UTILISATION OF BORROWED GOLD BY THE MINING INDUSTRY DEVELOPMENT AND FUTURE PROSPECTS - WORLD GOLD COUNCIL

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

WO R LD G O L D CO U NCI L UTILISATION OF BORROWED GOLD BY THE MINING INDUSTRY DEVELOPMENT AND FUTURE PROSPECTS Ian Cox, Ian Emsley Research Study No. 18

UTILISATION OF

BORROWED GOLD

BY THE MINING INDUSTRY

DEVELOPMENT AND

FUTURE PROSPECTS

Ian Cox, Ian Emsley

Research Study No. 18

April 1998

WO R LD G O L D CO U NCI L2

CONTENTS

The Authors..............................................................................................................4

Acknowledgements ................................................................................................5

Foreword ..................................................................................................................6

Introduction..............................................................................................................8

Summary ..................................................................................................................9

Part One

The Growth in Mine Utilisation of Borrowed Gold ........................................11

The Case for Hedging ..........................................................................................15

Hedging Instruments – Their Development and Usage ................................19

Australia ................................................................................................................21

North America ....................................................................................................22

South Africa ..........................................................................................................23

Gold’s Price Decline in 1996/97 – Its impact on Hedging Strategies ..........25

Part Two

The Supply of Leased Gold and Banking Risks in the

Gold Forward Market ......................................................................................29

The Market Supply of Gold to Lend: Private Investors and the

Central Banks ....................................................................................................29

Potential Supply and Likely Future Availability ....................................................29

The Return on Gold Lending and the Change in the

Perceived Risk/Reward Ratio............................................................................31

Legal Political and Institutional Constraints ..........................................................32

The Supply of Gold Hedging Services to the Producers:

The Bullion Banks ............................................................................................34

Counterparty Risks ..............................................................................................34

Interest Rate and Funding Mismatch Risks ..........................................................37

The Evolution of the Gold Risk Profile ..............................................................40

Increased Political Risk..........................................................................................40

The Credit Risk of New Hedgers ........................................................................40

The Rise of Project Finance..................................................................................41

The Future of Lease Rates....................................................................................42

Conclusions ..........................................................................................................43

Appendix

Hedging and the Forward Markets – Definition of Terms ..................................44

3THE AUTHORS

PART ONE

Ian Cox

Currently an independent consultant, Ian Cox worked for almost 20

years in the Precious Metals Department of Samuel Montagu, a

leading British merchant bank, and one of the founding members of

the London Gold and Silver Fixings. From 1986 onwards, he was

Head of the Trading Desk.

After gaining an M.A. degree at Cambridge University, where he

studied Natural Sciences, he worked for ICI in Australia and the UK

as a Research and Development Officer. During this period, he

undertook a number of raw material research studies for the

Purchasing Department, and later assumed responsibility for the

purchase of precious metals for the world-wide group, before

joining Samuel Montagu.

PART TWO

Ian Emsley

After higher education at the universities of Bristol and London, Ian

Emsley joined Anglo American Corporation of South Africa, where

he has worked as an economist and commodity analyst for 13 years.

Currently based in the London office of the Corporation, he spent

three years in Johannesburg between 1992-95.

4ACKNOWLEDGEMENTS

Much of the background material which forms the basis for this study

and accompanying statistical tabulations was obtained during the

course of discussions with a number of mining companies, dealers

and market analysts. The authors would like to thank them for their

assistance, and also staff of the World Gold Council whose comments

were most helpful in finalising the Study before publication.

The views contained in the report are those of the authors, and not

necessarily those of the World Gold Council.

5FOREWORD

Whatever happens to gold prices and the restructuring of the gold

industry, it is the authors’ view that gold lending and derivative

markets will continue to play an important role in gold markets.

Hedging strategies based on derivatives and lending meet basic risk

management needs that go beyond finance of new mine expansion.

During the 1980s advances in sophisticated financing techniques,

driven both by new analytic techniques and the availability of ever-

increasing amounts of computational power, spread to the gold

markets. Bullion banks saw the opportunity to augment their inter-

mediary role and the concomitant profits by applying both project

financing skills and derivative-based techniques to the needs of the

mining community. Gold producers had experienced a step change in

demand for finance generated by a dramatic increase in gold prices

during the 1970s. As a result, exploration grew strongly and the new

mines needed appropriate capital.

The new project financing strategies and derivative-centred

hedging required a source of borrowed gold and the traditional

sources of private gold deposits were declining. Bullion banks went to

the central banks and convinced them to move into the gold lending

market by offering steadily increasing interest rates for the use of a

previously dormant asset.

As a result, the gold banks were able to offer producers medium-

term gold loans which better matched assets and liabilities as well as

forward- and option-based structures to hedge existing (and new)

developments. These hedges retained exposure to gold price move-

ments, but provided shareholders with assurance that net worth

would be safeguarded in the case of violent price movements.

According to the authors, the gold banks did not gain their new-

found profitability without accepting some incremental risk. Central

banks continue to be loath to lend gold on a medium-term basis. The

bullion banks must accept the rollover risk in borrowing short-term

and lending long-term, as well as some gold interest rate mismatch risk.

Derivative-based hedging techniques required both the acquisi-

tion of sophisticated new knowledge (Black-Scholes option pricing,

delta hedging and others) and the willingness to act on that knowl-

edge by implementing complex skeins of obligations in spot, forward,

futures and options markets.

Confidence of all parties has increased substantially, as indicated by

a tripling of gold borrowing over the last 10 years to an estimated

4,000 tonnes per year currently. The market shows encouraging signs

of moving into longer-dated maturities. Central banks and commer-

cial banks continue to respond to increased demand with measured

supply. Both Germany and Switzerland, who have large gold reserves,

6recently entered the gold-lending market. Unless there is a large

default, the market should continue to push into new territory for

producer-related products.

In this valuable contribution that should help further public

knowledge of interesting developments in these important markets,

the authors take the view that the increase in central bank lending

and associated producer hedging has probably contributed to the

price trend. However, these practices have allowed central banks to

earn a return on their gold assets and for producers to facilitate mine

finance.

Robert Pringle

Centre for PublicPolicy Studies

7INTRODUCTION

Previous studies covering the growth and development of the gold

lending market have highlighted the prominent role played by the

mining industry through its use of borrowed gold to support hedge

programmes.

The first part of this study examines the processes which led to

the development of progressively more sophisticated hedging tech-

niques, and analyses the various factors which have produced a

considerable diversity in the use of hedge strategies. It also explores

the arguments for and against hedging, and finally assesses the impact

on the gold mining industry, following the substantial fall in prices

over the past eighteen months.

The second part focuses on the risk profile of the market, exam-

ined from the perspective of each of the three main participating

groups. It highlights the various factors which might act as a potential

constraint on the market’s future growth, and discusses the manner

in which problem areas are being addressed so as to ensure that

further expansion of the market can continue.

8SUMMARY

During the past ten years the market for gold borrowing has more

than tripled in volume, and is currently estimated at around 4,000

tonnes. The driving force behind this rapid expansion has been the

demand resulting from the hedging activities of the mining industry,

which increasingly has become the predominant user of borrowed

gold.

Development of the market has been facilitated by the interaction

of three major participating groups – the mining companies which

have successfully accessed and exploited new sources of gold supply

– the bullion banks, acting not only as intermediaries but also as inno-

vators of new and complex techniques in order to meet the needs of

the producers – and the central banks, which through loans and

swaps have provided a substantial proportion of the liquidity which

is essential for the funding of hedge transactions.

The resulting growth in mine hedging has increased its utilisation

of gold lending from around 400 tonnes, or less than 50% of the total

market a decade ago, to a current level estimated at between 2,550

and 2,650 tonnes, approximately 65% of all gold borrowing.

The rapid expansion over the last decade of the market for

borrowed gold has been made possible by central bank readiness to

lend gold from their reserves. Central banks have become more pro-

active in the management of their reserves in recent years and have

sought a higher return on their assets. The increase of average lease

rates to the 1-2% range has been sufficient to elicit increased levels

of central bank supply. Bullion banks have used borrowed gold to

expand the market for hedging services to gold producers and others.

Although gold hedge products carry lower risks for the bullion

banks than those which exist in the market for base metals hedging,

nonetheless, risks still exist, in particular counterparty risk and interest

rate/term mismatch risk.

Bullion banks are confident that the risks involved in gold hedge

products are relatively low. They have already managed these risks to

an extent by placing greater weight on options and floating gold rate

contracts. If the hedge market continues its rapid expansion, the risk

profile of the market may increase. Factors to be considered include:

the risk to producers of mining increasingly in politically unstable

parts of the world; the credit rating of companies seeking to increase

their hedging, in particular that of new mines carrying heavy debt

obligations; and the future level and volatility of gold lease rates.

9ESTIMATED BREAKDOWN OF DEMAND FOR GOLD BORROWING

End 1987: Total 800 - 900 Tonnes

Mine Hedging

45-50% Physical Market

Inventory Funding

40-45%

Speculative/Investment

Hedging

10-15%

End 1992: Total 2000 - 2100 Tonnes

Physical Market

Inventory Funding

Mine Hedging 25-30%

55-50%

Speculative/Investment

Hedging

10-15%

End 1997: Total 3900 - 4000 Tonnes

Physical Market

Inventory Funding

15%

Speculative/Investment

Mine Hedging Hedging

65% 15-20%

Source: Ian Cox

10PART ONE: THE GROWTH IN MINE UTILISATION OF

PART ONE: BORROWED GOLD

The mining industry over the past 10-15 years has emerged indis-

putably as the major utiliser of borrowed gold. Whereas in the early

1980s, producer hedging probably absorbed no more than 200-300

tonnes, by the end of the decade activity had accelerated so rapidly

that this sector’s requirement for borrowed gold exceeded the 1,000

tonne level. During the 1990s the pattern of growth has continued, but

somewhat more erratically than in the previous ten years. Never-

theless, boosted by some exceptionally large transactions in 1995, and

a record level of activity during the past year, the overall total of gold

borrowing to fund hedge transactions had risen to an estimated

2,550 - 2,650 tonnes by the end of 1997.

What were the underlying factors which enabled the market to

sustain this rate of expansion over a fifteen year period? This question

is best answered by examining the situation which existed in the early

1980s, and recognising that conditions were especially opportune for

the rapid development of hedging.

First, the gold mining industry had recently received an enormous

boost from the surge in gold prices during the previous decade, as a

result of which both production and exploration for new sources

were set on an expansionary course. Second, advances in the tech-

nology of extraction, especially the introduction of heap leaching,

had opened up the prospect of many new commercially viable

projects. Third, within the industry itself, previous perceptions of

risk were being re-evaluated. As a direct consequence, mining compa-

nies already aware of the uncertainties associated with exploration,

discovery and exploitation of new deposits, began to look favourably

at strategies which would protect the market value of assets in the

ground against future price fluctuations.

The producers were ably assisted in pursuing their newly found

strategies by the bullion dealing banks, operating with the enlisted

support of the central banks. Initially the dealers had been able to

draw on their own captive sources of liquidity, consisting essentially

of unallocated gold accounts held by private investors. These had

been steadily built up during the years in which gold had proved a

highly successful investment vehicle. It had quickly become apparent

however that this base of liquidity would soon be insufficient to satisfy

the longer term needs of a burgeoning demand from producers for

gold borrowing, especially as the amount of gold held in unallocated

accounts was itself beginning to decline. Investors were switching

out of gold into other higher yielding instruments. More gold was

being redistributed into the physical markets in order to satisfy

emerging consumer demand in the Middle East and Far East, thereby

1112

RESERVE

CHANGES IN INTERNATIONAL GOLD STOCKS AT THE NEW YORK FEDERAL RESERVE

600

400

200

0

Tonnes (end year)

-200

-400

-600

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 *1996 *1997

Source: New York Federal Reserve *Estimatebecoming no longer available to fund gold borrowing transactions.

The solution was to bring into play the enormous reserves held

by central banks and other monetary authorities, thus transforming

the potential scale on which future hedging business could be funded.

On a practical level, this process of mobilisation frequently necessitated

the transportation of gold physically from its former location, (e.g.

The Federal Reserve Bank in New York) to London, the pivotal market

for gold borrowing transactions, with upgrading where necessary to

meet current trading standards. Much of this work was undertaken by

the bullion banks themselves, as a means of building relationships

with the providers of liquidity. The innate caution of official institu-

tions towards this new sphere of activity was gradually overcome by

the attractive prospect of being able to demonstrate for the first time

a practical utilisation of a proportion of their reserves, which could

yield interest, and hence generate a regular annual income.

The bullion dealers’ second, and equally important contribution

to the expansion of mine hedging, was to adapt techniques and strate-

gies already used in other financial markets to meet the specific needs

of the gold mining industry. In particular, imaginative use was made

1

of the forward contango , a characteristic of the gold market which

over the years has offered enormous benefits to prospective hedgers,

and provided opportunities for the pricing of future production which

do not exist in most other metal markets. Such innovation has been

the main driving force behind the continued expansion of gold

borrowing into the 1990s, and a more detailed description of these

strategies and their application is given in a subsequent section of

this study. In broad terms however, the major developments have

been a significant extension of the range of hedge products, coupled

with a growing tendency to ‘tailor ’ solutions to meet the specific

needs of individual companies. Additionally there has been a consid-

erable lengthening of the time horizon for hedge transactions, in

some instances to as much as 12 years. As a result, mining compa-

nies now have the possibility to hedge much larger quantities of

future production should they so desire.

1

The contango or forward premium exists because of the size of the pool of liquidity,

relative to annual market supply, which is potentially available from long term

holders. It is this reserve which provides the capacity to fund forward hedging, and

which sets gold apart from other metal markets.

1314

THE CASE FOR HEDGING

Given that the hedging of commodities can be traced back far more

than a century, and that the bullion dealing banks have been offering

an ever increasing range of hedging facilities to gold mining compa-

nies during the past 25 years, it is perhaps surprising that the principle

of hedging is still the subject of much forceful debate, and that having

assessed all the arguments, mining companies can still differ dramat-

ically from each other in pursuing their declared policies.

At least it is possible now to regard some of the issues previously

the subject of hot debate as somewhat academic. For example it was

frequently argued that if mining companies did not hedge the price

would be higher, because there would be no impact on the market

from ‘accelerated supplies’ – i.e. gold sold but not yet produced.

Equally it has been suggested that if only the central banks would

desist from lending their gold to the market, the essential liquidity

which is needed to finance hedging would be denied to the

producers, and hence the temptation to sell forward, with its price-

damaging consequences, could not be realised in practice on any

significant scale.

Such viewpoints, whilst they may have some validity, have

nonetheless been overtaken by events, as the market has continued to

evolve. Mining companies operate in a highly competitive environ-

ment, and need to employ all means at their disposal, including

hedging, where they believe it to be advantageous for their business,

in order to maintain profitability. In the case of central banks, many

have concluded that whilst gold remains a part of their reserve port-

folio it should be actively managed alongside other assets. Lending

gold is just one option available, but as more official institutions,

including some very large holders, enter the market as a result of

careful consideration, it is apparent that such steps once taken are

unlikely to be easily reversed.

For some time certain commentators and analysts tried to deny

that forward sales had any effect on the spot price of gold, arguing

that any gold hedged in this way would eventually be delivered at

contract maturity, therefore no net impact on overall supply resulted.

Others have suggested that forward gold purchases from producers

by the bullion banks could somehow be fitted into a complex ladder

of existing transactions, utilising gold already available from within the

system, in such a manner as to nullify or at least to dampen any influ-

ence on the spot market. Adherents to such views however would

appear to be diminishing in number in recent years, possibly as a

result of acquiring a clearer understanding of the way in which bullion

banks offset potential price risk on forward transactions through their

use of the inter-bank market for spot gold. In addition, having exam-

15ined gold’s disappointing performance over the past ten years, it

would be difficult to conclude that the continued expansion of

producer hedging had not in some way been a contributing factor

to the overall trend in prices.

Given that a number of positive arguments can be put forward in

favour of hedging, it is nevertheless apparent that individual mining

companies need to be selective in adapting the basic principles to fit

the needs of their particular operations.

Certain advantages are readily discernible. For example budgetary

control is greatly enhanced by the pricing of a proportion of forward

production, since it increases the certainty of future revenue. Explo-

ration of new sources, the financing of projects, especially in the early

stages, and further expansion of existing operations all require

working capital, and through the appropriate use of hedge strate-

gies mining companies have the opportunity to generate ‘acceler-

ated income’, thereby facilitating the management of cash flows.

Finally in the event of a prolonged period of adverse market condi-

tions, revenue from previously established hedge transactions can

assist in meeting the cost of either closing an uneconomic operation,

or placing it on a care and maintenance basis.

The most commonly voiced concerns regarding hedging are the

potential impact of additional selling on the gold price, and the possi-

bility that shareholders, especially those investing in marginal mines,

will view adversely actions which might reduce the company’s capital

appreciation potential, expressed through its share value. Such consid-

erations probably account for much of the diversity among producers

in attitudes to hedging, ranging from the active, where as much as

10 times annual production may be hedged at any one time, to the

passive, where a stated policy of non-hedging exists.

On the first point, the significance of ‘accelerated selling’ cannot

be entirely discounted, but nevertheless it needs to be placed in the

context of a dynamic market in which a number of participants

including investors, speculators and central banks may equally act

as sellers at a given time or price. Mining companies operating in

such an environment have adopted a pragmatic approach, recog-

nising that their individual actions are insufficient to exert other than

a marginal influence on the market, given its current size. They have

consequently devoted primary consideration to the profitable manage-

ment of their operations, through appropriate use of the forward

markets.

With regard to the second concern, there are justifiable grounds

for individual companies to assess their particular place within the

cost spectrum, and to consider possible shareholder motivations.

However in practice, no unarguable case has been made which

suggests that producers with hedging programmes in place actually

suffer adverse shareholder sentiment as a result. In fact some mining

16companies have made direct reference to the extent of their hedge

programmes as a positive factor for shareholder consideration. More-

over the advent of more sophisticated option strategies has made it

much more possible for companies if they so desire to protect the

downside risk associated with assets in the ground which have yet to

be produced, whilst still retaining the potential to capitalise to a

considerable extent on any future market appreciation.

To summarise it is apparent that in today’s market there is a

growing consensus in favour of some form of hedging, and that many

of the differences within the industry revolve around such issues as

the degree of hedging which is appropriate and the type of strate-

gies to be deployed. Nevertheless it should be emphasised that the

decision making process for producers of gold has been greatly simpli-

fied by the continued presence of a contango market in each of the

currencies of the major producing countries. It is this factor above all

others that has ultimately proved decisive in persuading much of the

industry that hedging is beneficial for their business.

1718

MINE HEDGING: ESTIMATED GOLD BORROWING REQUIREMENTS

3000 450

430

2500

410

390

2000

370

1500 350

Goldprice, US $/oz

Gold borrowing, tonnes

330

1000

310

290

500

270

0 250

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

Source: Ian Cox Options Forwards/spot deferred Loans Annual Average Gold PriceHEDGING INSTRUMENTS – THEIR DEVELOPMENT AND USAGE

In the early 1980s when the gold mining industry first began to

develop an increasing appetite for hedging, the menu of available

products was distinctly limited. Loans made available by the bullion

dealing banks were for a relatively limited duration – 2-3 years was

generally the maximum term which could be negotiated – and

forward sales also were transactable only for similar periods. At that

time the gold options business was relatively undeveloped, and

confined to a small group of operators. The premiums payable

reflected both high underlying volatility and low market liquidity,

rendering such instruments more suitable for speculators than

producers seeking price protection for future output.

Whilst equity markets proved the preferred route for financing

much of the gold mining industry’s expansion through the 1980s,

gold loans also were extensively utilised as a means of funding explo-

ration and new project development. A relatively low interest cost,

paid in gold from future output, was viewed as advantageous when

compared with borrowing money, particularly in view of the high

interest rate environment which prevailed at that time.

Towards the end of the 1980s hedging activity began to accelerate

rapidly. Australian producers were very much in the forefront of this

development, although North American business also expanded in

conjunction with a sharp rise in output. The introduction into finance

departments of managers with a broad range of previous experience

in handling risk exposure helped to promote a greater awareness of

the opportunities presented by a combination of a spot market which

in late 1987 had briefly touched $500/oz, high domestic interest rates

in the major gold producing countries, and a newly developed depth

in the options market as more bullion banks began to offer a dealing

service.

A greater emphasis on derivatives business brought direct bene-

fits to mining companies seeking to increase their hedging

programmes, and many of the strategies were developed in co-oper-

ation with the bullion banks with the objective of meeting specific

needs. A common feature among many of the products was an inbuilt

flexibility which enabled the producers to manage their hedge

throughout its contract life, and to respond to signals marking a

change in interest rates, gold borrowing rates and currency parities.

Analysis of the hedging patterns which occurred during the 1990s

indicates that whilst volumes hedged maintained a broadly expan-

sionary trend, producers regularly shifted from one product to

another at different times, in seeking to maximise their returns, and

also to secure adequate protection against adverse price movements.

In the section which follows, a more detailed examination is made

1920

GEOGRAPHIC VARIATIONS IN ESTIMATED MINE HEDGING ACTIVITY

50

45

40

35

30

25

20

% of Total Producer Hedging

15

10

5

0

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

Source: Ian Cox

Australia North America South Africa Otherof some of the more popular hedge strategies followed by gold mining

companies within the major producing regions, and the differences in

approach prompted by considerations of movements in local interest

rates and currencies.

1. Australia During the initial period of worldwide resurgence in gold mining in

the early to mid 1980s, Australia followed a pattern of hedging

which was similar to that of other regions, deploying a mixture of

gold loans to finance new projects, and forward sales to lock in

future price returns. However the producers soon began to seek

more sophisticated products. A major benefit to be exploited arose

directly from the prevailing high level of domestic interest rates,

which at one point touched 18%, and which exceeded 14% for

lengthy periods. Despite the existence of double-digit domestic

inflation at that time, the industry took the view that after allowing

for the cost of borrowing gold, a net contango of around A$60/oz per

annum presented a hedging opportunity not to be missed. Since the

beneficial effects of high forward premiums became even more

apparent in the longer maturities, a concerted drive was made to

extend the boundaries for forward hedging beyond the normal 3-4

year maximum into the 5-7 year range. In fact this process has

proved to be ongoing, and despite a less favourable price

environment and much reduced contangos during most of the

1990s, some companies currently have established positions with

maturities as far out as 10-12 years.

During the period immediately preceding January 1991, Australian

producers were actively engaged in optimising returns ahead of the

imposition of a profits tax. Whilst undoubtedly this provided addi-

tional motivation at the time, nevertheless the clear benefits arising

from the extensive hedging undertaken in the run up to 1991 have

tended to reinforce the arguments for maintaining a sizeable hedge

programme relative to annual output, and the region has continued

to offer a lead in terms of volumes hedged as a ratio of annual produc-

tion, and also in the length of contract maturities.

Active utilisation of options has been another notable facet of

Australian hedge business. The existence of a sizeable contango in

Australian dollars price terms provided the opportunity to sell call

options at strike prices above the money and to utilise the premiums

to buy protective put options on a favourable ratio at zero cost. In

this way producers were guaranteed an eventual selling price within

a prescribed band, irrespective of the actual level of spot prices at

maturity.

A further imaginative use of the high contango led to the devel-

opment of the flat-rate forward contract and other variations based on

the same principle. In this instance the producer contracted for a

series of equal deliveries over a given period. Whereas under normal

21circumstances, each sale would progressively have yielded a higher

price for the longer maturity, the producer in practice received an

enhanced premium at the earlier stages, foregoing a portion of the

contango which would normally have been due for the later deliv-

eries. Such arrangements had the benefit of yielding enhanced cash

flow during the early life of the mine.

Options have continued to provide the most flexible medium for

the more active approach to price risk management, and the

Australian producers perhaps more than other mining groups have

proved especially receptive to the introduction of so called “exotic”

options, which became fashionable in the early 1990s. Many of these

products were cost effective through the employment of variations on

the barrier principle, whereby certain pre-set conditions were trig-

gered only if the underlying spot price of gold reached a certain level.

Other products which have also found extended use as hedging

tools include spot deferred contracts, where the seller retained flexi-

bility with regard to the actual delivery of physical metal, and floating

rate contracts, where the spot basis for the sale is fixed, but either the

gold borrowing rate or the currency interest rate is priced on an

agreed formula at fixed intervals during the life of the contract. These

arrangements have appealed especially to Australian producers

because of the scope which they offer for continuous hands-on risk

management, with the facility to anticipate movements in currencies

and interest rates.

2. North Whilst there have been periods of opportunity for North American

America producers, notably towards the end of the 1980s, when US$ interest

rates briefly touched 10%, in general terms the background scenario

has been less favourable for hedging than that available to their

major competitors.

The incentive offered to Australian producers in the years imme-

diately preceding 1991 produced an added surge in activity which

fortuitously coincided with a peak in spot prices and contangos. US$

interest rates have subsequently remained consistently below those

prevailing in either Australia or South Africa, and the returns achieved

by US producers, being measured in US$, have been denied the bene-

fits arising from currency depreciation. In other major producing

regions this factor has helped to sustain acceptable price levels for

forward hedging despite the general downtrend in gold prices during

the 1990s. Taking such factors into account, it is not altogether

surprising to find that compared with Australia the North American

producers are less extensively hedged, measured in terms of volume

relative to annual output, and also in the length of forward maturities.

Many of the hedging strategies operated by North American

producers have been dictated by the constraints of operating in a

forward market where US$ premiums have been relatively unat-

22tractive for prolonged periods. The effect has been to produce a much

greater bias towards the use of spot deferred contracts, and also a

more extensive deployment of option strategies. Whereas in some

instances calls have been sold to finance the purchase of puts, in other

cases, the call option premiums have been generated purely to provide

an added stream of income.

Active management of the hedge book risk has been a notable

feature of some of the largest producers in the region and strategies

have often been geared towards range trading – previously estab-

lished transactions regularly being closed out with the intention of

repositioning at a more favourable level. Finally there has also been a

tendency towards managing directly the cost of borrowing gold,

which proportionally has a greater impact on the net yield from

forward sales than in the regions which have the benefit of a higher

contango in their local currency.

3. South At first sight it would appear that many of the domestic financial

Africa circumstances which have combined to produce hedging

opportunities for Australian producers could equally well apply to

South Africa. However the world’s largest producer has tended over

the years to lag behind its competitors in hedging activity, especially

when the volume of business is compared with annual output.

Because of the restrictions imposed by the Reserve Bank on hedging,

the producers historically were limited in the scope available to them

for price protection. Eventually however these restrictions were

removed, enabling the industry to compete on more equal terms with

its rivals. The major mining companies were then able to view the

total spectrum of hedging opportunities in much the same terms as

their Australian counterparts.

A more conservative approach to hedging was not entirely the

consequence of domestic controls. During the 1980s Rand depreciation

against the major currencies acted as a corrective mechanism, making

the case for forward sales far less clear cut than in other gold

producing regions. Operating costs were heavily geared to the local

currency, particularly in respect of labour costs, a major component in

deep mining activities.

From around 1990 onwards however it became apparent that the

major mining companies were beginning to take a more aggressive

stance on hedging and the next few years involved something of a

catch-up process. One important difference at that time however was

that despite the existence of high contangos in Rand terms, the

volume of hedging was conducted for relatively short maturities,

chiefly in the two year time span.

In 1995 however two transactions took place which firmly estab-

lished South Africa in the major league of gold hedging, and

temporarily placed pressures on the borrowing markets which led

23to a sharp rise in rates, until corrective forces began to take effect.

The hedge programmes, although differing in certain elements, were

initiated for essentially the same purpose, primarily to secure a major

part of the funding associated with long-term expansion of production

at specific areas. The size of the transactions and their duration were

also features which set them apart from any previously negotiated

– Gengold’s Beatrix development involved 90 tonnes of gold, whilst

JCI’s expansion at the South Deep section of Western Areas required

a hedge covering no less than 227 tonnes, and operating over an

1

8 /2 year period.

The deal structures incorporated several techniques which had all

been utilised previously, but they provide an illustration of the

progress which has been made in tailoring a hedging product to suit

the requirements of a particular situation. First, the entire planned

production of the JCI project was sold forward in regularly spaced

increments. However the prices negotiated involved an element of

enhanced cash flow in the early stages, offset by a correspondingly

reduced return towards the end of the contract. Second, call options

were purchased for 55% of the volumes sold, in order to preserve

some degree of upside potential for returns in the event of a rise in

gold prices. Third, Rand call options were purchased for 45% of the

maturing gold forward sales value, in order to protect against the

possibility of a sharp depreciation of the Rand which would impact

directly on operating costs.

Transactions such as described above are likely to occur only rarely,

but they nevertheless highlight some of the background factors which

can result in a use of hedging techniques which goes far beyond the

simple objective of fixing the price of future production.

24GOLD’S PRICE DECLINE IN 1996/97 – ITS IMPACT ON

HEDGING STRATEGIES

In December 1997 the spot price of gold touched $283/oz, the lowest

for eighteen years, and the culmination of a downtrend which began

almost two years previously, producing an overall decline of almost

32% measured in US dollar terms. Whilst many market commentators

might have cautioned against over optimism in February 1996, when

the price had almost reached $415/oz, speculative buying was nearing

a peak, and prices had become detached from levels which had been

regularly supported by physical demand, nevertheless few observers

would have been bold enough to anticipate an impending collapse

even to below $350/oz.

The various factors which led to gold’s step by step retracement

have been well documented. During that time producers were forced

to react constantly to adverse circumstances, and to reformulate their

existing hedge policies. Risk management skills of the financial officers

of gold mining companies were tested to a far greater extent than in

any of the three years preceding.

During 1994 and 1995, whilst the market had encountered resis-

tance when approaching the $400/oz level, nevertheless the constant

reappearance of support from the physical markets had assisted in

producing a relatively narrow and stable trading range. Many

producers had enhanced the returns on their hedging programmes

by successfully anticipating and utilising these parameters to their

advantage. The series of events therefore which commenced in late

1996 and unfolded at regular intervals throughout 1997 required a

drastic reappraisal of previously held conceptions. The gradual real-

isation that through a combination of market factors gold prices were

on an extended downward path led to an accelerating pace in

hedging activity as the year progressed. In total an estimated 500

tonnes of additional market supply resulted, of which a significant

proportion, about 200 tonnes, was attributable to the delta-hedge

component of options transactions, most of which were put related.

Despite gold’s steep decline during 1997, currency considerations

partly mitigated the fall in some major producing regions. For example

whereas the difference between the high and low over the year in

US dollars was approximately 23%, weakness in the Australian dollar,

exacerbated by the growing financial crisis in Asia, restricted the

downturn to less than 9% in Australian dollars. In the case of South

Africa there was a much smaller currency depreciation, and prices

measured in Rand fell by around 20% over the year.

Of course at price levels of around $300/oz the gold producing

industry is facing a range of problems which goes far beyond the

question of whether to continue with hedge programmes and if so

25in what form. Nevertheless some new patterns are beginning to

emerge, which provide an indication of likely responses. One crucial

difference between the situation currently and that of a year earlier is

that pricing decisions taken now could well have a bearing on the

continued survival of very many more operations, whereas a year

ago success of a hedge programme was in most instances an added

benefit to be assimilated into the overall level of profitability of the

company.

One particular consequence of the drastic fall in prices is that the

industry faces a period of considerable rationalisation. Also it is

inevitable that many of the projects due to come on stream over the

next few years will be at the very least postponed, pending a degree

of recovery in prices. Both of these developments will have implica-

tions for hedging activity – the first being of greater impact short-

term, the second having more medium-term implications.

For those gold producers which had built up an established book of

hedge transactions there has been an opportunity to close out prof-

itable forward positions, thus providing immediate benefit to the

cash position of the mining company. However, taking such action

inevitably creates a fresh exposure to future spot price fluctuations,

and whatever the inner convictions of individual producers regarding

the prospects for recovery in the market, few are in a position to take

an extensive gamble on the price, given the events of the past year.

Accordingly exposure in almost all cases has been restructured

with a greater emphasis on options which serve as protection against

a worst-case scenario, but which tend not to lock in the producer too

tightly at current levels. Such strategies provide a degree of assur-

ance to shareholders, and at the same time will tend to relieve some

pressures on the spot market, because the net effect of these trans-

actions is a lower overall delta associated with the underlying hedge,

and hence a reduced funding requirement in terms of borrowed gold.

This factor coupled with the likelihood of delays and reductions in

the volume of new gold projects, which under normal circumstances

would have initiated additional hedge programmes, suggests that in

the short term at least the sum total of gold borrowing needed to

finance producer hedging could be somewhat reduced, and taking

1998 as a whole, the 500 tonnes of accelerated supply initiated by last

year’s producer hedging is unlikely to be repeated on the same scale.

Longer term however the situation could well be rather different.

Notwithstanding the earlier comments regarding new projects, the

search for, and successful implementation of low-cost gold projects

continues. This will eventually bring new volumes of hedging to the

market, especially as providers of project finance will be closely

concerned with ensuring the success of the operation in the early

years. In parallel with this development, gold producing companies

are also making strenuous efforts to reduce operating cost levels, and

26success in this direction over a period of time will not only create a

lower cost base across the industry, but would then make possible

opportunities for profitable hedging at lower market prices than

might be considered acceptable at present. Given the considerable

uncertainties which currently exist as to the future intentions of some

of the larger holders of gold in the official sector, and bearing in mind

recent experience of the extent to which gold prices can react to

events, it may well be that should more favourable conditions re-

emerge at a future date, some mining companies will seek to protect

a greater proportion of their future production than has been the

case to date. At the present time, despite the considerable differences

that exist within the industry, the volume hedged in relation to annual

output represents little more than one year’s production, averaged

across the market worldwide.

If the mining companies’ hedging activities and the demand for

borrowed gold continue to expand along the lines suggested above,

it becomes relevant to examine the question of whether such devel-

opments have any implications for the future risk profile of the

market. This issue is discussed in greater detail in the second part of

the study.

2728

PART TWO: THE SUPPLY OF LEASED GOLD AND BANKING RISKS

IN THE GOLD FORWARD MARKET

THE MARKET SUPPLY OF GOLD TO LEND: PRIVATE INVESTORS

AND THE CENTRAL BANKS

Over the past ten years use of the gold forward market by producers

has expanded at a rapid pace. Demand for gold loans was also strong

in the early phase of expansion of mine output during the 1980s, but

has subsequently declined, as repayments outweighed new business.

More recently, options have been utilised on a wider scale than previ-

ously and the delta component of all producer-based transactions

currently absorbs approximately a fifth of the total quantity of gold

borrowed to finance mine hedge business.

As has already been described in part 1 of this study, the expan-

sion of the market for gold loans, forwards, and options has been

greatly facilitated by the existence of a liquid gold lease market. Coun-

terparties have been able to finance their activities through the avail-

ability of low cost borrowing, which in turn has been responsible for

the maintenance of a contango on forward prices. A progressively

increasing contango makes the forward market very attractive to

mining companies seeking to hedge future production. This

structural feature of the gold forward market has proved possible

only because of the gradual entry into the market of central banks,

supplementing the previously existing supply of liquidity available

from private holdings. In today ’s market, the bullion banks have

come to depend almost entirely on the official sector to fund total

borrowing demand (of which producer hedging is by far the largest

component) and to meet any future growth in requirements. The

attitude of central banks towards the risks entailed by their gold loan

and swap activities is therefore of crucial importance to the future

development of the market.

Potential Despite continuing net official sales of gold in the last ten years,

Supply and central banks, excluding the IMF and EMI, still hold around 28,000

Likely Future tonnes. The distribution between countries largely reflects the

Availability position which obtained when gold’s official monetary role ended.

Consequently there exists a considerable diversity in the level of

gold holdings expressed as a percentage of total reserves. Given that

the present level of central bank lending is thought to be

somewhere in the region of 3,600 – 3,700 tonnes, (approximately

90% of the total liquidity available to the gold borrowing market),

the requirement for funding is unlikely to reach 20% of aggregate

2930

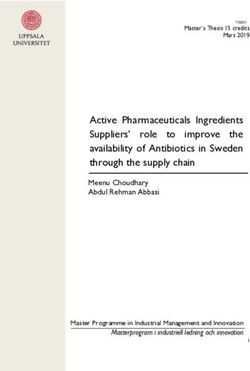

REPORTED CENTRAL BANK AND INTERNATIONAL AGENCY GOLD RESERVES

END 1997, TONNES

Over 500 200-499 100-199 50-99 10-49

United States 8140 Spain 486 BIS 194 Brazil 97 Slovak Republic 40

IMF 3217 Belgium 477 Algeria 174 Canada 96 Norway 37

Germany 2960 Russia 463 Iran 151 Indonesia 96 Peru 35

EMI 2782 Taiwan 422 Sweden 147 Romania 93 Afghanistan 30

Switzerland 2590 India 397 Saudi Arabia 143 Australia 80 Bolivia 29

France 2546 China, Peop. Rep. 397 Philippines 135 Kuwait 79 Poland 28

Italy 2074 Venezuela 356 South Africa 123 Thailand 77 Syria 26

Netherlands 842 Lebanon 287 Turkey 117 Egypt 76 Jordan 25

Japan 754 Austria 250 Libya 112 Malaysia 73 UAE 25

United Kingdom 573 Greece 107 Pakistan 64 Morocco 22

Portugal 500 Chile 58 Nigeria 21

Kazakstan 56 Neth. Antilles 17

Uruguay 54 Zimbabwe 16

Czech Republic 52 El Salvador 15

Denmark 52 Cyprus 14

Finland 50 Ecuador 13

Argentina 11

Colombia 11

Ireland 11

Korea 10

Luxembourg 10

Source: IMF, International Financial Statisticsreserves for some considerable time, even allowing for continued

rapid market growth. Clearly therefore no immediate constraint on

potential supply exists. However, in assessing the question of

availability, it becomes necessary to examine the motivations which

have drawn central banks into the lending market, and to assess the

likelihood that either those which are already active will commit

more of their reserves in the future, or alternatively that others

currently on the sidelines will follow their example.

The Return Fundamentally, the central banks have been attracted into gold

on Gold lending for one reason – the prospect of earning a return on assets

Lending and which would not otherwise generate any income. From a study of

the Change the fluctuating pattern of gold lending rates over the past ten years

in the it is apparent that at least a portion of central bank lending has been

Perceived available to the market even at quite low rates of around 0.5% per

Risk/Reward annum. More recently, however, the growing requirement for

Ratio liquidity to fund a steadily increasing volume of producer hedge

transactions has necessitated a gradual increase in the returns

available for gold lending, in order to attract the required volume of

supply. Since mid-1995 rates have tended to fluctuate around a

mean of 1.5%. This has produced the desired response from the

official sector, especially as the yield on competing financial

instruments has been falling in response to a general decline in

inflation within OECD countries. Thus the bullion banks have been

instrumental not only in encouraging a greater level of participation

from the existing pool of official lenders, in response to improving

rates of return, but have also offered a more challenging prospect to

those central banks which continue to operate a policy of inactive

ownership. The trend gradually emerging throughout 1997 strongly

reinforces the view that the number of lenders from the official

sector (currently estimated to be in excess of 60) is still expanding

and can continue to do so in the future.

Central banks are commonly regarded as risk-averse institutions,

and the process of overcoming the innate caution which governs

many of their actions has been a lengthy one, starting in the early

1980s. Some institutions still follow the preferred route of channelling

their gold lending through another official intermediary such as the

Bank of England as a means of ensuring greater security. The majority,

however, have developed direct relationships with the bullion banks

which in turn redistribute the liquidity supplied into the various

sectors which require funding. These banks are not only well capi-

talised, with high credit ratings, but are also supported by a depth

of experience in gold market dealings, and a diverse portfolio of finan-

cial activities. They are unlikely therefore to be unable to meet their

obligations to repay gold borrowed as a result of unforeseen shocks

from within either the gold market itself or the wider financial system.

31There has been one significant default with direct consequences for

certain central bank gold lenders, that of Drexel Burnham Lambert

in 1990, but this event, although entailing some initial losses of gold,

resulted in only a short-term contraction in official lendings. Lending

subsequently resumed in force, following the absorption of appro-

priate lessons, namely a closer attention to the credit rating of the

potential bullion bank counterparties and the greater exposure

incurred with loans as opposed to swaps.

Whilst the sudden collapse of Barings in 1995 may also have

provided central banks with an unpleasant reminder that commercial

banks are potentially vulnerable to the consequences of risks under-

taken on their behalf, authorised or otherwise, the scale of operations

in gold lending by the official sector, although not insignificant at

2

approximately US$ 35 billion , represents a small proportion of the

total spectrum of financial transactions in which central banks

regularly engage. Central banks are increasingly becoming more pro-

active in their approach to reserve asset management and have

educated themselves more thoroughly regarding the pitfalls and

opportunities in the market. As a consequence, many have decided

that lending a part of their gold holdings can be justified on a

risk/reward basis.

Legal The potential conflict between the central banks’ newly found

Political and appetite for increasing the returns on assets and at the same time

Institutional fulfilling their primary role of providing monetary stability and

Constraints financial order, finds expression in a number of possible

impediments to gold lending: legal, political and internal

considerations may each limit a central bank’s freedom.

Some official institutions are still prevented by law or by their arti-

cles of association from lending gold reserves, as is the case, for

example, in respect of the USA, holding 8,140 tonnes and the IMF, a

non-central bank official institution, but with assets of 3,217 tonnes.

Legal requirements, nevertheless, are not immutable and whilst

changes are not always easy to bring about, as instanced by the

continued opposition encountered by the IMF in seeking support for

proposals to sell a relatively small proportion of its gold to help in

financing debt write-offs and by Germany in attempting to revalue its

gold reserves prior to entry into EMU, there are indications that

central banks are beginning to re-examine more critically previously

long-established practices and policies, and to institute processes of

change where appropriate. In this regard there could be no more

influential example than that of the Swiss National Bank, which

during the past year has set out far reaching proposals which, if

approved through a referendum, will lead to a programme of sales to

2

This guideline figure has been calculated using the following assumptions:

1) Central bank lending estimated mean 3,650 tonnes

2) Gold price reference point $300/oz – $9,645/tonne

32provide an endowment for its Solidarity Fund. In the meantime it

has taken the necessary steps enabling it to commence gold lending

operations in November 1997.

Such actions as described above have understandably created an

atmosphere of anticipation in the market, especially as some recent

initiatives are emanating from the larger holders of gold reserves,

opening up the possibility that other countries will similarly review

existing policy. Nevertheless, public sensitivity to the management

of national reserves is still a factor to be recognised and may prove to

carry a greater weighting in some countries than others, especially

where severe monetary dislocation has occurred within living

memory.

Other political considerations may limit a central bank’s freedom to

lend gold. Gold loans may entail holding the metal beyond a country’s

territorial jurisdiction and, where there is reason to fear the possi-

bility of sanctions by other governments, physically relocating the

gold to London may be perceived as posing an unacceptable risk. A

number of countries, therefore, some holding quite sizeable reserves,

still prefer to retain direct control of their gold and accordingly are

prepared to forego the potential earning capability of the asset.

Finally, internal considerations will play a major role in deter-

mining a central bank’s attitude to lending, and in particular the

chosen mode of participation, in order to limit risk whilst still retaining

acceptable returns. Ideally, official institutions would prefer to deal

with only the most creditworthy of the commercial banks, but as the

market continues to expand in volume, the question of raising dealing

limits with counterparties in order to accommodate new business

could potentially pose constraints. Certainly there would appear to be

an opportunity for banks with high credit ratings, but which have

not yet engaged in gold lending activities, to enter the field so as to

widen the scope for the placing of official business.

In other areas central banks have traditionally sought to limit risks

– for example gold swaps might be considered preferable to loans,

since in the event of a default the potential deficiency to the central

bank would be related to the value of its forward purchase obliga-

tions, measured against the market price, rather than the total under-

lying value of the gold, as in the case of a loan. Equally many central

banks have restricted their loan or swap horizons to within either a

three or six months period, despite the bullion banks’ obvious

appetites for longer lending in order to more closely match producer

hedge business maturities. Nonetheless, some central banks in seeking

the higher yield which is generally available for maturities beyond

one year, have reassured themselves that such a policy is justified

despite the additional risk incurred. The proportion of longer-term

lending secured from the official sector, although it still remains small

in relation to the overall total, is therefore continuing to increase.

33You can also read