4Q 2019 Results Presentation 30 January 2020 - CDL ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

4Q 2019 Results Presentation

30 January 2020

Important Notice

This document may contain forward-looking statements that involve assumptions, risks and uncertainties. Actual future performance, outcomes and

results may differ materially from those expressed in forward-looking statements as a result of a number of risks, uncertainties and assumptions.

Representative examples of these factors include (without limitation) general industry and economic conditions, interest rate trends, cost of capital and

capital availability, competition from other developments or companies, shifts in expected levels of occupancy rate, property rental income, charge out

collections, changes in operating expenses (including employee wages, benefits and training costs), governmental and public policy changes and the

continued availability of financing in the amounts and the terms necessary to support future business. Predictions, projections or forecasts of the economy

or economic trends of the markets are not necessarily indicative of the future or likely performance of CDL Hospitality Trusts.

The value of Stapled Securities and the income derived from them may fall as well as rise. Stapled Securities are not obligations of, deposits in, or

guaranteed by M&C REIT Management Limited, as manager of CDL Hospitality Real Estate Investment Trust (the “H-REIT Manager”) or M&C Business

Trust Management Limited, as trustee-manager of CDL Hospitality Business Trust (the “HBT Trustee-Manager”), or any of their respective affiliates.

An investment in Stapled Securities is subject to investment risks, including the possible loss of the principal amount invested. Investors have no right to

request that the H-REIT Manager and/or the HBT Trustee-Manager redeem or purchase their Stapled Securities while the Stapled Securities are listed. It

is intended that holders of the Stapled Securities may only deal in their Stapled Securities through trading on Singapore Exchange Securities Trading

Limited (the “SGX-ST”). Listing of the Stapled Securities on the SGX-ST does not guarantee a liquid market for the Stapled Securities.

This presentation contains certain tables and other statistical analyses (the “Statistical Information") which have been prepared by the H-REIT Manager

and the HBT Trustee-Manager. Numerous assumptions were used in preparing the Statistical Information, which may or may not be reflected herein. As

such, no assurance can be given as to the Statistical Information’s accuracy, appropriateness or completeness in any particular context, nor as to whether

the Statistical Information and/or the assumptions upon which they are based reflect present market conditions or future market performance. The

Statistical Information should not be construed as either projections or predictions or as legal, tax, financial or accounting advice.

Market data and certain industry forecasts used throughout this presentation were obtained from internal surveys, market research, publicly available

information and industry publications. Industry publications generally state that the information that they contain has been obtained from sources believed

to be reliable but that the accuracy and completeness of that information is not guaranteed. Similarly, internal surveys, industry forecasts and market

research, while believed to be reliable, have not been independently verified by the H-REIT Manager or the HBT Trustee-Manager and neither the H-

REIT Manager nor the HBT Trustee-Manager makes any representations as to the accuracy or completeness of such information.

You are cautioned not to place undue reliance on these forward-looking statements, which are based on the current view of the H-REIT Manager or the

HBT Trustee-Manager on future events.

This document and its contents shall not be disclosed without the prior written permission of the H-REIT Manager or the HBT Trustee-Manager.

2

About CDL Hospitality Trusts

CDL Hospitality Trusts (“CDLHT”) is one of Asia’s leading hospitality trusts with assets valued at S$2.85 billion. CDLHT is a stapled

group comprising CDL Hospitality Real Estate Investment Trust (“H-REIT”), a real estate investment trust, and CDL Hospitality

Business Trust (“HBT”), a business trust. CDLHT was listed on the Singapore Exchange Securities Trading Limited on 19 July

2006. M&C REIT Management Limited is the manager of H-REIT, the first hotel real estate investment trust in Singapore, and M&C

Business Trust Management Limited is the trustee-manager of HBT.

CDLHT was established with the principal investment strategy of investing in a portfolio of hospitality and/or hospitality-related real

estate assets. As at 31 December 2019, CDLHT owns 16 hotels and two resorts comprising a total of 5,088 rooms as well as a

retail mall. The properties under CDLHT’s portfolio include:

i. six hotels in the gateway city of Singapore comprising Orchard Hotel, Grand Copthorne Waterfront Hotel, M Hotel, Copthorne

King’s Hotel, Novotel Singapore Clarke Quay and Studio M Hotel (collectively, the “Singapore Hotels”) as well as a retail

mall adjoining Orchard Hotel (Claymore Connect);

ii. three hotels in Brisbane and Perth, Australia comprising Novotel Brisbane, Mercure Perth and Ibis Perth (collectively, the

“Australia Hotels”);

iii. two hotels in Japan’s gateway city of Tokyo, comprising Hotel MyStays Asakusabashi and Hotel MyStays Kamata

(collectively, the “Japan Hotels”);

iv. one hotel in New Zealand’s gateway city of Auckland, Grand Millennium Auckland (the “New Zealand Hotel”);

v. two hotels in United Kingdom (Hilton Cambridge City Centre in Cambridge and The Lowry Hotel in Manchester) (collectively,

the “UK Hotels”);

vi. one hotel in Germany’s gateway city of Munich, Pullman Hotel Munich (the “Germany Hotel”);

vii. one hotel in the historic city centre of Florence, Italy, Hotel Cerretani Firenze - MGallery (the “Italy Hotel” or “Hotel Cerretani

Firenze”); and

viii. two resorts in Maldives, comprising Angsana Velavaru and Raffles Maldives Meradhoo (collectively, the “Maldives Resorts”).

3

References Used in this Presentation

1Q, 2Q, 3Q, 4Q refers to the period 1 January to 31 March, 1 April to 30 June, 1 July to 30 September and 1 October to 31 December

respectively

1H and 2H refers to the period 1 January to 30 June and 1 July to 31 December respectively

ARR refers to average room rate

AUD refers to Australian dollar

CCS refers to cross currency swap

DPS refers to distribution per Stapled Security

EUR refers to Euro

FY refers to financial year for the period from 1 January to 31 December

GBP refers to British pound

JPY refers to Japanese yen

NPI refers to net property income

NZD refers to New Zealand dollar

pp refers to percentage points

RCF refers to revolving credit facility

RevPAR refers to revenue per available room

SGD refers to Singapore dollar

TMK refers to Tokutei Mokuteki Kaisha

USD refers to US dollar

YoY refers to year-on-year

YTD refers to year-to-date

All values are expressed in Singapore dollar unless otherwise stated

Note: Due to rounding, numbers presented throughout this document may not add up precisely to the totals provided and percentages may not precisely reflect the absolute figures 4

Table of Contents

Key Highlights 6

Portfolio Summary 12

Healthy Financial Position 17

Singapore Market 22

Overseas Markets 32

Asset Enhancement Plans 40

Annexe 50

− Background and Structure of CDL Hospitality Trusts 50

− Location of CDL Hospitality Trusts Properties 65

5

Key Highlights

6

Key Highlights of the Year

Investing Close to S$800M in Two Singapore Hotels

Redevelopment of Novotel Singapore Clarke Quay* Acquisition W Singapore – Sentosa Cove*

Divestment of NCQ (57-year leasehold) for S$375.9M at 87% Secured luxury lifestyle hotel for S$324.0 million in tightly-held

premium over initial purchase price, unlocking value and Singapore market

redevelopment potential Sentosa will be a key future tourism driver for Singapore,

Forward purchase of a brand new, lifestyle hotel (fresh 99- various expansion plans will enhance Singapore’s

year leasehold (1)) at redeveloped Liang Court Site (2) at a attractiveness as a premier tourist destination

capped fixed price of S$475M or lower of 110% of W Hotel to be a beneficiary of the demand growth expected to

development cost be generated by the various medium to long-term plans

Achieved primary objective of retaining presence on Liang Capital value underpinned by high quality asset with generous

Court Site in prized Clarke Quay location room sizes

Both landmark transactions recently approved by Stapled Securityholders with >99% votes in favour

* Novotel Singapore Clarke Quay (“NCQ”), W Singapore – Sentosa Cove (“W Hotel”)

(1) From acceptance of lease renewal

(2) Liang Court Site comprises NCQ, Liang Court mall and Somerset Liang Court Singapore (“Liang Court Site”) 7

Key Highlights of the Year

Continued Investment in Existing Singapore Hotels to Stay Competitive

Makeover project for Orchard Hotel

started in 2018 and was completed in

2019, covering:

260 rooms in Orchard Wing

Lobby, all meeting spaces and F&B

outlets

Ongoing / planned asset improvement

projects for other Singapore Hotels

Grand Deluxe Room, Orchard Hotel Grand Ballroom, Orchard Hotel

RevPAR of Singapore Hotels

RevPAR YoY % Change in 2019 RevPAR in 2H

6.0% S$

5.1% 5.0%

4.9% 180 171 Two consecutive quarters of yoy

5.0%

162 RevPAR growth for Singapore Hotels

4.0%

160

3.0% Strongest periods of growth observed

2.0% 140 since 2012

1.0%

0.0% 120

-1.0% 1Q 2Q 3Q 4Q 2H 2018 2H 2019

-2.0%

-1.7%

-3.0% -2.4%

8

Results Highlights (4Q 2019)

Total Distribution (After DPS (1)

Net Property Income

Retention of Working Capital)

1.2% YoY 0.6% YoY 0.0% YoY

S$ million S$ million S$ cents

38.4 38.0 33.4 33.6

40.0 35.0 3.00 2.77 2.77

30.0 2.50

35.0 25.0

30.0 20.0 2.00

15.0 1.50

25.0 1.00

10.0

20.0 5.0 0.50

15.0 0.0 0.00

4Q 2018 4Q 2019 4Q 2018 4Q 2019 4Q 2018 4Q 2019

Higher NPI contribution from Singapore Hotels due to stronger performance

Highest quarterly YoY RevPAR growth since 2012

Inorganic contribution from Hotel Cerretani Firenze (2)

Overall NPI decreased slightly as lower contribution from other overseas markets more than offset growth

Significant portion of decline was due to expected reduced income from Pullman Hotel Munich, stemming from cyclicality in the city’s events

calendar

Total distribution in 4Q 2019 increased 0.6% YoY and DPS remained stable

Includes a partial distribution of proceeds from sale of Mercure and Ibis Brisbane

(1) Represents total distribution per Stapled Security (after retention of working capital). Total distribution per Stapled Security (before retention) for 4Q 2019 is 2.98 cents

(2) Hotel Cerretani Firenze was acquired on 27 Nov 2018 9

Results Highlights (FY 2019)

Total Distribution (After DPS (1)

Net Property Income

Retention of Working Capital)

3.3% YoY 2.0% YoY 2.6% YoY

S$ million S$ million 111.6 S$ cents

146.1 141.2 112.0 109.4 9.26

150.0 10.00 9.02

130.0 104.0 8.00

110.0 96.0 6.00

90.0 88.0 4.00

70.0 80.0 2.00

50.0 72.0 0.00

FY 2018 FY 2019 FY 2018 FY 2019 FY 2018 FY 2019

NPI declined due to:

Extensive renovation works at Orchard Hotel and absence of 2 major biennial events and a series of meetings/events for ASEAN

Chairmanship in 2018 for Singapore during 1H 2019

Closure of Raffles Maldives Meradhoo for renovation (2) and some disruption from renovation works in Angsana Velavaru

Decrease in contribution from some overseas markets (in part due to weaker currencies)

Partially mitigated by stronger 2H performance of Singapore Hotels, higher NPI for Pullman Hotel Munich and inorganic contribution from Hotel

Cerretani Firenze (3)

Total distribution and DPS lower as a result of the:

Decrease in overall NPI

Higher interest expense, mainly due to additional loans for asset enhancements, acquisition of Hotel Cerretani Firenze, as well as higher

funding costs

(1) Represents total distribution per Stapled Security (after retention of working capital). Total distribution per Stapled Security (before retention) for FY 2019 is 9.83 cents

(2) Resort was closed in Jun 2018 and opened in end Sep 2019

(3) Hotel Cerretani Firenze was acquired on 27 Nov 2018 10Details of Distribution

Distribution for the period 1 Jul 2019 to 31 Dec 2019 (after retention and including capital distribution) is

4.86 Singapore cents per Stapled Security comprising:

3.33 Singapore cents of taxable income + 0.52 Singapore cents of tax exempt income + 1.01 Singapore

cents of capital distribution

February 2020

Mon Tue Wed Thu Fri Sat Sun

Closure of books: 1 2

5 pm on 7 February 2020

3 4 5 6 7 8 9

10 11 12 13 14 15 16

Distribution Date:

26 February 2020 17 18 19 20 21 22 23

24 25 26 27 28 29

11Portfolio Summary

12NPI Performance by Geography

4Q ’19 4Q ’18 Change YoY FY ’19 FY ’18 Change YoY

S$’000 S$’000 S$’000 Change S$’000 S$’000 S$’000 Change

Singapore 24,566 23,527 1,039 4.4% 87,880 87,445 435 0.5%

New Zealand 4,699 4,846 (147) -3.0% 16,320 17,831 (1,511) -8.5%

Australia 2,249 2,368 (119) -5.0% 9,139 9,832 (1) (693) -7.0%

United Kingdom 3,310 3,299 11 0.3% 12,663 12,804 (141) -1.1%

Germany 1,861 2,703 (842) -31.2% 9,862 9,747 115 1.2%

Italy (2) 490 118 372 N.M 2,818 118 2,700 N.M

Maldives

(Closure of one resort (277) 258 (535) N.M (1,312) 3,425 (4,737) N.M

for renovations)

Japan 1,069 1,293 (224) -17.3% 3,792 4,852 (1,060) -21.8%

Total 37,967 38,412 (445) -1.2% 141,162 146,054 (4,892) -3.3%

(1) Includes 11 days of fixed rental income from Mercure Brisbane and Ibis Brisbane, which were divested on 11 Jan 2018

(2) Hotel Cerretani Firenze was acquired on 27 Nov 2018 13Well-Balanced NPI Exposure

Breakdown of Portfolio NPI by Country for FY 2018 and FY 2019 (1)

FY 2018 NPI – S$146.1 million FY 2019 NPI – S$141.2 million

Oceania

New Zealand: 12.2%

Australia: 6.7% (2) Oceania

Singapore Singapore New Zealand: 11.6%

Australia: 6.5%

18.9%

18.0%

15.5% Europe

UK: 9.0%

Europe 62.3% 18.0% Germany: 7.0% (3)

59.9% UK: 8.8% Italy: 2.0% (3)(4)

5.7% Germany: 6.7% (3)

Italy: 0.1% (4) 1.8%

Other Asia

Maldives: 2.3% Other Asia

Japan: 3.3% Maldives: N.M

Japan: 2.7%

(1) Numbers may not add up due to rounding

(2) Includes 11 days of fixed rental income from Mercure Brisbane and Ibis Brisbane, which were divested on 11 Jan 2018

(3) On the basis of a 100% interest before adjustment of non-controlling interests. CDLHT owns an effective interest of 94.5% and 95.0% in Pullman Hotel Munich and Hotel Cerretani

Firenze respectively

(4) Acquisition of Hotel Cerretani Firenze was completed on 27 Nov 2018 14Consistent Growth in Portfolio

2.3% YoY Growth in Portfolio Valuation as at 31 December 2019 (1)

S$ M

3,000 2,847

2,743 2,783

CAGR = 9.4% (2) 225

213 230

2,469 2,438

2,500 2,355

443

2,239 270 248 375 451

258

2,030 2,045 179 133 111

2,000 328

343

335 327 450 363

1,787 355 350 395

1,629 Sub-Prime

1,481 1,502 352

128

1,500 93 110

1,102

123

1,000 846

1,726 1,769 1,740 1,837

1,675 1,695 1,684 1,705 1,739

1,501 1,435

1,388 1,392

500 979

846

0

IPO 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Singapore Oceania Europe Other Asia

(1) Numbers may not add up due to rounding

(2) CAGR from IPO to 31 Dec 2019 15Geographically Diversified Portfolio

Breakdown of Portfolio Valuation as at 31 December 2019 (1)

Singapore 64.5% Oceania 12.1%

Orchard Hotel 16.4% New Zealand – Grand 7.0%

Europe

Millennium Auckland

Grand Copthorne Waterfront Hotel 13.0%

Australia 5.0%

Oceania

Novotel Singapore Clarke Quay 12.9%

Novotel Brisbane 2.4%

M Hotel 8.6%

Mercure Perth 1.6%

Studio M Hotel 6.1%

Ibis Perth 1.0%

Copthorne King’s Hotel 4.2% Other

Asia Other Asia 7.9%

Claymore Connect 3.3% Singapore

Maldives 4.9%

Europe 15.6%

Angsana Velavaru 2.7%

United Kingdom 7.1%

Portfolio Valuation Raffles Maldives Meradhoo 2.1%

Hilton Cambridge City Centre 3.9%

S$2.85 billion

Japan 3.0%

The Lowry Hotel (Manchester) 3.2%

MyStays Asakusabashi 1.8%

Germany – Pullman Hotel Munich (2) 6.1% (Tokyo)

Italy – Hotel Cerretani Firenze (2) 2.3% MyStays Kamata (Tokyo) 1.2%

(1) All properties, excluding Novotel Singapore Clarke Quay, were valued as at 31 Dec 2019. Novotel Singapore Clarke Quay was valued by Colliers International Consultancy &

Valuation (Singapore) Pte Ltd on 15 Oct 2019.

(2) On the basis of a 100% interest before adjustment of non-controlling interests. CDLHT owns an effective interest of 94.5% and 95.0% in Pullman Hotel Munich and Hotel Hotel

Cerretani Firenze respectively 16Healthy Financial Position

17Strong and Flexible Balance Sheet

Robust balance sheet with low gearing of 35.4% and ample debt headroom of S$526 million

Strong interest coverage ratio of 6.1x due to CDLHT’s proactive debt capital management

Well-positioned to actively pursue suitable acquisition opportunities and asset enhancement initiatives

Key Financial Indicators

As at 31 Dec 2019 As at 30 Sep 2019

Debt Value (1) S$1,068 million S$1,062 million

Total Assets S$3,061 million S$2,958 million

Gearing (2) 35.4% 36.3%

Interest Coverage Ratio (3) 6.1x 5.9x

CDLHT Debt Headroom at 45% S$526 million S$461 million

Weighted Average Cost of Debt 2.2% 2.3%

Net Asset Value per Stapled Security S$1.5240 S$1.4606

Fitch Issuer Default Rating BBB- BBB-

(1) Debt value is defined as bank borrowings and the TMK Bond which are presented before the deduction of unamortised transaction costs

(2) For purposes of gearing computation, the total assets exclude the effect of FRS 116/SFRS(I) Leases (adopted wef 1 Jan 2019). Refer to Page 25 Note 5 of the financial

statements announcement

(3) CDLHT’s interest cover is computed using FY 2019 and YTD Sep 2019 NPI divided by the total interest paid/ payable in FY 2019 and YTD Sep 2019 respectively 18Diversified Sources of Debt Funding

Debt Facility Details as at 31 Dec 2019 (1)

Multi-currency MTN Programme / Issued / Utilised Unissued / Unutilised

Tenure (years)

Facilities Amount Amount

S$1 billion MTN - - S$1.0B

S$250 million RCF (Committed) S$191.9M 3 S$58.1M

S$500 million Bridge Facility - - S$500.0M

Total S$191.9M

SGD Local Currency

Term Loans / Bond Tenure (years)

Amount Amount

SGD Term Loans S$273.6M S$273.6M 5

USD Term Loan S$88.1M US$65.0M 5

GBP Term Loans S$212.0M £120.5M 5

EUR Term Loan S$66.1M €44.0M 7

EUR/USD Cross Currency Swaps (2) S$157.4M €99.5M 5

JPY Term Loan S$40.4M ¥3.3B 5

JPY TMK Bond S$38.3M ¥3.1B 5

Total S$876.0M

Total Debt Value S$1,067.8M

(1) Numbers may not add up due to rounding

(2) Term loans fixed via a EUR/USD cross currency swap 19Debt Maturity Profile as at 31 Dec 2019

US$65.0 million 5-year term loan was successfully refinanced in Dec 2019

Well-balanced maturity profile with 60% of total debt maturing from 2022 onwards

Debt Maturity Profile (1)(2)

S$ million Currency Amount Type Expiry

Weighted Average Debt to Maturity ~ 2.9 years

400 Fixed Term Loan and

348 JPY S$78.8M Sep 2020

TMK Bond

32.6%

350 SGD S$83.6M Floating Term Loan Aug 2021

300 GBP S$117.0M Floating Term Loan Aug 2021

242

SGD S$147.9M (3) Floating RCF Dec 2021

250 22.7% 212

19.9% SGD S$44.0M Floating RCF Mar 2022

200 Term Loan fixed via

EUR S$103.2M Nov 2022

120 EUR/USD CCS

150

11.2% GBP S$95.0M Fixed Term Loan Dec 2022

79

100 66

7.4% SGD S$120.0M Fixed Term Loan Jun 2023

6.2%

50 Term Loan fixed via

EUR S$54.2M Jul 2024

EUR/USD CCS

0 SGD S$70.0M Fixed Term Loan Aug 2024

2020 2021 2022 2023 2024 2025

USD S$88.1M Floating Term Loan Dec 2024

EUR S$66.1M Fixed Term Loan Apr 2025

(1) Numbers may not add up due to rounding

(2) Based on exchange rates of US$1 = S$1.3548, £1 = S$1.7593, €1 = S$1.5028 and S$1 = ¥80.8407

(3) Multi-currency RCF 20Debt Profile as at 31 Dec 2019

Debt Currency Profile (1)(2)(3) Interest Rate Profile (1)(2)(3)

JPY Fixed Rate Floating Rate

7.4% Borrowings Borrowings

USD

8.2% SGD 40.8% 59.2%

USD - 100.0%

SGD

43.6% GBP 44.8% 55.2%

GBP

19.9%

JPY 100.0% -

EUR (4) 100.0% -

EUR (4) Blended Total 55.0% 45.0%

20.9%

(1) Numbers may not add up due to rounding

(2) Based on exchange rates of US$1 = S$1.3548, £1 = S$1.7593, €1 = S$1.5028 and S$1 = ¥80.8407

(3) Based on effective currency exposure

(4) Term loans fixed via EUR/USD cross currency swaps, effective exposure is in EUR 21Singapore Market

22CDLHT Singapore Properties Performance

YoY YoY

CDLHT Singapore Hotels 4Q ’19 4Q ’18 FY’19 FY’18

Change Change

Occupancy 87.2% 85.8% 1.4pp 87.5% 86.9% 0.6pp

ARR S$192 S$186 3.3% S$185 S$184 0.9%

RevPAR S$168 S$160 5.1% S$162 S$160 1.6%

RevPAR uplift driven by room rate growth and high

occupancy, which were supported by:

Healthy visitor arrivals

Strong convention business resulting in citywide

demand compression

Positive growth delivered despite ongoing room

renovations at Copthorne King’s Hotel since Oct 2019

Limited future supply is supportive for the hotel sector

As at 31 Dec 2019, committed occupancy of Claymore

Connect was 90%

Lobby, Orchard Hotel

23Healthy Growth in Tourism Demand

Visitor arrivals to Singapore grew 2.9% YoY to 17.4 million for YTD Nov 2019 (1)

2020 will see the return of biennial city-wide events such as the Singapore Airshow and Food&HotelAsia

and a number of inaugural events (2) such as the:

International Trademark Association’s 142nd Annual Meeting (~8,000 attendees)

103rd Lions Clubs International Convention (~20,000 foreign attendees)

International Visitor Arrivals to Singapore (1)

Million

12-year CAGR = 5.5% 2.9%

20.0 18.5

17.4 17.4

16.4 16.9

15.6 15.1 15.2

14.5

15.0 Sub-Prime 13.2

11.6

9.8 10.3 10.1 9.7

10.0

5.0

0.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

IPO

Full Year Visitor Arrivals STB Forecast Arrivals YTD Nov Visitor Arrivals

(1) Singapore Tourism Board (“STB”)

(2) STB, “STB unveils a selection of over 60 lifestyle experiences to entice business groups to Singapore”, 10 Sep 2019 24Geographical Mix of Top Markets (Singapore)

Increased visitation from China, USA, Japan and Indonesia contributed more than 75% of the growth

recorded

8 out of the top 10 inbound markets showed growth for YTD Nov 2019

Geographical Mix of Visitor Arrivals Top 10 Inbound Markets

For YTD Nov 2019 (1)(2) YoY Change for YTD Nov 2019 (1)(2)(3)

Others China USA 12.7%

26% 19%

Philippines 6.7%

Japan 6.3%

China 5.5%

UK Indonesia 2.6%

3% Indonesia

16% Australia 2.3%

South Korea

3% UK 2.0%

USA South Korea 1.6%

4% India

8% -1.7% India

Philippines

4% Malaysia -2.2% Malaysia

Japan Australia 6% -5.0% 0.0% 5.0% 10.0% 15.0%

5% 6%

(1) Numbers may not add up due to rounding

(2) Based on STB’s statistics published on 30 Dec 2019

(3) The top 10 inbound markets are ranked according to growth rates in descending order 25Singapore – Diversified Long Term Growth Drivers

of Demand

Top international meeting country for the 11th

year running in 2018 (1)

MICE 103rd Lions Clubs gamescom Rotary International Growing status as a leading MICE destination

International Convention asia Convention

2020 2024

with prominent events being added to its

2020

Expected Attendees: 20,000 Expected Attendees: 30,000 Expected Attendees: 24,000 calendar

Strong leisure and entertainment offerings and

continued investment in tourism infrastructure:

To boost leisure tourism

Leisure

Add to Singapore’s appeal as a MICE

destination

Encourage increase in the length of stay

Singapore as a business and financial hub will

Business continue to drive corporate travel into the city

Image Credits: Lions Clubs International Convention, asia gamescom, Rotary International Convention, Changi Airport Group, STB, F1, Michelin Guide, UFC, International Champions

Cup, HSBC Singapore Rugby 7s

(1) Singapore Exhibition & Convention Bureau, “Conferences, Events & Business Awards” 26Singapore – Investment in Tourism Infrastructure

for Decades Ahead

New Large-Scale Tourism Projects Being Planned Across the Entire Island

Changi Airport Jurong Lake District (3)

Jewel Changi Airport augments Set to be a new growth area with

Changi Airport’s position as one of two precincts – the commercial hub

the world’s best airports (1) at Jurong Gateway, and leisure

and recreational activities at

Extensive makeover of Terminal 2

Lakeside

by 2024 to increase passenger

capacity and enhance experience (2) A 7-ha site has been set aside for

an integrated tourism development

Terminal 5 is slated to open by

that will include attractions,

2030, which will double current

eateries and retail shops

capacity to 150 million passengers

per annum

Mandai Nature Precinct (4) Orchard Road (5)

Rejuvenation of Mandai into an Revamp of Orchard Road shopping

integrated nature and wildlife belt via 4 sub-precincts with new

destination retail concepts and attractions

Eco-tourism hub will house the Tanglin – Arts and lifestyle

new Bird Park and Rainforest Park

Orchard – Retail core

Development will be completed in

Somerset – Youth hub

phases, with the Bird Park and

Rainforest Park scheduled to open Dhoby Ghaut – Green and

by 2020 and 2021 respectively family-friendly attractions

Image Credits: STB, Mandai Park Holdings

(1) Jewel Changi Airport Fact Sheet

(2) Straits Times, “Changi's T2 will be greener, more spacious by 2024”, 17 Jan 2020

(3) Today, “Part of Jurong Lake District to be developed into a key tourist attraction by 2026”, 16 Apr 2019

(4) Channel NewsAsia, “New Mandai eco-tourism hub to feature global wildlife, create jobs”, 16 Jan 2017

(5) Straits Times, “Major revamp of Orchard Road announced with new developments, different offerings in sub-precincts”, 30 Jan 2019 27Singapore – Investment in Tourism Infrastructure

for Decades Ahead (Con’t)

New Large-Scale Tourism Projects Being Planned Across the Entire Island

Greater Southern Waterfront (1) Sentosa-Brani Masterplan (2)

Shifting of city port terminals and Reshaping Sentosa and Pulau

Pasir Panjang terminal to Tuas by Brani into a premier leisure and

2027 and 2040 respectively tourism destination over next 2 to 3

decades

Frees up ~2,000ha of land for a

new waterfront city (6x Marina Bay Both islands will be divided into 5

size) distinct zones for redevelopment

A new major gateway and vibrant Brani will be linked to Sentosa and

location for waterfront lifestyle mainland and will have large scale

attractions, recreational options attractions similar to USS

homes and offices

Marina Bay Sands (3) Resorts World Sentosa (3)

Marina Bay Sands to add 4th new Resorts World Sentosa expanding

tower which will have 30%-40% with multiple new attractions

more MICE space and a 15,000-

New Minion Park and Super

seat arena

Nintendo World in Universal

The new arena will be optimised Studios Singapore

for concerts with state-of-the-art

SEA Aquarium expanding to 3x its

production infrastructure, with the

current size

aim of drawing A-list artists

Phased opening of attractions from

Increase in gaming space

2020 to 2025

Image Credits: STB

(1) Straits Times, “National Day Rally 2019: 'Downtown South' resort likely to be built on Pulau Brani”, 19 Aug 2019

(2) Straits Times, “Sentosa Merlion to make way for new $90m themed linkway as part of Sentosa-Brani masterplan”, 21 Oct 2019

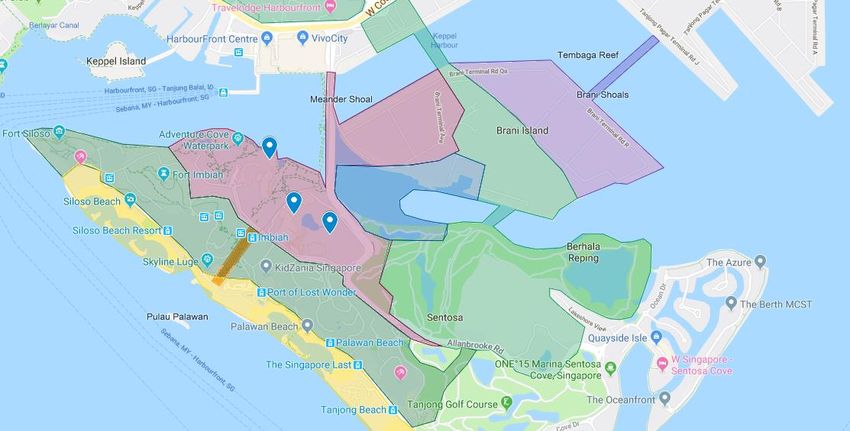

(3) Business Times, “Singapore IRs bet on S$9b expansion; exclusive licences extended to 2030”, 4 Apr 2019 28Singapore – Transformative Leisure and Tourism

Offerings Underway for Sentosa

Sentosa-Brani Masterplan (1)(2)

1 Vibrant Cluster Zone

Greater Southern

Waterfront Mega Spans both islands, will

have large scale

Development attractions

2 Island Heart Zone

RWS Expansion

3 Features hotels,

conference spaces, dining

and retail shops

1 3 Waterfront Zone

Pulau Brani will house a

“futuristic” Discovery Park

2

4 Ridgeline Zone

Connect green spaces

4 from Mt Faber to Mt

Imbiah; nature and

Sensoryscape 5 heritage attractions

1st

project under Masterplan (4Q

2019 to 2022)

S$90m, two-tiered walkway to W Hotel

5 Beachfront Zone

link RWS with Sentosa beaches To be rejuvenated with a

Comprising 30,000 sqm, it will water show, fair ground

be a multi-sensory experience and other attractions

Map is purely for illustration only and was adapted from public sources, as such, it may not be drawn to scale, fully accurate nor fully reflective of the actual zoning areas

(1) Straits Times, “Sentosa Merlion to make way for new $90m themed linkway as part of Sentosa-Brani masterplan”, 16 Apr 2019

(2) Zaobao, “让路给圣淘沙未来发展 圣淘沙鱼尾狮塔10月20日走入历史”, 21 Sep 2019 29Limited Growth in Singapore Hotel Room Supply

An estimated 789 rooms opening this year, representing approximately 1.1% of existing room stock (1)

Supply growth going forward is benign at a low CAGR of 0.8% for the next 4 years

Current and Expected Hotel Room Supply in Singapore (1)

No. of Hotel Rooms

4-year CAGR = 0.8%

80,000

75,000 403 338

789 717

0.6% 0.5% 70,944

1.1% 1.0%

70,000 68,697

70,203 70,606

68,697 69,486

65,000

60,000

55,000

50,000

End-2019 2020 2021 2022 2023 End-2023

Hotel Supply as at End-2019 Estimated Future Hotel Supply Estimated Hotel Supply by End-2023

(1) New supply of rooms is a summation of new rooms deducted by existing rooms taken out of inventory

Sources: STB, Horwath HTL (as at Dec 2019) and CDLHT research 30Potential Supply of New Singapore Hotel Rooms

Until 2023

No. of Expected No. of Expected

Name of Hotel Horwath Rating Location Name of Hotel Horwath Rating Location

Rms Opening Rms Opening

Outside City Outside City

Dusit Thani Laguna Singapore 206 Upscale/Luxury 2Q 2020 Rochester Commons 135 Upscale/Luxury 2021

Centre Centre

The Clan 324 Mid-Tier City Centre 2Q 2020

Outside City

Aqueen Hotel Geylang 100 Economy 2021

Centre

THE EDITION by Marriott 190 Upscale/Luxury City Centre 3Q 2020

Pullman Singapore 342 Upscale/Luxury City Centre 2022

Outside City

Aqueen Hotel Lavender 69 Economy 2020

Centre

Raffles Sentosa Resort & Spa

61 Upscale/Luxury Sentosa 2022

Pan Pacific Orchard Hotel Singapore

340 Upscale/Luxury City Centre 2021

Redevelopment

Outside City

Artyzen 142 Upscale/Luxury City Centre 2021 Banyan Tree Mandai 338 Upscale/Luxury 2023

Centre

Year No. of Rms Upscale/Luxury Mid-Tier Economy

2020 789 396 50% 324 41% 69 9%

2021 717 617 86% 0 0% 100 14%

2022 403 403 100% 0 0% 0 0%

2023 338 338 100% 0 0% 0 0%

(1)

Total (2020 – 2023) 2,247 1,754 72% 324 14% 169 8%

(1) Numbers may not add up due to rounding

Sources: Horwath HTL (as at Dec 2019) and CDLHT research 31Overseas Markets

32CDLHT New Zealand Hotel Performance

Total arrivals to New Zealand increased 0.8% YoY to 3.4 million for YTD November 2019 (1)

RevPAR for Grand Millennium Auckland increased 0.5% YoY for 4Q 2019 with healthy business in the high

season, supported by a stronger concerts calendar

NPI contribution in local currency terms improved slightly but was negatively affected by a weaker NZD

Growing hotel room stock in Auckland is likely to result in an increasingly competitive trading environment

In early 2021, Auckland will host a major sporting event: the America’s Cup sailing regatta and related

challenger series

Expected to drive hotel demand in the lead up to and during the event (2)

Grand Millennium Auckland Lobby, Grand Millennium Auckland

(1) Statistics – Tourism New Zealand

(2) CBRE Valuation Report (Grand Millennium Auckland), 31 Dec 2019 33CDLHT Australia Hotels Performance

No damage to Australia Hotels from country’s bushfires

Lease structure of the Australia Hotels provides CDLHT with fixed rent in local currency

Contribution for 4Q 2019 was affected by a weaker AUD

Beccaria Bar, Mercure Perth Gourmet Bar, Novotel Brisbane

34CDLHT Maldives Resorts Performance

4Q 2019 RevPAR for Angsana Velavaru declined 18.6% YoY as resort was affected by disruption from

renovation works and increased competition from supply growth

Raffles Maldives Meradhoo welcomed its first five-night buy-out since official opening in Sep 2019 due to

ongoing extensive sales and marketing efforts, which contributed significantly to revenue in 4Q 2019

Resort will undergo a gestation period for a few years before reaching a normalised occupancy level

While tourism demand in Maldives is healthy, driven by growth in Indian and European arrivals (1), trading

conditions continue to remain highly competitive in the near term due to new resorts supply

The government is also stepping up efforts to boost tourism, with a recent proposal to increase the 2020

state budget for tourism promotion by close to fifty percent (2)

InOcean Villa (Exterior), Angsana Velavaru Ocean Villa, Raffles Maldives Meradhoo

(1) Ministry of Tourism, Republic of Maldives, Tourism Monthly Updates

(2) Maldives Insider, “Maldives proposes tourism marketing budget hike, allocates $9.98 mln for 2020”, 6 Nov 2019 35CDLHT Japan Hotels Performance

Visitor arrivals grew 2.2% YoY to 31.9 million for 2019 (1) but the Japan-South Korea trade spat continues to

weigh on the economy and hospitality market

South Korean visitation, the 2nd largest source market, sharply declined by 64.7% (1) in 4Q 2019

Coupled with a softer citywide events and concert calendar, new limited-service hotel supply and rebound in

number of alternative accommodation listings (such as Airbnb) (2), RevPAR for the Japan Hotels declined by

14.4% YoY this quarter

Consumption tax hike (3) expected to affect consumer sentiment and spending

Demand driven by the Tokyo 2020 Olympics and Paralympics will provide some rate maximising

opportunities due to expected citywide compression

Looking further, new upcoming theme park attractions in Tokyo (between 2020 to 2022) and development of

integrated resorts will encourage future growth

Twin Room, MyStays Kamata Queen Room, MyStays Asakusabashi Modern Twin Room Aoba, MyStays Asakusabashi

(1) Japan National Tourism Organization

(2) Reuters, “Airbnb touts Japan recovery, bolstered by hotel listings”, 6 Jun 2019

(3) Business Times, “Japan proceeds with twice-delayed sales tax hike as growth sputters”, 1 Oct 2019 36CDLHT UK Hotels Performance

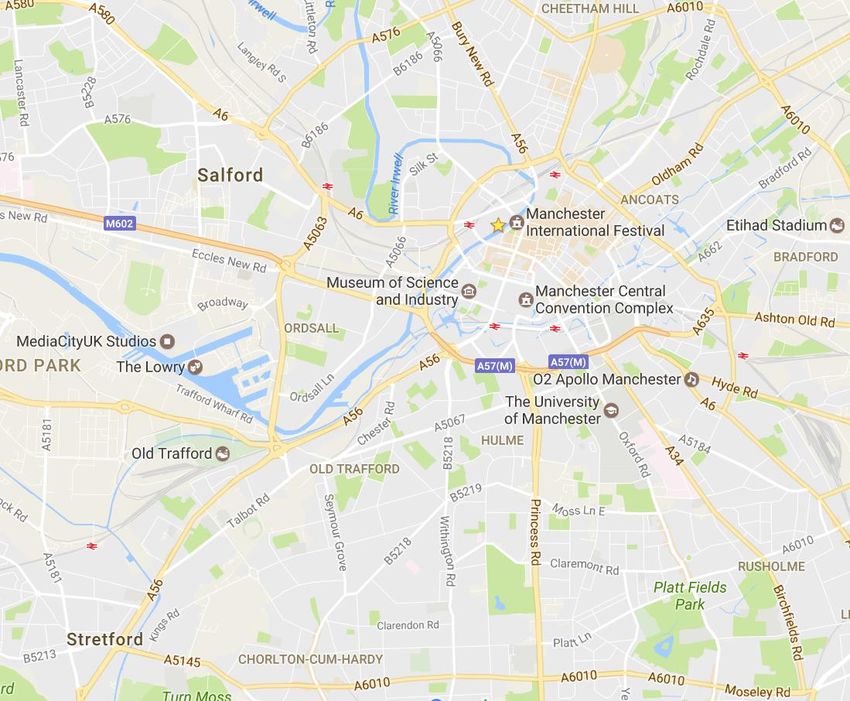

Fewer sporting events and a softer entertainment calendar affected The Lowry Hotel’s performance

Hilton Cambridge City Centre’s RevPAR declined marginally amidst a competitive trading environment

Overall, RevPAR of the UK Hotels decreased 3.7% YoY in 4Q 2019

Despite top line pressure, NPI was maintained at last year’s level

Both cities will see an increase in hotel room inventory in the near term

Public space at Lobby, The Lowry Hotel Executive Lounge, Hilton Cambridge City Centre

37CDLHT Germany Hotel Performance

Pullman Munich Hotel’s performance is driven by the cyclical nature of Munich’s fair calendar (1):

1H 2019 had 2 major events, which saw the hotel deliver a robust performance

2H 2019 had fewer events with the absence of a major congress and trade fair in 4Q, leading to

RevPAR contraction of 10.2% this quarter, which was fully anticipated

1H 2020 will see fewer events and this is expected to turn around in 2H 2020 with a robust line-up of

events

Munich’s tourism demand remains healthy with total arrivals growing 5.6% YoY to 8.0 million for YTD Nov

2019 (2)

Superior Room, Pullman Hotel Munich Lobby, Pullman Hotel Munich

(1) Events Eye

(2) München Tourismus 38CDLHT Italy Hotel Performance

Total visitor arrivals to Florence remains largely unchanged for YTD Sep 2019 (1)

Hotel Cerretani Firenze recorded a RevPAR increase of 2.6% YoY in 4Q 2019 (2), largely driven by growth

in room rate

Bar, Hotel Cerretani Firenze Superior Room, Hotel Cerretani Firenze

(1) Città Metropolitana Di Firenze

(2) The YoY RevPAR comparison assumes CDLHT owned Hotel Cerretani Firenze for the full corresponding period 39Asset Enhancement Plans

40Enhancing Competitiveness of Assets

Singapore

Continued investment to enhance competitiveness of

Singapore Hotels

Copthorne King’s Hotel: Signature Queen Room (New) – Copthorne King’s Hotel

Pipe works and refurbishment of guest rooms are currently

being carried out and are expected to complete in mid 2020

Phased refurbishment to help minimise disruption and the

hotel remains operational

Asset enhancement opportunities in other Singapore Hotels

are also being evaluated strategically

Signature Twin Room (New) – Copthorne King’s Hotel

41Asset Enhancement Plans – Copthorne King’s Hotel

Superior Room (before) Signature Studio (after)

Progressive renovation ongoing

42Enhancing Competitiveness of Assets

Maldives Strengthening Maldives Resorts’ product offerings amidst rising

competition

Raffles Maldives Meradhoo:

Gestation period of a few years is expected before reaching a

normalized occupancy level

Building up awareness of resort through sales and marketing

activities:

Raffles Maldives Meradhoo

Travel partners visiting the resort first before actively

promoting the refurbished resort into the market

Construction of new Presidential Villa, increasing key count from

37 to 38

Angsana Velavaru:

43 of the 79 land villas have been renovated, with infinity pools

added to 24 of these villas at the end of 2019

Angsana Velavaru

43Asset Enhancement Plans – Raffles Maldives

Meradhoo

New Presidential Villa (concept drawings – may be subject to changes)

44Asset Enhancement Plans – Angsana Velavaru

New infinity pools added to Land Villas

45Enhancing Competitiveness of Assets

United Kingdom

Upgrades at The Lowry Hotel to augment its position as The Lowry Hotel

the top hotel in Manchester

Five rooms were upgraded to junior suites in Oct 2019

At Hilton Cambridge City Centre, refurbishment of the

lounge bar was completed in Oct 2019

Hilton Cambridge City Centre

46Asset Enhancement Plans – The Lowry Hotel

Junior Suite – Completed in Oct 2019

47Asset Enhancement Plans – The Lowry Hotel

(Con’t)

Junior Suite – Completed in Oct 2019

48Asset Enhancement Plans – Hilton Cambridge

City Centre

Lounge Bar – Completed in Oct 2019

49Background and Structure

of CDL Hospitality Trusts

50Background on CDLHT

Background Price Performance

IPO on 19 July 2006

Listed on SGX

Mainboard

Sponsored by

Millennium &

Copthorne Hotels

Limited

First Hotel REIT in

Asia ex Japan

Market Capitalisation

S$2.0 billion as of 24

Jan 2020

Source: Bloomberg 51CDLHT Structure

Sponsor Investors

≈37.77% Holdings of Stapled Securities ≈62.23%

as at 31 Dec 2019 as at 31 Dec 2019

H-REIT Distributions HBT

Acts on behalf of

DBS Trustee the holders of H-

REIT Units

Stapling

Deed

Management

Management services

M&C REIT services M&C Business Trust

Management Limited H-REIT Rent HBT Acts on behalf

Management Limited

(H-REIT Manager) (owner and lessor) (owner or lessee) of the holders of (HBT Trustee-Manager)

Lease of the HBT Units

Hotels

Lease of

Rent

Hotels

Master

Active asset management Lessees

in close collaboration

with master lessees

Hotel Manager Hotel Manager

Note: For simplicity, the diagram does not include the relationships in relation to Claymore Connect. The H-REIT Manager manages Claymore Connect directly, hence the various

tenants of the retail units at Claymore Connect make rental payments directly to H-REIT under the terms of their respective leases. 52Blue Chip Sponsor and Parentage

Millennium & Copthorne Hotels Limited City Developments Limited

Internationally recognised hospitality and real One of the largest property developers in

estate group which owns and/or operates a Singapore with a market capitalisation of

portfolio of over 120 hotels worldwide ~ S$9.9 billion (1)

Subsidiary of City Developments Limited Debt to assets ratio of 36.5% as at 30 Sep 2019

(1) As at 24 Jan 2020

Source: Bloomberg 53Management Strategy

1 Acquisition Growth Strategy

Pursue quality assets with growth potential

Adopt a medium to long term perspective to ride through

market cycles

1 2 Partner with or tap on potential pipeline from M&C / CDL

Capitalise on historically low interest rates in certain markets

to enjoy spread over funding costs

2 Asset Management Strategy

Financial

Work closely with master lessees and/or hotel managers to

Foundation implement active revenue and cost management

Implement asset enhancement initiatives to optimise asset

3 potential

Evaluate divestment opportunities periodically to recycle

capital for better returns and unlock underlying asset values

3 Capital and Risk Management Strategy

Growing unitholders’ value via acquisition

and organic growth while keeping a firm Maintain a healthy balance sheet

financial foundation Enhance financial flexibility by maintaining diversified sources

of funding

Hedge against rising interest rates by refinancing with longer

term fixed rate borrowings 54CDLHT Asset Portfolio – Singapore

Grand Novotel

Copthorne Claymore Singapore

Properties Orchard Hotel Copthorne M Hotel Singapore Studio M Hotel

King’s Hotel Connect Portfolio

Waterfront Hotel Clarke Quay (1)

Located on

One of the largest Located in the Located within

Orchard Road, Stylish and

conference heart of financial close proximity to Located next to A family-friendly

with a large pillar- contemporary

facilities in district with strong CBD, Orchard Singapore’s mall with

Description less ballroom and design catering to -

Singapore – well- following of Road, Robertson premier enhanced retail

extensive business and

positioned for the business Quay and Clarke entertainment hub offerings

conference leisure segments

MICE market travellers Quay

facilities

Rooms 656 574 415 310 403 360 - 2,718

Date of

19 July 2006 19 July 2006 19 July 2006 19 July 2006 7 June 2007 3 May 2011 19 July 2006

Purchase

Title /

Leasehold Leasehold Leasehold Leasehold Leasehold Leasehold Leasehold

Remaining

interest / interest / interest / interest / interest / interest / interest / -

Term of Land

62 years 62 years 62 years 47 years 57 years 86 years 62 years

Lease (2)

Valuation (2) S$466.0M S$370.0M S$245.0M S$120.0M S$368.7M S$173.0M S$93.8M S$1,836.5M

(1) Divestment is expected to be complete on 30 Apr 2020

(2) As at 31 Dec 2019 except for Novotel Singapore Clarke Quay which was valued by Colliers International Consultancy & Valuation (Singapore) Pte Ltd on 15 Oct 2019 55CDLHT Asset Portfolio – Overseas

Novotel Brisbane Mercure Perth Ibis Perth

Properties Australia Portfolio

(Australia) (Australia) (Australia)

Comprehensive conference and

Situated in Perth’s CBD and within Located steps away from the

leisure facilities of 11 dedicated

Description walking distance to the Swan River, Murray and Hay Street shopping -

rooms with capacity for up to 350

shopping and entertainment districts belt within Perth’s CBD

delegates

Rooms 296 239 192 727

Date of Purchase 18 February 2010 18 February 2010 18 February 2010 -

Title / Remaining Term of

Strata Volumetric Freehold Strata Freehold Freehold -

Land Lease (1)

Valuation (1) A$73.0M / S$68.5M A$48.0M / S$45.1M A$31.0M / S$29.1M A$152.0M / S$142.7M

(1) As at 31 Dec 2019

Based on exchange rate of A$1 = S$0.9388 56CDLHT Asset Portfolio – Overseas

Raffles Maldives Hotel MyStays Hotel MyStays

Angsana Velavaru

Properties Meradhoo* Maldives Portfolio Asakusabashi Kamata Japan Portfolio

(Maldives)

(Maldives) (Tokyo, Japan) (Tokyo, Japan)

Located in central Tokyo,

Located near Keikyu-

Upmarket resort All-suite luxury resort, with with easy access to

Kamata Station which

offering a wide range of extremely spacious villas Asakusa & Akihabara. A

Description - is only a 10-min train -

dining, leisure and spa which are amongst the few stations away from

ride from Haneda

options largest in Maldives several popular

Airport

sightseeing spots

113 37

Rooms (79 beachfront villas (21 beachfront villas and 150 139 116 255

and 34 overwater villas) 16 overwater villas)

Date of Purchase 31 January 2013 31 December 2013 - 19 December 2014 19 December 2014 -

Title / Remaining

Leasehold interest / Leasehold interest /

Term of Land - Freehold Freehold -

28 years 36 years

Lease (1)

US$102.6M /

Valuation (1) US$57.6M / S$78.0M US$45.0M / S$61.0M ¥4.08B / S$50.5M ¥2.85B / S$35.3M ¥6.93B / S$85.8M

S$139.0M

*Previously known as Dhevanafushi Maldives Luxury Resort

(1) As at 31 Dec 2019

Based on exchange rate of US$1 = S$1.3548 and S$1 = ¥80.8407 57CDLHT Asset Portfolio – Overseas

Hilton Cambridge The Lowry Grand Millennium Pullman Hotel Hotel Cerretani

United Kingdom

Properties City Centre Hotel Auckland Munich Firenze CDLHT Portfolio

Portfolio

(United Kingdom) (United Kingdom) (New Zealand) (Germany) (3) (Italy) (4)

Iconic 5-star luxury

Upper upscale hotel New Zealand’s 4-star hotel boasting

hotel which is 4-star hotel located

and boasts a prime largest deluxe hotel an exceptional

located in proximity in close proximity to

Description location in the heart - which is located in location in the heart -

to the heart of major business

of Cambridge city the heart of of Florence’s historic

Manchester city districts

centre Auckland city centre

centre

Rooms 198 165 363 452 337 86 5,088

Date of

1 October 2015 4 May 2017 - 19 December 2006 14 July 2017 27 November 2018 -

Purchase

Title /

Remaining Leasehold interest / Leasehold interest /

- Freehold Freehold Freehold -

Term of Land 96 years (2) 127 years

Lease (1)

£115.5M / NZ$222.5M / €115.7M /

Valuation (1) £63.4M / S$111.5M £52.1M / S$91.7M €43.9M / S$66.0M (4) S$2,847.4M

S$203.2M S$200.5M S$173.9M (3)

(1) As at 31 Dec 2019

(2) The lease term may be extended for a further term of 50 years pursuant to lessee’s (CDLHT) option to renew under the lease granted by the head lessor (Cambridge City Council)

(3) On the basis of a 100% interest. CDLHT owns an effective interest of 94.5% in Pullman Hotel Munich

(4) On the basis of a 100% interest. CDLHT owns an effective interest of 95.0% in Hotel Cerretani Firenze

Based on exchange rates of NZ$1 = S$0.9009, £1 = S$1.7593 and €1 = S$1.5028 58Summary of Leases

Orchard Hotel, Grand Copthorne Waterfront Hotel, M Hotel, Copthorne King’s Hotel:

Rent: 20% of Hotel's revenue + 20% of Hotel’s gross operating profit, with a fixed rent floor of S$26.4 million

Term of 20 years from Listing (19 July 2006) with 20-year option

Claymore Connect:

H-REIT receives rents direct from tenants

Singapore IPO

Portfolio & Studio M

Studio M Hotel:

Rent: 30% of Hotel’s revenue + 20% of Hotel’s gross operating profit, with a fixed rent floor of S$5.0 million for the initial

10 years of the lease

Term of 20 years from 3 May 2011 with 20+20+10 years option

Novotel Singapore Clarke Quay:

Rent: Hotel’s gross operating profit less Accor’s management fee

Singapore NCQ The divestment of Novotel Clarke Quay has been announced on 21 Nov 2019 and approved by Stapled Securityholders

on 23 Jan 2020. The completion of the divestment is expected to be around end of April 2020.

59Summary of Leases

Grand Millennium Auckland:

New Zealand Rent: Net operating profit of the hotel with an annual base rent of NZ$6.0 million

Grand Millennium First 3-year term expired on 6 September 2019; lease provides for two 3-year renewal terms, subject to mutual

agreement

Auckland Lease renewed for second 3-year term from 7 September 2019, expiring 6 September 2022 (1)

Novotel Brisbane, Mercure & Ibis Perth:

Base rent + Variable rent

Australia Portfolio Base rent: A$9.6 million per annum

Variable rent: 10% of portfolio’s net operating profit in excess of base rent

Term ~ 11 years from 19 February 2010, expiring 30 April 2021

(1) Lease was renewed on 6 Jun 2019 60Summary of Leases

Germany Pullman Hotel Munich:

Pullman Hotel Rent: Around 90% of the net operating profit of the hotel subject to a fixed rent of €3.6 million

Term of 20 years from 14 July 2017, expiring 13 July 2037

Munich

Italy Hotel Cerretani Firenze - MGallery:

Hotel Cerretani Rent: Around 93% of the net operating profit of the hotel subject to a base rent of €1.3 million

Term of 20 years from 27 November 2018, expiring 26 November 2038

Firenze - MGallery

61Summary of Lease and Management Agreement

Angsana Velavaru:

Maldives Rent: Hotel’s gross operating profit less lessee’s management fee

Angsana Velavaru Tiered lessee’s management fee incentivises lessee to drive growth in gross operating profit

Term of 10 years from 1 February 2013, expiring 31 January 2023

Raffles Maldives Meradhoo:

Maldives HBT is the master lessee for the resort's operations

Resort reopened as “Raffles Maldives Meradhoo” in September 2019 after extensive renovation

Raffles Maldives AccorHotels is the hotel manager, appointed by HBT

Meradhoo Term of 20 years from 9 May 2019, expiring on 8 May 2039 (operator has right to extend another 5 years)

Typical management fees apply

62Summary of Management Agreement

Hotel MyStays Asakusabashi and Hotel MyStays Kamata:

HBT is the master lessee for the hotels’ operations

Japan Portfolio MyStays Hotel Management Co., Ltd. is the hotel manager, appointed by HBT

The hotel management agreements renew on a 3-year auto-renewal basis, unless terminated with notice

Typical management fees apply

63Summary of Management Agreement

Hilton Cambridge City Centre:

United Kingdom HBT is the asset owner and currently responsible for the hotel’s operations

Hilton Cambridge Hilton UK Manage Limited (an affiliate of Hilton Worldwide Inc.) is the hotel manager, appointed by HBT

Term of 12.25 years from 1 October 2015, expiring on 31 December 2027

City Centre Typical management fees apply

United Kingdom The Lowry Hotel:

The Lowry Hotel HBT is the asset owner and currently responsible for the hotel’s operations and management

64Location of

CDL Hospitality Trusts Properties

65Hotels in Strategic Locations

Singapore Hotels New Zealand Hotel

Orchard Hotel & Grand Copthorne Novotel

Grand Millennium

Claymore Connect Waterfront Hotel Singapore

Clarke Quay Auckland

H

H

H H

H

SINGAPORE

RIVER

CENTRAL MARINA BAY

BUSINESS SANDS H

DISTRICT

H

BUSINESS &

FINANCIAL

CENTRE SITE

Copthorne King’s Studio M Hotel M Hotel

Hotel AUCKLAND CITY CENTRE

66Hotels in Strategic Locations

Australia Hotels

Novotel Mercure

Brisbane Ibis Perth Perth

Brisbane CBD Perth CBD

H

H

H

CBD AREA

67Hotels in Strategic Locations

Japan Hotels

Hotel MyStays Hotel MyStays

Asakusabashi Kamata

Asakusabashi Kamata

H

H

68Hotels in Strategic Locations

United Kingdom Hotels

Cambridge Manchester

H

Hilton Cambridge City Centre The Lowry Hotel

69Hotels in Strategic Locations

Germany Hotel Italy Hotel

Munich Florence

H

H

Pullman Hotel Munich Hotel Cerretani Firenze - MGallery

70Resorts in Premium Destination

Angsana Velavaru

Malé Atoll

40 min

seaplane

flight

55 min

domestic

flight +

15 min

R speedboat Raffles Maldives Meradhoo*

ride

South

Nilandhe

Atoll

R

Gan International Airport

*Previously known as Dhevanafushi Maldives Luxury Resort 71THANK YOU

72You can also read