Broadcasting & Media Communications Department BCIT - Environmental Research Report By: Danielle Yallouz Site Centre

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Broadcasting & Media

Communications Department BCIT

Environmental Research Report

By: Danielle Yallouz

Site Centre

E xecutive Summary

The Television and Radio Broadcasting Industries in Canada are in a state of evolution.

Advancements in technology are causing a major shift in practices within the industry,

affecting not only companies participating and employees working in the industry, but

also who are studying to become a part of it. This report analyses both industries using

in-depth situation analysis. It also highlights the stages of product lifestyle, the

industry’s potential for growth, and external factors that are currently affecting the

industry.

Several major players who control the majority of the market share dominate both the

TV and radio broadcasting industry in Canada. This report investigates these

organizations’ responses to the expected transition and how they are dealing and

adapting with technological advancements.

Jobs within the field of television broadcasting and radio are also changing.

Companies are now requiring their employees have new, more modern skills sets, such

as digital publishing skills. Traditional jobs are being eliminated all together as the

online space begins to take over traditional forms of media. Furthermore, those who

have graduated with a broadcasting or journalism degree or diploma are working in

non-traditional jobs to the field, the majority business related.

There are multiple ways for broadcasters to stay relevant. These include embracing

non-linear distribution channels, exploring the world of website design and coding,

partnering with retail brands who are creating their own content, discovering the

concept of television and radio on the go, being part of the podcast generation, and

showcasing their personal brand through business education.

The top universities are starting to discover how to educate their broadcasting and

radio students in order to keep up with the digital media trend. Ryerson, Carleton, UBC

and the University of Guelph are just a few of the schools leading the way. This report

will outline exactly what they are doing to stay current.

It is important to note that the Canadian government is also supporting the television

and radio broadcasting industry by offering services in support of Canadian

broadcasters.

Lastly, a summary of Canadian scholarship and bursaries available for broadcasting

students concludes the report.

2

Television Broadcasting in Canada

Situation Analysis

Industry Definition

This industry is made up of facilities and studios that program and distributes audio-

visual content, which is then delivered to the public via over-the-air-transmission. It is

important to note that this industry does not include operators that only distribute

content online. However, it does include operators that are making the transition from

traditional broadcasting to online mediums.1

Category/Industry/Market Analysis

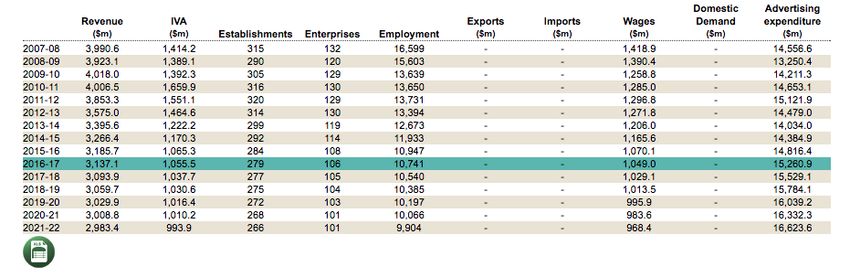

Aggregate Market Factors 1

a. Establisments: 279 (-)

b. Enterprises: 106 (-)

c. Employment: 10,741 (-)

d. Annual Revenue 2016/2017: $3137.1 million (-)

e. Industry Value Added (IVA): 1055.5 million (-)

f. Annual Growth Rate: -4.0%

*See Changes in Appendix A

Key E xternal Drivers 1

1. Total Advertising Expenditure

2. Number of Fixed Broadband Connections

3. Corporate Profit

4. Per Capita Disposable Income

Stage in Product L ife Cycle 1

The Broadcast Industry in Canada is currently in decline. It is predicted that the

Industry’s added value will diminish over the next 10 years at an annulized rate of

4.4%. In contrast, Canada’s GDP is expected to grow at an annulized rate of 1.8%

during the same time period.

Yet, experts have indicated that there is still hope for this decling industry. The media

landscape is drastically changing due to a rapid shift in technology. This shift is

causing a rise in audience consumption through online streaming channels and mobile

devices, disrupting traditional viewing practices.

3

Advertising revenue is now being captured by these new online media channels. So, the

industry is expected to restructre and embrace these new tehcnologies by using them

to enhance the broadcasting space. By changing their business models, operators are

hoping to recapture viewers and advertisers. Therefore, many experts are stating that

the indsutry is more accurately in transtion rather than in decline. 1

Sales Cyclicality /Seasonality

This industry is highly cyclical. Seasonal fluctuations also disturb broadcasting

revenue and are common within the industry. 2

Distribution Channels 1

a. Key buying industries-generating demand

i. Advertising Agencies in Canada

ii. Consumers in Canada

b. Key Selling Industries-generating supply

i. Movie & Video Distribution in Canada

ii. Movie, Television & Video Production in Canada

iii. Video Postproduction Services in Canada

Profits

At the end of 2017, profits are expected to equal a loss of 5.8% of revenue totaling $-

1.8 billon dollars. Over the last five years, advertisers have decreased investments in

traditional television channels. This is due to a shift in media consumption, mainly to

online platforms. It is causing advertisers to spend their budget on a diverse

assortment of media channels. As a result, television broadcasters have experienced a

major decline in revenue. In order to compensate, operators have lowered operating

costs by cutting labor and lowering investments in original programming.

Unfortunately, this has not done enough to counterbalance the decrease in revenue. 1

1“Television Broadcasting in Canada.”IBISWorld Canada , IBISWorld, 2017,

clients1.ibisworld.ca/reports/ca/industry/default.aspx?entid=1261.

2.Canada, Government of Canada Statistics. “Television Broadcasting, 2015.”Government of Canada, Statistics

Canada, 5 July 2016, www.statcan.gc.ca/daily-quotidien/160705/dq160705a-eng.htm.

4Porter’s F ive F orces Analysis

Threat of New E ntrants (L OW)

The threat of new entrants is LOW, so the barriers to enter the industry are HIGH. This

is mainly as a result of high market share concentration within the industry. There are

a few big players who dominate the broadcasting space, making it difficult for entrants

to access the viewer market as the existing operators have already captured them.

Furthermore, capital costs are increasingly high. The growth of external competition,

like alternate media including online streaming services, also causes difficulty for new

entrants. This industry is also highly regulated, which creates additional hurtles for

entrants to enter the industry. 1

Pressure from Substitutes (HIGH)

The threat of substitutes in the industry is extremely HIGH. Due to technology

developments, there has been major shift in the media landscape over the last five

years. Consuming media on mobile devices and online has become extremely popular.

This shift has eroded the television medium, which previously commanded the world’s

media sector and more importantly served as the main avenue for advertisers.

Consumers now have more options to consume content, threatening traditional

broadcasting operators. 1

It is interesting to note that over the last five years, total employment is estimated to

have decreased at an annualized rate of 4.8% to 10,741 workers. The number of

industry enterprises is also estimated to have fallen at an annualized rate of 3.9% to

106.3 This is all due to the threats from substitutes. A study done by Nielsen this year

has found that traditional TV viewing by 18-24 year olds has now fallen 41.3% since

2012; over a five-year period, more than 40% of this age group’s traditional TV viewing

time has been substituted by other activities or more likely alternative viewing

mediums, like online streaming.4

Industry Rivalry (HIGH)

Competition in this industry is HIGH exhibiting high market share concentration. In

2017, the top four players in the industry generated 75.3% of the industry’s total

revenue, dominating the market.1

3.Bradshaw, James. “Canada's New TV Rules Could Erode Jobs, Funding, Report Warns.” The Globe and Mail, The

Globe and Mail, 5 Jan. 2016, www.theglobeandmail.com/report-on-business/canadas-new-tv-rules-could-erode-

jobs-funding-report-warns/article28015965/.

4.“The Nielsen Total Audience Report: Q1 2017.” What People Watch, Listen To and Buy, 7 Dec. 2017,

www.nielsen.com/us/en/insights/reports/2017/the-nielsen-total-audience-report-q1-2017.html.

5.“Porter's Five Force Analysis for Lifestyle Broadcast Industry.” UKEssays,

www.ukessays.com/essays/business/porters-five-force-analysis.php.

5Bargaining Power of Suppliers (L OW)

In this Industry the Power of Suppliers is LOW. There are three main supply industries

supporting the Broadcasting Industry in Canada, movie and video distribution in

Canada, Movie, and Television & Video Production in Canada and video postproduction

services in Canada. Each of these industries has low market share concentration;

therefore there is not one company that has a majority of the market share giving

broadcasting networks many alternatives to choose from. 1

Bargaining Power of Buyers (HIGH)

Bargaining Power is HIGH for buyers in this industry. There is a vast amount of

channels and programs for viewers to choose from equating in high internal and

external competition within the industry. Furthermore brand loyalty for channels is

quite low, whereas loyalty to shows is usually high, giving the viewers even more power.

Lastly viewers are price sensitive when it comes to purchasing television packages

especially as technology evolves and provides viewers with less expensive viewing

options. 5

E nvironmental F actors

Demographics

The audience in Canada is changing. The Canadian Radio-television and

Telecommunications Commission (CRTC) stated that television demographics are now

more diverse, containing ethnic and linguistic groups, people with various disabilities

and a shifting age group.6 The Canadian population is getting older; causing a shift in

content that is targeting an older viewer demographic.

Technological

The media environment is very obviously evolving at quite high speeds. New

technology, including streaming networks, mobile devices- tablets and mobile

phones- and cable networks are disrupting the industry by causing it to fragment and

erode revenue streams. These new technologies are replacing the traditional television

medium, as well as becoming more and more popular. The number of fixed broadband

connections, which is negatively correlated with industry revenue because it

represents the number of households and businesses that have access to broadband

Internet, is expected to reach 14.8 million in 2022.1

6.Government of Canada, Canadian Radio-television and Telecommunications Commission (CRTC). “Offering

Cultural Diversity on TV and Radio.” Government of Canada, Canadian Radio-Television and Telecommunications

Commission (CRTC), 14 June 2017, www.crtc.gc.ca/eng/info_sht/b308.htm.

7.Watters, Haydn. “Here's What You Think a Pick-and-Pay Model Means for TV's Future.”CBCnews, CBC/Radio

Canada, 2 Feb. 2016, www.cbc.ca/news/business/pick-pay-cable-cbc-forum-1.3430193.

6This proves that viewers are starting to adopt mobile devices and streaming services.

In response, broadcasters are beginning to restructure their business models to better

serve their digital customers and recapture advertising revenue. Operators will become

more flexible in their content they offer to consumers. For example, offering a “pick

and pay model” where viewers can choose to subscribe to specific channels that they

most enjoy watching, without having to buy an entire package.7 Furthermore, the CRTC

is contemplating allowing greater access to non-Canadian programming.6 Next,

Broadcasters are anticipated to create more interactive ways of consuming television

by customizing the viewing experience for audiences and making TV more accessible

on multiple platforms. An example of this is allowing viewers to purchase products

displayed in commercials with “simply a click of a remote”. 6

Market Response

1. CBC-43.9% Market Share1

a. CBC has focused on expanding its digital and multi-platform offerings

and scaling back its traditional television offerings. Through these

digital advancements, CBC aims to give their content, which they air

first through a traditional broadcast, “a second life on digital platforms”.

CBC is working to establish a higher quality OTT video experience for its

viewers, set to replace the current CBC player, using the URL

“watch.cbc.ca”. CBC also pledges to focus on mobile content delivery. 9

“Embracing our digital shift means rethinking how we produce, format and distribute

content. Digital is no longer seen as a separate entity; it is woven into all that we do as

we work towards a truly multiplatform experience across our services.” –CBC Annual

Report 2015 9

2. Bell Canada- 18.2% Market Share1

a. Bell’s strategy is acquisition, focusing on relevant, high rated content,

sports and international news. They recently acquired “Astral Media”,

which was Canada’s largest radio broadcaster with 84 radio stations

across eight provinces. They were also a big player in specialty premium

television. The company predicts a shift to digital media and because of

their involvement in subscription television, expects higher

programming costs in the future. Bell is planning to focus on continuing

to improve on its popular LTE network, leverage its strong wireless

communications and innovate in emerging media platforms. Bell

continues to improve and innovate with their online steaming service

“CraveTV”, which is currently growing in audience. “CraveTV” has

7introduced a “TV Everywhere” option providing live and on demand

television content on mobile devices. 10

“Bell continued to build on our position as Canada’s broadband communications

leader in 2016. We are investing in the most advanced networks and service

innovations to lead in the marketplace and ensure Canada’s competitiveness in a

global digital economy, while delivering consistent dividend growth to you, the

shareholders who have invested in Bell’s broadband strategy.” –George A. Cope,

President CEO Bell Canada 10

3. Corus Entertainment Inc.-7.6% Market Share1

a. The company has become a major player in the Broadcasting Industry

after the acquisition of Shaw Media in 2016. Going forward, Corus vows

to share content across multiple platforms, coordinating digital and

traditional coverage of all major events, leveraging TV personalities as

well as bundling TV and radio together, thus creating new revenue

opportunities. Corus plans to continue investing in “Ad Tech” while

strengthening premium brands across not online television and radio

but digital and social channels as well. 11

“We are well positioned to continue to build on the significant advances we made this

year towards our goal of transforming Corus from a traditional broadcaster, into a

future-focused, integrated media and content company.” –Doug Murphy, President &

CEO Corus Entertainment Inc. 11

4. Rogers Media Inc.-5.6% Market Share1

a. At the end of 2016, Rogers announced a long-term partnership with

Comcast in order to improve its video experience by introducing the X1

an all IP-based video platform. This scalable IPTV is expected to be fully

functional in early 2018. With this exciting innovation, viewers will

benefit from future innovations in voice, data, video, and smart home

monitoring devices. Rogers Media has also made a commitment to shift

from print to digital to satisfy changing consumer demands. 12

*For breakdown of financial performance of all four major players see Appendix B-E.

9.“Financial Reports • CBC/Radio-Canada.” Financial Reports, www.cbc.radio-canada.ca/en/reporting-to-

canadians/reports/financial-reports/.

10.“Financial Reporting.” Bell Canada Enterprises :: Annual Report » BCE,

www.bce.ca/investors/financialperformance/annual.

11.“Financial Reports.” Corus Entertainment, www.corusent.com/investor-relations/financial-reports/.

12.“Rogers Investor Relations.” Rogers Investor Relations, investors.rogers.com/.

8Radio Broadcasting in Canada

Situation Analysis

Industry Definition

This industry consists of broadcasting stations, networks and syndicates that transmit

programming through AM, FM and satellite radio channels. The industry does not

include operators that broadcast content exclusively through the Internet.13

Category/Industry/Market Analysis

Aggregate Market Factors 13

g. Establisments: 1,163 (- )

h. Enterprises: 595 (- )

i. Employment: 10,287 (- )

j. Annual Revenue 2016/2017: 1,711.4 (- )

k. Industry Value Added (IVA): 1,093.7 (- )

l. Annual Growth Rate (11-16): 0.0%

Key E xternal Drivers 13

1. Per Capita Disposable Income

2. Total Advertising Expenditure

3. Number of Fixed Broadband Connections

4. Totally Vehicle Kilometres

Stage in Product L ife Cycle

The Radio Broadcasting Industry in Canada is currently mature. The industry’s added

value during the 10 years to 2021, is expected to increase at 0.8% annualized rate. At

the same time, the Canadian GDP is expected to grow at annulized rate of 1.8%.

Although, the industry has seen stabaliztion over the last five years, there is an

increasing number of external and internal competition from other forms of broadcast

media threatning the industry. 13

Sales Cyclicality /Seasonality

This industry is cyclical. Seasonal fluctuations also disturb the radio broadcasting

revenue and are common within the industry.

13“Radio Broadcasting in Canada.”IBISWorld Canada , IBISWorld, 2017,

clients1.ibisworld.ca/reports/ca/industry/default.aspx?entid=1261.

9Distribution Channels 13

c. Key buying industries-generating demand

i. Consumers in Canada

d. Key Selling Industries-generating supply

i. Advertising Agencies in Canada

ii. Data Processing & Hosting Services in Canada

iii. Music Publishing in Canada

iv. Wired Telecommunications Carriers in Canada

Profits

In 2016, the average profit margin equaled a loss of 18.9% of revenue totaling $-323.5

million dollars. Over the past five years advertising expenditure has steadily increased,

aiding the industry to maintain its average profit margin notwithstanding the decline

in popularity of the radio. Overall, the industry is expected to be profitable over the

next five years, as radio broadcasters continue to challenge competition like Internet

radio and mobile platforms. The major players in the industry, for example Bell Canada

or Rogers Communications, are able to achieve high profit margins up to 40%. 13

Porter’s F ive F orces Analysis

Threat of New E ntrants (L OW)

The threat of new entrants is LOW. Therefore, the barriers to entry in this industry

are high and steady. This is mainly as a result of the many regulations that must be

followed within the industry. For example, the Canadian Radio-television and

Telecommunications Commission (CRTC)’s Music, Artist, Performance and Lyrics

system have implemented a federal quota mandating that a percentage of radio

broadcaster’s musical selection must be written by, recorded, or performed by a

Canadian. Lastly, high consumer loyalty can act as an additional barrier to enter the

industry. 13

Pressure from Substitutes (HIGH)

External competition in the industry is quite HIGH and comes in many different

forms, including audio and visual media. For example, the increased popularity of

mobile music devices and streaming Internet radio is a threat to the industry. In

order to contest the emergence of new listening technology, broadcasters have

begun to stream their programs online and offer free mobile applications in order to

capture a younger audience. 13

Industry Rivalry (ME DIUM)

Competition in this industry is MEDIUM, exhibiting medium market share

concentration. In 2017, the top four players in the industry generated 57.0% of the

industry’s total revenue. 13 Because these companies own multiple stations and

control the majority of the market share, they are able to charge a premium-

10advertising rate to companies trying to reach a wide audience across multiple

locations. This makes it challenging for smaller operators to cover costs because

initially they do not have a large enough audience to capture advertisers willing to pay

premium.

Bargaining Power of Suppliers (Moderate)

Depending on the size of the radio broadcasting station, the industry has a varied

bargaining power for suppliers. However, because the nature of the industry is

changing and a growing number of larger radio operators are buying smaller

companies, we can conclude that suppliers are experiencing an increasing amount of

challenges when it comes to capturing businesses within the industry.

Bargaining Power of Buyers (HIGH)

Listeners have many options when it comes to choosing radio stations. The industry is

fairly concentrated and competitive; giving listeners the power to choose which

operator satisfies their audio needs the best. There is also a high availability of

substitutes, giving the listener even more power to the buyer.

E nvironmental F actors

Technological

This industry is being disrupted by many different shifts in technology. First, the

quality and definition of radio has improved significantly. Low quality, static

transmission is increasingly rare. This is because many stations have transitioned

from AM to FM due to FM’s wider transmission spectrum that enables a clearer and

crisper broadcasting quality. Most radio stations have also adopted “Program

Associated Data” (PAD), which displays channel information, including a specific song

name and artist that is playing, right on in-car-radio displays. Online streaming has

also become extremely popular. Many stations have expanded broadcasting content

onto the Internet, which reaches a wider global audience. Lastly, mobile technology,

such as phones and MP3 players, has made an impact on the industry as well.

Although portable radio devices have existed for long period of time, digital devices

that are able to receive high quality sound have helped increase mobile radio’s

popularity. These mobile devices have radio tuners built in or are able to access online

radio streams using cellular data or WIFI. Mobile radio apps also expand the reach of

the radio broadcaster. 13

Wireless networks and devices are becoming more advanced and sophisticated,

resulting in the rise of Internet-based radio applications. Consumers are finding it

easier and quicker to receive data driving the evolution of wireless data services and

increasing consumer demand for mobile devices and on demand content. This is lead

to the trend of streaming audio programming, which has increased to 82.6% in 2016

in comparison to downloading song and albums, which has dropped to 15-24%. 14

11Radio broadcasters are now forced to create content that is compatible with new and

improved data networks like LTE and 5G technologies. International Data Corporation

stated “ wireless market penetration in Canada is approximately 83% of the population

and is expected to grow at an estimated 0.9% annually over the next four years”.15 In

conjunction with this evolution of wireless data, the CRTC has also limited consumer

wireless term contracts to two years, encouraging consumers to complete and review

contracts quicker than before.

Market Response

1. Bell Canada-28.1% Market Share13

2. Newfoundland Capital Corp. Ltd. -9.8% Market Share13

3. Rogers Communications Inc.- 9.7% Market Share13

4. Corus Entertainment- 9.3% Market Share13

The Radio Broadcasting Industry has suffered a major shift over the last five years.

Alternative media, such as streaming media services, mobile applications and

podcasts, have disrupted the industry by stealing audiences and advertising revenue.

Due to this disturbance, the Radio Broadcasting Industry has struggled to maintain its

relevance to the average consumer. In order to combat this decline in audience, the

big players in the industry have started to participate in merger and acquisition

activity. Traditionally, many independent stations served their own niche, individual

markets; however, because of the change, the industry’s dominating broadcasting

operators have acquired smaller stations, streamlining their programming and

expanding their network. This more effectively captures a greater number of

advertisers.

Furthermore, broadcasters are starting to embrace online media radio channels. A

study done by PWC found that by 2021 US online radio advertising revenue would

account for more than one-tenth of the global online radio advertising revenue.16

Currently, radio advertising accounts for 81% of total radio revenue, however in the US

alone, online radio advertising is anticipated to see a $1.4bn increase in the next year

and a $2.0bn increase by 2021.16

14.Hartung, Adam. “4 Trends That Will Forever Change Media, Advertising And You In 2017 And Beyond.” Forbes,

Forbes Magazine, 6 Jan. 2017

15.“News Releases.” BCE Bell Canada Enterprises: Canada's Top Communication Company, www.bce.ca/news-

and-media/releases/show/BCE-reports-2016-Q4-and-full-year-results-announces-2017-financial-targets-

Common-share-dividend-increased-5-1-to-2-87-per-year-1.

16.PricewaterhouseCoopers. “Radio.” PwC, www.pwc.com/gx/en/industries/entertainment-

media/outlook/segment-insights/radio.html.

12For example, in October 2016, Bell Media introduced the iHeartRadio brand to Canada,

a service that offers consumers online access to Bell Media’s 105 radio stations

across Canada.17 Corus Entertainment has integrated their Radio and News in hopes

to “leverage synergies between the two while creating growth through content sharing,

cross promotion and advertising bundling”.11

“Radio is everywhere. It is accessible. It is local. This is the key to radio’s future.

Whether in your vehicle, streaming from a computer or listening to the Radioplayer

Canada App on your phone or tablet, radio is a part of your everyday life.” –Rob Steele,

President & CEO Newfoundland Capital Corporation Limited 18

*For breakdown of financial performance of all four major players see Appendix F-I.

Radio Broadcasting in Canada & Television Broadcasting in Canada

Jobs in the Industry

Traditional Jobs

Photojournalism, Communications, Sports Journalism, Foreign Correspondent,

Newspaper reporter, Magazine editor, Public relations, Social media, Investigative

journalism, Editor, TV Producer/writer, News Broadcaster, TV/Radio Host.

In March 2016, the CRTC made changes to their regulations, revolutionizing the way

consumer purchase broadcast products. Under these new policies, Media companies

can now sell individual stations to consumers. By unbundling TV packages, audiences

now have choice, empowering the consumer while reducing costs. However, this has

had a major negative effect on the creation of Canadian TV programs and in turn

increased the amount of layoffs within the industry. 19

17.Bradshaw, James. “IHeartRadio Joins Canada's Streaming Market through Partnership with Bell.” The Globe

and Mail, The Globe and Mail, 6 Jan. 2016, www.theglobeandmail.com/report-on-business/iheartradio-joins-

canadas-streaming-market-through-partnership-with-bell/article28028272/.

18.“Annual Reports.” Newcap Radio, www.ncc.ca/annual-reports-information-circulars-annual-information-

forms/.

19.Bradshaw, James. “Canada's New TV Rules Could Erode Jobs, Funding, Report Warns.” The Globe and Mail, The

Globe and Mail, 5 Jan. 2016, www.theglobeandmail.com/report-on-business/canadas-new-tv-rules-could-erode-

jobs-funding-report-warns/article28015965/.

13Bell Media, one of the largest, most successful telecommunications company in

Canada, announced in January of 2017 that they would be reducing positions at more

than 24 locations nationally, including radio and television stations. The restructuring

was deemed the result of increasing competition due to the evaluation of broadcast

technologies and advertising and regulatory pressure. The last major round of layoffs

made by Bell Media was in 2015 when they cut 380 positions across the country. 20

ESPN also announced in April of 2017 the layoff of about 100 employees. This is in

addition to the 300 employees they laid off in 2015. However, ESPN has stated the

layoffs come as Disney speeds up efforts to introduce an ESPN branded subscription-

streaming service. 21

“You have to be willing to either create or experience some distribution as we migrate

from what has been a more traditionally distributed world to a more non-traditional

distribution world,” Robert A. Iger, Disney’s chief executive, told analysts on a

conference call in February. “ 21

Digital Native Publishers

A study done by the Bureau of Labor Statistics’’ Occupational Employment Statistics

(OES) program found that the number of journalists at digital native publishers has

more than tripled over the past 10 years. 22

It is evident that because of its popularity, radio and TV broadcasters are starting to

explore employment opportunities in OTT. Whether that is online creative, news or live

content, broadcasters have started launching their own OTT services or partnering

with existing online platforms. Knowing how to create an IT environment with high

quality content delivered to consumers through new media channels is what gives

broadcasters the edge in such a crowded online space.

A study done “Monster”, an American online publication, using data from U.S. Bureau

of Labor Statistics and PayScale, found that Broadcast and Journalism graduates’ top

10 jobs after graduation are not very traditional. The jobs include: Content Marketer,

Copywriter, Corporate Communications Specialist, Editor, Grant Writer, Public

Relations Specialist, Reporter, Social Media Specialist, Sports Information Director,

and a Technical Writer. 38

20.Jackson, Emily. “Bell Media Cites CRTC Super Bowl Ad Policy as a Factor in Latest Round of Layoffs.” Financial

Post, 31 Jan. 2017, business.financialpost.com/technology/bell-media-cites-crtc-super-bowl-ad-policy-in-

latest-round-of-layoffs.

21.Bonesteel, Matt, and Cindy Boren. “ESPN’s Massive Round of Layoffs Hit Familiar Faces, Including Marc Stein,

Andrew Brandt and Adam Caplan.” The Washington Post, WP Company, 1 May 2017

22.“Employment Picture Darkens for Journalists at Digital Outlets.” Columbia Journalism Review,

www.cjr.org/business_of_news/journalism_jobs_digital_decline.php.

38.“Top Jobs For Journalism Graduates & Degrees.” Monster Career Advice, www.monster.com/career-

advice/article/top-10-jobs-for-journalism-grads.

14How to Stay Relevant

Traditionally, the TV Industry relied on two main sources of revenue: advertising and

subscription. The majority of networks’ revenue streams come from a hybrid of both

models. However, subscription based programming streamed through Internet is

starting to thrive, giving the viewer more control over programming for a cheaper

price. In order to capitalize on this industry trend broadcaster should take the

following into consideration.

1) E mbrace Non- L inear Distribution: New Platforms & Digital Space

The digital online space has shaken the media environment over the last decade,

fundamentally changing the way viewers consume content. In such a cluttered and

fragmented environment consumers are engaging with more content conveniently

over multiple platforms and devices. Rather than seeing this as a threat, broadcasters

should look at this new form of consumption as an opportunity to better interact and

co-create with its viewers. By offering multiplatform OTT distribution, broadcasters

can widen viewership and better engage. Corus Entertainment Inc. has being doing

just that. In fiscal 2016, its social content was viewed over one billion times. Corus

subsidiary Globalnew.ca receives more than 56 million total view monthly. On its

websites alone, Corus reaches 10 million Canadians monthly.11 They are also able to

reach even more Canadians via mobile apps which provides consumers live stream “on

the go” across devices. CBC is following close behind, in 2015/16, about 15 million

Canadian used CBC’s digital sites every month with more than half of these consumers

streaming this content on mobile devices. This number has grown by 3 million in the

past year alone.9

2) E xplore Web Design and Coding

Broadcasters need to learn how to control the space by becoming experts in

streaming and coding. For example, having the knowledge to create apps is a strong

asset for broadcaster. Coding will give broadcasters better control over where and how

to publish content. This will empower the creator to connect with audiences in a more

interactive way. It is about staying relevant, giving the audience what they want and

communicating in the way that individual now prefer to consume news and creative

content.

3) Work With Retail Brands Who Are Now Creating Their Own Content

Channels

Companies like Red Bull and GoPro are creating their own channels in order to help

market their products. Yahoo just recently announced that they have received the

rights to stream NFL games live this year.23 Additionally, Google has already introduced

a TV network called Google Fiber.24 Lastly, Disney just recently announced the 2019

launch of a branded direct-to-consumer streaming service for their content as well as

15a new ESPN video streaming service in early 2018.25 Those who have studied

Broadcasting or Journalism, or have experience in the industry, can now use their skills

in a whole new way by working for big brands producing content that will help market

and attract a new audience.

4) Stay Relevant: TV on the Go

In order to stay relevant, Broadcasters must also react to the variations in their

audience’s viewing habits; they need to fulfill the consumers’ need to experience

interactive, engaging, and convenient broadcasts. “TV on the go” is a model that is

becoming extremely popular within the industry. Streaming broadcast through mobile

devices will help capture a wider audience, while making it seamless to share content

with others through social platforms. Using a second screen device in conjunction with

TV broadcasting allows viewers to not only watch, but discuss content in real time with

their friends and family as well as interact with the broadcast and advertising contact.

TV viewing is becoming a more holistic, high quality and engaging experience for

viewers. Many major networks have moved online in order to better the viewer

experience. 25

5) Stay Relevant: Radio on the Go

Radio broadcasting is developing in a very similar way to TV as they too are seeing the

need to create a more personalized experience for listeners. For example, the popular

music-streaming app Spotify recently added radio, creating stations based on

listeners’ music preferences. It is estimated that it won’t be long until other radio

stations follow suit. BBC’s Radio 1 has relocated online and even has their own

YouTube channel with almost 4 million subscribers and 1.1 billion views. 26

6) Be a Part of the Podcast Generation

One in four Americans listened to at least one podcast in the past month, according to

recent research from Edison Research and Triton Digital. Now totalling 57 million

Americans listening monthly (up 23% year-over-year) this industry is becoming

lucrative for those who enter. For example, the sport-broadcasting network ESPN is

paving the way with the 30 for 30 podcast. This podcast, led by Jody Avirgan, will tell

original sport stories featuring interviews and archival audio. Contrarily, networks are

using podcasts as inspiration for TV content. For example, Fox 21 is planning on

adapting the iconic podcast series “Serial”. ABC is bringing the podcast “Startup” to

life and lastly award winning podcast “Lore” is going to be remade by Amazon. 27

23. Schwab, Frank. “Yahoo Will Broadcast First Free Global Live Stream of NFL Game.” Yahoo! Sports, Yahoo!, 3

June 2015, sports.yahoo.com/blogs/nfl-shutdown-corner/yahoo-will-broadcast-first-live-stream-nfl-game-on-

oct--25-151500015.html.

24.Google Fiber | High Speed Internet Service & TV, Google, fiber.google.com/about/.

39.Castillo, Michelle. “Disney to End Movie Deal with Netflix and Start Its Own Streaming Services.” CNBC, CNBC, 9

Aug. 2017, www.cnbc.com/2017/08/08/disney-will-pull-its-movies-from-netflix-and-start-its-own-streaming-

services.html

167) Showcase your Personal Brand by L everaging Business Knowledge

Showcasing a unique personal brand has never been more important. There are many

opportunities online for broadcasters to create new revenue streams through non-

traditional mediums. Because of the increased popularity of YouTube, Snapchat,

Twitter, Instagram and Facebook Live and podcasts, it is possible for broadcasters to

not only make a living by building their own brand online, but also to become true

entrepreneurs. Having concrete, basic, business skills, as well as a keen understanding

of the corporate world, is now more beneficial than ever before.

Canadian Institutes: Competition for BCIT

Ryerson University

The RTA School of Media has four programs for students including: Media Production,

Sports Media, New Media and Media Production. Although each program is unique,

encompassing different aspect of the Media environment, each program encourages

students to take courses like social media management, media entrepreneurship, and

marketing and even introductory web design. Ryerson’s School of Media is embracing

the current trends and teaching their students tangible skills that will allow them to

thrive in the new and exciting media space. 28

Carleton University

Carleton’s Journalism program is the oldest in the country, however built by a rich

history of experience; the program has continued to grow with the industry and has

produced many successful graduates. By enriching their students with the most

relevant areas of journalism as well as teaching strategic communication, digital

media and media law, students are exposed to multiple aspects of the industry. 29

25.Minas, Chris. “How Mobile Technology Is Changing the Face of Broadcast.” The Guardian, Guardian News and

Media, 31 Jan. 2013, www.theguardian.com/media-network/media-network-blog/2013/jan/31/mobile-changing-

face-broadcast.

26.“Press Office - Broadcast Journalism in the Digital Age: Mark Byford Speech.” BBC, BBC,

www.bbc.co.uk/pressoffice/speeches/stories/byford_leeds.shtml.

27.Research, Edison. “The Infinite Dial 2017.” Edison Research, Edison Research

Http://Www.edisonresearch.com/Wp-Content/Uploads/2014/06/Edison-Logo-300x137.Jpg, 30 Mar. 2017,

www.edisonresearch.com/infinite-dial-2017/.

28.“Journalism.” Ryerson University, www.ryerson.ca/graduate/journalism/.

29.“Admissions.” Undergraduate Admissions Broadcasting Career, admissions.carleton.ca/careers/broadcasting/.

30.“UBC Bachelor of Media Studies.”Bachelor of Media Studies, mediastudies.arts.ubc.ca/.

31.“University of Guelph-Humber.” Media Studies, www.guelphhumber.ca/media.

17UBC Bachelor in Media Studies

This new program to UBC investigates into technological innovations, which enable

new ways for society to communicate. This includes Radio, TV, Film, Blogs, Twitter and

Instagram as all media channels being explored. The UBC Bachelor in Media Studies

combines traditional hands on skills with new technology. Students are required to

take creating writing, journalism, film studies and production, podcasting, social media

management, statistics and even computer science courses. 30

University of Guelph- Humber

The Bachelor of Applied Arts in Media Studies (BAMS) - Diploma in Media

Communications at Guelph aids to students in exploring the new and exciting world of

broadcast and journalism by learning things like producing a newspaper or television

broadcast, promoting and managing a large event, producing a body of photographic

work, or creating of multi-platform communication vehicles through digital

technology. What makes this program unique is its recognition of the importance of

business as an aspect in new media, and its incorporation of business courses. 31

Government Funding

In Canada, broadcasting operators function together with the Canada Media Fund,

while following quotas imposed by the Canadian Radio-television and

Telecommunications Commission (CRTC). They receive some public support from the

Canadian Government. A study done in 2016 by Nordicity, found that Canada exhibits

one of the lowest levels of public funding for public broadcasting among 18 major

Western Countries. The nation, which receives funding annually, was the third lowest

when evaluating the level of per capita public funding, receiving just over $1 billion or

$29 per capita. 32

Broadcasting operators in Canada also make 37% of its total revenue from

commercial sources and 20% share from sale of advertising and sponsorships,

ranking fourth and seventh respectively among 18 major Western Countries. 32

The Canadian Government also provides indirect support to Canada’s broadcasting

operators. This is done through the implementation of section 19.1 of the Income Tax

Act as well as many regulations that prevent international competition; specifically

from US stations for Canadian advertising spend.32

However in March of 2016, it was announced that Canadian Federal government is

committed to helping drive pubic broadcasting’s shift to the digital platforms by

increasing CBC funding. The budget pledges $675 million, which includes a $75 million,

increase for the rest of the year and an additional $150 million annually until 2021. 33

18CRTC will also introduce $90 million in additional supports for local TV in September

2017. Furthermore, the Canadian Periodical Fund currently donates $75-million a year

to magazine publishers.36

These types of organizations are not stopping there, in June 2017, News Media

Canada, a group that supports and advocates for print and digital media in Canada,

requested that the federal government set up a $350 million fund to support

journalism in Canada. 37

Canada Media Fund

Canada Media Fund is a non-profit corporation supported by the Canadian

government. It receives financial contributions from the government as well as

Canada’s cable, satellite and IPTV distributors. The corporation’s main goal is to

support, through financial aid, Canadian television and digital media industries. The

Canada Media Fund allocated a total of $349.7 million dollars for 2017-18. 34

Canada Council for Arts

The Canada Council for Arts is a federal crown corporation that provides financial aid

to Canadian artists, groups and organizations that use film, video, new media and

audio as a form of expression enhancing the viewing and listening experience of the

Canadian audience. They provided $144.8 million dollars to 2,055 artists in 2015-16. 35

Scholarships for Broadcasting 36

CTV Broadcasting Scholarship

Available to a full-time Cambrian College student enrolled in the Journalism or Public

Relations program. Value $1000 dollars and to be awarded to one student annually.

Astral Media Scholarship

Provided by the Canadian Association of Broadcasters for all Universities. Value $5000

for full time students. Eligible Provinces: Alberta, British Columbia, Manitoba, New

Brunswick, Newfoundland, Nova Scotia, Ontario, Prince Edward Island, Quebec,

Saskatchewan.

Bayshore Broadcasting Media Scholarship

Provided by Bayshore Broadcasting Media, Community Foundation Grey Bruce for all

Universities in the following provinces: Alberta, British Columbia, Manitoba, New

Brunswick, Newfoundland, Nova Scotia, Ontario, Prince Edward Island, Quebec,

Saskatchewan.

19Global Television Network Broadcasters of the Future Awards-

Internship Award for a Canadian with a Physical Disability - Canadian

Scholarships

Provided by Global Television Network for student at BCIT. Value $15,000 for one

student.

Global Television Network Scholarship Award for a Canadian Visibility

Minority Student

Provided by Global Television Network for all Universities in the following provinces:

Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland, Nova Scotia,

Ontario, Prince Edward Island, Quebec, Saskatchewan. Value $4500 for one student.

Ruth Hancock Scholarship

Provided by the Broadcast Executive Society, this scholarship is specifically for

broadcasting students at Canadian Colleges and universities. Value $1500 dollars

annually.

32.“Public Broadcaster Comparison 2016.” Analysis of Government Support for Public Broadcasting, CBC/Radio

Canada, 11 Apr. 2016, www.cbc.radio-canada.ca/_files/cbcrc/documents/latest-studies/nordicity-public-

broadcaster-comparison-2016.pdf.

33.Bradshaw, James. “Federal Budget Pledges $675-Million in CBC Funding.” The Globe and Mail, The Globe and

Mail, 23 Mar. 2016, www.theglobeandmail.com/report-on-business/liberals-pledge-675-million-in-cbc-

funding/article29354285/.

34.“Interested in CMF Funding? Here’s Everything You’Ll Need to Know.” Canada Media Fund, www.cmf-

fmc.ca/programs-deadlines.

35.“Funding.” Canada Council for the Arts, canadacouncil.ca/funding.

36.Media Studies Scholarships in British Columbia, www.canadian-universities.net/Scholarships/British-

Columbia/Media-Studies.html.

36.Kuitenbrouwer, Peter. “Newspaper Publishers Ask Ottawa for $350 Million a Year to Save Print

Journalism.” Financial Post, 16 June 2017, business.financialpost.com/news/newspaper-publishers-ask-ottawa-

for-350-million-a-year-to-save-print-journalism.

37.Press, The Canadian. “Media Group Asks Ottawa for $350-Million Canadian Journalism Fund.” Macleans.ca, 17

June 2017, www.macleans.ca/news/canada/media-group-asks-ottawa-for-350-million-canadian-journalism-

fund/

20Appendices

Annual Change Broadcasting in Canada Industry

Appendix A

Financial Performance of Market Leaders- Television Broadcasting in Canada

Appendix B

21Appendix C

Appendix D

Appendix E

22Financial Performance of Market Leaders- Radio Broadcasting in Canada

Appendix F

Appendix G

Appendix H

23Appendix I

24You can also read