WESTERN UNION FINANCIAL SERVICES (CANADA), INC. AGENT ANTI-MONEY LAUNDERING COMPLIANCE MANUAL

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

WESTERN UNION FINANCIAL SERVICES (CANADA), INC. AGENT ANTI-MONEY LAUNDERING COMPLIANCE MANUAL May 2012 The WESTERN UNION name, logo and related trademarks and service marks, owned by Western Union Holdings, Inc., are registered and/or used in the U.S. and many foreign countries. This material is confidential and is proprietary to Western Union and is not to be reproduced, disclosed, or used except in accordance with program license or other written authorization of Western Union. Any use, copying, manipulation, or reproduction of Western Union trademarks, logos, or material created by Western Union, its subsidiaries, affiliates or its business units, in whole or in part in any medium for any purpose whatsoever, is strictly prohibited without the prior written permission of Western Union.

Table of Contents Overview of Policies, Procedures and Requirements .............................................................. 4 Compliance Officer Responsibilities ....................................................................................... 5 AML Compliance Policies and Procedures .............................................................................. 7 AML Compliance Policy ............................................................................................................... 7 Suspicious Transaction Referral/Report Policy ........................................................................... 8 Employee Training Policy .......................................................................................................... 10 Identification and Record Keeping Requirements .................................................................... 11 Compliance Monitoring Policy .................................................................................................. 13 Splitting Transaction Policy ....................................................................................................... 14 Government Sanctions and Interdiction Policy ........................................................................ 15 AML Compliance Training .................................................................................................... 16 Introduction .............................................................................................................................. 16 Overview of Money Laundering and Terrorist Financing ......................................................... 17 What Is Money Laundering? ..................................................................................................... 17 The Risks of Money Laundering ................................................................................................ 17 The Basic Stages of Money Laundering: ................................................................................... 18 What Is Terrorist Financing? ..................................................................................................... 19 Penalties for Money Laundering ............................................................................................... 19 Tipping Off................................................................................................................................. 19 Key Points on Money Laundering and Terrorist Financing ....................................................... 20 Proceeds of Crime (Money Laundering) and Terrorist Financing Act ...................................... 20 General Requirements: ............................................................................................................. 21 How These Requirements Apply to You: .................................................................................. 21 Key Points - Proceeds of Crime (Money Laundering) and Terrorist Financing Act .................. 22 Record Keeping Requirements ................................................................................................. 22 Record Keeping Requirements for Money Transfers ........................................................ 22 Record Keeping Tips ............................................................................................................ 24 Acceptable Forms of Identification ...................................................................................... 24 Key Points – Recording Keeping Requirements ........................................................................ 25 Reporting Requirements ........................................................................................................... 26 Reporting Requirements ...................................................................................................... 26 Suspicious Transaction Referrals/Reports ............................................................................ 26 What Is Suspicious Activity? ..................................................................................................... 27 Red Flags............................................................................................................................. 27 Structuring: ................................................................................................................. 29 Completing a Suspicious Transaction Referral/Report ............................................................. 30 Helpful Tips about the Information for Suspicious Transaction Referrals/Reports ................. 30 © 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 2

Submitting and Keeping Suspicious Transaction Referrals/Reports ........................................ 31 Monitoring Responsibilities ...................................................................................................... 31 Monitoring Hints ....................................................................................................................... 32 Key Points – Reporting Requirements ...................................................................................... 33 Fraud Prevention ................................................................................................................. 33 © 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 3

Overview of Policies, Procedures and Requirements

This Agent Anti-Money Laundering Compliance Manual ("Manual") is issued on behalf of

Western Union Financial Services (Canada), Inc. (“Western Union”). Western Union is

mentioned throughout this manual. The Manual describes the anti-money laundering

compliance requirements applicable to Western Union in Canada. The Manual also includes a

quick reference card with a summary of the identification, record keeping and reporting

requirements. The quick reference card is included and intended to be a guide that is kept in a

safe, convenient place for easy reference.

The Manual is organized into four sections that you need to be aware of as an Agent. The

sections are as follows:

Responsibilities:

o Each Agent location must designate a person responsible for overseeing the

implementation and adherence of the policies, procedures and requirements set forth

in this Manual. This person is referred to as the Compliance Officer.

Policies and Procedures:

o Policies are general statements of broad intent and direction, whereas procedures are

more detailed instructions for day-to-day activities. Policies and procedures may be

updated from time to time as the result of changes in laws, regulations, business

operations, or Western Union policy.

Training:

o The Compliance Officer must ensure that all employees who handle transactions are

trained on anti-money laundering as well as policies and procedures included in this

Manual. The training section has been designed to help you provide the required

training to your employees.

Forms:

o This Manual includes report referral forms, a monitoring log and a training log. These

can be removed and copied by the Agent as needed. If additional copies of these forms

are required by the Agent, they can be obtained by contacting your local representative

or by calling Western Union at 1-800-235-0000

This Manual outlines the requirements of an Agent. Your Agent location may choose to

implement additional internal requirements in keeping with the best practices of your business,

so long as such requirements are not inconsistent with those set forth in this Manual.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 4

Compliance Officer Responsibilities

The Compliance Officer is the person responsible for compliance in your Agent location. This

person is responsible for overseeing and monitoring adherence by your location with the

policies, procedures and requirements set forth in this Manual.

The duties and responsibilities of the Compliance Officer are outlined below and may be in

addition to the other duties and responsibilities of the appointed individual.

The Compliance Officer will work in collaboration with Western Union and has the following

specific responsibilities:

Training

1. Ensures that new employees complete anti-money laundering compliance training.

2. Ensures that all employees receive, at minimum, annual refresher training on anti-money

laundering compliance, including report referrals and identification requirements.

3. Ensures that all employees review compliance training and educational materials provided

periodically by Western Union.

4. Provides supplemental training to employees as needed to address compliance deficiencies

with the policies and procedures that are noted through monitoring, regulatory

examinations or compliance reviews.

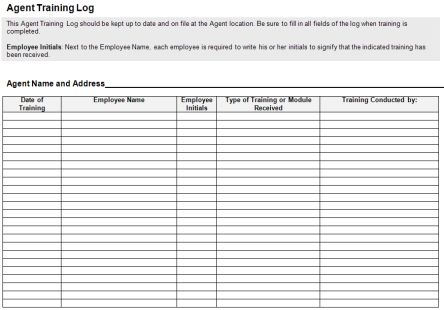

5. Ensures that initial and ongoing training efforts are documented for each employee. A

Training Log has been provided and is available in this Manual as an example of training

documentation.

Monitoring

1. Ensures that employees follow policies and procedures at all times when engaging in

Western Union transactions.

2. Periodically reviews daily reports, the Compliance Monitoring Report, forms and/or printed

receipts to ensure proper completion and accurate entry of consumer information as well as

proper identification acceptance by Agent employees.

3. Ensures that employees identify and refer/report suspicious activity to Western

Union/FINTRAC using the Suspicious Transaction Referral/Report process for both

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 5

completed and attempted transactions. (Note: If you are an MSB or other reporting entity,

you must complete a Suspicious Transaction Report and file electronically with FINTRAC.

4. Reviews all Suspicious Transaction Referrals/Reports for accuracy, completeness and timely

submission.

5. Develops and implements appropriate corrective action for any deficiencies identified

during the monitoring process.

6. Educates staff on observable behaviours that could warrant Suspicious Transaction

Referrals/Reports.

Record Keeping

1. Ensures that the Manual is maintained in an accessible location and that any updates

received from Western Union are incorporated into the Manual.

2. Maintains the AML-related monitoring and training records.

3. Ensures that all required reports/referrals and supporting documents are retained for 5

years.

4. Ensures all completed transaction forms and receipts are kept for a minimum of 6 months

and then destroyed unless the forms were involved in a STR report.

Other

1. Serves as the primary contact with Western Union Compliance Department and with

Canadian governmental officials and staff during regulatory audits or compliance

examinations (if applicable).

2. Serves as the primary contact for Agent Compliance Reviews, responds to compliance

review findings, and implements any required corrective actions.

3. Coordinates the process for identifying suspicious activity, completing Suspicious

Transaction Referrals/Reports for completed or attempted suspicious transactions and

maintaining supporting documentation for 5 years.

4. Ensures that every employee who conducts money transfer transactions has a separate and

unique user ID and password and that password are kept confidential.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 6

AML Compliance Policies and Procedures

AML Compliance Policy

Agents and their employees must comply with anti-money laundering policies

and procedures, which may be updated from time to time.

All employees conducting transactions must know and comply with the policies, procedures

and requirements set forth in this Manual, as updated from time to time.

All employees conducting transactions must have and use their own separate user ID and

password for the money transfer system. Employees may not share user IDs or passwords

or conduct transactions using another employee’s user ID.

Records of completed employee training and compliance monitoring must be documented

and retained for a minimum of 5 years.

Suspicious activity identified during interactions with a consumer must be referred to

Western Union or reported directly to FINTRAC for MSBs and other reporting entities as

described herein. Western Union will file reports with FINTRAC based on such referrals as it

deems necessary and appropriate. Agents are required to keep copies of referrals/reports

submitted and any supporting documentation including proof of submission for 5 years.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 7

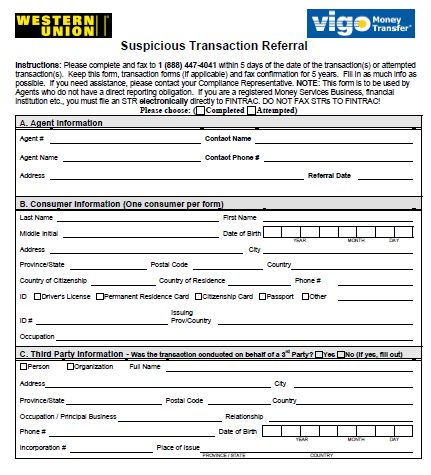

Suspicious Transaction Referral/Report Policy

Agents and their employees will take reasonable steps to identify suspicious activity and

submit Suspicious Transaction Referrals/Reports to Western Union/FINTRAC as appropriate.

The Agent should attempt to get as much information as possible about the consumer(s);

however, the Agent shall not inform a consumer that a Suspicious Transaction

Referral/Report is being completed. If the Agent thinks that asking for additional information

will tip off a consumer about a report, do not ask for further information. This requirement

applies to completed as well as attempted transactions that are suspicious.

SUSPICIOUS TRANSACTION REPORT REFERRAL PROCEDURE:

A Suspicious Transaction Referral/ Report must be submitted to Western Union/FINTRAC for

any completed or attempted transaction for which there is a reasonable basis to suspect

that the transaction or attempted transaction is related to a money laundering or terrorist

financing offence. A copy of the Suspicious Transaction Referral form is located in the Forms

section of this Manual. (Registered MSBs and other reporting entities would be required to

file an STR directly with FINTRAC. AGENTS THAT ARE NOT REPORTING ENTITIES (ie grocery

stores, convenience stores, any location that does not offer a regulated product of their

own) MUST NOT FAX OR SUBMIT INFORMATION DIRECTLY TO FINTRAC. THIS

INFORMATION MUST COME TO WESTERN UNION FOR REVIEW AND SUBMISSION.

Suspicious activity includes possible attempts to launder money, structure transactions to

avoid reporting or record keeping requirements, and/or terrorist financing activities.

Employees must take reasonable measures to obtain as much information as possible for

completion of the Suspicious Transaction Referral/Report, keeping in mind that you do not

want to tip off the consumer that a referral is being completed. If you think that the

consumer will be tipped off to your suspicions, do not ask additional questions.

Under no circumstances may an employee inform a consumer that a Suspicious Transaction

Referral/Report is being submitted.

Suspicious Transaction Referrals/Reports are to be reviewed for completeness and accuracy

prior to submission to Western Union. The referral form may be amended from time to time

by Western Union as it deems necessary to meet its regulatory and legal obligations.

The Compliance Officer will fax the completed Suspicious Transaction Referral form to

Western Union at 1-888-447-4041 as soon as possible and within 5 days of detecting the

suspicious activity. Registered MSBs and other reporting entities should file the report

directly with FINTRAC electronically within 30 days of identifying the suspicious activity.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 8

The Compliance Officer will serve as the contact person should Western Union have any

questions about Suspicious Transaction Referrals/Reports.

Copies of Suspicious Transaction Referrals/Reports and evidence of submission to Western

Union/FINTRAC, along with all supporting information, must be retained for a period of 5

years.

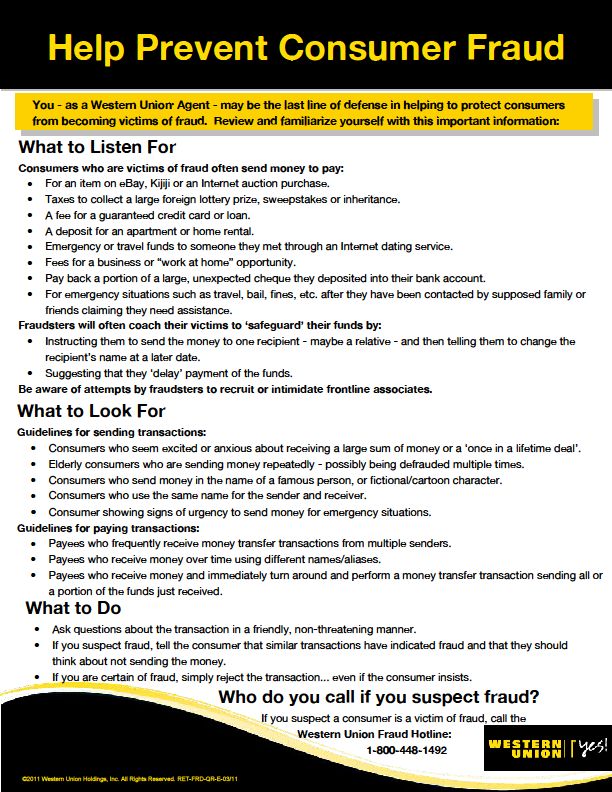

Examples of Suspicious Activity:

The consumer displays unusual behaviour or provides potentially improper documentation. For

example, if the consumer:

is nervous, rushed or aggressive

is reluctant to show identification

provides identification that seems unusual, false or altered

presents different identification or address each time they complete a money transfer

spells their name differently or uses a different name each time they complete a money transfer

Transactions that do not make economic sense:

A sender regularly sends money home once a month and suddenly begins sending larger

amounts every week to other people

A sender comes in more than once during the same day or over several days and sends amounts

just under the identification threshold to different people who are in the same geographic area

Large and regular transactions that cannot be identified as legitimate, especially if sent to

countries associated with the production or processing of narcotics or other illegal drugs

A consumer who receives a number of small transactions on the same day, or within several

days, and subsequently sends one or more transactions of about the same total amount to

another person

Refusing Transactions:

If you are uncomfortable about a transaction, ask for help from a more experienced associate, your

manager or Compliance Officer. You have the right to refuse a transaction. Whether a transaction is

completed or attempted, it is always best to report your concerns/suspicions using the Suspicious

Transaction Referral/Report)

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 9Employee Training Policy

All Agent employees who conduct transactions must receive Anti-Money

Laundering training.

EMPLOYEE TRAINING PROCEDURE:

Western Union will provide AML training materials for Agents and their employees on:

o Money laundering, terrorist financing and laws and regulations designed to combat

them, including applicable sections of the PCMLTFA and its implementing regulations.

o Suspicious activity identification and the Suspicious Transaction Referral process

o Identification and record keeping requirements

o Western Union policies and procedures

Initial AML compliance training for current employees must occur promptly upon your becoming an

Agent and prior to employees conducting transactions.

New employees must receive AML compliance training prior to conducting money transfer

transactions.

At least annually, all employees who conduct money transfer transactions should receive AML

refresher compliance training.

Ongoing additional AML compliance training should occur as new information or requirements

become available or if compliance issues are identified. In addition, Western Union may periodically

provide educational materials, such as newsletters and bulletins that discuss compliance

requirements or anti-money laundering issues that should be communicated to staff at Agent

locations and documented.

Evidence of completed AML compliance initial and refresher training must be documented, and such

documentation must be retained by the Agent location for 5 years. A training log is included in the

Forms section of this Manual for documenting training.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 10Identification and Record Keeping Requirements

Agents and their employees must obtain and record all consumer information

required by identification and record keeping policies and procedures. All such

information obtained by the Agent will be retained by Agent. This includes all

forms and receipts, referrals/reports and any supporting documentation.

All such information obtained by Agent will be retained by Agent. Unless otherwise specified, money

transfer transaction forms (“To Send Money,” “To Receive Money” and “Quick Collect”) and receipts are

to be retained for a period of 6 months and then destroyed. However, if a money transfer transaction

form relates to a report/referral, the form should be retained for 5 years along with the referral/report

itself.

ACCEPTABLE FORMS OF IDENTIFICATION:

When you are required to verify a consumer’s identity by reviewing an identification document, AML

policy requires that the identification document:

Is government issued

Includes a photo of the consumer

Is current (not expired)

Examples of acceptable forms of identification include a provincial driver’s license, a Canadian or foreign

passport, a Permanent Resident Card, or a Quebec Issued Health Card. (Note: Social Insurance Number

and Health Cards from Ontario, Manitoba and PEI are specifically NOT accepted.) On the following page

is a list of the information required at various thresholds:

DATA PROTECTION/CUSTOMER PRIVACY

In addition to meeting your recordkeeping requirement, you should protect your customer data.

Protecting customer data includes:

Shredding forms or any documents containing customer and/or transaction information

after the required retention period ends.

Maintaining customer records in a secure location. This can include forms, Suspicious

Transaction referrals and monitoring information that includes customer data.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 11IDENTIFICATION AND RECORD KEEPING REQUIREMENTS:

Employees conducting Money Transfer transactions must obtain and record all information required by

identification and record keeping policies and procedures. Employees must ensure that all required

information is contained on the appropriate money transfer transaction form (“To Send Money,” “To

Receive Money” or “Quick Collect”), receipts and/or entered into the Money Transfer system.

It is important to make sure the information contained in the ID documents matches that provided by

the consumer. If information does not match, a second piece of ID should be requested. If not available

or does not provide confirmation, the transaction should be refused.

MONEY TRANSFER

Identification and Record Keeping Requirements

Dollar Threshold Requirement

Less than $1,000 send Send transactions: Obtain and record the name,

address and telephone number of the Sender.

and

Receive transactions: Obtain and record the name,

below $300 receive address and telephone number of the Receiver. In

addition, either review the Receiver’s Photo ID or obtain

the answer to the test question.

$1,000 or more for SEND transactions or Record the Sender’s or Receiver’s name and address,

over $300 for RECEIVE transactions telephone number, date of birth, country of birth and

occupation.

Verify the identity of the Sender or Receiver by

reviewing current, government-issued, photo

identification (ID) – such as a driver’s license or passport.

Write down the ID type, number, place of issuance and

expiry date (if applicable)

In addition to the $1,000 requirements above, the Sender

$7,500 or more in single SEND must complete an interview with a Western Union

transaction Customer Service Operator:

The interview process is very important as it protects the

consumer against possible fraudulent transactions and

also collects information required.

Transactions should never be “split” to avoid the

interview process.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 12Compliance Monitoring Policy

The Compliance Officer will periodically monitor compliance with the policies,

procedures and requirements set forth in this Manual.

COMPLIANCE MONITORING PROCEDURE:

The Compliance Officer must monitor and document a review of transaction activity

conducted at his or her location to verify that:

1. Where appropriate, Suspicious Transaction Referrals/Reports were completed

correctly and submitted to Western Union/FINTRAC within the required timeframe,

and copies along with any supporting documentation were retained at the Agent

location.

2. Information and identification requirements were met and identification policies

were followed.

3. Where applicable, Send and Receive Forms and receipts were completed correctly

and information on the forms matched the printed money transfer receipts.

4. All record keeping requirements have been complied with.

5. Existing employees received Western Union refresher training and new employees

successfully completed Western Union compliance training.

6. All employees have and are properly using separate user IDs and passwords for

conducting Western Union money transfer transactions.

7. Monitoring daily activity reports in conjunction with reconciliation of money

transfers and identifying and reporting suspicious activity on the Suspicious

Transaction Referral/Report when applicable. Initialing or signing the reports as

evidence of review.

If monitoring discloses potential compliance issues, the Compliance Officer will identify the

cause of the potential issue and determine the appropriate corrective measures, if any, such

as additional training or clarification of procedures.

Evidence of monitoring Must be documented and retained for at least 5 years. You may use

the Monitoring Log attached to this manual to record your monitoring activities.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 13Splitting Transaction Policy

Agents and their employees must follow procedures for handling suspicious activity as

outlined in this Manual if it is determined that a consumer is splitting a transaction for

illegitimate reasons.

SPLITTING TRANSACTION PROCEDURE:

This splitting policy provides guidance regarding the handling of two or more transactions that, whether

intentionally or unintentionally, avoid record keeping requirement or identification thresholds.

The term “split” is defined as:

A transaction that is broken apart for the purpose of decreasing the amount of each single transaction.

The activity of splitting or separating one transaction into two or more transactions can be done for

legitimate reasons or it can be done for illegitimate reasons.

Example of splitting transactions:

Joe, the sender, wishes to send $3,000 to a criminal associate in Europe; however Joe is advised he

needs to provide photo identification and address information in order for the transaction to be

processed. Subsequently, Joe sends three separate transactions for $999 each, and therefore avoids

showing any identification documents.

If a sender chooses to split a transaction so that is below the identification threshold, or the sender

comes in regularly to send funds just below the identification threshold, you may prompt the System

using the “Consumer ID” button in the Translink system or by selecting the “Show Compliance” link in

WUPOS and collect the consumer’s identification details. This should always be used if the sum of the

consumers transactions in a single visit total $1000 or more.

As an Agent, you can witness the consumer’s actions and are in a position to make a decision as to

whether the splitting is for a legitimate reason or not. Remember, you are able to ask for ID at any

amount and if it is felt that the purpose for splitting is for illegitimate reasons an STR should be filed.

.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 14Government Sanctions and Interdiction Policy

Various governments and governmental organizations prohibit businesses, including

money transfer service providers, from engaging in transactions with listed

individuals, entities or countries. Western Union screen transactions against

applicable lists of individuals and entities provided by such governments and

organizations. Western Union also screens transactions against lists of individuals

and entities with whom it has determined not to do business for a variety of reasons.

GOVERNMENT SANCTIONS AND INTERDICTION PROCEDURE:

The Western Union systems screen money transfer transactions against applicable lists of

people and entities with whom we are prohibited from doing business, as well as lists of people

and entities with whom we have determined not to business for various reasons.

If a match is identified, Western Union must research the transaction in more detail. In many

cases, consumers are required to provide additional identification or information about the

transaction. The required research may delay the release of the transaction for payment.

If you or a consumer has questions about this topic, please contact Western Union.

LAW ENFORCEMENT REQUESTS:

From time to time Western Union receives requests from Law Enforcement Agencies. If an Agent’s

employees receive such a request, they must forward it to their Compliance Officer or directly to the

Western Union Compliance Department.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 15AML Compliance Training Training is a critical component of an Anti-Money Laundering (AML) Compliance program. The following questions and answers will help you understand the training requirements. Who should take AML training? Every employee who is involved in money transfer transactions. Before selling any services, each employee should read the Anti-Money Laundering Training Modules included in this folder and correctly answer all of the AML Compliance Quiz questions. The Compliance Officer should use the answer key located at the back of the Training section for scoring each employee’s quiz. How often should employees be trained? As a part of ongoing training, employees should be retrained at least annually. How do I document employee training? We recommend that the Compliance Officer have each employee sign and date their Quiz and file them for future reference. The Agent Training Log should be used to document all employee Compliance training. This includes both the Quiz and any ongoing training, such as reading compliance articles in newsletters and other publications. How long do I have to keep employees training records? Training materials must be kept with your Compliance records for at least 5 years. Introduction This training is an important part of the Anti-Money Laundering (AML) Compliance Program. We provide the training to assist you in adhering to the requirements of our Compliance Program and to help you and your employees better understand how to protect your business operations from being used for illicit purposes. In addition to periodic training, the Compliance Program requires your following our policies and procedures and designating a Compliance Officer who is responsible for overseeing AML compliance at your Agent location. Training Modules: This packet contains four separate training lessons to assist you in training employees. The format allows training to be conducted in a group or individually. © 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 16

Each lesson presents a different aspect of Anti-Money Laundering Compliance: Lesson One: Overview of Money Laundering and Terrorist Financing Lesson Two: Proceeds of Crime (Money Laundering) and Terrorist Financing Act Lesson Three: Record Keeping Requirements Lesson Four: Reporting Requirements Agent Training Log: This log will help you track and record your training. The log should be kept current and on file at your location. Be sure each employee initials the training log after completing the training. Overview of Money Laundering and Terrorist Financing What Is Money Laundering? Money laundering is the process of disguising the source of money that was obtained illegally in order to make it appear legitimate. Many types of criminal activity, such as drug trafficking, generate money for the criminal and his organization. In order to use that money without being detected, the criminal must disguise its origins and make it appear legitimate. Money laundering is the process by which the criminal does this. If successful, the criminal is able to use the criminal proceeds freely. How big a problem is money laundering? The International Monetary Fund estimates that C$900 billion to C$2.25 trillion of illegal money is circulating worldwide each year. So, you can see why Western Union devote significant resources to comply with the anti-money laundering regulations everywhere they do business. The Risks of Money Laundering It hurts our communities and our country. It damages our business reputation. It allows criminals and terrorists to use our financial system for illegal purposes. © 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 17

The Basic Stages of Money Laundering:

Placement Placement is the attempt to place illegally obtained funds in the

financial system without attracting attention.

A send transaction could be the placement of cash with an Agent

(e.g. Money from the sale of stolen goods/drug money). This is the

Example of initial stage and is very hard to establish. Western Union

Placement recommends that if you are suspicious of any activity at your

location, you should report it. Details of reporting Suspicious Activity

are covered later in this Manual.

Layering is the second stage of the money laundering process where

funds are moved around to hide them from their source. This

Layering “movement” often involves a complex series of transactions in order

to create confusion and complicate the paper trail.

A consumer might go into several different Agent Locations and

Example of complete the same or similar transactions in the hope of not being

Layering detected. If you notice this behaviour, you should bring it to the

attention of your Compliance Officer and Western Union by

completing a Suspicious Transaction Referral/Report.

Integration is the ultimate goal of the money laundering process.

Once the illegal funds are placed into the financial system and are

Integration insulated through the layering stage, they are used to buy goods and

services that appear as “legitimate” wealth.

Example of

One or more consumers send several transactions to one receiver.

Integration This receiver collects the transactions and subsequently sends

another transaction or tries to invest in a legitimate product.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 18What Is Terrorist Financing? Over the last several years, combating terrorist financing has become an important part of most anti- money laundering efforts. Terrorists, like most criminals, try to conceal their activities (including their financing) to avoid detection. Terrorist financing is a little different than traditional money laundering because terrorists often finance their activities with money that was obtained legally. Terrorists know if they use illegally obtained money, they are more likely to be caught before they can use their money to fund their terrorist activity. What terrorists try to hide is the connection between themselves, their financing, and their terrorist activity. Let’s look at some examples to demonstrate the difference between money laundering and terrorist financing. Example of Money Laundering: Joe, by selling illegal drugs, generated a large sum of money. Now he must find a way to use the funds without attracting attention to his criminal activity. Joe attempts to hide the unlawful funds by transferring small amounts of money to various individuals who deposit it in bank accounts that Joe controls. Example of Terrorist Financing: A foreign organization on a government watch list needs to provide funds to its operatives for a terrorist act in Canada. The funders understand that sending large amounts of money, even legal money, will arouse suspicion. Therefore, they divide a large sum of into smaller amounts, which they transfer to associates claiming to be foreign college students living in Canada. These individuals posing as students then get the money to the operatives. Penalties for Money Laundering Ignoring “red flags” and not completing a Suspicious Transaction Report (STR) that indicates that funds could involve illegal activities can potentially expose a person or business to criminal penalties under a legal doctrine known as “willful blindness.” It is a crime to engage in a financial transaction knowing that it involves the proceeds of drug trafficking, tax evasion, terrorist activities or other illegal activities. Tipping Off It is a crime to advise an individual that you have filed a Suspicious Transaction Report based on their transaction activity or attempted transaction activity or other factors that make the activity suspicious. © 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 19

Key Points on Money Laundering and Terrorist Financing

Money Laundering:

Begins with funds gained from crime

Attempts to wash dirty money so that it cannot be easily traced

Moves money through the financial system so it can later be used for

legitimate purposes

Terrorist Financing:

Often uses money acquired through legal means

Attempts to hide the connection between the funders of terrorism, their

money, and terrorist activity

Proceeds of Crime (Money Laundering) and Terrorist Financing Act

Both money laundering and the financing of terrorist activities are criminal offences under Canada’s

Criminal Code. However, the primary law governing the anti-money laundering and terrorist financing

obligations of financial institutions in Canada is the Proceeds of Crime (Money Laundering) and Terrorist

Financing Act (the “PCMLTFA”).

The PCMLTFA was originally enacted in 1991 to deal with money laundering by providing law

enforcement with a “paper trail” of certain financial transactions, such as those involving large amounts

of cash. In 2001, it was amended to deal with terrorist financing activities as well. In 2007, it was

expanded to bring Canada more fully in line with international anti-money laundering and terrorist

financing guidelines.

The PCMLTFA has three key objectives:

To detect and deter money laundering and the financing of terrorist activities and to facilitate

investigations and prosecution of the related offences;

To respond to the threat posed by organized crime by providing law enforcement officials with the

information they need to deprive criminals of the proceeds of their criminal activities;

To help fulfill Canada’s international commitments to fight multinational crime.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 20General Requirements:

In general, the PCMLTFA requires financial institutions, including “money services businesses,” to:

Establish and maintain an anti-money laundering compliance program,

File certain reports with the government

Maintain records of certain transactions, and

Ascertain client identity in certain situations.

The primary reports required by the PCMLTFA are (i) reports of suspicious transactions and attempted

suspicious transactions, (ii) reports of large cash transactions, and (iii) reports of large electronic funds

transfers.

Compliance with these requirements is overseen by the Financial Transactions and Reports Analysis

Centre (FINTRAC), which operates as part of the Ministry of Finance. In addition, FINTRAC collects and

analyzes these reports and refers cases of possible money laundering and terrorist financing to law

enforcement. Law enforcement uses information provided by FINTRAC to investigate and prosecute

those who may have engaged in illegal activity.

How These Requirements Apply to You:

As a money services business, Western Union is required to have an anti-money laundering compliance

program and to comply with the record keeping, reporting and client identification requirements of the

PCMLTFA. Agents must provide products and services in a manner that enables Western Union to meet

its legal obligations. Specifically, each Agent location is required to follow

operational and compliance policies and procedures which include, among other

things:

Obtaining and recording certain information when a consumer conducts

a money transfer. In many cases, compliance with these requirements

involves recording complete and accurate information according to

prompts on the transaction screen for money transfers.

Verifying the identity of consumers who are subject to the money transfer record keeping

requirements listed on the ID summary card provided to you.

Submitting a Suspicious Transaction Referral/Report to Western Union/FINTRAC for completed

or attempted transactions of any type that you believe are suspicious. (Note: If you are a

registered Money Services Business or other reporting entity you would be required to file a

Suspicious Transaction Report directly to FINTRAC.)

These requirements are discussed in more detail in the following training modules.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 21Key Points - Proceeds of Crime (Money Laundering) and

Terrorist Financing Act

The PCMLTFA sets record keeping, reporting and customer

identification requirements on money services businesses such

as Western Union.

Agents must follow Western Union’s policies and procedures so

that we all comply with requirements of the PCMLFTA.

Agents are required to obtain and record certain information

and review identification documents for money transfer

transactions at or above certain dollar amounts as indicated on

the ID Summary card.

Suspicious Transactions (Completed or Attempted) must be

referred to Western Union using the Suspicious Transaction

Referral. If you are a registered Money Services Business or

other reporting entity you would be required to file a Suspicious

Transaction Report directly to FINTRAC.

Record Keeping Requirements

Record Keeping Requirements for Money Transfers

Money Transfer Sends of less than $1000 and Receives under $300.

When you conduct a Money Transfer SEND transaction of less than $1000 or a Receive under $300, you

need to obtain and record the following information from the sender or receiver:

Name and address

Telephone number

In addition, for receive transactions you must review the Receiver’s Photo ID or obtain the

answer to the test question.

Money Transfer Sends of $1,000 or More and Receives over $300

When you conduct a Money Transfer SEND transaction of $1,000 or more, or RECEIVE over $300, you

need to obtain and record certain information and confirm the consumer’s identity by reviewing a

current, government-issued photo identification (ID) - such as a driver’s license. Specifically, you need

to see the ID and record the following information from the sender or receiver:

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 22 Name and address

Telephone number

Date of birth

Country of birth

Occupation

The type of identification, its number, place of issuance and expiration date (if there is one)

In most cases, you can meet these requirements by making sure that you obtain all of the information

called for on the To Send or To Receive forms or by the money transfer system.

Money Transfers of $7,500 or More

When you conduct a Money Transfer SEND transaction of $7,500 or more, in addition to obtaining the

information mentioned above, the consumer will be interviewed by a Customer Service Operator during

which additional information will be obtained and updated into the Western Union system.

Summary

The following table summarizes the record keeping requirements for money transfers.

MONEY TRANSFER

Identification and Recordkeeping Requirements

Dollar Threshold Requirement

Less than $1,000 send Send transactions: Obtain and record the name, address and telephone

number of the Sender.

and

Receive transactions: Obtain and record the name, address and telephone

below $300 receive number of the Receiver. In addition, either review the Receiver’s Photo ID

or obtain the answer to the test question.

$1,000 or more for SEND Record the Sender’s or Receiver’s name and address, telephone number,

transactions or over date of birth, country of birth and occupation.

$300 for RECEIVE

transactions Verify the identity of the Sender or Receiver by reviewing current,

government-issued, photo identification (ID) – such as a driver’s license or

passport.

Write down the ID type, number, place of issuance and expiry date (if

applicable)

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 23In addition to the $1,000 requirements above, the Sender must complete an

$7,500 or more in single interview with a Western Union Customer Service Operator:

SEND transaction The interview process is very important as it protects the consumer against

possible fraudulent transactions and also collects Third Party Determination

information required.

Transactions should never be “split” to avoid the interview process.

Record Keeping Tips

When obtaining information about a consumer’s occupation, make sure you get a specific occupation.

Answers such as “business,” “self employed,” or “manual labor” are not acceptable. You should ask for

more details, such as “owner of convenience store” or “self employed plumber.”

When obtaining a consumer’s address, do not accept a P.O. Box. Instead, you should obtain street

address information, including lot and concession (if applicable).

Acceptable Forms of Identification

As described above, you must review an acceptable form of identification when making money transfer

or money order transactions over certain dollar amounts. An acceptable form of identification is a:

Driver’s license

Passport

Quebec-Issued Health Insurance Card (only if offered by the consumer)

Other current Photo ID issued by provincial, territorial or the federal government

The identification document must be an original – a copy is not acceptable – and must contain a

photograph of the individual. In addition, it must be currently valid. For example, an expired driver’s

license would not be acceptable. A social insurance card is specifically NOT acceptable as an

identification document.

When you look at an ID, you should make sure the information is consistent with the information

provided by the Sender or Receiver (i.e., name, address, age). You should also compare the photograph

on the ID with the person in front of you. If the ID does not match or appears to be a forgery, you

should not accept it. If you don’t feel comfortable with the ID provided, ask for a second piece of ID to

confirm the consumer’s identity.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 24Key Points – Recording Keeping Requirements

The record keeping requirements for Money Transfers include obtaining

and recording information about consumers sending $1,000 or more and

receiving over $300.

Western Union will conduct an interview for money transfer transactions

that are $7,500 or more.

Acceptable IDs must be original, currently valid government issued

documents with a photograph, such as a driver’s license or passport.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 25Reporting Requirements

Reporting Requirements

One of the ways the PCMLTFA combats money laundering and terrorist financing is to

require financial institutions and other entities to take reasonable measures to detect and

report suspicious transactions and attempted transactions. Another is to require certain

entities to report receiving $10,000 or more in cash or for sending $10,000 or more out of

Canada or for receiving $10,000 or more in Canada from another country. In order for

Western Union to meet these requirements, Agents need to enter accurate information

into their money transfer system, and also to monitor their transactions and either refer

certain transactions to Western Union for reporting or in the case of a registered MSB or

other reporting entity, to file electronically to FINTRAC directly.

In this lesson, you will learn what kind of transactions must be referred, what forms to use,

and how you can effectively monitor daily transactions.

Suspicious Transaction Referrals/Reports

Structured transactions or

transactions that could involve

money laundering, terrorist

financing or other illegal activity

involving the use of or movement

of funds are considered suspicious

activity. Under the PCMLTFA,

certain entities including Western

Union must report suspicious

activity to FINTRAC. To help us

meet this obligation, Agents that

only offer Western Union services are required to submit Suspicious Transaction Referrals

for any completed or attempted transaction that the Agent considers suspicious. If you are

a registered Money Services Business or other reporting entity you would be required to file

a Suspicious Transaction Report directly to FINTRAC.

The Suspicious Transaction Referral is a tool for identifying and reporting

transactions or attempted transactions that could be related to money laundering

or terrorist financing. You need to be specific when providing your narrative about

the transaction - What did you see? What did you hear? What made you

suspicious of the transaction? You need to refer any transactions or attempted

transactions you consider suspicious to Western Union by:

Completing a Suspicious Transaction Referral for any transaction or pattern of

transactions – completed or attempted – that is suspicious.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 26Fax the completed form – to 1-888-447-4041 within 5 days from the date you saw the suspicious

activity. DO NOT FAX ANY FORMS DIRECTLY TO FINTRAC. If you are a registered Money Service

Business or other reporting entity submit your report following your established process.

You may be wondering how you know if a transaction or attempted transaction is suspicious. Let’s

examine what might be suspicious activity.

What Is Suspicious Activity?

Spotting suspicious activity is the first phase of the referral process. In general, a transaction or

attempted transaction is suspicious when you have reason to believe that it is being used to launder

money or finance terrorism, avoid reporting or record keeping requirements or be part of other illegal

activity.

We understand that you may not be certain if a consumer is making a transaction for a criminal purpose.

You are only required to identify transactions that are “suspicious,” that is, activity that could involve

illegal or criminal activity. To help you identify these transactions, there are a number of key signals –

commonly referred to as “red flags” – that may indicate suspicious activity. Red flags generally consist

of certain behaviour or characteristics about a consumer and the transaction that could cause you to be

concerned and suspicious.

Financial Agents

Through websites or emails criminals try to recruit account holders in your country in order to misuse

them and their accounts for so called financial agent activity. The recruited Financial Agents are asked

to receive a credit transfer on their bank account from an unknown person. Then they are instructed by

mail, telephone or SMS to withdraw the cash and send it via Western Union to another person in a

foreign country they do not personally know. As a reward, the Financial Agent is allowed to keep a

certain percentage of the transferred money. The funds the Financial Agent moves usually originate

from cybercrime activities (hacked bank accounts, etc.). The Financial Agent commits the offence of

money laundering. You as an Agent are obliged to do your part to prevent the misuse of tour system by

Financial Agents. Every suspicion that leads in this direction must be reported to Western Union by

completing a Suspicious Transaction Referral, or if you are a registered Money Services Business or other

reporting entity you would be required to file a Suspicious Transaction Report directly to FINTRAC.)

Red Flags

When one or more factors signal that a transaction is unusual and possibly suspicious, it is called a “red

flag.” Observing a red flag should trigger some questions, such as:

Is the amount of the transaction unusually large for the typical consumer?

Does the consumer make the same or similar transactions more frequently than normal?

Does the type of transaction seem unusual for the consumer?

Other examples of red flags include:

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 27 Consumer uses a fake ID, or multiple IDs on different occasions (name, address, or

identification number may be different)

Two or more consumers use the same or similar ID (photo or name may be different).

Consumer changes a transaction after learning that he or she must show ID.

Consumer conducts transactions so that they fall just below amounts that require reporting or

record keeping.

Two or more consumers, trying to evade report or record keeping requirements, seem to be

working together to break one transaction into two or more transactions.

You know or have reason to suspect that the transaction involves funds from illegal activity.

The transaction does not appear to have a lawful purpose.

Be aware of consumers who:

Are hurried, nervous or evasive

Are aggressive or uncooperative

Are reluctant to provide ID or information

Appear at store opening, closing or peak times

Try to impress you with substantial future business or wealth

Offer you a tip, bribe or other inappropriate gift

Provide inconsistent information when asked questions

Come in several times in one day to conduct transactions that are just below the amounts that

require recording

Are not concerned about price or are too familiar with the reporting rules

Be alert for transactions that:

Are just below the threshold amount for reporting (such as a $9,900 cash transaction), or record

keeping/identification ($950-$999 for money transfers)

Are changed frequently by the consumer at the desk

Are conducted by familiar consumers who have a sudden change in pattern

Have inconsistent or non-existent relationship between the sender and the receiver or payee

Are conducted by multiple individuals who appear to know each other outside the premises, but

ignore each other while they are inside the business

Keep in mind, a consumer with any of the red flag behaviours should not automatically be considered a

money launderer or terrorist. However, one or more red flags should put you on alert to look for other

clues that something could be wrong with the transaction. Also keep in mind that by submitting a

Suspicious Transaction Referral/Report, you are not accusing the consumer of being involved in criminal

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 28activity. You are only reporting activity that appears suspicious. Western Union will decide whether the

activity warrants the filing of a Suspicious Transaction Report for those Agents submitting referrals.

If you are suspicious about a transaction, ask about the intent of the transaction and familiarity with the

other party. If there are clear signs that the transaction is connected with illegal activity, refuse or do

not complete the transaction. Whether the transaction is completed or refused, file a Suspicious

Transaction Referral/Report with the information available to you.

Structuring:

In order to avoid record keeping, reporting or ID requirements, a money launderer may break up a large

amount of money into a number of smaller transactions. For example, in order to avoid having to show

an ID, a consumer may send four $900 money transfers rather than a single money transfer for $3,600.

This is commonly referred to as “structuring.” This should be reported to Western Union/FINTRAC using

the Suspicious Transaction Referral/Report.

The following are examples of possible structuring:

A consumer wants to make a money transfer for $2,500. When he learns that he must provide

information and show an ID, he asks to send three separate money transfers to the same

receiver, each for less than $1,000.

Three people come into your location and you see them split money between them. Each then

makes a money transfer of less than $1,000 to the same receiver.

Basic Rules:

Before looking at how to complete a Suspicious Transaction Referral/Report, let’s review some basic

rules.

Never tell a consumer that you are going to submit a Suspicious

Rule #1 Transaction Referral/Report to Western Union/FINTRAC. In addition,

be careful not to tell – or “tip off” – the consumer that you are going

to do so.

If you strongly suspect that a transaction involves illegal activity, do

Rule #2 not complete the transaction. However, you may complete the

transaction if you believe you or your employee would be in danger

by refusing to do so.

A Suspicious Transaction Referral/Report should be submitted even if

Rule #3 you don’t complete a suspicious transaction – for example, if you

refuse to complete a transaction because the consumer has

presented an obviously forged ID.

© 2008-2010 Western Union Holdings, Inc. All Rights Reserved. Confidential and Proprietary 29You can also read