10% in the September quarter, then

falling to 7.6% in June 2021, 5.7% in June 2022,

and 5.2% in June 2023.

Will taxes need to go up in order to get debt levels

down again?

Page | 4

Tony’s View

Emailed Queries demand. Investors are facing extremely low returns

on simple assets like bonds and term deposits and

will be searching for higher yields from assets

Is this a credit crunch which will cause banks to expected to produce reasonably reliable income.

restrain lending all through 2021?

Additionally, the experience of other countries post-

NZ banks pre-GFC got 45% of their funding from GFC was that the printing of money resulted in

offshore, but that is now below 20%. This is not a upward pressure on asset prices including housing,

banking crisis and current strong offshore demand shares, and commercial property. In the United

for NZ government bonds, and maintenance of credit States commercial property prices fell on average

ratings with positive outlooks by the rating agencies, near 30% during the GFC then doubled in the ten

in conjunction with the lauding of our virus progress years following

overseas, means investors will willingly continue to

supply NZ banks with the funding they need. If they What impact will there be from the predicted fall in

don't then the RBNZ have already made clear that the dairy payout to below $6.00 a KG of milk solids?

they will provide whatever funding is desired by and The dairy industry accounts for near 3.5% of New

large in the short-term. Zealand’s GDP. A reduction in the payout from a

projected $7.00 - $7.60 plus dividends this season to

When NZ banks can see recovery appearing and the as low as $5.75 would see some a reduction in on-

end of the layoffs period, they will become more farm dairy income of about $2.5bn or some 0.8% of

willing to lend. Until then some extra constraints GDP. The payout would be the lowest since the

could easily appear. Property buyers will just need to 2015-16 year and would come about as a result of

stay engaged with the market, build up their deposit, not just weaker world growth/recession, but the

and be ready to move when the lending restraints special reduction in demand for dairy products from

are eased off again, perhaps coming into summer the deep cutbacks in eating out.

this year.

Payout projections can be highly volatile.

We are thinking of selling a retail property in Nevertheless, the coming reduction means it would

Hamilton soon. Is there likely to be much demand? be unreasonable to think in terms of our economy

being pulled out of recession by the farming sector.

For Hamilton over the medium to long-term I see It is more the case that farming exports have

excellent growth prospects on the basis of proximity assumed even greater importance in generating

to Auckland and vastly improving transport export revenue and the government needs to take

connections. Regarding the next 18 months or so, I that into account as it considers a range of legislative

expect the economy to be performing very well by changes which would retard growth in our long-

the end of 2021 with an assumption that a vaccine running economic and export base. Will the

exists for Covid-19. government look toward the farming sector as a

potential area for rapid short-term jobs growth? No.

In the near future banks are not going to be willing

providers of funding for anyone contemplating a How do I go about finding out what to invest in?

property purchase in the areas of hospitality, The options for what one can do with investable

retailing, tourism, or offices. Therefore, anyone funds are near endless. You need to speak with a

selling a commercial property will find the pool of financial advisor. They will try to get a gauge for how

funds able to be utilised by others to make a much risk you are willing to tolerate, what your level

purchase will be much smaller than in more normal of understanding is of various options, when you

times and it is likely that this will influence selling plan using the saved funds and so on. For your own

prices for non-residential properties. research I'd suggest either finding an online course

or a book on the subject. Certainly not anything on

In addition, given the uncertain outlook surrounding social media, and nothing from any of your mates or

not just the economy but the retailing sector in relatives. You know deep down many of them are

particular and how people will shop, the willingness morons, but you might have forgotten it under

of people to purchase or build retail premises is likely pressure these days not to express honest views

to be further reduced. about people.

If older people want to keep working then they

Therefore, until underlying factors like population should continue to do so.

growth assisted by net inward migration and

eventually shortages of commercial property caused

by weak construction become dominant, prices for

these assets are likely to be compromised. Note

however that this is not to say there will be no

Page | 5

Tony’s View

New Zealand’s Housing Markets

Early days as yet Waikato was also weak, but everywhere else

around the country more investors are being seen.

On Monday I sent out the results of this month’s Both investors and first home buyers hunt at the

monthly Tony’s View Real Estate Survey. You’ll lower-priced range in each market. This suggests

find the pdf here in case you missed it. it will be at the upper and maybe upper-middle

http://tonyalexander.nz/resources/Tony's%20View%20Real%20

Estate%20Survey%20May%202020.pdf sections that we will see greatest price weakness.

The 236 respondents reported an unusually high Responses from agents suggest that we can put

level of interest from investors and first home buyers roughly into at least four categories.

buyers and the latter result at least was backed up

by Trademe Properties. They reported a 38% rise 1. Early lookers hoping for some bargains and

throwing in very low offers.

compared with a year ago in the number of 18-29-

2. Buyers who intend selling in the same market

year olds recently browsing their site. The result

so are not worried much about what prices will

will be biased upward by people having time on do and just want to get on with their lives.

their hands and that probably explains also a 3. First home buyers sensing that they might

130% rise in all property viewings online for the finally be able to find a place they want and

Queenstown-Lakes area. Property porn one hoping banks might ease up on their lending

suspects. criteria now that LVRs have been abolished.

4. Buyers prepared to wait until the six-month

My survey found that a net 27% of agents mortgage deferrals start, at which time they

responding feel this is a buyer’s market. But a net expect more weak sellers will be out there.

10% in Wellington think this is still a seller’s

market, as did a net 7% in wider Nelson and in

Canterbury only a net 2% view things as in favour For your guide. In Australia, one small lender has

of buyers. Why might this be? suspended financing of off-the-plan purchases

because of uncertainty about where prices may go

Ahead of the GFC the number of properties listed and the extra risks attached to such ventures.

for sale on www.realestate.co.nz was 58,000 in

April 2008. The number listed in March this year RB House Price Assumption

was under 19,000. We went into this with a listings

shortage. In their Monetary Policy Statement released on

Wednesday the RB predicted that this calendar year

average house prices around New Zealand will fall

by 9%. Is this likely?

In December 2008, just after the world’s financial

markets seized up, in their Monetary Policy

Statement the RB predicted a 16% fall in NZ house

prices from the peak of 2007 through to the end of

2010 – with downside risks. In fact, prices only fell

over that period by 7.7% and they reached their

absolute low point in the very month the RB

predicted the 16% decline.

That is, they fell 11% from mid-2007 to December

2009 then rose 3.8% by December 2010. Ultimately,

The survey also showed that a net 16% of agents their forecast was out by about 9%.

are seeing more investors in the market (sniffing

opportunities) and a net 4% said they were seeing Our central bank has an unfortunate history of over-

more first home buyers (hoping for availability and estimating house price declines.

excited by LVRs disappearing). Investor interest

was weakest in Otago with a net 14% of

respondents there seeing fewer investors.

Page | 6

Tony’s View

Interest Rates

The chances are strong that following some small China has a history of using trade access as a

reductions in one- and two-year fixed mortgage weapon against countries which upset the CCP.

rates this week, further reductions will happen This is not a new practice but something which

soon. The Reserve Bank is clearly frustrated at has been around for centuries. The new elements

behaviour by banks, writing the following in their however of this approach are the communities of

discussion of the expansion of their money Chinese nationals in countries which act to further

printing operation China’s interests and suppress local pushback

against China’s goals. Plus, the role of China in

“We expect to see retail interest rates decline the world economy has become extremely

further as lower wholesale borrowing costs are important – though it has yet to regain its previous

passed through to retail customers. It remains in standing of accounting for near one-third of global

the best long-term interests of the banking sector GDP over two centuries ago. The current

to promptly maximise the effectiveness of our contribution is near 21% from less than 2% in

LSAP programme.” 1980.

It sounds like something an authoritarian state The reputation of China is falling around the world

might say to a wayward country. in response to the authoritarian state’s covering

up of initial information about the virus outbreak in

In response to the RB’s comments, the sharp Wuhan, and the damage appears greatest in the

jump in their quantitative easing plan size, and the United States and Australia. But Europe along

fact that they have not yet 100% ruled out a with the UK are starting to push back and many

negative cash rate, this week wholesale interest other countries are reacting, if not because of the

rates have fallen slightly. The three-year swap outbreak, because of the poor quality of medical

rate has decreased to 0.14% from 0.24% while the goods shipped by China to other countries once

five year rate has declined to 0.22% from 0.37%. the outbreak spread elsewhere.

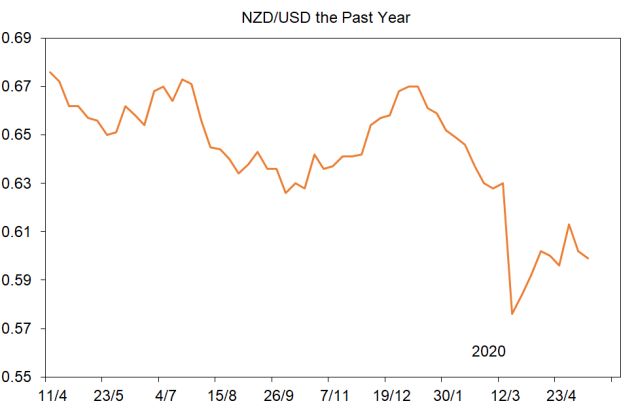

NZ Dollar It is difficult to know where this will go, and given

the trade dependence of NZ and Australia on

China it is hard to imagine full shirt-fronting of

The Kiwi dollar initially firmed this week in China. There is no economic upside to that

response to a couple of factors. approach. President Trump might do this anyway

with rising need for an issue to galvanise US

• Improved risk tolerance generally in financial voters ahead of November’s Presidential election

markets as investors focussed more on plans now that he cannot tell a story of great economic

for gradual reopening of economies rather success, and his administration’s management of

than economic data showing the depth of the the virus in the US has been and remains

current downturn. incompetent.

• Some improvement in minerals commodity

prices taking the AUD higher and ourselves We are likely to see enhanced volatility in financial

along for the ride. asset prices in coming months as concerns about

the deepening cold war between the United States

But then there was some mild selling pressure and China wax and wane. The challenge for the

associated with AUD weakness in response to the NZ and Australian governments will be

deepening chagrin of China with Australia’s call maintaining strong trade relationships with China

(supported by NZ) for an enquiry to figure out whilst adhering to the values key to our way of

where Covid-19 came from. China has banned living and culture.

imports of meat from four Australian abattoirs and

a hefty tariff on imported Australian barley is The NZD this afternoon was trading just below US

expected – though the process for doing that 60 cents from just above this level last week. No

started a long time ago in the context of concerns trend is apparent.

about dumping.

Page | 7

Tony’s View

The chances are we may lose some slight extra

ground against the AUD, but not all that much.

Since 2014 the Kiwi dollar has sat above 90 cents

practically the whole time, and respective

monetary policies are unlikely to diverge much

from current settings in the near future.

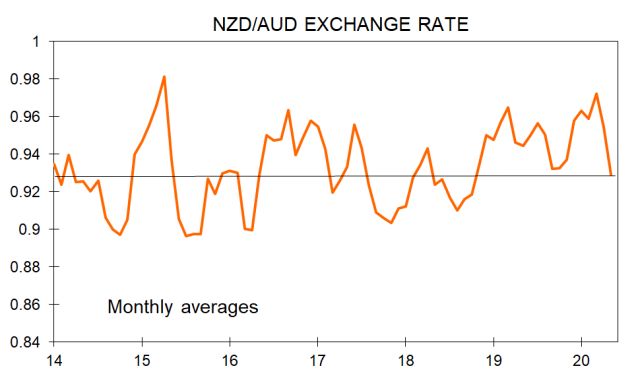

Against the Australian dollar we have ended near

92.9 cents from 93.8 cents last week. The trend

here has been down since the brief trades above

parity in mid-March.

The biggest risk may be if dairy prices start to

adjust to the demand and supply situation

offshore.

CHOOSING YOUR FIXED MORTGAGE RATE TERM

Finally – some rate cuts.

When fixing a mortgage rate term most people take whichever rate is the lowest. So, each week I shall

calculate what rates would have to be in the future to make this option better than some alternatives. Note,

there are far, far more alternatives than calculated here. And always remember, it is worth paying a premium

for rate certainty over a longer period of time. It’s also worth using a broker to get the best deal. Broker use

is far higher in Australia than New Zealand but we will probably catch up.

Current minimum fixed rates across the main banks. *

1 year 2.89% down from 3.05%

2 years 2.99% down from 3.35%

3 years 3.39% down from 3.65%

4 years 3.49% down from 3.79%

5 years 3.59% down from 3.89%

I can fix 1 year at 2.89%.

Is this better than fixing 2 years? Yes, if in 1 year the 1-year rate is below 3.09%.

Is this better than fixing 3 years? Yes, if in 1 year the 2-year rate is below 3.64%.

Is this better than fixing 4 years? Yes, if in 1 year the 3-year rate is below 3.69%

Is this better than fixing 5 years? Yes, if in 1 year the 4-year rate is below 3.77%.

Is it likely that in one year’s time the one-year fixed rate will be above 3.09%? No. So if two years was

as far out as I was looking, I would personally opt to fix one year currently. In a year’s time what are the

chances that the two-year rate is above 3.64%? Again, not strong. So, I again would fix one year then

look to fix two years one year from now if a three-year exposure was my preference. We Kiwis tend to

fix at whatever the lowest rate is, and the balance of probabilities suggests doing just that currently will

Page | 8

Tony’s View

yield the lowest debt cost for the next few years. However, I personally am a conservative borrower. If

someone were to offer me a three-year fixed rate at 3.3%, I’d probably take it. Westpac offer a nice

3.39% three-year fixed rate and that will suit people just slightly more conservative in their det

management than myself.

*Minimum 20% deposit, owner occupiers, 6 largest lenders.

Compounding is minor so is ignored.

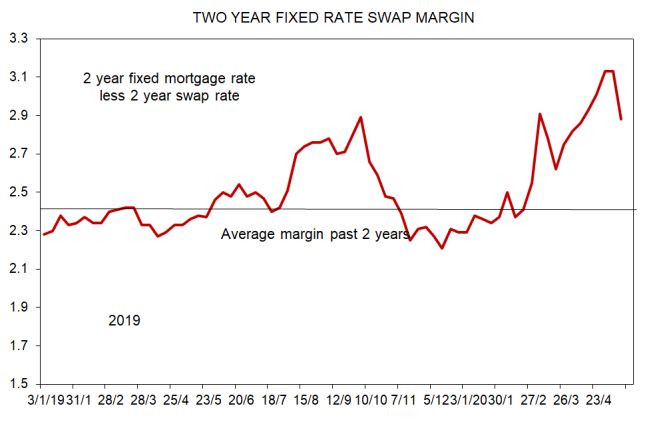

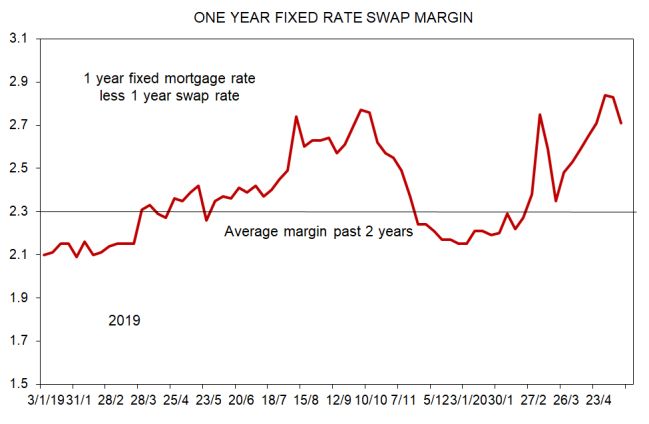

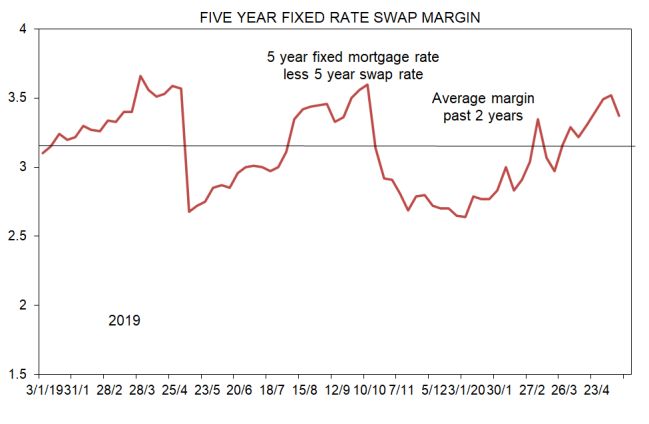

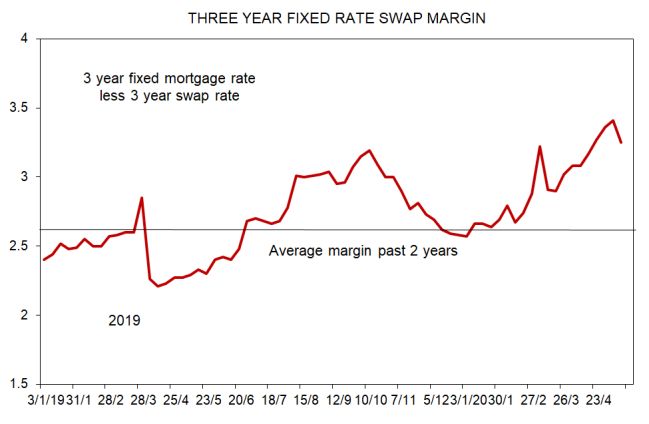

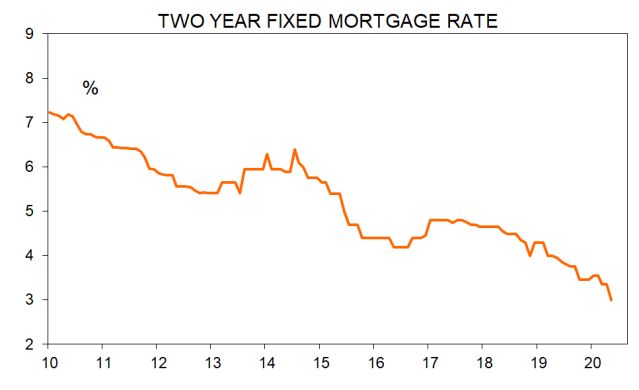

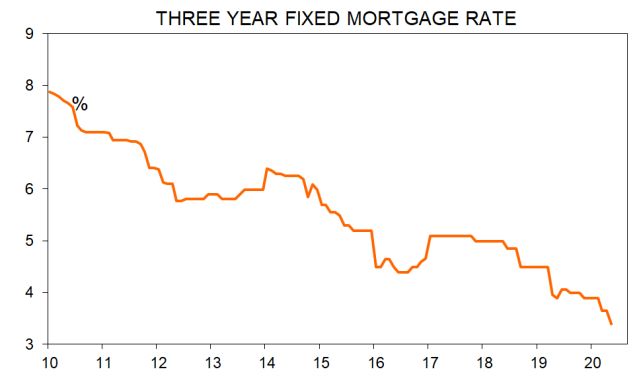

IS A FIXED RATE CHANGE IMMINENT?

Perhaps behind closed doors the Reserve Bank expressed their frustration at bank tardiness in cutting

lending rates before they near explicitly warned them of consequences in yesterday’s Monetary Policy

Statement. Whatever, banks have moved and margins have declined. But they remain high, so

eventually further rate cuts are likely.

You can form your own opinion as to whether banks might be about to raise or lower their fixed rates by

looking at the following graphs. They compare published fixed rates with the most frequently changing

component of the total cost of funds – the swap rate. Note that there are other funding costs which will not

be captured here, but they change infrequently. But be warned. There is no real forecasting insight delivered

by a thing (equity, exchange rate etc.) moving further from some concept of fair value or average. If a thing

is 10% above trend, it might simply be on its way to being 40% above trend. For good bank rate comparisons

access www.interest.co.nz

Page | 9Tony’s View

My daughter Lilia Alexander (finalist in the Youth category for Wellingtonian of the Year 2019) owns and runs

Social Media based Wellington – LIVE (>200,000 followers)

https://www.facebook.com/WellingtonLIVENZ/

“…the largest go-to social media-based updates and news platform for the Wellington region…” Wellington – LIVE offers

advertising options for local events and businesses.

Email: info@wellington.live

She also now has a photography site. https://www.liliaalexander.com/photography

This publication is written by Tony Alexander, independent economist. You can contact me at tony@tonyalexander.nz Subscribe here

https://forms.gle/qW9avCbaSiKcTnBQA

This publication has been provided for general information only. Although every effort has been made to ensure this publication is

accurate the contents should not be relied upon or used as a basis for entering into any products described in this publication. To the

extent that any information or recommendations in this publication constitute financial advice, they do not take into account any person’s

particular financial situation or goals. We strongly recommend readers seek independent legal/financial advice prior to acting in relation

to any of the matters discussed in this publication. No person involved in this publication accepts any liability for any loss or damage

whatsoever which may directly or indirectly result from any advice, opinion, information, representation or omission, whether negligent

or otherwise, contained in this publication.

Page | 10You can also read