WE TRANSFORM VISIONS INTO PLASTIC SOLUTIONS - Investors Presentation Autumn 2021 - Polytec Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

WE TRANSFORM VISIONS Autumn 2021 INTO PLASTIC SOLUTIONS Investors Presentation

POLYTEC AT A GLANCE

Technology-independent

developer and manufacturer of

high-quality plastic solutions

Automotive and

~3,600 522 MIO 35 YEARS

EMPLOYEES SALES REVENUES OF EXPERIENCE non-automotive industry

2

LOCATIONS

PRESENT ON 4 CONTINENTS CHINA

17 X IN EUROPE

1 X IN ASIA

1 X IN AMERICA

1 X IN AFRICA

USA

SOUTH AFRICA

3

STRATEGY

1 2 3

Strengthening of the Development of new A focus on customer

market position in Europe technologies and applications benefits

4

TECHNOLOGICAL DIVERSITY

INJECTION MOULDING COMPOSITES SMALL SERIES TECHNOLOGIES PRE- & POST-PROCESSING

2k injection moulding Production of glass fibre SMC Class-A paint coating Just-in-Sequence-Delivery

Multi-component injection Production of carbon fibre SMC PUR RRIM / RRIM Lightweight Tool making

moulding SMC/LFT/GMT compression moulding PUR rigid / semi-rigid Mechanical engineering

Assembly injection moulding UD-Tape application PUR-processing (moulding parts) (multi-component dosing system)

WIT (water injection technology) Hybrid compression moulding PUR spraying Testing & Validation

GIT (gas injection technology) (LWRT-LFT) PUR casting Trimming & Cutting

PIT (projectile injection technology) Wet pressing PUR foaming (milling, laser, water jet)

In-Mould-Decoration In-Mould-Coating Blow moulding Joining & Welding

Injection-Moulding-Compounding In-Mould-Painting Processing of metal & premium steel (hot gas, ultra-sonic,…)

High-gloss technology

Up to 4000 tons clamping force Up to 4300 tons clamping force Up to 630 tons clamping force

5

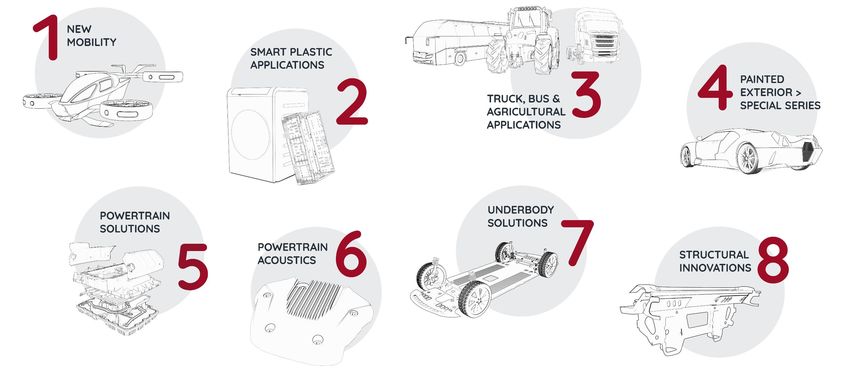

POLYTEC PRODUCT LINES 6

INVESTING IN NEW PLANTS

▪ Tianjin (PRC) ▪ Telford (UK) ▪ East London (RZA)

SOP HY2 2021

7

FINANCIALS 2020 FY

FINANCIAL FIGURES

SALES REVENUES, EARNINGS, EQUITY

676,4 636,4 627,1 522,0

2017 2018 2019 2020

Turnover

9

SALES REVENUES BY CUSTOMERS 2017–2020 FY 10

SALES REVENUES SPLIT 2020 FY

etc.

Passenger Cars &

Light Commercial Cars

Commercial Cars

14.4% Smart Plastics &

Industrial Applications

22.6%

63.0% 2020 FY Exterior

13% Powertrain

14% Interior

40%

3% Structure

6%

et 24% Industrial Applications

c. Tooling

11FINANCIALS H1 2021

KEY FIGURES H1 2021 (VS H1 2020)

▪ Sales revenues EUR 291.7 million (H1 2020: EUR 242.3 million)

▪ EBITDA EUR 24.2 million (H1 2020: EUR 10.7 million)

▪ EBITDA margin 8.3% (H1 2020: 4.4%)

▪ EBIT EUR 10.1 million (H1 2020: EUR –7.0 million)

▪ EBIT margin 3.5% (H1 2020: –2.9%)

▪ Earnings after tax EUR 6.8 million (H1 2020: EUR –8.9 million)

▪ Earnings per share EUR 0.30 (H1 2020: EUR –0.42)

▪ Equity ratio 44.2% (H1 2020: 40.0%)

▪ Net debt EUR 121.2 million (H1 2020: EUR 153.4 million)

▪ Employees (FTE incl. leasing personnel) as at 30.06.2021 3,708 (30.06.2020: 3,870)

13OUTLOOK 2021 FINANCIAL YEAR The POLYTEC GROUP management continues to anticipate consolidated sales revenues of about EUR 575 million for the 2021 financial year. On the basis of a reassessment of current risks, EBIT is likely to amount to around EUR 30 million. Nonetheless, the realisation of this outlook is prone to a number of significant uncertainties. In particular, the drastic increases in raw material prices, which already had a considerable impact upon the result for the second quarter, will again constitute a considerable risk to profitability in the second half-year. In this connection, the current negotiations with customers regarding compensation for the price rises are of vital importance to the realisation of the outlook forecasts. A continuation of the short-term reductions in automotive call-offs beyond the summer months, shortages of raw materials – in particular electronic chips – as well as the repeated disruptions to production, would also have an additional impact upon results. In addition, the possible negative effects of the corona epidemic on consolidated sales revenues and the operative result further complicate the outlook. 14

SALES REVENUES, EBIT MARGIN – QUARTERLY

in EUR m

147,8 143,9

142,5

137,1

13,4%

93,2

4,5%

2,4%

0,6%

-10,4%

Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

15EBITDA, EBITDA MARGIN – QUARTERLY

in EUR m

19,4%

27,7

9,3%

7,2% 13,8 7,3%

9,9 10,4

-1,0%

-1,0

Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

16EARNINGS FIGURES – QUARTERLY

EARNINGS AFTER TAX in EUR m

EPS in EUR

19,8

EARNINGS PER SHARE

4,8

0,79

2,1

0,21 0,09

Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

-1,5 -0,48 -0,08

-10,3

17NET DEBT, GEARING – QUARTERLY

Net debt in EUR m

153,4 157,1

116,8 121,2

105,8

0,64 0,66

0,43 0,46 0,47

Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

18EQUITY, EQUITY RATIO – QUARTERLY

256,9 in EUR m

254,9

247,5

238,3

237,1 43,6% 44,2%

42,6%

40,5%

40,0%

Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

19ESG – SUSTAINABILITY

STRATEGIC ENVIRONMENTAL OBJECTIVES

RESOURCE CONSERVATION

▪ Reduced consumption of natural resources through focus on lightweight construction

and functional integration

▪ Increased use of recycled materials

ENHANCED ENERGY EFFICIENCY

▪ Use of modern and environmentally friendly equipment

▪ Installation of highly efficient heat recovery systems

▪ Consistent use of sustainable LED lighting

REDUCED ENVIRONMENTAL EMISSIONS

▪ Increasing the share of energy from renewable sources

▪ Investment in photovoltaic systems

21POLYTEC ENERGY AND ENVIRONMENTAL TARGETS

Target definition Dimension Key indicator

Strategic objective: Resource protection

Reduction of raw material consumption through an improvement in the reject ratio 15% by 2023 kg/kg

Increase in the recycling share through project realisation minimum 2 projects p.a. number completed pro.

Strategic objective: Increased energy efficiency

Reduction in energy consumption (base load) 20% by 2025 kWh/EUR k

Reduction in electricity consumption due to compressed air leakages 50% by 2025 kWh/EUR k

Equipping of all plants with energy monitoring realisation by 2025 number of plants

Strategic objective: Environmental emission minimisation

Establishment of monitoring for carbon footprint (CFP) and reduction (Scope 1 and 2) 20% by 2025 %

Reduction in waste quantities through improvement of the reject ratio 15% by 2025 %

Increase in the share of recyclable waste through improved waste sorting 0.75%/year & 8% by 2025 %

Uniform hazardous material management realisation by 2022

Development of innovative products (e. g. lightweight design), which through their use minimum 2 projects p.a. number completed pro.

reduce environmental emissions

22CO2 NEUTRAL PLANT IN EBENSEE (AUSTRIA) 23

PLANT EBENSEE

▪ Ground area: 82,000 m2

▪ Buildings: 34,000 m2

▪ Personnel: 187 (152 + 35 leasing p.)

▪ Automotive products, e. g. for trucks

▪ Logistic boxes (food retail)

24RECYCLING OF IFCO LOGISTIC BOXES IN THE PLANT

▪ The recycling facility was agreed in the course of

the IFCO supplementary order

▪ Returned damaged boxes are granulated

▪ Ground polypropylene plastic is temporarily

stored in silos

▪ On demand, the PP is conveyed to the moulding

machines and processed again into new boxes

+ Conveyor belt with metal detector

+ Cutting mill for wet material

+ Friction separator

+ Separator containers

+ Drainage screw

+ Mechanical drier

+ Material transport into the silos after dedusting

+ Mechanical process water treatment

+ Extended water treatment (possible expansion project)

25POLYTEC PHOTOVOLTAIC PROJECTS

▪ Electricity from renewable energy sources will make a

significant contribution to CO2-neutral production at POLYTEC.

Plant Wolmirstedt (DE)

▪ POLYTEC already covers a large part of its electricity needs

with green electricity (100% in AT).

▪ Furthermore, suitable roof surfaces of the POLYTEC sites will

be equipped with photovoltaic systems from 2021.

Plant Lohne (DE) – Symbol photo

Plant Hörsching (AT)

26ESG RATINGS BY GAIA & VIGEO ERIS

Benchmark

27APPENDIX

EARNING PER SHARE, DIVIDENDS 2006 – 2020

EPS in €

DPS in €

DIVIDEND POLICY

▪ based on profitability

▪ strategic growth perspectives

▪ capital requirements of the POLYTEC GROUP

29SHARHOLDER STRUCTURE – RESEARCH COVERAGE

1,50%

29,04% Price

Institute (as at 16.08.2021) Rating

target

BAADER-Helvea Research, Munich BUY EUR 16.0

ERSTE Group Research, Vienna BUY EUR 14.8

M.M.Warburg Research, Hamburg BUY EUR 16.0

69,46%

Raiffeisen Research, Vienna BUY EUR 13.5

Average price target EUR 15.1

Free float Huemer Group Treasury Shares

30POLYTEC SOLUTION FORCE

Bundling of competences from the

entire POLYTEC GROUP:

▪ Technology and manufacturing expertise

of the various locations

▪ High degree of value added

▪ Innovative strength from product and

material development

▪ Profound market understanding

31MAIN APPROACHES OF THE POLYTEC SOLUTION FORCE PERFORMANCE IN PLASTICS POLYTEC is a lightweight construction specialist. FUNCTIONAL INTEGRATION POLYTEC develops multifunctional products. ECONOMIC AND COST EFFICIENCY POLYTEC optimises the product and its manufacturing process. USER ORIENTATION POLYTEC thinks of the product users‘ needs. 32

AUTOMOTIVE MARKET H1 2021

NEW PASSENGER CAR REGISTRATIONS IN EUROPE

JAN-AUG 2021 (COMPARED TO THE SAME PERIOD OF THE PREVIOUS YEAR)

EU: 6 807 706 (+683 651) +11.2%

▪ In August 2021, car registrations across the European Union

decreased by 19.1% to reach 622,993 units.

▪ August performance of EU’s largest markets:

France -15.0%, UK -22.0%, Germany -23.0%, Italy -27.3%, and

Spain -28.9%

▪ „Big 5“ YTD

1. GE: 1 820 589 +2.5%

2. FR: 1 126 543 +12.8%

3. UK: 1 101 302 +20.3%

4. IT: 1 060 182 +30.9%

5. ES: 588 314 +12.1%

Source: ACEA

34REGISTRATIONS of NEW CARS in international markets 35

REGISTRATIONS of NEW CARS in Europe (EU, EFTA & UK) 36

REGISTRATIONS of NEW CARS in Europe (EU, EFTA & UK) BY DRIVE TECHNOLGY 37

REGISTRATIONS of NEW COMMERCIAL VEHICLES in Europe (EU, EFTA & UK) 38

MAKE YOUR NOTES 39

CONTACT:

POLYTEC Holding AG

Mr. Paul Rettenbacher – Investor Relations Manager

E-Mail: paul.rettenbacher@polytec-group.com

https://www.polytec-group.com/investor-relations/newsYou can also read