2020 BKD Telecommunications Accounting Seminar

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2020 BKD Telecommunications Accounting Seminar

Revenue Recognition in the Telecom World August 13, 2020

To Receive CPE Credit › Individuals • Participate in entire webinar • Answer polls when they are provided › Groups • Group leader is the person who registered & logged on to the webinar • Answer polls when they are provided • Complete group attendance form • Group leader sign bottom of form • Submit group attendance form to training@bkd.com within 24 hours of webinar › If all eligibility requirements are met, each participant will be emailed their CPE certificate within 15 business days of webinar

Presenters

Jessica Richter, CPA, CITP, CISA®

Partner

jrichter@bkd.com

Eric Babler, CPA

Director

ebabler@bkd.comOur Goals for Today Refresh our understanding of ASC 606 Understand the effects on various telecoms that have implemented ASC 606 Learn what the potential future effects on operations may be for telecoms

ASC 606 Refresher

Creating a One-Stop Shop for

Revenue Literature

Current Guidance New Principle

Real Estate – General – Revenue Recognition

General Recognition

Construction- & Production-Type Contracts

Concepts

Real Estate – Retail Land – Revenue

Real Estate Sales (Subtopic 360-20)

Contractors – Construction Revenue

Recognition (Subtopic 976-605)

Industry-Specific Guidance

Software (Subtopic 985-605)

Persuasive evidence of The transfer of a

an arrangement exists promised good or

(Subtopic 910-605)

(Subtopic 970-605)

(Subtopic 605-35)

service determines when

Recognition

Delivery has occurred or revenue is recognized &

services have been occurs when (or as) the

rendered customer obtains control

of the asset. Transfer

can be made either at a

Price is fixed or

determinable point in time or over time

Collectibility is reasonably

assuredScope › Contracts with customers, except • Lease contracts • Insurance contracts • Financial instruments • Certain guarantees (other than product warranties) • Certain nonmonetary exchanges

The Five-Step Model

• Identify contract(s) with customer

Step 1

• Identify performance obligations

Step 2

• Determine transaction price

Step 3

• Allocate transaction price to performance

Step 4 obligations

• Recognize revenue when (or as) performance

Step 5 obligation is satisfiedStep 1 – Identify Contract(s) with

Customer

› Contract = “agreement between two or more parties that

creates enforceable rights & obligations” & meets the

following criteria

• Commercial substance

• Approval & commitment by all parties

• Identifiable rights, obligations, & payment terms

• Collectibility threshold

Step 1: Step 2: Step 3: Step 4:

Step 5:

Identify Identify Determine Allocate

Recognize

Contract(s) Performance Transaction Transaction

Revenue

with Customer Obligations Price PriceStep 2 – Identify Performance

Obligations

› Performance obligation

• Promise to transfer goods/services to customer

• Can be explicitly identified in contract or implied by customary

business practices

• One contract could equal one or many performance obligations

• Significant judgment may be required

Step 1: Step 2: Step 3: Step 4:

Step 5:

Identify Identify Determine Allocate

Recognize

Contract(s) Performance Transaction Transaction

Revenue

with Customer Obligations Price PriceStep 3 – Determine Transaction Price

› Transaction price = amount of consideration entity expects to be

entitled to (after collectibility threshold is met)

• Variable consideration

• Revenue constraint

• Significant financing component

• Noncash consideration

• Consideration payable to a customer

Step 1: Step 2: Step 3: Step 4:

Identify Step 5:

Identify Determine Allocate

Contract(s) Recognize

Performance Transaction Transaction

with Customer Revenue

Obligations Price PriceStep 4 – Allocate Transaction Price to

Separate Performance Obligations

› Allocate based on relative standalone selling prices of separate

performance obligations

• Observable price when sold separately (best evidence); otherwise, estimate

based on

o Adjusted market assessment

o Cost plus margin

o Residual value – only if highly variable or uncertain

Step 1: Step 2: Step 3: Step 4:

Identify Determine Allocate Step 5:

Identify

Contract(s) Transaction Transaction Recognize

Performance

with Customer Price Price Revenue

ObligationsStep 5 – Recognize Revenue When (or as)

Performance Obligations Are Satisfied

› Revenue recognized when (or as) control of good/service is

transferred to customer

› Transfer of control occurs when customer has ability to direct use

of, & receive benefits from, good/service

› Can be recognized over time or at a point in time, depending on

how performance obligations are

Step 1: Step 2: Step 3: Step 4:

Identify Determine Step 5:

Identify Allocate

Contract(s) Transaction Recognize

Performance Transaction

with Customer Price Revenue

Obligations PriceOverview of Transition Methods

› Full retrospective method

• Restate all prior years presented in the financials as if ASC 606 was in

place

› Modified retrospective method

• Recognize the cumulative effect of initially applying the new revenue

recognition guidance as an adjustment to the opening balance of

retained earnings as of the date of adoption, e.g.,1/1/2019

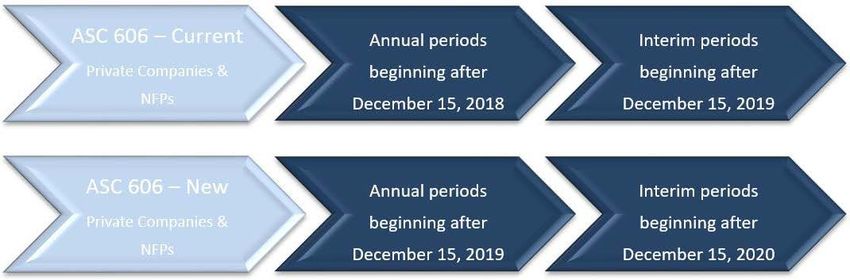

• Chosen by majority of companiesEffects of Implementation

Effects of Transition on Telecoms

› Overview – transition – example

• Telephone and Data Systems, Inc. (TDS)

ASC 606 Cumulative adjustment to retained earnings (in millions of dollars)

Cumulative

Cumulative Adjustment as

Adjustment to a % of

Retained Operating Operating

Earnings Revenue Revenue

TDS 164 5,109 3.21%

U.S. Cellular 175 3,967 4.41%

Non-Wireless Related (11) 1,142 -0.96%

Amounts from annual reports

http://s1.q4cdn.com/183458318/files/doc_financials/annual/2019/USM-PDF-AR-2018.pdf

https://s22.q4cdn.com/412964029/files/doc_financials/annual/2018/18-41220-1_343935_client.pdfEffects of Transition on Telecoms

› Overview – transition

• ILEC, CLEC, broadband (wired & wireless), video

o Most impacts were related to movement of revenues between line items on the income

statement

• Allocation of bundle discounts

o Very few had a retained earnings adjustment

• No change in the timing of the revenues

o Some had changes due to promotions for free installations with a contract of a certain

lengthEffects of Transition on Telecoms

› Overview – transition

• Cellular

o Frequently had a retained earnings adjustment

o Changed the timing of revenue & expense recognition

• Primarily related to free/discounted phones with contract

• Timing of recognition of commission expense

o Changed line items where revenue was recognizedSignificant Areas Affected › Allocation of discounts › Upfront payments made by customers › Commissions paid to employees › Directory revenue & expense

Allocation of Discounts

› Requirements

• If the sum of the standalone selling prices of a bundle of services

exceeds the consideration, then the discount is generally allocated

proportionately to all performance obligations in the contractAllocation of Discounts › The guidance does state that if there is evidence that the entire discount relates to only one or more, but not all performance obligations, the discount is not allocated proportionately to all performance obligations in the contract • The bar is high • We have not seen many companies meet the requirements

Allocation of Discounts

› Issue

• Most telecoms arbitrarily recorded whole discount to internet (highest

margin service)

Fixed discount of $15 when taking three services – INCORRECT

Standalone Selling Discount Discount Allocated Selling

Price Percentage Allocation Price

Local $18.00 0% $ - $ 18.00

Long distance $10.95 0% $ - $ 10.95

Internet $69.95 100% $ (15.00) $ 54.95

Video $99.95 0% $ - $ 99.95

Set-Top Box $5.95 0% $ - $ 5.95

$204.80 $ (15.00) $ 189.80Allocation of Discounts

Fixed discount of $15 when taking three services – CORRECT

› Effects

• Increase in internet revenue Standalone Selling Discount Discount Allocated Selling

Price Percentage Allocation Price

• Decrease in

Local $18.00 9% $ (1.32) $ 16.68

o Video revenue

o Local service revenue Long distance $10.95 5% $ (0.80) $ 10.15

o Other revenues Internet $69.95 34% $ (5.12) $ 64.83

• Re-imagining the bundle Video $99.95 49% $ (7.32) $ 92.63

• Consolidating bundles Set-Top Box $5.95 3% $ (0.44) $ 5.51

• Moving away from bundles $204.80 $ (15.00) $ 189.80Upfront Payments Made by Customers

– Activation & Installation

› Issues

• Many contracts include nonrefundable upfront fees that are paid at or

near contract inception

• Must assess whether the fee relates to the transfer of a promised good

or service to the customer

• Fees administrative in nature are not separate performance obligations

• Activities that improve the telecom’s network do not transfer a good or

service to the customerUpfront Payments Made by Customers

– Activation & Installation

› Effects

• Installation fee may need to be recognized over time

o Deferred revenue recognized over the life of the contract

• Most companies have determined these charges to be administrative in

nature

• May include a truck roll, but most times de minimis to the customer

• For most companies, this revenue is not material to the financial

statementsUpfront Payments Made by Customers

– Installation Fees Waived

Annual Internet Service Revenue

Customer Contract Term Monthly Fee Total Days 12/31/2020 12/31/2021 12/31/2022 12/31/2023 Total

Customer A 6/1/2020 6/1/2023 $ 69.95 1,095 $ 489.65 $ 839.40 $ 839.40 $ 839.40 $ 3,007.85

Customer B 3/1/2020 3/1/2023 $ 69.95 1,095 $ 699.50 $ 839.40 $ 839.40 $ 839.40 $ 3,217.70

Customer C 2/1/2020 2/1/2023 $ 69.95 1,096 $ 769.45 $ 839.40 $ 839.40 $ 839.40 $ 3,287.65

Customer D 1/1/2020 1/1/2023 $ 69.95 1,096 $ 839.40 $ 839.40 $ 839.40 $ 839.40 $ 3,357.60

Customer E 4/1/2020 4/1/2023 $ 69.95 1,095 $ 629.55 $ 839.40 $ 839.40 $ 839.40 $ 3,147.75

Customer F 5/1/2020 5/1/2023 $ 69.95 1,095 $ 489.65 $ 839.40 $ 839.40 $ 839.40 $ 3,007.85

Customer G 8/1/2020 8/1/2023 $ 69.95 1,095 $ 349.75 $ 839.40 $ 839.40 $ 839.40 $ 2,867.95

Customer H 9/1/2020 9/1/2023 $ 69.95 1,095 $ 279.80 $ 839.40 $ 839.40 $ 839.40 $ 2,798.00

$ 559.60 $ 4,546.75 $ 6,715.20 $ 6,715.20 $ 6,715.20 $ 24,692.35Upfront Payments Made by Customers

– Installation Fees Waived

Install Discount

Customer Contract Term Install Fee Total Days 12/31/2020 12/31/2021 12/31/2022 12/31/2023 Total

Customer A 6/1/2020 6/1/2023 $ (150.00) 1,095 $ (29.18) $ (50.00) $ (50.00) $ (20.82) $ (150.00)

Customer B 3/1/2020 3/1/2023 $ (150.00) 1,095 $ (41.78) $ (50.00) $ (50.00) $ (8.22) $ (150.00)

Customer C 2/1/2020 2/1/2023 $ (150.00) 1,096 $ (45.71) $ (49.95) $ (49.95) $ (4.38) $ (150.00)

Customer D 1/1/2020 1/1/2023 $ (150.00) 1,096 $ (49.95) $ (49.95) $ (49.95) $ (0.14) $ (150.00)

Customer E 4/1/2020 4/1/2023 $ (150.00) 1,095 $ (37.53) $ (50.00) $ (50.00) $ (12.47) $ (150.00)

Customer F 5/1/2020 5/1/2023 $ (150.00) 1,095 $ (33.42) $ (50.00) $ (50.00) $ (16.58) $ (150.00)

Customer G 8/1/2020 8/1/2023 $ (150.00) 1,095 $ (20.82) $ (50.00) $ (50.00) $ (29.18) $ (150.00)

Customer H 9/1/2020 9/1/2023 $ (150.00) 1,095 $ (16.58) $ (50.00) $ (50.00) $ (33.42) $ (150.00)

$ (1,200.00) $ (274.98) $ (399.91) $ (399.91) $ (125.20) $ (1,200.00)Upfront Payments Made by Customers

– Installation Fees Waived

Revised Annual Revenue

Customer Contract Term Monthly Fee Total Days 12/31/2020 12/31/2021 12/31/2022 12/31/2023 Total

Customer A 6/1/2020 6/1/2023 $ 69.95 1,095 $ 460.47 $ 789.40 $ 789.40 $ 818.58 $ 2,857.85

Customer B 3/1/2020 3/1/2023 $ 69.95 1,095 $ 657.72 $ 789.40 $ 789.40 $ 831.18 $ 3,067.70

Customer C 2/1/2020 2/1/2023 $ 69.95 1,096 $ 723.74 $ 789.45 $ 789.45 $ 835.02 $ 3,137.65

Customer D 1/1/2020 1/1/2023 $ 69.95 1,096 $ 789.45 $ 789.45 $ 789.45 $ 839.26 $ 3,207.60

Customer E 4/1/2020 4/1/2023 $ 69.95 1,095 $ 592.02 $ 789.40 $ 789.40 $ 826.93 $ 2,997.75

Customer F 5/1/2020 5/1/2023 $ 69.95 1,095 $ 456.23 $ 789.40 $ 789.40 $ 822.82 $ 2,857.85

Customer G 8/1/2020 8/1/2023 $ 69.95 1,095 $ 328.93 $ 789.40 $ 789.40 $ 810.22 $ 2,717.95

Customer H 9/1/2020 9/1/2023 $ 69.95 1,095 $ 263.22 $ 789.40 $ 789.40 $ 805.98 $ 2,648.00

$ 559.60 $ 4,271.77 $ 6,315.29 $ 6,315.29 $ 6,590.00 $ 23,492.35Commissions Paid to Employees

› Issues

• Companies may pay a commission to personnel for new customer sign-

ups.

• Sales commission meet the criteria for recognition as an asset as a cost

to obtain a contract which is then recognized as expense over the life of

the contract with the customer.

o Contract may not have a specific life & you will have to determine average life of the

customerCommissions Paid to Employees

› Effects

• Few companies pay employees commissions, mostly larger ones

• Amortize expense over contract term or customer life

• Expenses are spread out over the contract life rather than being

recognized all upfront when paidCommissions Paid to Employees

Expense

Employee Contract Term Commission Total Days 12/31/2020 12/31/2021 12/31/2022 12/31/2023 12/31/2024 12/31/2025 12/31/2026 Total

Employee A 6/1/2020 6/1/2025 $ 5,000.00 1,826 $ 583.24 $ 999.45 $ 999.45 $ 999.45 $ 999.45 $ 418.95 $ - $ 5,000.00

Employee B 3/1/2020 3/1/2026 $ 2,500.00 2,191 $ 348.01 $ 416.48 $ 416.48 $ 416.48 $ 416.48 $ 416.48 $ 69.60 $ 2,500.00

Employee C 2/1/2020 2/1/2023 $ 3,000.00 1,096 $ 914.23 $ 999.09 $ 999.09 $ 87.59 $ - $ - $ - $ 3,000.00

Employee A 1/1/2020 1/1/2024 $ 1,500.00 1,461 $ 374.74 $ 374.74 $ 374.74 $ 375.77 $ - $ - $ - $ 1,500.00

Employee B 4/1/2020 4/1/2024 $ 4,000.00 1,461 $ 750.17 $ 999.32 $ 999.32 $ 999.32 $ 251.88 $ - $ - $ 4,000.00

Employee C 5/1/2020 5/1/2026 $ 3,500.00 2,191 $ 389.78 $ 583.07 $ 583.07 $ 583.07 $ 583.07 $ 583.07 $ 194.89 $ 3,500.00

Employee A 8/1/2020 8/1/2025 $ 2,000.00 1,826 $ 166.48 $ 399.78 $ 399.78 $ 399.78 $ 399.78 $ 234.39 $ - $ 2,000.00

Employee B 9/1/2020 9/1/2026 $ 1,000.00 2,191 $ 55.23 $ 166.59 $ 166.59 $ 166.59 $ 166.59 $ 166.59 $ 111.82 $ 1,000.00

$ 22,500.00 $ 3,581.89 $ 4,938.51 $ 4,938.51 $ 4,028.04 $ 2,817.25 $ 1,819.47 $ 376.31 $ 22,500.00Amortization of Revenue & Expenses

› Issue

• Amortize revenue & expenses on a systematic basis, consistent with the

pattern of transfer of the service

o Over length of the contract

o No contract, use judgment to calculate average customer term

• Churn = customers who churned/beginning customers

• Lifetime = one/churn

› Effect

• Change in timing of recognitionAmortization of Revenue & Expenses

Customer Term as Reported Term as Reported

Company Customer Type contracts? on 10-Q - 9/30/2018 on 10-Q - 3/31/2019

Mediacom Residential No 36 months 36 months

Business Yes 1 to 10 years 1 to 10 years

CenturyLink Residential Yes 30 months 30 months

Business Yes 1 to 5 years 1 to 5 years

TDS Residential Not Reported Not Reported 14 to 60 months

Business Not Reported Not Reported 14 to 60 months

Frontier Residential Not Reported 3.8 years 3.8 years

Business Not Reported 3.8 years 3.8 years

Charter Residential No 6 months 6 months

Small Business No 6 months 6 months

Enterprise Yes 2 to 7 years 2 to 7 years

Information from September 30, 2018 10-Q as reported on https://www.sec.gov/edgar/searchedgar/companysearch.html

Information from March 31, 2019 10-Q as reported on https://www.sec.gov/edgar/searchedgar/companysearch.htmlDirectory Revenue & Expense

› Issue

• Companies should record revenue & expense when physical directory

is published

• Change from current practice

• Digital or online directory

o No change from current practiceDirectory Revenue & Expense

› Effect

• Revenue & expense recorded in month of publication

• Monthly & quarterly reporting obligations requiring GAAP financials are

impacted

• For most companies, revenue & expenses not material to the financial

statementsFuture Considerations

Future Considerations › Recent effective date update › Collaborative effort › Ongoing evaluation › Conversations with consultants

Effective Date Update

› Recently issued ASU 2020-05 postponed effective dates as

follows

• The delay is only effective if the entities have not yet issued or made

available for issuance their financial statementsEffective Date Update

› Delay does NOT impact ASU 2018-08, Not-for-Profit Entities:

Clarifying the Scope and the Accounting for Contributions

Received and Contributions Made

› Delay of ASC 606 implementation is NOT required

• With ASC 842, Leases coming, it might make a lot of sense to get ASC

606 done now

› Early adoption is encouragedCollaborative Effort

› Management will want to work closely with accounting

department to understand & champion accounting & reporting

requirements

› Requires collaboration across departments

• Marketing to assess new service & product offerings

o Discounts, bundles, other promotions

• Plant to assess activation & installation charges

• Human resources to assess commission pay structureOngoing Evaluation

› Effort doesn’t stop once the standard has been adopted

› Evaluation of current & future discounts/promotions offered to

customers

• Any change in price

• Any change in discounts

• Any change is service/product offerings

• Any concessions

o For example: free install for some customersOngoing Evaluation › Future changes in activation & installation charges › Changes to or addition of commissions to employees › Changes in directory revenue & expenses • Publication date change • Physical to digital directory

Conversations with Consultants

› Discuss accounting changes with

• External accounting firm

o To understand accounting & reporting requirements

o Effect on any loan covenants

o Don’t let the accounting of a decision drive the decision

• Cost consultants

o To understand any changes in timing of revenue & expense recognition

o To understand any new assets & liabilities on the balance sheetSummary

› Implementation & ongoing compliance with ASC 606 is a complex

process that requires

• Collaboration with multiple departments at the company

• Good documentation around the five-step model

• Strong communication with various stakeholders

o Board

o Consultants

o Owners

o Regulators

o LendersQuestions?

Continuing Professional Education

(CPE) Credit

BKD, LLP is registered with the National Association of State Boards

of Accountancy (NASBA) as a sponsor of continuing professional

education on the National Registry of CPE Sponsors. State boards of

accountancy have final authority on the acceptance of individual

courses for CPE credit. Complaints regarding registered sponsors

may be submitted to the National Registry of CPE Sponsors through

its website: www.nasbaregistry.orgCPE Credit › CPE credit may be awarded upon verification of participant attendance › For questions, concerns or comments regarding CPE credit, please email the BKD Learning & Development Department at training@bkd.com

Thank You! The information contained in these slides is presented by professionals for your information only & is not to be considered as legal advice. Applying specific information to your situation requires careful consideration of facts & circumstances. Consult your BKD advisor or legal counsel before acting on any matters covered

You can also read