12 ways to spend that financial windfall wisely - MoneySENSE

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE STR AITS

TIMES

12 ways to spend that financial

windfall wisely

! PUBLISHED JAN 21, 2018, 5:00 AM SGT

Instead of blowing that year-end bonus or profit from a collective sale,

use it to clear debts or start an investment plan, advise experts

"

Lorna Tan Invest Editor/Senior Correspondent (mailto:lornatan@sph.com.sg)

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 1 of 19

With the year ahead of us, it is an opportune time to review our financial health, ensure that we

are on track to achieve our goals and make necessary adjustments.

Buoyed by a booming economy, many are looking forward to a round of hefty salary increments

and year-end bonuses.

Some of you might be on the receiving end of a handsome windfall, thanks to the unexpected

collective sale fever that gripped Singapore last year. There were about 27 collective sales with a

total transactional value of more than $8 billion, up from $1 billion in 2016.

Financial experts say it is prudent to resist the tantalising temptation to splurge it all. Before you

rush out to make a down payment on a new car or buy that two-carat diamond ring, think about

how you can use this extra cash for even greater long-term gains and financial security.

"Take the opportunity to do a complete portfolio review and this should include your assets,

investments, your loans and insurance policies. Apportion your bonus based on your needs for

loan repayment, insurance, investment, and cash holdings which include funds for emergencies,"

says Mr Brandon Lam, Singapore head of financial planning group at DBS Bank.

Review your priorities such as much-needed home renovations, family holidays or festivities. Also

remember to top your Supplementary Retirement Scheme (SRS) account for tax savings, Mr Lam

adds.

The Sunday Times highlights 12 financial tips for 2018.

1. Pay off debts with high interest costs Financial experts are unanimous when it comes to which

debts almost invariably incur the highest interest costs. Focus on clearing off personal debts that

are costly to maintain, such as credit cards, which charge as high as 24 per cent a year.

The trouble with making just the minimum payment on your credit card bill, instead of paying in

full each month, is that interest is charged on the principal sum owed. So if you have a $5,000

debt against your card for a year, you could end up paying $1,200 in interest alone.

Bear in mind the so-called Credit Limit Management Measure has kicked in since Jan 1. It is aimed

at borrowers with unsecured debt, such as personal loans or credit card debt, that exceeds six

times their monthly income. Banks will not be allowed to grant any increase in credit limits or any

new unsecured credit facilities to such a person if these cause his total credit limit to exceed 12

times his monthly income. Affected borrowers can continue to use their existing unsecured credit

facilities.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 2 of 19

Try a different approach to monthly budgeting: Pay yourself first. Saving

just 10 per cent of your net pay is a good start to accumulating wealth

over time. This will force you to become more frugal and careful in your

spending as the other bills must still be paid. In fact, if you are fortunate

to get a pay rise, putting away the increment each month will go a long way

towards helping you achieve medium-or long-term goals.

#

It is a good idea to review your portfolio once a year and consider

rebalancing your plan whenever you go through major life events, such as

getting married or having a baby.

#

To check your outstanding balances and credit limits with all the banks, you can buy a credit

bureau report.

For those saddled with heavy debts, check out assistance schemes and repayment plans, such as

the Debt Consolidation Plan (DCP). Under a DCP, multiple debts are consolidated into a single

account so borrowers need to pay only a fixed monthly amount to one financial institution,

making it easier for them to clear their debts.

Do not bother about investing until you have lowered your debt to a manageable level.

2. Kick-start a savings plan A windfall presents a good opportunity to kick-start a savings plan.

Many people prioritise their monthly spending in this order: The biggest item is likely to be the

mortgage or rental, followed by car loan instalments, utility bills and food. They then scrape the

bottom of the barrel to cover the monthly minimum on their credit card bills.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 3 of 19

Learn about investment products and strategies and start to invest – even in small amounts – regularly,

advises DBS’ Mr Brandon Lam.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 4 of 19

Try a different approach to monthly budgeting: Pay yourself first. Saving just 10 per cent of your

net pay is a good start to accumulating wealth over time. This will force you to become more

frugal and careful in your spending as the other bills must still be paid.

In fact, if you are fortunate to get a pay rise, putting away the increment each month will go a long

way towards helping you achieve medium-or long-term goals.

Mr Vasu Menon, senior investment strategist at OCBC Bank, suggests setting some of your bonus

aside into a savings account or time deposit, as unexpected events could hurt the economy or the

industry you are working in, and this in turn could dampen your job prospects.

"The peace of mind that comes with knowing you have sufficient funds to tide you over should

you lose your job is priceless," he says.

And if you do not have an emergency fund that can cover at least six months of your monthly

expenses, your bonus can be used to start one. Aside from the risk of a job loss, the fund can also

help you to cover other unforeseen events such as unexpected medical expenses due to an illness

or temporary disability due to an accident, adds Mr Menon.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 5 of 19

Use your bonus to start an emergency fund that can cover at least six months of expenses, if you do

not have one yet, says OCBC’s Mr Vasu Menon.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 6 of 19

MoneySmart.sg editor Mark Cheng recommends opening more than one savings account to save

money more effectively to meet daily, short-term and long-term goals. "For long-term savings,

pick an account that offers better interest rates for you to store and grow your cash... An account

for short-term goals is something to consider as well," he says.

3. Earn more interest for 'loyalty' savings accounts In the past few years, several banks have

rolled out "loyalty" programmes for customers to earn higher interest rates and enjoy direct

monthly cashback capped at a certain amount, when they can fulfil some criteria like regular

banking transactions, card spend, investments, and/or salary crediting.

These include the Bank of China SmartSaver, DBS Multiplier account, OCBC 360 account, POSB

cashback bonus programme, and UOB One account.

4. Spend your bonus wisely One factor that comes into play is the life stage that you are in.

Naturally, a couple planning to get married or a middle-aged couple with children will look at

their bonuses differently from someone who is nearing retirement.

"The first may allocate more cash towards a grand wedding or honeymoon, or even set aside

money to make the down payment on their matrimonial home. The middle-aged couple may

have a longer-term plan in mind, and keep the money for their children's tertiary education. Some

may even use the money to settle their debts, like a mortgage, if they are working towards being

debt-free as soon as possible," says Mr Menon.

Those nearing retirement, on the other hand, may treat themselves to a holiday abroad, provided

they have been diligent in building their retirement nest egg.

If they are still planning for their retirement, then they should probably use the bonus to meet

this objective, like contributing to their SRS account which can yield attractive income tax

benefits, or investing the money into a less risky product that can yield decent returns, he adds.

5. Top up CPF accounts To maximise your nest egg or that of your loved ones, consider topping

up Central Provident Fund (CPF) accounts so as to leverage attractive interest rates and

compounding.

6. Kick-start an investment plan Financial experts advise wannabe investors to map out their

investment time horizon, determine a realistic timeframe versus liquidity needs and decide which

asset classes are the most appropriate.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 7 of 19

When constructing a portfolio, asset allocation and diversification is key, says HSBC’s Mr Cameron Senior.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 8 of 19

Once a holistic financial plan is in place, you will have a framework in which to make future

financial decisions, which include knowing how best to optimise your windfall.

To understand the power of compounding interest, use the simple "rule of 72" to calculate how

long a sum will take to double. If the investment return is, say, 10 per cent, then it would take

slightly longer than seven years for an initial investment of $10,000 to double to $20,000. The

number of years is calculated by dividing 72 by 10, that is, the rate of investment return.

Mr Lam's advice is to start by learning about investment products and strategies and begin to

invest - even in small amounts - regularly.

If you have sufficient risk appetite, you could adjust your portfolio to higher risk - more exposure

to risky assets - by overweighting your investment capital in shares versus in bonds or deposits.

But you should always make sure you can afford the losses in worst-case scenarios. Insufficient

loss tolerance can affect your morale and judgment so you should always stay within your

tolerance limits. "It is always encouraged to start with a regular savings plan. With a disciplined

approach to savings or investment, the commitment is fixed regularly and yet takes advantage

during market volatility through dollar cost averaging and achieving diversification," Mr Lam

says.

The POSB Invest-Saver is one such regular savings plan investing in an exchange-traded fund. It

is suitable for consumers who are thinking of investing for better returns but may not have a huge

capital, want to potentially grow their long-term savings for their children or their own retirement

funds and are looking to diversify their portfolio.

7. Review your investment portfolio When constructing a portfolio, asset allocation and

diversification is key, says Mr Cameron Senior, head of wealth and international at HSBC Bank

(Singapore). This is because it is very unlikely that a single asset class will deliver the highest

return all of the time. Therefore combining different asset classes in a portfolio can diversify the

risks and improve returns over the longer term.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 9 of 19When refinancing a loan, ensure the total amount saved from doing so exceeds the cost, such as pre-

payment penalties, says OCBC’s Ms Phang Lah Hwa.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 10 of 19"The start of a new year is always a great time to review your investment portfolio. Not only would

you have a sense of market sentiments given most governments and financial institutions would

be providing their outlook for the year... (but) you would also have a clearer view of key life

changes that will affect you in the year ahead," he says.

Furthermore, review and rebalance your plan as personal circumstances change. It is a good idea

to review your portfolio once a year and consider rebalancing your plan whenever you go through

major life events, such as getting married or having a baby.

Mr Senior suggests investing into multi-asset funds as these are typically structured to provide

sustainable returns and ride out market volatility given their exposure to different asset classes,

industries and geographic regions. Such funds are one of the more cost-effective ways for retail

investors to gain access to diversification benefits, he adds.

8. Assess insurance needs Have a thorough audit to assess your insurance plans and cover. If

both areas are lacking, you could consider using part of the windfall to pay for the cost of any

additional insurance coverage.

However, do ensure that any additional regular premiums are affordable and sustainable.

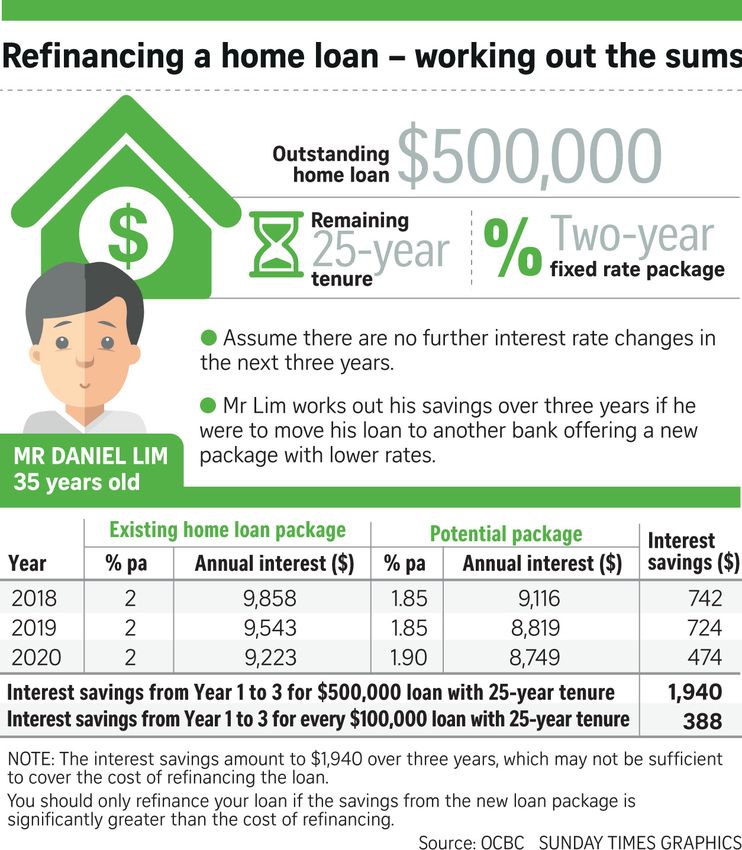

9. Refinance home loans if it results in savings The rising Singapore Interbank Offered Rate

(Sibor) has prompted major local banks to raise their home loan rates since November and it is

likely that Sibor will continue in an upward trajectory, says Mr Ee-Qiang Baey, head of mortgage

at MoneySmart.sg. At the same time, those who want to sign on to a new fixed deposit-linked

home loan rate are also faced with price hikes.

Refinancing - switching to a loan package that offers lower rates - is a great alternative for those

whose lock-in periods are ending. However, says Ms Phang Lah Hwa, head of consumer secured

lending at OCBC Bank, do ensure that the total amount saved from doing so exceeds the cost,

such as refinancing fees, legal fees and pre-payment penalties or if you are able to secure an

additional facility if required. She cautions that interest savings will diminish in a rising interest

rate environment.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 11 of 19More home owners tend to perform capital repayment to reduce their loan amount at the start of the year,

probably using their bonus or savings, says DBS’ Ms P’ing Lim.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 12 of 19"Most home loan packages come with lock-in periods of two or three years, and there are penalty

charges for redeeming the loan early. Hence, you should refinance your loan only if the savings

from the new loan package are significantly greater than the penalty charges," she says. "After the

lock-in period, you can choose to refinance with another bank or reprice the loan with the

existing bank, if the cost of switching and the new offering yield savings compared to the existing

package."

Ms P'ing Lim, DBS' head of deposits and secured lending, says other options to manage your

home loan commitments include right-sizing your loan amount via capital repayment or

lengthening your loan tenor.

She has observed that more home owners perform capital repayment to reduce their loan

amount in the beginning of the year, probably using their bonus or savings.

"This is a good practice to reduce your financial commitment especially if these are spare funds

where you are unable to get a yield higher than your loan rate. Generally, we advise home owners

to use cash instead of CPF funds since CPF pays at least 2.5 per cent and the funds could be used

for retirement or for a rainy day," she adds.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 13 of 19When picking a credit card, look for one with perks that match categories you typically spend in, says

MoneySmart.sg’s Mr Vinod Nair.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 14 of 19Regardless of interest rate trends, Ms Lim advises anyone with a housing loan to set aside funds

as a buffer against interest rate hikes or any unforeseen circumstances.

"Ideally, home owners should set aside some savings in cash, CPF funds or liquid assets that can

be used to pay their monthly instalments for the next two years. This gives them sufficient time to

restructure the loan or even sell the property should they run into any financial issues," she says.

10. Beware of credit traps when stepping up expenses When spending your windfall, ensure it

will not increase your overall monthly expenditure. Do not fall into the trap of making new

acquisitions that will be paid by instalments which, when added up, might exceed the original

windfall - this would eat into other savings.

The fastest way to build your savings is to maintain your regular expenditure when your income

rises and to save most of your annual bonuses.

11.Look out for credit cards that best suit your needs With the wide selection of cards and their

reward schemes, it is no wonder that some people are confused as to which is the best credit

card. The truth is that there is no perfect card, but there is usually one that matches a certain

lifestyle, says Mr Vinod Nair, chief executive at MoneySmart.sg.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 15 of 19With the right credit card, cardholders might actually generate more savings with their usual purchases, says

DBS’ Mr Anthony Seow.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 16 of 19He recommends that people first identify their spending categories. Banks have partnerships

with various retailers to bring shoppers the best savings with their purchases.

The next step would be to look at the card's rebate limit. A high cashback rate may appear

attractive at first glance, but it is usually capped at a certain point. Lastly, shoppers should find

out the minimum spending to qualify for rebates - they should ensure that they are comfortable

with spending that amount each month.

Mr Anthony Seow, DBS' head of cards and unsecured loans, says that with the right credit card,

cardholders might actually generate more savings with their usual purchases. "Customers can

enjoy card benefits such as discounts, cashback rewards or miles on all their purchases. The

POSB Everyday Card, for example, offers up to 6 per cent in cash rebates on purchases at

merchants such as SPC, Sheng Siong, Watsons, StarHub and SP Group.

"For those who love travelling, DBS Altitude Card offers the fastest way to earn air miles with up

to 3 miles per $1 on your purchases, and points never expire," he says.

It is also prudent to take a close look at the various card fees first. These include annual fees, late

fees and interest levied on outstanding debt, says a Maybank spokesman.

12. Live a little While bonuses may be a windfall, pay increases should be viewed as a buffer

against inflation, says OCBC's Mr Menon.

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 17 of 19For those who have addressed their immediate savings and retirement needs adequately, treat

yourself a little. After all, your bonus is something you have worked hard for and you deserve to

enjoy some of the fruits of your labour, he adds.

$ Refinancing a home loan – working out the sums

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 18 of 19% Terms & Conditions % Data Protection Policy

% Need help? Reach us here. % Advertise with us

SPH Digital News / Copyright © 2018 Singapore Press Holdings Ltd. Co. Regn. No. 198402868E. All rights reserved

http://www.straitstimes.com/business/invest/12-ways-to-spend-that-financial-windfall-wisely 14/2/18, 14?14

Page 19 of 19You can also read