ARC Resources Ltd. Investor Presentation - July 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ARC Resources Ltd. Investor Presentation July 2021

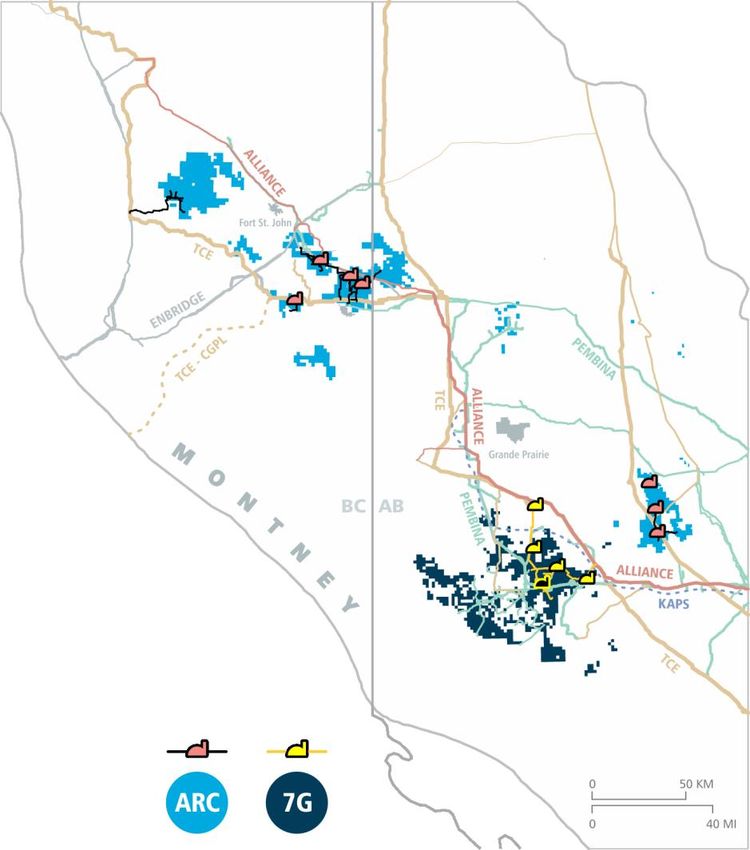

ARC Is the Largest Pure-play Montney Producer

Shares outstanding 725 million

Market capitalization1 $7.7 billion

Net debt2 $2.4 billion

Enterprise value1 2 $10.1 billion

Quarterly dividend $0.06/share

Dividend yield3 2.3%

Montney production4 5

Mboe/day

~340

4%

21%

~340

15%

60%

(1) Market capitalization as of June 29, 2021.

Crude oil Condensate

ARC

Peer

Peer

Peer

Peer

Peer

Peer

(2) Combined pro forma net debt excluding lease obligations as of March 31, 2021. Refer to the “Capital Management” note in ARC’s financial statements and to the

section entitled “Combined Pro Forma Reconciliations” within the Advisory Statements to this presentation for the calculation of Seven Generations’ net debt

1

2

3

4

5

6

excluding lease obligations as of March 31, 2021.

(3) Dividend yield as of June 29, 2021. NGLs Natural gas

(4) Source: Company reports, estimated operated Montney volumes used in the absence of public disclosure.

(5) Includes ARC’s non-core Pembina production.

ARC is the premium investment opportunity for exposure to the Montney 2

ARC’s Guiding Principles

Sustainable business Risk management

around all aspects of the Superior capital discipline

model with best-in-class business including focused on maximizing free

people and assets along with maintaining a strong funds flow1 to optimize

a relentless focus on financial position through shareholder returns

long-term profitability commodity price cycles

Owned-and-operated

Operational excellence

infrastructure to support and top-tier ESG performance

operational control, low cost through efficient and

structure, and optimized disciplined execution

revenue streams

(1) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

ARC’s guiding principles are enduring 3

ARC Is a Premier Business

Strong balance sheet

Net debt1 is forecasted to be ~$1.5 billion or less than one times funds from operations by Q3 20212

Substantial free funds flow3

Free funds flow3 is forecasted to be ~$1.0 billion and free funds flow yield is forecasted to be ~15% in 20212

Sustainable dividend and increased returns to shareholders

ARC expects to pay $151 million or $0.24/share in 2021 and allocate a portion of free funds flow2 to increased returns

Modest production growth through profitable development activities

ARC has decades of premium drilling locations in its portfolio, targeting a long-term organic growth rate of 5%

Leading ESG performance and transparency

ARC has the lowest GHG emissions intensity amongst Canadian upstream E&P companies and sets measurable targets

(1) Net Debt excludes lease obligations. Refer to the Advisory Statements to this presentation.

(2) Based on forward price curve and share price as of June 29, 2021.

(3) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

3

ARC delivers financial strength, free funds flow , returns to shareholders, profitable growth, and ESG excellence 4

2021 Outlook

2021 Plan – Executing on ARC’s Disciplined Strategy

Fully integrate Seven Generations

Integrate people, assets, and processes while focusing on realizing immediate cost savings and synergies

Enhance current investment-grade financial position

Reduce net debt1 to ~$1.5 billion or ~1.0 times funds from operations

Sanction and commence development of Attachie West Phase I

Execute leading development opportunity in the most efficient and profitable manner possible

Sustainably increase dividend

Demonstrate commitment to shareholders by prioritizing increased distributions of income through increased cash dividends

Initiate normal course issuer bid to repurchase ARC common shares

Demonstrate commitment to shareholders by prioritizing growth in per share metrics

(1) Net Debt excludes lease obligations. Refer to the Advisory Statements to this presentation.

(2) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

2

ARC’s 2021 plan increases total shareholder value and delivers on free funds flow priorities 6

1

Delivering on Free Funds Flow Priorities

US$55/bbl WTI

Free funds flow1:

Cdn$2.50/GJ AECO

• Current dividend

• Attachie West Phase I

US$45/bbl WTI • Sustainable dividend

Cdn$2.25/GJ AECO increases

• Share repurchases

• Strategic M&A

US$40/bbl WTI Maintenance capital:

Cdn$1.90/GJ AECO $1.0 billion to $1.1 billion

annually to sustain

production at

340,000 boe/day

Funds from Maintenance Capital Current Dividend Attachie West Phase I Incremental Returns Excess Free Funds

Operations Capital to Shareholders Flow

(1) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

ARC’s maintenance capital and current dividend break-even is less than US$40/bbl WTI and Cdn$1.90/GJ AECO 7

Q1 2021 in Review

Production Capital expenditures

boe/day $ millions

ARC 170,430 ARC 125.7

Seven Generations 180,774 Seven Generations 148.3

Combined pro forma1 351,204 Combined pro forma1 274.0

Funds from operations Free funds flow2 Net debt3

$ millions $ millions $ millions

ARC 273.9 ARC 148.2 ARC 568.0

Seven Generations 300.6 Seven Generations 152.3 Seven Generations 1,786.9

Combined pro forma1 574.5 Combined pro forma1 300.5 Combined pro forma1 2,354.9

(1) Combined pro forma production, capital expenditures, funds from operations, and free funds flow represent the results of ARC plus Seven Generations for the three months ended March 31, 2021. Combined pro forma net debt excluding lease obligations represents net debt excluding lease obligations of ARC plus Seven Generations as of

March 31, 2021. Refer to the section entitled “Combined Pro Forma Reconciliations” within the Advisory Statements to this presentation for the calculation of Seven Generations’ funds from operations and free funds flow for the three months ended March 31, 2021, and Seven Generations’ net debt excluding lease obligations as of March

31, 2021.

(2) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

(3) Excluding lease obligations. Refer to the “Capital Management” note in ARC’s financial statements.

ARC is well-positioned to deliver on its 2021 business priorities following excellent performance in Q1 2021 8

Enhancing Current Investment-grade Financial Position

Long-term notes repayment schedule1 2021F net debt2 sensitivities

Cdn$ millions $ billions, ratio

600 2,400 2.0

450 3.72% US$ Note

8.21% US$ Note 1,800 1.5

5.36% US$ Note

300 3.31% US$ Note

3.81% US$ Note 1,200 1.0

150 4.49% Cdn$ Note

2.354% Cdn$ Note

600 0.5

3.465% Cdn$ Note

0

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

0 0.0

US$40/bbl WTI & US$50/bbl WTI & US$60/bbl WTI &

ARC has ample liquidity US$2.30/MMBtu US$2.60/MMBtu US$2.90/MMBtu

+ $2.0 billion unsecured extendible revolving credit facility NYMEX Henry Hub NYMEX Henry Hub NYMEX Henry Hub

+ $1.2 billion of available liquidity Net Debt (LHS) Net Debt to Funds from Operations (RHS)

(1) Assumes Cdn$/US$ exchange rate of 1.2572 as of March 31, 2021.

(2) Net Debt excludes lease obligations. Refer to the Advisory Statements to this presentation.

Investment-grade credit rating allows for access to low-cost debt 9

$160 Million in Annual Synergies from 7G Acquisition

Synergies expected by 2022

$160 million

180

Synergies

$25 million

150

$25 million

$15 million

120

$50 million1

90

60

$45 million

Realized Cost Savings:

+ Corporate Costs

30

+ Finance Costs

0

Corporate Costs Finance Costs Operating Efficiencies Market Optimization Drilling & Completions Efficiencies Annual Synergies

(1) Finance costs are expected to be approximately $50 million lower for the combined entity than they would have been if the Seven Generations senior notes remained outstanding.

Seven Generations integration is progressing on schedule and is expected to be completed by year-end 2021 10Evaluating Strategic M&A Opportunities

Assets must be as good or better than ARC’s existing assets

Infrastructure must be largely owned and operated

Assets must have similar ESG characteristics and performance

Assets must be able to generate free funds flow1 at reasonable commodity prices

Opportunity can create scale and/or unique synergies

(1) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

ARC has no holes in its portfolio but will continue to evaluate strategic M&A opportunities with the Company’s screening criteria 11Industry-leading Financial Performance amongst Peers

Comparative cash returns1 2 2021E return on average capital employed3 4

24% Canadian E&Ps 16% Canadian E&Ps

US E&Ps US E&Ps

18% 12%

12% 8%

6% 4%

0% 0%

ARC ARC

Average Free Cash Flow Yield (2021E to 2022E)

Dividend Yield (Current)

(1) Source: Barclays Capital Markets; FactSet (April 2021). Peer group includes North American E&Ps: APA, AR, CLR, CNQ, CNX, COG, COP, CVE, DVN, EOG, EQT, FANG, MRO, OVV, PXD, RRC, SWN, TOU, XEC.

(2) Free Cash Flow Yield is calculated as funds from operations less capital expenditures and dividends.

(3) Source: Peters & Co. “E&P Overview Tables” (May 17, 2021). Peer group includes North American E&Ps: APA, AR, CNQ, COG, DVN, EOG, FANG, OVV, PXD, TOU.

(4) Return on Average Capital Employed is calculated as unhedged cash flow less Peters & Co.’s estimate of required capital spending to maintain flat production volumes year-over-year, expressed as a percentage of capital employed. Capital employed is defined as average shareholders’ equity excluding impairment plus net debt.

ARC is expected to deliver the highest cash return and return on average capital employed amongst its Canadian peers 12Guidance – Production

Q1 2021 Q2 to Q4 2021 2021

Actuals Guidance1 2 Guidance1 2

Production

Crude oil (bbl/day) 13,647 12,000 - 13,500 12,000 - 13,500

Condensate (bbl/day) 13,812 69,000 - 75,000 55,000 - 60,000

Crude oil and condensate (bbl/day) 27,459 81,000 - 88,500 67,000 - 73,500

Natural gas (MMcf/day) 794 1,200 - 1,255 1,100 - 1,140

NGLs (bbl/day) 10,620 49,000 - 52,000 40,000 - 42,000

Total production (boe/day) 170,430 330,000 - 350,000 290,000 - 305,000

Q2 2021: ~7% lower than Q1 2021 combined pro forma production of 351,204 boe/day due to significant

turnaround activity and spring break-up impacts

Q3 2021 and Q4 2021: ~340,000 boe/day

(1) ARC acquired Seven Generations Energy Ltd. on April 6, 2021, and as such, 2021 guidance includes ARC’s financial and operational results for the three months ended March 31, 2021, plus the Company’s expectations for the combined financial and operational results of ARC’s and Seven Generations Energy Ltd.’s operations for the

remaining nine months of 2021.

(2) COVID-19 impacts on demand and market volatility may impact ARC’s future financial and operational results. ARC will continuously monitor its guidance and provide updates as deemed appropriate.

13Guidance – Expenses and Capital Expenditures

2021

Guidance1 2

Expenses ($/boe)

Operating 4.10 - 4.60

Transportation 4.50 - 5.00

G&A expense before share-based compensation expense3 0.90 - 1.00

G&A - share-based compensation expense4 0.30 - 0.45

Transaction costs 0.20 - 0.30

Interest and financing 0.70 - 0.80

Current income tax expense as a per cent of funds from operations 1-5

Capital expenditures before land and net property acquisitions (dispositions) ($ millions) 950 - 1,000

(1) ARC acquired Seven Generations Energy Ltd. on April 6, 2021, and as such, 2021 guidance includes ARC’s financial and operational results for the three months ended March 31, 2021, plus the Company’s expectations for the combined financial and operational results of ARC’s and Seven Generations Energy Ltd.’s operations for the

remaining nine months of 2021.

(2) COVID-19 impacts on demand and market volatility may impact ARC’s future financial and operational results. ARC will continuously monitor its guidance and provide updates as deemed appropriate.

(3) Excludes transaction costs associated with the acquisition of Seven Generations Energy Ltd.

(4) Comprises expense recognized under all share-based compensation plans, with the exception of the Deferred Share Unit Plans.

14Guidance – Capital Program of $950 Million to $1.0 Billion

Attachie

~$5MM

~3,500 boe/day

Complete detailed engineering

work for Attachie West Phase I Ante Creek

~$60MM ● 16 wells

~17,000 boe/day

Deliver profitable light oil

Greater Dawson production by leveraging

2020 facility expansion

~$240MM ● 44 wells

~93,000 boe/day

Sustain production and complete

small-scale facility sour conversion and Kakwa

optimization project at Parkland/Tower Kakwa

~$525MM ● 55 wells

~180,000 boe/day

Integrate asset and focus

Sunrise on maximizing free funds

flow1 generation

~$80MM ● 9 wells

~40,000 boe/day

Expand existing facility by 40 MMcf/day

and maximize throughput to capitalize on

anticipated strength in natural gas pricing

Note: Well counts denote wells drilled in calendar year; number of wells with completions activities in calendar year may vary.

(1) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

1

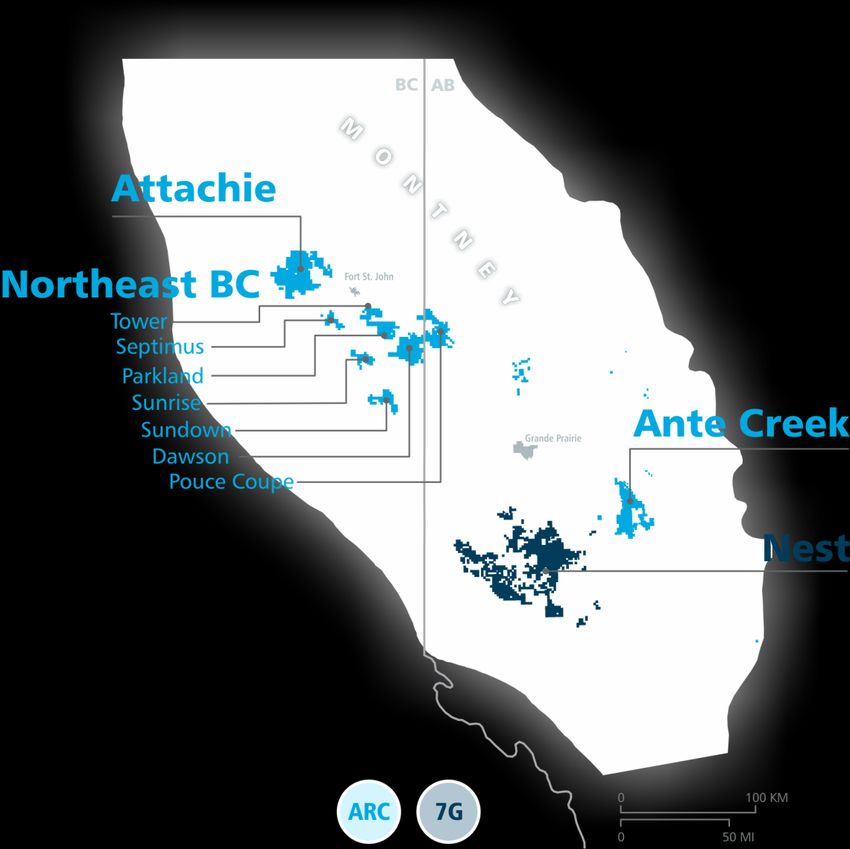

Focused on asset integration, sustaining production, and maximizing free funds flow generation 15Asset Overview

Greater Dawson Overview

Snapshot

Overview Low break-evens2

Production1 Dawson & Parkland

100 Mboe/day (21% liquids) $0.26/Mcf to $0.39/Mcf

Land position

Tower 149,800 net acres (97% W.I.)

Phase I & II

Gas Plants

Phase III & IV

Gas Plants

Parkland Large resource Significant optionality

Phase I & II

Dawson Gas Plants

Drilling inventory3 4 Integrated infrastructure allows

>1,200 locations ARC to prioritize wells based on

Pembina & Enbridge `` Years to sustain return on investment and

TCPL ~20 years prevailing commodity prices

Parkland-Dawson Interconnect Pipeline

(1) Represents financial and operational results for the three months ended March 31, 2021.

(2) Break-even prices are at Cdn$/Mcf AECO. Break-even analysis is run on a single commodity and is defined as the price at which NPV10 is equal to zero.

(3) Comprises approximately 20 per cent of 2P booked undeveloped locations and approximately 80 per cent of internal inventory estimates.

(4) Subject to change based on technology and economic environment.

(5) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

5

Low reinvestment rates and strong lower Montney liquids performance driving significant free funds flow generation 17Sunrise Overview

Snapshot

Overview Low cost structure

Production1 Operating expense

~280 MMcf/day ~$0.20/Mcf

Optimally positioned for Finding and development cost

LNG supply ~$0.35/Mcf

Phase I & II

Gas Plants

Efficient resource Environmental

performance

Land position Electrified facility and field drive

23,100 net acres (93% W.I.) ultra-low emissions profile

Drilling inventory2 3 Up to five layers of development

400 locations significantly reduces footprint

Coastal GasLink

(1) Sunrise Phase I & II facility expansion of 40 MMcf/day was brought on-stream in Q2 2021.

(2) Comprises approximately 25 per cent of 2P booked undeveloped locations and approximately 75 per cent of internal inventory estimates.

(3) Subject to change based on technology and economic environment.

Lowest-cost dry natural gas play in North America 18Kakwa Overview

Snapshot

Gold Creek

Gas Plant

Overview Near-term objective

Production1 Integrate asset into portfolio and

Cutbank

Gas Plant

181 Mboe/day (56% liquids) focus on realizing immediate

Land position operations, drilling, and

498,500 net acres (99% W.I.) completions synergies

Karr

Facility

Capital efficiency Right-size

Pembina

Kakwa River

Lator

Gas Plant

and decline rate transportation

contracts

Focus on improving capital Align transportation levels with

efficiencies and reducing decline physical transportation needs to

rate of 40% by ~2% per year increase free funds flow2

NGTL

Alliance

Pembina

(1) Represents financial and operational results for the three months ended March 31, 2021, on a pro forma basis. The Kakwa assets were acquired through the acquisition of Seven Generations Energy Ltd., which closed on April 6, 2021.

(2) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

2

Premium condensate-rich and high-deliverability natural gas play that generates significant free funds flow 19Ante Creek Overview

Snapshot

Overview Stable cash flows

2-26 Production1 Balanced commodity mix and

Gas Plant 17 Mboe/day (50% liquids) moderate decline rates

Land position Break-even2

125,500 net acres (100% W.I.) US$20/bbl

10-7

Gas Plant

Efficiency Optimizing

10-36

Gas Plant

evolution infrastructure

Well and pad design Leveraging 2020 facility

improvements are delivering expansion to efficiently grow free

strong capital efficiencies and funds flow3 profile

enhanced profitability

(1) Represents financial and operational results for the three months ended March 31, 2021.

(2) Break-even prices are at US$/bbl WTI. Break-even analysis is run on a single commodity and is defined as the price at which NPV10 is equal to zero.

(3) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

3

Highly profitable, stable light oil development generating significant free funds flow 20Attachie Overview

Snapshot

Overview Significant resource

Pilot production1 Resource in place2

4.5 Mboe/day (57% liquids) 8.9 Bbbl of liquids

32 Tcf of gas

Phase I

Gas Plant

4-20 Development Delineation

Battery potential complete

Land position Piloting activities have set the

202,000 net acres (99% W.I.) stage for efficient execution of

Drilling inventory3 4 large-scale development

Pembina >1,500 locations

North Montney Mainline

(1) Represents financial and operational results for the three months ended March 31, 2021. ARC has been conducting piloting activities in Attachie West prior to the planned sanctioning of Attachie West Phase I.

(2) Total Petroleum Initially-in-Place as of December 31, 2018.

(3) Comprises approximately two per cent of 2P booked undeveloped locations and approximately 98 per cent of internal inventory estimates.

(4) Subject to change based on technology and economic environment.

Attachie is the premier development opportunity within ARC’s portfolio 21Attachie West Phase I Design

Total Condensate and Natural Gas Forecasted Capital

Processing NGLs Processing Processing Investment

Capacity Capacity Capacity (2022 to 2023)

40 Mboe/day 25 Mbbl/day 90 MMcf/day ~$600 million

Targeted Sanction Date: Q4 2021

Targeted On-stream Date: Q3 2023

Subject to Board approval, ARC is ready to sanction Attachie West Phase I once its debt reduction targets are met 22Attachie West Phase I Cash Flow Profile

$500,000,000 45, 000

40, 000

$400,000,000 35, 000

30, 000

$300,000,000 25, 000

20, 000

$200,000,000 15, 000

10, 000

$100,000,000 5,0 00

0

$0 -5,000

2021F

2022F

2023F

2024F

2025F

2026F

2027F

2028F

2029F

2030F

-10,000

($100,000,000) -15,000

Netback1 2

-20,000

($200,000,000)

Capital Expenditures -25,000

Free Funds Flow1 3 -30,000

($300,000,000) Production -35,000

(1) Economics run at US$55/bbl WTI and US$2.75/MMBtu NYMEX Henry Hub flat pricing.

(2) Netback is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

(3) Free Funds Flow is a non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Refer to the Advisory Statements to this presentation.

2

Once on-stream, Attachie West Phase I is expected to generate free funds flow of $250 million annually 23Network of Owned-and-operated Infrastructure

Combined network of owned-and-operated infrastructure

+ Natural gas processing and sales capacity of 1.5 Bcf/day

+ Ability to optimize larger portfolio, which has access to

downstream markets across North America

Benefits of owned-and-operated infrastructure

+ Lowers cost structure and increases funds from

operations

+ Provides ability to manage production based upon

prevailing commodity prices to optimize revenues

+ Retains economics of facility optimization projects

Owned-and-operated infrastructure affords greater optionality and control over cost structure 24ARC’s ESG Excellence

Global oil and gas companies’ relative ESG rankings1 2

64

ARC

Social and Governance Score

58

Africa

Asia

Canada

52 Europe

Latin America

Middle East

Russia

46

United States

40

38 46 54 62 70

Environmental Score

(1) Source: BMO Capital Markets; CSRHub; Bloomberg (January 2021).

(2) ARC scores represented are prior to the acquisition of Seven Generations Energy Ltd., which closed on April 6, 2021.

ARC scores among the best in the world for environmental, social, and governance performance 25Strong Performance across Key ESG Factors

Environmental Social Governance

1 1

Emissions performance Safety Executive compensation

+ Lowest GHG emissions intensity + Number one corporate priority + 97% shareholder approval of ARC’s

amongst Canadian upstream E&P + Absolute focus on workplace safety for 2020 “say on pay” advisory vote

companies employees and contractors + Majority of executive pay “at risk” and

+ “A-” score by CDP for Climate Change tied to medium- and long-term share

disclosure and performance price and ESG performance

1

Water usage Diversity and inclusion Board of Directors

+ Responsibly manage water usage in + 30% Club and Bloomberg Gender- + 9 of 11 directors are independent

operations Equality Index member + >99% shareholder approval rating in

+ 90% of water used on ARC’s legacy + 25% of executive team and 36% of 2020

assets is recycled directors are female

+ “B” score by CDP for Water Security

Jantzi Social Index constituent

Minimizing the environmental Stakeholder benefits across all Governance principles aligned to

impact of resource development aspects of the business shareholder values

(1) Results represented are prior to the acquisition of Seven Generations Energy Ltd., which closed on April 6, 2021.

ARC’s ESG commitment leads to joint stakeholder and shareholder benefits 26ARC’s Resource and Scalability Potential

Drilling locations by area1 2 Resource potential

2,000

1,500

1,000

500

0

Attachie Greater Kakwa Sundown Ante Sunrise Septimus 2020

Dawson Creek Base Production Future Development Projects

(1) Comprises 2P booked undeveloped locations and internal inventory estimates.

(2) Subject to change based on technology and economic environment.

ARC has decades’ worth of premium drilling locations with commodity and geographic optionality 27Additional Information

Natural Gas Financial and Physical Price Management

WCSB demand and export capacity growth1 Natural gas realizations2 3 and diversification4 5

5.00 $4.39

4.00 $1.41

5.4 Bcf/day Demand & Export Capacity $2.82

Cdn$/Mcf

3.00 Realized Gain (Loss) on

Growth Expected by 2025 $2.14 $2.03 $2.18 Risk Management Contracts

2.00 $0.11 $0.02 Diversification Activities

$0.09

$2.94 $3.19 Average Price before

1.00 $2.13 $2.07 $2.26 Diversification Activities

LNG Canada Phase 1 ($0.06)

0.00 ($0.08) ($0.15) ($0.10)

+2.1 Bcf/day by 2025 ($0.06) ($0.21)

(1.00)

Intra-Alberta Demand Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021

+1.5 Bcf/day by 2025

100%

Enbridge T-South Capacity 8% 9% 9% 9%

+0.2 Bcf/day by 2021 NGTL East Gate Capacity 7% 9% 9% 12%

1% Dawn Floating

+1.3 Bcf/day by 2022 6%

75% 17%

% of Total Production

28% 15% Malin Floating

24%

NGTL West Gate Capacity Henry Hub Floating

15% 16%

+0.3 Bcf/day by 2023 50% 13% Midwest US Floating

21% WCSB Floating

39% Hedged

25% 41%

43%

31%

11%

7%

0%

Bal 2021 2022 2023 2024

(1) Source: ARC Risk Research, TC Energy, Enbridge, company reports.

(2) Natural gas realizations are for ARC as a stand-alone entity.

(3) Realized gain (loss) on risk management contracts is not included in ARC’s realized natural gas price.

(4) Diversification based on internal volume and marketing assumptions for the combined pro forma entity, adjusted for ARC’s heat content.

(5) “Hedged” includes all physical and financial fixed price swaps, collars, and 3-ways.

Well-diversified North American natural gas exposure increases optionality 29Canadian Condensate Market

Crude oil and condensate pricing1 WCSB condensate supply and demand2 3

US$/bbl Mbbl/day

80 800

60 600

40 400

20 200

0 0

2017 2018 2019 2020 2021 2017 2018 2019 2020 2021F 2022F 2023F 2024F

WTI Condensate WCS WCSB Condensate Supply Imports Required WCSB Condensate Demand

• Heavy reliance on imported volumes from the US results in • WCSB condensate demand is expected to stay well in excess of

Canadian condensate trading within a very tight range to WTI local supply for the foreseeable future

(1) Source: Bloomberg.

(2) Source: ARC Risk Research, AER, BCOGC, COLC.

(3) Forecast includes the impact of GEI/USD Diluent Recovery Unit assuming 2021 on-stream date.

Continued reliance on imported condensate volumes is constructive for Canadian condensate pricing 30Significant Cash Flow Protection

Crude oil and condensate production hedged1 Natural gas production hedged1

Mbbl/day, % MMBtu/day, %

48 60% 720,000 60%

36 45% 540,000 45%

24 30% 360,000 30%

12 15% 180,000 15%

0 0% 0 0%

Q2 2021 Q3 2021 Q4 2021 2022 Q2 2021 Q3 2021 Q4 2021 2022

Production Hedged % Hedged Production Hedged % Hedged

(1) Positions as of May 5, 2021.

Well-hedged with a long-term focus on reducing downside risk in funds from operations and creating certainty in cash flows 311

Risk Management Contracts Positions at March 31, 2021

Q2 2021 to Q4 2021 2022 2023 2024 2025

Crude Oil – WTI US$/bbl bbl/day US$/bbl bbl/day US$/bbl bbl/day US$/bbl bbl/day US$/bbl bbl/day

Ceiling 56.65 12,113 56.17 11,000 - - - - - -

Floor 48.63 12,113 47.05 11,000 - - - - - -

Sold Floor 40.01 8,662 37.81 8,000 - - - - - -

Swap 40.01 1,662 - - - - - - - -

Sold Swaption2 43.00 1,338 - - - - - - - -

Total Crude Oil Volumes (bbl/day) 13,775 11,000 - - -

Crude Oil – MSW (Differential to WTI)3 US$/bbl bbl/day US$/bbl bbl/day US$/bbl bbl/day US$/bbl bbl/day US$/bbl bbl/day

Swap (6.11) 5,000 - - - - - - - -

Natural Gas – NYMEX Henry Hub4 US$/MMBtu MMBtu/day US$/MMBtu MMBtu/day US$/MMBtu MMBtu/day US$/MMBtu MMBtu/day US$/MMBtu MMBtu/day

Ceiling 3.15 177,891 3.13 115,000 2.74 10,000 2.74 10,000 - -

Floor 2.61 177,891 2.60 115,000 2.50 10,000 2.50 10,000 - -

Sold Floor 2.12 136,727 2.19 85,000 2.10 10,000 2.10 10,000 - -

Natural Gas – AECO 7A Cdn$/GJ GJ/day Cdn$/GJ GJ/day Cdn$/GJ GJ/day Cdn$/GJ GJ/day Cdn$/GJ GJ/day

Ceiling 2.41 120,000 2.52 160,000 2.40 90,000 2.40 90,000 2.73 20,000

Floor 1.95 120,000 1.99 160,000 1.87 90,000 1.87 90,000 2.00 20,000

Sold Floor - - 1.75 20,000 - - - - - -

Swap 2.30 83,345 2.23 20,000 2.06 10,000 2.06 10,000 - -

Sold Swaption2 - - 2.00 20,000 - - - - - -

Total Natural Gas Volumes (MMBtu/day) 370,625 285,607 104,782 104,782 18,956

Natural Gas – AECO Basis (Differential to NYMEX

Henry Hub) US$/MMBtu MMBtu/day US$/MMBtu MMBtu/day US$/MMBtu MMBtu/day US$/MMBtu MMBtu/day US$/MMBtu MMBtu/day

Sold Swap (0.93) 66,673 (0.88) 35,000 (0.91) 70,000 (0.91) 70,000 (0.66) 25,000

Total AECO Basis Volumes (MMBtu/day) 66,673 35,000 70,000 70,000 25,000

Natural Gas – Other Basis (Differential to NYMEX Henry

Hub)5 MMBtu/day MMBtu/day MMBtu/day MMBtu/day MMBtu/day

Sold Swap 110,000 110,000 80,000 4,973 -

Foreign Exchange Contract Settlement Date Notional Amount ($ millions) Exchange Rate (Cdn$/US$)

Bought Forward April 1, 2021 360 1.2605

Bought Call April 13, 2021 25 1.2810

Variable Rate Collar6 August 23, 2021 10 1.2549 - 1.3000

(1) The prices and volumes in this table represent averages for several contracts representing different periods. The average price for the portfolio of options listed above does not have the same payoff profile as the individual option contracts. Viewing the average price of a group of options is purely for indicative purposes. All positions are

financially settled against the benchmark prices.

(2) The sold swaption allows the counterparty, at a specific future date, to enter into a swap with ARC at the above-detailed terms. These volumes are not included in the total commodity volumes until such time that the option is exercised.

(3) MSW differential refers to the discount between WTI and the mixed sweet crude oil grade at Edmonton, calculated on a monthly weighted average basis in US dollars.

(4) Natural gas prices referenced to NYMEX Henry Hub Last Day Settlement.

(5) ARC has entered into basis swaps at locations other than AECO.

(6) Variable rate collar whereby if the Cdn$/US$ spot rate is below 1.2825 at expiry, the ceiling will re-adjust to 1.3000.

32Asset Details

Greater Dawson Sunrise Kakwa Ante Creek Attachie

Net production – Q1 2021

Crude oil & liquids (bbl/day) 20,885 41 101,300 8,534 2,619

Natural gas (MMcf/day) 469 245 477 51 12

Total (boe/day) 99,003 40,913 180,774 17,099 4,593

Land1

Net sections 231 36 779 196 308

Net acres 149,800 23,100 498,500 125,500 202,000

Working interest ~97% ~93% ~99% ~100% ~99%

PDP Reserves (MMboe) 139 66 259 22 7

Liquids (MMbbl) 26.5 - 141.2 11.1 3.3

Gas (Bcf) 679 394 708 67 20

(1) Denote Montney sections and acreage only.

Commodity and geographic diversity across asset portfolio provides optionality 331

Historical Performance

Production Net debt2 to FFO Dividends3

Mboe/day $ billions, ratio $ billions, % of FFO

180 1.6 2.5 8 120%

2.0

135 1.2 6 90%

1.5

90 0.8 4 60%

1.0

45 0.4 2 30%

0.5

0 0.0 0.0 0 0%

2021 YTD

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021 YTD

2021 YTD

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Montney Natural Gas (boe/day)

Non-Montney Natural Gas (boe/day) Net Debt (LHS)

Montney Crude Oil & Liquids (bbl/day) Annualized Funds from Operations (LHS) Cumulative Dividend (LHS)

Non-Montney Crude Oil & Liquids (bbl/day) Net Debt to Annualized Funds from Operations (RHS) Dividends as a % of Funds from Operations (RHS)

(1) Historical performance is for ARC as a stand-alone entity and presents results up to and including March 31, 2021.

(2) Net debt presented for 2021 onwards excludes lease obligations. Refer to the “Capital Management” note in ARC’s financial statements.

(3) Dividends as a per cent of funds from operations calculated as dividends before Dividend Reinvestment Plan and Stock Dividend Program.

ARC has managed a profitable business through all commodity price cycles 34

with its efficient Montney assets, capital discipline, and strong balance sheetESG Recognitions and Rankings

Member of MSCI Global Sustainability Index

MSCI ESG Rating: AAA Member of FTSE Russell’s FTSE4Good Index Series since 2018

Voluntary participant since 2007 Member of the 30% Club since 2018

2020 Climate Change Score: A-

2020 Water Security Score: B

Member of Sustainalytics’ Jantzi Social Index Member of Bloomberg’s Gender-Equality Index since 2021

View ARC’s 2020 ESG Report at www.arcresources.com/responsibility 35Advisory Statements

Advisory Statements

Notes Regarding Forward-looking Information

This presentation contains certain forward-looking statements and forward-looking information (collectively referred to as “forward-looking information”) within the meaning of applicable securities legislation about current

expectations about the future, based on certain assumptions made by ARC. Although ARC believes that the expectations represented by such forward-looking information are reasonable, there can be no assurance that such

expectations will prove to be correct. Forward-looking information in this presentation is identified by words such as “anticipate”, “believe”, “ongoing”, “may”, “expect”, “estimate”, “plan”, “forecast”, “will”, “continue”, “project”,

“sustain”, “maintain”, “target”, “objective”, “strategy”, or similar expressions and includes suggestions of future outcomes. In particular, but without limiting the foregoing, this presentation contains forward-looking information with

respect to: ARC's strategies and guiding principles; the ability of ARC to generate free funds flow and the anticipated uses thereof; the continued payment of ARC's quarterly dividend and its value and potential growth; the

anticipated growth in production through profitable development activities; the planned integration of Seven Generations Energy Ltd. and the benefits, cost savings, and synergies related thereto; the anticipated reduction in net

debt and expectations regarding net debt and net debt to funds from operations by year-end 2021; anticipated free funds flow and free funds flow yield for 2021; ARC's drilling inventory and planned organic growth; the

characteristics of ARC's core areas including production, drilling inventory, reserves life index, break-even prices and operating expenses, expected capital efficiencies, and planned development thereof; the planned

development of Attachie West Phase I and the targeted milestone dates, the anticipated capacity, the forecasted capital investment, expected netback, capital expenditures, production processed, and the generated free funds

flow related thereto; the planned normal course issuer bid to repurchase ARC common shares and the planned commitment to prioritizing returns to shareholders by growing per share metrics; the focuses and planned priorities

and objectives of ARC's assets and business in general; the anticipated core areas of ARC's future production; the anticipated Montney production level and associated maintenance capital; ARC's deleveraging plan; ARC's

expected liquidity pursuant to its credit facility and through other sources; the anticipated strength in natural gas pricing; the continued evaluation of strategic M&A opportunities; the expected cash return and return on average

capital employed in comparison to its Canadian peers; the ongoing impact of COVID-19, its effect on demand and market volatility, and its possible effect on ARC's future financial and operational results; guidance with respect to

ARC's production, expenses, and capital expenditures for 2021; ARC's 2021 capital program and the allocations to each of ARC's core properties and facilities; ARC's intention to monitor its guidance in respect of COVID-19 and

provide updates as required; ARC's continued commitment to ESG and the anticipated stakeholder and shareholder benefits; and other statements.

Readers are cautioned not to place undue reliance on forward-looking information as ARC's actual results may differ materially from those expressed or implied. ARC undertakes no obligation to update or revise any forward-

looking information except as required by law. Developing forward-looking information involves reliance on a number of assumptions and consideration of certain risks and uncertainties, some of which are specific to ARC and

others that apply to the industry generally. Material factors or assumptions on which the forward-looking information in this presentation include: ARC's ability to successfully integrate the business of Seven Generations Energy

Ltd.; access to sufficient capital to pursue any development plans; ARC's ability to issue securities; the impacts the acquisition of Seven Generations Energy Ltd. may have on the current credit ratings of ARC; forecast

commodity prices and other pricing assumptions; forecast production volumes based on business and market conditions; the accuracy of outlooks and projections contained herein; projected capital investment levels, the

flexibility of capital spending plans, and associated sources of funding; achievement of further cost reductions and sustainability thereof; applicable royalty regimes, including expected royalty rates; future improvements in

availability of product transportation capacity; opportunity for ARC to pay dividends and the approval and declaration of such dividends by the board of directors of ARC; cash flows, cash balances on hand, and access to ARC's

credit facility being sufficient to fund capital investments; foreign exchange rates; near-term pricing and continued volatility of the market; the ability of ARC's existing pipeline commitments and financial hedge transactions to

partially mitigate a portion of ARC's risks against wider price differentials; estimates of quantities of crude oil, natural gas, and liquids from properties and other sources not currently classified as proved; accounting estimates and

judgments; future use and development of technology and associated expected future results; ARC's ability to obtain necessary regulatory approvals; the successful and timely implementation of capital projects or stages thereof;

the ability to generate sufficient cash flow to meet current and future obligations; estimated abandonment and reclamation costs, including associated levies and regulations applicable thereto; ARC's ability to obtain and retain

qualified staff and equipment in a timely and cost-efficient manner; ARC's ability to carry out transactions on the desired terms and within the expected timelines; forecast inflation and other assumptions inherent in the guidance

of ARC; the retention of key assets; the continuance of existing tax, royalty, and regulatory regimes; the accuracy of the estimates of each of ARC's and Seven Generations Energy Ltd.’s reserve volumes; ARC's ability to access

and implement all technology necessary to efficiently and effectively operate its assets; the ongoing impact of COVID-19 on commodity prices and the global economy; and other risks and uncertainties described from time to

time in the filings made by ARC with securities regulatory authorities.

The forward-looking information in this presentation also includes financial outlooks and other related forward-looking information (including production and financial-related metrics) relating to ARC, including: the expectations of

ARC regarding free funds flow, free funds flow yield, net debt excluding lease obligations, production, funds from operations, net debt to funds from operations, netback, dividends, maintenance capital, available liquidity, capital

investments, capital expenditures, returns to shareholders, cash returns, return on average capital employed, expenses and expenditures, and anticipated cost savings. Any financial outlook and forward-looking information

implied by such forward-looking statements are described in ARC's MD&A, and its most recent annual information form, which are available on ARC's website at www.arcresources.com and under ARC's SEDAR profile at

www.sedar.com and are incorporated by reference herein.

37Advisory Statements

Basis of Preparation

All financial figures and information have been prepared in Canadian dollars (which includes references to “dollars” and “$”), except where another currency has been indicated, and in accordance with International Financial

Reporting Standards (“IFRS” or “GAAP”) as issued by the International Accounting Standards Board. Production volumes are presented on a before royalties basis.

Non-GAAP Measures

Certain financial measures in this presentation do not have a standardized meaning as prescribed by IFRS, such as free funds flow, free funds flow yield, return on average capital employed (“ROACE”), and netback, and

therefore are considered non-GAAP measures. See the “Capital Management” note of ARC's unaudited condensed interim consolidated financial statements as at and for the three months ended March 31, 2021 for further

information on other measures contained in this presentation including funds from operations and net debt. These measures may not be comparable to similar measures presented by other issuers. These measures have been

described and presented in order to provide shareholders, potential investors, and analysts with additional measures for analyzing ARC. This additional information should not be considered in isolation or as a substitute for

measures prepared in accordance with IFRS.

Free Funds Flow and Free Funds Flow Yield

Management uses free funds flow as a measure of the efficiency and liquidity of its business, measuring its funds available for capital investment to manage debt levels, pay dividends, and return capital to shareholders. The

Company computes free funds flow as funds from operations generated during the period less capital expenditures before undeveloped land purchases and property acquisitions and dispositions and free funds flow yield by

dividing free funds flow per share by the market price per share. By removing the impact of current period capital expenditures from funds from operations, Management believes this measure provides an indication to investors

and shareholders of the funds the Company has available for future capital allocation decisions.

Netback

ARC calculates netback on a total and per boe basis as commodity sales from production less royalties, operating, and transportation expense. ARC discloses netback both before and after the effect of realized gain or loss on

risk management contracts. Realized gain or loss represent the portion of risk management contracts that have settled in cash during the period and disclosing this impact provides Management and investors with transparent

measures that reflect how ARC’s risk management program can impact its netback. Management believes that netback is a key industry benchmark and a measure of performance for ARC that provides investors with

information that is commonly used by other oil and gas producers. The measurement on a per boe basis assists Management with evaluating operational performance on a comparable basis.

Return on Average Capital Employed

ARC calculates ROACE, expressed as a percentage, as net income (loss) plus interest and total income tax expense (recovery) divided by the average of the opening and closing capital employed for the 12 months preceding

period end. Capital employed is the total of net debt plus shareholders’ equity. ROACE since inception is the annual average net income (loss) plus interest and total income tax expense (recovery) for the years 1996 to 2020

divided by the average of the opening and closing capital employed over the same period. Refer to the “Capital Management” note in ARC’s financial statements for additional discussion on net debt. ARC uses ROACE as a

measure of long-term operational performance, to measure how effectively Management utilizes the capital it has been provided and to demonstrate to shareholders the sustainability of its business model and that capital has

been invested profitably over the long term.

Barrels of Oil Equivalent

Natural gas volumes have been converted to barrels of oil equivalent (“boe”) on the basis of six thousand cubic feet (“Mcf”) to one barrel (“bbl”). Boe may be misleading, particularly if used in isolation. A conversion ratio of 6 Mcf:

1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent value equivalency at the wellhead. Given that the value ratio based on the current price of crude oil

compared with natural gas is significantly different from the energy equivalency conversion ratio of 6:1, utilizing a conversion on a 6:1 basis is not an accurate reflection of value.

Throughout this presentation, crude oil refers to tight, light, medium, and heavy crude oil product types as defined by National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (“NI 51-101”). Natural gas refers

to shale gas and conventional natural gas product types as defined by NI 51-101. ARC’s production of conventional natural gas is considered to be immaterial. ARC’s core producing properties that are considered to be shale

gas include Attachie, Dawson, Parkland (including parts of Tower), and Sunrise, and as such, natural gas, condensate, and natural gas liquids (“NGLs”) are disclosed. ARC’s core producing properties that are considered to be

tight oil include Ante Creek and parts of Tower, and as such, crude oil, natural gas, and NGLs are disclosed. ARC’s core producing property that is considered to be light crude oil is Pembina, and as such, crude oil, natural gas,

and NGLs are disclosed. NGLs for Kakwa refer to natural gas liquids, except for condensate, which is reported separately. Natural gas for Kakwa refers to conventional natural gas and shale gas combined.

Throughout this presentation, when condensate is disclosed, it is done so as it is the product type that is measured at the first point of sale. As per the Canadian Oil and Gas Evaluation (“COGE”) Handbook, condensate is a by-

product of the NGLs product type. NGLs by-products include ethane, butane, propane, and pentanes-plus (condensate).

38Advisory Statements

Information Regarding Disclosure on Oil and Gas Reserves, Resources, and Other Oil and Gas Metrics

Unless otherwise specified, all reserves estimates disclosed in this presentation are derived from ARC's independent reserve evaluation prepared by GLJ Ltd. (“GLJ”) dated January 29, 2021, evaluating the crude oil, natural

gas, natural gas liquids, and sulphur reserves attributable to ARC's properties as of December 31, 2020 (the “Reserves Report”), and all resources estimates disclosed in this presentation are derived from ARC's independent

evaluation prepared by GLJ of ARC's lands in the Montney region, including Dawson, Parkland/Tower, Sunrise/Sunset, Sundown, Septimus, Attachie, Red Creek, and Mica in northeast British Columbia, and Pouce Coupe and

Ante Creek in Alberta as of December 31, 2018. The reserve and resource estimates contained herein are estimates only and there is no guarantee that the estimated reserves or resources will be recovered. Actual crude oil,

natural gas, and natural gas liquids reserves may be greater than or less than the estimates that are provided herein. ARC's belief that it will establish additional reserves over time with conversion of resources into reserves and

probable undeveloped reserves into proved reserves are forward-looking statements and are based on certain assumptions and is subject to certain risks, as discussed under the heading “Notes Regarding Forward-looking

Information” and in ARC's annual information form for the year ended December 31, 2018, dated March 14, 2019.

This presentation references “Total Petroleum Initially-In-Place” or “TPIIP”. TPIIP, as defined in the COGE Handbook, is that quantity of petroleum that is estimated to exist in naturally occurring accumulations. It includes that

quantity of petroleum that is estimated, as of a given date, to be contained in known accumulations, prior to production, plus those estimated quantities in accumulations yet to be discovered. A portion of the TPIIP is considered

undiscovered and there is no certainty that any portion of such undiscovered resources will be discovered. If discovered, there is no certainty that it will be commercially viable to produce any portion of such undiscovered

resources. With respect to the portion of the TPIIP that is considered discovered resources, there is no certainty that it will be commercially viable to produce any portion of such discovered resources. A significant portion of the

estimated volumes of TPIIP will never be recovered.

This presentation discloses ARC's expectations of future drilling inventory or locations. While certain of these estimated drilling locations may be consistent with “booked” drilling locations identified in the Reserves Report, as

having associated proved and/or probable reserves, other locations are considered “unbooked” as they have no associated proved and/or probable reserves in the Reserves Report or any associated resources other than

reserves. All drilling locations have been presented on a net basis. Unbooked locations are generated by internal estimates of Management based on prospective acreage and an assumption as to the number of wells that can

be drilled per section based on industry practice and internal review. Unbooked locations do not have attributed reserves or resources. Unbooked locations have been identified by Management as an estimation of the multi-year

drilling activities based on evaluation of applicable geologic, seismic, engineering, historic drilling, production, commodity price assumptions, and reserves information. There is no certainty that all unbooked drilling locations will

be drilled, and if drilled, there is no certainty that such locations will result in additional oil and gas reserves, resources, or production. The drilling locations on which wells are actually drilled will ultimately depend upon the capital

allocation decisions of royalty payors who have working interests in respect of such drilling locations and a number of other factors including, without limitation, availability of capital, regulatory approvals, crude oil and natural gas

prices, costs, actual drilling results, additional reservoir information that is obtained, and other factors. While certain of the unbooked drilling locations have been de-risked by drilling existing wells in relative close proximity to

such unbooked drilling locations, other unbooked drilling locations are farther away from existing wells, where Management has less information about the characteristics of the reservoir and therefore there is more uncertainty

whether wells will be drilled in such locations, and if drilled, there is more uncertainty that such wells will result in additional crude oil and natural gas reserves, resources, or production.

This presentation contains certain oil and gas metrics, including finding and development costs (or “F&D costs”) and reserves life index (or “years to sustain”) which do not have standardized meanings or standard methods of

calculation and therefore such measures may not be comparable to similar measures used by other companies and should not be used to make comparisons. These metrics have been included herein to provide readers with

additional measures to evaluate the Company's performance; however, such measures are not reliable indicators of the future performance of the Company and future performance may not compare to the performance in

previous periods and therefore such metrics should not be unduly relied upon. F&D costs are calculated by dividing the sum of the total capital expenditures for the year, in dollars, by the change in reserves within the applicable

reserves category, in boe. F&D costs, including future development costs (“FDC”), includes all capital expenditures in the year as well as the change in FDC required to bring the reserves, within the specified reserves category,

on production. F&D costs take into account reserves revisions and capital expenditure revisions during the year. The aggregate of the costs incurred in the financial year and changes during that year in estimated FDC may not

reflect total F&D costs related to reserves additions for that year. Management uses F&D costs as a measure of its ability to execute its capital program, the success in doing so, and of ARC's asset quality. Reserves life index or

“years to sustain” are calculated by dividing the reserves (in boe) in the referenced category by the midpoint of the production guidance (in boe) for the following year. Management uses this measure to determine how long the

booked reserves will last at current production rates if no further reserves were added

39Advisory Statements

Advisory – Credit Ratings

Credit ratings are intended to provide investors with an independent measure of credit quality of an issue of securities. Credit ratings are not recommendations to purchase, hold, or sell securities and do not address the market

price or suitability of a specific security for a particular investor. There is no assurance that any rating will remain in effect for any given period of time or that any rating will not be revised or withdrawn entirely by the rating agency

in the future if, in its judgment, circumstances so warrant.

Third-party Information

This presentation includes market, industry and economic data which was obtained from various publicly available sources and other sources believed by ARC to be true. Although ARC believes it to be reliable, it has not

independently verified any of the data from third party sources referred to in this presentation or analyzed or verified the underlying reports relied upon or referred to by such sources or ascertained the underlying economic and

other assumptions relied upon by such sources. ARC believes that its market, industry and economic data is accurate and that its estimates and assumptions are reasonable, but there can be no assurance as to the accuracy or

completeness thereof. The accuracy and completeness of the market, industry and economic data used throughout this presentation are not guaranteed and ARC makes no representation as to the accuracy of such information.

40Advisory Statements

Combined Pro Forma Reconciliations

This presentation includes certain financial and operational results of Seven Generations for the three months ended March 31, 2021, which are derived from the unaudited condensed interim consolidated financial statements of

Seven Generations as at and for the three months ended March 31, 2021 (the “Seven Generations Financial Statements”). The Seven Generations Financial Statements have been prepared in accordance with IFRS following the

same accounting policies as the annual audited consolidated financial statements of Seven Generations as at and for the years ended December 31, 2020 and 2019. Copies of the annual audited consolidated financial statements

of Seven Generations as at and for the years ended December 31, 2020 and 2019 are available under Seven Generations' SEDAR profile at www.sedar.com. The Seven Generations Financial Statements were reviewed and

approved by the Board of Directors of Seven Generations, consisting of ARC management, on April 29, 2021, and were reviewed by the Audit Committee of ARC on May 5, 2021. These results are included to provide the reader with

an understanding of how ARC established its expectations of the financial and operational results of the Company for the balance of 2021 and beyond following the completion of the Business Combination. In this presentation,

when these financial and operational results are added to the results of ARC for the three months ended March 31, 2021, they are referred to as “combined pro forma” results and assume the completion of the Business

Combination as of such date. The combined pro forma results stated herein do not have any standardized meanings under IFRS and therefore may not be comparable to similar measures presented by other entities.

Combined Pro Forma Funds from Operations Combined Pro Forma Net Debt excluding Lease Obligations

$ millions For the three months ended March 31, 2021 $ millions As at March 31, 2021

Seven Generations Seven Generations

Cash provided by operating activities 327.5 Senior notes 1,536.8

Change in non-cash working capital (53.1) Credit facility draws 180.0

Change in other long-term liabilities related to operating activities 26.2 Long-term portion of lease liabilities 50.1

Seven Generations funds from operations 300.6 Long-term portion of share-based compensation liability 7.1

1

ARC funds from operations 273.9 Current assets (411.8)

Combined pro forma funds from operations 574.5 Current liabilities 567.9

Combined Pro Forma Free Funds Flow 1,930.1

$ millions For the three months ended March 31, 2021 Current portion of risk management assets 22.5

Seven Generations Current portion of risk management liabilities (115.6)

Cash provided by operating activities 327.5 Net debt 1,837.0

Change in non-cash working capital (53.1) Long-term lease liabilities (50.1)

Change in other long-term liabilities related to operating activities 26.2 Seven Generations net debt excluding lease obligations 1,786.9

1

Funds from operations 300.6 ARC net debt excluding lease obligations 568.0

Investments in oil and natural gas assets (148.3) Combined pro forma net debt excluding lease obligations 2,354.9

Seven Generations free funds flow 152.3 (1) Refer to Note 9 “Capital Management” in ARC’s financial statements as at and for the three months ended March 31,

2 2021 and to the sections entitled “Funds from Operations” and “Capitalization, Financial Resources and Liquidity” in

ARC free funds flow 148.2 ARC’s MD&A.

Combined pro forma free funds flows 300.5 (2) Non-GAAP measure that does not have any standardized meaning under IFRS and therefore may not be comparable

to similar measures presented by other entities. Refer to the section entitled “Non-GAAP Measures” in ARC’s MD&A

and the advisory titled “Non-GAAP Measures” above. 41You can also read