2020/2021 Zambian Maize Outlook and Regional Analysis - IAPRI

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Indaba Agricultural Policy Research Institute

Zambian Maize Outlook

and Regional Analysis

2020/2021

By Brian P. Mulenga and Antony Chapoto Downloadable at http://www.iapri.org.zm

Executive Summary

COVID-19 pandemic shaped most of the conversations The 2020 Maize Outlook and Regional Analysis

around agricultural marketing and trade in 2020. summarizes the maize market during the 2020/2021

Luckily, the pandemic did not affect maize production market season in Zambia and presents insights

in Zambia as the first cases and restrictions to curb from the region; analyses government policy and

the spread of the pandemic were reported just stakeholder response and provides an initial forecast

before harvest. Thus, the major concerns regarding for next season’s harvest and recommendations for

the pandemic and the agriculturl sector had to do the upcoming maize season.

with harvesting and marketing. The rainfall during

Key findings: Analysing the Maize Market

the 2019/2020 agricultural season was good and

contributed significantly to improved production of 1. Similar to the previous season, the 2020/2021

maize and other field crops. Following two consectutive marketing season as at November 2020 was

seasons (2017/2018 and 2018/2019) with reduced characterised by high private sector participation.

maize harvest, Zambia recorded an above average Most private sector buyers entered the market as

maize harvest in the 2019/2020 agricultural season, early as April 2020 and were offering an average

with an estimated total production of 3,387,469 price of Zambia Kwacha (ZMW) 125-130 per 50kg

metric tons (MT) up from 2,004,389 MT in 2018/2019 bag by June in Eatsren, Copperbelt, Central and

production season (MoA and ZamStats, 2020). For the Southern province. An exceptionally high price was

past five agricultural production seasons (2014/2015 observed in Mpongwe district of the Copperbelt,

– 2018/2019), Zambia’s annual maize production has where traders were purchasing maize at ZMW 150

averaged about 2.7 million MT, X percent above local – 165/50 Kg bag between April/May. However,

national requirements. prices were relatively lower in Muchinga, Luapula

and parts of Northern province, hovering around

The 2019/2020 production represents a 69 percent

ZMW 100 -110/50Kg bag in, prompting farmers

increase from the previous season and 25.5 percent

to call for the FRA to announce its buying price in

from the five-year historical average. However, the

hopes of influencing traders to increase their buying

country’s opening stock at the beginning of the

price. .

2020/2021 marketing season was 79 percent from

the previous season. However, the above-average 2. The FRA announced its intention to procure

harvest during the 2019/2020 agrcultural season was 1 million metric tons (MT) of maize grain

enough to compensate for the low opening stock, thus partly as a contingency against COVID-19

the country remained food secure with 210,099MT and unpredictable weather pattern.

exportable surplus.

1

When the Food Reserve Agency (FRA) announced areas, thus eroding their purchasing power and

its purchase price of ZMW110/50 Kg bag, there access to food. This prompted government through

were concerns that prices will drop given that the the Ministry of Community Development and

FRA is a key player in the market. However, this was Social Services in partnership with UN agencies to

not the case as prices remained higher than ZMW implement emergency cash transfers to the affected

110/50 Kg bag in most parts of the country except households.

in Muchinga province where prices ranged between

7. Looking ahead, much of Zambia is likely to receive

ZMW 110- 115/50kg bag . The higher prices offered

normal to above-normal rainfall during the 2020/2021

by private sector contributed to FRA’s failure to meet

rainfall season, with a few places expected to

even half of the targeted 1 million MT of strategic

experience dry-spells between January and March.

grain reserves (SGR). Instead, by the end of the FRA’s

This forecast, combined with the early distribution

statutory buying season on 31 October, the Agency

of inputs under the Farmer Input Support Program

had only managed to procure about 350,000 MT –

(FISP), will most probably result in another above-

representing about 34 percent of the target.

normal maize harvest in 2021. However, COVID-19

3. Prices of maize and mealie meal started to drop still presents a risk mainly through disrupting labor

between March and May 2020 and this was driven supply and agricultural input supply. Another risk

mostly by the boost in domestic supply following is the migratory locusts, which were reported in

the above-average harvest. As at end of November the country in September 2020. The country has

2020, maize grain prices were averaging ZMW so far sprayed about 20,000 hectares of land

120 -130/50Kg bag in most parts of the country. against the locusts, but more remains to be done.

However prices were much higher in shang;ombo

and Kasumbalesa districts averaging ZMW 18- Recommendations

185/50Kg bag. Breakfast mealie meal prices were

Maize market development in Zambia continues to

averaging ZMW130/25 Kg bagBoth maize grain and

develop slowly because of continued inconsistent

mealie meal prices are lower compared to previous

and sometimes ad hoc maize marketing policy. The

season.

participation of FRA in the market continues to be

4. Despite the country producing a major surplus in expanded and as a results over burdening the National

2020, the government maintained the export ban Treasury. Private sector in Zambia has demonstrated

on maize and mealie meal until the FRA meets its that it has the capacity to effectively provide market

targeted 1 million MT. This ban has been in effect and associated sirvices to farmers particularly in

since May 2019 and continues to be in place. After accessible areas. Hence, the government should

protracted discussion with Zambia Farmers Union, provide the needed space and regulations for private

the government in July 2020 allowed exports of sector to sustainably investment in the maize sub-

maize and mealie meal only from early maize that sector. Purchasing an abnormally high strategic grain

was produced under an agreement with commercial reserve only discourages private sector-led agricultural

farmers. The early maize was exported under the marketing and trade. Another major concern has to do

government-to-government agreement to DRC with the imposition of export bans. Zambia has the

5. The export ban on maize grain and maize meal potential to become a reliable maize grain and maize

has not deterred informal trade with neighbouring meal supplier in the region but the stop and go approach

countries including DRC, Malawi, and Tanzania. on trade policy is squandering this opportunity. To help

Informal trade is taking place and continued to thrive bring about confidence in the maize sub-sector, reliable

throughout the season. Informal trade was driven by market information is key. Hence, there is an need to

price differentials with neighboring countries where expedite the operationalization of Zambia Agriculture

maize and mealie meal prices continue to be more Information System (ZAIS) that will help provide reliable

favorable than domestic prices. the stocks and prices information to guide informed

national grain marketing decisions.

6. Despite the above-average output at the national

level, there were localized deficits in some parts The production of early maize by commercial farmers

of the country, owing to droughts and fall army should continue to be supported because this can

worms in some parts of the Southern and Western enhance Zambia’s export position. Early maize

provinces, and floods in parts of the northern region. produced by commercial farmers is normally expensive

The Disaster Management and Mitigation Unit maize due to supplemental irrigation. Hence, it is very

(DMMU) and partners provided relief food directly important for the government to continue providing

to the most vulnerable households, but at much incentives and clear market signals for early maize

lower scale than in 2019. Further, the COVID-19 production by commercial farmers. Across the board

pandemic resulted in loss of business and wage export restrictions and/or ban discourages early maize

income for many people both in the rural and urban production by these farmers.

2

List of Acronyms

DMMU Disaster Management and Mitigation Unit

FAO Food and Agriculture Organization

FEWS NET Famine Early Warning Systems Network

FISP Farmer Input Support Programme

FRA Food Reserve Agency

GTAZ Grain Traders Association of Zambia

IAPRI Indaba Agricultural Policy Research Institute

MAZ Millers Association of Zambia

MoA Ministry of Agriculture

MT Metric Tonnes

SA RSMO Southern Africa Regional Supply and Market Outlook

SGR Strategic Grain Reserve

USD United States Dollar

WFP World Food Programme

ZAIS Zambia Agriculture Information System

ZAMACE Zambia Agrciculture Commodity Exchange

ZamStats Zambia Statistics Agency

ZMW Zambian Kwacha

ZNFU Zambia National Farmers Union

3

Introduction

Following two consectutive seasons (2017/2018 and Most private sector buyers who entered the market ear-

2018/2019) with reduced maize harvest, Zambia record- ly were offering a buying price ranging from ZMW120

ed an above-average maize harvest in the 2019/2020 – 130 per 50kg bag in most provinces, with a few areas

agricultural season, with an estimated total production like Mpongwe offering significantly higher prices aver-

of 3,387,469 metric tons (MT) up from 2,004,389 MT aging ZMW 160/50 Kg bag between May and June.

in 2018/2019 production season (MoA andZamStats, With the announcement of the Food Reserve Agency

2020). For the past five agricultural production seasons, (FRA) buying price of ZMW 110/ 50 Kg bag, similar to

from 2014/2015 to 2018/2019, Zambia’s annual maize previous season price, private sector buyers adjusted

production has averaged about 2.7 million MT based their price downwards but still outbidding the Agency.

on crop forecast estimates by the Ministry of Agriculture This situation made it difficult for the FRA to meet its

(MoA) and Zambia Statistical Agenecy. The 2019/2020 announced buying target of 1 million MT for 2020/2021

production represents a 69 percent increase from the marketing season.

previous season and 25.5 percentabove the five-year

historical average. The increase in production in the Although maize prices showed signs of retreating from

2019/2020 season was largely attributed to the fa- the 2019/2020 levels, as a result of increased produc-

vorable rainfall received in most parts of the country. tion, prices remained relatively high in the context of an

However, the 69 percent expected increase in maize above-average production (69 percent higher than the

production in 2019/2020 agricultural season from the previous season and 25.5 percent higher than the his-

previous season demonstrates the problems of heavily torical five-year average). This is mainly attributed to the

relying on rain-fed agricultural system. fact that the country opened the 2020/2021 marketing

season with very low carryover stock, thus moderating

Typically, with an above-average harvest, prices are total supply on the market. The receding maize grain

expected to be relatively low, however, the country prices have been transmitted to mealie meal prices,

opened the 2020/2021 marketing year with a low open- significantly reducing average nominal as well as real

ing stock of about 179,000 MT compared to 475,000 prices relative to the previous season.

MT the previous year, and way below the five-year av-

erage of about 780,000 MT. The low opening stock In terms of governement policy, the most significant

prompted the government to continue with the maize policy pronouncement was to do with export ban and

grain and mealie meal export ban that was imposed substantial increase in targeted SGR. Governemnt’s de-

back in March 019. cision to sustain export ban on maize and mealie meal

Besides Zambia, other countries in the region, experi- and FRA’s intentions to procure 1 million MT of SGR left

enced favorable weather leading to increased produc- private sector players on edge and highly cautious in re-

tion relative to the previous season. South Africa, the gards to purchasing maize grain. Historically, FRA par-

largest surplus country in the region, recorded a 21 per- ticipartion of this magnitude tended to destroy private

cent increase in production and a surplus of about 5.6 setor maize market as the Agency ended up offload-

million MT, while Malawi recorded a 25 percent increase ing highly subsidized maize to selected millers in the

in production, with a surplus of 583,000 MT. Mozam- year. With regards to exports, there was an exception.

bique’s production saw an uptick of about 9 percent, The government, through the tripartite agreement with

with a marginal surplus of 65,000 MT, whereas Tanzania commercial farmers (who produced early maize) and

to the east recorded a 3 percent production increase the DRC governement signed and executed a mem-

with a surplus of 750,000 MT. For Zimbabwe, despite orandum of understanding (MoU) for Zambia to export

recording a 17 percent increase in output relative to the up to 600,000 MT of maize grain and mealie meal to

revious season, the country recorded yet another sign- DRC. This was strictly for early maize and mealie meal

gificant deficit estimated at about 1.2 million MT, mainly produced from it. However, key informant interviews

attributed to severe drought conditions in some parts of with industry players revealed that there were reports

the country. of commercial farmers taking advantage of the MoU to

export maize from the normal harvest. These reports

In regards to marketing, the season kicked off relative- prompted government to halt the export by commercial

ly early, where player entered the market around early farmers to allow for further investigations. By the end

April. Like the previous season, private sector entered of November XXX MT had been exported under this

the market first, although the level of private sector par- agreement.

ticipation appeared to have been subdued by a number

of factors with the COVID-19 pandemic restrictions and

export ban being key among them.

4

Despite the sustained ban on formal exports of maize factors affecting maize market performance and their

grain and mealie meal, informal trade continues to thrive major outcomes. The analysis is based on the 2020/2021

between Zambia and neighboring Malawi, DRC, and marketing season and 2019/2020 production season.

Tanzania. Substantial price differential between Zambia Data for this report were drawn from various sources,

and neighboring countries has largely contributed to including the Ministry of Agriculture’s Crop Forecast

informal trade. For example, the price of a 50 Kg bag Survey (CFS), Zamba Statistics Agency, Food and

of white maize grain in the DRC at Kipushi border Agriculture Organization (FAO), and Famine Early

was fetching ZMW 350 in July and 410 in November , Warning System Network (FEWS NET), among others.

whereas the FRA was buying at ZMW 110/50 Kg bag. Data from these sources were used to construct key

A 25 Kg bag of breakfast meal was going for ZMW 185 trends and make assumptions about likely outcomes

at Kipushi border whereas the average price in Lusaka in the 2020/2021 marketing season. These data were

was at ZMW 117/25 Kg bag. This price differential has complemented by key informant interviews with industry

continued to attractflows of these major commodities players and government officials.

from Zambia into DRC, with mealie meal dominating

in terms of volumes exported to DRC. The bulk of the Maize Stocks Position

maize informally exported from Zambia was destined for

Malawi, followed by Tanzania. At the opening of the 2020/2021 marketing season in

May 2020, Zambia had an estimated opening stock

In regards to food security, the situation at national of 179,247 MT of commercially available maize, down

level remained favorable and stable compared to the from previous season’s 475,042 MT (Stocks Monitoring

previous season. This was mainly attributed to the Committee 2020), representing 62 percent decline from

above-average production for maize and other food previous season and about 77 percent from the five-

crops during the 2019/2020 agricultural season, which year historical average (Mulenga, Kuteya and Chapoto

resulted in increased food supply at both household 2020; FEWSNET, IAPRI and WFP 2020). It should be

and national level. However, there were still cases of noted that this stock level does not account for maize

localized deficits, but these were few mostly in parts of grain still held by smallholder farmers.

Western and Southern provinces as a result of drought

conditions and fall army worm. The northern region also The distribution of the opening stock was highly

experienced deficits in some areas due to the floods that skewed, with the FRA holding the highest stock at

affected crops and even displaced people, with about 82,982 MT, followed by Millers Association of Zambia

700, 000 people in 28 districts directly affected (Zambia (MAZ) with 42,020 MT, with Zambia National Farmers

Daily Mail, March 23, 2020). Owing to the above-average Union (ZNFU) holding 8,320 MT and about 45,000 MT

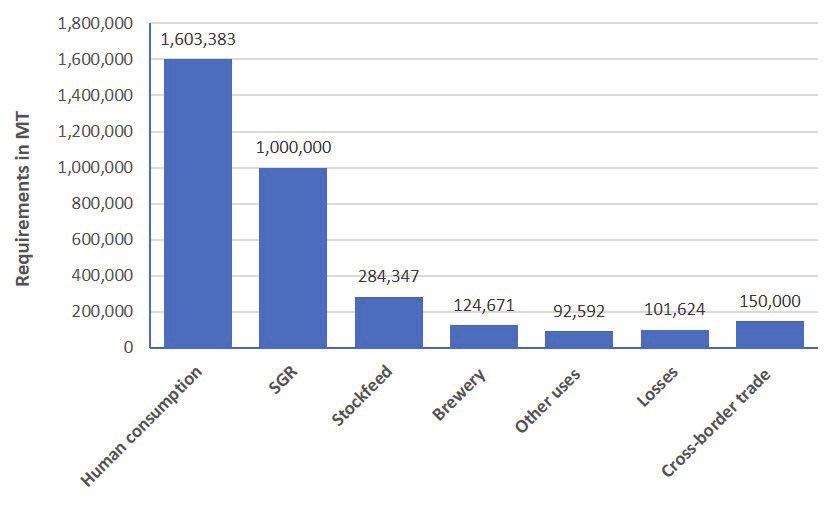

harvest, the demand for FRA maize was significantly of early maize. Grain Traders Association of Zambia

lower than previous season, with FRA having utilized (GTAZ) reported that they had no stock remaining at the

only about 4,000 MT by end of September compared beginning of the marketing season. With an estimated

to over 40,000 MT the previous season. national production of 3,387,469 MT, the country had

an estimated total supply of 3,566,716 MT against

Having presented an overview of the maize market for an estimated total national requirement of 3,356,617

the previous and current marketing season, this outlook (Figure 1 for distribution) Therefore, the country had an

provides deeper insights into the domestic and regional estimated exportable surplus of 210,000 MT.

Figure 1. Distribution of National Maize Requirements for 2020/2021 Marekting Year

Source: Stocks Monitoring Committee, 2019

5

Based on the above distribution, the country had a minor contribute towards enhancing crop market information

surplus of 210,000 MT, slightly less than the 218,000 availability on which stakeholders, both government

MT estimated the previous season. This low surplus at and private sector can base their decisions.

the heels of an above-average harvest should not come

as a surprise given the more than three-fold increase in As illustrated in Figure 2, FRA held the larger proportion

targeted SGR (from 300,000 MT the previous season to of stocks at the beginning of the season in May. This

1 million MT in the current season) and the low opening was despite the high demand for FRA maize by DMMU

stock. As at end of October 2020 -- when FRA was and other relief organizations responding to food

expected to close its marketing exercise-- the country’s emergencies duringt the previous season. For example,

commercially available maize stocks were estimated by August 2019, DMMU had drawn about 30,000 MT

to be at approximately 940,124 MT, similar to previous compared to less than 4,000 MT the current season

season’s 926,911 MT at the end of October 2019. This during the same period. As the season progressed,

estimate is based on the known stocks held by FRA private sector progressively held more stocks than

and registered members of MAZ, GTAZ, ZNFU. FRA, given the early market entry and higher price

offered to farmers by private traders, thus attracting

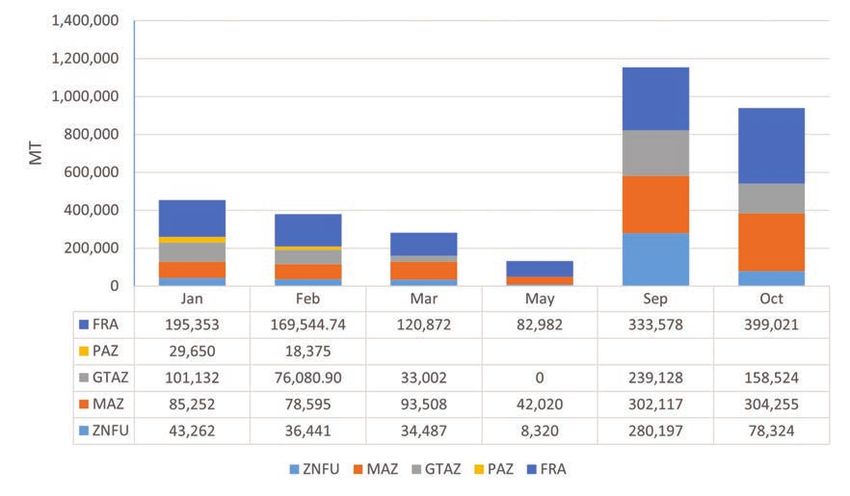

Figure 2 shows stocks held by various major players in more maize supply. However, the level of private sector

the market at different time points during the marketing participation was lower than the previous season mostly

season. As only FRA is mandated by law to report due to government decision to maintain the export ban

maize stocks held, the figures presented by other and the intentions by the FRA to procure 1 million MT

stakeholders in the Stocks Committee meeting are for the SGR. Combined, these factors discouraged

based on the stocks voluntarily reported by MAZ, GTAZ, private sector participation as the export ban meant no

and ZNFU. Hence, the stock figures are most likely only outlet beyond Zambia’s borders while the 1 million SGR

a conservative representation of total maize availability created speculation that the FRA will eventually offload

in the country, because not all millers are members of this maize at a price than the market price later in the

MAZ, nor do all farmers report their stock level to ZNFU, season. This presents a price risk for private sector

and not all grain traders belong to GTAZ. Further, these thus discouraging them from procuring large volumes.

figures do not account for grain held by smallholder In addition, the COVID-19 pandemic restrictions and

farmers and various small private traders. It is expected control protocols contributed to market uncertainities

that operationalization of the now established Zambia and increased cost of doing business for larger and

Agricultural Information System (ZAIS) will provide a formal traders, thus slowing down private sector

more comprehensive and accurate picture of stock participation in the market.

levels in the country at any given time point, and thus

Figure 2. Maize Stocks Held by Various Players between January and October 2020

Source: Stocks Monitoring Committee (2020).

6

Maize Production

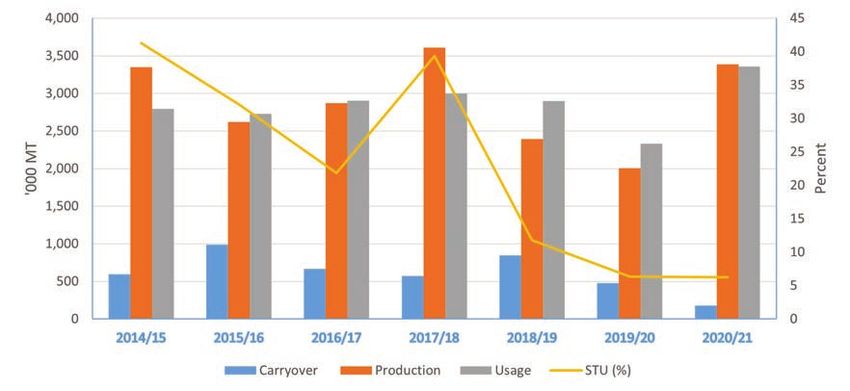

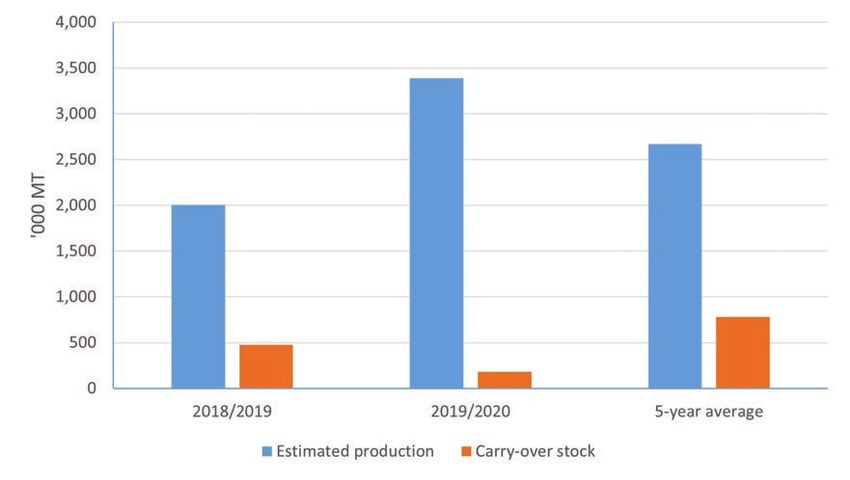

Production in the 2019/2020 agricultural season surged Figure 3 presents a summary of harvest and opening

to 3,387,469 MT from 2,004,389 MT in 2018/2019 stock for the 2019/2020 and 2018/2019 production

– a 69 percent increase from previous season. The seasons, as well as the five-year average. Two key

increase in production was mostly driven by favorable points from the graph are: 1) production increased

weather that was experienced in most parts of the substantially relative to the previous season and five-year

country much of the season. Good weather, among average; and 2) carry-over stock significantly declined

other factors, contributed to improved yield, with the relative to previous season and five-year average. As

season recording an average yield of 2.07 MT/ Hectare earlier stated, the increase in production in 2019/2020

(Ha) compared to 1.29 MT/Ha recorded the previous production season was mainly driven by favorable

season. The increase in production was further boosted weather pattern in most parts of the country as well as

by an expansion in area planted to 1,634,874 Ha, a 5 area expansion relative to the previous season. Despite

percent increase from previous season’s 1,557,314 Ha. the significant increase in production, total supply was

The apparent correlation between rainfall and maize only slightly higher than the five –year average, owing

production highlights Zambia’s agricultural production to the low carry-over stock this season, as shown in

exposure and vulnerability to weather shocks. Figure 3. The low carry-over stock resulted from tight

maize supplies in the previous season due to drought

conditions.

Figure 3. Domestic Maize Supply Estimates

Source. MoA Crop Forecast Surveys and National Food Balance Sheets (2015 – 2020)

7

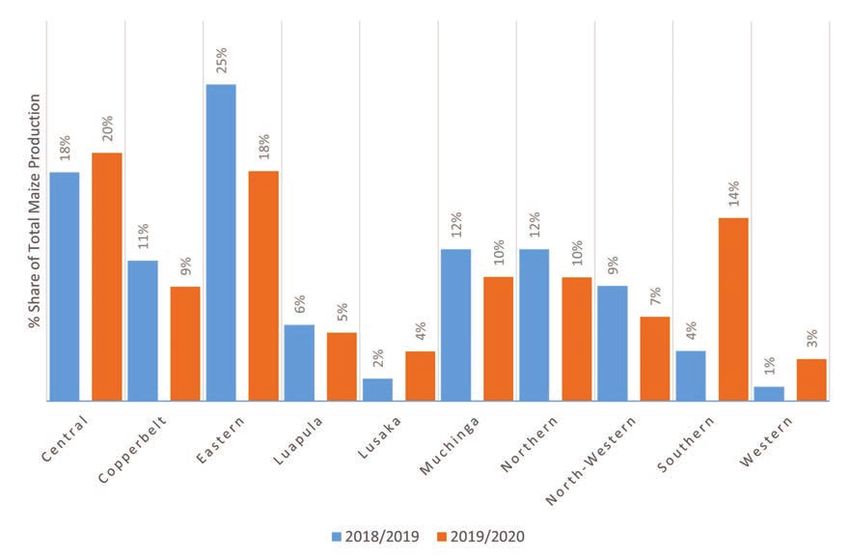

Figure 4. Provincial Maize Production Share to National Production - 2018/2019 and

2019/2020 Seasons

Source: MoA Crop Forecast Surveys (2019 and 2020)

Source: MoA Crop Forecast Surveys (2019 and 2020)

Favorable rainfall helped increase production in Unlike the previous season where maize grain prices

provinces that saw significant decline in production maintained an upward trend even during the main

previous season due to droughts. Figure 4 presents harvest, in the 2020/2021 marketing season saw maize

a summary of the contribution of all the 10 provinces grain wholesale prices declining between April and

to national output in the both the previous and current June, as the new crop was rolling in the market.

season. The graph reveals wide variation in terms of

provincial share to national total output in both seasons. At the end of May 2020, the FRA announced its crop

In the 2019/2020 production season, Central province purchase prices for maize, soybean, and rice. Maize

contributed the highest at 20 percent, followed by prices was ZMW110 per 50 Kg bag (ZMW 2.2/kg),

Eastern at 18 percent, and then Southern province with similar to the previous season. The price though at the

14 percent, while Western ranked lowest at 3 percent. same level as previous season was generally lower than

Compared to the previous season, the contribution of what private traders were offering for maize (ZMW 120

most provinces declined in the current season, whereas -130 per 50 Kg bag) in most parts of the country. As

that of Southern and Western province increased. at end of June, 2020, prices were highest in Eastern

Therefore, in general Southern province despite the province ranging between ZMW 2.5- and ZMW 2.6 per

changing rainfall patterns and some parts receiving kg (or 125- 130 per 50kg bag), followed by Central

erractic rainfall remains a major contributor to national province where prices were around ZMW 2.4 per kg ,

maize grain production. and the lowest being Muchinga, Luapula, and Northern

provinces with prices at ZMW 2.2 –ZMW 2.3 per kg (or

Maize Market Prices 110- 115 per 50kg bag),, almost matching the FRA

price.

The 2019/2020 marketing season experienced an

atypical trend in maize prices, where grain prices

continued to increase throughout including during and

after crop harvest (April –June).

8Figure 5. Maize Grain Wholesale and Mealie Meal Reatil Prices for the Period May

2019 – November 2020

Source: GTAZ reference prices, ZamStats, and IAPRI commodity price (2019 and 2020)

Figure 5 shows the trend in wholesale maize grain prices the lean season in October 2019, breakfast mealie meal

and mealie meal retail prices for the period May 2019 prices were 140/25 Kg, whereas in 2020 October they

to November 2020. The trend clearly shows a stark hovered around 129 – 135 per 25 Kg.

difference between the two seasons, with the current

season prices rising slower than the previous season. The current season’s increase in production, though

For example, in 2019, maize wholesale prices increased significant, did not appear to be sufficient enough to

by 11 percent between April and June (harvest period), depress domestic prices to a considerable level. This

whereas they declined by 17 percent in 2020 during the was partly due to the low opening stock the country had

corresponding period. Between August and October at the beginning of the 2020/2021 marketing season,

(peak marketing season) grain prices increased by which resulted in a low stocks-to-use (STU) ratio.1

about 43 percent in 2019, whereas they only went up

27 percent in 2020 during the corresponding period.

The slow rise in prices in the 2020/2021 marketing

season was mostly influenced by an improvement

in both domestic and regional market supply, which

contributed to moderating the increases.

As market activity slowed down at the end of October,

prices were 7 percent lower in 2020 compared with

prices during the same period in 2019. As maize grain

is the main input in mealie meal production, declining

maize prices were transmitted to mealie meal prices,

with both breakfast and roller meal prices retreating

from the 2019 levels and closely tracing the maize grain

price trends (Figure 5). For example, at the beginning of

1 Stocks to use ratio is a indicative measure of supply and demand interrelationships of commodities. The ratio indicates the level of carryover stock as a percentage of the total use

of the commodity. A lower ratio indicates tight supply and vice-versa. The ratio thus helps in estimating and predicting the direction of the price trend as well as the probable extent of

price change whether higher or lower.

9Figure 6. Trend in Carryover stock, Production, Usage and Stocks to Use Ratio

Source: Calculated from MoA Crop Forecast Survey and National Food Balance Sheet (2014/2015 – 2020/2021)

Figure 6 shows a seven-year trend in the STU ratio, towns, prices were relatively high in Kabwe, Kapiri

which clearly shows that the current season’s STU ratio Mposhi, and Mkushi (Central province), and lowest in

is similar to that of the previous two seasons, which Mpika (Muchinga province). The relatively higher prices

were characterized by droughts and tight supplies, and in Central province are not surprising as it was reported

contributed to rising prices. that most millers were sourcing their maize from Central

province, some entered the market as early as March

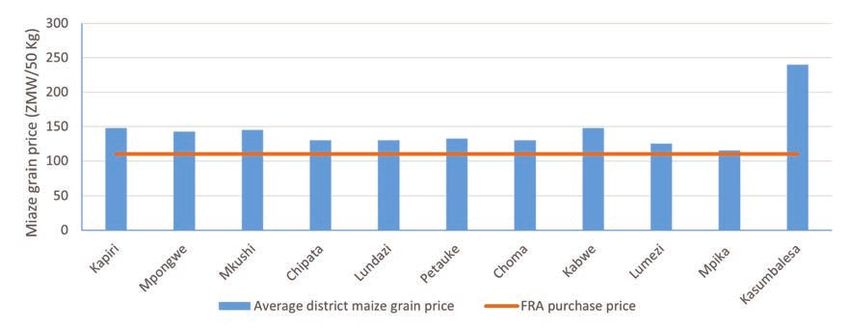

Figure 7 shows the prices at which the private traders 2020, thus exerting upward pressure on local prices.

were buying maize grain from farmers in selected The above FRA prices across the country is a sign

districts benchmarked against the FRA price of ZMW of competition that private sector could exert in the

110 per 50 Kg bag. Generally, the average market price market as long as the supply conditions appear to be

for maize grain in all the assessed districts was higher tight. Consequently, due to private sector competitive

than that of FRA. Despite the FRA being a big player in behaviour, the FRA failed to meet its target in these

the market, it appears the Agency’s price had very little provinces. It is important to note that this situation does

impact on the market, as other traders maintained a not translate to food insecurity because any maize

higher price. Kasumbalesa, the Zambian town bordering held by private sector is maize that can be utilised in

DRC, had the highest price (averaging ZMW 240 per the country. The situation on the ground points to the

50 Kg bag), driven by the high demand for Zambian urgent need for the country to offload some of the maize

maize and maize products in DRC. Away from border stocks in the country to the regional market.

Figure 7. Private Sector and FRA Maize Buying Prices in Selected Districts, October/

November, 2020

Source: IAPRI Rapid Market and Food Security Assessment October/November 2020.

10FRA Maize Purchase and Pricing

As is normally the case, the FRA announced its pan As a result of this realease, the FRA was unusually

territorial purchase price and intended SGR target at efficient in paying farmers who sold maize to the Agency.

the start of the marketing season. On May 29, 2020, Farmers were paid within 5 days of delivering their maize

the FRA announced a price of ZMW 110/50 Kg bag to the Agency, a move that was highly commended by

– the same price it offered in 2019. Further, the FRA stakeholders, and contributed to many farmers selling

announced that it intended to purchase 1 million MT of their maize to the Agency.

maize grain, more than threefold increase from previous

season’s target of 300,000. The 1 million MT target was Despite FRA’s price announcement, market prices

at wide variance with the budget as announced by the remained above ZMW 110/50 Kg bag in most parts

minister of finance during his National Budget address in of the country for much of the season. The efficient

October of 2019 (2020 National Budget Address), where payment system by FRA, might have somewhat created

Minister Bwlaya Ng’andu indicated that the FRA would competition for private sector buyers who in turn tried

purchase 300,000 MT of maize grain for SGR in 2020. to offer competitive prices possibly higher than FRA

The decision to increase the SGR purchases to 1 million to attract more supplies, as spot cash alone was not

MT was announced as part of government’s COVID-19 enough to incentivize farmers.

repsonse under the MoA COVID-19 contigency plan.

Another reason cited by the FRA for increasing the SGR Compared to 2019, FRA’s purchases started on a

was to boost the national stocks given the low stock good note, with the Agency setting up 1,200 satelite

carryover from the previous season. When Predisent depots across the country. Figure 8 shows the monthly

Edgar Lungu made the announcement that FRA should progression of FRA purchases from July to October. The

purchase 1 million MT of maize for SGR, he cited climate figure shows a significant increase in purchase between

change and weather unpredictability as reasons why July and August, after which the rate of increase declined

the country needed to increase its SGR, especially in a from September to October. Within the first month of

bumper harvest year like 2020 (Lusaka Times, April 30, entering the market, FRA had managed to purchase

2020). 98,000 MT compared to only about 51,311 MT of maize

purchased in the previous season during the first month

At the time FRA was announcing its ZMW 110/50 of market entry. By the end of October, 2020, which

Kg bag price, market price was way above this level, marks the end of FRA maize purchases, the Agency

hovering around ZMW 125 per 50Kg bag. Thus, there had procured a total of 349,405 MT, representing 34

were concerns from stakeholders, particularly farmers, percent of the targeted 1 million MT.

that FRA’s lower than market price will influence other

buyers to start buying at a lower price, considering that FRA’s failure to meet the targeted SGR of 1 million MT did

FRA is a major player in the market and was setting not come as a surprise, as most stakeholders predicted

a trend. This created fears in the market that private this outcome given the Agency’s bid price which was

buyers might exploit farmers by offering even lower than lower than that offered by the private sector. Normally,

the FRA price. Further considering that FRA does not FRA closes its maize purchasing exercise on October

pay spot cash, and in fact takes months to pay farmers, 31 of every year, however, the Agency has continued

there were concerns that farmers might be compelled to purchase maize beyond the statutory ending date in

to sell at a lower price to private traders who offer spot an attempt to mop up maize not procured by private

cash. sector.

Determined to purchase the 1 million MT, the government

through the Treasury Department of the Ministry of

Finance released ZMW 1 billion to FRA for purchase

of SGR (maize, soybeans, and paddy rice) purchases

(Ministry of Finance, 2020), with the bulk of it budgeted

for maize purchases.

11For example, in 2019/2020 marketing season, Zambia

experienced one of the worst food emergencies in

Figure 8. Cummulative FRA Maize Purchases

recent history, with more than 2 million people in 53

July to October 2020

districts requiring relief food.

Even under this worst case scenario, stock drawdown

from FRA to respond to food emergency was only

175,000 MT (Mulenga, Kuteya and Chapoto 2020).

Thus, with an SGR of almost 350,000 MT this season

as at end of October, FRA has more than enough maize

to respond to unforessen deficits.

Instead of worrying about the failure of the Agency to buy

the targeted 1 million metric tonnes,, the Governement

should ensure that the more than 300,000 metric tonnes

SGR it has is well managed by reducing the amount

of maize that is given to millers at subsidized prices as

was the case in the previous season. The reduction in

supplies of subsidized maize to millers is a step in the

right direction as processors should be encouraged to

procure their own stock during the marketing season or

buy stock held by private traders. This trend will help

Source: FRA and Stocks Monitoring Committee (2020) completely wean millers off of government subsidies,

as research evidence has shown that the subsidy to

millers is not effectively passed on to consumers. By

In terms of geographic distribution of purchased further improving its targeting and ending the practice of

volumes, the bulk of the maize FRA procured was from subsidizing millers, government can ensure food security

Central, Eastern, Muchinga, and Southern provinces. through a scaled back SGR of 300,000 to 350,000

Out of the total FRA purchase, about 30 percent was MT, including or supplemented by ‘virtual reserves’,

from Northern province, and in second place was which will create a win-win of reducing fiscal costs and

Luapula with about 17 percent, and in close third place crowding-in the private sector to boost productivity.

was Muchinga province accounting for 15 percent.

Lusaka and Western provinces contributed the least Owing to the above-average harvest this year, demand

at 1 percent and 0.9 percent respectively. The low for FRA maize is likely to remain low, as there are few

purchase by FRA in Western province is attributed to the localized deficit areas in need of relief food. This implies

low output experienced in the province due to drought that the Agency will enter the next marketing season

conditions and fall army infestation experienced in the with a relatively higher carryover stock. Thus, in the

2019/2020 production season. Even in high production next season, FRA should consider scaling back the

areas such as Central, Southern, and Eastern province, volume of SGR to be purchased, and concentrate on

FRA struggled to purchase maize due to competition procuring from remote areas to ensure with minimal to

from private sector who were offering a higher price than no private sector presence. However, the target should

the ZMW 110/50 Kg bag offered by FRA throughout the be kept within the recommended size of between

season. 300,000 to 350,000 MT. FRA can achieve this target

by: i) purchasing maize at market price and ensure

The failure by FRA to purchase the 1 million MT coupled efficient payment system as the case was this season;

with the low stock carryover from previous season ii) focus on purchasing maize from remote areas with

resulted in the Agency recording an SGR of less than very minimal or no private sector presence; and iii) FRA

500,000 MT in the 2020/2021 marketing season. The should consider purchasing and holding a grain option

349,405 MT of SGR secured by the FRA so far, though from ZAMACE or regional commodity exchanges

less than half of the targeted SGR, should not be cause ‘virtual stocks’ to be drawn upon when responding to

for concern as IAPRI research has shown that the FRA unforeseen deficits, rather than purchasing and holding

can ensure food security with stock levels not exceeding large physical stocks, as this has fiscal implications and

350,000 MT (see Mulenga, Kuteya, and Chapoto 2020; crowds-out private sector participation. This would

Kuteya and Samboko 2018). require an effective food security early warning system

to be put in place.

12Private Sector Participation In For example, in March 2020, Copperbelt province

Grain Marketing Minister Japhen Mwakalombe was quoted by the

media threatening to close down shops that were

Generally, the 2020/2021 marketing season was selling mealie meal at prices above ZMW 130/ 25 Kg

characeterized by low private sector participation bag (Zambia Reports, March 26, 2020).

comparable to the 2019/2020 season. However, similar

to the previous season, private sector started the season In regards to exports, governement only allowed early

with an early entry in the market around early April. The maize and mealie meal produced from it to be exported

private traders include aggregators for millers, animal under the tripartite agreement with the DRC. In the

feed manufacturing companies, medium- scale traders, previous season, government imposed an export ban

and a myriad of small-scale individual traders (popularly on the heels of a reduced harvest and the need to ensure

known as Briefcase Buyers). The pronouncement by the that there was enough maize domestically to meet the

FRA that it intended to procure 1 million MT discouraged national requirements and keep prices within affordable

private traders from engaging in the market to the extent range for majority Zambians. Unfortunately, this ban

seen in the previous two seasons. has remained into effect despite the country recording

a surplus and the prospects for a good harvest in 2021

The positive strides and momentum, in terms of private are high.

sector participation, that was witnessed the previous

two seasons when FRA confined its participation in the Despite the sustained ban on formal exports of maize

market to only purchasing the recommended level of grain and mealie, informal trade flows continued

SGR appear to have been hampered this season. This between Zambia and neighbouring Malawi, DRC, and

somewhat buttresses the evidence that FRA market Tanzania. Governement defense wings intensified their

interventions, when excessive, crowds out private security operations to curb illegal exports, with a number

sector participation. The heightened private sector of arrests recorded during the season. In March, seven

participation in the previous two seasons resulted (7) trucks laden with mealie meal destined for Malawi,

in increased economic activity, particularly in rural was intercepted in Chipata by officers from the Zambia

areas and possibly job creation, but equally important National Service (Zambia Daily Mail, March 24, 2020).

helped with fiscal savings for the governement. The And this was only among the many reported cases of

pronouncement by FRA to increase SGR far beyond the traders attempting to export maize and mealie meal

recommended level sent a signal to market players that across borders.

large quantities of maize will be offloaded on the market

by FRA later in the season, and thus depress domestic Informal trade was mostly driven by substantial price

prices. This discouraged traders from purchasing large differential between Zambia and neighboring countries.

volumes, and constrained private sector participation For example, in late August and early September, the

only in accessible areas. price of a 50 Kg bag of white maize grain in the DRC at

Kipushi border was selling for ZMW 350 while the FRA

Government Intervention in the was buying at ZMW 110/50 Kg bag. A 25kg bag of

breakfast meal was costing ZMW 185 at Kipushi border

Maize Sub-Sector while the average price in Lusaka was at ZMW 117/25

Kg bag. This price differential attracted flows of these

Unlike the previous season when government instituted

major commodities from Zambia into DRC, with mealie

several interventions, including exports ban, temporally

meal dominating in terms of volumes exported to DRC.

price controls (Mulenga et al. 2019) in an attempt to

For the most part of the season, the bulk of informal

moderate grain and maize meal prices owing to the tight

maize grain exports were destined for Malawi, followed

supplies, the 2020/2021 marketing season is different in

by Tanzania and DRC, whereas bulk of mealie meal

terms of number of interventions. In the current season,

exports were destined for DRC, followed by Tanzania

government’s key intervention was to do with banning

and Malawi.

exports, and almost no attempt to control prices, except

a few threats from government officials.

13

13Regional Maize Production and the 2020/2021 marketing season. In Malawi, opening

Trade stocks were well below average following strong informal

export demand from Tanzania during the previous

This section draws heavily from the 2020 Southern marketing season, mostly destined for the Greater

Africa Regional Supply and Market Outlook (SA Horn of Africa and low SGR procurement during the

RSMO) analysis conducted by FEWSNET, IAPRI and previous year. Maize opening stocks were average in

WFP. The Regional Supply and Market Outlook report typically self-sufficient Mozambique and below average

provides a summary of regional staple food availability, across the region’s other structurally deficit countries

surpluses and deficits during the current marketing such as Botswana, Lesotho, Namibia, and Eswatini. In

year, projected price behavior, implications for local and Zimbabwe and DRC, opening stocks were negligible

regional commodity procurement, and essential market

monitoring indicators. The report covers southern, On aggregate, the 2020 maize harvest for the region

central, and part of east Africa region. was 20 percent above the previous year and five-year

average. The above-average harvest in the region

Regional Maize Production was mostly driven by favorable weather experienced

Generally, the southern African region produced a during the production season. In most parts of the

surplus unlike the previous season when the region was region, the start of season was characterized by erratic

in deficit by about 0.69 million MT. An analysis of the and insufficient rains, however, the latter half of the

Southern Africa Regional Supply and Market Outlook season saw favorable rains in surplus-producing areas

conducted by FEWSNET, IAPRI and WFP (2020) which helped with crop recovery and improved crop

shows that at the start of 2020/21 marketing season, conditions. However, poor rainfall in structurally deficit

opening stocks across the region were significantly southern DRC and Zimbabwe coupled with chronically

below average.2 In surplus producing South Africa, limited extension and input services led to well below

opening stocks were near average and in Tanzania they average production (Figure 9) Countries which posted

were above average despite high export flows within large declines in their maize harvest compared to the

and beyond the region during the previous marketing five-year average were those which were particularly

year. However, in Zambia, one of the region’s largest affected by poor rainfall, namely: southern DRC (-60

producers and exporters, maize harvests during the percent), Lesotho (-56 percent), Zimbabwe (-23

previous season were more than 32 percent below the percent), Madagascar (-23 percent), and Namibia (-25

recent five year average for a second consecutive year, percent).

resulting in limited opening stocks for the country in

Figure 9. Cumulative precipitation as a percent of normal for October 1, 2019

to March 25, 2020

Source: USGS/FEWS NET (2020)

14

14Table 1. Regional Maize Balance Sheet for the Period of April 2020 – March 2021

Source: FEWS NET, IAPRI, WFP estimates based on SAGIS, SADC, FAO/GIEWS and Ministries of Agriculture data (2015 -2020)

Table 1 gives a summary of the regional maize balance Figure 10 shows maize self-sufficiency for countries in

sheet for the period of April 2020 to March 2021. the region. On the whole, the region is self sufficient, with

The region’s harvest was 20 percent relative to the key producing countries (South Africa, Zambia, Malawi,

2019/2020 marketing season and the 5-year average. Mozambique, and Tanzania) recording above-average

However, opening stock was down 22 percent and harvest. However, a number of countries remained in

21 percent relative to the 2019/2020 season and the a deficit state, and these include, Botswana, Namibia,

five-year average. The above-average harvest helped South DRC (Haut-Katanga), and Zimbabwe. These

to compensate the low opening stock, and boosted countries will rely on imports from the region and

maize during the 2020/2021 marketing season. possibly international markets to meet supply shortfalls.

South Africa, the leading producer in the region, saw its

total maize harvest for 2020 go up 27 percent above

Figure 10. Maize Self-Sufficiency Status

average, with white maize production reaching over 40

(2020/21 Marketing Year)

percent above average. As a result, there is more than

adequate supply of both yellow and white maize for local

and regional demand. South Africa has also continued

to export maize grain to international markets (e.g. East

Asia) since early 2020 (SAGIS 2020; Dhlamini 2020).

South Africa has also intensified exports to Zimbabwe

with the recent easing of its phytosanitary restrictions

and import duties (maize meal, wheat grain, and flour).

Zambia, the region’s second largest exporter historically,

has maintained its formal export ban on maize grain and

maize meal. Despite the export ban, Zambia exported

maize grain and maize meal to the DRC under a special

government-government arrangement. The maize

exported under this arrangement was strictly produced

as early maize under irrigation and mechanical drying

by large scale/commercial farmers in Zambia. Between

April and May 2020, informal maize grain and maize

meal outflows from Zambia to DRC intensified. Informal

maize grain exports from Zambia to Malawi continued

through much of the season, as Malawi’s Agricultural

Development and Marketing Coropration (ADMARC)

was purchasing maize at a price higher than the Source: FEWSNET, IAPRI and WFP estimates (2020)

prevailing market price in many places of neighboring

Zambia and Mozambique.

15

15Regional Maize Prices The majority of maize grain imports into Zimbabwe

As the 2020/2021 marketing season kicked off, were by private commercial millers. The majority of

maize grain prices in many countries remained above- those maize imports remain financially inaccessible

average levels, mainly due to the persistent effects to the country’s poor households. Furthermore, the

of the previous year’s tight supply (Figure 11). With government’s subsidized maize meal scheme was

the progression of harvest and marketing, prices fell not well funded or supplied, limiting the availability of

rapidly in Malawi, Mozambique, Tanzania, and Zambia, subsidized maize meal on the market.

although they remained above-average. In South Africa

prices declined in May after remaining unusually stable Strategic Grain Reserve Purchases

in April due to a combination of factors, including State agencies responsible for strategic grain reserves

strong regional export demand, a late start of season, continued their active participation in the markets within

and the epreciation of the South African Rand (ZAR). respective countries. In the case of Zambia, the FRA

announced that it would purchase 1 million MT of maize

– a significant increase from the original plan of 300,000

Figure 11. May 2020 maize prices compared MT. FRA’s buying price of 110 ZMW/50kg was initially

to 5-year average below prevailing market prices (ZMW 120 to ZMW 130

per 50 Kg bag) in May and early-June. Market prices

nevertheless decreased biut only marginally despite

FRA’s price announcement because it had not yet

started procuring. Prices rebounded slightly by early

July, after FRA purchases began and remain relatively

high throughout the season ranging between ZMW 120

– ZMW 140 per 50 Kg bag.

In Malawi, ADMARC, the state-owned agency involved

in grain marketing and storage, was purchasing

maize grain at MWK 200 per Kg, which was above

prevailing market prices across much of Malawi as

well neighboring areas of Mozambique and Zambia.

However, due to funding constraints, purchases were

erratic. The price differentials of the ADMARC purchase

prices attracted heavy informal maize flows into Malawi

despite the country’s above-average production.

The government of Zimbabwe’s Grain Marketing Board

(GMB) began purchasing maize and small grains in

May. Purchase volumes are currently higher than 2019,

Source: FEWS NET (2020) but well below average due to below average domestic

availability and strong imports from neighboring South

Africa. This is also despite a 77 percent increase in the

maize purchase price relative to 2019 coupled with a

In Zimbabwe, maize prices continued to increase, 30 percent top up incentive. By May 2020, prevailing

mostly driven by effects of the volatile macroeconomic market prices were 16 times higer than previous year

environment and low production levels. This is despite levels and 32 times the average levels. Due to limited

the recent reintroduction of a multicurrency system local maize grain availability, the GMB sales of subsidized

(approved among measures to ease the effects of maize meal have been limited.

COVID-19 on economic activities) and strong imports

from South Africa.

16

16South Africa’s 2020/2021 total maize surplus of 5.5

Figure 12. Projected Regional Maize Trade million MT is expected to help offset deficits in countries

Flows such as Botswana, Lesotho, Namibia, and Eswatini.

South Africa’s maize export volumes to Zimbabwe

are likely to remain significantly above average (SAGIS

2020). Due to sufficient regional maize supply this

year, South Africa is expected to continue exporting to

international markets (East Asia in particular), although

some imports of yellow maize for the livestock feed

industry are anticipated (Figure 12). Zimbabwe will

source both white and yellow maize primarily from

regional markets. Rice imports from international

markets will fill domestic supply gaps in consuming

countries such as Mozambique and Madagascar.

Production estimates for Zambia indicated that the

country’s total production was about 25 percent above

historical five-year average, but opening stocks were

over 70 percent percent below average. Thus, supplies

are expected to be near average. Since 2019, Zambia

has maintained a formal maize export ban, although

informal exports are ongoing. The FRA’s ambitious

goal to purchase 1 million MT implies that Zambia’s

exportable surplus will only be about 210,000 MT, which

is approximately 70 percent below-average. However,

Source: FESNET, IAPRI and WFP (2020)

informal exports from Zambia to neighboring countries

have been taking place and are projected to continue

throughout the season.

Projected Market and Trade Trends

For 2020/2021 Table 2 shows informal cross border maize grain trade

volumes for the period April 2020 to September 2020.

Owing to the combination of above-average regional Zambia’s informal exports were mostly to Malawi,

harvests and below average opening stock levels, Tanzania and the DRC, with informal exprts to Malawi

Southern Africa remains self-sufficient in terms of maize reaching a high of over 4,000 MT in the month of June.

supply. Zimbabwe and DRC (Haut Katanga) had an Malawi also exported a sizeable volumes of maize grain

estimated above-average deficits of about 1.1 million mainly exported to Tanzania. Mozambique’s informal

MT and 0.8 million MT respectively. After accounting for maize grain exports were mostly destined for Malawi.

regional requirements, the estimated regional surplus of Malawi appears to be a transit country for further export

4.5 million MT remains the largest since the 2010/2011 to Tanzania.

marketing season.

Table 2. Informal Regional Maize Grain Trade Volumes – April 2020 to September 2020

Source: FEWS NET and WFP

17

17Notwithstanding the maize export ban in Zambia, Rather, COVID-19 related lockdown measures and

informal maize trade thrived, with exports mainly movement restrictions have heavily affected population

destined for DRC, Malawi, and Tanzania. During the movement in Southern Africa. This has negatively

period June to September, Zambia informal maize impacted income earning opportunities especially

exports to the the aforementioned countries increased among daily-wage laborers and small scale cross

in 2020/2021 season compared to the previous season border traders. Unrelated to maize, domestic and cross

during the corresponding period, with the exception of border marketing activities of fresh horticultural crops

August when the 2020/2021 volumes fell behind the (e.g. tomatoes) and cash crops (e.g. tobacco) were

2019/2020 season (Figure 13). Besides maize grain, affected by border clearing delays necessitated by

informal mealie meal exports from Zambia also surged, intensified border screening protocols. Uncertainties

with DRC being the main destination. Similar to the regarding how neighboring countries will respond as

previous season, the increase in infomal exports for cases continue to rise presents a market challenge,

both mealie meal and maize grain was mainly driven where players are unsure how lockdowns and other

by the wide price differential between Zambia and contigent measures would impact exports and imports.

neighboring countries. For example, in June, a 50 Kg Thus market players are on edge cautiously weighing

bag of maize was fetching ZMW 130 on the Zambian the potential impact of the pandemic on regional food

side whereas on the Malawian side the same bag was markets.

trading at ZMW 273.

Several regional currencies were already depreciating

prior to the onset of the COVID-19 pandemic. However,

Figure 13. Zambia’s Informal Exports to between January and May 2020, the Congolese Franc

DRC, Tanzania, and Malawi – 2019/2020 and (CDF), ZAR, and ZMW, among others, depreciated

2020/2021 Marketing Seasons partly due to reductions in export earnings linked to the

contracting global economy.

In the East, Tanzania’s informal maize grain exports

to East African markets slowed since March 2020,

compared to 2019 when exports flows from Tanzania

reached very high levels. Border movement restrictions

resulted in delayed border clearing processes.

Government of Kenya, the main recipient of Tanzanian

maize, announced in March that it would import over

350,000 MT of maize grain from international markets

to offset any eventual COVID-19 related supply

disruptions, further contributing to declining exports

from Tanzania.

At a country level, COVID-19 pandemic in Zambia

Source. FEWS NET, IAPRI and WFP(2020) informal cross border resulted in loss of business and wage income for

trade monitoring system

many people both in the rural and urban areas, thus

eroding their purchasing power and access to food.

Impact of COVID-19 This prompted government through the Ministry

of Community Develoment and Social Services in

With regards to COVID-19, the regional maize partnership with UN agencies to implement emergency

production was not affected in any discernable way, as cash transfers to the affected households.

the regional maize harvests were already underway at

the onset of the pandemic in early March 2020.

18

18You can also read