Baker Tilly 2020 National Budget - Taxation Highlights - Baker Tilly Chartered Accountants

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Baker Tilly

2020 National Budget

Taxation Highlights

Preamble

Objective

The 2020 National Budget

marks the transition from

austerity to a growth

stimulation and employment

generation era. Therefore,

the 2020 Budget prioritises

the following areas:

Content

Details on the economy, >Growth and productivity

budget priorities and >Job creation;

summarised allocations. >Competitiveness; and

>Strong, Sustainable and

Shared Development.

02 04

01 03 05

Baker Tilly Input

Theme

Announcement Summary of the proposed

“Gearing for Higher

The 2020 National Budget Productivity, Growth tax and customs measures.

was announced by the Hon. and Job Creation”.

Minister of Finance and

Economic development Prof

Mthuli Ncube on Thursday

the 14th of November 2019.

Key Budget Highlights

GDP Growth Fiscal policy

The economy is expected to contract by The fiscal policy objective is directed

about -6.5% in 2019, with prospects for at managing expenditure within the

marginal recovery by 3.0% in 2020 allocated budget supported by

non-inflationary financing and

complemented by a tight monetary

policy framework.

Inflation Budget deficit

Monthly inflation is expected to fall A budget deficit of ZWL$5.2 billion

to single digit figures from the first is anticipated which is 1.55% of GDP.

quarter of 2020 to close the year

around 2%.

Tax Highlights

1.0 Value Added Tax (VAT) 1.1 Value Added Tax Rate • Value added tax standard rate to be reduced from 15% to 14.5% with effect from 1 January 2020. 1.2 VAT registration threshold • The VAT threshold for compulsory registration has been reviewed from ZWL$60 000 to ZWL$1 000 000 for a period of 12 months. • The effective date is 1 January 2020. 1.3 Value Added Tax on Foreign Services • The definition of input tax has been amended to include imported services, meaning that registered operators will be able to claim input tax on foreign services.

2.0 Employment tax (PAYE) 2.1 Deemed Motoring Benefit • The proposed monthly deemed motoring benefits are as follows: • Executives of grant aided institutions to be exempted from the tax on deemed motoring benefits. • The proposal comes into effect on 1 January 2020.

2.2 Proposed employment tax bands and rates 2.3 Bonus exemption • Tax free threshold to be reviewed from ZWL$1,000 to ZWL5,000 with effect from 1 November 2019. 2.4 Taxation of retrenchment package • The non-taxable portion of the retrenchment package to be reviewed from ZWL$10 000 to ZWL$50 000 or one-third of the package, to maximum of ZWL$80 000, with effect from 1 January 2020

3.0 Corporate Tax 3.1 Intermediated money transfer tax Value of Non-Taxable Transactions • Tax free threshold to be reviewed from ZWL20 to ZWL100 • The maximum tax payable per transaction by corporates to be reviewed from the current ZWL$15 000 to ZWL$25 000 on transactions with values exceeding ZWL$1 250 000. • The measure is effective from 1 January 2020. IMTT incidence • The person undertaking the transaction has the obligation to account for IMTT not the mediator. Financial institutions will withhold and remit the tax to ZIMRA. Bulk Payments through Mobile Banking Platforms • Social transfers by Development Partners accredited in terms of the • Privileges and Immunities Act [Cap 3:03] to be exempted from IMTT with effect from 1 January 2020. • All other bulk payments through mobile Money Banking Platforms attract intermediated money transfer tax.

3.2 Corporate Income Tax Rate • Corporate income tax rate to be reviewed from the current rate of 25% to 24%, with effect from 1 January 2020. 3.3 Estimation of Corporate Income Tax • With reference to the 10% margin of error rule, the Commissioner General will exercise discretion to waive interest on taxpayers with a good track record of compliance, among other considerations in view of the prevailing unpredictable economic conditions. 3.4 Limitation of Interest on Foreign Denominated Loans • To minimise the loss on corporate income tax revenue, interest expenses on foreign loans will only be allowable as deductible expenses to the extent that the foreign currency exchange rate on such loans is determined through the inter-bank market. • This measure is with effect from 1 January 2020.

3.5 Youth Employment Tax Credit • A tax credit of ZWL$500 per month per employee to be introduced for corporates that employ an additional employee in a year of assessment. • The credit will be limited to a maximum of ZWL$60 000 per year of assessment. • The support Framework to be published through regulations, will target employers who meet the following conditions, among others: • The company should be registered for Personal Income Tax and compliant for the preceding tax period; • Tax credit will only be claimed after the additional employee has served a period of 12 consecutive months; • Employees should be aged 30 years and below at the time of employment; • For the purposes of the incentive, “employee” excludes a trainee, intern and apprentice; • The minimum wage payable to the new employee should be at least ZWL$2 000; • The tax credit will not apply to supervisory grades; and, • The tax credit will not apply to corporates with a turnover exceeding an equivalent of US$1 million. • The measure comes into effect from 1January 2020.

3.6 Taxation of E-Commerce • The tax threshold for e-commerce tax to remain in foreign currency. • Assessed losses to be removed from the computation of taxable income of non-resident person that provides satellite broadcasting services or facilitates trade of goods and services through electronic commerce platforms. • Non-resident persons that provide satellite broadcasting services or facilitate trade of goods and services through electronic commerce platforms to appoint a Representative Taxpayer, within 30 days of becoming liable to tax.

4. Customs and Excise 4.1 Suspension of Duty on Semi-Knocked Down (SKD) Kits • SKD kits to be removed from the specified list of goods liable for duty in foreign currency. • The facility to import SKD kits for double and single cabs motor vehicles at a reduced customs rate of 10% to be extended for another 3 years with effect from 1 December 2019. 4.2 Suspension of excise duty for paint manufacturing industry • Excise duty to be suspended for 150 000 litres of illuminating power kerosene per month imported by Approved Paint Manufacturers for a period of 12 months. • Effective date is 1st of January 2020. 4.3 Duty refund facility for small scale furniture manufacturers • A Duty Refund Facility on imported raw materials by Small Scale Furniture Manufacturers to be introduced. The duty will be claimable on a quarterly basis. • This measure is with effect from 1 January 2020.

4.4 Rebate on raw materials for pharmaceutical manufacturers • Additional raw materials to be imported under Rebate of Duty, with effect from 1 January 2020 as tabulated below:

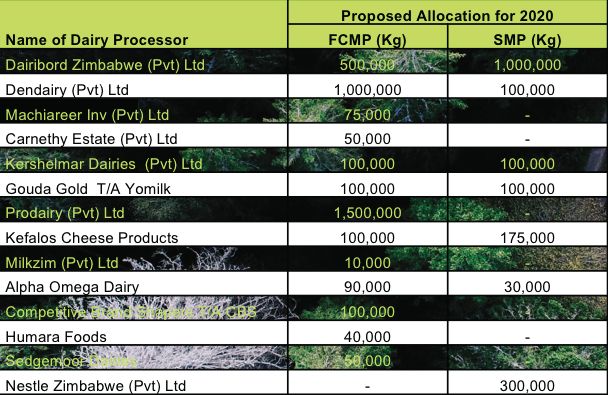

4.5 Suspension of Duty on Milk Powder • Duty suspension on milk powder to be extended to the year 2020. The table below details the allocation:

4.6 Suspension of Duty on Raw Cheese • Duty to be suspended on ring-fenced quantities of raw cheese, amounting to 25 000 kgs per month, for a period of 12 months beginning 1 January 2020. 4.7 Clothing Manufacturers Rebate • The Clothing Manufacturers Rebate Facility to be extended for a further 2 years, beginning 1 January 2020, in order to lower the cost of production. 4.8 Luggage Ware Manufacturers’ Rebate • Rebate of Duty facility on luggage ware manufacturers to be extended for a period of 2 years. • The Luggage Ware include handbags and inputs used in the production of handbags. • Effective date is 1st of January 2020. 4.9 Suspension of Excise Duty on Raw Wine • Excise duty free import quota on raw wine to be increased from 175 000 litres to 200 000 litres per annum for a period of 2 years beginning 1 January 2020. 4.10 Rebate of Duty on Capital Equipment • Rebate of Duty on capital equipment imported by operators of hotels and lodges to be extended for a further 3 years. • Effective date is 1 January 2020. 4.11 Suspension of Duty: Safari Operators • Suspension of Duty on motor vehicles used by Safari Operators for game views and drives to be extended for 24 months, beginning 1 January 2020.

4.12 Suspension of Customs Duty on Vehicles: Car Hire Companies for tourism purposes • Duty on vehicles by car hire companies to be suspended for a period of 12 months beginning 1 January 2020. • Beneficiaries of this facility should have been registered with the Zimbabwe • Vehicle Rentals Association and the Zimbabwe Tourism Business Council for a minimum of three years. • The facility will be restricted to new vehicles and the ring-fenced allocation is as follows: 50 light passenger motor vehicles of CIF values not exceeding US$50 000; and, 30 shuttle buses of a carrying capacity of 8–60 passengers. • The allocation will be determined by the size of business based on previous tax returns, and also limited to a maximum of 5 vehicles per operator. 4.13 Suspension of Customs Duty on Specified Vehicles: Tour Operators • Duty suspension on importation of vehicles for shuttle services provided by hotels and lodges to be extended for a further 1 year. 4.14 Suspension of duty on Cross-Border Luxury Coaches • Suspension of duty for cross border luxury coaches to be extended for a period of 12 months taking into account the outstanding quota. • Luxury bus operators have not been able to fully utilise the facility, due to foreign currency challenges. 4.15 Reduced customs rate on Public Services Buses • The facility for the importation of 100 buses at a reduced customs rate of 5% to be extended for 12 months beginning 1 January 2020. • Approval will be determined by the size of businesses based on previous tax returns, but limited to a maximum of 5 buses per operator.

4.16 Excise Duty on Tobacco

• Excise duty on tobacco to be reviewed from ZWL$50 to ZWL$100 per

1 000 cigarettes, with effect from 1 December 2019.

4.17 Rebate of Duty on motor vehicles imported by returning

students

• The value of motor vehicles that may be imported by returning students

has been limited to US$ 5 000 with effect from 1 January 2020.

4.18 Excise Duty on Fuel

• 5% of excise duty revenue collected on fuel to be channelled towards the

construction and rehabilitation of Beitbridge-Harare-Chirundu highway.

• This measure is effective from 1 January 2020.

4.19 Customs duty on Solar Home Lighting

• Customs duty on Solar Home Lighting Kits (Solar Home Systems) to be

removed and the list of energy saving products that are exempt from duty

to be expanded and include, Light-Emitting Diode (LED) Lamps and Solar

Street Lights.

• The effective date is 1 January 2020.

4.20 Customs duty on sanitary wear

• The exemption of customs duty on sanitary wear to be extended by a

further twelve months, with effect from 1 January 2020.

• Furthermore, sanitary cups and pants to be included on the list of duty

free products.

4.21 Review of Specific Rates of Customs & Excise Duty

• It is proposed that the prevailing Customs Exchange rate apply on specific

rates of customs and excise duty that were denominated in USD, with

effect from 1 December 2019.4.22 Rebate of Duty Facility on Motor Vehicles Imported by

Serving Public Servants

• In order to improve transparency and accountability in the utilisation of the

Rebate of Duty Facility on Motor Vehicles Imported by Serving Public

Servants, the following conditions to effected with effect from 1 January

2020:

Only motor vehicles purchased from traceable and registered Car

Dealers shall be eligible for rebate of duty;

Provide for the requirement for proof of source of funds where

Treasury has reservations;

In cases of suspected undervaluation, ZIMRA will revalue the motor

vehicle in line with the existing Customs Valuation regulations; and,

Variations in the maximum import values, depending on Grade as

follows:

• Failure to meet the above additional conditions will result in disqualification

of applications.4.23 Rebate of Duty on Goods Imported for Use in Approved Projects • In order to ensure transparency and accountability in the utilization of the facility of rebate on duty on imported goods for use in approved projects, the following additional conditions to be introduced: Completed Feasibility Studies endorsed by the responsible Ministry; Proof of funding for the project; Evidence of the physical place of business where the project will be undertaken; and Compliance to regulatory requirements such as Environmental Impact Assessments (EIA) and Local Authority by-laws. • Rebate of duty shall not be extended to beneficiaries who fail to demonstrate utilization of previous concessions.

5.0 Capital gains tax 5.1 Currency of payment • CGT to be paid in foreign currency where specified assets are disposed in foreign currency, or the seller fails to provide documentary evidence of local currency transaction. • Tax on the gross capital amount shall be paid in foreign currency. 5.2 Capital Gains Tax on Donated Houses • Donations of houses to Community Development Trusts to be exempted from capital gains tax.

6.0 Withholding Tax 6.1 Withholding Tax on Non-Executive Directors Fees • With effect from 1 January 2020, withholding tax on NED fees will be a final tax. Therefore, the NEDs will not be required to submit an income tax return at the end of the year of assessment. 6.2 Royalty on diamond • The royalty on diamond has been revised from 15% to 10% of the gross profit from 1 January 2020.

7.0 Tax administration measures 7.1 Reward for information • Penalties and interest to be removed from the definition of revenue for purposes of reward for information. • Currently revenue includes penalties and interest, which are, however, imposed at the discretion of the Commissioner. 7.2 Regulation of Clearing Agents • The period to acquire the requisite qualifications to practice as a clearing agent to be extended by a further 12 months with effect from 1 January 2020. 7.3 Designation of Port of Entry and Customs House • Mlambapele to be designated as a Port of Entry with effect from 1 December 2019. It will operate from 7.00am to 4.30pm daily. • To facilitate Ease of Doing Business the Minister has proposed the appointment of a Customs House in Gwanda with effect from 1 December 2019. 7.4 Customs Dry Ports • The Minister has proposed to designate Customs Dry Ports in Masvingo, Bulawayo, Makuti and Mutare, in order to relieve pressure on Ports of Entry.

8.0 Legislative Amendments

8.1 Tax Exemption on Venture Capital Financing

• The following conditions to apply on venture capital companies:

The Venture Capital Fund or company as well as the Recipient Company

should be residents and also be tax compliant.

The Recipient Company should not be listed on the stock exchange;

Recipient Companies should be in critical sectors of the economy, in

particular, agriculture, mining, manufacturing and tourism;

The Venture Capital Fund or company should not control (directly or

indirectly through a related entity) a Recipient Company in which it holds

shares; and,

Recipient Companies should primarily be financed through equity as

opposed to debt.

• For the avoidance of doubt, the Venture Capital Fund shall not benefit

from tax exemption if they invest in the following:

Trade carried on in respect of immovable property;

Trade carried on by financial institutions;

Trade carried on in respect of financial or advisory services, including

trade in respect of legal services, tax advisory services, stock broking

services, management consulting services, auditing or accounting

services; and,

Trade carried on in respect of gambling.ADVISORY • AUDIT • TAX • ACCOUNTING Phibion Gwatidzo Courage G. Matsa CA(Z) Chief Executive Officer Partner Cel: +263 772 209 211 Cel: +263 782 734491 phibion.gwatidzo@bakertilly.co.zw courage.matsa@bakertilly.co.zw Tapiwa Vela-Moyo Nyasha N. Machiri Leona Makuyana Tax Manager Senior Tax Consultant Tax Consultant Cel: +263 772 113820 C: +263 773 854919 C: +263 775 387478 tapiwa.vela-moyo@bakertilly.co.zw nyasha.machiri@bakertilly.co.zw leona.makuyana@bakertilly.co.zw Unit D & H Block 1, Celestial Park, Borrowdale Road, Harare Zimbabwe T: +263 242 369 730, 369 737, 301 598, 301 537 enquiries@bakertilly.co.zw www.bakertilly.co.zw Baker Tilly Chartered Accountants trading as Baker Tilly is a member of the global network of Baker Tilly International Ltd., the members of which are separate and independent legal entities.

You can also read