Chengdu Hosted in Southwest University for Nationalities

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CFA Institute Research Challenge

Hosted in

Chengdu

Southwest University for Nationalities

Student Research

Manufacturing Sector: New Energy Industry

This report is published for educational purposes only by students Hong Kong Exchange (HKEx)

competing in The CFA Institute Research Challenge

BYD Company Limited

Date:31-Aug-2016 Closing Price: HKD54.00 Recommendation: BUY (20.17% upside)

Ticker: BYDHK: Wind Database CNY1.00: HKD1.18 Target Price: HKD64.89 (CNY54.86)

Executive Summary

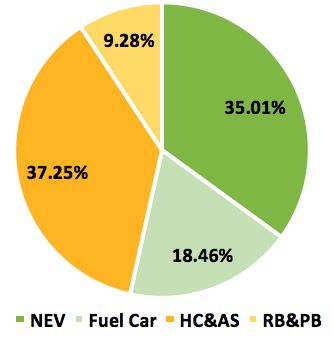

Table 1: Market Profile BYD Company (Hong Kong) Limited (BYDHK or the Company) is a Chinese manufacturing

Market Profile company, which covers three main areas: Automobile Business (AB), Handset Components and

Assembly Services (HC&AS), and Rechargeable Battery and Photovoltaic Business (RB&PB).

Closing Price HKD54.00

Investment Recommendation

52-Week High/Low HKD54.00/HKD30.50

We issue a Buy recommendation on BYDHK with a four-month target price of HKD64.89, that is

Average Volume(1Y) 6,122,016 20.17% over its August 31, 2016 closing price of HKD54.00. Our target price is primarily based on:

Diluted Shares Out 2,728,142,855 Investment Thesis and Outline

Market Cap(HKD in Backed by a promising industry outlook, BYDHK continues its leading position in new energy

Millions) 16,436

industry. The combination of the Sum-of-The-Parts valuation and current market view of BYDHK’s

Beta 1.19

every sector suggest that the stock price of BYDHK is undervalued. This represents an opportunity

EV/EBITDA 24.52 to invest in China’s new energy industry. After determining BYDHK’s exposure and mitigants to

P/B 3.88 investment risks and evaluate the corresponding impacts on valuation, we arrived a Buy

recommendation.

P/E 44.37

• Promising Industry Outlook, with the rising concern over environmental and energy problems,

Source: Wind Database

and strong policy support for new energy industry, the demand of new energy market is on the

rise.

Table 2: Valuation

• Leading Position in New Energy Vehicle (NEV) Market, BYDHK occupied the market share

Valuation of around 27% of Chinese NEV market, and with its advanced battery technology and vertical

integration ability, and independent research and development (R&D) technologies which will

Valuation DCF Multiples soon be used in every BYDHK’s NEV, it is believed that this will enhance BYDHK’s competitive

Estimated Price HKD74.60 HKD55.18 position and will at least secure BYDHK’s market share.

- BYDHK is expected to reach RMB122.8 billion in NEV market by 2020.

Weights 50% 50%

- In HC&AS field, BYDHK will get more orders from manufactures in its filed through its new

Target Price HKD64.89

material and advanced technologies.

Source: Team Calculations • Highly Integrated Business Mode, BYDHK believes through integrating solar power, energy

storage and electrified transportation together can achieve company’s main strategy, this will

drive BYDHK:

Figure 1: Monte Carlo Simulation - More competitive in energy field by reducing manufacturing costs.

30000

Sell Hold Buy

- Fully integrating new energy market from electric power generation to electric storage, and

25000 4.19% 35.21% 60.6% finally to electric applying in NEVs and other fields.

Frequency

20000

• Sum-of-the Parts Valuation, using the Discounted Cash Flow (DCF), and three ways of

15000 Relative Multiples Valuation to value AB, HC&AS and RB&PB separately.

10000

• Investment Risks, including regulatory, market, and operational risks that were assessed 1) for

5000 impact and likelihood and subsequently ranked in a risk matrix, and 2) modeled through a Monte

Carlo simulation.

0

- The results of the Monte Carlo simulation show: 60.6% of the simulations support a buy

recommendation, 35.21% support a hold recommendation, and 4.19% support a sell

Sell Hold Buy

recommendation.

Source: Team Calculations

Table 3: Key Financials and Ratios

Figure 2: Share Price Movement Key Financials and Ratios

70 4500 2014 2015 2016F 2017F 2018F 2019F 2020F

4000

60

RevenueҁCNY in Billions҂ 55.4 77.6 101.5 120.9 145.6 177.0 217.1

3500

50

Net ProfitҁCNY in Billions҂ 0.7 3.1 5.2 7.3 10.0 13.4 17.8

Hang Seng Index

3000

Price Per Share

40 2500 Net Profit Maigin 1.34% 4.04% 5.15% 6.03% 6.86% 7.57% 8.21%

30 2000

Fixed Asset Turnover 1.49 1.99 2.15 2.31 2.46 2.60 2.74

1500

20

1000

Long-term Liabilities to Assets 0.12 0.10 0.06 0.05 0.03 0.02 0.02

10

500 Interest Coverage 1.53 3.07 3.80 4.71 5.72 6.43 7.05

0 0

Earnings Per Share (EPS) 0.18 1.12 1.75 2.48 3.42 4.61 6.16

BYDHK HSCI.HI Return on Equity (ROE) 2.56% 8.71% 9.33% 11.47% 13.52% 15.29% 16.86%

Source: Wind Database Source: Company Data,Team Calculations

1

Figure 3: Milestones of BYDHK Business Description

Founded in February 1995, BYDHK was listed on Hong Kong Stock Exchange and Shenzhen Stock

1995: BYD Company founded, with capital Exchange in July 2002 and June 2011, respectively (Figure 3). BYDHK principally engaged in AB

of RMB2.5 million and 20 members including traditional fuel-powered vehicles and NEV, as well as handset, computer components and

assembly services, and BYDHK is also developing other new energy products such as

rechargeable battery (RB), solar power station, energy storage station, LED business, etc.

2002: Listed on the Hong Kong Stock

Exchange Main Board (1211.HK) Currently, BYDHK has nearly 200,000 employees and 22 industrial parks in the globe. BYDHK has

reached revenue of RMB43,745 million in the first half of 2016 (1H16) (Figure 4), representing a

year on year (YoY) increase of 43.74%, having made a profit of RMB2,260 million with YoY growth

2003: Purchased Xi’an Tsinchuan of 384.23%. The earnings per share was RMB0.87, implying a YoY increase of 359.90%.

Automobile Company Limited Automobile Business

In 2003, BYDHK purchased Xi’an Tsinchuan Auto Co.,Ltd and formed the present BYD Auto Co.,Ltd,

2007:BYD-E listed on the Hong Kong Stock which formally symbolized its entry into the vehicle manufacturing and selling. Nowadays, BYDHK

Exchange Main Board(0285.HK) has established six industrial parks of auto industry. The automobile products include high, medium

and low end of fuel cars, and also include auto mold, auto parts, dual model electric vehicles and

2008: Warren Buffett invested $232 pure-electric vehicles. The total sales volume of car increased to 180,000 with the YoY growth of

million to take a 9.89% stake in BYDHK -14.28% in 1H16 (Figure 5). Comparing with the decline in sales volume of fuel cars, NEV has

realized a rapid growth, whose sales volume has increased to 49,000 with YoY growth of 130.74%

and ranks the first in the world reaching out to 190 cities in 43 countries of six continents. In public

2011 BYD (002594.SZ) was listed on the

Shenzhen Stock Exchange transportation, BYDHK will continue to expand the application of pure-electronic buses and taxis in

global markets. BYDHK has successively won the UN-DESA Energy Grant and Zayed Future Energy

Prize since its popularization and application of the green energy.

2014: BYDHK announced the “5-4-2

Initiative” for NEV Handset Components and Assembly Services

As one of the most comprehensively competitive HC&AS suppliers around the world, BYDHK

provides vertically integrated one-stop services from whole product design, component

2015: BYDHK launched “7+4” Vehicle manufacturing to assembly services for both domestic and overseas markets, and also provides

Electrification Strategy other electronic products’ design, component production and assembly services. According to the

interim report in 2016, this business realized a revenue of approximately RMB16,293 million, of

Source:Company Data which 95.03% came from its holding company-BYD Electronic (International) Company Limited

(BYD-E) (Figure 7). Handset assembly mainly including EMS and ODM and metal casing are the

products that contribute most to the revenue of this business.

Rechargeable Battery and Photovoltaic Business

Figure 4: 1H16 Revenue Breakdown BYDHK’s RB business mainly includes the lithium-ion battery and nickel battery, which are widely

used on handsets, digital cameras, power tools, electric toys and all areas of portable electronic

devices. And, BYDHK also actively researches on and develops power batteries, energy storage

batteries and solar battery products to be applied in the NEV, storage power station and

photovoltaic power station. The company focuses on the new energy chains to provide clients with

the integrative solutions in power generation, storage, transmission and utilization. Several solar

programs of BYDHK have already successively operated in the international markets, including the

United States, German, Japan, United Kingdom, Indian and South Africa, having recorded the

revenue of RMB4.06 billion in 1H16 and turned around with a profit (Figure 8). Meanwhile, BYDHK

has its advanced Double-glazed Solar Photovoltaic module technology, which has a longer product

life cycle and more durable than other products.

Strategy

• Three Green Energy Dreams. This is the final vision of BYDHK to realize the zero emission,

zero pollution, green energy solutions of the whole industry chain from power generation, storage,

transmission to usage (Figure 9).

Source: 2016 Interim Report • The Strategy of Vigorously Developing the NEVs

- BYDHK put forward the “7+4” Vehicle Electrification Strategy (“7+4”) (Figure 6), sparing no

efforts to realize the market diversification. “7+4” refers to popularizing the NEV and realizing

its overall coverage in seven conventional fields (private cars, buses, taxis, sanitation

vehicles, urban commodity logistics, passengers transportation and urban construction

logistics) and four specialized fields (warehousing, mines, ports and airports).

Figure 5: Sales Volume and

YoY Growth of AB

Figure 6: “7+4”

0.6 2

0.5

1.5

0.4

1

Million

0.3

0.5

0.2

0

0.1

0 -0.5

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 1H16

sales volume of BYDHK' A&B yoy BYDHK'volume growth

Source: Company Data,Team Calculations Source: Official Website

2

Figure 7: HC&AS’s Revenue - In April 2014, BYDHK published the “5-4-2 Initiative” target for the NEV in the future and

and YoY Growth redefining the standards of the NEV from three aspects: performance, security and fuel

35 50%

consumption. As for the “5-4-2 Initiative”, “5” represents the 0 - 100 km/h acceleration time of

30 40% less than 5 seconds, “4” refers to electric four-wheel drive, “2” means within 2 liters of fuel

25 30% consumption per 100 km. In the future, most of BYDHK’s NEV will implement the standard of

20 “5-4-2 Initiative”.

Growth

20%

billion

15 10%

• Low-cost Strategy

10 0% - BYDHK makes the vertically integrated industry chain in all three businesses, adheres to self-

5 -10% owned brand, independent R&D, forges one-stop service with the core of R&D design and

0 -20%

independently assembly manufacturing.

20092010201120122013201420151H16

- BYDHK enters into the market by selling and also actively plans, optimizes technological

BYDHK BYD-E Growth of BYDHK process in the field of new energy҅lowering the per unit production cost through economies

Source: Annual Report of scale.

- In June 2016, BYDHK signed the “Cooperative Framework Agreement on the Exploitation of

Figure 8: The Revenue of Lithium Resources in Salt Lake” with Qinghai Salt Lake Industry Co., Ltd(QHSL) and

RB&PB Sector Breakdown Shenzhen Hongdatong Industry Co.,Ltd, in developing the lithium resource of the Salt Lake

together and lower the production cost from the upstream.

700

600

500 Corporate Governance

Thousand

400

Shareholder Structure

300

As of July, 2016, Wang Chuanfu is the first major shareholder, also the ultimate controlling owner,

200

owning 18.79% of the common shares directly. On the whole, three top managers (Wang Chuanfu,

100 Lv Xiangyang and Xia Zuoquan) of BYDHK own 38.08% of the outstanding shares directly or

0 indirectly (Table 4), and 16.15% of all common shares are held by corporations and institutional

2010 2011 2012 2013 2014 2015 1H16

Revenue investors. The public owns the remaining 45.77% (Figure 10) (Appendix 22).

Source: Annual Report,Team Calculations Corporate Governance

The appraisal system of corporate governance mainly consists of equity structure, dividend policy

and organization structure.

Figure 9: Three Green Dreams • Equity Structure: the gap of shareholding ratio among the major shareholders of BYDHK is

quite small and the inside directors account for the largest proportion of shares among the top 10

major shareholders while the Board of Directors owns the high control power, which is beneficial

for the company’s sustainable development but goes against the protection of minority interests

(Appendix 26).

• Dividend Policy: dividend instability will be detrimental to equity financing since BYDHK’s

higher research and development cost and it needs to unload the last year’s profits as the next

year’s capital (Appendix 27).

• Organization Structure: BYDHK owns the Board of Directors, Board of Supervisors, CEO and

Source: SINA all kinds of committees.

- Board of Directors, which has complete structure, meets the relevant regulation of the

Table 4: Shareholding of Top corporate law and rich experienced members can provide constructive feedbacks and

Management development direction for our company’s development. As the founder of the company as

well as the major stockholder, the inside board has strong control power of the company,

Shareholding of Top Management which is conducive to the company’s continuous and stable development but against the

Directly Indirectly

internal supervision (Appendix 23).

- Board of Supervisors, which has complete structure, conforms with the relevant regulation

Wang Chuanfu 18.79% 0.18% and the rich experienced members, whose average educational background are

undergraduate course, can provide effective and scientific supervision for the company. The

Lv Xiangyang 8.77% 5.96%

supervision of the board of supervisors will be more powerful if the outside and inside boards

Xia Zuoquan 4.36% 0.02% of supervisors could be supplemented with each other. Besides that, the average age of the

supervisors except for the chairman of the board of supervisor is 42.5, so the board of

Source:Company Data supervisor performs well.

- CEO has the strong control power and performs well but it will be detrimental to realizing the

scientific decision and well supervision since it plays multiple roles and has the absolute

Figure 10: Shareholder Structure control power in the company (Appendix 24).

- Committee with complete inside control system meets the standard and manages well.

Overall, the corporate governance is in accordance with its articles of association, without any

obvious conflict. It is reasonable to conclude that nowadays BYDHK manages and operates well,

but still exists risks.

Social Responsibility

BYDHK has established the CSR supreme decision-making body—CSR Management Council,

defining the management method of CSR, organizing and formulating the unified CSR working plan

to make CSR management identification and standardization and realize the unified organization

and effective management of CSR work. BYDHK did well in social responsibility, environmental

Source:Company Data protection, employee policies and it has received a number of awards and honors (Appendix 25).

3

Figure 11: Real GDP Industry Overview and Competitive Positioning

10.0

Macro Economic Analysis

8.0

6.0

• The growth of macro economy has slowed down, but progressed steadily, In 2016,

global economy has made deep changes. Developed economies are recovering slowly while

4.0

economic growth rate of emerging countries is decreasing. With the growth rate of 6.7% 1H16,

2.0 China has seen a drop in its growth. But the government moderately expanded its gross demand,

0.0 actively promoted the structural reform on supply, which makes the national economy increases

2013

World

2014 2015 2016F 2017F 2018F

Advanced Economies

while maintaining steady (Figure 11).

United States EMDE*

China India

• The income of urban and rural residents remains fast growth, and potential

Source: IMF consuming capacity is improving, in recent years, fast growth of China’s economy has made

the income of urban and rural residents remain faster growth, and per capita consumption

Figure 12: Contribution Rate expenditure is increasing. In 2015, China’s ultimate consuming contributed 66.4% of economic

of Combustion to GDP growth, which is 14.8 percentage point higher than in 2014 (Figure 12).

100 • Supportive Policies

90

80 - Stimulus of the Demand in NEVs

70

60 • Measures to Manage Quota on New Energy Vehicles’ Carbon Dioxide Emission

50 (Consultation Document).

• Development Plan for Energy Conservation and New Energy Vehicles

40

30

20 • Assessment Measures for New Energy Public Transportation Promoted Application (Trial)

10

0

• Notice on the 13th Five-year Plan in relation to the Incentive Policies on New Energy

1979 1985 1991 1997 2003 2009 2015 Vehicle Charging Infrastructure and the Promotion of Application of New Energy Vehicles.

- Government Subsidies for Photovoltaic Electric Price

Source: Wind Database,

• Subsidies compensated by National Development and Reform Commission has given great

iFinD Database impetus to the development of photovoltaic business.

- Policies Overseas

Table 5: Electric Price of • Energy Independence and Security Act

Photovoltaic • National Policy Energy Act

2015 2016 Industry Analysis

Resource Photovoltaic Photovoltaic Cities in Each

Region Electric Electric Region

Price Price • Automobile Industry

Ning Xia,Hai

- Automobile industry is growing slightly in whole. The growth of fuel cars is

RMB0.90 RMB0.80 Xi(Qing Hai),Jia weakening, but the growth of NEV is strong. Traditional fuel cars still dominate market

Ⅰ Region per kwh per kwh Yuguan(Gan share, but the growth of traditional vehicles field has been slowing down in recent two years.

Su),Ha Mi(Xin

Jiang),etc By virtue of favorable policies and technological progress, new energy market is developing

Beijing,Tianjin, aggressively. NEV’ substitution for fuel cars already has the realistic base (Figure 13).

Ⅱ Region

RMB0.95

per kwh

RMB0.88

per kwh Hei Longjiang, - Carmakers will increase input on industry segments and competition in these

Sichuan,etc

fields will be fiercer. Sport utility vehicle (SUV) has remained strong growth since 2013

Other cities

Ⅲ Region RMB1.00 RMB0.98 except in Ⅰ, Ⅱ and HAVAL H6 tops the SUV sales; BYDHK has become the technological innovator in NEV

per kwh per kwh region industry (Figure 14).

Source: National Development and - Subsidy policy of new energy has been adjusted. NEV industry will become more

Reform Commission standardized. China is gradually making adjustments in NEV subsidy policies. They have

the intention of turning NEV industry from driving by policy to driving by market and

upgrading the technology by combating subsidy frauds and regulating the development.

Figure 13: YoY Industry Growth - The popularized application of Internet of vehicles has become a developing

400.00%

trend. The industry will focus more on the application and progress of technology, and smart

350.00% driving will become the new growth point of this industry.

300.00%

250.00% • Handset Components and Assembly Services Industry

200.00% - The handset market is gradually saturated and will remain slight growth. Global

150.00%

100.00% shipment of smartphones raises only 0.2% to 0.678 billion handsets in 1H16, which is the

50.00% slowest YoY growth over the years. According to IDC, its growth speed will decline little by

0.00%

2010 2011 2012 2013 2014 2015 little, at an expected CAGR of 4.1% from 2016-2020.

YOY Growth of Fuel Car Industry

YOY Growth of NEV Industry - China will still be the largest smartphone market in the world. Smartphones

YOY Growth of SUV Industry

promoted by China’s brand manufacturer account for 42% of global market share. China’s

Source: CAAM,Team Calculations shipment of smartphones is 235 million in 1H16, with YoY growth of 13.0%.(Figure 14)

- Penetration of metallic parts is promoting rapidly. Sound mechanic performance and

outstanding appearance have contributed to improving the recognition of metal casings.

Figure 14: Smartphone Shipments Metallic parts are used commonly. Their market volume is expanded (Figure 15). Competition

in terms of seizing the market share among FIH Mobile Limited (FIH), Catcher Technology

Co.,Ltd, TongDa Group Holdings Limited (TongDa) and BYD-E is becoming fiercer and

fiercer. Each supplier enlarges the production capacity of CNC, improves product yield and

production efficiency, and stays competitive.

- Consumer electronics undergo frequent upgrading and fast market changes.

Updated needs of the consumers make this industry upgrade quickly. Although metal shell is

very popular now, 3D glass casing has made first appearance.

• Rechargeable Battery and Photovoltaic Industry

- Needs of traditional battery are weakening. The growth of global consumer electronics

is pacing down, but they still remain greater consumption; their competition is fierce, and

Source: Wind Database,

iFinD Database needs for lithium-ion battery and nickel battery are expected to remain in weak state in future

market (Figure 16).

4Figure 15: Utilization of Metallic Parts - Power battery and energy storage battery have increased rapidly and are

40% extremely competitive. With the aid of the rapid growth of NEV, many battery suppliers

35% are increasing their R&D investment in this field, expanding the production capacity so that

30%

they can catch the opportunity of the fast growth in market (Figure 17). The future

25%

competition will be expected to be very fierce.

20% - Opportunities and challenges coexist in photovoltaic. After terrible shuffle in the

15%

previous years, the whole industry reentered into growing path in 2015. Installed capacity

10%

has been growing rapidly, and it is expected to remain stable and orderly in its growth during

5%

the period of 13th Five-Year Plan. However, market competition is still severe and downward

0%

2012 2013 2014 2015 pressure on price is larger.

Source: News Competitive Positioning

• Technological threshold diminishes the threat from new entrants. Fast development of

Figure 16: Volume of 3C in Main NEV benefits BYDHK as a leading company in this industry. BYDHK has mastered core

Manufacturing technology of cell, engine and electric control. In addition, BYDHK has established Central

250

Research Institute, Electric Power Research Institute and Auto Engineering Research Institute

200

concentrating on the R&D and application of technology (Figure 18).

• Fierce competition among existing rivalries. NEV is the main developing trend of future

100 Million

150

vehicles. All auto manufacturers make layouts in industrial segments. What the BYDHK faces not

100 only is the pressure of other domestic brands, but also seizes the global market share. Its new

50

energy passenger vehicle(NEPV) sales volume outside of China is nearly zero.

0 • Suppliers’ ability to bargain is limited. Industries such as auto parts, steel, glass and rubber

2009 2010 2011 2012 2013 2014 2015 are very mature. Together with QHSL, BYDHK develops the lithium mineral in Salt Lake and

integrates the upstream of industrial chain vertically.

Source: Wind Database

• Moderate bargaining power of customers. For HC&AS, revenue mostly depends on the

large orders of brand handset manufacturers. Therefore, the customers remain some ability to

Figure 17: 2015 Market Scale in bargain.

Li-coin Manufacturing

90% • BYDHK has long competitiveness. BYDHK insists on self-owned brand and self-research

81%

80% and development. It has set up Intellectual Property Department and has initiated Talents Training

70% 60.30%

Program. By self-researching and developing to promote automobile performance and reduce the

60% cost, adverse impacts on adjusting subsidy policies and decreasing local subsidy can be

50% counteracted. Then, cost performance can be promoted in whole; brand planning and media

40% 32.30% communication and planning department have been built to improve brand image; its business

30%

17% layout is comprehensive (Figure 19) (Appendix 21).

20%

7.40%

10% 2% Investment Summary

0%

energy storage power parts 3C We issue a BUY recommendation on BYDHK with a 4-month target price of HKD64.89 by

2014 2015 combining a DCF Analysis and a Relative Multiples Valuation. This offers a 20.17% upside from its

Source: CNII closing price of HKD54.00 on August 31, 2016.This valuation is supported by numerous merits, as

outlined below, as well as concerns taken into consideration.

Figure 18: Porter's Five Forces MERITS

• High Growth in Sales Revenue of NEV

- As the environmental and energy problems have become increasingly prominent, and

the government has paid more attention to the NEV industry, NEV industry will enter into

a period of rapid growth. (Figure 20).

- BYDHK is the leader in the field of NEV industry. In the aspects of strategy, the company has

implemented the "7+4" and "5-4-2 Initiative” with a clear management idea; in the aspects of

production, BYDHK is currently the only company mastered the core technology of electric

cars including cell, engine and electric control in the world, owning an obvious technical

advantage.

• Expectations on the Outbreak of Sales Revenue of RB&PB

Source: Team Calculations Rechargeable Battery Business

- With the widespread use of lithium battery in NEV and power storage station market, BYDHK

RB will enter into a new period of growth.

- BYDHK has the technological superiority on the RB. Owning the key technology, BYDHK’s

Figure 19: SWOT Analysis lithium iron phosphate battery takes the domestic market share of more than 25%, ranking

first. In the aspect of ternary batteries, company has a long-term accumulation of R&D as well

as full technical reserves. The ternary batteries have been put into use in the plug-in hybrid

electric vehicle (PHEV).

- BYDHK has the advantages on battery production capacity. BYDHK had built the world's

largest lithium iron phosphate battery production base in 2015. The company expands the

capacity of lithium battery, and is expected to reach more than 13GWH in lithium battery

production capacity by the end of 2016 (Figure 21).

Photovoltaic Business

- There are opportunities exist in the field of photovoltaic industry. In 2015, the global

photovoltaic installed capacity has a rapid growth, and the newly increased installed capacity

Source:Team Calculations

in China hit a record high. Although the product price in photovoltaic industry still maintained

long-term low (Figure 22), it may bring the explosive growth of sales revenue to BYDHK with

the development of the photovoltaic industry. 5Figure 20: Sales Volume of NEV Industry - BYDHK has the advantages of industrial chain in the photovoltaic business. In the terms of

1.8 the photovoltaic business, BYDHK is planning a complete new energy industry chain, which

1.6 provides customers an integration scheme with the power generation, transmission and

1.4

storage of electricity. It is unique in the global market.

1.2 •Sustainable Development of HC&AS

- The shipment of the global smartphone market slowed down, but the replacement rate of

Million

1

0.8 intelligent mobile phone will maintain steady growth. And, metal casing expands the scope of

0.6 application from the high-end models to low-end models with its superior quality and

0.4 performance, and is expected to have more shares in the future.

0.2

- BYDHK has the advantage of technology. In the application of key raw materials, BYDHK has

0 developed PMH technology, realizing the Nano-level fusion of metal and plastic and solving

2011 2012 2013 2014 2015 2016F 2017F 2018F 2019F 2020F

sales volume of NEV industry sales volume of BYDHK's NEV

signal problem. In the aspect of design, the company has SBID technology and can meet the

needs of high-end mobile phone manufacturers.

Source: CAAM,Team Estimates - Keeping cooperation with major manufacturers. Its assembly business gained EMS orders

from the domestic leading brands of smartphones in 2015, and is expected to continue the

cooperation in the future.

• Cost Advantage of the Vertical Integration Mode

Figure 21: Battery Capacity AB: most of BYDHK auto parts can achieve self-sufficiency. For the NEV, BYDHK can supply

three key parts of cell, engine and electric control.

14

12

Rechargeable Battery Business: BYDHK can product electrolyte diaphragm and cathode

materials by itself. And in 2015, the company joined efforts in developing lithium mineral with

10

QHSL , controlling the raw materials.

8

GW

6

Photovoltaic Business: BYDHK has a whole production chain from silicon, PV module to the

solar power station. By controlling the costs of raw materials, the company can minimize the

4

costs, equaling the cost of photovoltaic power with that of coal power. And coupled with the

2 layout of power storage station conducted by the company, it forms a strong synergistic effect.

0

2014 2015 2016F HC&AS: Thanks to the vertical integration platform, BYDHK has cut the product costs and

significantly reduce the development cycle.

Source: Wind Database

Valuation Method

We used a DCF, a Relative Multiples Valuation. The weight of each method is equal to 50%.

Concerns(Possible Investment Risks)

Figure 22: Polycrystalline’s Price

• Policy Risks: The demands of NEV may be in an insufficient situation, which will be incapable

60

of completing the target sale volume. Decelerated growth of China’s GDP, declining policy

subsidies, and insufficient support of the government may affect the sales of NEV.

50

40

• Industrial Risks: 1)The prospect of NEV industry attracts more manufacturers to research the

NEV, increasing competition. 2)The demands for nickel battery decreased year by year, and it will

RMB

30

affect BYDHK's revenue in a way. The prior-period investment of BYDHK was mainly in the R&D

20 of the iron battery, so it does not have an absolute advantage in the production of the ternary

10 battery. If the ternary batteries become the main trend in the future, the company will not have the

absolute competitiveness. 3) The product prices of photovoltaic industry may slump in the future,

0

and competition will be more intense in such an environment. 4) The saturation of global

smartphone and computer markets will aggravate competitions among existing competitors.

• Operational Risks: The company's brand image needs to be improved. The appearance

Source: Wind Database design has been criticized for a long time; the amount of the quality complaints of fuel vehicles

has ranked near the top in the last year; staffs in some sales region appears serious violations.

The company's sales revenue will be negatively affected if it does not resolve the problems

existing in brand image and sales management.

Figure 23: BYDHK Share Prices and News Flow

70

Subsidies to BYDHK's New Energy bus program Financing

BYDHK popularized in

NEV in Beijing, and finished China's market is

60 American Energy completed

Shanghai crashing

market

50

Orders from abroad of

pure-electric bus; air

40 polution causes energy

saving

30

Smart Driving has been carried

out

20 BYDHK is plainning to raising

RMB15 billion after trading Chinese president Xi

Explosion of charge suspension in May

10 Jinpin visited BYDHK's

station for taxi in

factory in UK

Hong Kong

0

Dec-12

Dec-13

Dec-14

Dec-15

Jun-13

Jun-14

Jun-15

Jun-16

Aug-12

Aug-13

Aug-14

Aug-15

Aug-16

Oct-12

Oct-13

Oct-14

Oct-15

May-13

May-14

May-15

May-16

Nov-12

Nov-13

Nov-14

Nov-15

Jul-15

Jul-16

Feb-13

Apr-13

Jul-13

Feb-14

Apr-14

Jul-14

Feb-15

Apr-15

Feb-16

Apr-16

Sep-12

Sep-13

Sep-14

Sep-15

Mar-13

Mar-14

Mar-15

Mar-16

Jan-13

Jan-14

Jan-15

Jan-16

BYDHK

6Table 6: Valuation Valuation

Valuation

Estimated

Weights In order to estimate the share price of the BYDHK, we mainly used the following two valuation

Price

methods: a 5 years DCF and a Relative Multiples Valuation (Table 6).

DCF(CNY) 63.06 50.00% DCF Model

The DCF method is the discounted value of the free cash flow based on the predicted financial

P/E(CNY) 35.12 16.67%

statements, discounting to estimate the intrinsic value of BYDHK stocks. With the diversity of

P/B(CNY) 79.05 16.66%

BYDHK business and its stock ownership, we predicted the financial situation of BYD-E (HC&AS)

and remaining parts except for the mobile phone business (AB, RB&PB) five years after. We

EV/EBITDA(CNY) 25.77 16.67% calculated the free cash flow and equity value of two sections respectively, then added the stock

value of Holitech held by BYDHK, finally got the stock price by dividing the fully diluted shares

Target Price(CNY) 54.86 outstanding. According to the detailed analysis above, the target price is expected to be HKD74.60

(Table 7).

Target Price(HKD) 64.89

The base case for this model was formulated considering about BYDHK’s historical performance,

Source: Team Calculations our evaluations of industry outlook and its competitive positioning, and revenue growth among

businesses. The DCF is most sensitive to the following inputs, the derivations of which are

explained below:

Table 7: The DCF Model • Weighted Average Cost of Capital(WACC)

To better estimate the value, we calculated the WACC and cost of equity of HC&AS, and other

The DCF Model businesses (AB and RB&PB) respectively to reflect the cost and risk of each business. The revenue

BYD-E

Remaining

Buisinesses

Holitech of HC&AS (95.03% in 2016 interim report) mostly comes from its holding company: BYD-E. We

utilized two methods (CAPM and APT) to estimate the cost of equity (Appendix 9). For the CAPM,

PV of FCF/EV 1,981 247,368 17,561

we ran the linear regression of BYDHK’s stock yield against the HSCI for two time intervals(5-year

Less Net Debt 10,566 67,897 / monthly and 3-year weekly) and then averaged to calculate Beta (Appendix 8). And the Beta for the

Less Minority remaining businesses was calculated through comparable companies methodology, and then

Interest / 3,989 /

weighted it according to the operating revenue in 2015 (Appendix 10). The risk-free rate was based

Proportion of

Shares 65.76% 100% 12.59% on 1-year government bonds benchmark yield. The expected market return was the average return

PV of FCF of HSCI over the past ten years. We calculated the cost of debt by weighting and averaging the

Belonging to (5,646) 175,482 2,211 short and long term debt data adopted from 2015 annual report (Table 8) (Appendix 11).

BYDHK

Total EV of 172,047 • Revenue Growth

BYDHK For sales growth rate, we mainly forecast by using the sales of BYDHK's core business, that is the

Financial Data(in Millions) AB, RB&PB, HC&AS. HC&AS’s revenue is represented by BYD-E’s (Figure 27) (Appendix 13).

Fully Diluted

Shares AB: we added the revenue of the four parts together (fuel car excluding fuel SUV, fuel SUV, NEV

2,728

Outstanding excluding pure-electric bus, pure-electric bus) to get the AB’ revenue (Appendix 14).

(CNY) - Sales Volume Forecast: The sales volume of fuel vehicles shows a slow downward trend

Target Price under the condition that SUV sales rise. The NEV sales volume is expected to maintain a

(CNY) 63.06

rapid but stable growth, keeping an estimated annual growth rate of 35.86% of the industry;

Target Price 74.60 sales volume of pure-electric bus is expected to reach 23,747 in 2020 (Figure 24).

(HKD)

- Price Forecast: We used data from the BYDHK’s official website to calculate the average

Source: Team Calculations price of fuel car excluding fuel SUV, fuel SUV, NEV excluding pure-electric bus. Pure-electric

bus price was gotten from team calculations (Appendix 15). Then according to BYDHK’s

annual data of 2015 to adjust to the average price of four classifications, and we finally got

each price (Table 10).

Table 8: WACC Analysis Table 9: Relative Valuation

WACC Analysis Relative Valuation

HC&AS Remaining Businesses EBITDA(CNY in Millions) 11,036

EV from EBITDA(CNY in Millions) 130,330

Risk-free Rate 2.67% 2.67%

Less:Debt(CNY in Millions) 78,895

Beta 1.62 1.16

Plus:Cash and Cash Equivalents(CNY in Millions) 19,323

Market Risk Premium 5.58% 5.58%

Less:Minority Interst(CNY in Millions) 445

Cost of Equity from CAPM 11.73% 9.14%

Market Value(CNY in Millions) 70,312

Cost of Equity from APT 9.27% / Fully Diluted Shares Outstanding (in Millions) 2,728

Pre-tax Cost of Debt 0 4.86% Price from EV/EBITDA(CNY) 25.77

Earnings(CNY in Millions) 5,380

Average Tax Rate 11.91% 16.39%

Price from P/E(CNY) 35.12

Cost of Debt after Tax 0 4.06%

Book Value(CNY in Millions) 60,005

Weight of Equity 100.00% 81.73%

Price from P/B(CNY) 79.05

Weight of Debt 0 18.27%

Average Price(CNY) 46.65

WACC 10.50% 8.21% Average Price(HKD) 55.18

Source: Team Calculations Source: Team Calculations

7Figure 24: Sales Volume of RB&PB: RB welcomes a new round of outbreak because of the development of new energy

BYDHK’s A&B industry, and we have expectations to photovoltaic industry. Based on that, we calculated the

800

cubic equation of sales of RB&PB in line with the future time trend (Figure 25).

600 HC&AS: BYDHK plans to give the whole HC&AS to BYD-E, so we replaced the revenue of

HC&AS with BYD-E future sales forecast. After the regression on many variables, we have found

Thousand

400

that the semi-annual revenue of BYD-E highly fits semi-annual copper production reported by

National Bureau of Statistics of China (NBS), and the R-squared of the quadratic and exponential

200

equations of copper production in six months are very high (Appendix 16). Finally, we got the

0

forecast sales of BYD-E (Figure 26).

2016F 2017F 2018F 2019F 2020F

Pure-electric Bus NEV exculding Pure-electric Bus • Capital Expenditure

Fuel SUV Fuel Car(excluding Fuel SUV) - Due to changes in the business structure, capital expenditures will change significantly in the

Source: Team Calculations next five years: capital expenditures for NEV will increase substantially in order to implement

‘5-4-2 initiative’, to develop NEV and energy storage battery, and to upgrade technology to

Table 10: Price Estimate maintain its leading role; implement “7+4”, launch a variety of new models, realize

industrialization and cover the market.

Price Estimate - HC&AS expanded its production capacity (increased CNC equipment) in 2015; the growth of

(CNY in Thousands)

smartphones is becoming slow, which is not expected to have a greater capital expenditure in

Fuel Car Excluding Fuel SUV 54.58 the future.

Fuel SUV 74.30 • Terminal Growth

Terminal growth is based on the predicted inflation and the growth rate of new energy business.

NEV Excluding Pure-electric Bus 217.31 Considering handset and fuel automobile business have entered a mature business stage, and the

new energy business still has much development space, we predicted the terminal growth is 2.88%,

Pure-electric Bus 1335.07 the sum of the expected inflation rate and the growth rate of new energy.

Relative Valuation

Source: Team Calculations Because of the diversity of BYDHK, it was not easy to find a direct comparison of the company, so

we looked for comparable companies for each business. For the three major businesses of BYDHK,

Figure 25: RB&PB's Sales we looked for companies with a high degree of similarity in business or having a competitive

Revenue relationship in the business, covering Hong Kong, Taiwan, the Chinese Mainland and overseas

18

markets. First we calculated the average relative multiples of each business, then according to each

16

business share of predicted total revenue in 2016 to get the final P/E, P/B and EV/EBITDA, and

14

y = 18023x3 - 130526x2 + 367891x + 4E+06 then calculated them with 2016 forecasted EPS, EBITDA and BVPS to get three different share

12 R² = 0.93658 prices; finally we averaged the three to obtain the price of HKD55.18 (Table 9) (Appendix 12).

10

Million

8 Financial Analysis

6

4

Financial Condition 2013 2014 2015 2016F 2017F 2018F 2019F 2020F

2

0 Profitability

2010 2011 2012 2013 2014 2015 2016F 2017F 2018F 2019F 2020F

Source: Team Estimates Net Profit Maigin 1.56% 1.34% 4.04% 5.15% 6.03% 6.86% 7.57% 8.21%

Gross Margin 13.09% 13.77% 15.28% 17.79% 19.21% 20.69% 22.23% 23.83%

ROE 3.12% 2.56% 8.71% 9.33% 11.47% 13.52% 15.29% 16.86%

Figure 26: HC&AS’s Sales

Revenue ROA 0.99% 0.79% 2.72% 3.40% 4.26% 5.00% 5.64% 6.21%

70

60 Liquidity

50 Current Ratio 0.69 0.77 0.82 0.88 0.85 0.84 0.83 0.83

40

Quick Ratio 0.49 0.58 0.59 0.69 0.65 0.64 0.64 0.64

Million

30

Cash Ratio 0.10 0.07 0.09 0.22 0.20 0.18 0.18 0.17

20

10

Activity

0 Inventory Turnover 5.37 5.07 5.09 5.16 5.43 5.44 5.44 5.42

Accounts Receivable

Turnover 4.31 3.11 3.16 3.43 3.57 3.74 3.74 3.74

Source: Team Estimates Fixed Asset Turnover 1.42 1.49 1.99 2.15 2.31 2.46 2.60 2.74

Total Asset Turnover 0.64 0.59 0.67 0.66 0.71 0.73 0.75 0.76

Figure 27: Revenue Structure Financial Leverage

100% Total Liabilities to Assets 0.68 0.69 0.69 0.64 0.63 0.63 0.63 0.63

90%

33.5% 32.8% 31.7% 30.3% 28.6%

80% 42.4% Interest Coverage 1.76 1.53 3.07 3.80 4.71 5.72 6.43 7.05

70% 7.5%

6.3% 6.5% 6.8% 7.1% Total Liabilities to Equity 2.14 2.25 2.21 1.75 1.69 1.70 1.71 1.71

60% 9.4% 7.3%

7.4% 15.2% 11.9%

50% 19.2% Equity Multiplier 3.14 3.25 3.21 2.75 2.69 2.70 2.71 2.71

40% 25.7%

30%

Long-term Debt to Equity 0.35 0.38 0.31 0.17 0.13 0.09 0.06 0.05

20% 49.6% 53.2% 56.6%

41.1% 45.6% Long-term Debt to Assets 0.11 0.12 0.10 0.06 0.05 0.03 0.02 0.02

10%

24.4%

0% Shareholder Ratio

2015 2016F 2017F 2018F 2019F 2020F

NEV Fuel Car RB&PB HC&AS EPS (CNY) 0.23 0.18 1.12 1.75 2.48 3.42 4.61 6.16

Source: Company Data,Team Estimates Source: Company Data,Team Calculations

8Figure 28: Gross Margin Optimization of Business Structure Contributed by NEV's Sales Growth

Combined with the revenue structure in 1H16 (Figure 4) and BYDHK’s prospects, we estimate that

NEV will be the main force of the company’s revenue in the future. Due to the turnaround of

photovoltaic industry, RB&PB in BYDHK is expected to recover sluggishly. At the same time, the

market growth of smartphones and computers tends to saturation, and the HC&AS’s contribution to

total revenue is decelerating (Figure 27). The company will gradually form a new revenue model

dominated by NEV to create greater margins, which will increasingly bring more benefits to

shareholders than before.

Upgrading of Industrial Structure Conducive to Cost Savings

In the future, the revenue of BYDHK will increasingly rely on NEV. We expected that the gross profit

Source: Company Data, of BYDHK will be efficiently promoted (Figure 28), due to: 1) continuously increasing NEV sales

Team Calculations revenue, as the main source of revenue, will enlarge the company’s economies of scale and reduce

the unit cost (Figure 20). 2) BYDHK’s layout in NEV industry chain will decrease intermediate costs

Figure 29: Liabilities Structure substantially under the new revenue model.

100%

90% Capital Structure Optimized with Solvency Promoted

80%

70%

BYDHK’s long-term debts have an obvious drop with discharging a great deal of maturing debts in

60% 2015 and 2016. The company has financed RMB14.4 billion by private placement in July, 2016, and

50% to some extent, improved the structure of debt-equity. It is believed that the company will have less

40% debt burden in the long run implying long-term debts to assets decreasing with the continuous

30%

20%

increase in margin. And, the drop of debt burden significantly leads to the decline of financial cost,

10% which creates a favorable impact on net profit margin (Appendix 5). In addition, current liabilities will

0% account for more portion of total liabilities due to repayment of a large number of long-term debts

2014 2015 2016F 2017F 2018F 2019F 2020F

Current Liabilities Non-current Liabilites (Figure 29).

Source: Company Data, The Influence of NEV Market and Operating Capacity Keeping Rising

Team Calculations We estimate that BYDHK will keep the leading position in the future NEV market based on its

advanced industrial layout and leading-edge technology (Figure 20). Relying on the rapid

development of NEV market, the sales of BYDHK seems very optimistic. The rapid growth in sales

Figure 30: Total Asset&Fixed volume will effectively promote the inventory turnover and accounts receivable turnover speed,

Asset Turnover which can shorten the operating cycle (Appendix 6). It will also improve the liquidity of assets

3.00 (Figure 30)and make the utilization of assets more efficient, increasing the ROA level obviously

2.50 (Appendix 6).

2.00

Strong Operating Cash Flow Facilitating Reinvestment

1.50 The newly equity financing increased the capital strength of BYDHK and provided security

1.00 guarantee for capital expenditure and investment. We estimate BYDHK will increase investment in

0.50

the future, focusing on NEV and energy battery program (Figure 31). The growth of net profit mainly

benefited from NEV program will generate more and more operating cash inflow which will be used

0.00

2014 2015 2016F 2017F 2018F 2019F 2020F into reinvestment. Under the support of strong operating cash inflow and stable financial pattern, we

Total Asset Turnover Fixed Asses Turnover estimate the cash flow obtained by financial activities is stable (Appendix 3).

Source: Company Data,

Team Calculations DuPont Analysis

For the reason of rapid growth of the NEV sales volume, BYDHK’s net profit will obviously ascend

driven by uprating business structure. We forecast the ROE will increase, that of 2020 doubling

Figure 31: Reinvestment Ratio

more than that of 2015. Simultaneously, the rapid growth of revenue will promote asset turnover

efficiently better than 2015 and have a slow rise. Besides, thanks to the recent debt repayment,

equity financing and promising revenue growth, the company will maintain a stable financial pattern,

which means the total debt to equity will make a minor effect on ROE (Appendix 31).

Dividend Payment and EPS Analysis

We predict that BYDHK will not distribute dividend to shareholders and remain the present shares

outstanding in the next five years since its rare dividend payment in the past and the large

requirement of capital for investment in NEV industry. Shareholders will benefit from the continuous

rise in EPS whose rapid growth relies on the net profit mainly generated by increasing revenue and

gross profit (especially by NEV) (Figure 32).

Source: Company Data,

Team Calculations ROE Decomposition

2013 2014 2015 2016F 2017F 2018F 2019F 2020F

Figure 32: EPS (in CNY)

ROE 3.12% 2.56% 8.71% 9.33% 11.47% 13.52% 15.29% 16.86%

Net Profit Magin 1.56% 1.34% 4.04% 5.15% 6.03% 6.86% 7.57% 8.21%

Total Asset Turnover 0.64 0.59 0.67 0.66 0.71 0.73 0.75 0.76

Equity Multiplier 3.14 3.25 3.21 2.75 2.69 2.70 2.71 2.71

Source: Company Data, Source: Company Data,Team Calculations

Team Calculations

9Figure 33: Risk Matrix Investment Risk

Regulatory Risk

• Reduction of Government Subsidies and Shrink of Profit Margins (R1) / (High

Likelihood, High Impact)

- NEV: As the government subsidies for PHEV with a range of 100 to 150 kilometers reduced

from RMB31,500 to RMB25,000 per vehicle to 2020, the profitability of new energy business

would be shrinking (Appendix 17).

- Photovoltaic: Decline in subsidies for electricity prices due to the electricity market reform,

which weakens BYDHK’s profitability and financing ability and make it more difficult for the

construction and operation of photovoltaic power plants. In 2016, the electricity price of Class

I, Class II resource were reduced by RMB0.1 and RMB0.07 per kwh respectively and Class

III resource was decreased by RMB0.02 per kwh (Appendix 18).

Source: Team Analysis

Market Risk

Table 11: Mitigation

• Slowdown of China's Economic Growth (M1) / (High Likelihood, Moderate Impact)

Risks Mitigating Factors The slowdown of china’s economic growth leads to a serious overcapacity problem. The GDP

Regulatory risk growth rate of China has continued to decline (Figure 11). Since 2011, the GDP growth rate of

China has continued to decline. In 2012, the GDP growth rate has dropped below 8% while that

Government Rising sales of NEV, subsidies

barrier and technological in 2015 went down to 6.9% for the first time in nearly 30 years. The profitability and growth

Subsidies(R1)

innovation. capability of enterprises have been greatly restricted.

Market risks

The new energy market is • Foreign Exchange Risk (M2) / (High Likelihood, High Impact)

Slowdown of China's BYDHK's foreign exchange risk mainly exists in foreign business income, international

Economic during a period of

Growth(M1) development; the growth of procurement and assembly service business. We expect a rising trend of the exchange rate of

consumption maintains robust

HKD against RMB as a result of a continuous rise of exchange rate (HKD against RMB) since

Foreign Exchange Using financial tools to hedge December 2015. According to sensitivity analysis, the increase in exchange rate (HKD against

Risk(M2) foreign exchange risks RMB) by 2% will result in a target price drop from HKD64.89 to HKD63.73 (Table 12).

Absolute cost advantage; long-

Decline in Oil

Prices(M3)

term trends in new energy • Decline in Oil Prices (M3) / (Moderate Likelihood, Low Impact)

industry.

The decline in oil prices and its long-term maintenance will dampen consumers’ enthusiasm of

1.Huge demand;2.Competition buying NEV. It will benefit traditional fuel cars and restrain the demand for new energy cars in

impels improvement and the short term.

Unstable Market innovation; subsidies barrier;

Demand(M5) industry chain integration;

3.Structural optimum of mobile • Unstable Market Demand (M4) / (Moderate Likelihood, High Impact)

business

- Lack of charging pile: As of the end of 2015, China's NEV to its charging pile ratio is more

Operate risks

than 10:1, which severely inhibited its market demand.

Higher decision making

Corporate efficiency; Solidified cohesion - Consumers buy electric cars for policy incentives rather than their car needs.According to

Governance and enhanced competitiveness statistic, only 5% of the people purchase NEV out of their car requirements (Appendix 19).

Risk(O1) owing to the 2015 employee’s

stock ownership plan. - According to statistics, there are 64% of quality complaints of pure-electric vehicle with regard

RMB4 billion repaid the loans, to battery, and 36% of quality complaints of PHEV concerning engine.

Financial Risk(O2)

optimized the capital structure.

- Market competition intensifies. 1) AB: an increasing number of potential entrants in new

Low Consumer The cooperation with Center energy market. 2) HC&AS: oversupplied mobile phone casing and intensifying competition

Satisfaction(O3) Art will improve vehicle design

and enhance the brand image. among metal casing suppliers lead to a price fall of phone casing. The profit margin shrinks.

The industry chain integration According to sensitivity analysis, if the total sales sales volume of NEV changes from 131,300

Cost Control(O4)

reduced the cost. below to 122421, our recommendation will change from buy to hold while further drop to 78,559

for a sell recommendation (Table 12).

Source: Team Analysis

Operational Risks

Table 12: Sensitivity Analysis

• Corporate Governance Risk (O1) / (Moderate Likelihood, Moderate Impact)

̴ Base Case Buy Sell

Both the position of chairman and the general manager are the real controllers of the company

The Exchange Rate

0.8454 0.8889 1.2673 —Wang Chuanfu. The structure of centralized management will cause an opaque information

of HKD to RMB

problem and may endanger the company into a latent operational risk.

Ratio of Cost to

81.61% 83.44% 94.06%

Income • Financial Risk (O2) / (Moderate Likelihood, Moderate Impact)

Sales Volume of In Debt Maturity Structure҅short-term debt is mainly considered in the debt financing. With high

NEV Excluding 118000 128001 56345

Pure-electric Bus ratio of short-term debt is destabilizing the use of capital. In general, financial leverage is

Sales Volume of

12000 9106 /

decreasing, while still in the relatively high level.

Pure-electric Bus

Total Sales Volume • Low Consumer Satisfaction (O3) / (High Likelihood, High Impact)

131300 122421 78559

of NEV BYDHK's sloppy design and excessive imitation of the appearance fail to meet consumers’

Source: Team Analysis demands and preference for original design. Besides, a bunch of after-service complaints

revealed due to technical constraints and deficiency in ideology of after-service.

Table13: Rating Guide • Cost Control (O4) / (Low Likelihood, High Impact)

buy hold sold The adjustment of subsidies makes BYDHK face the risks of cost increasing and profit margins

bigger than range from -15% to smaller than

declining. According to the sensitivity analysis, if the proportion of sales cost against revenue

15% 15% 15% rises 2%, our target price will drop from HKD64.89 to HKD62.40 (Table 12).

10Appendices

Appendix 1: Statement of Comprehensive Financial Position (BYDHK)

CNY in Million 2013 2014 2015 2016F 2017F 2018F 2019F 2020F

Assets

Cash & Cash Equivalents 4,511 3,950 6,011 19,323 19,032 21,197 24,994 30,505

Derivative Financial Instruments - - 18 25 31 37 46 58

Short-term Deposits 200 139 269 274 279 285 291 297

Accounts & Bills Receivables 13,135 22,435 26,679 32,478 35,291 42,639 52,063 64,179

Other Receivables 2,676 3,900 5,419 7,290 8,750 10,666 13,170 16,443

Inventories 8,776 10,046 15,807 16,556 19,412 23,033 27,613 33,412

Other Current Assets 668 364 317 323 329 336 343 350

Current Assets 29,966 40,834 54,519 76,270 83,124 98,193 118,520 145,245

PP&E-net 34,935 37,213 39,039 47,120 52,373 59,170 67,956 79,333

Equity Capital Investment 1,084 1,414 1,889 1,795 2,079 2,456 2,952 3,605

Available-for-sale Financial Assets 9 35 3,071 3,071 3,070 3,070 3,070 3,069

Goodwill and Intangible Assets 4,995 6,373 7,169 11,006 13,232 16,179 20,064 25,178

Prepaid Land Lease Payments 4,628 4,448 4,656 7,907 9,305 11,126 13,482 16,524

Other Non-current Assets 2,398 3,692 5,143 6,571 7,806 9,396 11,442 14,081

Non-current Assets 48,049 53,175 60,967 77,470 87,865 101,397 118,967 141,790

Total Assets 78,015 94,009 115,486 153,740 170,989 199,590 237,487 287,035

Liabilities

Trade and Bills Payables 22,293 25,851 30,656 41,904 49,169 58,408 70,120 84,976

Tax Payable 166 143 289 399 475 570 692 846

Interest-bearing Bank and Other Borrowings 16,172 19,173 26,413 32,223 33,892 41,346 51,171 63,804

Other Current Liabilities 4,713 7,856 8,752 11,676 13,809 16,571 20,135 24,736

Current Liabilities 43,344 53,022 66,110 86,201 97,345 116,895 142,118 174,363

Interest-bearing Bank and Other Borrowings 8,652 10,979 11,230 9,469 7,985 6,733 5,677 4,787

Other Non-current Liabilities 1,162 1,113 2,116 2,116 2,116 2,116 2,116 2,116

Non-current Liabilities 9,814 12,092 13,346 11,586 10,101 8,849 7,794 6,903

Total Liabilities 53,158 65,114 79,457 97,787 107,446 125,745 149,912 181,266

Equity

Equity Attributable to Owners of the Parent 21,710 25,366 32,294 51,964 59,281 69,293 82,713 100,575

Share Capital 2,354 2,476 2,476 2,728 2,728 2,728 2,728 2,728

Reserves 19,238 22,890 26,618 46,036 53,353 63,365 76,784 94,647

Proposed Final Dividend 118 - - - - - - -

Perpetual Loans - - 3,200 3,200 3,200 3,200 3,200 3,200

Non-controlling Interests 3,147 3,529 3,735 3,989 4,261 4,552 4,862 5,194

Total Equity 24,856 28,894 36,029 55,953 63,543 73,845 87,575 105,769

Total Liabilities and Equity 78,015 94,009 115,486 153,740 170,989 199,590 237,487 287,035

Predicted Statement of Comprehensive Financial Position is summarized by Statement of Financial Position of HC&AS (Equals to BYD-E

(0285.HK)) and Remaining Businesses (AB, RB&PB).

11HC&AS (Equals to BYD-E) Remaining Businesses

CNY in Million 2016F 2017F 2018F 2019F 2020F 2016F 2017F 2018F 2019F 2020F

Assets

Cash & Cash Equivalents 1,296 2,210 2,759 3,652 4,990 18,027 16,822 18,438 21,342 25,515

Derivative Financial Instruments - - - - - 25 31 37 46 58

Short-term Deposits 274 279 285 291 297 - - - - -

Accounts & Bills Receivables 8,542 9,226 10,735 12,463 14,446 23,936 26,065 31,904 39,600 49,734

Other Receivables 628 732 851 987 1,143 6,662 8,019 9,815 12,183 15,300

Inventories 4,246 4,925 5,695 6,570 7,567 12,310 14,487 17,338 21,043 25,845

Other Current Assets 1 1 1 1 1 322 328 335 342 349

Current Assets 14,987 17,374 20,326 23,964 28,443 61,283 65,750 77,867 94,556 116,801

PP&E-net 7,043 7,916 8,912 10,052 11,361 40,077 44,457 50,258 57,904 67,972

Equity Capital Investment 400 400 400 400 400 1,395 1,679 2,056 2,552 3,205

Available-for-sale Financial Assets - - - - - 3,071 3,070 3,070 3,070 3,069

Goodwill and Intangible Assets 23 27 31 36 42 10,983 13,205 16,148 20,028 25,136

Prepaid Land Lease Payments 359 416 481 555 639 7,548 8,889 10,645 12,928 15,885

Other Non-current Assets 722 842 979 1,137 1,320 5,849 6,964 8,417 10,305 12,761

Non-current Assets 8,547 9,600 10,803 12,181 13,762 68,923 78,265 90,594 106,786 128,028

Total Assets 23,534 26,974 31,129 36,145 42,205 130,206 144,015 168,461 201,342 244,830

Liabilities

Trade and Bills Payables 9,953 11,545 13,350 15,401 17,738 31,950 37,624 45,058 54,720 67,239

Tax Payable 149 174 202 235 272 250 301 368 457 574

Interest-bearing Bank and Other Borrowings - - - - - 32,223 33,892 41,346 51,171 63,804

Other Current Liabilities 1,760 2,037 2,351 2,708 3,114 9,915 11,772 14,220 17,427 21,622

Current Liabilities 11,862 13,756 15,903 18,344 21,124 74,339 83,589 100,992 123,775 153,238

Interest-bearing Bank and Other Borrowings - - - - - 9,469 7,985 6,733 5,677 4,787

Other Non-current Liabilities - - - - - 2,116 2,116 2,116 2,116 2,116

Non-current Liabilities - - - - - 11,586 10,101 8,849 7,794 6,903

Total Liabilities 11,862 13,756 15,903 18,344 21,124 85,924 93,690 109,841 131,568 160,142

Equity

Equity Attributable to Owners of the 11,672 13,217 15,225 17,801 21,081 44,345 50,116 58,120 68,964 83,547

Parent

Share Capital 4,052 4,052 4,052 4,052 4,052 2,728 2,728 2,728 2,728 2,728

Reserves 7,619 9,165 11,173 13,749 17,029 38,417 44,188 52,192 63,036 77,619

Proposed Final Dividend - - - - - - - - - -

Perpetual Loans - - - - - 3,200 3,200 3,200 3,200 3,200

Non-controlling Interests - - - - - 44,345 50,116 58,120 68,964 83,547

Total Equity 11,672 13,217 15,225 17,801 21,081 48,334 54,378 62,672 73,826 88,740

12You can also read