A Review of Aspen / Hardwood Resources in Northeast British Columbia - Northern Rockies ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A Review of

Aspen / Hardwood Resources in Northeast

British Columbia

April 2018

Prepared for

[Potential Investors in the Northern Rockies Regional Municipality]

Prepared by:

INDUSTRIAL FORESTRY SERVICE LTD.

1595 Fifth Avenue

Prince George BC

V2L 3L9

250 564 4115

EXECUTIVE SUMMARY

Industrial Forestry Service Ltd. (“IFS”) of British Columbia (“BC”), Canada was retained by

the Northern Rockies Regional Municipality (NRRM) to conduct an analysis and produce

a report describing the aspen / hardwood resources in the Fort Nelson Timber Supply

Area (TSA). This report was expanded to include a description of the forest tenure system

in BC, how access to fibre is acquired, the competitors and potential customers of milling

by-products and incidental softwood logs. The report was also expanded to provide an

assessment of delivered log costs. Each section of the report identifies key conclusions

or facts. These key points are described below:

The Forest Industry in BC

• Access to timber is facilitated through agreements (tenures) with the Provincial

government. There are several forms of tenure that vary with respect to duration

and responsibilities. Each tenure is specific to one management unit, such as a

Timber Supply Area.

• The primary unit of log measurement is the cubic metre. Cubic metre

measurements are adjusted for decay, waste and breakage. The weighted-

average adjustment for deciduous trees in the Fort Nelson Timber Supply Area is

34% (i.e. each cubic metre of standing hardwood timber in a stand is reduced

34%, on average, to derive net merchantable volume).

• The BC Timber Sales program exists province wide and auctions compose

approximately 20% of the Provincial Allowable Annual Cut (AAC).

• Open log markets exist in BC and information regarding volume and price is

provided to government. The average BC interior log price for hardwoods has

ranged from $35 to $40 per cubic metre in the past 10 years.

• The AAC is determined and regulated by government.

• AACs across most of the BC interior are declining.

• Stumpage for deciduous timbers are $0.50 per cubic metre for Grades 1 and 2

(higher quality) and $0.25 per cubic metre for lower quality logs.

Industrial Forestry Service Ltd., Prince George, BC, Canada

ii of xiii

Log Supply and Apportionment

• The AAC for the Fort Nelson TSA has been 1.625 million cubic metres for the past

11 years. A new AAC Determination is overdue, and should be completed in early

2019. There is some downward pressure on the AAC as a result of caribou habitat

concerns. Still, there is also considerable opportunity to increase the AAC if

performance in higher cost stands is proven.

• Two initiatives in development that will reduce the TSAs AAC are a new

Community Forest Agreement (CFA) and a First Nations Woodland Licence. While

collectively these licences would reduce the TSA AAC by 210,000 cubic metres,

this volume would remain within the region and may be available through

negotiation with the licence holders.

• Canadian Forest Products Ltd. (Canfor) is the primary licensee in the region

possessing a Replaceable Forest Licence for 553,000 cubic metres per year and

a Pulpwood Agreement for 610,000 cubic metres per year. The Pulpwood

Agreement expires in December 2019.

• The volume associated with Canfor’s Pulpwood Agreement effectively has no

value, since the Province has indicated that it will not be renewed. Any new

development initiative should engage with senior BC government officials, as they

have considerable flexibility in regard to new licences through the current

accumulated undercut and expiry of the Pulpwood Agreement.

• The BC government agency BC Timber Sales (BCTS) has the ability to auction

approximately 300,000 cubic metres per year of fibre from within their operating

areas. Since there are virtually no forestry operations occurring in the region,

timber auction prices should be very favourable to a new investor.

• Government is in the process of completing a Timber Supply Review (TSR) of the

Fort Nelson TSA. This information will be used by the Provincial Chief Forester

when deciding on the next AAC levels.

Log Processing Industry

• There have been no forest processing operations occurring in the Fort Nelson area

since 2008.

Industrial Forestry Service Ltd., Prince George, BC, Canada

iii of xiii

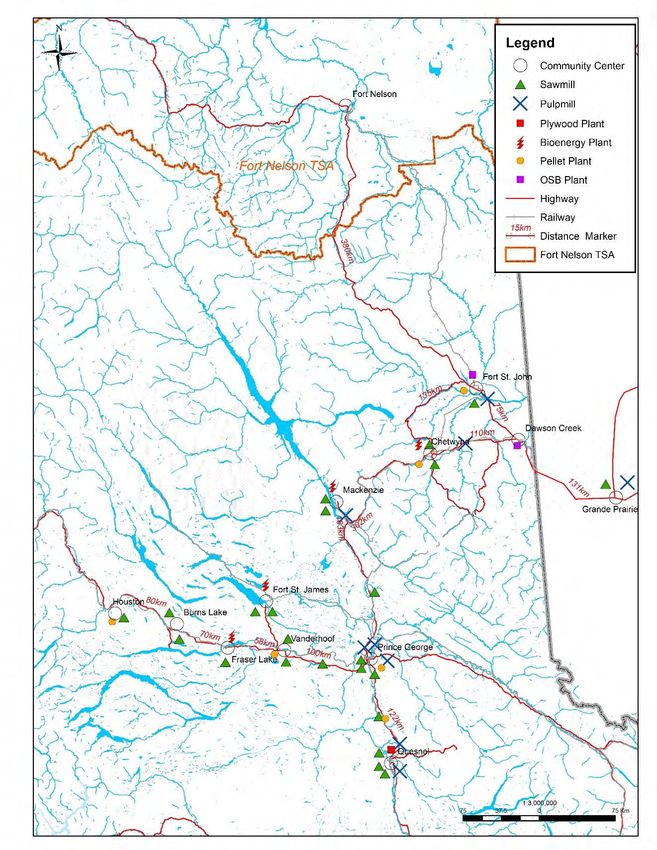

• There is still an extensive and diverse log processing industry in areas south of

Fort Nelson, the closest of which include a conifer sawmill and an OSB plant 390

kilometres south of Fort Nelson.

• Since 2010, BC Regulations have prohibited burning of sawmill waste by-products

(i.e., sawdust, shavings and bark) in bee-hive burners. Hence the development

and expansion of pellet plants and bioenergy plants throughout the BC interior.

• When logs are harvested and then moved on public roads in BC, they are allocated

a timber mark and subsequently scaled. Scaling determines log volume, grade,

and owner, which is used to determine stumpage.

• For deciduous species, Grade 1 and 2 logs have $0.50 per cubic metre stumpage

applied, Grade 4 and 6 (pulpwood) are set at $0.25 per cubic metre. The majority

(82%) of deciduous logs harvested in the Fort Nelson TSA have been Grade 4.

• In the early 2000’s, 61% of the volume harvested in the TSA was aspen. Spruce

trees were 29%.

• Due to extensive oil and gas activity, the eastern part of the region has an

integrated network of all-season roads. However, soils are generally unfavorable

for road construction (clays and muskeg) and new construction costs are

expensive. As a result, most forestry operations have occurred during winter

months when construction on frozen ground, or across frozen rivers, kept

development costs to a minimum.

Hardwood Resources

• The TSA is 9.9 million hectares in area. Within this area, approximately 5.7 million

hectares is productive forest, and 4 million hectares is the timber harvesting land

base that is supporting the current AAC.

• The current mature merchantable land base from within the Timber Harvesting

Land Base (THLB) contains 248 million cubic metres of fibre. Aspen is estimated

to be 47% of this volume or 116 million cubic metres (net).

• The amount of merchantable volume in pure aspen stands (where the conifer

component is

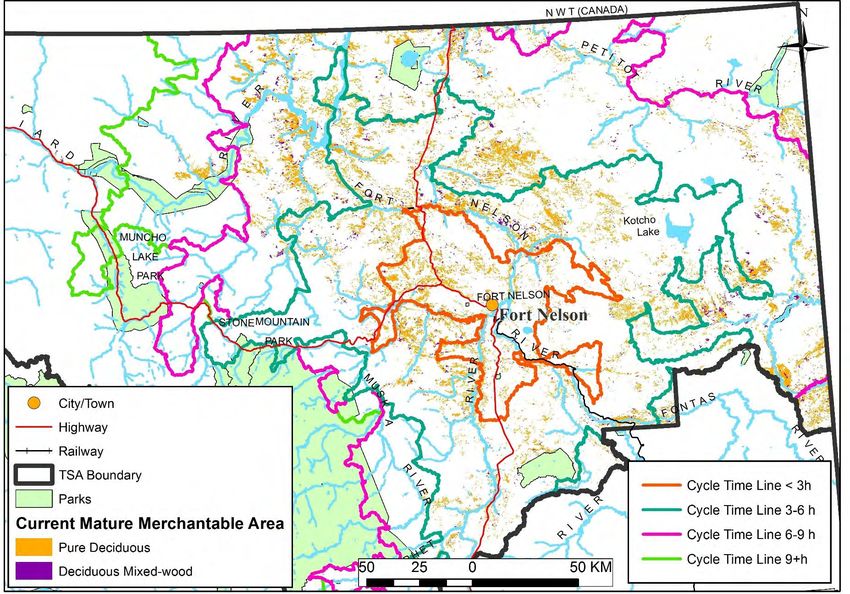

• The amount of merchantable aspen close to Fort Nelson (< 3-hour cycle time) and

in high volume stands (>300 cubic metres per hectare) is estimated to be 10.7

million cubic metres.

• Additional hardwood volume exists in mixed-wood stands. However, some

commercial outlet for the non-aspen trees would be required.

• Risks to timber supply include Acts of God, land base withdrawals for social,

economic or biologic reasons, First Nation Land Claims and errors with the forest

inventory. Although all of these are difficult to quantify, the risks are somewhat

controlled through activities that the BC government attempts to proactively

manage.

• Natural pests affect about 6% of the area. Wildfires affect about 1% of the total

land base.

• Caribou habitat strategies may cause the availability of fibre to drop by 15 to 20%.

• First Nation land claims are addressed through Treaty 8; a long-standing

agreement between First Nations and the Canadian government.

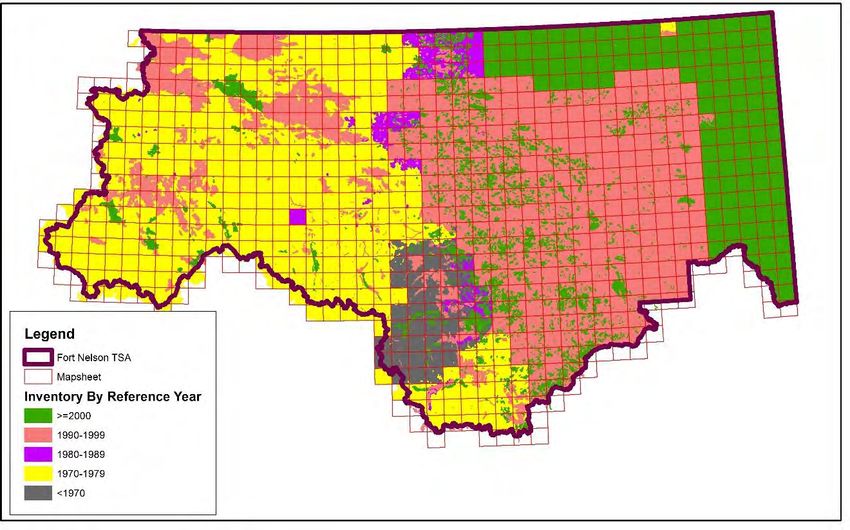

• The forest inventory in some parts of the TSA is old. This places some uncertainty

around the amount of deciduous-leading area that may have transitioned to

conifer-leading. The level of risk is mitigated in part by the fact that the old inventory

exists in parts of the TSA where forestry operations are forecast to be minimal (i.e.,

the mountains to the west of Fort Nelson).

Delivered Log Costs

• The total cost of log delivery is the sum of administration, planning, road

construction, road maintenance, logging, processing, trucking, silviculture, camp

costs and stumpage. These variables remain relatively constant, but their

attributes will vary from location to location.

• An analysis of delivered log costs in the Fort Nelson TSA suggests that the

weighted-average cost of deciduous logs (across the entire current mature

merchantable land base) would be $50.80 per cubic metre from pure deciduous

stands, and range from $32.33 per cubic metre to $82 per cubic metre.

Industrial Forestry Service Ltd., Prince George, BC, Canada

v of xiii

• Analysis of the volume in pure deciduous stands having less than or equal to a

delivered log cost of $40 per cubic metre reveals that 15.4 million cubic metres

meets this criterion.

Considerations for Economic Development

• Although access to fibre in the Fort Nelson TSA is relatively straight forward, the

disposal of undesired tree species and sawmill or board plant by-products should

be a consideration.

• The reduction in AACs in central interior BC TSAs will result in increased demand

for conifer sawlogs. Similarly, the closure of sawmills will increase the demand for

sawmill residual by-products.

• Rail rates and truck haul rates from Fort Nelson to markets to the south are quite

high. Much of the profit from the sale of incidental conifer harvesting or pulp chips

would be consumed by the transportation costs.

• Transportation costs currently exceed the value placed on sawmill residues

(sawdust, shavings and hog fuel). Alternative disposal arrangements will need to

be considered.

Summary

• The Fort Nelson TSA has a large, underutilized supply of coniferous and deciduous

fibre.

• Though most of the Allowable Annual Cut has been allocated, flexibility exists

within government to immediately allocate additional volume on a short term basis,

and on a longer term basis within a few years. Access to fibre is also currently

available through the BC Timber Sales program via market auctions.

• The eastern half of the TSA is well-roaded, primarily as a result of oil/gas

development. However, the soils are such that forestry operations are typically

restricted to winter months.

• The current AAC is 1.625 million cubic metres per year. There are over 248 million

cubic metres of mature merchantable volume in the TSA. Approximately 118

million cubic metres (47%) is aspen, on a net volume basis.

Industrial Forestry Service Ltd., Prince George, BC, Canada

vi of xiii

• The BC government adjusts the whole stem volume of deciduous trees by an

average of 34% downwards to arrive at net merchantable volume. The adjustment

of 18% for decay provides opportunities for incremental increases in the total

volume available, depending on the log specifications of the manufactured product.

• The cost to deliver hardwoods to Fort Nelson averages about $50 per cubic metre

when weighted against all of the merchantable stands. However, considerable

volume exists below $45 per cubic metre. This distribution of merchantable volume

in deciduous-leading stands and the estimated delivered log cost is shown in the

Figure below.

18

16

Current Mature Merchantable timber

14

12

(cubic metres)

10

Millions

8

6

4

2

0

$31

$36

$42

$48

$54

$60

$66

$72

$78

$84

$90

Delivered log cost ($/m3)

Pure Deciduous Deciduous Mixedwood

Industrial Forestry Service Ltd., Prince George, BC, Canada

vii of xiii

Contents

EXECUTIVE SUMMARY .................................................................................................................. II

1.0 INTRODUCTION........................................................................................................................ 1

1.1 SCOPE ............................................................................................................................... 2

1.2 QUALIFICATIONS ................................................................................................................. 2

1.3 DATA SOURCES .................................................................................................................. 3

1.4 TERMINOLOGY .................................................................................................................... 4

2.0 THE FOREST INDUSTRY IN BC IN GENERAL .............................................................................. 6

2.1 LAND OWNERSHIP / FOREST MANAGEMENT UNITS ............................................................... 6

2.2 REGULATORY ENVIRONMENT .............................................................................................. 7

2.3 TENURE SYSTEM ................................................................................................................ 7

2.4 THE “OPEN MARKET” - BC TIMBER SALES ........................................................................... 8

2.5 LOG MARKETS.................................................................................................................... 9

2.6 REGULATING THE HARVEST...............................................................................................10

2.7 GOVERNMENT FEES (STUMPAGE) .....................................................................................10

2.8 ALLOWABLE ANNUAL CUTS ...............................................................................................12

2.9 CLARIFICATION OF VOLUME MEASUREMENTS .....................................................................13

2.10 CONCLUSIONS REGARDING THE FOREST INDUSTRY IN BC ..................................................15

3.0 FORT NELSON TSA LOG SUPPLY AND APPORTIONMENT .........................................................15

3.1 THE FORT NELSON TSA - AAC .........................................................................................16

3.2 APPORTIONMENT OF THE FORT NELSON AAC ....................................................................18

3.2.1 BCTS APPORTIONMENT ............................................................................................19

3.2.2 CANFOR’S PULPWOOD AGREEMENT...........................................................................21

3.2.3 RECENT DEVELOPMENTS WITH REGARD TO APPORTIONMENT......................................22

3.3 CONCLUSIONS - LOG SUPPLY AND APPORTIONMENT ..........................................................23

4.0 NORTH-EASTERN BC LOG PROCESSING INDUSTRY ................................................................24

4.1 HISTORIC LOG UTILIZATION ...............................................................................................26

4.2 ROAD NETWORK...............................................................................................................30

4.3 CONCLUSIONS - LOG PROCESSING INDUSTRY ....................................................................32

5.0 FORT NELSON TSA HARDWOOD FOREST RESOURCES ...........................................................33

5.1 PURE VERSUS MIXEDWOOD ..............................................................................................34

Industrial Forestry Service Ltd., Prince George, BC, Canada

viii of xiii

5.2 HARDWOOD AREAS AND VOLUMES ....................................................................................35

5.3 RISKS TO FIBRE SUPPLY ...................................................................................................39

5.3.1 INSECTS, PATHOGENS AND IMPACT ............................................................................39

5.3.2 CARIBOU HABITAT .....................................................................................................41

5.3.3 FIRST NATIONS LAND CLAIMS ....................................................................................42

5.4 FOREST INVENTORY .........................................................................................................42

5.5 CONCLUSIONS - HARDWOOD RESOURCES .........................................................................43

6.0 DELIVERED LOG COSTS ........................................................................................................45

6.1 ADMINISTRATION AND PLANNING .......................................................................................45

6.2 ROAD CONSTRUCTION AND MAINTENANCE.........................................................................45

6.3 LOGGING AND PROCESSING ..............................................................................................46

6.4 TRUCKING ........................................................................................................................46

6.5 SILVICULTURE ..................................................................................................................48

6.6 CAMP COSTS ...................................................................................................................48

6.7 STUMPAGE .......................................................................................................................48

6.8 CALCULATED DELIVERED W OOD COST BY STAND TYPE .....................................................49

6.9 CONCLUSIONS - DELIVERED LOG COST .............................................................................51

7.0 CONSIDERATIONS FOR ECONOMIC DEVELOPMENT ..................................................................52

7.1 CONCLUSIONS - CONSIDERATIONS FOR ECONOMIC DEVELOPMENT .....................................53

8.0 CONCLUSIONS ......................................................................................................................54

List of Figures

Figure 1: BC Interior Deciduous Log Market ................................................................................. 10

Figure 2 BC Interior Historical Harvest and Forecast AAC ........................................................... 13

Figure 3: Fort Nelson, Historic AAC, Species Partition and Potential Future AAC ....................... 18

Figure 4: Log Harvests from within the Fort Nelson TSA .............................................................. 28

Figure 5: Historic Grades Harvested by Species .......................................................................... 29

Figure 6: Species Harvested from within the TSA – 2001 - 2017 ................................................. 30

Figure 7: Species Distribution in the Current Mature Merchantable Land Base ........................... 34

Figure 8: Deciduous Volume by Cycle Time ................................................................................. 37

Figure 9: Fort Nelson TSA – Historic Wildfires .............................................................................. 40

Industrial Forestry Service Ltd., Prince George, BC, Canada

ix of xiii

Figure 10: Delivered Log Cost of Deciduous Leading Stands ...................................................... 50

Figure 11: Delivered Log Cost of Coniferous-Leading Stands ...................................................... 50

List of Tables

Table 1: Access to Crown Timber ................................................................................................... 8

Table 2: Conversion from Whole Stem to Merchantable Volume ................................................. 14

Table 3: Fort Nelson TSA – 2018 Harvest Apportionment ............................................................ 18

Table 4: Regional Fibre Processing Facilities ............................................................................... 26

Table 5: Area and Current Mature Merchantable Volume within the TSA .................................... 33

Table 6: Pure Deciduous – Species, Volumes, and Cycle Time to Fort Nelson ........................... 36

Table 7: Mixed Deciduous - Species, Volumes, and Cycle Time to Fort Nelson .......................... 37

Table 8: Pests and Natural Disturbance Affecting the Fort Nelson TSA in 2015 .......................... 40

Table 9: Fort Nelson, Estimated 2018 Delivered Log Costs ......................................................... 49

Table 10: Transportation Costs ..................................................................................................... 52

List of Maps

Map 1: General Location of the Fort Nelson TSA ........................................................................... 1

Map 2: Fort Nelson TSA .................................................................................................................. 6

Map 3: Location of Fort Nelson TSA and Licensee Operating Areas ........................................... 20

Map 4: Northern Timber Processing Facilities .............................................................................. 27

Map 5: Existing Road Network ...................................................................................................... 31

Map 6: Leading Deciduous Stands and Cycle Time ..................................................................... 38

Map 7: Age of the Original Forest Inventory .................................................................................. 43

Industrial Forestry Service Ltd., Prince George, BC, Canada

x of xiiiA Review of the Aspen / Hardwood Resources

in the Fort Nelson TSA

1.0 Introduction

The following report describes the results of an analysis and review of the forest resources

in BC generally and the hardwood resources in the Fort Nelson Timber Supply Area (TSA)

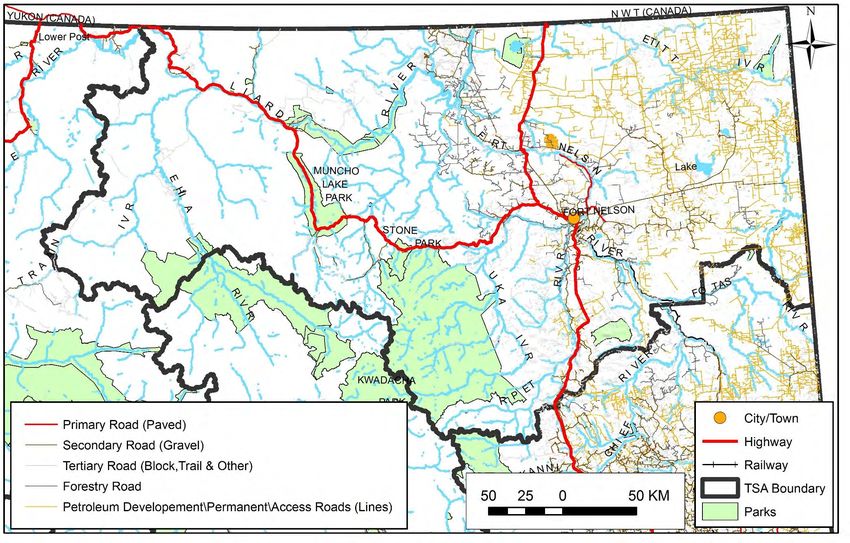

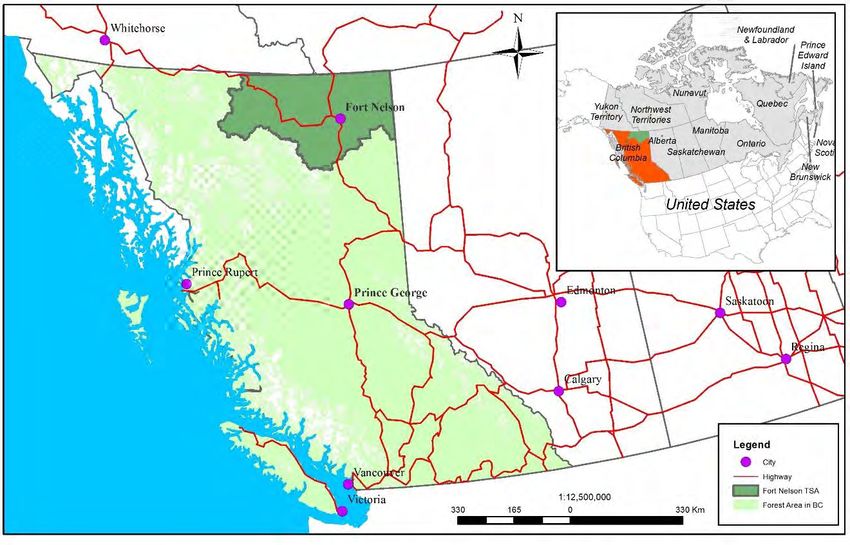

specifically. The general location of the Fort Nelson TSA is shown in Map 1. The report

was prepared by Industrial Forestry Service Ltd. (IFS) for the Northern Rockies Regional

Municipality. Its intention is to provide information for potential forest industry investors

into the region on the opportunities, challenges and costs associated with log processing

generally and with specific focus directed towards the utilization of hardwood species. To

facilitate understanding of Fort Nelson hardwood fibre, an overview of the BC Forest

industry regulatory structure is provided, along with specific details regarding the

hardwood resource with respect to volumes, costs and availability.

Map 1: General Location of the Fort Nelson TSA

Industrial Forestry Service Ltd., Prince George, BC, Canada

1 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

1.1 Scope

Recognizing that foreign investors may be interested, but are unfamiliar with forestry and

forest resources within BC, the scope of this report includes:

• A general description of the forest industry in BC.

• A review of existing and former forest industry activities specific to northeast BC.

• Statistics regarding the existing hardwood forest resources in NE BC, with specific

attention given to location, area, volume, delivered log costs, and log quality.

• Considerations for economic development

• Analysis of risks

• Our opinions and conclusions.

1.2 Qualifications

The author of this report is a natural resource consulting firm (Industrial Forestry Service

Ltd.) that was established in Prince George, British Columbia in 1952.1 Employed by a

wide range of clients within the BC Interior, the foresters and technicians at the firm are

responsible for the pre-harvest planning and development of approximately five million

cubic metres of logs per year. The author has extensive experience conducting analyses

of timber supply in forest management units throughout BC, with recent analyses of

biomass fuel supply plans in support of investments in bioenergy production. Specific to

this assessment, the author has outlined all relevant experience:

• Completed three assessments of the forest industry in Fort Nelson and potential

for economic development, prepared between 2010 and 2017 for BC Hydro, to

facilitate future estimates for the demand for incremental electrical power.

• Completed a review of the birch resource for a First Nations client in 2015/2016,

to assess utilization feasibility.

• Completed a review of the birch resource near Fort Nelson in 1995 and again in

2003 for confidential clients.

• Completed a timber supply analysis of the deciduous resources in the Fort Nelson

TSA in 1993 in support of the development of a Chopstick Manufacturing facility.

1 http://www.industrialforestry.ca

Industrial Forestry Service Ltd., Prince George, BC, Canada

2 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

• Completed a delivered log cost analysis of the forest resources in the Fort Nelson

TSA in 1991 and again in 1998 for the BC Ministry of Forests.

• Completed a 20-year harvest plan of BC Timber Sales operating areas within the

Fort Nelson TSA in 2008, to facilitate forest development planning.

• Completed timber supply analyses of the forest inventory in the Fort Nelson TSA

for government and industry between 2001 and 2010.

• Managed and provided annual updates to software used by the forest industry and

BC Government in Fort Nelson, to determine pre-harvest timber volumes (Cruise

Compilations) and to calculate government stumpage.

• Contracted by government to conduct aerial overview surveys of the Fort Nelson

TSA for forest health, annually between 2011 and 2017.

1.3 Data Sources

To prepare this report we reviewed the following material:

• BC Ministry of Forests, Lands, Natural Resource Operations and Rural

Development (“FLNRORD”) web site and publicly available data. Most of this data

is publically available at https://catalogue.data.gov.bc.ca/dataset/

• Industry publications and data.

• FLNRORD analysis reports specific to the Fort Nelson Region, available at

http://www.for.gov.bc.ca/mof/branches.htm

• Media articles.

• Company web sites and annual reports.

• Industrial Forestry Service Ltd. internal models and reports.

Additional independent work was completed by Industrial Forestry Service Ltd. to clarify

and verify data. This work involved:

1. Creation of a spatially explicit Geographic Information System computer model to

assess forest inventory attributes that currently exist within the Fort Nelson TSA.

2. Utilized FLNRORD reports and additional forest inventory data to program and

spatially recreate the timber harvesting land base for the Fort Nelson TSA.

3. Utilized cycle time information developed by IFS in 1998 at the region compartment

level to facilitate development of a delivered wood cost model to determine the

weighted-average cost to deliver logs to Fort Nelson.

Industrial Forestry Service Ltd., Prince George, BC, Canada

3 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

4. Reviewed ministerial documents that pertained to the probable future direction of

government policy regarding hardwoods in the Fort Nelson TSA.

1.4 Terminology

The following abbreviations and industry terms are used in the report:

AAC - Allowable Annual Cut – the maximum annual harvest for a TSA set by the Provincial

Chief Forester every 5 to 10 years, after consideration of social (i.e., visual quality and

recreation), economic and biological concerns. In this report AAC is also used in reference

to the annual apportionment of Crown Timber volume in a TSA to the holder of a forest

licence.

BC – British Columbia.

BCTS - British Columbia Timber Sales – a Crown corporation mandated with the sale of

public timber for consumers in order to help establish a market price for the sale of logs to

all tenure holders in a given TSA. Approximately 20% of the BC harvest is auctioned by

BCTS each year.

BC Hydro - British Columbia Hydro and Power Authority (a Crown utility) - the majority of

electricity in BC is generated at hydroelectric dams.

Crown Licence - A legal agreement between the BC Government and an individual or

company to harvest timber on public (Crown) lands.

Cycle Time - The total time required to travel from the mill site to the harvesting site, load

a truck with logs, return to the mill site and unload the logs.

FLNRORD - BC Ministry of Forests, Lands, Natural Resource Operations and Rural

Development – also called the Forest Service, this is the BC Government agency

responsible for forest management.

Hectare - a metric unit of area equal to 2.47 acres.

Hembal - Balsam fir and hemlock tree species commonly found together on the BC Coast

Hog Fuel - a term used to describe tree bark that has been processed through a "hogger",

which grinds the wood into uniform chunks.

IFS - Industrial Forestry Service Ltd., the author of this report.

Km - Kilometre. a metric unit of distance equal to 0.62 miles.

Lumber - The final sawmill product.

Industrial Forestry Service Ltd., Prince George, BC, Canada

4 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

m3 - Cubic metre. A common metric volume measure used to quantify the harvest of logs

in BC. There are 423.7 board feet and 35.3 cubic feet in one cubic metre.

Merchantable Timber - trees of a size suitable for the production of lumber. In BC the AAC

is based upon the harvest of merchantable timber.

MFBM - Thousand foot board measure – industry measurement used to quantify lumber

production.

MPB - Mountain Pine Beetle - an insect that kills lodgepole pine trees, which are a principle

commercial tree species found in the BC interior.

NRFL – Non replaceable forest licence. A short-term licence, typically from 5 to 10 years

that provides a tenure holder with the right to harvest timber, subject to various conditions.

ODT - Oven dry tonne - equal to 1000 kilograms or 2,204 pounds of biomass dried to zero

percent moisture and approximately equal to 2.44m3 of timber.

Province - the Province of British Columbia.

RFL - Replaceable Forest Licence – a long-term perpetually renewable harvesting licence.

Sawmill Residues - Term used to describe Sawdust, Shavings, Chips, Trim Blocks and

Hog Fuel that are co-produced during the production of lumber from sawlogs.

SPF - Spruce, pine, fir - a term applied to lumber that is produced in Western Canada and

typically used for house construction.

Stem - The bole of a tree.

Stumpage - Revenue collected by the provincial government in exchange for a prescribed

amount of Crown timber that is “on the stump”. Stumpage does not include harvesting or

delivery costs.

TSA - or Timber Supply Area, a geographic administrative boundary (typically 1 million to

10 million hectares in size) and used to derive AACs and allocate Crown licences.

TSL - Timber Sale Licence - A timber licence issued under auction by BCTS.

Note regarding use of measurement: The most common units of volume measure used

throughout this report are cubic metre (m3) and oven dry tonne (ODT). Cubic metre is used

in BC to define the volume of standing timber that a company can harvest. ODT is used

in BC to define the weight of sawmill residuals such as Sawdust, Shavings, Chips and

Hog fuel.

Industrial Forestry Service Ltd., Prince George, BC, Canada

5 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

2.0 The Forest Industry in BC in General

2.1 Land Ownership / Forest Management Units

Almost 60 million hectares, representing two-thirds of the land base in BC, is forested.

Most of this land (i.e., 94%) is publicly owned, which means that the lands are held by the

Government in the name of the monarch and are called Crown Lands. The Crown

transfers specific rights to tenure holders to use Crown forest land and its resources

through various tenure arrangements. The form, extent and duration of these rights and

attendant management responsibilities vary with each tenure agreement.

Timber tenure agreements prescribe how, and to whom, rights to timber will be awarded

and the related price(s) and responsibilities.

The Province of BC is divided into many distinct geographic units for forest management

purposes. All forest licences are tied to a geographic area. The largest of these

management units is a Timber Supply Area (TSA). There are 37 TSAs distributed

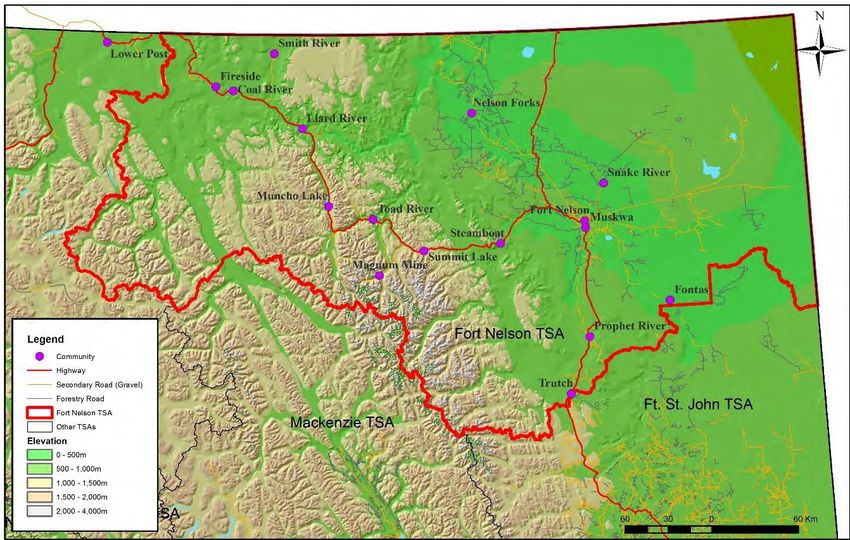

throughout BC. The Fort Nelson TSA is the northeastern most TSA within the Province.

Map 2 depicts some of the topography and location of communities within the Fort Nelson

TSA.

Map 2: Fort Nelson TSA

Industrial Forestry Service Ltd., Prince George, BC, Canada

6 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

2.2 Regulatory Environment

The right to harvest and extract wood from Crown Land in the Province of British Columbia

requires a timber tenure from the BC Ministry of Forests, Lands, Natural Resource

Operations and Rural Development (FLNRORD). Specific to Fort Nelson, a district office

is serviced by a small staff of government officials. The activities related to forests in BC

are controlled through several statutes and many regulations. Principle among these are:

(i) the BC Forest Act, which primarily describes the forest licence/tenure conditions and

general provisions associated with licences, such as payments, transfers, timber scaling,

cut control and regulations; and (ii) the Forest and Range Practices Act, which outlines

how all forestry practices are to be conducted on Crown Land in BC.

In 2018, the FLNRORD has a hierarchal structure with Forest Minister Doug Donaldson

currently the elected official leading the Ministry. Tim Sheldan is the senior Deputy Minister

dealing with forest policy. The province is divided into three areas of operation – Northeast,

Omineca and Coast. Karrilyn Vince is the current Regional Executive Director (RED) of

the Forest Service in the Northeast. Reporting to each of the RED’s are district managers

with staff responsible for the daily operations of the forest service. The Provincial Chief

Forester, Diane Nicolls, reports to the Deputy Minister providing guidance and direction

on forest stewardship and determining the level of harvest within each timber supply area.

2.3 Tenure System

Timber tenures can take the form of an agreement, a licence or a permit. Each is a legally

binding contract that provides the holder with specific rights to use the public forest over

a specified time period in exchange for meeting various government objectives (including

forest management) and payment of fees (including stumpage). There are over a dozen

different kinds of tenure, each having different terms, restrictions and contractual

obligations. The six primary timber tenures relevant to the Fort Nelson TSA are described

in Table 1.

Industrial Forestry Service Ltd., Prince George, BC, Canada

7 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

Table 1: Access to Crown Timber

Revenue to

Licences Rights Duration Responsibility

the Crown1

Grants the right to harvest

part of an AAC within a 20 years,

Replaceable Forest Protection, Forest

TSA. Typically must

replaced Stumpage, Stewardship Plan, operational

Forest Licence coordinate harvest with

other licensees also every 5 to 10 annual rent planning, road building,

(RFL) reforestation.

having volume rights years

within the same TSA

Grants the right to harvest

Non- part of an AAC within a

Up to 20 Stumpage, Forest Protection, Forest

TSA. Typically must

Replaceable bonus offer, Stewardship Plan, operational

coordinate harvest with years, not

Forest Licence other licensees also

bonus bid, planning, road building,

replaced annual rent reforestation.

(NRFL) having volume rights

within the same TSA

Grants a conditional right Up to 25 Operational planning,

to harvest “pulp quality

Pulpwood years BUT no Stumpage, obligation to maintain a timber

timber” where other

Agreement sources are insufficient or longer being annual rent processing facility,

issued reforestation

uneconomic.

Grants the right to harvest

a volume of timber from a Stumpage,

Timber Sale specified area within a bonus offer,

Up to 4 years Forest Protection

Licence (TSL) TSA. Issued only by BCTS bonus bid,

(government) under annual rent

auction.

Greater than

25 and less Forest Protection, Forest

Community Grants the exclusive right Stewardship Plan, road

than 99 yrs; Stumpage,

Forest to harvest an AAC within a building, strategic and

specified area replaced annual rent

operational planning, forest

Agreement

every 10 inventories, reforestation

years

Greater than

25 and less Forest Protection, Forest

First Nations Grants the exclusive right Stewardship Plan, road

than 99 yrs; Stumpage,

Woodland to harvest an AAC within a building, strategic and

specified area replaced annual rent

operational planning,

Licence

every 10 inventories, reforestation

years

Note: 1. A Bonus Offer is a lump sum amount, in addition to the total amount of stumpage that is tendered to acquire the

right to harvest Crown Timber under a TSL or NRFL. A Bonus Bid is a cubic metre amount that is tendered and is payable

upon the harvest of merchantable timber under the licence.

2.4 The “Open Market” - BC Timber Sales

BC Timber Sales (BCTS) is a division of the BC government that is mandated to provide

cost and price benchmarks for timber harvested from public land in BC. They accomplish

this through public auctions of Timber Sale Licences (TSLs) to the highest bidder after

performing the required administrative and pre-harvest planning. BCTS manages

approximately 20% of the provincial Crown Allowable Annual Cut that is distributed in

operating areas throughout the province. Each of these operating areas were selected

based on having characteristics that were representative of the larger Timber Supply Area

(TSA) within which they exist.

Industrial Forestry Service Ltd., Prince George, BC, Canada

8 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

The TSLs range between 10,000 and 200,000 cubic metres. The buyer of a TSL pays a

bid fee and earns the short-term (4 year) right to access this timber at the buyers

convenience.

2.5 Log Markets

The occurrence of private woodlots, Crown woodlots, community forests, First Nations

woodland licences, various forms of licence-to-cut tenures and BCTS means that a

substantial amount of the volume of logs harvested across BC is sold to sawmills and

pulp mills through arms-length transactions. The BC government requires that all

sawmills, pulp mills, plywood plants, OSB plants, pellet plants, and specialty mill log

purchasers report all arm’s length log purchase transactions for logs originating in the BC

Interior for consumption within the BC Interior. An “arm’s length transaction” is defined as

a sale involving two parties who are independent of each other. The purchase price is in

dollars per cubic metre (including stumpage, bonus and penalties) in Canadian dollars

FOB mill. This information must be submitted monthly. In the Interior, where private lands

and woodlots are relatively minor compared to the harvest by BCTS, most of the log

market purchases would have in fact been BCTS TSLs that a market logger bid on with

the intent to sell the logs to a log processing facility.

The government produces both Interior and Coastal log market reports on a monthly and

three-month basis. The reports detail volume (in cubic metres) by product (e.g. sawlog,

peelers, pulpwood) by tree species group (e.g. deciduous, SPF, hembal etc), and average

price ($/m3) for each product and species group.

The 3-month change in the historic price of deciduous logs sold and delivered in the BC

interior is shown in Figure 1. As can be seen in Figure 1, many periods have no data. To

ensure that individual company confidential information is not disclosed, the government

restricts publishing data when less than 3-companies report.

Also seen in Figure 1, the average price of deciduous logs for the past 10 years has been

between $35 and $40 per cubic metre.

The author speculates that the majority of these third-party transactions would have

occurred between private land owners and Louisiana Pacific in the Dawson Creek and

Fort St. John Timber Supply Areas.

Industrial Forestry Service Ltd., Prince George, BC, Canada

9 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

Figure 1: BC Interior Deciduous Log Market

300000 50

Weighted-Average Selling Price ($/m3)

3-month Volume Sold (cubic metres)

45

250000

40

35

200000

30

150000 25

20

100000

15

10

50000

5

0 0

Sep-09

Sep-10

Sep-11

Sep-12

Sep-13

Sep-14

Sep-15

Sep-16

Sep-17

Mar-09

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Date

3-month volume $/cubic metre

Source: BC Interior Log Market Reports, www2.gov.bc.ca

2.6 Regulating the Harvest

British Columbia carefully regulates the amount of timber that may be harvested each

year. The amount of timber that can be harvested in a specified area of land is known as

the Allowable Annual Cut (AAC). Each TSA has a designated AAC that is determined by

the Provincial Chief Forester. After the AAC is determined, the Minister of Forests

apportions the volume to licensees operating within a TSA, such that the sum of the

apportioned volume does not exceed the AAC for that TSA. On an annual basis, a licensee

can exceed their annual apportionment subject to the terms of the Cut Control Regulation.

Typically, cut-control is measured over a 5-year period and a licensee’s cumulative

harvest should be within 10% of their 5-year apportionment, otherwise over-cut or

undercut penalties may be applied.

2.7 Government Fees (Stumpage)

Tenure related fees include: (i) annual rent, (ii) stumpage, and (iii) waste assessments.

Industrial Forestry Service Ltd., Prince George, BC, Canada

10 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

Annual Rent

Annual rent is $0.37 per cubic metre of AAC for Forest Licences, and must be paid

annually to the government.

Stumpage

Stumpage is a fee paid by forest licensees to the Provincial government for timber

harvested from Crown Land.

Stumpage rates for deciduous “sawlogs” within BC are fixed at a flat rate of $0.50 per

cubic metre and are payable to government only upon harvesting. Lower grade deciduous

logs are either $0.25 per cubic metre or have no stumpage applied.

Stumpage rates for coniferous species vary depending on the volume of deciduous within

the stand. If the coniferous volume comes from the harvest of stands where the volume is

incidental (i.e., less than 30% of the stand volume is coniferous and greater than 70% is

deciduous) then the conifer stumpage is a tabular rate that is updated periodically. At the

present time (March 2018) this rate is $4.14 per cubic metre of coniferous sawlog

harvested from the Fort Nelson TSA. In a strong competitive market, this rate could climb

to $25 per cubic metre.

Stumpage fees on coniferous sawlogs, where the deciduous volume is less than 70%, is

pre-determined and a reflection of many factors including market value, tree species,

wood quality and harvesting costs. Stumpage rates for conifer logs can range from $0.25

per cubic metre to $80 or more per cubic metre. Within the adjacent southern Fort St John

Timber Supply Area, conifer stumpage rates have varied between $0.25 and $65 in the

past 12 months. The average rate was $4.14 per cubic metre.

Waste Assessments

Waste assessments are payable to government when it is determined that merchantable

Crown timber (whether standing or felled and that is not reserved from cutting) remains

on site upon completion of logging a cut block. The fee is based on the grade and

stumpage value of the timber, had it been delivered at the completion date of primary

logging.

Industrial Forestry Service Ltd., Prince George, BC, Canada

11 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

2.8 Allowable Annual Cuts

The Allowable Annual Cut for each Timber Supply Area is determined by the Province’s

Chief Forester. The determination is made in consideration of: (i) the composition and rate

of growth of the forest, (ii) the short and long term implication to BC of alternative rates of

harvest, (iii) the economic and social objectives of the government, and (iv) abnormal

infestations and major salvage programs.

Many of the TSAs in the BC Interior have had AAC uplifts applied in the early and mid-

2000’s to facilitate the salvage of pine trees that were killed by a massive mountain pine

beetle epidemic. In almost all Interior management units this salvage program is effectively

complete and the AACs in most Interior TSAs are in the process of being reduced.

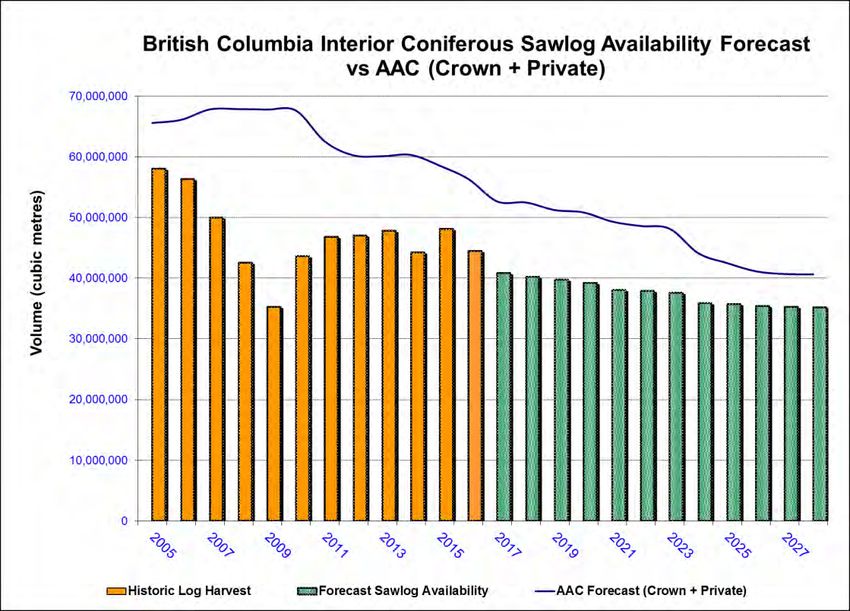

Figure 2 shows both the historic and forecast AAC for the BC Interior, as well as historic

sawlog utilization and forecast sawlog supply from within the AAC. As can be seen in

Figure 2, the Interior AAC has been declining steadily since 2010. The gold bars,

representing historic log harvests have been significantly below the AAC, in part due to

the recession commencing in 2008, and in part due to sawmills inability to process all of

the available timber resulting from the AAC uplifts. As the AAC continues to decline, the

future AAC will stabilize at about 40 million cubic metres. The green bars reflect the

coniferous sawlog component within the AAC, and the gap between the AAC and the

green bars reflects the availability of sawlogs. By 2028, sawlog availability is forecast to

be about 35 million cubic metres annually. This is below the 2017 utilization of BC Interior

mills, which consumed about 41 million cubic metres of timber in 2017.

Industrial Forestry Service Ltd., Prince George, BC, Canada

12 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

Figure 2 BC Interior Historical Harvest and Forecast AAC

Source: BC Fibre Model

2.9 Clarification of Volume Measurements

In BC, log volumes are typically measured in cubic metres (m3), and weights are in Oven

Dry Tonnes (ODT) or Bone Dry Tonnes (BDT). A cubic metre is 35.3 cubic feet or 423.8

board feet – assuming a straight solid wood conversion and ignoring lumber recovery

factors.

Although AACs are expressed in cubic metres, additional clarity is required since the cubic

metres assigned in an AAC are at a defined “close” utilization level and net of decay waste

and breakage. The close utilization levels of a merchantable tree are typically defined as:

• a 30 centimeter (cm) stump height.

• 17.5 cm or greater diameter out-side of the bark when measured 1.3 metres above

ground (“breast height”) for all species except pine. Pine diameters are typically

12.5 cm or greater at breast height.

• A 10 cm top diameter measured inside the bark.

Industrial Forestry Service Ltd., Prince George, BC, Canada

13 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

• Volume measurements associated with these utilization factors are described in

a program produced by the BC government. Volumes are derived using taper

equations and in consideration of stand basal area, stand height and average

diameter.2

Close utilization typically results in a 6% reduction from the whole stem volume. Additional

volume adjustments are subsequently applied in consideration for log decay, waste and

breakage. These adjustments vary by species, stem diameter, stand age, are based upon

historic measurements taken with a sawlog / lumber production objective in mind. The

volume-weighted average adjustments for decay, waste and breakage for mature aspen

(hardwoods) and mature spruce (softwoods) in the Fort Nelson TSA are shown in Table

2.

Table 2: Conversion from Whole Stem to Merchantable Volume

Weighted-average percent reduction to determine

Volume Measure merchantable volume

Aspen Spruce

Whole Stem 0% 0%

Close Utilization 6% 6%

Decay 18% 3%

Waste 5% 1%

Breakage 5% 1%

Total Adjustment 34% 11%

Understanding these adjustments is relevant to log utilization. Hardwood logs that are

consumed for lumber need to be of higher quality than logs consumed to make OSB

stands. An AAC of 1 million cubic metres of aspen, based on close utilization and volumes

net of decay, waste and breakage, would in fact yield more cubic metres equivalent of

OSB strands, under the assumption that the decay values overstate desired fibre quality.

2 See https://www2.gov.bc.ca/gov/content/industry/forestry/managing-our-forest-resources/forest-

inventory/growth-and-yield-modelling/variable-density-yield-projection-vdyp/growth-relationships-and-model-

components

Industrial Forestry Service Ltd., Prince George, BC, Canada

14 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

In this report, all volumes are reported as close utilization and are net of decay, waste and

breakage.

2.10 Conclusions regarding the Forest Industry in BC

• Access to timber is facilitated through agreements (tenures) with the Provincial

government. There are several forms of tenure that vary with respect to duration

and responsibilities. Each tenure is specific to one management unit, such as a

Timber Supply Area.

• The primary unit of log measurement is cubic metre. Cubic metre measurements

are adjusted for decay, waste and breakage. The weighted-average adjustment

for deciduous trees in the Fort Nelson Timber Supply Area is 34% (i.e. each

cubic metre of standing hardwood timber in a stand is reduced 34%, on average,

to derive net merchantable volume).

• The BC Timber Sales program exists province wide and auctions compose

approximately 20% of the Provincial Allowable Annual Cut.

• Open log markets exist in BC and information regarding volume and price is

provided to government. The average BC interior log price for hardwoods has

ranged from $35 to $40 per cubic metre over the past 10 years

• The AAC is determined and regulated by government.

• AACs across most of the BC interior are declining.

• Stumpage for deciduous timbers are $0.50 per cubic metre and for lower quality

deciduous logs, $0.25 per cubic metre.

3.0 Fort Nelson TSA Log Supply and Apportionment

In BC timber supply areas, log supply is determined by the Provincial Chief Forester

through the determination of an Allowable Annual Cut. This determination is made every

5 to 10 years. Once an AAC is determined, the Forest Minister apportions the AAC.

Industrial Forestry Service Ltd., Prince George, BC, Canada

15 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

3.1 The Fort Nelson TSA - AAC

The Fort Nelson TSA’s AAC, from 1990 to 2017, is shown in Figure 3. Prior to 1995, the

AAC was 1 million cubic metres and contained a partition separating the utilization of

hardwood and softwood species. In 1995, the AAC was increased to 1.5 million cubic

metres with a reduction to the softwood partition and an increase in the hardwood partition.

In 2006, the AAC was increased to 1.625 million cubic metres and the partition was

removed.

The AAC has remained at 1.625 million cubic metres since 2006. As indicated previously,

AACs are due to be reviewed and re-determined every 5 to 10 years. The AAC

determination for the Fort Nelson TSA is overdue. It is the author’s understanding that the

government is currently conducting a timber supply analysis of the Fort Nelson TSA and

anticipates a determination in early 2019.

Figure 3 provides some magnitude of what a potential future AAC for the Fort Nelson TSA

may be. A high and low scenario are depicted in consideration of several factors:

1) In 2006, a timber supply analysis of the TSA suggested that the harvest level could

be increased to 3.1 million cubic metres (much higher than the historic level). The

2006 analysis suggested that a partition of 1.7 million cubic metres for conifer and

1.4 million cubic metres for deciduous species could be maintained indefinitely.

The Chief Forester did not increase the AAC to this level, due primarily to

uncertainty around (i) the extensive future utilization of lower volume deciduous

stands, and (ii) the future utilization of marginally economic stands located in the

western most portions of the TSA.

2) The Fort Nelson TSA, due to its location, lack of pine, and cold winter

temperatures, has not been impacted by the mountain pine beetle epidemic.

Barring the changes to the Fort Nelson TSA boundaries, it is expected that, unlike

many other TSAs in the BC Interior, the AAC for the Fort Nelson TSA should

remain relatively stable.

3) The TSA currently includes “core” caribou habitat areas. It is probable that future

harvesting in these areas will be prohibited. This would reduce the timber

harvesting land base by about 14% and likely have a similar impact on the AAC.

Industrial Forestry Service Ltd., Prince George, BC, Canada

16 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

4) The TSA currently does not have legislated direction regarding Caribou “range

management”. It is expected that harvesting restrictions may reduce the amount

of future harvesting that can occur in these range areas. The author’s professional

opinion is that these harvesting restrictions will constrain the AAC by an additional

12%.

5) The final AAC for the TSA will likely be reduced for the creation of a new community

forest and new First Nations Woodland licences. Combined these reductions

would reduce the TSA’s AAC by approximately 210,000 cubic metres. The areas

supporting this 210,000 cubic metres would be removed from the TSA and

allocated to two new forest management units. However, the wood supply would

still be contained within the region. It would just be apportioned to the community

and local First Nations and they would decide how to utilize the available harvest

volume (i.e. develop their own processing facility, or more likely, sell the volume

into the market).

As can be seen in Figure 3, there is considerable upside and some small downside to

future AAC determinations. Caribou habitat strategy development will reduce the operable

timber harvesting land base, whereas operational performance in high-cost, low-volume

deciduous stands, or high-cost stands located in the far west portion of the TSA have the

potential to significantly increase future AACs.

Industrial Forestry Service Ltd., Prince George, BC, Canada

17 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

Figure 3: Fort Nelson, Historic AAC, Species Partition and Potential Future AAC

3,000,000

2,500,000

Volume (cubic metres)

Post-2018 Potential

2,000,000 Future Fort Nelson TSA

AAC, high and low

1,500,000 scenarios

1,000,000

Tree species partition

500,000 removed after 2006

0

1990 1995 2000 2005 2010 2015 2020 2025 2030

Conifer Partition Deciduous Parititon

Historic AAC Future AAC high scenario

Future AAC low scenario

3.2 Apportionment of the Fort Nelson AAC

Table 3 describes the volume allocated to each licensee operating within the Fort Nelson

TSA in 2018. The current AAC for the Fort Nelson TSA is 1,625,000 cubic metres per

year.

Table 3: Fort Nelson TSA – 2018 Harvest Apportionment

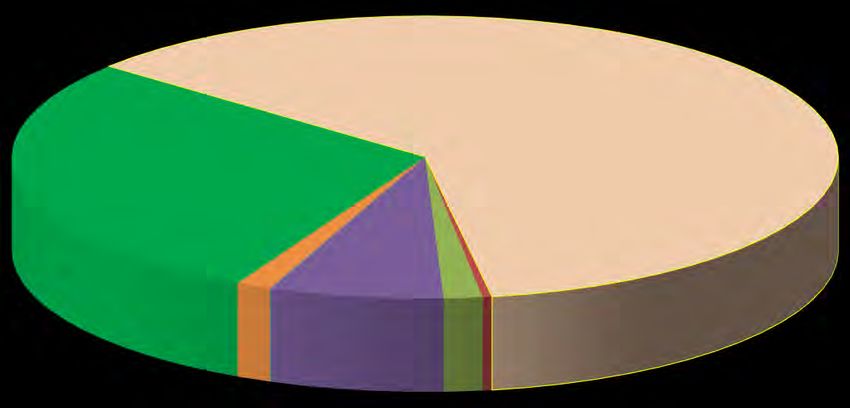

Tenure Type Licensee Total (m3) Percent to Total

Replaceable Forest Licence Canadian Forest 553,716 34%

Forest Licences Non-replaceable Not assigned

Products Ltd 83,000 5%

BC Timber Sales BC Timber Sales 299,668 18%

Pulpwood Agreement Canadian Forest 610,000 38%

Community Forest Agreement Products

Not Ltd

assigned 18,000 1%

Forest Service Reserve Not Assigned 60,616 4%

Total All 1,625,000 100%

Canadian Forest Products Ltd. (Canfor) is the predominant licensee within the Fort Nelson

TSA. Canfor possessed volume-based Replaceable Forest Licence (“RFL”). This

Industrial Forestry Service Ltd., Prince George, BC, Canada

18 of 54Review of the Aspen / Hardwood Resources within the Fort Nelson TSA

replaceable (i.e., renewable) form of tenure provides long-term timber security akin to a

perpetual lease. The term of the tenure is guaranteed and the licence will remain in good

standing provided Canfor pays the Crown its annual rent, any calculated stumpage fees

associated with harvesting, and fulfills all of its forest management obligations (e.g.

reforestation treatments).

Canfor also possesses a pulpwood agreement within the Fort Nelson TSA (described

further in Section 3.2.2). This form of tenure is no longer being issued within BC. The

Minister of Forests has indicated that Canfor will lose this tenure when it expires in

December 2019 and it will not be replaced or converted into another type of tenure.

The RFL held by Canfor provides access to 553,716 cubic metres of merchantable timber

each year in the Fort Nelson TSA. Under this licence there is no distinction between

softwood (coniferous) and hardwood (deciduous) utilization. The Pulpwood Agreement

held by Canfor provides access to 610,000 cubic metres per year of deciduous-leading

timber stands within the TSA.

3.2.1 BCTS Apportionment

BCTS has a current apportionment of just under 300,000 cubic metres per year in the Fort

Nelson TSA.

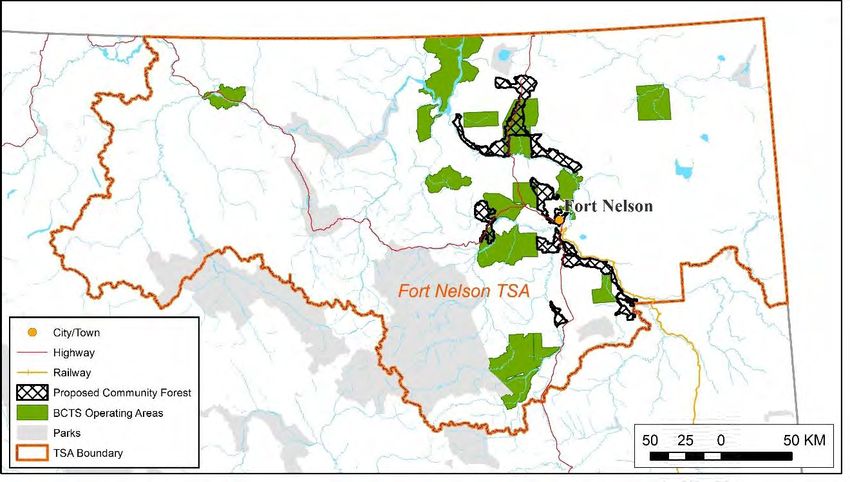

The BCTS operating areas closest to Fort Nelson are represented by the dark green color

in Map 3.

The presence of BCTS operating areas in close proximity to Fort Nelson provides a forest

licensee operating in the TSA with the opportunity to acquire timber supply through the

BCTS auction program.

Industrial Forestry Service Ltd., Prince George, BC, Canada

19 of 54You can also read