Understanding Carbon Prices: Muyi Kazim - Standard Bank Group - February 2010

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Understanding Carbon Prices:

Muyi Kazim – Standard Bank Group

February 2010

INTRODUCTION

2

Preamble:

Without knowledge of the market it can be difficult to tell

what the right carbon price is for a CDM project.

(Having said that don’t worry too much about determining

price by yourself)

Topics:

The different factors affecting carbon prices and indications of a

likely contract price for the credits you generate.

Factors affecting future market prices will also be discussed.

Our Approach to pricing

About Standard Bank

CER – Registration Risk and Primary Price

3

Price of Exchange Traded Carbon from

March 2008 - Current

4

• Prices have been as high as €24 a tonne for guaranteed delivery CERs – traded on the ECX

• Alternatively they have been as low as €7.50 in early 2009 – as a result of the global economic

downturn reducing production rates in manufacturing and thus lowering power consumption

• Primary prices are artificially held up by the Chinese government ruling the lowest price €8 up to

2012.

• Primary prices are less volatile – generally prices have ranged between €7 and €13.

Factors Affecting Market Prices

Next 12 Months 2010 and Beyond 5

Size of the recovery and developments for the post 2012 environment,

post COP 15.

If there is no agreement for post 2012 and Europe adopts a lower target

2013 - 2020 then prices will fall as there will be less demand from that

period to soak up excesses from this period.

UNFCCC bottlenecks/approval innovations

DOE suspensions/delays

GDP and therefore manufacturing etc will be the main driver behind

prices, a quick pick up in GDP will lead to a quick pick up in carbon

prices.

In the EU more manufacturing – more power required – more emissions

– more requirement to purchase offsets

SB Trading desk view is that we may well see a sell off in carbon prices

in the first half of this year before they find some support. Expect to see

prices rise in 2011 and 2012.

The above said there will remain a premium for African/LDC CERs even

in the short – medium term due to demand still outstripping supply.

New sources of supply from LDCs and Africa; ie Re/Afforestation,

Biofuels, Programmatic approachPricing of CERs via trades

With Risk Factors 6

Spot trade:

− Wait until issuance and then sell

− Highest price but exposed to price movement risk until issuance

− Documentation: Spot ERPA or ISDA confirmation

Forward:

− Sell now for future delivery and payment

− Avoids price risk but no up-front finance

− Discounted price compared to spot but buyer takes price risk

− Documentation: ERPA

Futures

− Enter a derivative contract for a fixed future price

− Hedges price risk but penalties for non-delivery and need

sophisticated trading arrangements

− Documentation: ISDABuying Carbon credits from a Project

7

Standard Bank have one of the most active trading desks in the carbon markets,

based in our office in London

Due to our high level of experience in market and sophisticated valuation tools we

can accurately price primary project risk and offer competitive price on primary

carbon projects

Alternative pricing tools under ERPA agreements

Fixed price over the term of ERPA – both pre and post 2012.

Floating price over the period (On every delivery the current market price – less %

is paid)

Floating price with a floor and cap (limiting downside – showing possible financing

a minimum income)

Guaranteed delivery of a portion of the volume (this has a potential downside for

the project owner)

Ability of SB to prepay and cover CDM costsCarbon Finance – Trade Finance

8

Transacting to purchase carbon credits from a project under Clean Development

Mechanism

Purchase under an ERPA Agreement

Deliveries are only ‘expected’ volumes

Payment made only on delivery

This creates a requirement for funding of either the project itself, the CDM costs or both.

Trade Finance (Pre- Payments against carbon credits)

CDM Specific Costs

► Project Development (PDD completion)

► DOE fees (validation and verification)

► UNFCCC fees (reviews, registration)

► Consultants (Feasibility Studies, Brokers)

Carbon Specific

− Pre pay expected deliveries of credits

► Risk of non-registration

► Risk of non-delivery

► Risk of under-delivery

► Risk of delayed delivery

► Counterparty Risk – credit standing of counterparty, possible Step-In/ Novation

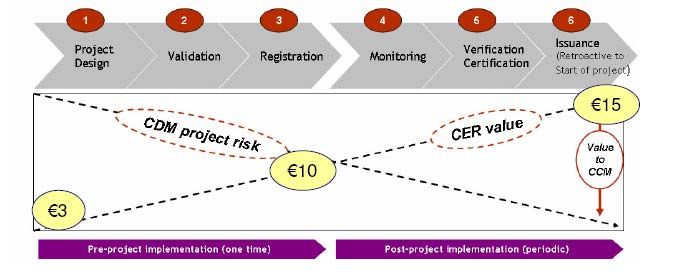

► Regulatory risk – post 2012Risks Associated with Carbon Credit Projects

9

Carbon reduction Carbon

Construction Issue of credits

assessment transaction

Feasibility and Validation and Verification and

Commissioning

financing registration certification

Resources

Counterparty Natural Business

Political risk and supplies

credit risk hazards interruption

delivery risk

Conventional project cycle Technology Eligibility and Delay in start Validation and

Carbon related project cycle

risk approval up reporting

Project risks

Carbon risksCarbon Finance – Project Finance

10

Project Finance (Debt financing against projects)

Finance of the project itself - Higher price potential for CERs

− Standard Bank has a large capability in renewable project finance

► Protected by the assets of the project

► Possible recall over other assets of the owner

► Project has an off taker with a signed Power Purchase Agreement

Debt finance against carbon

− As with the above, finance given is protected by assets or transaction flows

within the project.

► Power purchase Agreement in place

► Carbon Credit Off take in place (In-house /higher price)

► Creditworthy Off takers for both the above

► Can be worked against single or multiple transactionsCase Study – Structured Finance/Programmatic CDM

11

Structured Finance (multiple financing tools)

• A multiple of financing tools can be used together to achieve a pre-payment for project owners

•POA/CPA (CDM Program of Activities could also benefit from this approach)

A “first to market” transaction where we assisted an aggregator

of carbon credits (Camco), structured and placed a proportion of

their primary credit portfolio in the market

Project Tranche A

1,2,3,4…9

Tranche B

Project pool Tranche C

2008

Up front payment

Best Trade Award

Camco Structured

DistributionActions to improve carbon finance in Africa

12

African CERs are more isolated from regulatory risk than (for example)

Chinese CERs. Good and Bad for pricing

− Ability to use LDC CERs post-2012

Standard Bank is making a major effort to boost sub-Saharan African

CDM

− Specific Team dedicated to Carbon Origination in Africa

− Working internally and with other African FIs to develop financing

capacity in programmatic projects, small-scale projects and less

‘conventional’ project types and methodologies

− JV with UN agencies aimed at supporting CDM process financing,

supplying access to consultants, both at no cost

Requires cooperation across private and public sector

− To meet challenges of

1. Feasibility study financing

2. Early stage Equity financingOther External Factors Effecting CER Prices

13

There are over 10,500 installations throughout Europe that have been allocated

emission ‘caps’ and have the obligation to remain within their caps on an annual

basis

In order to achieve emission reduction targets the ‘cap’ set for each installation will

reduce every year, thereby forcing the installation to reduce emissions by internal

abatement or by them compensating by buying allowances to ‘offset’ their excess

emissions

There is therefore the ability for a polluting power station in Europe that would find it

very costly to reduce emissions to purchase credits from projects in non-Annex 1

countries under the Clean Development Mechanism (CDM)

In order to promote a certain amount of internal abatement however the EU

countries have set limits on the amount of CERs that compliance buyers can use in

conjunction with their EUA allowances – for example

UK limit = 9%,

Germany = 20%

This means that an installation in the UK with a cap of 100,000 tonnes per year that

intends to emit exactly to their cap, may replace up to 9,000 tonnes a year of their

EUAs with CERs

There is a financial incentive to do this as historically CERs have traded at a varying

discount to EUAs. Penalties are expensive ie EUR100, plus CC purchase price.

Limit in CERs leads to ongoing price differential, but demand for African CERS still

outstrips supply due to low CER production from African projectsStandard Bank, also trading as Stanbic:

The largest financial institution in Africa

14

A global emerging markets bank, headquartered in South Africa

In terms of total assets, Standard Bank is the largest bank domiciled in Africa

Full-service bank covering:

− Personal & Business Banking

− Corporate & Investment Banking

− Investment Management & Life Insurance

Leading financial services provider in South Africa – one of the fastest growing emerging market

banking sectors. Growing market share across all sectors and a consistent track record of

increasing profitability and franchise value

The largest bank in Africa with presence in 17 countries

Global reach on the ground in 16 countries outside Africa with distribution capabilities in the

world’s leading financial centres – New York, London and Hong Kong

Signed strategic partnership with the Industrial and Commercial Bank of China Limited (ICBC),

one of the largest banks in the world by market capitalisation

Total assets approximately US$162 billion (December 2008)

Market capitalisation of approximately US$14 billion (December 2008))

Present in 33 countries around the world

Employs over 50,000 people (including Liberty Life)Awards

15

2005 - 2008 2008 2007 2008

Best bank for Best Trade Finance Carbon Credits

payments and Bank in sub-Saharan Emerging Markets Best Trade Award

collections in Africa Africa Bank of the Year Camco Structured

Distribution

2006, 2007, 2008 2008 2006 – 2007, 2009 2008

Best overall bank Leading Trade Services

Best debt research Africa Bank for cash management Bank in sub-Saharan

house in of the Year in Africa Africa

South AfricaContact Details

16

Africa

Muyi Kazim (Lagos)

Muyideen.kazim@stanbic.com +234 802 042 0070

Trading, Structuring and Placement

Fenella Aouane, Geoff Sinclair, Mark Codling +44 20 3145 6888

fenella.aouane@standardbank.com

geoff.sinclair@standardbank.com

mark.codling@standardbank.com

CO2@standardbank.comDisclaimer

17

This presentation is provided on the express understanding that the information contained herein will be regarded and treated as

strictly confidential. It is not to be delivered nor shall its contents be disclosed to anyone other than the entity to which it is being

provided and its employees without the prior consent of the Standard Bank Plc (“SB Plc”). Moreover, it shall not be reproduced or

used, in whole or in part, for any purpose other than for the consideration of the financing described herein, without the prior written

consent of SB Plc. The information contained in this presentation does not purport to be complete and is subject to change. This

document does not constitute an offer, or the solicitation of an offer, for the sale or purchase of any investment or security. The

information contained in this document does not purport to be complete and it is subject to change. This is a commercial

communication. If you are in any doubt about the contents of this document or the investment or security to which this document

relates you should consult a person authorised under the Financial Services and Markets Act 2000 who specialises in advising on

such investments or securities. This document relates to derivative products and you should not deal in such products unless you

understand the nature and extent of your exposure to risk. No liability is accepted whatsoever for any direct or consequential loss

arising from the use of this presentation. This presentation is not intended for the use of retail clients. This document must not be

acted on or relied on by persons who are retail clients. Any investment or investment activity to which this document relates is only

available to persons other than retail clients and will be engaged in only with such persons. SB Plc is authorised and regulated by the

Financial Services Authority (“FSA”), entered in the FSA’s register (register number 124823) and has approved this document for

distribution in the UK only to persons other retail clients. Persons into whose possession this document comes are required by the SB

Plc to inform themselves about and to observe any such restrictions. You are to rely on your own independent appraisal of and

investigations into all matters and things contemplated by this document. By accepting this document, you agree to be bound by the

foregoing limitations. Kindly note that this presentation does not represent an offer of funding since any facility to be granted in terms

of this presentation would be subject to Standard Bank Plc obtaining the requisite internal and external approvals.

Standard Bank Plc, 20 Gresham Street, London EC2V 7JE

Value Added Tax identification number 625861525You can also read