CFA Institute Research Challenge - CFA Society Italy Right Tails

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CFA Institute Research Challenge

Hosted by

CFA Society Italy

Right Tails

CFA Institute Research Challenge

Initial Coverage | 16th February 2018

Italy | Luxury | Fashion, Apparel

Moncler SpA

Investment summary

HOLD

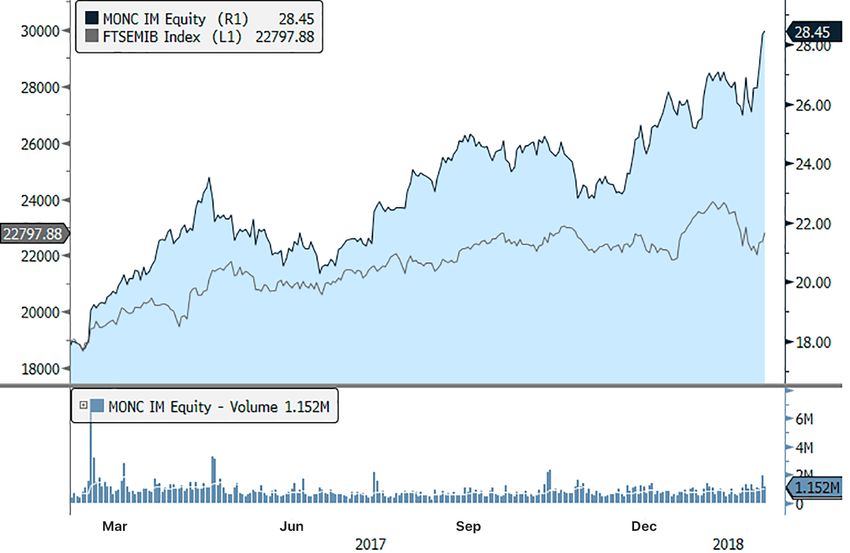

Moncler: the French down jacket is now global Price: €28.45

We initiate our coverage on Moncler SpA (MONC) with a HOLD recommendation, reflecting

a €25.85 target price by the end of 2018. This would represent a potential downside of 9.1%,

Target Price: €25.85

dividends excluded (considering 16th February closing price). We believe the current market Downside: -9.12%

price is over-appreciating the terrific growth of sales and EBIT reported in recent years

(both around 21% CAGR 2013-16) driven by opening of new Directly Operated Stores (DOS), Listed on: Italian Stock Exchange

increased from 107 in 2013 to 190 in 2016 (195 at 3rd quarter 2017) and a solid relationship Ticker symbol: MONC:IM (BB), MONC.MI(TR)

with the wholesale mono-brand network.

Heritage, Uniqueness, Quality, Consistency: the road to success Market Data

MONC’s success comes from a painstaking attention to details, portrayed both in the product-

Main Shareholders

making and in the management of the company, especially regarding financial aspects. The

Ruffini Partecipazioni S.r.l. 26.3%

Ruffini administration turned Moncler into a company with best-in-class results: ROS of

ECIP M S.A. (Eurazeo) 5.3%

28.61% (avg sector Returns on Sales is 15.54%), ROE of 27.90% (avg 12.94%). Moncler has

Treasury Shares 0.8%

a cash-positive financing position: this is the result of the ability to generate abundant cash

Norges Bank I.M. 2.66%

flows, grown by +120% in 2013-2016.

Free Float 67.6%

Market Cap (€ bn)

Asia and Americas: key drivers for organic growth

Shares Outstanding (mln) 253.1

Revenue’s growth has been driven by Asian and Americas’ markets, we believe that this trend

will continue in the years to come, albeit slowing down to a high single digit CAGR 2016-2022.

Asia and Rest of the World (ROW) will account for 46.2% of sales in 2022 (from 40% in 2016,

Stock Data

it was 34% in 2010), while a significant boost could come from Latin America, where MONC

has only one DOS. EMEA and Italy should reduce their weight on sales, with respectively 5% 52-week range €17.48 – 28.75

and 3% CAGR 2016-2022. Average daily volume 0.9m

The Genius project has just started: it will see 8 designers working each one on a specific

line of the brand, with new collections presented every month. Genius represents the vision

of the future for Moncler, the consumers’ approval will mean a lot to results in the next years. Key Financials

Millennial customers, online sales and tourist spend will be other key drivers for growth (see

Driver for Growth), given the difficulty in carrying out acquisitions that could significantly 17E 18E 19E

impact earnings in the short term. EPS 0.99 1.03 1.15

DPS 0.34 0.37 0.47

Div. Yield 1.26% 1.45% 1.83%

1Y Daily Price Performance

ROE 27.89% 23.76% 22.13%

ROCE 45.42% 33.84% 35.89%

MONC price €26.78 €25.85 €25.85

Source: Bloomberg

CFA Institute Research Challenge · 16th February 2018 1

Financial highlights

Sales 2012-2016

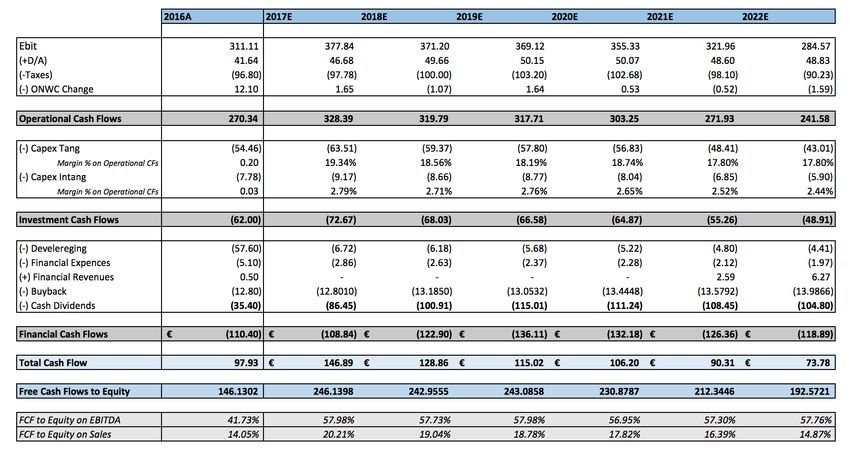

Our estimates on Moncler showed an increase of revenues and profitability, basing on the

1100

assumptions of the Average scenario (see Annexes). Inter alia, sales are expected to grow

7.8% CAGR 2016-2022 to over €1600 mln, while EBIT should reach €443 mln with a 6.1% 900

CAGR 2016-2022. EPS in our assessment could grow to €1.15 from €0.78 in 2016 and FCF to

700

Equity are supposed to nearly double to €292 mln in 2022.

500

Valuation

The issued TP is based on the assumption of a robust expansion of revenue and the capacity 300

of generating plentiful cashflows, mostly thanks to the persistent growth of the Asian & ROW

100

and Americas’ markets. Our estimates were built through stochastic evolutions regarding

2012A 2013A 2014A 2015A 2016A

revenue and every key financial variable, all included in a three-stage DCF model with three

Italia EMEA Asia & ROW Americas

possible scenarios, supported by different macroeconomic views. We also performed a

multiples analysis in order to evaluate Moncler with a market based approach on comparables Source: Team Estimates

Sales 2017-2022

firms through P/E and EV/Ebitda: for each peer, historical series were collected spanning from

1800

2013 to 2017. An average of the historical averages was used in order to find a fair value for

1600

the multiples of the entire sector.

1400

A weighted average (80% DCF, 20% multiples) of these valuations brought us to a final target

1200

price of €25.85.

1000

800

600

400

200

0

2017E 2018E 2019E 2020E 2021E 2022E

Italia EMEA Asia & ROW Americas

Geographical Sales Breakdown Source: Company Data, Team Estimates

2012A 2016A 2022E

10% 17% 14% 18% 11%

26% Italia

25% EMEA

32%

29%

Asia & ROW

40%

32% 46% Americas

Source: Company Data, Team Estimates

Italia EMEA Asia & ROW Americas Italia EMEA Asia & ROW Americas Italia EMEA Asia & ROW Americas

CFA Institute Research Challenge · 16th February 2018 2

Business Description

Company presentation

Collections Founded in 1952 in Monastier-de-Clermont, near Grenoble (France), Moncler (MONC) created the first nylon

jacket in 1954 and quickly expanded, being selected as official supplier at the 1968 Winter Olympic games.

Main Warm, lightweight and declined many shades, Moncler’s down jackets made the history of winter fashion in

the 80s. Near bankruptcy, pinched between the viral expansion of luxury brands like Prada and Gucci and

mega sportswear companies like the North Face, in 2003 the company was bought by Italian entrepreneur

Remo Ruffini: thanks to his innovative contribution and to the know-how of several private equity operators,

Moncler’s revenues surpassed €1bn in 2016. Headquartered in Milan, in 2013 the firm has been listed on the

Milan Stock Exchange and from March 2014 it is part of FTSE MIB index.

Nowadays Moncler is a luxury fashion company with directly operated stores (DOS) worldwide and a relevant

presence in the European and in the Asian market. Its main product is the goose down jacket, for which it

is famous all over the world. The company is trying to convey its uniqueness and heritage also through its

accessories, to feed the disruptive growth of recent years (+20.8% sales CAGR 2012-16).

Business model

Moncler believes that its main asset is its own heritage, which permeates its entire strategy, in addition to

Grenoble

its products and communication policy. MONC adopts an integrated and flexible business model, where the

objective is the direct control of the most delicate production phases; instead it outsources other activities

such as cutting and packaging to subcontractors, which requires high quality standards. The style department

is supported by the merchandising team and product development that support the construction of the

collection and develop creative ideas. The production cycle follows these five phases: collection development,

purchase of raw materials, production, quality control and shipping. The selling side of the business is based

on two different channels: wholesale stores and proprietary retail. The first, even if with limited margins, is a key

competitive tool, since a wholesale store is actually a physical arena where the consumer has the possibility

to choose to buy one brand or another one: Moncler is so able to assess its competitive position thanks to the

selling statistics collected by the wholesale seller about all the brands sold. The retail channel has obviously

higher selling margins but it required a more dynamic attitude to the creation of new products, as the time to

market for this channel is following a decreasing trend in these years: fashion trends are very fast and volatile,

so a flexible attitude in the development, production and selling processes is needed.

Accessories Business segments

MONC’s business is segmented by geographic areas and products. Revenues are divided as follows:

• Asia & ROW: €418.5 mln, 40% of revenues, +28.2% CAGR 2012-16, from 31 to 93 DOS in 4 yrs

• EMEA (ex-Italy): €303.3 mln, 29% of revenues, +17.8% CAGR 2012-16, from 31 to 55 DOS in 4 yrs

• Americas: €175.3 mln, 17% of revenues, +28.2% CAGR 2012-16, from 6 to 8 DOS in 4 yrs

• Italy: €143.2 mln, 14% of revenues, 4.3% CAGR 2012-2016, from 15 to 19 DOS in yrs

Its product portfolio is divided in:

• Main, including “iconic product” as the down jacket, which represents 80% of sales

• Grenoble, the sport and technical collection

• Enfant, products for children

• Special Project, collaborations with new designers

• Further collections, among which the accessories

Italia 14%

EMEA 29%

Asia & ROW 40%

Americas 17%

Source: Company Data

CFA Institute Research Challenge · 16th February 2018 3

Industry Overview & Competitive Positioning

The fashion luxury market

In recent years, a profound change occurred in the geographic localization of fashion luxury customers, with a progressive shift from Western

to Asian markets, such as China, Japan and South Korea, and also a boost from the South American market which is constantly growing. These

aspects, together with the growth of online sales and an increasing attention to ESG and CSR criteria alongside quality and price, changed the

fashion industry. Market players are progressively creating more competitive business models by implementing their production processes in

order to shorten the time-to market, with the aim of promptly meeting the customers’ needs, trying to anticipate their competitors. Considering

all segments, the luxury market grew by 5% to an estimated €1.2 trillion globally in 2017. China was a clear top performer: Chinese consumption

bounced back in 2017, fueled by renewed consumer confidence and the rapid emergence of a new – and increasingly fashion-savvy – middle

class. Local buying by Chinese customers boosted sales in mainland China by a remarkable 15% at current exchange rates, to a total market size

of €20 billion; buying abroad increased, too. Globally, the share of personal luxury goods purchased by Chinese nationals reached 32% in 2017.

Growth will continue at a 4%–5% compound annual rate over the next three years (at constant exchange rates), with the market for personal

luxury goods reaching €295–€305 billion by 2020. The relentless march toward e-commerce continued, with online sales jumping by 24% in

2017, reaching an overall market share of 9%. (Bain & Company, 2017)

Two key trend will characterise the luxury goods markets (Deloitte, 2017):

• From physical products to digital experiential: consumers are asking for more shopping channel and home delivery, the essence of

luxury is changing from an emphasis on the physical to a deeper connection focused on experiences and the feelings that luxury products

can evoke in their purchasers. However, premium quality remains a ‘must have’ and consumers retain a keen eye for craftsmanship and

hand-made products.

• From standardisation to personalization: expansion through globalisation necessitated a one-size-fits-all approach. Changing luxury

shopper behaviour demands a different, more personalised response. Moreover, consumers are also asking a reward for their loyalty.

Digital channels are creating a need for large-scale high-quality personalised content: some luxury goods companies have started to open

up a dialogue with consumers and involve them in the marketing process, a highly- demanding challenge.

Driver for growth

The main driver for growth in fashion market are sales in emerging markets, especially in Asia. In these areas of the world, in addition to

registering significant GDP growth rates, a new middle class is emerging, which represents the target customer for luxury companies. We

estimate that in the next 5 years MONC’s growth will settle over 10% CAGR, bringing revenues of Asia & ROW to €750 mln. A further boost could

derive from openings in Latin America, where there is currently only one store in Brazil: we expect an overall growth of the Americas in the 40%

in 5 years, with a turnover that should reach €300 mln. The EMEA market is expected to continue its expansion around 5%, taking advantage

of openings in tourist cities and in Eastern European countries, with Italy gradually reducing its weight on overall sales, growing in the order of

3-4 % in the next years. Tourist spend will provide a key extra boost in every region.

• The focus concerning new products is on Moncler Genius, the new project that will see 8 designers working each one on a specific line of the

brand and collections will be presented every month. Each fashion brand has striven and still strives to figure out the preferences and needs

of final consumers within the market with the right timing. Time-to-market, i.e. the time between the ideation of the product and its effective

marketing, is a notable aspect on which Moncler is working hard: like any revolution, we have to wait to see if consumers will appreciate it.

Another relevant matter is to reduce warehouse capacities, with a consequent decrease in logistics costs, minimizing the risk of having

excessive inventories. This is compliant with the logic of the luxury market, where the scarcity factor is a way to increase the intrinsic value

of the product perceived by consumers.

• Speaking of consumers, Millennials, which have grown up in a time of rapid change, giving them a set of priorities and expectations sharply

different from previous generations. They are the first digital natives, always connected to social media, they have less money to spend

than previous and at the same time they focus on products’ quality. Their affinity for technology is reshaping the retail space: by 2020,

Millennials will account for one in three adults and they are more than 2x influenced by advertising than older generations. With product

information, reviews and price comparisons at their fingertips, Millennials are turning to brands that can offer maximum convenience at the

lowest cost: a strong brand probably will not be enough to lock in a sale in the future.

• Regarding online sales, an historical US-centric market, Asia and Europe will be the main growth engines, with 2013-2017 24% CAGR for

luxury market (Bain & Company, 2017). Currently online sales account for only 7% of Moncler’s revenue, but apparel sector is expected to

60.00%

50.00%

40.00% Asia-Apac

30.00% Europe

20.00% America

10.00%

Row

0.00%

‘

Source: Companies Data

CFA Institute Research Challenge · 16th February 2018 4

provide good performance, also thanks to wholesale online. Moreover, brands will capitalize proactively on the channel potential through

their own websites, ensuring greater margins. Accessory, on which MONC is focusing with the “monclerization”, will be the top category,

with shoes consistently outperforming.

• Tourism: tourist spending will provide a key extra boost in every region, growing faster than the local one: Moncler takes advantage of this

growth trend by renting DOS in areas with a high tourist flow, most buyers are generally Chinese and Japanese tourists. Consumers who

are travelling, either in a foreign market (31%) or while at the airport (16%) make almost half of luxury purchases. This percentage rises

to 60% among consumers from emerging markets, who typically do not have access to the same range of products and brands that can

be found in more mature markets (Deloitte, 2017). It should be noted that a backdrop of uncertainty – the new US government, Brexit and

terrorist attacks in several European cities – has deterred many potential Chinese buyers from travelling to key shopping destinations in

the US and Europe.

MONC’s competitive advantages

Moncler, determined with the concept of continuous innovation, is trying to differentiate product range from outerwear (currently 80% of sales)

to other categories, like soft accessories and shoes, which are growing two times faster than the main collection, within flagship stores with

an average floor area which is going from 120m2 to 200m2. We estimate an ideal weight of 65%/70% in 4/5 years. This widening of the product

range will exploit the powerfull brand awareness and the stickiness to the brand that Moncler has built over the years around its down jacket:

the ‘monclerization’ process will extend this powerfull attachment to the brand to a diversified portfolio of new products.The brand value can

be maintained and strengthened over time also thanks to strategic locations of Moncler stores in the most important fashion sites around the

world, like Via Montenapoleone in Milan. In addition to the opening of new DOS, especially in Asia and Americas, the company is supporting

revenues’ increase paying particular attention to the development of the website and following the global growth trend of HNWI. Moreover, the

company is considering to participate as a supplier to the 2022 Winter Olympic games in China, where the government aims to have 50 million

skiers in a few years. Finally, we should consider the tourists’ flow: in 2016, 284 mln people travelled to Asia and the Pacific area, 155 mln to

Norh America and 482 mln visited Europe.A maniacal attention to financial data (e.g. 1yr payback period for new DOS) and no acquisition in the

short term, assisted by a decreasing tax rate (thanks to a patent box), will probably increase the pay-out ratio. An important backing for growth

will come from the optimization of logistics: for this purpose a new manager has been hired.

Financial Analysis

Moncler has experienced a phenomenal improvement in its financial status since 2013,

ONWC on Sales

in particular thanks to the inception of Ruffini administration, that succeeded in joint

0,45

in a perfect equilibrium a turnaround of the fashion brand and an efficient financial

0,40

0,35

management. The analysts have noticed a significant improvement in many strategic

0,30 financial ratios from 2013 onward and these could be a leverage tool for future

0,25

expansion. From a liquidity point of view, the quick ratio followed an improvement path:

0,20

from a not aligned with the average of the industry level of 0.90 in 2013 to a strong level

0,15

0,10

of 1.36, with an increment of about +50%, mainly due to an effective improvement in the

0,05 management of the inventory: today the Moncler policy expects to contain inventory

- under a decreasing level, trying to produce all the products that the market will absorb,

2013 2014 2015 2016

Moncler Kering Cucinelli LVMH Prada Burberry Tod's without allocate wealth in assets that will be unsold.

Moreover, the management succeeded decreasing the weight of ONWC on sales, a

measure of efficiency in the management of operational liquidity of the society: from a

ROI yet positive level of 0.11 to 0.05, with a decreasing of about -50% in 4 years.

0,70

The improvement in the operational liquidity can also be assessed through the historical

0,60

analysis of the cash conversion cycle: Moncler shows a very low level of 47 days, ranking

0,50

absolute first among competitors, which present an average level of 90.

0,40

0,30

Furthermore, the operational cash flows on sales is an impressing indicator for Moncler:

0,20 28.17% in 2016, while the competitors showed a lower average level of 13.52%.

0,10

- The liquidity standing is high, it could be a key competitive driver in the future, in

2013 2014 2015 2016

Moncler Burberry LVMH Cucinelli Prada Tod's Kering

particular in the shortening of the time to market, to boost efficiency.

Moreover, the good liquidity standing is a key driver for the operational productivity:

in fact, the rotation of the invested capital is quite high and above the average of the

sector, with a level of 1.73 in 2016.

CFA Institute Research Challenge · 16th February 2018 5

ROE

Given the high level in the rotation and a phenomenal Return on Sales of 28.71% (average

0,35

ROS for the sector is 15.54%), the company is able to show a first at all level of ROI at 49.55%.

The ROI was improved in the recent years in particular thanks to the increase in the invested

0,30

capital rotation, given an historical stable level of ROS.

0,25

The Return of Equity is above all the comparables: Moncler shows a level of 27.90% with an

0,20

average of 12.94%.

0,15

0,10

The financial position is very strong and on line with the competitors on the industry: the

net financial position is positive (cash positive), with an amount of cash of 243 million and a

0,05

financial debt of 140 million at the end of 2016.

- Given the huge amount of operational cash that MONC is able to produce and considering

2013 2014 2015 2016

Moncler Burberry Cucinelli LVMH Prada Tod's Kering increasing probability of a monetary tightening in Eurozone, given also the recent steeping in

the yield curve, the analysts think that the management will absorb cash in order to partially

Source: Companies Data deleveraging the financial debt toward a physiological level of 50 million in 2022.

The financial situation shows a robust structure under every point of view and this certainty

allow Moncler to stay competitive in the industry and to be able to expand its market shares

around the world.

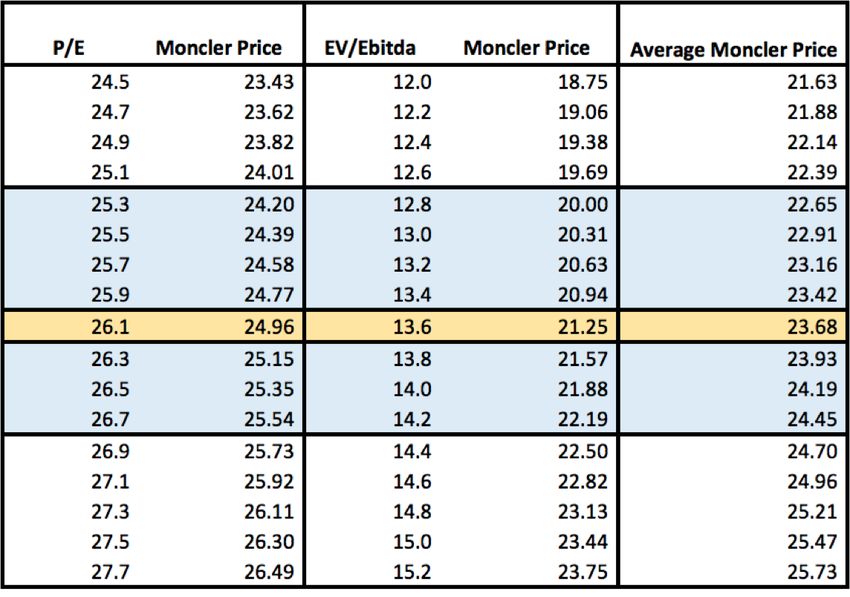

Valuation

We foresee a target price (TP) of €25.85, reflecting a 9.1% potential downside on 16th February 2018 closing price. In order to estimate a fair

value, we centred our valuation on a three-stage DCF model with three possible scenarios, which suggested a TP of €26.56 (weight on final

TP: 80%). A relative analysis, based on competitors’ historical P/E and EV/EBITDA averages, was performed in order to support the DCF result:

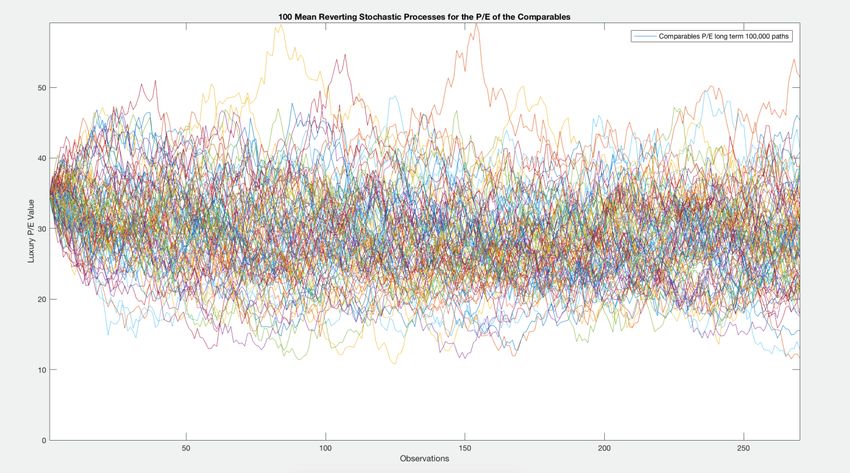

it confirmed the market’s overvaluation for MONC, showing a fair value of €23.03 (weight on final TP: 20%). To further corroborate our view, we

carried out a mean – reverting stochastic process applied to the P/E of the luxury sector (see Annexes).

DCF Model

The analysts have performed the valuation through a DCF model applied to the Free Cash Flow to Equity that will be generated by Moncler in the

three different scenarios of the world defined above both as Average, Best and Worst case scenarios, each of them featured by macroeconomic

and microeconomic trends that will affect the performance of Moncler in the future. The analysts have adopted a three-stage model: the

data referred to the next five years have been estimated punctually according to the assumptions made by the analysts on the different items

of the IS and CF statement, while from 2023 onwards a decreasing growth rate in revenues converging toward the long-term inflation rates

for the stand-alone economies in 2029, from which year the inflation rates are supposed to drive the growth on revenues toward perpetuity

(Damodaran). The long-term inflation rates for the macro regions come from the forecast of the International monetary fund and are exploded

below.

The cost of equity with which discount the Free Cash Flow to Equity is ke equal to 9.53%, according

to the cost of equity estimation. The analysts have performed the DCF model on the three following

scenarios, simulating through Matlab 10.000 target prices for each scenario defined, obtaining three

different average target prices. (see Annexes)

Average Case Scenario

Revenues Evolution

CFA Institute Research Challenge · 16th February 2018 6

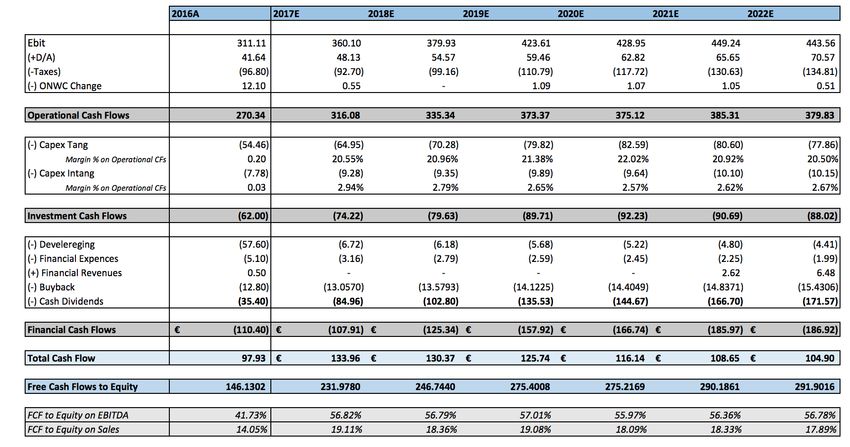

5Y Income Statement (First Stage) 5Y Cash Flow Statement – Free Cash Flow to Equity (First Stage) CFA Institute Research Challenge · 16th February 2018 7

FCF to Equity (First and Second Stage)

Terminal Value (Third Stage – Growth Long Term Inflation Rate)

Multiples Valuation Method

The market multiples designated by the analysts in order to evaluate Moncler through a market based approach on comparables firms are P/E

and EV/Ebitda. For each peer, historical series for P/E and EV/Ebitda were collected spanning from 2013 to 2017 and an average was computed

on them for each stand-alone firm: in our opinion the price incorporates the expectation of repetition in the future years of the recent extremely

positive trend for this sector, furthermore there is no sense at all in evaluate Moncler with the actual level of market multiples, since all the

financial securities have been clearly driven up by the huge amount of liquidity injected in the financial systems. Therefore, in order to price

MONC, the analysts have performed an historical average of the multiple for each peer, that has been considered as the fair multiple for that

particular stock. Moreover, the analysts compute an average of the historical averages in order to find the fair value for the multiple for the

entire sector.

Price Earning

Enterprise Value on Ebitda

Source: Team estimates

Sensitivity Analysis

The analysts have performed a sensitivity analysis on the multiple, that brings an

average target price of 23.68, suggesting a Sell recommendation.

The relative valuation has been supported by a mean – reverting stochastic process

applied to the P/E of the luxury sector: according to our view the actual P/E for

Moncler and its peers is historically too high and it will in the future converge

toward its long term fair value, following the same stochastic path that is usually

tracked by the interest rates in the long run. See Annexes for further details.

CFA Institute Research Challenge · 16th February 2018 8

Investment Risks

Financial

MONC does not suffer of typical financial risks, as many of its competitors. The company has a positive Net Financial Position (NFP),

having a sum of cash and cash equivalent higher than the sum of short-term and long-term financial debt. A rate hike or credit crunch

would hardly affect Moncler’s results, minimizing the interest rate risk. The same reasoning applies about liquidity risk: more than €100mln

in cash and generous cash flows are an assurance against every worst scenario. Since 2014 MONC initiated a strategy to hedge the

risks associated with exchange rates fluctuations, covering almost the entire currency risk. Moncler brand products are distributed even

through 42 wholesale mono-brand shop-in-shops, which accounts for 26.5% of revenues. The firm operates in accordance with a credit

control policy aimed at reducing risks resulting from insolvency of its wholesale clients.

Legal

Regulatory risk

Moncler operates in a complex international environment: the company is subject, in the various jurisdictions in which it operates, to a lot

of different rules and regulations. This could pose a threat, especially for all matters relating to health and safety of workers, environmental

protection, rules around manufacturing of products and their composition, protection of intellectual and industrial property rights and

fiscal rules.

Strategic

A single man in charge

The brand awareness was achieved thanks to the creative director, Remo Ruffini, who revived the brand giving it a new identity, tied to

the past and ready to face the future. Mr. Ruffini re-launched the brand internationally and, through a continuous pursuit of excellence,

created one of the most important group in the luxury fashion field, in less than ten years. If he leaves the company, nobody knows what

the repercussions could be.

Concentration risk

Moncler’s collections focus on Autumn/Winter: 80% of revenues accounts on outerwear, the lack of diversification represents a serious

risk for the future growth of the brand, although management has undertaken a path aimed at the insertion of different products.

Production concentrated

Production concentrated in a single factory in Romania is a major threat: the possibility of an accident, the demand for higher wages or

geopolitical tensions involving nationalistic changes could represent a serious hazard. Furthermore, the risk of insufficient production

capacity should not be overlooked, with the possibility that having a single plant represents a bottleneck difficult to overcome in the short

term.

Sustainable growth and future profitability

The considerable estimated increase in revenues constitute a threat to the defense of high returns on sales (ROS), and everything to do

with brand perception and heritage to be preserved also in consideration of the creation of new products, historically not belonging to the

DNA of Moncler. Sustainability of growth will be a serious challenge for the management: it will have to differentiate the range of products

sold, in order to partially decorrelate its total revenues from the down jacket and keep the future sales amount in a more stable path of

growth. Different products will yield different margins so the real challenge will be to maintain the productivity at a stable level and not to

dilute the brand perception.

Counterfeiting risk

For every fashion brand, the counterfeiting of garments is a risk to be constantly monitored. It represents a doubly negative aspect for the

company, causing a loss of turnover and image. (see SWOT analysis)

Reputational risk

A relevant aspect for a brand that bases its strength on the public image is the reputational damage that could derive from scandals

involving the company’s value chain. In 2014 Moncler suffered a huge reputational damage following the journalistic investigation of the TV

broadcast Report, in which were shown ill-treatments to the geese from which the feathers destined to Moncler down jackets came from.

Macro

Customs duties rising

An increase in customs duties is anything but remote, considering the recent tensions between the US and China. This could lead to

significant price increases for Moncler’s products, with a consequent risk of dropping sales.

Stagnation risk

A stagnation risk for EMEA market and reduction in growth of Americas and Asia in a worst-case scenario would affect significantly MONC,

which today expects an extraordinary increase in sales in the years to come. (see Valuation in worst-case scenario)

CFA Institute Research Challenge · 16th February 2018 9ESG – Environmental, social and governance

Since 2016, Moncler publishes the “Sustainability Report”, in order to show its tangible actions and improvements in this field. In 2017 Standard

Ethics upgraded the company’s rating to E+, on a scale of 9 levels (EEE; EEE-; EE+ ; EE; EE-; E+; E; E-; F), thanks to enhancements of its

sustainability strategy in a long term view.

Environmental

Following the “Report” case, MONC concentrated its efforts on monitoring and assessing environmental impacts, in order to achieve ISO 14001

certification. With the aim to reduce its impact on the environment, the company signed a supply contract for the purchase of renewable energy

in Italy and adopted efficient technologies: green ICT solutions and a sustainable logistics system. Regarding the supply chain, it has launched

the DIST (Down Integrity System and Traceability) Protocol for down traceability and, farming standards and animal welfare. Moncler verifies

that all its suppliers respect DIST. (see ESG in Annexes)

Social

Investments in training activities, both for office employees and for sales personnel, grow year by year. The “Control, Risk and Sustainability

Committee” has been established as a committee of the Board of Directors, to face sustainability issues. A “Supplier Code of Conduct” has

been approved by the BoD, based on the declarations of the International Labor Organization (ILO) about fundamental principles and rights at

work. With regard to community, in 2016 Moncler provided support to social projects, regarding the cancer prevention and the fight against

AIDS, through institutions such as Umberto Veronesi Foundation and amfAR (American Foundation for AIDS Research).

Governance

Moncler implements a traditional administration and control system, compliant with Italian corporate governance best practices (“Codice di

Autodisciplina”), even if it should be emphasised that Mr. Remo Ruffini is both chairman and CEO. Eleven directors that sit in the board, six of

these are independent directors and three of them are executive directors. Two committees have been established to support the corporate

governance: the “Nomination and Remuneration Committee” and the “Strategic Committee”. Moreover, the company has adopted an integrated

Enterprise Risk Management (ERM) system based on international best practices. With respect to remuneration policy, Moncler adopts two

compensation practices: a fixed remuneration for independent and non-executive directors and a remuneration consisted of a fixed component

and a variable component, connected to MBO, for executive directors and CEO. In addition, the company established various stock-option plans

and one performance share plan.

Source: Company Data

CFA Institute Research Challenge · 16th February 2018 10Annexes 1. Industry Overview and Competitive Positioning Porter’s Five Forces Analysis SWOT Analysis 2. Valuation DCF Model Assumptions Cost of equity P/E Mean Reverting Stochastic Process - Matlab Income Inequality Model Environmental, Social and Governance 3. Environmental, Social and Governance ESG Analysis Board of Directors CFA Institute Research Challenge · 16th February 2018 11

Industry Overview and Competitive Positioning

Porter’s Five Forces Analysis

Potential of new entrants into the industry 2

Power of customers 2

Threat of substitute products 2

Power of suppliers 3

Competition in the industry 4

Competition in the industry: High. Competitiveness in the sector is high, and represents one of the main core

of the fashion luxury market. Companies seek to establish themselves through multiple channels, such as

consolidation of the brand, innovation, marketing and product quality. To be stressed some main trends: a

growing exposure to APAC, online sales and ESG policies: topics to which consumers are increasingly careful.

Potential of new entrants into the industry: Low. The fashion luxury market, to which Moncler belongs, relates to

a few large companies with a strong brand identity and already established production facilities which allow

to achieve economies of scale and scope. The brands are already well established globally, the know-how

held by these companies is a key element to build a high-end product: it comes from experience gained

over the years, hardly imitable by new players. The market has oligopolistic characteristics: there are few

companies with high barriers to entry, natural barriers, economies of scale and high developed marketing and

R&D functions. Establishing a new brand to overcome the yet established others is hard!

Threat of substitute products: Low. It can be said that there are practically no substitutes for luxury goods

because each brand holds its own uniqueness. Despite that, a possible issue for Moncler could be the increase

in worldwide shipping of counterfeit products, especially from China. New systems of protection of image

rights through apps and identification codes allows the client to be protected from this risk, along with legal

actions against sellers of counterfeit products.

Power of customers: Low. Luxury goods tend to have a rather inelastic demand: prices of luxury goods tend to

be high even during an economic downturn. Despite having a European backdrop of the past few years, the

luxury goods industry has continued to thrive. As a matter of fact, in the luxury goods industry a decrease in

price may be perceived as a decrease in quality of the product and this may lead to a decrease in demand.

Rather, an increase in the price of the luxury goods may also attract more customers, because they can

equalize an increase in price with an increase in quality. Moncler banned any kind of seasonal sales, to ensure

a constant demand for its top-quality products and the capacity to obtain huge returns on sales.

Power of suppliers: Moderate. As far as it concerns the weight of the suppliers on the total supply, an important

figure is that fifty suppliers provide 72% of total supply for Moncler. Thus, the granularity of the suppliers leads

to the reduction of the weight of each individual supplier, which however represents an important driver as it

already possesses the know-how necessary for the production of the goods, according to the customized and

high quality characteristics required. Therefore, the relationship with the suppliers is very important. However,

given that Moncler is a relevant client, it continues to hold a significant bargaining power over their suppliers.

Source: Team analysis

CFA Institute Research Challenge · 16th February 2018 12SWOT Analysis

STRENGTHS

• An increasingly established brand: the brand is known for the creation of the down jacket and Remo Ruffini has managed to create a

strong and constantly evolving association between the concept of this item of clothing and the Moncler brand. The genetic DNA of the

down jacket gives life to the whole range of products, which have a peculiar style and heritage: this creative concept has been named

"monclerization" by management and should guarantee strong resistance to the brand over time and space.

• Global presence: the company has 195 directly operated stores (DOS) in 26 countries and 48 wholesale points all over the world. 73.5% of

total revenues worldwide come from the DOS network and the remaining 26.5% from wholesale channel. Given its global presence, Moncler

has a significant residual margin to grow in subsequent years.

• High operating margins and strong balance sheet: huge margins on sales and the negative net financial position makes Moncler a

company with low financial risks. It also allows the firm to exploit all kinds of opportunities for both internal and external growth and a major

capacity to distribute dividends.

• Increasing the demand of premium products: there is a strong growth in the demand for high quality products, the luxury market is

experiencing a period of strong expansion in recent years.

• A resilient business: MONC operates in a typically defensive sector, less exposed to the economic cycle. They managed to have the

master order for every collection closed one year in advance, facilitating management forecasts.

WEAKNESS

• Predominance in the Asian markets: 39% of sales comes from Asian markets where the company operates in the area with 95 stores that

represent 49% of total DOS. The majority of them are in China, where political instability given by the Chinese government could lead to

relevant change the regulations without forewarning. Furthermore, the recent diplomatic instability between South Korea and China with

the travel ban for Chinese tourists could affect the Korean fashion luxury market.

• High exposition to Fall/Winter collection: Moncler product portfolio is highly unbalanced on clothing for the cold seasons, with a

reputation strictly related to the down jacket. This item represents 80% of the weight of sales, at the expense of Spring/Summer collection.

• A brand not “made in Italy”: MONC is not classifiable as a “made in Italy” company, production of the goods takes place outside the

Italian country. The qualification of “made in Italy”, often, conveys the customer a high quality of the product and a creativity in the design,

especially in the luxury fashion industry.

• Outage in collaboration with famous designers: Moncler recently interrupted Gamme Rouge and Gamme Blue, its high-end collections,

ending a long lasting relation with two important designers, Giambattista Valli and Thom Browne. This could create a reputational loss:

these products were exhibited during the events of international importance in the fashion world.

• Engagement with the community: Moncler clearly understands that interactive and engaging social media is vital to enable them to

appear relevant to their target audience. Despite that, Moncler has a gap with respect to its competitors in terms of its presence in social

media, which can be filled with investments in targeted marketing policies. The company has 2.9 mln followers on Facebook and 1.2 mln

on Instagram, less than its competitors.

Facebook Instagram

• Moncler – 2.9 mln • Moncler – 1.2 mln

• Prada – 6.3 mln • Prada – 14.6 mln

• Burberry – 17 mln • Burberry – 10.8 mln

• Tod’s – 1.1 mln • Tod’s – 925k

• Cucinelli – 75k • Cucinelli – 211k

• LVMH (Louis Vuitton) – 20 mln • LVMH (Louis Vuitton) – 21.2 mln

• Kering (Gucci) – 16 mln • Kering (Gucci) – 21.1 mln

OPPORTUNITIES

• Developing emerging markets: the strong presence in the emerging markets (Asia and Latin America) is a key element to success. If the

growth of Asian markets is now stable at high levels, we must not forget that Latin America is a virtually unexplored market: Moncler has

only a retail store in Brazil.

• Expansion in product line: MONC is aiming to diversify its product portfolio through the "monclerization" ideology, going from 80% of

the outerwear to a gradual reduction to 65%/70% over 4/5 years. This is to introduce new accessories, approaching a younger audience,

such as the generation Y. The accessories as well as having a good margin allows the implementation of cross-selling strategies, without

departing from the original Moncler concept.

• Improvement of the E-commerce: online will represent a more and more important channel for sales. A recent report from Bain & Company

shows for online shopping a 24% YoY growth rate and in Asia more than 75% of the population uses this channel habitually. These aspects

will allow a decline in the cost of sales.

CFA Institute Research Challenge · 16th February 2018 13• Focus on the tourist market: The double-digit growth in the flow of tourists at a global level has led and can still lead management to

increase exposure in the airport areas, in tourist resorts and in the larger hubs.

THREATS

• Maintaining a premium price range: even though a high price it’s justified by quality and desirability, Moncler’s products are achievable

only for a narrow range of consumers. Millennials have less money to spend compared to baby boomers: this can pose a threat to the

future.

• Competitors: players like Gucci, Louis Vuitton, Prada and Burberry are present worldwide and pose a serious threat. Capturing fast

changes in consumer preferences with an excellent time to market will be more and more challenging, with every brand fighting for market

shares.

• Counterfeit products: trademarks and other intellectual property (IP) rights are fundamentally important to reputation, success and

competitive position. Unauthorized use of these, as well as the distribution of counterfeit products, damages the brand image and profits.

Moncler products are among the most counterfeited in the world with a consequent drop in sales and reputational. In recent years, systems

for checking the authenticity of products have been developed, but the threat is to be constantly monitored.

• Production concentrated in Romania: 80% of the total production of Moncler is located in Romania. This relevant concentration lead to a

serious geopolitical risk (see Investment Risks).

• High rents in top retail locations: an important amount of the selling expenses comes from the rent of the real estate where Moncler set

the location of its DOS. They are often located in the city centre, in high-class shopping districts: rents are expensive and the bargaining

power of the landlords is relevant.

• Relevant presence of Private Equity: in the shareholder structure of Moncler is still present a Private Equity player, Eurazeo. In addition,

the deputy CEO of Eurazeo, Virginie Morgon sits in the BoD and she is the vice-chairman of the BoD. This could limit the freedom of action

in decision-making.

Valuation

DCF Model Assumptions

The forecasts implicit in the estimation of the income statements and cash flow statements for the next years have been constructed starting

from an historical basis and adding volatility noise in function of the different micro and macro-economic scenarios on which Moncler will be

incepted in the next five years.

Revenues

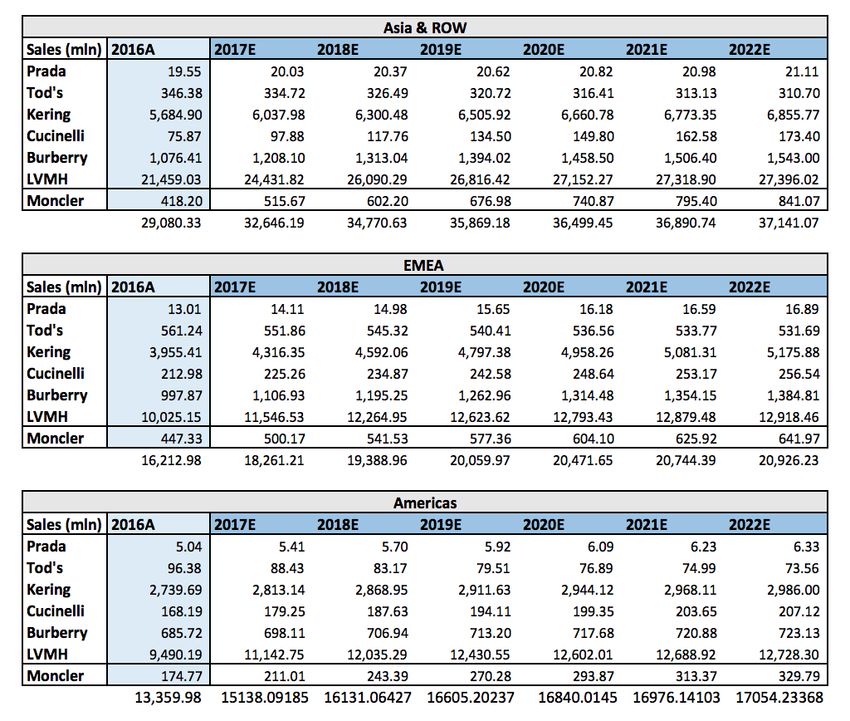

The forecasts on revenues have been exploded into the four different macro regions and they vary in the three different scenarios designed by

the analysts, mainly relying on the statistics coming from the International Monetary Fund for the macroeconomic trends, on the analysis related

to the international luxury fashion market and the dynamics of the competitors’ market shares.

Income inequality and luxury fashion market

The Moncler products, in particular the down jacket, the most important one at the moment in term of weight on total sales, are considered

luxury goods. The American economist and sociologist Thorstein Bunde Veblen invested his life in studying the main microeconomic and

macroeconomic factors that impacts the level of consumption of luxury goods in an economic environment.

His theory, known as the Veblen effect, shows an abnormal market behaviour where consumers purchase the higher-priced goods whereas

similar low-priced (but not identical) substitute are avaible on the market. This apparently non-rationale effect is caused either by the belief that

higher price means higher quality, or by the desire for conspicuous consumption (to be seen as buying an expensive, prestige item).

As shown in the analytic demonstration in the annexes, one of the main macroeconomic factor that increases the demand of luxury goods in

an economic environment is the level of income inequality, statistically measured through the Gini index, while the microeconomic indicators

are more related to the social aspect of consumption, that is not of interest in this section: what the analysts want to demonstrate is that an

economic environment with an increasing income inequality usually fosters consumption of luxury goods.

The relationship found is an addictive forecast tool for the analysts to predict the growth rates in the revenues for Moncler in the different macro

regions around the world.

What would be the impact for Moncler revenues?

Moncler is massively exposed to the Asian market, in particular toward the Chinese market, where, in the average case scenario, Moncler will

sell around the 50% of its revenues in the next decade. The Chinese economic environment presents a huge level of income inequality at the

moment, one of the highest level of the world, with the richest 1% of households owning a third of the country’s total wealth and the poorest

25% of the population owning only 1% of the total wealth, according to a report recently published by Peking University. In fact, the Gini Index, a

recognised index of measure for the income inequality in an ecosystem, is at a very high level in China in 2017, around 0.48 in the most advanced

Chinese provinces: Shanghai, Tianjin, Jiangsu, Zhejiang, Guangdong, Shandong, and Fujian, where Moncler is massively present with a huge

concentration of stores.

CFA Institute Research Challenge · 16th February 2018 14According to the World bank, a level in the Gini Index above 0.4 has to be considered as a very dramatic level in the income inequality for a country. The forecasts for the Chinese economy income distribution are not optimistic: the income inequality will remain stable to the actual level, according to the forecast of the World bank. At the same, the Brazil ecosystem, where Moncler has at the moment only one store and so huge potential to grow, presents a higher level of Gini index, one of the highest level in the world: 0.51 and not decreasing in the long run (World Bank data). This trend in the income inequality is also spread in the entire Latin America. Given these macroeconomics trends in income inequality in the strategic regions of Asia and South America, the analysts have found another proof to sustain the assumptions on macro and microeconomic drivers for the growth rates exploded below, in particular on those regions where a high stable level on income inequality will have a positive effect on the consumption of luxury goods, among those the Moncler products. HNWI and income inequality Besides the Gini Index, another measure used in the recent years to track the income inequality in a country is the number of High Net Worth Individuals (HNWI), individuals that have a net wealth of 1 million USD. China is experimenting an increasing number of HNWI in these years: in 2008 the number amounted to 2.4 million and nowadays is reaching 6 million. The same trend has been followed in South America, with a number of HNWI at 0.2 million in 2008 to 0.6 at the moment. The increasing number of HNWI is symptom of an increasing income inequality in these countries, where Moncler could so sell more of its fashion luxury products. 1. Average case scenario - Target Price: €26.93 - Probability 80% Macroeconomic Trends In the average-case scenario, the international economic system will track the following paths. The economic environment in the USA will experiment a soft landing in term of decreasing but positive growth: from a growth rate of 1.8% expected in 2018 to a stable 1.1% in 2022. The USA performance will be driven by a probable macroeconomic policy mix: the FED will soon accelerate the tapering and at the same time the fiscal expansionary policy will lead to a strong consolidation, in particular for the small medium cap firms, that will allow the USA economy to maintain stable growth in the long run. In the South America, the status quo will continue: some countries, like Venezuela, will fail in trying to reach an economic independence from energy commodities and stabilize their economies, but many others, like Brazil, will strengthen their economic environment and their main cities will experiment huge tourism inflows. This positive effect will put upward pressure on the average macroeconomic performance of Latin America, that, according to the IMF, will grow from 0.8 in 2018 to 1.7% in 2022. In the European Union, the “wait and see” status will prevail: a weak stable average growth between member states, characterized by increasing divergence between core Europe and South Europe. The Euro-area on its complex will grow from 1.8% in 2018 to 1.4% in 2022, with the following divergent paths for the stand alone main countries: from 1.7% to 1.3% for Germany, from 1.3% to 1.4% for France, from 1.1% to 0.9% for Italy and 2.7% to 1.8% for Spain. Nationalism political movements will remain minorities in the European political environment and stability will allow more convergence to a more and more united Europe. China will slowly affirm its leading country status in the world, with a positive stable growth driven by an affirming middle class that will dispone of an increasing purchasing power and an even higher will to align itself to occidental standards: China will grow from 5.9% in 2018 to 5.1% in 2022. Middle East will continue its plan in converting its economy toward a more diversified ecosystem, open to foreign capital flows and investments. UAE will experiment consolidated growth rates from 3.9% to 4.3% in 2022. Microeconomic Trends Moncler will succeed in increasing its market share among all the regions, in particular thanks to an aggressive plan of CAPEX in advertising and a more flexible business structure that will allow a deep reduction in time to market. The market share in Asia&ROW will increase from 1.44% to 2.22%, from 2.76% to 3.14% in EMEA and from 1.31% to 1.88%, on a market considered composed by Moncler and its direct peers. What will be the impacts on Moncler Revenues? The combination of macro and microeconomic trends will have an average positive impact on the revenues of Moncler that will experiment a stable but limited growth aligned to the actual rate of growth in Italy, with total sales of €172 mln in 2022, and EMEA, where Moncler will sell €409 mln in 2022. In the Americas, the growth in revenues will be driven mainly by an expansion on the South part, where the presence of Moncler and competitors is practically insignificant at the moment and the space to grow is very wide, and by the consolidated USA market: the revenues in the Americas will reach €296 mln in the next 5 years. The mainly part of the growth in sales will be driven by high Chinese demand that will lead the Chinese market to have a weight of 46-48% in the long run, with a level of €753 mln. CFA Institute Research Challenge · 16th February 2018 15

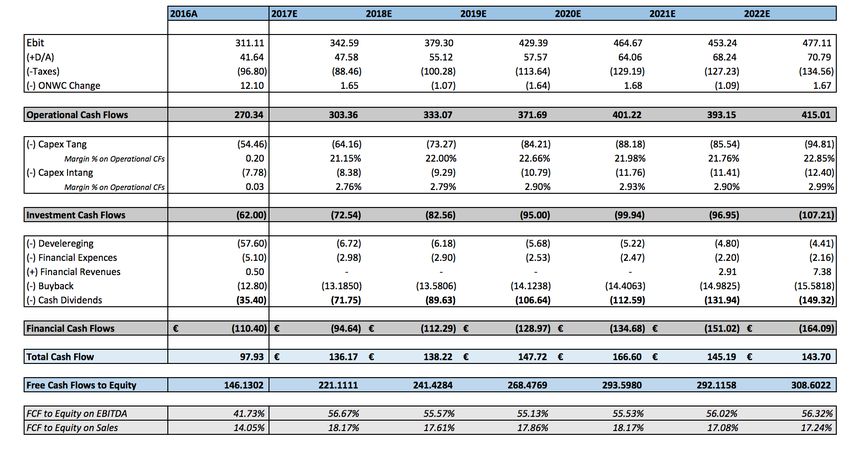

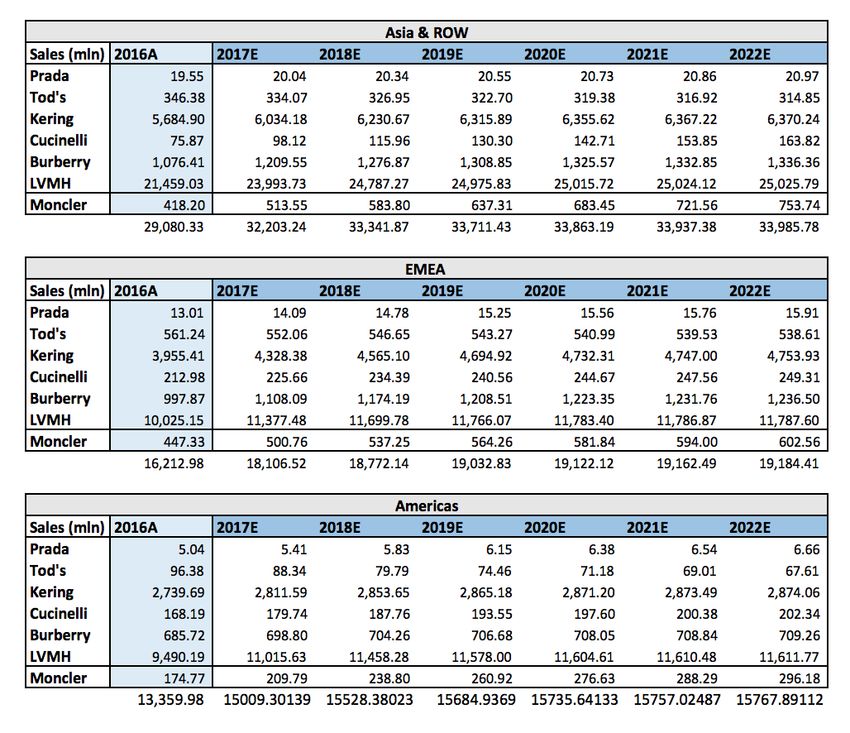

Source: Team estimates 2. Worst Case Scenario - Target Price: €20.35 - Probability 10% Macroeconomic Trends In the worst-case scenario, the international economic system will experiment the following trends. The USA as a leading country will no longer be a reality: it will soon arrive to the end of its expansive cycle. The downside trend will be further amplified by the tensions with others powers around the world that will lead to a significant slowdown in commercial traffics, so a reduction in the exports volumes and of the GDP. In the Latin America, countries will fail on convert their commodities depended economies, exposing themselves to high risk of slowdown on commodities prices. On this weak economic environment, countries like Venezuela will impose a huge risk of contagion: a sovereign debt crisis could be fostered and followed by a deep loop recession. Europe will enter a long period of political instability due to the emerging and affirming sovranist political movements. The expansionary monetary policy will soon come to an end and the south European countries will experiment a destabilizing sovereign debt crisis driven by the increase on credit spreads: given the huge stock of sovereign debt on the balance sheets of the European banks, the recession caused primarily by a heavy austerity will be further amplified by a banking doom loop and credit crunch that will further amplify the recession. In the Asian macro area, the geopolitical tensions between China and North Korea will lead to a slowdown in commercial traffics, with huge increase on import duties and more travel bans imposed by the Chinese government to the Chinese population around the world. This is an extreme left tail scenario for describing what will be the international economic environment on which Moncler could have to live in the next years. The downside impact on Moncler revenues in the four different macro regions around the world will be significant but, given the non–cyclicality of luxury business, restrained. One the possible path that the Moncler revenues will follow under these assumptions has been reported below. Microeconomic Trends Moncler will succeed in defending its market shares among all the regions. The market share in Asia&ROW will remain stable at around 1.5%, 2.8% in EMEA and 1.4% in the Americas, on a market considered composed by Moncler and its direct peers. What will be the impacts on Moncler Revenues? The combination of macro and microeconomic trends will have an average negative impact on the growth rate of revenues for Moncler that will experiment a positive but decreasing growth, with total sales of €1.21 bn in 2017 and a level of €1.29 bn in 2022. In particular, in Italy the growth rate will converge to zero in five years, with a total revenue of €157 mln in 2022. The same trend will be followed by all the EMEA macro region, with a revenue of €362 mln in 2022. The revenues in the Americas will reach €224 mln in the next 5 years, given a decreasing and converging to zero growth rate. The main part of the revenues will come from the Asiatic regions, where Moncler will sell a total worth of €551 mln in 2022. CFA Institute Research Challenge · 16th February 2018 16

Revenues Evolution 5Y Income Statement (First Stage) CFA Institute Research Challenge · 16th February 2018 17

5Y Cash Flow Statement – Free Cash Flow to Equity (First Stage)

FCF to Equity (First and Second Stage)

Terminal Value (Third Stage – Growth Long Term Inflation Rate)

Source: Team estimates

3. Best Case Scenario - Target Price: €29.84 - Probability 10%

Macroeconomic Trends

In the best-case scenario, the international economic system will follow the paths below.

The strong USA economy continues its phenomenal positive trend in the short term and will experiment a stable growth in the long run.

In the Latin America, an affirming political stabilization paired with a credible plan of economic conversion toward a less commodities dependent

ecosystem will allow the South American countries to boost growth and maintain it in the long term, containing the level of debt and attracting

growing masses of tourists.

In the European Union Area, the United States of Europe will be a reality and the Eurozone will finally converge toward an optimal monetary

equilibrium, thanks to a more symmetric economic environment and a very flexible job market. On this context, Germany will significantly

expand his public spending and so contributing to boost all the economies in the Union toward convergence. North Africa countries will become

strategic commercial partners with huge potential in the long run, toward the rebirth of a fertile Mediterranean economic system.

China will converge toward a foreign friendly economic model, inclined to international commercial traffic, in a context of political stabilization.

Import duties will be strongly reduced and the new Silk Road will sign a leading partnership between Asiatic countries and the Middle East,

especially with the growing UAE.

China will follow a long-term path of investments on social, environmental and energetic sectors, that will allow to the country to affirm itself as

a leading country in the next decades.

CFA Institute Research Challenge · 16th February 2018 18You can also read