Coca-Cola Hellenic Field trip presentations - Dimitris Lois, CEO

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Coca-Cola Hellenic

Field trip presentations

Dimitris Lois, CEO

Forward-looking statements Unless otherwise indicated, the condensed consolidated financial statements and the financial and operating data or other information included herein relate to Coca-Cola HBC AG and its subsidiaries (‚Coca-Cola HBC‛ or the ‚Company‛ or ‚we‛ or the ‚Group‛). This document contains forward-looking statements that involve risks and uncertainties. These statements may generally, but not always, be identified by the use of words such as ‚believe‛, ‚outlook‛, ‚guidance‛, ‚intend‛, ‚expect‛, ‚anticipate‛, ‚plan‛, ‚target‛ and similar expressions to identify forward-looking statements. All statements other than statements of historical facts, including, among others, statements regarding our future financial position and results, our outlook for 2014 and future years, business strategy and the effects of the global economic slowdown, the impact of the sovereign debt crisis, currency volatility, our recent acquisitions, and restructuring initiatives on our business and financial condition, our future dealings with The Coca-Cola Company, budgets, projected levels of consumption and production, projected raw material and other costs, estimates of capital expenditure, free cash flow, effective tax rates and plans and objectives of management for future operations, are forward-looking statements. You should not place undue reliance on such forward-looking statements. By their nature, forward-looking statements involve risk and uncertainty because they reflect our current expectations and assumptions as to future events and circumstances that may not prove accurate. Our actual results and events could differ materially from those anticipated in the forward-looking statements for many reasons, including the risks described in the UK Annual Financial Report and the annual report on Form 20-F filed with the U.S. Securities and Exchange Commission (File No 1-35891) for Coca-Cola HBC AG and its subsidiaries for the year ended 31 December 2013. Although we believe that, as of the date of this document, the expectations reflected in the forward-looking statements are reasonable, we cannot assure you that our future results, level of activity, performance or achievements will meet these expectations. Moreover, neither we, nor our directors, employees, advisors nor any other person assumes responsibility for the accuracy and completeness of the forward-looking statements. After the date of the condensed consolidated financial statements included in this document, unless we are required by law or the rules of the UK Financial Conduct Authority to update these forward-looking statements, we will not necessarily update any of these forward-looking statements to conform them either to actual results or to changes in our expectations.

Italy is important to the Group

Significant part of the Group

Group Italy

GDP per capita GDP per capita

12,800 US$ 31,100 US$

Population Population1

Share in

585m revenue 56m

Plants Plants2

68 5

NARTD volume3

2,354m u.c.

1 Excludes Sicily

2 Three sparkling beverages plants and two water plants

3 Source: Canadean

4

Growing the top line

660

584

• Increasing sparkling 2013 Total sparkling category servings

per capita

beverages consumption

within NARTD 321

353

280 288 298

• Growing value share in 166

204 209 219

water, tea and juice 93

134 142

47

• Working with customers to

increase availability and

United States

Italy

Mexico

Romania

Bulgaria

Switzerland

Nigeria

Russia

France

Spain

Europe average

Great Britain

Coca-Cola HBC

Poland

Ukraine

value creation

Per capita consumption: Average number of 237ml or 8oz servings consumed per person per year in a specific market.

Coca-Cola Hellenic’s per capita consumption is calculated by multiplying our unit case volume by 24 and dividing by the population.

Source: The Coca-Cola Company, 2013 data

5

Growing the bottom line

• Business impacted by the Eurozone

crisis

– c.40% EBIT decline in the last four

years

• Significant restructuring of the

manufacturing base

– Consolidation of plants

• Reduction in operating expenses

– Taking out fixed operating expenses

• Further opportunities in warehousing,

logistics and route-to-market

6

Executing strategy in Italy

Winning in the market

• Combine demand creation and

demand delivery

– Brand investment

– Joint initiatives with customers

– Execution in the market

• Strong leadership position in

sparkling beverages

– Room for further growth,

particularly in flavours

• Low share in still drinks

– Grow value profitably and

sustainably

8

Growing revenue ahead of volume

• Occasion-based brand, price,

package, channel (OBPPC)

strategy

– Growing single-serve multi-packs

in the modern trade

– Increasing presence in the

immediate consumption channel

– Making products relevant to the

consumer

– Addressing affordability

9

Taking cost out

• Optimising infrastructure

– Reducing the number of plants

from five to three

• Centralising IT and procurement

• SAP Wave

• Shared Services Centre

• More to come

– Outsourcing of warehousing

– Phase 2 of deployment to Shared

Services Centre

10Generating cash

• Sharp focus on working capital

management

• 40% of cash-flow from operations

channeled into revenue-generating

investment

• Cold drink equipment

• Modernising production

11Five elements of strategy in Italy

Sparkling is our top priority Driving profitable

volume in still drinks

OBPPC, Customers’ profitability, Execution

Tight control Optimising Working capital

of expenses infrastructure management

12Agenda

Dimitris Lois Italy in the context of the Group

Jenny Stoichkova, Coca-Cola Italy Italy: Opportunity to grow

Sotiris Yannopoulos

and Enrico Galasso Capturing the opportunity in Italy

Dimitris Lois Closing remarks

Q&A

13Italy: Opportunity to grow

Evguenia Stoichkova

Operations Director TCCCRecovering confidence: Priority for Italy

Germany UK France Spain Italy

92 99

88 90 95

87 87 88 87 87 87

86 92 84

90 90

79 79

77 77

75 75

72 73

71

67 69

61 61 61 61 61

60 58 59

56 55 56

54 53

57 50 52 52 51

55 48 48

52 53 46 47

47 44 45

49

44 41

45 46

41 39

Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014

Source: Nielsen Consumer Confidence Research 15Job security is the biggest concern

Job security 30 11

The economy 13 12

Italy - Unemployment Rate (%)

12.4

12.1 Debt 9 7

Increasing utility bills

5 11

(electricity, gas, heating, etc)

10.7

Health 5 10

Biggest concern

Childrens' education and/or welfare 6 8

8.4 8.5

Second biggest

7.8 Political stability 5 9

concern

7.7 Work/life balance 5 7

6.8 Increasing food prices 4 6

6.7

6.1 Crime 3 5

No concerns 2

Source: Nielsen Business Indicators; Nielsen Global Consumer Confidence 16Consumption behaviour is

deeply impacted by the crisis

There are signs of recovery in 2013 – more

savings & holidays – even though spending

is still decreasing for many categories. In

Italy crisis has changed purchase behaviours

more than in other EU countries

Compared to this time last year, have you changed your

spending to save on household expenses?

Nielsen Consumer Confidence 17As well as shopping behaviour

63% (+4 pp vs ‘12) have a strict

budget and buy only what they need

86% (=) prepare a

shopping list before the trip

45% (+2 pp vs ‘12) usually

purchase only what they planned

Source: Nielsen shopper trends 18Key Italy insights

1. In the last four years Italy has had the lowest consumer confidence index among

the big western European countries

Country

2. Job security is the biggest concern for Italians, as unemployment doubled since

2007

3. As a reaction to uncertainty, Italians modified consumption behavior more than

other Europeans , down-trading (more discounters) and down-grading (more

private label)

4. There are however signs of recovery: in 2013, a growing number of Italians are

able to save money. These trends are expected to continue in the coming years.

TCCC

1. Italy has the highest Coke Brand Love (5.6) in Europe

2. Number 2 in Europe in % of households buying Coke classic on an annual basis

3. Italy shows low % of people that reject / never tried the Sparkling category

4. Coke Regular is the most preferred NARTD brand for 50% of Italians

NARTD: Non Alcoholic Ready To Drink Beverages 19The Italian NARTD market landscape

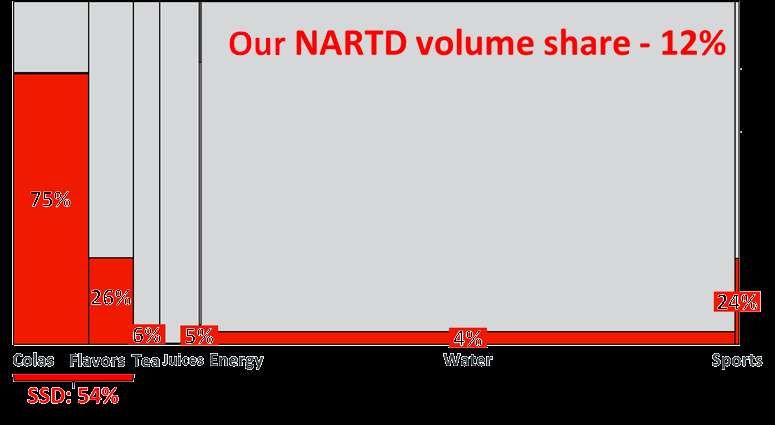

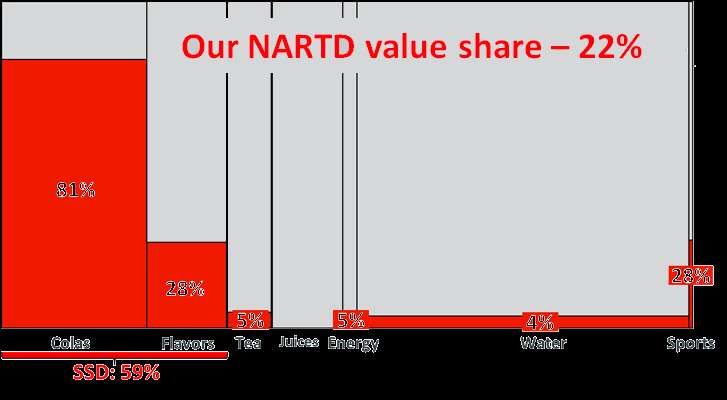

NARTD Volume (2,354m u.c.) Retail Value (14,891m €)

6

258 168

129 13

85 SSD Colas

164 SSD Colas

225

SSD Flavours 960 1753 2924 SSD Flavours

Water Water

RTD Teas 2022 RTD Teas

Juices Juices

1732 Energy 6806 Energy

Sport Sport

Source: 2013 Internal estimates based on Canadean and Red Book – CCH territory only 20We have a strong position

in a small portion of the market

Source: Internal estimates based on Canadean and Red Book ” CCH territory only 21Capturing more value Source: Internal estimates based on Canadean and Red Book ” CCH territory only 22

New trends - Mindset

HEALTH & BEAUTY INNOVATION & GREEN INTERNET

“ 57% of Italians feel QUALITY “ 42% consider buying “ 38.9m had access to the

green/low impact Internet in 2012 (+7.8%)

overweight “ 56% do not withdraw products

from quality and are

“ +40% penetration of

“ 46% are trying to lose willing to pay more for it

“ 24% bought more green smartphones

weight (fitness & diet) products than in the

“ 39% love trying new past “ 26M consider

brands and new products Internet as the main source of

“ 26% are keen to pay a information

premium for organic,

23% low-impact and “ 21M read opinions of other

fair-trade products consumers about products

and services

Source: Nielsen shopper trends 23Expected development of the Italian

beverage landscape

• Italy is the 2nd country worldwide in terms of ageing population; this will drive

still beverages volume growth

• In the short term, decreasing Disposable Income (index 88 in 2014 vs. 2008 )

will further impact high value NARTD categories

• Growing health and wellness concerns will favour still beverages and especially

infused RTD Tea which in Italy is perceived as one of the healthier drinks

SSD ’14-’20 +8 servings per

+20m u.c. capita vs today

NARTD ’14-’20

+80m u.c.

Still ’14-’20 Water ’14-’20

+60m u.c. +55m u.c.

24How we plan to capture

these opportunities

Grow Sparkling per capita Gain share in Still Beverages

(Italy per cap is 91 vs EU average of 141)1 (currently 4%)

1. Consumption with food @ home is

#1 occasion (39% of total beverage

consumption) and TCCC share is 7% 1. Become a significant player in water

2. Socialising out of home is #3 and improve the profitability

occasion (13% of total beverage 2. Re-launch RTD Tea business to

consumption) and TCCC share is 9% become a strong #3 player in

3. Category permissibility with volume and #2 in value

shoppers is the entry point to 3. Create a dedicated business model

improve incidence and frequency to drive volume and value in small

4. Leverage portfolio of brands to profitable categories and innovation

maximise user base (adults aged 30-

49 are 31% of Italian population)

1 Consumption per capita per annum of TCCC sparkling soft drinks 25Our success comes when we have

LOVED FROM A TRUSTED IN A RELEVANT

BRANDS COMPANY CATEGORY

26Entrenched in Italian society

Reasons to Believe Sharing the passion for football Own the summer:

Crazy for Good Say it with Coke and a song

Leverage our Flavours sparkling portfolio to gain new consumers Restart advertising behind Lilia

27And the ‘At Home with Food’ occasion

Family Couple Friends

Point of Sale Activations Extrinsic POS Visuals Intrinsic POS Visuals

POS: Point of sale 28With dedicated programmes

for Coke Zero & Light…

Double-digit growth Targeting women

through recruitment with fashion

Coke Regular, Coke Zero & Coke Light Execution

Coke TM Asset in-store activation

29Ensuring Category Acceptance

4 Commitments of Coca-Cola with Italians

SMALLER PACKS MORE CHOICE FOR EVERY WE ENCOURAGE THE PASSION IN

FOR EVERYONE LIFESTYLE SPORT. SINCE ALWAYS.

INFORMATION FRONT OF PACK and responsible communication policy

30From a trusted company

Participation in EXPO to support the Coca-Cola Cup promotes active healthy

Refresh 2020 commitments lifestyle in Italian schools

2,806 schools

330,000 students

Supporting local communities and the

Commitment to the environment

economy

Package

innovation Coca-Cola

has an

Decreasing our

Italian Heart

footprint yoy

31Our enablers

• Joint scorecard

•Aligned System • Monthly review between country teams

vision

• Quarterly review with Regional Teams / BU

• Increased marketing

investment

•Up to date and

relevant marketing • TCCC: Demand Creation

approach

• CCH: Demand Delivery

32Capturing the opportunity

Sotiris Yannopoulos

General Manager, ItalyOur reference point

is our Strategic Framework

34Based on that we

have a clear Job Ticket for Italy

Grow Per Capita & Share

while defending profit

1 2 3

GET BACK TO GROWTH TAKE CHARGE WIN TOGETHER

Create Demand with: Deliver Demand with: Increase Productivity with:

• Permissibility • Best-In-Class Execution • Governance & Control

• Relevance • Customer Service • Engaged Talent

35Get back to growth

Get Back to Growth elements

Drive per capita consumption and share of MyCoke

Sparkling

Beverages

Grow market share in SSD premium flavours

Revamp Water business profitably

Still

Beverages

Claim our fair share position in RTD Tea

37We have a strong

market share position in SSDs

+5.3pts

CAGR ‘08-’13 CAGR ‘08-’13

38

Source: Internal estimates based on CANADEAN & Market SizesGrowth drivers for SSDs

•70% of beverages consumption is water (2nd highest in Europe)

• Low SSDs per capita despite highest brand love

• SSDs are more profitable than Water for retailers

• 39% of beverages consumption is with meals

- MyCoke share with meals is only 7%

• Socialising Out of Home is the #3 occasion with 13% of consumption

” My Coke share in socialising is only 9%

• Italian population is ageing

• Adult Flavours (tonic, lemonades, bitter) are the only growing segments

Source: TCCC syndicated researches

39Creating Demand

with focused initiatives

REFRESH 2020 MEALS ASSET EXPLOITATION

COCA-COLA CUP SOCIALISING

Enabled with a focused and segmented OBPPC strategy

OBPPC: Occasion-Brand-Pack-Price-Channel

40Our OBPPC supports our

strategy to increase consumption

Meets all shopper needs Implementation

and creates value The right pack, in the right zone

Modern Trade: the right sizes & recommended

INCIDENCE ZONE

prices to meet all shopper needs and basket types 1. Dairy NEW

+1

All prices are RECOMMENDED.Pricing decision are at sole discretion of the retailer

zone

Vs py

2. Water Section

RSP €/lt 3. Check-out&cooler

1L 0.50L

4. Bakery

Entry Pet 1L 1.25 € 1.25/lt

FREQUENCY ZONE

Pet 1.75L 1.89 € 1.08/lt 1. Cheese&Cold Cuts (Counter)

2. Ready Meals

Frequency

3. Fruit & Vegetables

Can 0.33x6 3.49 € 1.76/lt 4. Pasta 1.75L 6x0.33L

UPSIZE ZONE

Pet 1.5L x 2 3.19 € 1.06/lt

1. Promotional Main Hall

Upsize 2. Promotional Area

Pet 1.5L x 4 5.99 € 0.99/lt 2x1.5L 4x1.5L

UPSCALE ZONE +1

Pet 0.5L x 4 3.65 € 1.82/lt 1. Cookies&Snacks

zone

Vs py

2. Juices for Minican

Upscale 3. Check-out

Can 0.15x12 4.99 € 2.77/lt 4. Spirits NEW 12x0.15L 4x0.5L

41Delivering demand

in Modern Trade flawlessly

• Extra Displays: right packs in • Permanent COMBO deals • Coke Regular, Zero & Light in-

the right zones store activation

Modern Trade key pillars

• Co-marketing with food

•Claims & POS materials • Big & impactful Extra Displays

• Quarterly Household Penetration, focus Female 30+

KBIs

• Basket Incidence, focus Small Baskets

• Total Volume on Extra-Display

42As well as in Fragmented Trade

• 3-pack strategy activation • Permanent ‚meal‛ solutions • Dedicated Artwork

(quick stop, meals, on the go)

Fragmented Trade key pillars

• Coolers Visibility & Quality

• Glass bottle conversion &

distribution •Dedicated

point of sale materials

(Menu boards, etc)

• Coke incidence with meals

KBIs

• 3-packs & Glass distribution

• Coke incidence in Socializing occasion

43Leveraging our portfolio

to excite teens

New Teens advertising Back to advertising

campaign support

NBA asset exploitation

Local asset exploitation

44Leveraging our portfolio

to win with adults

Brand relevance with Kinley Capitalise Fanta Lemon success

Population is ageing Doubled volume in 2013

consumer Association s worldwide (35 countries)

‘Product of the year’ is a consumer award issued every year by

• •

• Launch of Kinley in 2013 • +6 share points in Lemonades

• Opportunity to more than triple the • +0.2 share points in SSDs

business in five years • Won ‘Product of the Year’ Award

• Advertising support

45Playing to win market share with Flavours

• Dedicated Assets exploitation • NBA Asset exploitation in store • Glass exploitation

in Extra Displays

Demand Delivery key pillars

• Extra Displays with Fanta • Availability and Visibility

• ‘Rainbow’ ED with MyCoke

• Share on Extra-Display

KBIs

• Users base

• Volume Share

46Working with our retailers

• Lower cost of doing business

• Higher EBITDA for the point of sale

Driven by

Premiumness Higher sales rate Value added services

1400€

Margin/pos

+1000€ +900€ +600€ +500€

vs. leading vs. vs. leading

vs. crisps

candies chocolate crisps

Source: DPP Carrefour, BAIN 2013; Internal estimate based on ad-hoc test 47Moving into Water

CAGR CAGR

‘08-’13 ‘08-’13

Source: Internal estimates based on CANADEAN & Market Sizes 48Addressing brand equity, availability

and sustainability in Water

to build and sustain brand equity

to drive distribution with customers

to drive product sustainability

Source: TCCC syndicated researches 49Building a national brand with Lilia

NEW POSITIONING CONTINUOUS MEDIA SUPPORT PACK INNOVATION

‘Lilia, a simple choice that 3.5m € / year - Highest ever Plant Bottle, up to 30% from

matters’ Share of Voice plants

6th biggest investor in the

Water category

LILIA

A SIMPLE CHOICE

THAT MATTERS

50Recovering profit with value and cost

efficiency, while improving execution

• Increased availability • Command better value: • Light Weighting (Best in Class)

(Distribution in Modern Trade Retail sales price index

from 34% to 65%) from 72 to 90 vs. average - Short neck finish

Demand Delivery key pillars

• Highest ever number of points

of sale activated - New Squared Bottle 1.5l

• Focus on single-serve and

HoReCa (0.5 liter in HoReCa is

the most profitable water SKU)

• Zero touch logistics

• Distribution in Modern Trade

KBIs

• Number of points of sale activated

• Single-serve availability in Fragmented Trade

51Ample room for

market share gains in RTD Tea

Our Vol. Share (RTD Tea)

-6.9pts

12.7%

5.8%

2003 2013

RTD Tea Volume Sales (MUC) CAGR RTD Tea Retail Value Sales (M€) CAGR

‘08-’13 1500 ’08-’13

1228

90 92

85 1067

90 960

1000

60

500

30

- 0

2003 2008 2013 2003 2008 2013

52

Source: Internal estimates based on CANADEAN & Market SizesDriving growth in RTD Tea with relevant

taste, brand equity and availability

to build & sustain Brand equity

Brand Leader = Estathé, 7m€ / year

Infused formulas = 40% of volumes and growing

Lemon & Peach flavours = 90% of market

Full distribution and in-store activation

Source: TCCC syndicated researches 53A new and relevant

proposition for Italians

NEW PREMIUM

PRODUCT FORMULATION

POSITIONING

• A sip of freedom • New infused Tea formula

• 5 m€ investment with lemon and peach

54Delivering results

with the right execution

• Increased distribution (Modern • Step up in-store presence • Relevant line-up to meet

Trade target from 45% to 85%) through in-store promotions, shopper & consumer needs

extra-displays, leaflets, trade

Demand Delivery key pillars

kits, point of sale material

(posters, rotairs, etc)

85 85

45 45

WD WD

• Distribution in Modern Trade & Normal Trade

KBIs

• Number of stores activated

55Take charge

Enrico Galasso

National Sales DirectorCreating value for our customers

We are Italy’s #1 Beverage Supplier

Our route-to-market We understand the

fits the Italian trade customer strategies and

landscape tailor our plans for our

Key Accounts to meet

their needs

Our best-in-class

sales force provides our

customers with services

at the point of sale and We have shopper

unparalleled brand insights that drive our

activation OBPPC and plans

JVC: Joint Value Creation; OBPPC: Occasion-Brand-Pack-Price-Channel; RED: Right Execution Daily;

RTM: Route To Market 57Driving customer satisfaction

through Joint Value Creation (JVC)

‘BeverageWorld’ ‘On Shelf Availability’ Top to Top Routines with all

Category reinvention at customers

Up to 440 POS activated in 2014

Out of Stock reduction

Store based action plan

58Step-changed execution

Number of Extra Displays (,000) FC RED Score

RED: Right Execution Daily is our holistic KBI measuring execution excellence

59Italian trade landscape drives

our Route-to-Market strategy

Less concentrated trade vs. rest of Europe with strong regional focus

Weight of Top 3 retailers

• Multifunctional customer teams

Modern Trade

Source:Nielsen 2012

• Strong national and regional customer

management focus

• Multi-level interface with customers

• Tailored Joint Value Creation programs

RTM reflects opportunities of specific Channel structure

Food & Bev Producers sell-in (20 Bn €)

Fragmented Trade

• Direct Sales and Wholesaler

Direct Sales Intermediaries management capabilities in place

18% 57% 16% 8% • Partnership with wholesalers

WHS C&C GDO

• Segmented approach to outlets

coverage and activation

IC Channels (Day Time Bar, Restaurants, etc)

60Excellent

sales and execution capability

• OBPPC and RED

• Sales and negotiation

• Shopper Insights and Category Management

• Revenue Growth Management

• Financial basics

• Project management

61Win together

We work across all areas

to be #1 in cost leadership

SLE (System Line Efficiency) & productivity 2.5pp

Energy cost reduction*

Production network review

Logistics network review

Plant warehouse outsourcing

Customer collaboration & service level (DIFOTAI)

Total inventory days

Forecast accuracy

* Supply Chain cost reduction as % of net sales revenue over three years (2010-2013) 63We have optimised

our supply chain network

Core Core

production production

network network

2012

2014

5 3

PLANTS PLANTS

Opportunities to address High speed What we have executed

- Network complexity of implementation

- 3 plants near the biggest demand areas

- Leverage the size of our plants - No plant under 40 M UC

- Asset utilisation

14 - +10 % on asset utilisation

- Reduce fixed cost months

- New high speed line in Nogara

- High speed line 64Improving competitiveness

and better service to customers

Supply chain cost 1 % NSR Service Level (DIFOTAI 2)

+620bps

-90 bps

18.3% 96.2%

90.0%

17.4%

2010 2013 2010 2013

1 Supply Chain cost: Production Overheads+Warehousing+Distribution+Haulage

2 DIFOTAI: Delivered in full on time accurately invoiced 65Taking full charge

of our operating expenses

Cost leadership

Accountability efficiency

Lean organisation

2.1pp

Standardisation reduction*

Integration

Business knowledge

Discipline

Efficiency

Partnership

Focus on business

* Reduction in operating expenses as a % of net sales revenue over three years (2013 vs. 2010) 66Contributing to our Zero

Working Capital journey

-Product rationalisation

-Forecast accuracy

22% reduction in

working capital

2013 vs. 2010

67Generating significant Cash Flow

To CCHBC Group

from operations

last 3 years 173m€

290m€

0.19 € (60%)

Investments for growth

0.32 €

per UC sold 117m€

0.13 € (40%)

68Becoming a source of good

for the local communities

69Developing internal talent

Fuel leadership pipeline at all Key Positions covered by Key Make our managers talent

layers People (KPe/KPo) builders

• Fast Forward program

• KBIs in country scorecard

• Management trainee program

• Performance Management

• KPe/KPo and IDP

• Talent acquisition program and Development process

completion as incentivised

objective in MBOs for

• Internal promotions • Individual Development Plans

senior leaders

(IDP)

• Our KPe/KPo grew by 21%

• Successors rate to KPo grew by 10%

70Engaged and

values driven people

+12% +6%

70% 67%

58% 61%

2012 2013 2012 2013

71External endorsement

Award for FINANCIAL STRENGTH

World’s largest employer branding online survey

(7,000 respondents aged 16-65; 150 largest companies assessed)

72We are ready to step up

As the external environment gets better

73Closing remarks

Trading conditions Looking ahead

Underlying trading environment

continues to be challenging

First quarter was weak due to

timing of Easter and liquidity Profitable and sustainable

constraints in the market growth through a

combination of economic

recovery and our efforts

Good trading during Easter and

in May, recouping some of the

volume lost in the first quarter

75Q&A

You can also read