Baird 2018 Global Industrial Conference - NYSE: TEN - Tenneco Inc.

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Baird 2018 Global Industrial Conference Chicago, IL NYSE: TEN November 8, 2018

Safe Harbor

Forward-Looking Statements

This communication contains forward-looking statements. These forward-looking statements include, but are not limited to, (i) all statements, other than statements of

historical fact, included in this communication that address activities, events or developments that we expect or anticipate will or may occur in the future or that depend

on future events and (ii) statements about our future business plans and strategy and other statements that describe Tenneco’s outlook, objectives, plans, intentions or

goals, and any discussion of future operating or financial performance. These forward-looking statements are included in various sections of this communication and the

words “may,” “will,” “believe,” “should,” “could,” “plan,” “expect,” “anticipate,” “estimate,” and similar expressions (and variations thereof) are intended to identify forward-

looking statements. Forward-looking statements included in this communication concern, among other things, benefits of the Federal-Mogul acquisition; the combined

company’s plans, objectives and expectations; future financial and operating results; and other statements that are not historical facts. Forward-looking statements are

subject to a number of risks and uncertainties that could cause actual results to materially differ from those described in the forward-looking statements, including the

outcome of any legal proceeding that may be instituted against Tenneco and others following the announcement of the transaction; the possibility that the combined

company may not complete the spin-off of the Aftermarket & Ride Performance business from the Powertrain Technology business (or achieve some or all of the

anticipated benefits of such a spin-off); the possibility that the transaction may have an adverse impact on existing arrangements with Tenneco, including those related to

transition, manufacturing and supply services and tax matters; the ability to retain and hire key personnel and maintain relationships with customers, suppliers or other

business partners; the risk that the benefits of the transaction, including synergies, may not be fully realized or may take longer to realize than expected; the risk that the

transaction may not advance the combined company’s business strategy; the risk that the combined company may experience difficulty integrating or separating all

employees or operations; the potential diversion of Tenneco management’s attention resulting from the transaction; as well as the risk factors and cautionary statements

included in Tenneco’s periodic and current reports (Forms 10-K, 10-Q and 8-K) filed from time to time with the SEC. Given these risks and uncertainties, investors should

not place undue reliance on forward-looking statements as a prediction of actual results. Unless otherwise indicated, the forward-looking statements in this release are

made as of the date of this communication, and, except as required by law, Tenneco does not undertake any obligation, and disclaims any obligation, to publicly disclose

revisions or updates to any forward-looking statements.

In addition, please see Tenneco’s financial results press release for factors that could cause Tenneco’s future performance to vary from the expectations expressed or

implied by the forward-looking statements herein.

2

Transformation in the Auto Space

Autonomous Driving Mobility Aftermarket Electrification/Hybridization Emissions Regulations

Tenneco is well-positioned to benefit from industry trends

3

Proven Track Record of Growth

(Tenneco only)

Since 2000, Tenneco has delivered: Tenneco Revenue (billion)

Industry Production◆ (million)

6%

• Value-add (VA) Revenue* growth outpacing LV industry production CAGR

• Margin expansion of over 300 bps

• Double-digit annual adjusted EPS growth $7.1B 6%

CAGR

$6.3B 2%

VA Revenue ($ billions) CAGR

3%

Adjusted EBIT† as a CAGR

% of VA Revenue

$4.7B

$3.8B 9.1% 9.1%

$3.1B

• Over past 10+ years, TEN outpaced industry

production by 2x

6.6% • Expect 3x outperformance through 2020

6.4%

6.0%

Leading ROIC† Performance

Total Revenue $ 3.5 $ 4.4 $ 5.9 $ 8.2 $ 9.3 5-year average 22.8%

Substrate Sales $ 0.4 $ 0.6 $ 1.2 $ 1.9 $ 2.2

◆ Source IHS Automotive January 2018 global light vehicles

Built to outperform – revenue growth and investment returns

* Value-add (VA) Revenue is total revenue less substrate sales. See slide 37 for further explanation. † See reconciliations to U.S. GAAP at end of presentation. 4

Transaction Unlocks Significant Value

acquired

Acquisition closed October 1, 2018; separation expected to be complete late 2019

This acquisition builds on Tenneco’s long-term strategy:

• Positions us to realign and then separate Tenneco’s and

Federal-Mogul’s lines of business, allowing them to be

managed according to their unique value propositions

• Enhances our ability to serve customers in both lines

• Opens up new opportunities to drive growth with products that

are complementary to Tenneco’s current product offering

• Building upon the strength, depth and industry experience of

the combined teams

• Significant synergies will drive shareholder value

Focused strategic objectives – moving faster and further to unlock value

5

Creating Two Focused Companies

Transformational acquisition of Federal-Mogul complete; plan to separate into two focused,

industry-leading, publicly traded companies

• Expect annual run-rate earnings synergies of at least $200M and one time working capital synergies of at least $250M

expected within 24 months after closing

Realignment and separation to unlock significant shareholder value

1. The Clean Air Aftermarket business is intended to be allocated to the Ride Performance business

6

Aftermarket & Ride Performance Company

One of the largest global multi-line, multi-brand aftermarket suppliers, with

an outstanding strategic position to capture Asia Pacific aftermarket growth

with a broad range of products. Strong systems capabilities will capitalize on

OE market trends in mobility, electrification/autonomous driving.

Revenue by Geography* Revenue by Product Revenue by Customer

PRO FORMA Volkswagen 7%

APAC 12% Motorparts (OE)

2017 REVENUE AAP / Carquest 6%

15%

$6.4B NAPA / Alliance 6%

Motorparts (AM)

North 37% Ford 5%

America

51% Other O’Reilly 5%

EMEA 56%

37% Ride Performance (OE) General Motors 5%

28%

Pep Boys / Auto Plus 3%

The Group 3%

Daimler 2%

Clean Air (AM) Ride Performance (AM) FCA 2%

5% 15%

Leading positions in established

markets – Americas & EMEA 57% aftermarket Very diversified customer base

* EMEA includes Tenneco South America and APAC includes Federal-Mogul South America 7

Aftermarket & Ride Performance

Aftermarket – Well Positioned to Win in All Markets

Products Position

• Shocks and struts Well-positioned to win in China

• Suspension systems

#1 Globally

• Steering, hubs #1 North America

• Combined strong “house of brands” expected to

• Driveline #3 EMEA capture growth in China

• Brake pads, shoes, linings

#1 North America

‒ Shared investments in salesforce & distribution

• Rotors and drums

‒ Combined brand power & OE pedigree

• Gaskets

• Seals

#1 Globally ‒ Product line & coverage

• Underhood service ‒ Wear and tear products (e.g. brake pads, wipers) can

• Ignition

#3 Globally provide earlier entry into market

• Brake pads, shoes, linings #2 EMEA

Global Vehicles in Operation

Unprecedented growth expected over next 15

• Emission control products #1 NA & EMEA years led by China

• Suspension links, bushings,

mounts, exhaust isolators #1 South America

• Shocks and struts

Trends in Americas and EMEA 1950 1960 1970 1980 1990 2000 2010 2020 2025 2030

• Vehicles in operation continue to grow and age

• Vehicle miles traveled increasing in Americas China forecast to be largest AM market by 2025

• Growing demand for advanced suspension products Source: OCIA, Frost & Sullivan

8

Aftermarket & Ride Performance

Complete “Around the Wheel” Offering

Comprehensive ride performance product portfolio

Upper control arm

Strut top mount

Ball joint

Leader in shocks, Strut assembly Leader in steering,

struts and suspension and

NVH/elastomers Inner and outer tie rods Hub assembly braking

Focused on Focused on

Suspension, Chassis and

including the Braking

Dampers

intelligent suspension (not shown)

portfolio Brake pads

Bushings

Linkages Lower control arm Brake rotors

Improved system level capability to capture intelligent suspension growth trends

Note: AM brands represented here; however, OE offerings are typically branded "Tenneco" or “Federal-Mogul" for respective components

Source: Company websites 9

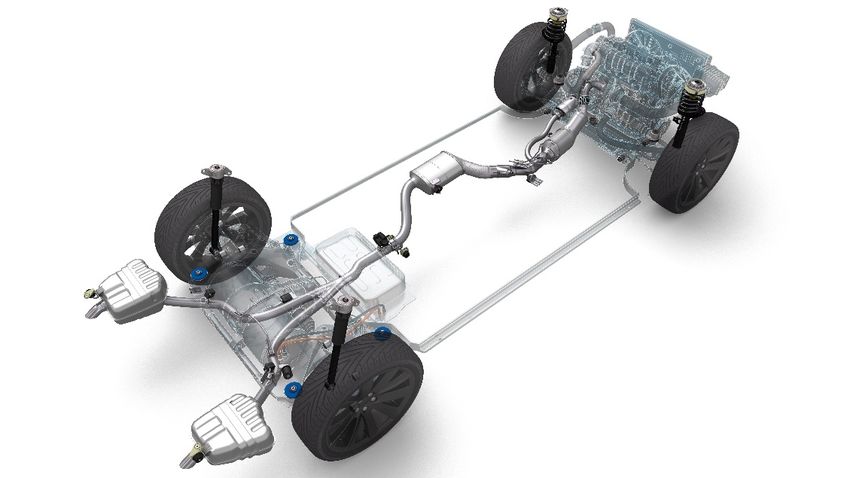

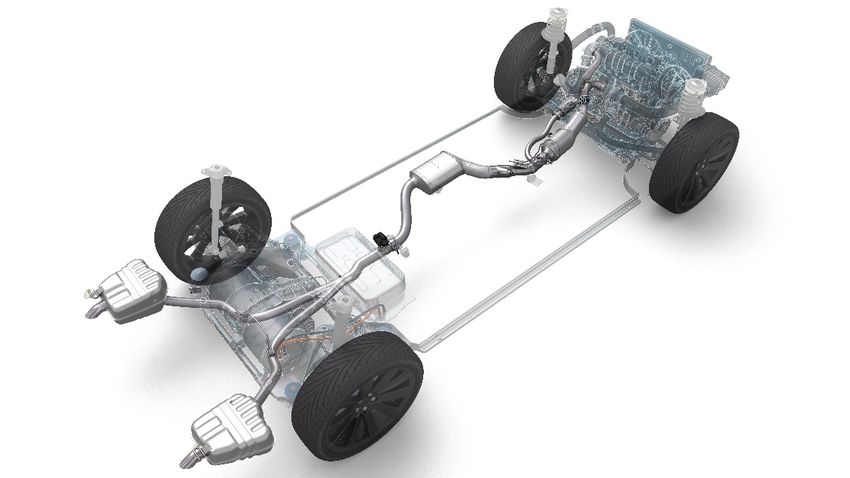

Powertrain Technology Company

Full Exhaust

Systems

Pistons Bearings

Catalytic Converters

Ignition Valves

One of the largest pure play powertrain suppliers globally positioned

Electronic Valve

to capture content growth due to tightening fuel economy and criteria

pollutant regulations, light vehicle hybridization trends and

Gasoline System Sealing /

commercial truck and off-highway expansion opportunities Particulate Filters Protection Heat Shields

Revenue by Geography* Revenue by End Market Revenue by Customer

PRO FORMA 2017 CTOH

APAC 15% General Motors 15%

REVENUE $10.7B 20%

VA REVENUE $8.5B North Industrial

America 9% Other VW 10%

39%

41%

Light Vehicle

76% Ford 10%

EMEA

39% Cummins 2%

Jaguar 2% FCA 8%

BMW 2% Daimler 6%

Renault Nissan Caterpillar

3% 3%

Leading positions in all geographies ~25% non-light vehicle Well represented across

all global OEMs

* EMEA includes Tenneco South America and APAC includes Federal-Mogul South America 10Powertrain Technology

Complementary Portfolio Brings Unique Competitive Position

Delivering an optimized trade-off between fuel economy and emission control from the cylinder to the tailpipe

MA N AGES: NOx MA N AGES:

• Friction / performance • Conversion efficiency

• Combustion temperature CO PM • Thermal management

• Ignition timing • Precious metal loading

Greenhouse Gases / Criteria Pollutants

Fuel Economy FULL SYSTEM

EMISSION

CONTROL

Regulation Driven

F-M Engine Components Tenneco Hot End Components

System capabilities enable better powertrain efficiency at a lower total system cost

11Powertrain Technology –

Significant Ongoing Light Vehicle Opportunity

Global light vehicle sales volume (M)

120 115 116 118 • ICEs are a significant portion

112 114

105

109 110 111

8% 9% 11% 13% BEV of vehicles moving forward

4% 6% 7%

102

99

100 94

97 1% 14% 15%

• Powertrain technology

90 91 5% 18% 19%

1%

3%

21% 23%

26% HEV

components support

80 hybridization; increased

complexity and content vs.

60 87% ICE

93% 92% 89% 85%

HEV or • Increasing CO2 and criteria

95% 94% 83%

40

97% 96% 79% 76% 73% 70% 66% 61% ICE1

ICE in pollutant emissions

2030 regulations provide organic

20

growth opportunities

• Content per vehicle increases

0 in both cylinder and

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

aftertreatment systems

1. Includes mild hybrid electric vehicle

Note: ICE = internal combustion engine, HEV = hybrid electric vehicle, BEV = battery electric vehicle

Source: BCG estimates

ICE and hybrids expected to be 85%+ of vehicle sales through 2030

12Powertrain Technology –

Significant Commercial Truck and Off-Highway Opportunity

Americas EMEA Asia Pacific

2030 CTOH Production: 1.3 million 2030 CTOH Production: 1.8 million 2030 CTOH Production: 6.6 million

Regulated Diesel 2018: 57% Regulated Diesel 2018: 62% Regulated Diesel 2018: 15%

Regulated Diesel 2030: 93% Regulated Diesel 2030: 94% Regulated Diesel 2030: 89%

Europe 757 1,180 239

504 Japan/Korea

1,026 China

537

1,578 1,399

North America

460

India

1,530

2030 Units (thousands) 133

129

Commercial Truck South America

Off-Highway Engines

CTOH regulated diesel volume may increase by nearly 6 million units by 2030, driven mainly by APAC

Source: PSR April 2018 & Tenneco forecasts, Fuel type = Diesel, NG/LPG, excluding emissions compliance = None 13Significant Synergy Potential

At Least $200M1 Earnings Synergies Expected Within 24 Months

($ in millions)

• Separate, dedicated integration

management team in place

Aftermarket & Sales and • Complementary product portfolio

Supply Chain G&A and Engineering

Ride Performance Go-To Market

reduces level of integration

$115 $35 $50 $30 complexity

‒ 80% - 85% of employees

Estimated costs to achieve of ~$80 million unaffected by integration

‒ No revenue synergies included

‒ No manufacturing synergies

included (footprint/process)

Powertrain • Reduction from three to two

Supply Chain Sales, G&A and Engineering corporate structures generates

Technology

$85 $40 $45 majority of G&A savings

• Expect 75% synergy run rate within

Estimated costs to achieve of ~$70 million one year of close

In addition, one time working capital synergies expected of at least $250M

1. Net of estimated public company costs.

14Key Transaction Progress –

Acquisition Closed on October 1, 2018

Antitrust clearance received from all Communicated net leverage expectation of

jurisdictions future companies at separation

• Expect Aftermarket & Ride Performance company (SpinCo)

On September 12, 2018, shareholders net leverage (net debt/adjusted EBITDA) around 3.0x at

approved all proposals necessary to complete separation – future net leverage goal of 1.5x to 2.0x

the acquisition of Federal-Mogul • Expect Powertrain Technology company (RemainCo) net

leverage around 2.3x at separation – future net leverage

CEOs named to lead two future independent goal of 1.0x to 1.5x

companies

• Brian Kesseler – CEO, Aftermarket and Ride Performance Completed syndication of new credit facility

Company

• Revolver $1.5B (see pricing grid)

• Roger Wood – CEO, Powertrain Technology Company

• Term Loan A $1.7B (see pricing grid)

• Term Loan B $1.7B (L + 275 @ 99.0 OID)

Powertrain Technology is the RemainCo

and will retain the Tenneco name Revolving Credit Facility

Net Leverage*

= 1.50x and =2.50x L+175

Separation into two publicly traded companies expected to be complete late 2019

*Net leverage as defined in credit agreement 15Substantial Value Creation Opportunity

(EV / 2018E

EBITDA)*

Reducing

16.0x

multiple gap Aftermarket & Powertrain

Ride Performance Technology

generates Comparables Comparables

12.0x

value creation

9.9x

opportunity

8.0x 7.0x

4.4x

4.0x

0.0x

Tiger Auto Aftermarket Powertrain Systems

Suppliers Suppliers

*FactSet and Company Filings as of April 6, 2018.

Separation provides investors with distinct investment opportunities

Note: Multiples shown represent medians of respective comp sets. Auto Aftermarket Suppliers includes MPAA, DORM and SMP. Powertrain Systems Suppliers includes BWA, CMI and DLPH.

1617

Key Terms of the Acquisition

• Purchase price of $5.4 billion; represents Enterprise Value / 2017 Adjusted EBITDA of 7.2x

Transaction Terms (5.4x1 including earnings and working capital synergies)

• Consideration funded with a combination of cash and Tenneco equity

• Cash portion of transaction financed through new senior credit facility

• Expected pro forma Net Debt / Adjusted EBITDA of approximately 3x at closing

Financing

• Targeting net leverage profile of ~2.5x by the end of 2019 through profitable growth and debt

reduction funded by cash flow

Icahn Enterprises, LP (“ Seller” ) received:

Ownership ‒ 5.65M Class A Voting Shares, representing 9.9% of Class A shares outstanding

‒ 23.79M Class B Non-Voting Shares, together representing 36.4% of total shares outstanding

• Seller will have one board member from close to separation and on Powertrain Technology after

the separation

Other ‒ Seller's Board representation will not transfer to the Aftermarket Ride Performance business on

separation

• As part of the transaction, the Seller will enter into a customary lock-up and standstill agreement

Timeline • Acquisition closed on October 1, 2018

1. Calculation: Purchase price less working capital synergies ($250M) / Federal-Mogul EBITDA plus earnings synergies ($200M) 18Federal-Mogul Overview

Federal-Mogul Revenue by Segment

Motorparts

Motorparts

2017 42%

• Over 20 strong market-leading brands in the

Revenue: $7.8B global vehicle aftermarket

EBITDA: $753M • Sells and distributes a broad portfolio of

Powertrain aftermarket products globally

58%

• Strong market position in OE braking

• Operates 33 manufacturing sites in 15 countries

and 33 distribution centers in 12 countries

Revenue by Geography* Revenue by End Market

APAC

15%

Industrial 10% Powertrain

CTOH 11% • One of the world’s leading powertrain

component and assembly providers

North

America

• Market leading positions across product

44% Light Vehicle categories

Aftermarket 49%

EMEA 30% • Operates 87 manufacturing sites in 19 countries

41%

Federal-Mogul is a leading global supplier to OEMs and the aftermarket

* APAC includes Federal-Mogul South America

19Tenneco Pro Forma Financial Overview

Tenneco Pro Forma Financial Overview

Total Value-add Adjusted Earnings EBITDA

Pro Forma FY 2017 Revenue ($B) Revenue ($B) EBITDA ($M) Synergies ($M)(2)(3) (w/ synergies) ($M)

Ride Performance (Plus CA AM)(1) $3.1 $3.1 $335 10.8% - -

F-M Motorparts 3.3 3.3 260 7.9% - -

Aftermarket & Ride Performance Company $6.4 $6.4 $595 $115 $710

Value-add EBITDA margin (w/ synergies) 9.3% (11.1%)

Clean Air (Less CA AM)(1) $6.2 $4.0 $533 13.3% - -

F-M Powertrain 4.5 4.5 493 11.0% - -

Powertrain Technology Company $10.7 $8.5 $1,025 $85 $1,110

Value-add EBITDA margin (w/ synergies) 12.1% (13.1%)

Pro Forma Tenneco $17.1 $14.9 $1,620 $200 $1,820

1. The Clean Air Aftermarket business is intended to be allocated to the Ride Performance business.

2. Represents annual run rate synergies expected to be achieved within 24 months.

3. Additional one time working capital synergies of at least $250M expected.

20Unique Strategic Combination

Aftermarket & Ride Performance Company Powertrain Technology Company

RIDE PERFORMANCE CLEAN AIR

One of the world’s leading multi-line One of the largest global pure play

aftermarket and OE suppliers powertrain suppliers

• Premier aftermarket brands, broad product coverage • Portfolio of engine-to-tailpipe products and system

and strong distribution solutions

• Strong portfolio of OE braking and advanced • Excellent position to capture content growth from:

suspension technologies and capabilities 1. Demand for improved engine performance

2. Tightening fuel economy and criteria pollutant

• Outstanding strategic position to regulations

1. Improve go-to-market capabilities in Americas & EMEA 3. Light vehicle hybridization trends

2. Capture Asia Pacific aftermarket growth with a broad 4. Commercial truck and off-highway expansion

range of products opportunities

3. Capitalize on new OE trends in mobility and • Well positioned to further build out the product

electrification / autonomous driving portfolio in an evolving powertrain market

Creates two strong businesses with scale and strategic and financial flexibility to drive long-term value creation

21Strong Balance Sheet

• Debt financing in place

Pro Forma Capitalization

• Robust liquidity over $2 billion

($ in millions)

Tenneco

12/31/2017

Transaction

Adjustments

Pro Forma

12/31/2017

• Cash flow generation enables rapid deleveraging

• Appropriate capital structure for each company will be

Cash & Equivalents $318 $460 $778

Undrawn Revolver 1,356 144 1,500

determined prior to separation

Liquidity $1,674 $604 $2,278

Revolving Credit Facility 244 (244) - Maturity Schedule

Term Loan A 390 610

1,310 1,000

1,700

Term Loan B - 1,700

2,400 1,700

2,400 $mm

Tenneco Notes 725 - 725

2,400

Federal-Mogul Notes - 1,278 1,278

2,000

Other Debt 95 160 255

Less: Unamortized Debt Issuance Costs (13) (98) (111) $1,598

1,600

Total Debt $1,441 $4,106 $5,547

$1,250

Net Debt $1,123 $3,646 $4,769 1,200 $1,022

Adj. EBITDA (before synergies) $868 $753 $1,620

800 $685

Net Leverage 1.3x - 2.9x $500

Net Leverage (after run rate synergies) - - 2.6x

400

$102 $102 $145

Pro Forma Shares Outstanding

0

Class A Shares Outstanding 51.4 5.7 57.1 2019 2020 2021 2022 2023 2024 2025 2026

Class B Shares Outstanding - 23.8 23.8

TLA TLB

Total Shares Outstanding(1) 51.4 29.4 80.9 Notes due 2022 (FM) Floating Notes due 2024 (FM)

Notes due 2024 (FM) Notes due 2024 (TEN)

1. Represents undiluted shares outstanding; pro forma ownership not adjusted for Tenneco’s Funding Adjustment Right. Notes due 2026 (TEN)

22Transformational Step –

Compelling Strategic Rationale

AM & RP PT

Strategically positions each company

Increases scale and broadens portfolio for respective markets

Enhances capabilities to capture growth with focused investments

Significant synergy potential in both new companies

Provides investors with distinct investment opportunities

Extends

Extendsexisting

existingstrategy

strategy and

and accelerates long-termvalue

accelerates long-term valuecreation

creation

23Stronger Together – Expanded Aftermarket

and Ride Performance Product Offering

Tenneco Ride Performance Federal-Mogul Motorparts

1 3

3 1 2

1 2 4

1 5

6

Chassis Brake pads

2 1 3 & Rotors

Suspension Systems 2 3

1 3 1 2 4

3 1 2

Engine (Pistons, Sealing &

2 2 Bearings, Valves) Gaskets

Elastomers

5 6

1 3

Exhaust Systems 1 2 Ignition Underhood

Not shown: wipers Service

Key Brands Legend Key Brands

Tenneco Ride Performance

Federal-Mogul Motorparts

Extensive portfolio of leading global and regional aftermarket brands

24Aftermarket & Ride Performance – Scale

Top Global AM Supplier Benefits of Scale

Aftermarket 2017 Revenues, Global ($B)

6

~6 • Broad product portfolio enables differentiated

5.6

customer and channel support

• Cross-category sales incentives with retailers and

4 3.7

Includes services, diagnostics, etc.

3.6

warehouse distributors

2.3 • Scale to support investments in digital and China,

1.8

2

1.5

1.3

and focused AM branding/marketing capabilities

Batteries only

1.2 1.1 1.0 1.0 0.9

• Rationalization of distribution networks for

0 improved service at lower cost

Tiger

SMP

Federal-Mogul

Bosch (est.)

SKF

Dorman

ZF

Valvoline

JCI

Mahler

KYB

AM/Ride Performance

Delphi Tech.

Tenneco

• Best practice sharing in go-to-market,

manufacturing and distribution

Leading global multi-line aftermarket supplier with a broad product portfolio

Source: Company estimates

25Aftermarket & Ride Performance

...Providing a Platform to Capture Growth in AV Trends and Ride Differentiation

The future of mobility is being re‐engineered

Physical

Vehicle Systems Infrastructure

Chassis Roads and Highways

T

Interior Vehicle to

O Control Systems Infrastructure

T

M Energy

O

O

D

R

A

R

Y Vision and

O Sensing Connected

W Road Detection 5G

Sensor Fusion Vehicle to Vehicle

ADAS System Cybersecurity

AR/VR Over the air

Intelligent Suspension: Reinventing the Ride of the Future

26Aftermarket & Ride Performance

Intelligent Suspension

• Expect advanced suspension to grow from 2% to more than 15% of LV production by 2025,

representing >40% of available market in 2025

• 25% revenue CAGR opportunity for advanced suspension growth through 2025

• Autonomous trend drives additional opportunities

Content per Vehicle

More than

A C T I VE S U S P E N SI ON 6x

RIDE PERFORMANCE

Average

S E M I -A C T I VE S U S P E N S I ON 4x

CO N VE N T I O N A L S U S P E N S I ON $50-$60

A segment F segment

Increasing demand for advanced suspension technologies to differentiate ride

Source: IHS database and Tenneco analysis 27Stronger Together –

Expanded Powertrain Product Offering

Tenneco Clean Air Federal-Mogul Powertrain

1

1 2 4 2 3

5

6 1 2 3

Catalytic Converters Full Exhaust Systems 1

3 5

6

3 4 7 Bearings Ignition Valves

Gasoline

4

Particulate Filters Electronic Valve 4 5 6

Diesel Particulate Filters

6 2 Sealing /

Pistons System

6 Protection Heat Shields

7 5

Selective Catalytic Diesel Oxidation

Reduction Catalyst

Key Trends

Key Trends Legend • CO2 / Fuel economy regulations

Tenneco Clean Air • Engine performance – downsized,

• Tightening emissions regulations

Federal-Mogul Powertrain higher output engines

• Electrification / Hybridization

• Strong OEM investments in ICE

• Strong OEM investments in powertrain

ICE powertrain

One of the largest pure powertrain suppliers with engine to tailpipe solutions,

addressing both greenhouse gas and criteria pollutant emissions

28Stronger Together – Enhanced Commercial Truck

and Off Highway Product Offering

Tenneco Clean Air Federal-Mogul Powertrain

1 2

1 2 3

Catalytic Converters Hydrocarbon

Manifold Dosing

3 Bearings Valves Steel

4 pistons

Gasoline Diesel Particulate

Particulate Filters 2 1 2 4 5

Filters

3 4 5

5 6 3 4 1 Systems Sealing /

Selective Catalytic Mixers 6 Protection Heat Shields

5

Reduction (SCR)

Systems

Key Trends

Key Trends • Tightening emissions regulations,

• Tightening emissions regulations, especially diesel NOx emissions

Legend

especially in India and China • Technology: alternative fuels,

Tenneco Clean Air

• More newly regulated powertrains dual fuel, friction reduction

through 2025 than regulated today Federal-Mogul Powertrain • CTOH industry consolidation

• CTOH industry consolidation • Global engine programs

• Global engine programs

Enhanced capabilities to provide products and systems solutions for the CTOH markets

29Controlled Power Technologies (CPT) Increases

Electrification and Hybridization Systems Capability

Sample Products Description Application

Provides inroads into

the hybrid market and CPT SpeedStart Substitute for standard alternator or starter motor in some Light vehicle

powertrain efficiency applications

technology that will enable Relevant for hybrid and start/stop vehicles

new growth opportunities Recuperates kinetic energy lost during deceleration

for PT Tech in the future Additional CPT variant– Speedtorq– offers torque profiling

COBRA • Stands for Controlled Boosting for Rapid Response Application • Industrial

• Type of water cooled electric supercharger

Recently secured a $100M • Capable of increasing air supply to internal combustion engines

OE contract launching in • Additional Cobra variant– FC– designed for fuel cell vehicles

2021 for development and

series production of TIGERS • Stands for Turbo-generator Gas Energy Recovery System • Commercial

advanced starter

• Converts exhaust gas energy into electrical energy • Light Vehicle

generator systems

• Key component in Clean Air’s Rankine systems and heat • Heavy duty

exchangers designed for CTOH markets

Source: Federal-Mogul

30Tightening Emissions Regulations

Regulatory-driven growth accelerates through the next decade

• Commercial Truck

– 2020-21 / 2023 – China VIa/VIb** Growth of Powertrains Under Regulation

– 2020 – India BS VI (skipping BS V)

– 2023-2027 – CARB & EPA Low NOx** (millions) 2016 2020 2025 CAGR

• Off-Highway CT: Euro VI (equivalent) 1.1 2.2 3.2 13%

– 2019 – EU Stage V Regulated Off-Hwy 1.1 2.1 4.3 16%

– 2020 – China 4R (equiv. EU Stage 3B + DPF) Total 2.2 4.3 7.5 15%

– 2020/2024 – India BS IV/India BS V

• Light Vehicle

Source: PSR production forecast and Tenneco estimates

– 2017-2025 – US Tier 3

– 2017-2021 – Euro 6c/6d Real Driving Emissions

– 2020/2023 – China 6a /6b**

– 2020 – India BS 6 (skipping BS 5)

CTOH market expands with increasing number of vehicles under regulation

** Tenneco estimates 31Clean Air – Hybrid Growth

Continuing Growth in Electrified Powertrains

Increasing space scarcity in hybrids drives higher engineering

System Design Average Value-Add Content

complexity and tougher packaging requirements EU6 Hybrid*

CPV expected to increase 30%-40% by 2025

Time Driver Example Gasoline System Design

$155 - $165

$135 - $145

2015 $110 - $120

Nomination

2015 2020 2025

GPF

Euro 6c

• 2017: 17 hybrid programs in production

Incremental

CPV • 2018: 11 hybrid program launches

$35 - $45

GPF + Resonator

Performance Secured Hybrid Program Wins

• Pre-2016 28 programs

• 2016 16 programs

Incremental • 2017 20 programs

High Voltage

Hybridization Li-Ion CPV

10% - 15% • YTD Q3 2018 9 programs

Battery

Program wins in hybrid electrified powertrains drive future Clean Air growth

* Market weighted average

32Diversified Business Profile

As a % of 2017 Revenue Product Applications

(VA Revenue)

CTOH

11%

Other GM

16.6% 13.9% Aftermarket

18%

2017

Chang'an 0.9% Clean Air

Geely 1.2% LV

49%

O'Reilly 1.2%

Ride

BMW 1.4% Performance

Ford LV

Beijing Automotive 1.5%

13.2% 22%

Advance 1.8% More than 600

NAPA/Alliance 2.0% customers Regions

John Deere 2.0%

(Total Revenue) (VA Revenue)

PSA 2.1% VW Group Rest of

AP

Caterpillar 7.9% 5%

2.6% China

Renault/ 15%

Nissan

3.4% Daimler

Toyota North

3.4%

FAW

6.3% 2017 America

46%

Tata

4.3% SAIC FCA

4.3% 5.0% Europe

5.0% 30%

South America

4%

Diversified business profile enables long-term growth

33Diversified Profile – Robust Platform Mix

As a % of Total 2017 Revenue

34Financial Results Disclaimer

Use of Non-GAAP Financial Information

In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”)

included in this presentation, the company has provided information regarding certain non-GAAP financial measures.

These measures include Earnings Before Interest Expense, Income Taxes, Noncontrolling Interests and Depreciation and

Amortization (“EBITDA*”), Net Debt, Value-Add Revenue, Adjusted EBITDA*, Adjusted Earnings Before Interest Expense,

Income Taxes and Noncontrolling Interests (“Adjusted EBIT”), Adjusted Earnings Per Share, and Return on Invested Capital.

Reconciliations of these non-GAAP financial measures to the comparable GAAP measure are included in this presentation.

* Including noncontrolling interests.

35Tenneco Projections

Tenneco’s revenue outlook for 2018 is as of January 2018. Revenue assumptions are based on projected customer production schedules, IHS Automotive January

2018 forecasts, Power Systems Research January 2018 forecasts and Tenneco estimates.

Tenneco’s revenue outlook for 2020 is as of January 2018. Revenue assumptions are based on projected customer production schedules, IHS Automotive January

2018 forecasts, Power Systems Research January 2018 forecasts and Tenneco estimates.

In addition to the information set forth on slide 4, Tenneco’s revenue projections are based on the type of information set forth under “Outlook” in Item 7 –

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” as set forth in Tenneco’s Annual Report on Form 10-K for the year

ended December 31, 2017. Please see that disclosure for further information. Key additional assumptions and limitations described in that disclosure include:

• Revenue projections are based on original equipment manufacturers’ programs that have been formally awarded to the company; programs where the

company is highly confident that it will be awarded business based on informal customer indications consistent with past practices; and Tenneco’s status as

supplier for the existing program and its relationship with the customer.

• Revenue projections are based on the anticipated pricing of each program over its life.

• Except as otherwise indicated, revenue projections assume a fixed foreign currency value. This value is used to translate foreign business to the U.S. dollar.

• Revenue projections are subject to increase or decrease due to changes in customer requirements, customer and consumer preferences, the number of

vehicles actually produced by our customers, and pricing.

Certain elements of the restructuring and related expenses, legal settlements and other unusual charges we incur from time to time cannot be forecasted

accurately. In this respect, we are not able to forecast EBIT (and the related margins) on a forward-looking basis without unreasonable efforts on account of these

factors and the difficulty in predicting GAAP revenues (for purposes of a margin calculation) due to variability in production rates and volatility of precious metal

pricing in the substrates that we pass through to our customers.

Tenneco’s revenue projection constitutes a forward-looking statement. We also refer you to the cautionary language regarding our forward-looking statements set

forth in the Safe Harbor statement on slide 2.

36Adjusted EBIT as a Percentage of Value-add Revenue –

Reconciliation of Non-GAAP Results

$ Millions

2017 2015 2010 2006 2005 2000

Value-add revenue (1) $ 7,087 $ 6,293 $ 4,653 $ 3,755 $ 3,759 $ 3,127

Clean Air substrate sales $ 2,187 $ 1,888 $ 1,284 $ 927 $ 681 $ 401

Total revenue $ 9,274 $ 8,181 $ 5,937 $ 4,682 $ 4,440 $ 3,528

EBIT $ 417 $ 508 $ 281 $ 196 $ 217 $ 122

Adjustments (reflect non-GAAP (2) measures)

Restructuring and related expenses 72 63 19 27 12 61

Pension / post retirement charges 13 4 6 (7) - -

New aftermarket customer changeover costs - - - 6 10 -

Goodwill impairment 11 - - - - -

Reserve for receivables from former affiliate - - - 3 - -

Antitrust settlement accrual 132 - - - - -

Warranty settlement 7 - - - - -

Gain on sale of unconsolidated JV (5) - - - - -

Other non-operational items - - - - - 4

Adjusted EBIT (non-GAAP Financial Measures) (3) $ 647 $ 575 $ 306 $ 225 $ 239 $ 187

Adjusted EBIT as a % of value-add revenue (4) 9.1% 9.1% 6.6% 6.0% 6.4% 6.0%

(1) Tenneco presents the above reconciliation of revenues in order to reflect value-add revenues separately from substrate sales, which include precious metals pricing, which may be volatile. Substrate sales occur when, at the direction of its OE customers,

Tenneco purchases catalytic converters or components thereof from suppliers, uses them in its manufacturing processes and sells them as part of the completed system. While Tenneco original equipment customers assume the risk of this volatility, it impacts

reported revenue. Excluding substrate sales removes this impact. Tenneco uses this information to analyze the trend in revenues before this factor. Tenneco believes investors find this information useful in understanding period to period comparisons in the

company's revenues.

(2) Generally Accepted Accounting Principles.

(3) Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results in a manner that allows a better understanding of the results of operational activities separate from the financial impact of decisions made for

the long-term benefit of the company and other items impacting comparability between the periods. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar types of adjustments can reasonably be expected to be

recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because its calculation is based on the subjective determinations of management regarding the nature and classification of events and

circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and analyze the results of the business. The company believes investors

find the non-GAAP information helpful in understanding the ongoing performance of operations separate from items that may have a disproportionate positive or negative impact on the company’s financial results in any particular period.

(4) Tenneco presents adjusted EBIT as a percentage of value-add revenue to assist investors in evaluating our company’s operational performance without the impact of substrate sales.

37Adjusted Earnings Per Share –

Reconciliation of Non-GAAP Results

$ Millions 2017 2000

Earnings Per Share $ 3.91 $ (1.18)

Adjustments (reflect non-GAAP measures):

Restructuring and related expenses 1.12 1.21

Antitrust settlement accrual 1.61 -

Goodwill impairment 0.20 -

Warranty settlement 0.09 -

Gain on sale of unconsolidated JV (0.08) -

Pension / post retirement charges 0.17 -

Costs related to refinancing 0.02 -

Tax adjustments from US tax reform 0.28 -

Net tax adjustments (0.43) -

Other non-operational items - 0.07

Adjusted Earnings Per Share (1) $ 6.89 $ 0.10

(1) Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results in a manner that allows a better understanding of the results of operational activities separate from

the financial impact of decisions made for the long-term benefit of the company and other items impacting comparability between the periods. Adjustments similar to the ones reflected above have been recorded in

earlier periods, and similar types of adjustments can reasonably be expected to be recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because

its calculation is based on the subjective determinations of management regarding the nature and classification of events and circumstances that investors may find material. Management compensates for these

limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and analyze the results of the business. The company believes investors find the non-GAAP information helpful in

understanding the ongoing performance of operations separate from items that may have a disproportionate positive or negative impact on the company’s financial results in any particular period.

38Return on Invested Capital –

Reconciliation of Non-GAAP Results

$ Millions, Unaudited 2012 2013 2014 2015 2016 2017

Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31

Short-term Debt $ 113 $ 83 $ 60 $ 86 $ 90 $ 83

Long-term Debt 1,052 1,006 1,055 1,124 1,294 1,358

Redeemable Noncontrolling Interests 15 20 34 41 40 42

Tenneco Inc. Shareholders' Equity 246 432 495 425 573 686

Noncontrolling Interests 45 39 40 39 47 46

Invested Capital $ 1,471 $ 1,580 $ 1,684 $ 1,715 $ 2,044 $ 2,215

Average Invested Capital $ 1,526 $ 1,632 $ 1,700 $ 1,880 $ 2,130

EBIT $ 422 $ 489 $ 508 $ 516 $ 417

Adjustments (reflect non-GAAP (1) measures)(2)

Restructuring and related expenses 78 49 63 36 72

Antitrust settlement accrual - - - - 132

Goodwill impairment - - - - 11

Warranty settlement - - - - 7

Gain on sale of unconsolidated JV - - - - (5)

Bad debt charge - 4 - - -

Pension / post retirement charges / Stock vesting - 32 4 72 13

Adjusted EBIT (non-GAAP financial measure)(2) 500 574 575 624 647

Effective Tax Rate 35.7% 33.7% 32.9% 26.6% 24.5%

Tax effected Adjusted EBIT $ 321 $ 381 $ 386 $ 458 $ 488

Return on Invested Capital (ROIC)(3)

21.1% 23.3% 22.7% 24.4% 22.9%

(non-GAAP financial measure)(2)

5 year Average Invested Capital $ 1,785

5 years Average tax effected Adjusted EBIT 407

5 year Average ROIC 22.8%

(1) Generally accepted Accounting Principles

(2) Tenneco presents the above reconciliation of non-GAAP results in order to allow a better understanding of our performance.

(3) We consider Return on Invested Capital (ROIC) to be a meaningful indicator of our operating performance, and we evaluate ROIC because it measures how effectively we use the capital we invest in our operations. Tenneco defines ROIC as tax effected

Adjusted EBIT divided by Average Invested Capital, which is the beginning and ending balances of debt, equity and noncontrolling interests. See the tabular calculation above. 39Adjusted EBITDA –

Reconciliation of Non-GAAP Results

$ Millions Year Ended December 31, 2017

Tenneco Federal Mogul Pro Forma

Net Income $274 $361 $635

Interest Expense 73 148 221

Income Tax Expense / (Benefit) 70 (190) (120)

Depreciation and Amorization 224 398 622

EBITDA $641 $717 $1,357

(1)

Adjustments (reflect non-GAAP measures)

Restructuring and related expenses 69 37 106

Pension and post retirement charges 13 - 13

Goodwill and intangible asset impairment 11 11 22

Antitrust settlement accrual 132 - 132

Warranty settlement 7 - 7

Gain on sale of unconsolidated JV (5) - (5)

Loss on debt extinguishment - 4 4

Gain on sale of assets - (7) (7)

Gain from termination of customer contract - (6) (6)

Warranty release - (4) (4)

Release of deferred purchase price payment - (3) (3)

EBITDA contribution of pending asset sales - (2) (2)

Other - 6 6

Adjusted EBITDA (non-GAAP Financial Measure)(2) $868 $753 $1,620

1. Generally Accepted Accounting Principles.

2. Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results in a manner that allows a better understanding of the results of operational activities separate from the financial impact of decisions made for

the long-term benefit of the company and other items impacting comparability between the periods. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar types of adjustments can reasonably be expected to be

recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because its calculation is based on the subjective determinations of management regarding the nature and classification of events

and circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and analyze the results of the business. The company believes

investors find the non-GAAP information helpful in understanding the ongoing performance of operations separate from items that may have a disproportionate positive or negative impact on the company’s financial results in any particular period.

40Reallocation of Clean Air Aftermarket –

Reconciliation of Non-GAAP Results

Year Ended December 31, 2017

$ Millions Clean Air Ride Performance Other Total

Total Revenue $ 6,517 $ 2,757 - $ 9,274

Less: Clean Air Substrates (2,187) - - (2,187)

Reported Value Add Revenue $ 4,330 $ 2,757 - $ 7,087

Less: Reallocation of Clean Air AM (302) 302 - -

Value Add Revenue (post Reallocation of Clean Air AM) $ 4,028 $ 3,059 - $ 7,087

Adjusted EBIT $ 478 $ 255 ($86) $ 647

Plus: D&A 147 77 - 224

Less: Restructuring adjustments included in Other segment - - (3) (3)

Adjusted EBITDA $ 625 $ 332 ($89) $ 868

Less: Allocation of Other segment (54) (35) 89 -

Less: Reallocation of Clean Air AM (38) 38 - -

Adjusted EBITDA (post Reallocation of Clean Air AM)

$ 533 $ 335 - $ 868

(non-GAAP Financial Measure)1

(1) Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results in a manner that allows a better understanding of the results of operational activities separate from the financial impact of

decisions made for the long-term benefit of the company and other items impacting comparability between the periods. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar types of adjustments

can reasonably be expected to be recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because its calculation is based on the subjective determinations of management

regarding the nature and classification of events and circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and

analyze the results of the business. The company believes investors find the non-GAAP information helpful in understanding the ongoing performance of operations separate from items that may have a disproportionate positive or negative

impact on the company’s financial results in any particular period.

41You can also read