ACCOUNTANT GENERAL (A&E) HIMACHAL PRADESH SHIMLA-171003 - OFFICE OF THE MANUAL OF

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

For use of A&E Office only

OFFICE OF THE

ACCOUNTANT GENERAL (A&E)

HIMACHAL PRADESH SHIMLA-171003

MANUAL OF THE

PROVIDENT FUND SECTIONS

Issued by

Accountant General (A&E) H.P.

SHIMLA-171003

1

OFFICE OF THE ACCOUNTANT GENERAL (A&E)

HIMACHAL PRADESH SHIMLA-171003

GPF MODULE INDEX

TABLE OF CONTENTS

CHAPTER I-CONSTITUTION, CONTROL AND DISTRIBUTION OF WORK

Sr. No. Particulars PARAGRAPH PAGE

1 Nature of work, Constitution and 1-3 2-7

distribution of work

2 General instructions on work 4 7-11

allocation, Closing of Accounts,

Admission, Final Withdrawal/TOB,

Clearance of Missing Credits previous

year/current year, misc. works etc., &

closing of Register

CHAPTER-II PROCEDURE AND MAINTENANCE OF ACCOUNT

Sl.No. Particulars PARAGRAPH PAGE

1 Institution of General Provident Fund 1 12

2 Interpretation of Rules 2 12

3 Eligibility of Intending Subscribers 3 12

4 Allotment of Account Number 4 13

5 Logon Screen - 14

6 Main Menu Screen - 15

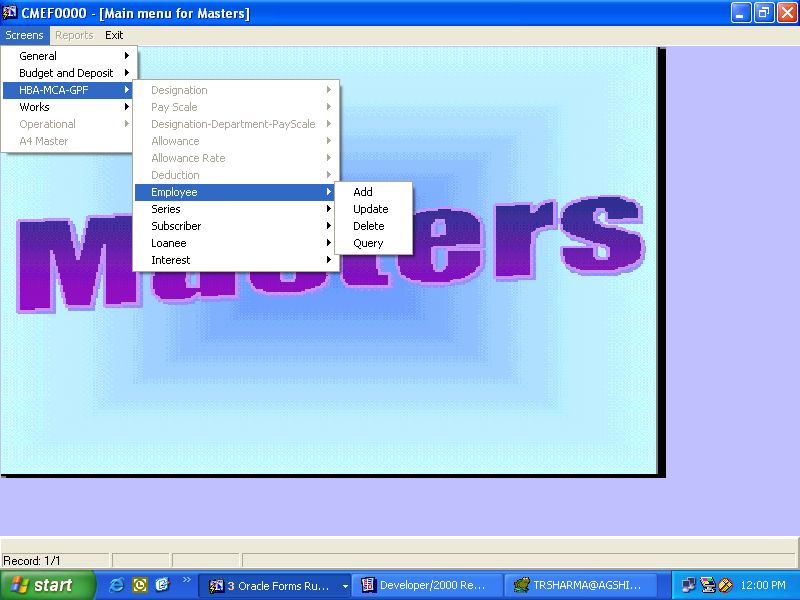

7 Master Screen - 16

8 Screen for Add New Employees - 17

9 Screen for Update Subscriber 18

10 Query Screen of Series - 19

11 Screen for Subscriber - 20

12 General Index Register 5 21

13 Alphabetical Index Register 6 21

14 Nominations 7 22-23

15 Arrangement of Leger Card 8 24

16 Posting of Accounts 9 24

17 Screen for Voucher Posting, Credit - 25

Posting, Debit Posting, Suspense entry,

Sanction entry, Abstract Creation and

Closure of Abstract etc.

18 Screen for query on New Abstract 26

19 Screen for Creation of Voucher - 27

20 Query Screen of Voucher/Challan - 28

21 Screen for Credit Posting - 29

22 Screen for Updating of Credit Posting - 30

23 Screen for add New Subscriber for - 31

Transfer(Transfer of balance from one

series to another)

24 Screen for add New Abstract for - 32

Suspense Clearance)

25 Screen for Query on Suspense - 33

26 Screen for Debit Voucher Creation - 34

27 Screen for Posting of Debit Sanctions - 35

28 Sanction Screen - 36

29 Screen for Posting of Debits - 37

30 Screen of update of Debit Postings - 38

31 Screen for query on Abstract Closure 39

32 Schedules of deduction from Pay Bills 10-11 40-43

33 Staff sanction for forming Peripatetic 12 43-44

Parties

34 Cash Recoveries and other Credits 13 44-45

35 Withdrawals 14 45

36 Consignment of Vouchers 15 39-40

37 Unposted Items 16 46

38 Register of Missing 17 46-48

Credits and Debits

39 Annual Closing 18 48-49

40 Statement of Subscriber Account 19 49

41 Collateral Evidence 20 49-50

42 Calculation of Interest 21 50-51

43 Incentive Bonus Scheme 22 52-53

44 Period of Non-Withdrawal reduced to 23 53

three years

45 Incentive Bonus Scheme for 24 54

subscribers to GPF(Central Services)

46 Incentive Bonus Scheme for P.F. 25 54-56

Subscribers

47 Adjustment of Interest 26 56-57

48 Final Withdrawals 27 57-59

49 Procedure for Final Payment in case of 28 59

Death of Subscriber

50 Payment in the absence of Natural Heir 29 59

51 Payment on the disappearance of a 30 60

Subscriber

52 Payment outside the state 31 60

Subject:- Preparation of Manual of GPF Module.

As per instructions of the Hqrs Office, manual of GPF

module has been prepared and placed below for approval of the Deputy

Accountant General (Funds).

We may, if approved, also sent a copy of the manual to Audit

Office for vetting/checking. Draft letter in this regard is also added for favour of

approval please.

Submitted please.

S.O./Fds-1

Sr.A.O/Fds-1

Office of the Sr. Deputy Accountant General (A&E)

Himachal Pradesh Shimla-171003

No:-Fund-1/GPF Manual/2007-08/1098 Dated:-25-10-2007

To

Sr. Audit Officer,

I T Audit cum EDP Cell

O/o the Accountant General (Audit)

Himachal Pradesh Shimla-171003

Subject:- Vetting of Procedural Manual of GPF Module

Sir,

I am directed to enclose a copy of procedural manual of

GPF Module prepared by this office as per directions of Hqrs Office for

vetting.

This issue with the approval of DAG (Funds)

Encl:-As aboe Yours faithfully,

Sr. Accounts Officer

PREFACE

Consequent upon introduction of GPF computersization in the office of the

Accountant General (A&E), Himachal Pradesh, Shimla this is the first procedural manual

of General Provident Fund incorporating various activities of Department. Codal

provisions and accounting concepts were kept in view while finalizing this module.

2. Fund-1 Section will be responsible for keeping the manual upto date as also for

ensuring that all orders, instructions, modifications etc. in future are incorporated in the

Manual with care and promptitude by way of issue of correction slips.

3. Any error and omission noticed in this manual and also suggestions for its

improvement may be brought to the notice of the Fund-1 Section of this office.

Accountant General (A&E)

GPF

Manual

Office of the Accountant General (A&E)

H.P. Shimla-171003

Subject:- Procedural Manual of GPF Module

Procedural manual of GPF module sent to Audit Office i.e. I T Audit

cum EDP Cell vide this office letter No.Fnd-1/GPF Manual/2007-08/1098 dated 25-10-

2007 was received back vide AG (Audit) letter No.IT/EDP/AU/30/VLC Manual/2007-

08/597 dated 05-12-2007 with certain observations.

The observations have been attended and the changes/corrections advised

by Audit Office have been incorporated and revised printout of GPF Manual has been

taken. After vetting of the Manual by the Audit Office the same is to be got vetted by the

IT Auditor. As per Hqrs Office instructions, the Group Officer holding the charge of

Accounts and VLC were to be nominated as IT Security Manager by the Head of the

Office. As such Deputy Accountant General holding the charge of Accounts and VLC

were got nominated as Security Manager by the Establishment –II Section.

As the GPF Manual which has been vetted by the Audit Office is also be

vetted by the IT Auditor, the same is submitted for vetting to the I.T. Auditor i.e. Dy.

Accountant General (A/Cs & VLC).Submitted Please.

SO/Fds-1

Sr.AO/Fds-1

ubject:- Procedural Manual of GPF Module

Note at Pages 1/N to 4/N may also kindly be glanced through.

The Procedural Manual of GPF Module has been prepared by the Fund-1

Section and has been vetted by the I T Audit cum EDP cell, of the Office of the Pr.

Accountant General(Audit) H.P.Shimla-3 and IT Auditor i.e. Dy. Accountant

General(Accounts & VLC). The corrections pointed out by the IT Audit cum EDP cell

and IT Auditor have been carried out and the revised print has been taken. Index and

Preface has been prepared and attached with the Manual. The Manual is submitted for

signatures by the worthy Accountant General (A&E).

Submitted please.

SO/Fds-1

Sr.AO/Fds-1CHAPTER –I

1. Nature of work

The work of Funds Group consists (i) maintenance of Provident

Fund accounts,(ii) issue of Annual Account Statements and (iii) authorization of

Final withdrawals. Sr. Dy. Accountant General maintains the accounts of (a) the

General Provident Fund H.P. State Govt. Employees and (b) All India Service

Provident Fund of H.P. Cadre.

2. Constitution

Funds Group is divided into GPF Sections and Funds Library.

Fund-1 Section controls and co-ordinates the work of other GPF sections.

GPF accounts are maintained in Computer from 2002-03 Accounts.

GPF sections attend to all items of work regarding maintenance of GPF accounts

started from the admission of the subscribers to the Fund, till final closure of their

accounts. Each section is supervised by an Assistant Accounts Officer(AAO) or

Section Officer(SO) or Supervisor. The sections are under the immediate charge of

Assistant Accountant General or Senior Accounts Officer or Accounts Officer.

3. Duties

Important items of work to be attended to by each section of Fund

Group include the following:

a) Fund-1 Section:-

(i) Maintenance of GPF Accounts of All India Service Officers of H.P.

cadre.

(ii) Co-ordination work and all general matter relating to entire Group.

(iii) Distribution of work between the sections of Funds Wing.

(iv) Consolidation and submission of periodical reports/returns to the

authorities within the office/outside the office and Hqrs office.

(v) Preparation of staff proposal and Budget estimates.

(vi) Upkeep of Fund Library and ensuring prompt supply of ledger cards

to the Fund sections.

(vii) Issue of General Circulars, Office orders etc.

(viii) Examination of important cases/ references received from other

sections in the Group.

2(ix) Attending to write off proposals for the adjustments made on

collateral evidence and on affidavit basis sent by the sections.

(x) Maintenance of PF Suspense Broadsheet.

(xi) Drawing up and circulation to the Fund sections of the programme

for posting of Debit/ Credit, closing of accounts and issue of Annual

Account Statements

(xii) Maintenance and updating the model Calendar of Return GPF Rules

and this Manual.

(xiii) Finalization of Honorarium claims of Funds Wing.

(xiv) Collection of statistics and submission of Fair Index.

(xv) Annual adjustment of interest based on actuals before close of

March (sy) accounts.

(xvi) Furnishing report on Review of Balances to Book Section.

(xvii) Preparation of annual indent for standard forms.

(xviii) Follow up action on ITAs Triennial Review and Test Audit Reports

and Director of Inspection’s report etc.

(xix) Marking of disputed letters to the sections concerned within the

Group.

(xx) Any other work allotted by Branch Officer/Group Officer.

b) GPF Sections

(i) Receipt and check of schedules and vouchers, arranging and

stitching of the same and collecting/calling for wanting items. (Schedules containing

corrections and over-writing should be checked critically. Doubtful cases should be

checked with the schedules of previous/subsequent month)

(ii) Scrutiny of applications for admission to the Fund and allotment of

Account Numbers to the subscribers covered under GPF Rules.

(iii) Scrutiny and maintenance of nominations of GPF subscribers.

(iv) Agreement of balances with booked figures and preparation of

master cards as per approved programme.

(v) Checking of correctness of figures booked by VLC Section.

(vi) Checking and review of credit and debit posting made by Data

Entry Operators (DEOs).

(vii) Handing over of schedules and vouchers to the section concerned

immediately after completion of posting work.

3(viii) Tracing of credits in the schedules for posting the same in the Hand

Posting Register while finalizing FW cases.

(ix) Attending to ITA objections (Triennial review and test audit) and

IAD objections.

(x) Servicing of subscribers with regard to Accounts Slips.

(xi) Maintenance of register (computer printouts) of PFW sanctions.

(xii) Clearance of compensating errors, if any in posting, before

preparation of Annual Accounts Statements.

(xiii) Review of individual accounts and finalization of FW/TOB cases.

(xiv) Registering of FP cases and their status updation in the computer for

IVRS purpose.

(xv) Registering of all GPF sanctions received from the DDOs,

generation of sanction report and tally with the sectional diary/record.

(xvi) Generating all required reports due to the AG, Group Officer, BO

and reports due to Hqs office such as missing credit report/Unposted reports etc.

(xvii) Clearance of Unposted, ‘Full Want’ and ‘Part Want’ items.

(xviii) Issue of authorization for final withdrawals and residual Balance.

(xix) Review and dispatch of annual accounts statements to the

subscribers.

(xx) Consignment of record to the Record Branch /Funds Library.

(xxi) Receiving suspense slips from Account Current sections and

clearing them by means of transfer entries.

(xxii) Ensuring that all adjustments have been carried out and TEs posted.

(xxiii) Generating and dispatch/handing over annual accounts statements to

the representatives of the DDOs after exercising required manual checks.

(xxiv) Attending to all complaints including complaints received through

Subscribers Grievance Cell within the prescribed time limit.

(xxv) Disposal of inward Dak and other correspondence.

(xxvi) Other items of work as entrusted by the BO/Group Officer.

c) Debit Section/Funds-17 Section

(i) Receipt of debit vouchers of GPF from all sources and their posting

i.e. data entry in the computer after exercising all checks required w.r.t. receipt and

agreement of debit vouchers.

4(ii) Receipt and deposits of valuables in respect of GPF contributions.

(iii) Receipt of credits schedules in r/o TE, Cash & Exchange in r/o 104-

AIS and cash, Exchange a/c in r/o 101-GPF and their posting in computer.

(iv) Segregation of debit vouchers treasury wise & serieswise, generation

of lists of debits for validation treasury wise and series wise and their further

transmission to the concerned Funds sections for validation.

(v) Generation of all controlled reports such as report of unposted items,

missing credits, minus balance cases, Master cards(credits &debits),Unit Broadsheets

and Consolidated Broadsheet, Generation of ledger cards and Annual GPF statements

or any other connected work.

(vi) Providing of annual interest figure of GP Fund accumulation to Fund-1

section.

(vii) Providing of booked figures, posted figure and difference

figures(quarterly) to Fund-1 section for workout posting efficiency and further

submission to Hqrs Office.

(viii) Other technical work relating to GPF computerization and IVRS,

technicalities involved in running of various processes, distribution of passwords and

maintenance of secrecy thereof to be looked after by the Branch Officer Incharge

VLC Section.

(ix) Receipt of GPF sanction of all series and there feeding in the computer

and maintenance of records and reports thereof.

d) Electronic Data Processing Cell(VLC)

(i) Maintenance of GPF accounts of State Government employees in

computer files- creating and maintaining Master files, posting of debits and credits

(Regular, TEs and adjustments), carrying out corrections and other related works.

(ii) System maintenance including LAN security.

(iii) Maintenance of Log books, giving and changing of pass words,

creating restriction for users in terms of time, accessibility etc.

(iv) Reporting any hardware problem to the quarter concerned/agencies

and ensuring remedial action.

(v) Co-ordinations with various firms such as NIIT,NIC etc., and Govt.

agencies like CPWD.

(vi) Attending to various problems shooting works.

(vii) Development of computer programmes required for maintenance of

GPF accounts, generating various reports/returns and/or making program

modifications.

5(viii) Checking of system every day to ensure that there are no

unauthorized programmes and computer viruses etc.

(ix) Year end jobs like verifying the correctness of OB with reference to

CB of previous year.

(x) Data management- General maintenance of entire data, keeping

back up files in a separate place/room etc.

(xi) Assessing the annual and periodical requirements of stationery and

other consumables.

(xii) Co-coordinating with GPF Sections’ staff and helping them to take

printouts and view the data.

(xiii) Rectification of compensating errors before closing of annual

accounts.

e) Fund-15 Section

(i) Maintenance of CPS accounts of State Govt. Employees recruited on

or after 15-05-2003 and covered under the CPS scheme .

(ii) Scrutiny of applications for admission to the CPS and allotment of

Account Numbers to the subscribers covered under CPS Rules.

(iii) Scrutiny and maintenance of nominations of CPS subscribers.

(iv) Receipt and check of schedules and vouchers, arranging and stitching

of the same and collecting/calling for wanting items. (Schedules containing

corrections and over-writing should be checked critically. Doubtful cases should be

checked with the schedules of previous/subsequent month)

(v) Receipt of Credit schedules and their posting .

(vi) Preparation, review and dispatch/handing over annual accounts

statements to the representatives of the DDOs after exercising required checks.

f) Funds Libraries

(i) Proper arranging and safe custody of GPF ledger cards in the

libraries.

(ii) Prompt supply of ledger cards to the sections as and when indented

for and watching their return from the sections.

(iii) Maintenance of issue register and their closing on the 5th of every

month for submission to Branch Officer Fund-1 or the Branch Officer of the section

controlling Fund Libraries.

6g) Record Branch

(i) Receipt of records such as schedules/debit vouchers etc. from the funds

section.

(ii) Weeding out the schedules and unwanted records annually for

destruction.

4. General instructions on work allocation

All items of accounting and entitlement work should be distributed among all

the Sr. Accountants /Accountants/DEOs by the AAOs /SOs of the section in such a

way that entire work relating to maintenance of GPF accounts such as admission to

GPF, credit check from the system, debit check of the dump, disposal of FW/RB

cases, clearing of ITAs objections as well as objections raised by the Director of

Inspection and Audit Office etc., adjustment of missing credits/debits and Unposted

items and related correspondence . Sectional head of Computer Cell should assist the

Sectional head of Fund sections in checking the work of DEOs/Poster. Dealing

DEOs/posters will take immediate steps to collect the wanting documents, if any,

from the concerned Compilation Sections/ Treasuries and DDOs. On the whole

DEOs/Posters/dealing Acctts./SOs/AAOs/BOs are accountable in their capacity to the

quality of the accounts maintained by them under the respective suffix/districts

DDOs. Activities and accountability will be as under:

Activity Accountability

(i) Receipt of monthly account of Cr./ Dr. and listing them in the

Schedule Receipt Register and take immediate steps to obtain

wanting schedules/vouchers from the Compilation

sections/Treasury/DDOs after comparison of schedules/vouchers

with abstracts and prepare a list of Full want/Part want items and DEO/Poster

note them in the“wanting schedule register. DEOs should maintain

a register to note correct a/c numbers if wrong a/c numbers are

given in the vouchers and schedules. The DDOs should be

requested to quote correct a/c No’s in future).

(ii) Posting of monthly a/c of Drs./Crs.(including those collected

or received belatedly) and make arrangement of positing with the

abstracts. While posting, the DEO should identify cases of varying DEO

subscription/refund and ascertain reason for the changes

(iii) Clear Part Want/Full Want items by collecting the wanting Sr.Acctt/.DEO

documents from the Compilation Sections/Treasury/DDOs.

(iv) Checking of credit posting by viewing Computer files SA with the

help of DEO

(v) Generate debit dump soon after the posting of debits and hand I/C Funds

over the same to the sections Computer Cell

(vi) Conduct 100% check of debit posting with debit dump SA

7(vii) Make random check and certify correctness of Credit AAO/SO

postings

(viii) Conduct review of debit vouchers(Quantum of review is as AAO/SO/BO

below)

Description AAO/SO B.O.

Vouchers for amounts 100% 5% of vouchers

not exceeding upto Rs.10000 and all

vouchers of FP cases.

Rs.10000

> Rs. 10000 100% 100%

(ix) Carry out credit corrections and debit corrections DEO

b) Closing of Accounts

(i) Post DB figures, generate report on agreement of posting VLC

suffix-wise and district wise every month and hand over one copy

to Fund-1 another copy to the respective section.

(ii) Generation of Unit Broadsheets Debit Section

(iii) Analyse differences of Broadsheets SAs

(iv) Comparison of Error Reports supplied by VLC and the SAs

register of wanting schedules maintained in the sections to

reconcile the correctness of wanting schedules

(v) Printing of Annual Account Statements Debit Section

(vi) Handing over/dispatch of Annual Accounts Statements Fund Sections

c) Admission

(i) Receipt of application through Skelton and other sources, Diarist

diarize them and hand over to the respective SAs

(ii) Allotment of GPF A/C Nos. in the General Index Register SAs

after verify the completeness of details/admissibility required for

new admission, and after the approval of BO, it will be handed

over to poster for feeding in the Computer. Send intimation to the

DDOs concerned alongwith copy of accepted nominations and

previous nominations, if any.

(iii) Placing /keeping accepted nominations/revised nominations SAs

8in the folders in the almirahs under the safe custody of BO.

(iv) Submission of General Index Register to the BO SAs

(v) Arrange the applications and admission forms suffix-wise and SAs

get them stitched in 100s for safe keeping.

(vi) Maintenance of Alphabetical Register. SAs

d) Final Withdrawal /TOB(cases should be distributed equally among all

SAs)

(i) Receipt of applications for FW/TOB from Diary Branch and Diarist

other sources and dairies them in the sectional diaries/Registers

and handing them over to the dealing SAs

(ii) Examine the cases and return the incomplete cases to the SAs

respective DDOs.

(iii) Collect Ledger Cards relating to old period from Library SA SA

and obtain current status from the sectional poster

(iv) Calculation of interest, fill up check memo, questionnaire SA

etc., submit the case to AAO/SO and BO.

(v) Preparation of authorization for approval of the BO and SA

dispatch the same after approval and making entries in the related

register

(vi) Further correspondence, issue of authorization of RB etc. SA

(vii) Safe custody of FW application in proper file SA

*The Branch Officer should insist for noting the following details

also on the face of the FP/TOB files:-.

1 GPF A/C No. and name of the subscriber

2 Month upto which interest allowed

3 Serial No. of FP Register

4 Serial No. of Closed A/C Register

5 Serial No. of RB Register in case of RB case

e) Clearance of missing credits and other correspondence

(i) Previous Years

a) Verify the Master Cards and make adjustments in the SA

adjustment register, if possible

9b) Call for details if details are not available SA

c) Hand over the missing credit papers (where details are SA

available, but need to be verified from the system )to the

sectional DEOs with acknowledgement which will be

returned by the DEOs Within 3 working days.

d) Adjustment of missing credits/debits through EPS and SA

making entries in the EPS register and send intimations to the

subscriber/DDOs after approval of the sectional head/BO

e) Handing over EPS account to the poster on 5th of each SA

month enabling him /her to complete posting by 15th of that

month

f) Allot definite time frame to each DEO each day for I/C

attending to the work of posting/ adjustments and other Debit Section

corrections etc.

(ii) Current Year

a) Correspondence relating to wanting documents/Unposted SA

items.

b) Verify Register of Wanting documents/Unposted list. SA

c) Post the details received from the department. DEO

f) Miscellaneous works

i) Complaints/request for duplicate Account Statements etc.

Request for duplicate account statements and complaint should be

sent to the dealing sections for necessary action. Complaints received from SG Cell

should be attended to by the SAs of the respective section within four days.

ii) GPF Sanctions

PFW/TA sanctions will be received in the Debit Section which will

further hand over sanctions to the DEOs for entering the details of sanctions in the

computer system. Debit Section will generate lists of PFW sanctions and TA

sanctions separately Series /Try wise List of PFW sanctions will be filed properly for

being used as the NRA Sanction Register which should be closed monthly.

iii) Clearance of observations relating to GPF

ITA section conduct Test Audit, Triennial Review, System Review,

review of outstanding balances under Suspense Head, 5% check of debit vouchers,

review of debit items etc. The Sectional SA will attend to the objections raised by ITA

section settlement of paras raised by Director of Inspection on priority basis by the

specified dates.

10iv) Miscellaneous items of work

Miscellaneous works such as clearance of Unposted Credit/Debits,

Minus Balances, Dormant Accounts, clearance of objections raised by Central Audit

Party and by the Accountant General(Audit) etc. should be attended to by the

sectional SA.

v) Closing of Registers

All the registers mentioned above and enlisted in the Calendar of

Returns should be closed as per provisions contained in this Manual and instructions

issued by the Hqrs Office from time to time. All the reports and returns due to BOs,

controlling section, Group Officer, AG and Hqrs Office should be submitted on or

before the prescribed due dates.

11CHAPTER II

PROCEDURE AND MAINTENANCE OF ACCOUTS ETC.

Institution of General Provident Fund

1. According to Section 49 of Himachal Pradesh Act, 1970, General Provident

Fund (Central Services) Rules, 1960 in force immediately before January 25, 1971

continue to be enforce in Himachal Pradesh till they are altered or replaced or

amended (H.P.Govt.Endst.No.12-40/68 Fin(R&E) III dated 11-02-1971 file inT.M/4-

2/Misc.sanction/70-71 Vol.II file)

Interpretation of Rules

2. The Comptroller and Auditor General of India has held that the State govt. is

now free to interpret their GPF Rules and that is not incumbent upon them to adopt

the interpretations given by the Govt. of India. They are also to issue special order in

individual cases, without having general application under section 241 (5) of the

Govt. of India Act,1935 as adopted. Their order should be expressed as an order of the

Governor and it is not necessary for Accounts Office to insist that such an order

should receive the personal approval of the Governor. The above orders continue to

be enforce in view of Article 372 of Constitution of India.

(Hqrs Officer letter No. 448 –NGE/106/39 dated 17-04-1939)

Eligibility of intending Subscribers

3. All temporary Govt. servants after a continuous service of one year, all re-

employed pensioners other than those eligible for admission to the Contributory

Provident Fund, and all permanent Govt. servants except those permitted to subscribe

to a Contributory Fund are required to subscribe to the General Provident Fund. A

Govt. servant who is required or permitted to subscribe to Contributory Provident

Fund cannot be eligible to join or continue as a subscriber to the G.P Fund, while

he/she retains his/her right to subscribe to such a Fund.

Note 1: Apprentices and Probationers are treated as Govt. servants for purpose

of this rule. Apprentices/Probationers who have been appointed against regular

vacancies and are likely to continue for more than a year can subscribe to a GP Fund

any time before completion of one year.

Note 2: The H.P. State Govt. employees joined service on or after 15-5-2003

are not eligible to Subscribe to GPF as they are covered under the Contributory

Pension Scheme introduced by the H.P. Govt.

(Notification No. Fin (Pen) A (3)-1/96 dated 17-8-2006)

12Allotment of Account Number

4. When a Govt. servant apply to become a GPF Subscriber through DDOs

concerned, his/her eligibility should be carefully tested with reference to the relevant

rules of Fund “Central “or “State” as applicable. No one should be allowed to

subscribe for the first time without a provident fund account No. being allotted by this

office. Following steps should be taken while allotting account Nos:

i) If an applicant is found eligible, his name should be entered in the

Index Register as well as in the Alphabetical Register alongwith his/her father’s

/husband ‘s name, serial number assigned to his/her GP Fund account.

ii) Incomplete application should be returned to the DDOs before

allotment of account number, especially where date of birth, date of joining and

Father/Husband name have not recorded in the application.(This is to ensure that

another number has not been allotted to the subscriber earlier.)

iii) After allotting account No. to the eligible applicant in the General

Index Register, the Suffix/Series code under which number allotted should be

indicated in the appropriate column in the application and top corner of the

nomination by writing Accepted, Indexed and Acknowledged.

iv) After checking by the AAO/SO all the entries made in the register and

other papers , it should be submitted to Branch Officer for approval.

v) On obtaining approval of the Branch Officer, one copy of the statement

indicating the account numbers allotted to each of the Govt. Servant will be returned

to the DDOs alongwith second copy of accepted nomination with the request that it

should always be quoted in all communications with this office as well as in schedule

of deductions attached to the pay bills.

vi) Accepted nomination should be kept in the nomination folders in the

almirahs under the safe custody of Branch Officer.

vii) The Poster/DEO should open the Master in computer and enter series

code, account number with Suffix/ series code, name, designation, date of birth, date

of joining service, date of admission to the Fund, Father/Husband name, name of

DDO etc.

Note 1: It is necessary that the date of birth should be indicated in the

applications for admission to the Fund so that the probable date of superannuation can

be ascertained from the GPF account itself and action can be initiated in time to

complete the subscriber’s account before retirement to avoid any possible delay in

the settlement of PF claims.

Note 2: The Head of Office while forwarding the statement to the Accountant

General should record the following statement in the place provided for above the

signatures of Head of Office “Certified that all the employee’s whose names are

shown above are eligible to subscribe to the G.P Fund in accordance with the relevant

rules”. ( G.I. M.F., O.M., No. 29(4)-E.V.(b)/74, dated 10th August, 1976)

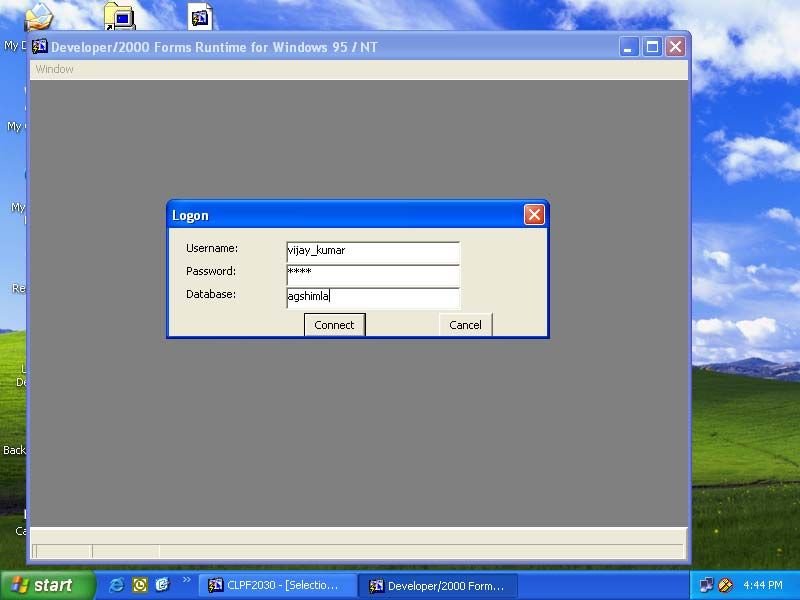

13‘LOGON’ SCREEN

In this screen, a user has to enter the following information

USER NAME (User authorized to login)

PASSWORD (Supplied to user by DBA can be changed by the user

DATABASE agshimla

14‘MAIN MENU’ SCREEN

Depending upon the username and password entered in the aforesaid screen, the user is allowed

access to the relevant module appearing on the Main Menu Screen.

15Master screen

This screen used for creation, updation, deletion and query of the data fed in the

computer. Each Employee is identified by a unique Employee Number.(GPF Account

Numbers allotted to the employees, have been adopted as Employee Number).

Information relating to the Department, DDO and Designation is captured from the

concerned master. Date of Birth, Date of joining. Father’s/Husband’s Name, Marital

status and sex of the employee is also entered to complete the information about each

employee. This information is fed and updated in the computer by the DEOs/Poster.

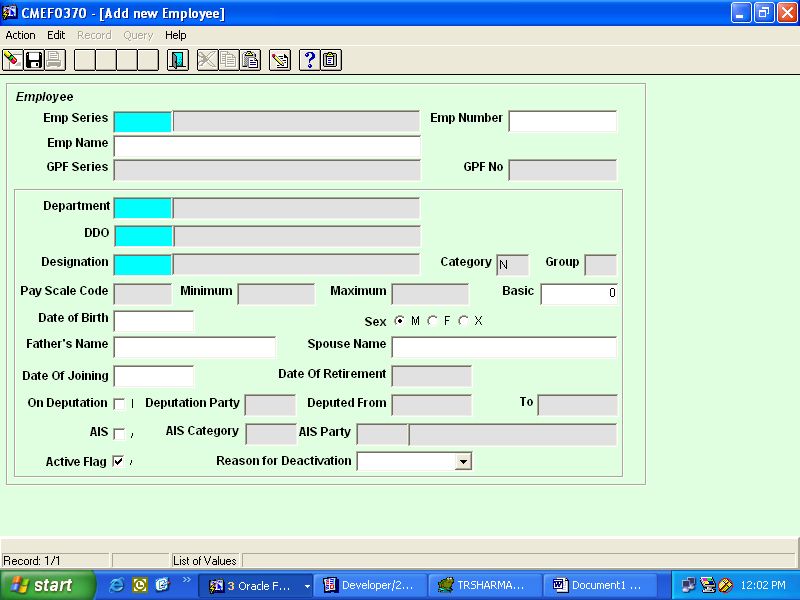

16‘ SCREEN FOR ADD NEW EMPLOYEE’

17‘SCREEN FOR UPDATE SUBSCRIBER’

18Series

1. Series represent the GP Fund series under which the employees of various

departments of the Government are allotted the GPF numbers.

2. Each series has been allotted a unique series code.

Query Screen of Series

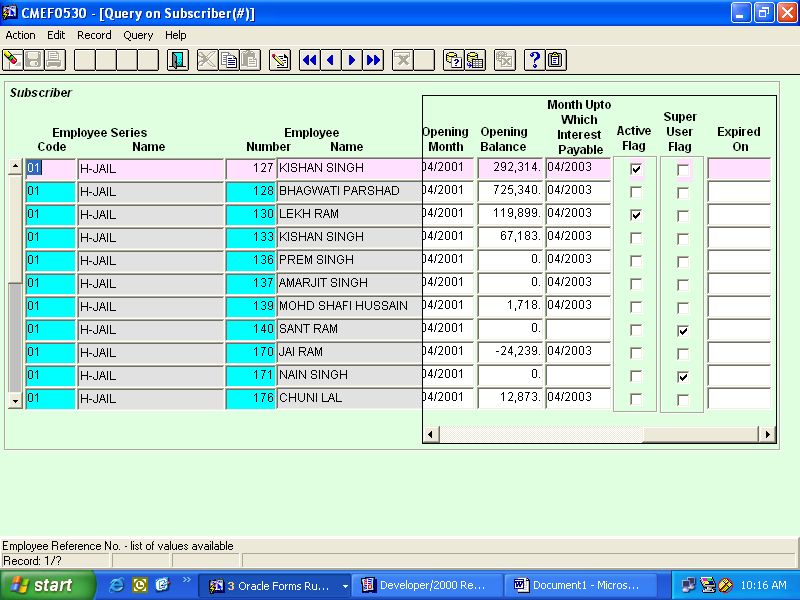

19Subscriber

Each employee contributing to GP Fund is a subscriber and is allotted a

number which combined with the series code makes a unique subscriber code.

205. General Index Register

An Index Register should be maintained separately for each department and

the procedure prescribed in Paragraph 389 of the CAG ‘s Manual of standing

orders(Tech) Vol. I should be followed.

The Index Register should be closed monthly by using the following format:

Opening Balance =

* Received from 16th to 15th =

Total

Incomplete application returned =

Cases in which GPF No. allotted =

Closing Balance =

th

*For instance, cases received from 16 Feb to 15 March should be shown as

receipt in report due on 5th April.

6. Alphabetical Index Register

(a) In the General Index Register, the names are serially arranged according to

account numbers.

In order to have an index register in alphabetical order it is advisable to have

in addition to the General Index Register, an Alphabetical Index Register, prepared

for each series separately by computer/unit recording so that names are arranged

correctly as in a dictionary. The register may be used to find out correct A/c No. of a

subscriber when an A/c No. is incorrectly given or no A/c No. is given in the

voucher/GPF schedule. In order to distinguish between subscribers having the same

names, father’s name and date of birth should also be given.

( Hqrs Office D.O. No.2459-TA-II/30278 dated 3-10-1978 )

(b) Updating the Alphabetical Index Register

With a view to update the alphabetical Index register, the Comptroller

and Auditor General has prescribed the following procedure:-

(i) The Alphabetical Index Register prepared should be prepared on

computer and supplied to all Fund Sections for their use.

(ii) Sufficient number of blank pages may be left after each letter of the

alphabet leaving room for fresh name.

(iii) The fresh names may be added in the register by manual process till

the next list is printed.

217 Nominations

(a) The Government servant are required to send, at the time of joining the

Fund, a nomination in the appropriate form prescribed in the rules applicable to them

alongwith their applications for admission to that Fund. The nomination should be

examined by the Sr. Accountant with reference to the prescribed rules and submitted

for final acceptance to the Gazetted Officer-in-Charge in accordance with the

instructions laid down in Appendix -8

(b) Custody of Nomination

The Comptroller and Auditor General of India has observed that a

nomination is one of the most important document and serves the same purpose as a

Will or Testament of the sub scriber and if it is somehow lost, legal disputes may arise

and the office may be in endless trouble. It has, therefore, been decided that instead of

taking away the original nomination, the Accountant concerned should make out a

true copy thereof, duly attested by the Gazetted Officer-in-Charge for use. The

original nomination should not go out of the custody of the Gazetted Officer-in-

Charge except in case where it is to be forwarded to another Account Office to which

the account of the subscriber has been transferred.

(Para 4.16 of Provident Fund Manual of the Office of the

A.G.C.R.(now D.A.C.R) New Delhi copy received with Comptroller and Auditor

General’s letter No.823-TA-II/109-78 dated 1-6-78 filed in Fds AS-S/P.F. Manual/77-

78 file)

Note 1-The nomination of the depositors who have ceased to be to be

members of the Fund and have been finally paid up, should be preserved (from the

date of such final payments) for the period prescribed for the preservation of the

vouchers of the final payments of GP Fund money as laid down at the item No.4 of

Appendix 5 of this manual.

Note 2-Any form of Declaration submitted by a subscriber revocable at any

time. A fresh Declaration shall be operative only on being received by the Accounts

Officer. On a subscriber’s marriage or re-marriage, any declaration already submitted

by him shall forthwith become null and void and , unless a revised form a declaration

is received, the amount of his accumulation shall be dealt with under Rule 33 of

General Provident Fund( Central Services) Rules.

Note 3- It has been decided by the C.A.G. that the nominations relating to

closed accounts should be segregated in two guard files depending upon the period of

preservation. After giving a note of final payment the nominations will be kept in the

relevant guard file. For this purpose two guard files will be opened as follow-

(i) Nominations relating to accounts in which final payment were/are

made to subscribers themselves or to the major members of the family in accordance

with those nominations.

(ii) Nominations relating to accounts in which final payments were/are

made to minors according to nominations or in any other manner. The period of

preservation of the cases at (i) above is 6 years where payments were prior to 1-4-

221964 and 3 years where payments are made after 31-3-1964 while in case at (ii) above

it is 30 years where payments were made prior to 1-4-1964 and 25 years where

payments are made after 31-3-1964.

(C.A.G. letter No. 1092-T-Admn. II/282-70 dated 19-6-1970 read with

Funds-1 letter No.Funds- 1/As-II/Instt. H.Qrs./1286 dated 17-2-1987)

If minor are nominated in from of Declaration, the person or persons

to whom sums intended for their benefit are to be paid may be stated in the form of

Declaration. The payment on account of General Provident Fund should be made to

the persons nominated on behalf of the minor in the declaration form disregarding

any other persons whether appointed a guardian of the property of a minor beneficiary

or not, so long as the person, whom the deceased appointed to receive the money on

behalf of minor, alive and capable of receiving the money.

(Advocate General’s opinion embodied in paragraph 59 of Bombay Fund

Manual- Para102 of A.G. Punjab Manual.)

c) Cancellation of Nomination

A nomination, which is expressly cancelled by a subscriber by giving a

written notice to the Accounts Officer, should be cancelled and returned to him/her

even though it is not replace by another valid nomination. If the subscriber fails to

furnish a fresh nomination in accordance with the rules subsequently, and the PF

balance become payable on account of death of the subscriber, the payment should be

made in accordance with rules of Funds as if no valid nomination subsists.

Note 1:- Nomination made while in service can be changed even after

retirement so long as the amount remain unpaid.

d) Validation of Nomination on execution.

Nomination executed by the subscriber and submitted by him/her to

the Head of the Office well before his death should be treated as valid nomination

notwithstanding the facts that it did not reach to the Account Officer before the death

of the subscriber.

238. Arrangement of Ledger Card

The GPF account of the subscriber were maintained in this office on Fox-Pro

software from 04/2002 accounts and from 04/2005 accounts, these are maintained on

Oracle based system. Computerized ledger cards prescribed by the Hqrs Office are

generated annually (series-wise) immediately after closing of annual accounts. From

2006-07 these are to be generated Treasury-wise, DDO wise. These ledger cards are

kept in the section Treasury-wise/DDO wise.

9. Posting of Accounts

General Provident Fund Accounts are posted in computer from the following

documents:

(i) GPF Schedules in Form TR-56

(ii) Schedules of Cash recoveries by the districts containing all the

necessary information in r/o the subscriber concerned or supported by Fund

Schedules.

(iii) Vouchers of withdrawals received from Treasuries.

(iv) GPF Transactions appearing through Inter State Suspense Account and

cash settlement account duly supported by Funds Schedules.

(v) GPF transactions appearing through Transfer Ledger Abstracts.

24The following screens will be available in GPF folder on the computer to

enable the poster to start posting of accounts:

This screen is used by the Posters for Voucher Posting, Credit

Posting, Debit Posting, Suspense entry, Sanction entry Abstract

creation and closure of Abstract etc.

25‘SCREEN FOR QUERY ON NEW ABSTRACT’

26This screen is used for creation of the vouchers. In the regular heads

vouchers are directly fetch from the VLC and in the case of Cash,

Exchange, TE and Forest Series vouchers are fed by the

DEOs/Poster.

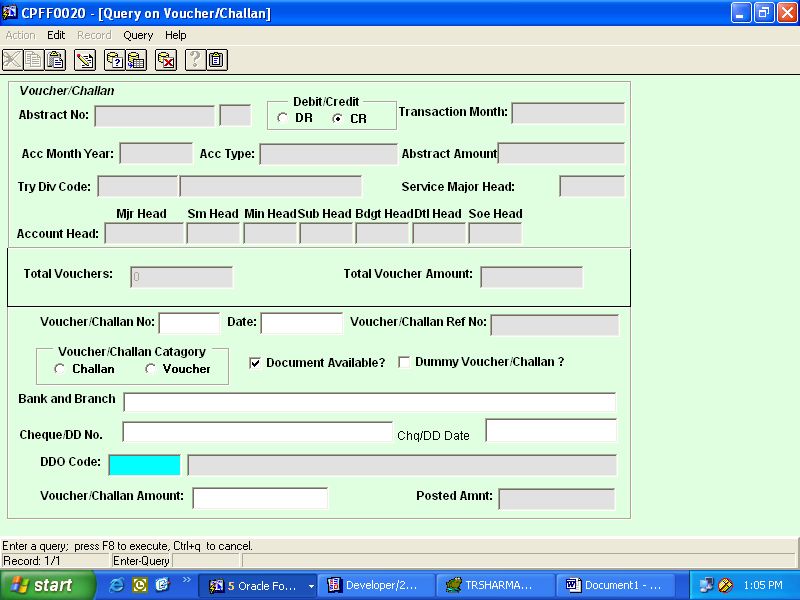

27Query Screen of Voucher/Challan

28Screen of Credit Posting

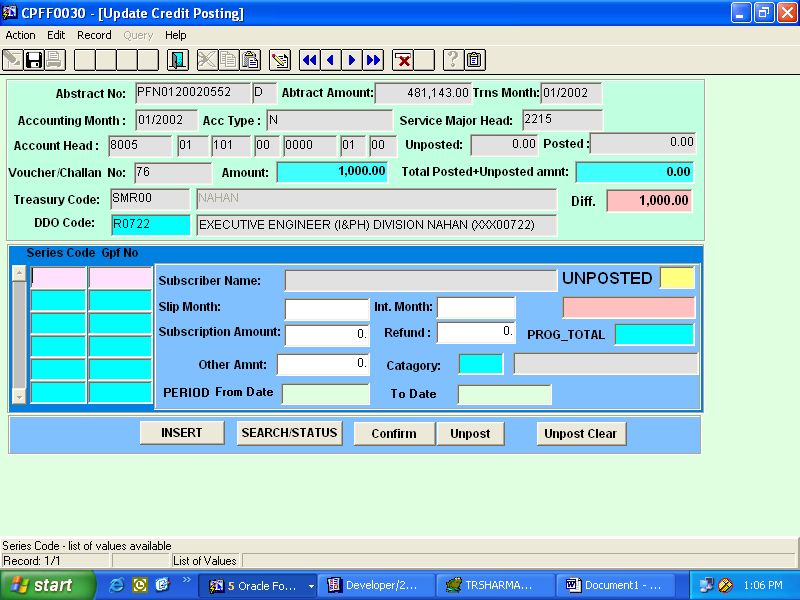

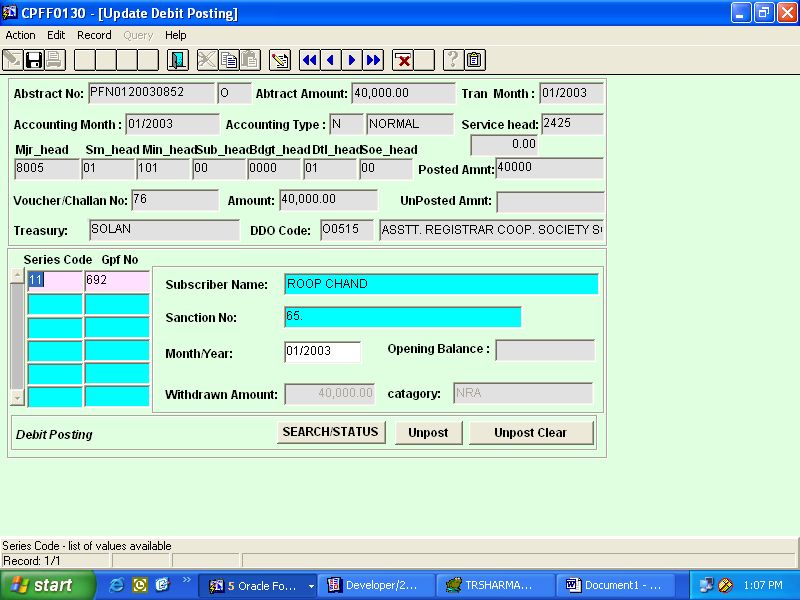

29Screen of Updating of Credit Posting

This screen is used for updating the credit posting. When the credit

posting is to be completed it is the duty of the Poster to close the

abstract and generate the validation reports.

30‘SCREEN FOR ADD NEW SUBSCRIBER FOR TRANSFER’

This screen is used for transfer of balance from one series to another series

Except AIS-HIM series for which TE will be required..

31‘SCREEN FOR ADD NEW ABSTRACT FOR SUSPENSE CLEARANCE’

32‘SCREEN FOR QUERY ON SUSPENSE’

33Debit Voucher Creation:

Office receives the monthly complied accounts in respect of GPF

payment from all the 15 treasuries. From the monthly lists of payments of

GPF all the vouchers are to be feeded to ensured that the detail figure of

the concerned treasury get agreed as such

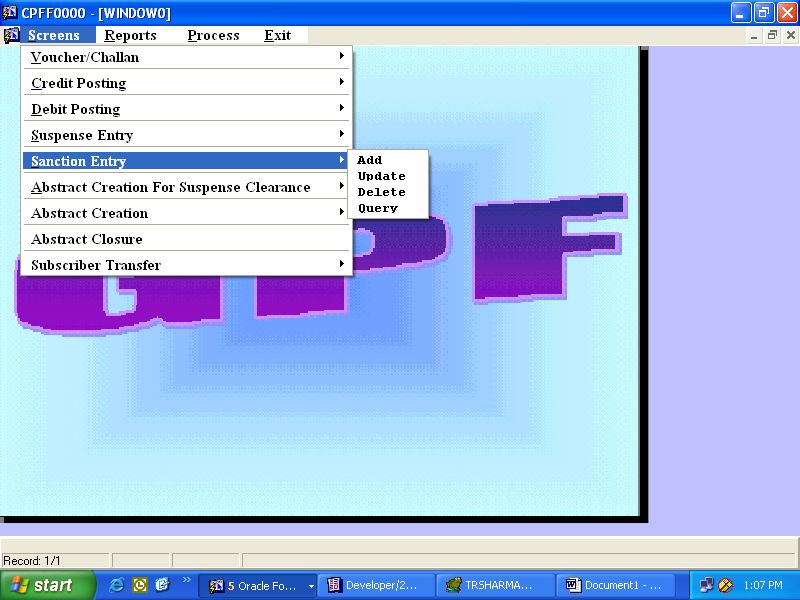

34Posting of Debit Sanctions

All the monthly debit voucher sanctions got entered in through the

following screen. Further sanctions so entered turns to be List of value.

subsequently for the posting of Debits. Hence the Debit posting is

primary based on the post of sanction. As such without posting of

sanctions posting of debit is restricted.

SANCTION ENTRY SCREEN

35‘SANCTION SCREEN’

36POSTING OF DEBITS

After Debit Voucher creation and posting of sanctions final step is

posting of monthly Debits. In the module ‘posted figure’ of the Debit is

got fetched from the sanction amount entered already and not from the

voucher amount entered too in the system. This gives the module a

feature that debit cannot got posted without entering the sanction.

DEBIT ABSTRACT SELECTION SCREEN

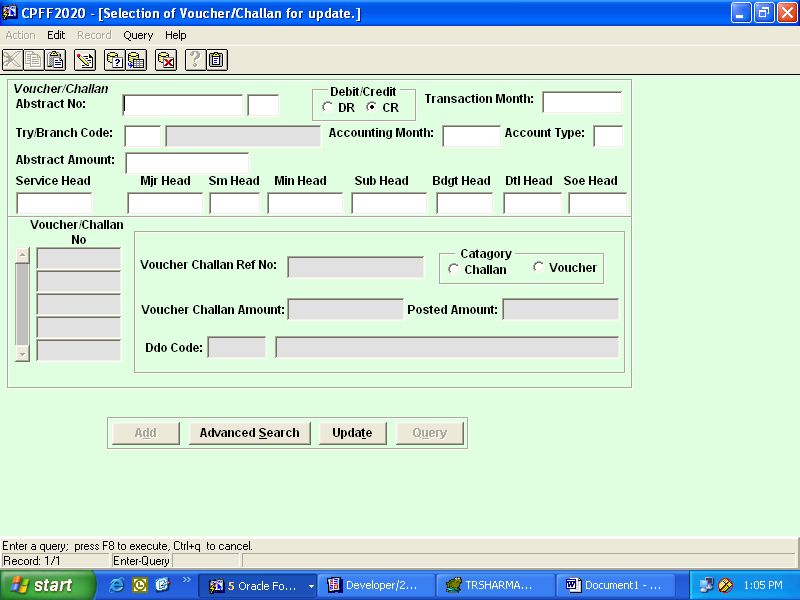

37Screen of update of Debit Posting

(i) CPFF2020-(Selection of Vouchers/Challan for update

(ii) CPFF0020-(Update Vouchers/Challan)

(iii) CPFF2030-( Selection of Credit Posting for update)

(iv) CPFF 0030-(Update Credit Posting)

(v) CPFF-0040-(Add new Sanction)

(vi) CPFF-2130-(selection of Debit Posting for update)

38‘SCREEN FOR QUERY ON ABSTRACT CLOSURE’

3910. Schedules of deduction from Pay Bills

Every pay bill which contains deductions of subscriptions to the GPF has to be

accompanied by a schedule in Form 56 which has to be prepared in accordance with

the instructions and check lists for the Drawing and Disbursing Officers. After the

compilation of accounts these schedules and cash accounts( of recoveries in cash)

should be detached and made over by the respective Compiling Section to PF section

by the 20th of the month following that to which the account relates alongwith a

separate covering list in the form given for each treasury department.

FORM

Covering list of General Provident Fund Schedules relating to the Department

of __________________ for the month of

______________________________________

Sr. No. District Voucher No. Amount

Total

Grand Total

Certified:-

1. That the individual treasury and grand totals have been verified and agreed

with the relevant figures in the Classified Abstract.

2. That I have personally satisfied that all the Provident Fund Schedules,

vouchers and details of adjustments ate furnished herewith.

Date_________ Section Officer

Section

(Comptroller & Auditor General’s letter No. 2192- Admn. 487-89 dated 24th

October 1950)

It should also be ensured by the Compiling Section that : -

(i) No schedule is wanting.

40(ii) If a schedule is not found attached with the pay bill for any reason,

duplicate schedule is prepared from the pay bill.

(iii) If, an account number has not been quoted in the bill, and the schedule has

also not been attached to the pay bill a schedule in the manuscript showing the

name/names of the subscribers may be prepared to avoid lump sum posting as

unposted items(s).

(iv) the total is carefully checked.

(v) printed form covering abstract is used as far as possible.

(vi) proper and timely despatch of schedules is watched through control

registers.

(D.O. No. 2459-TA-II/302-78 dated 3rd October 1978 from the officer of

Comptroller and Auditor General of India.)

On their receipt in the Fund Section:-

(i) the schedules should be checked with the covering abstract.

(ii) Schedules found wanting should immediately be obtained.

(iii) the total should be verified, and

(iv) any omission found in them should be got rectified and Fund section

should then proceed to check them carefully as indicated below:-

When any subscription is paid for the first time and in regard to subscriptions

for March due in April whether subscription is paid for the first time or revised rate

adopted, it should be seen that the subscription paid is in whole rupees and is within

the prescribed minimum/maximum percentage of pay. It should further be seen that

the rate of pay of the subscriber as on 31st March is correctly shown on the Schedule

for March paid in April and entered in the ledger card against the entries of different

years. In the case of subscriptions for other month, it should be seen that the amount

paid agrees with the rate adopted in the first month of the year except when a

subscriber is on leave or under suspension. For all month of the year it should be seen

41that all compulsory subscriptions are paid. Whenever the subscription is varied during

the course of a financial year, reasons for variation should be enquired and indicated

on the ledger card.

Note 1- In the case of all new names in each schedule, it should be seen that

the name of the office from which the subscriber has been transferred is noted therein.

Information regarding new names, date of leave, retirement and death if not already

given in the schedules, should be called for by the Fund section and recorded in the

remarks column.

Note 2- The Comptroller and Auditor General has decided that as an

experimental measure Accountants of Accounts Office may be sent to some treasuries

on tour at the end of each month in order to scrutinize the bills and other vouchers on

the spot and to ensure that they are complete in all respects. The Accountants should

check that:-

(a) Schedules for the recoveries of the PF and other deductions have been

attached to pay bills wherever necessary;

(b) The totals of these schedules work out to the total amounts deducted as PF

subscriptions etc. in the relevant bill; and

(c) The account numbers and names entered in the schedules are correct, there

being no omission to indicate either of them in any case.

It should be ensured that the Accountants who are sent to treasuries carry with

them a complete list of Provident Funds subscription in the concerned District

alongwith their account numbers etc. For this purpose district-wise lists of subscribers

must be got ready, lists upto date with reference to transfers, allotment of new

numbers, admission of new subscribers etc. All the schedules received from each

District should be checked with reference to records in Accounts Offices and to make

them upto date and correct. An easy , method for preparing the District-wise lists will

be to collect all the schedules relating to particular District from the various Provident

Fund Sections, stitch them together and make them into a reference book. In this way,

schedules will be available drawing office-wise and in case these are arranged

alphabetically according to the office, checking of the pay bills in the treasury will be

42rendered easier. It should be possible for Accounts Office to spare a few Assistants

for this work which may best occupy only 6 to 8 days in a month. The Assistant can

also be utilized for obtaining information regarding missing credits and unposted

items, wherever this can be done without prejudice to his normal work. The State

Govt. should be approached and requested to issue suitable instructions to the

treasuries to allow the staff to carry out the duties mentioned above in the treasuries

selected by the Accounts Office for the purpose.

(C.A.G’s letter No. 329- TA. II/56-79 dated 9-3-1979, filed at Page 1/c of file

No, Funds 1/AS-II/79-81)

Note-3 The Comptroller and Auditor General of India has decided that

the system of on spot check of schedules and vouchers at treasuries should be made a

permanent exercise and should be extended to all treasuries and sub- treasuries.

(C.A.G’s letter No.1070-TA.II/56-79 dated 25-8-1980. Filed at page 185/c of

file Funds-1/AS-II/79-81 ).

11. The Comptroller and Auditor General of India has directed that the Group

Officer of Fund and Compilation Section should co-ordinate to see that no schedules

are wanting. For this purpose the Accountant General may obtain every month a joint

report from the two Group Officers on the schedules not received in Fund Group

alongwith reasons for non- transmission by the Compilation Sections. This report

should also reflect the position of the schedules not received in earlier month.

If the Fund Section fails to make a report in time about the non- receipt of

schedules it shall be assumed that schedules had been received in Fund Section and

that they had been lost by the section. Responsibility where necessary should be fixed

on this presumption.

(CAG’s D.O. letter No. 2459-TA. II/302-78 dated 3rd October,1978)

12. Staff sanction for forming Peripatetic Parties.

With a view to monitoring the work done by the party to bring about

substantial improvements in the maintenance of Provident Fund Accounts, it has

been decided by the Comptroller and Auditor General of India that the report on the

43progress of work done by the party may be sent to the Hqrs Office quarterly in the

following proforma:-

(i) Number of offices visited during the quarter.

(ii) Total number of missing credits/debits pertaining to these office on the

date of visit.

(iii) Total number of unposted credits/debits outstanding in respect of these

offices as on the date of visit.

(iv) Item cleared Number Amount

(a) Missing Credits.

(b) Missing Debits.

(c) Unposted Credits.

(d) Unposted Debits.

(v) Action proposed to be taken in

respect of items not reconciled even

after this visit of the Peripatetic Party.

(C.A.G’s letter No.1809-AC.II/276-84 dated Sept, 1985. Filed in file Funds-

1/Peripatetic Parties/84-86).

13. Cash Recoveries and other Credits

Separate schedule of cash recoveries received are, after agreement with the

account passed on by Book Section to the Fund Section supported by Fund Schedules.

As these schedules are consolidated one for all the departments, items relating to

different departments should be sorted out in the Fund Computer Cell Sections

(presently Fund-17 Section). A consolidated Compilation sheet should be prepared

and arranged series wise of all credits t the Fund by payment in cash, by deduction

from bills as per schedules or through Inter State Suspense Account or Transfer

Ledger Abstract communicated to the Fund Section by a section other than

Compilation sections. This information as to the total amount recovered on account of

GPF in a month becomes available by district and by the department for which

separate accounts are compiled. After this consolidated compilation has been made,

the amount of cash recoveries are added to the total of the relevant covering schedules

as stated above before these compilation are made over to the Accountant for posting

accounts.

44In respect of Government servants who are on deputation to Central

Government or are on Foreign Service, the subscription to the Provident Fund are

received through bank drafts. These bank drafts are usually for ‘net amount’ i.e.

payments made on account of Provident Fund advances or part withdrawals are

deducted from the total credits. When drafts are received, it may be seen that:-

(i) they are promptly encashed,

(ii) they are accompanied by proper schedules and payment vouchers,

(iii) credits received through bank are properly classified, and

(iv) Subscriber’s account are properly debited/credited.

(CAG’s DO letter No.2459-TA. II/302-78 dated 3rd October,1978.)

14. Withdrawal

Schedules of withdrawals supported by vouchers received from treasuries will

be received in the Debit Section (presently Fund-17) dealing with posting work of

debits and also from Forest A/c Section dealing with Forest Department in respect of

subscribers of Forest Department after agreement with lists of payment, Similarly,

debits of GPF received through Inter State Suspense Account and transfer ledger

abstract are communicated by the Account Current and other sections. After

completing posting of debits, district /department wise ( i.e. series wise/ Section-wise)

segregation of the debit vouchers should be done by debit posting Section and pass on

to the Sections concerned on or before the date circulated through schedule for

posting programme alongwith validation reports . Account must be supported with

covering lists together with a certificate to the effect that the total figures entered

therein agree with the account.

The items appearing in the Transfer Ledger Abstract maintained in the Book

Section are copied from it by the concerned Accountants of Fund Sections for being

posted in the account of the subscriber concerned.

15. Consignment of Vouchers

The vouchers pertaining to the payments out of various Provident Funds are

received in Fund Sections from the following different sources:-

(1) From the Book Section representative of Treasury where the payments

have been booked by the Treasury Officer direct.

(2) From the Compilation Sections in respect of payments which are initially

classified by the Treasury Officers under Departmental suspense and later on are

taken under the corrected head by the compilation sections.

(3) From the Account Current Sections.

(4) From Forest Account Section,

45(5) From other sources such as adjustment proposed by fund sections and

receipt of voucher from Book Section etc. in subsequent months.

The vouchers from the above sources are received alongwith a covering list by

the DEOs/Poster attached to Fund Cell. The DEOs/Poster will check the vouchers

with the covering lists before receiving them. He will sort them out according to the

department(series-wise) for posting. After posting he will return the vouchers,

schedules, compilation sheets and covering lists to the concerned Fund section. In

case of vouchers retained by him he will give a suitable note on the original covering

schedule over his dated initials for future reference.

16. Unposted Items.

It is of utmost importance that fresh accretion of unposted items is controlled

and minimised. The report of unposted items should be generated from the computer

by the DEOs/Poster at the end of each month and sent the report to the concerned

Fund sections.

Following action should be taken to minimise new accretion:-

i) Alphabetical Index Register/Card be used for tracing correct account

number.

ii) Unposted credits and debits of a section be checked by the Section Officer

and Branch Officer before finalisation of Register of unposted items/Master Card of

unposted items before account are closed.

iii) By making a reference to each DDO in a standardized form for all

credits/debits remaining at the end of the month in respect of that DDO. The Branch

Officers should verify that this has been done before finalization the Register of

unposted items/Master Cards.

iv) Maintenance of diary of sanction to advance and withdrawals (for debit

items.)

17. Register of Missing Credits and Debits

The Missing credits and debits report should be generated from the computer

by the DEOs/Poster at the end of each month and sent the report to the concerned

Fund sections. The concerned Fund Section should maintained a register of missing

credits/debits in the prescribed form. The register is intended for recording missing

46credits viz. original subscriptions and recoveries of temporary withdrawals. The

register should be written up by the Accountant reviewing the ledger cards. After

writing up the register quarterly, the number of missing credits/debits i.e. number of

accounts affected and number of items should be worked out and noted at the end of

register.( while computing the number of account only those accounts that are

affected for the first time since the beginning of the year should be counted.)

The Comptroller and Auditor General of India has decided that the register of

missing credits/debits should be maintained in the revised form and closed half yearly

instead of quarterly.

a) The ledger cards should be reviewed six monthly, once after posting of

September Accounts and next after annual closing of accounts and all missing

credits/debits should be posted in the space provided therefore, in the ledger card. The

particulars of adjustment made should also be noted therein.

b) The missing credit register may be opened series-wise or departmental-wise

as may be considered necessary. Separate folio may be allotted to one or more

subscribers, as may be found convenient.

c) Total numbers of missing credits/debits alongwith the year-wise details

should be copied from the ledger cards in the register of missing credits/debits.

d) The letter should be issued to the DDOs at the end of mid year. Six-monthly

review requesting for details of missing items relating to the period April to

September each year.

e) An abstract may also be prepared at the end of the register to indicate the

balance of missing credits/debits at the time of previous closing, additions and

clearance made during six months and closing balance at the end of present closing.

f) After closing of annual Accounts for the year and before issued of annual

accounts statements, ledger cards should be reviewed and missing credits and debits

covering the period of accounts from October to March (including March final and

March Supplementary) each year identified and noted in the ledger cards. Upto date

missing credits and debits with particulars of months should be noted in the Accounts

47You can also read