Consistency case study: actions supporting Article 2.1c of the Paris Agreement in Colombia

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Climate-consistency of finance flows: iGST case study series

Consistency case study: actions

supporting Article 2.1c of the

Paris Agreement in Colombia

Alejandra Lopez Carbajal, Ximena Rojas Squella

and Charlene Watson

Climate-consistency of finance flows: iGST case study series

Consistency case study: actions

supporting Article 2.1c of the Paris

Agreement in Colombia

Alejandra Lopez-Carbajal, Ximena Rojas-Squella and Charlene Watson

March 2021

© iGST 2021

Cite as: Lopez Carbajal, A., Rojas Squella, X. and Watson, C. (2021) ‘Consistency

case study: actions supporting Article 2.1c of the Paris Agreement in Colombia’.

San Francisco and London: Climate Works Foundation and ODI. Part of ‘Climate-

consistency of finance flows: iGST case study series’.

Download the report

www.independentgst.org

About the iGST initiative and the Finance Working Group

The Independent Global Stocktake (iGST) is a consortium of civil society actors working

together to support the Global Stocktake (GST), the formal process established under the

Paris Agreement to periodically take stock of collective progress toward its long term goals.

The iGST aligns the independent community — from modelers and analysts, to campaigners

and advocates — so we can push together for a robust GST that empowers countries to take

greater climate action. www.independentgst.org

The Finance Working Group (FWG) is an open partnership bringing together expert

perspectives from the global north and south on the progress made towards financing climate

action. Considering the provision of support to developing countries to mitigate and adapt to

climate change and the consistency of finance flows with climate objectives, the FWG aims to

support the UNFCCC GST process as well as independently benchmark the official GST. The

group is co-chaired by Charlene Watson of ODI and Courtnae Bailey of Imperial College

London.

The Finance Working Group (F Finance Working Group (FWG) is an open partnership bringing together expert

perspectives from the global north and south on the progress made towards financing climate action. Considering

the provision of support to developing countries to mitigate and adapt to climate change and the consistency of

finance flows with climate objectives, the FWG aims to support the UNFCCC GST process as well as

independently benchmark the official GST. The group is co-chaired by Charlene Watson of the Overseas

Development Institute and Courtnae Bailey of Imperial College London) is an open partnership bringing together

expert perspectives from the global north and south on the progress made towards financing climate action.

Considering the provision of support to developing countries to mitigate and adapt to climate change and the

consistency of finance flows with climate objectives, the FWG aims to support the UNFCCC GST process as

well as independently benchmark the official GST. The group is co-chaired by Charlene Watson of the Overseas

Development Institute and Courtnae Bailey of Imperial College London

Acknowledgements

The authors would like to thank all of the interviewees and reviewers for their invaluable input,

including Giovanni Pabón, Mariana Rojas, Germán Romero, María Lemos, Maritza Florián,

Santiago Briceño, Angela Rivera, Carolina Figueroa, Diana Barba, Isabel Mantilla, Anibal

Pérez and Carlos Casallas. The authors would also like to thank the Finance Working Group

members for their valuable contributions, in particular the steering group for ‘Climate-

consistency of finance flows: iGST case study series’, including Julia Bingler (ETH), Courtnae

Bailey (Imperial College London) and Stephan Kellenberger (WWF Switzerland), and

reviewers Carolina Aguirre Echeverri, Manuela Ríos (MOFA, Colombia), María Laura Rojas

(Transforma), Camila Cristancho (Transforma), Sarah Colenbrander (ODI), Chavi Meattle

(CPI) and Hannah Roeyer (Climate Works Foundation). The authors are thankful to the

Climate Works Foundation for providing the resources and support to make this case study

possible. All omissions and errors remain the authors’ own.

Climate-consistency of finance flows: iGST case study series

Consistency case study: Colombia March 2021

Contents

Acronyms .................................................................................................................................5

+ Executive summary ............................................................................................................6

+ 1. Why collate country actions supporting Article 2.1c of the

Paris Agreement? ..........................................................................................................11

+ 2. Country framing: interpreting the consistency of finance flows

at the country level ........................................................................................................13

2.1 Key economic sectors facing climate-related risks in Colombia .................................. 14

2.2 Nationally relevant targets for the consistency of finance flows .................................. 15

2.3 The potential impact of Covid-19 on Colombia’s climate objectives............................ 16

+ 3. Public levers supporting the consistency of finance flows with

low-emission, climate-resilient development pathways in Colombia .......................17

3.1 Key actions considered to be consistent with climate objectives ................................ 17

3.2 Key actions considered to be inconsistent with climate objectives.............................. 23

3.2.1 Deforestation and agriculture in Colombia ............................................................ 23

3.2.2 Energy transition in Colombia ............................................................................... 23

+ 4. Private sector actions towards the consistency of finance flows with

low-emission, climate-resilient development pathways ............................................26

4.1 Colombia’s private sector and market structure .......................................................... 26

4.2 Bank lending ................................................................................................................ 31

4.3 Bond markets .............................................................................................................. 31

4.4 Insurance sector .......................................................................................................... 33

4.5 Listed equity ................................................................................................................ 34

4.6 Private equity ............................................................................................................... 34

4.7 Investment decision-making ........................................................................................ 35

+ 5. Conclusion ...................................................................................................................36

+ References ........................................................................................................................39

Climate-consistency of finance flows: iGST case study series 4Acronyms

CCADI Colombian Climate Asset Disclosure Initiative

CDM Clean Development Mechanism

CGF Financial Management Committee (Comité de Gestión Financiera)

ESG environmental, social and governance

GHG greenhouse gases

GST Global Stocktake

iGST Independent Global Stocktake

MRV measurement, reporting and verification

NAMA Nationally Appropriate Mitigation Action

NDC nationally determined contribution

SFC Financial Superintendence of Colombia (Superintendencia Financiera

de Colombia)

TCFD Task Force on Climate-related Financial Disclosures

UNFCCC United Nations Framework Convention on Climate Change

Climate-consistency of finance flows: iGST case study seriesConsistency case study: Colombia March 2021 + Executive summary The third long-term goal of the Paris Agreement, if operationalised, stands to have tremendous impact. Article 2.1.c is a commitment from Parties to ‘mak[e] finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development’ (UNFCCC, 2015). This long-term goal recognises that we not only need an increase in finance that supports climate action, but must also redirect the finance, both public and private, that is locking countries into high-emission, low-resilience futures. It is only through meeting this third long-term goal, and the very idea of consistency of public and private financial flows, that we can also deliver on the two other long-term goals of the Paris Agreement, on adaptation and mitigation. This goal is relevant to developing and developed countries alike, although it should not detract from the obligation of developed countries to provide and mobilise climate finance for mitigation and adaptation to countries that have not historically contributed to climate change (Article 9, UNFCCC, 2015). Article 14 of the Paris Agreement obliges Parties to assess collective progress toward the purpose and long-term goals of the Paris Agreement, including Article 2.1c. The first of these Global Stocktakes (GST) is to be completed in 2023. As of today, there is no formal United Nations Framework Convention on Climate Change (UNFCCC) guidance on how to make financial flows consistent with climate action. This is likely to hinder the assessment of collective progress in the first GST. As appropriate transparency will ultimately build trust and confidence for effective implementation of the Paris Agreement, it becomes critical therefore that measurement and reporting of the consistency of finance flows towards low-emission, climate-resilient development pathways is continuously increased. While interpretation might vary across countries and stakeholders, country case studies are intended to be conversation starters, highlighting progressive and best practice examples arising from these efforts. Colombia is an upper-middle-income country (World Bank, 2020a) with steady economic growth. Over the past decade, the economy grew by an average of 4.6% per year (Delgado et al., 2020) and growth projected to continue at an average 2.9% per year towards 2050 (Bataille et al., 2020). This has helped the country to reduce poverty and increase social security, and to become a member of the Organisation of Economic Cooperation and Development (OECD) in 2020. Economic growth over the past decade has been linked to growth in the mining and oil sectors, as well as to an increase in foreign investment and high prices for oil and basic products. However, a higher income has also increased the demand for fossil fuels, especially in the transportation, manufacturing and power generation sectors (Calderón et al., 2016). Colombia’s economy remains highly dependent on natural resources, which makes it particularly vulnerable to the adverse effects of climate change (Murillo, 2017), 1 and a high share of its current greenhouse gas (GHG) emissions come from agriculture, forestry and other land use (AFOLU) (Gobierno de Colombia, 2015). These factors present pressing social and economic challenges for the decarbonisation and climate-resilience transition of the country. It is further foreseen that the recession due to the Covid-19 pandemic will have a strong negative effect on poverty rates and on the overall economic performance of the country. Gross domestic product (GDP) is projected to have fallen by 8.2% in 2020 (IMF, 2020) due to Covid-19, and a post-Covid-19 recession will have a direct impact on 1According to the National Unit for Risk Disaster Management, between 1998 and 2012, 90% of the country’s emergencies were related to hydroclimatic events. Climate-consistency of finance flows: iGST case study series 6

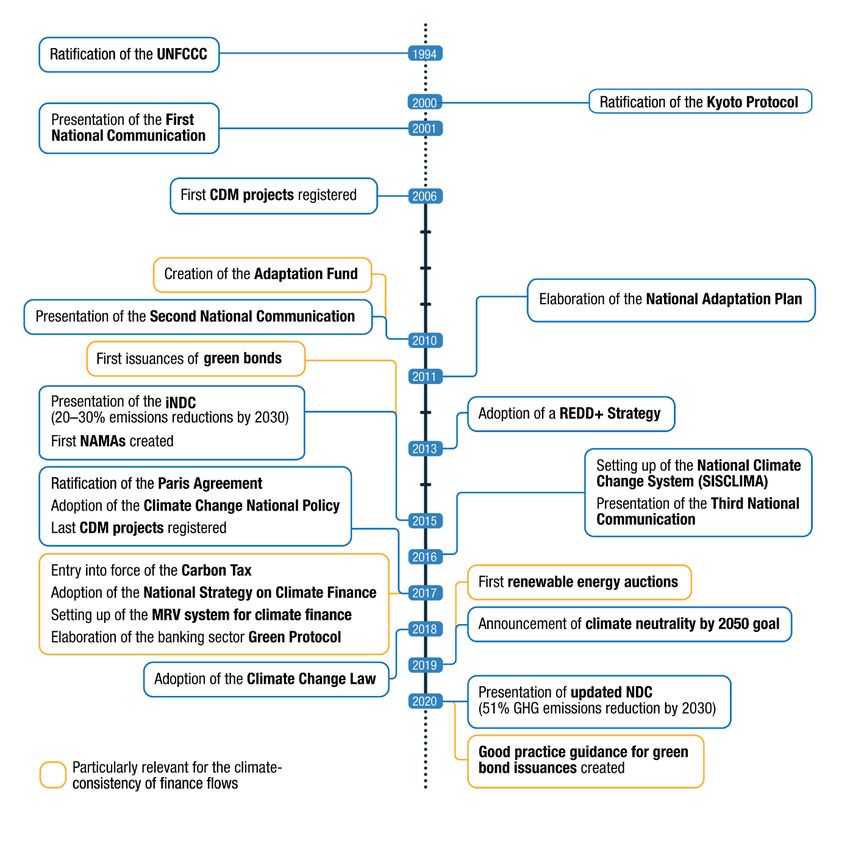

Consistency case study: Colombia March 2021 poverty rates, raising them by over 10% in the Latin American region (Cárdenas and Guzmán Ayala, 2020). Like most developing nations, Colombia’s early climate action focused on the elaboration of National Communications (2001, 2010), as well as on the implementation of the Clean Development Mechanism (CDM) 2 of the Kyoto Protocol followed by Nationally Appropriate Mitigation Actions (NAMAs), 3 the latter two of which aimed to attract international resources to domestic climate action. Nevertheless, in the past decade Colombia has seen an increasing number of public and private climate actions, policies and investments. Among these, the most relevant are the Climate Change National Policy (2017) and the Climate Change Law (2018), which have enabled more specific institutional, financial and economic instruments (i.e. the National Strategy on Climate Finance (2017), the Carbon Tax (2017), renewable energy auctions (2019) and the Adaptation Fund (2010)). These recent policies and investments are mostly driven by the implementation of the Paris Agreement, and in turn have led to the adoption of a domestic long-term goal of reaching carbon neutrality by mid-century (Presidencia de Colombia, 2019) 4 and an updated 2020 nationally determined contribution (NDC) that has the goal of reducing Colombia’s GHG emissions by 51% by 2030 (Gobierno de Colombia, 2020) (Figure 1). The private sector has also started to lead actions to align its financing activities with a low- emission, climate-resilient pathway. The banking sector has led the elaboration of a Green Protocol (2017), in which government and private financial institutions join to make a more sustainable and climate-resilient financial system; certified green bonds have been issued since 2015; and the insurance sector leads the way in integrating climate risk into business and investment decision-making and has developed climate scenario assessments of its aggregate portfolio. This case study finds a nascent process of alignment of Colombian public and private financial flows with low-emission, climate-resilient development pathways (Figure 2 and Figure 3). However, additional measures are required. In particular, there needs to be a shift away from market dependence on fossil fuel production and exporting and from the continuing investment in fossil fuels. This requires the promotion of a just transition of the energy sector, a transition that enhances industrial competitiveness and modernisation of transport systems. A thorough social and economic transformation to reduce agriculture- and deforestation-related emissions, while ensuring economic development and poverty alleviation, access to energy and rural development, with strong, active participation of the private sector, would also be necessary. These measures ought to be in line with Colombia’s carbon neutrality goal and its updated 2020 NDC. 2 From 2006 to 2017, Colombia registered 67 CDM projects (CDM Registry, 2020). 3 Between 2015 and 2016, Colombia elaborated 17 NAMAs for the agriculture, energy, transportation, industry, waste, livelihoods and forestry sectors (MADS, 2016). Some of these NAMAs continue to be implemented, and the coffee NAMA was integrated into Colombia’s 2020 updated NDC (Gobierno de Colombia, 2020). 4 As part of Colombia’s announcements during the UN Climate Action Summit held in September 2019. Climate-consistency of finance flows: iGST case study series 7

Consistency case study: Colombia March 2021 Figure 1 Timeline of climate action in Colombia Source: Authors’ own elaboration It is important to note that this report corresponds to a high-level review 5 of Colombia’s progress towards Article 2.1c. However, the research did not follow a census method or use a statistically representative sample. In this sense, although the sources analysed may not represent the universe of public and private financial flows in the country, the results do provide a general overview and, hopefully, will help to initiate a conversation about the consistency of these flows with climate objectives in Colombia. 5 The research comprised an extensive literature review, analysis of existing legislation and interviews with key stakeholders. Climate-consistency of finance flows: iGST case study series 8

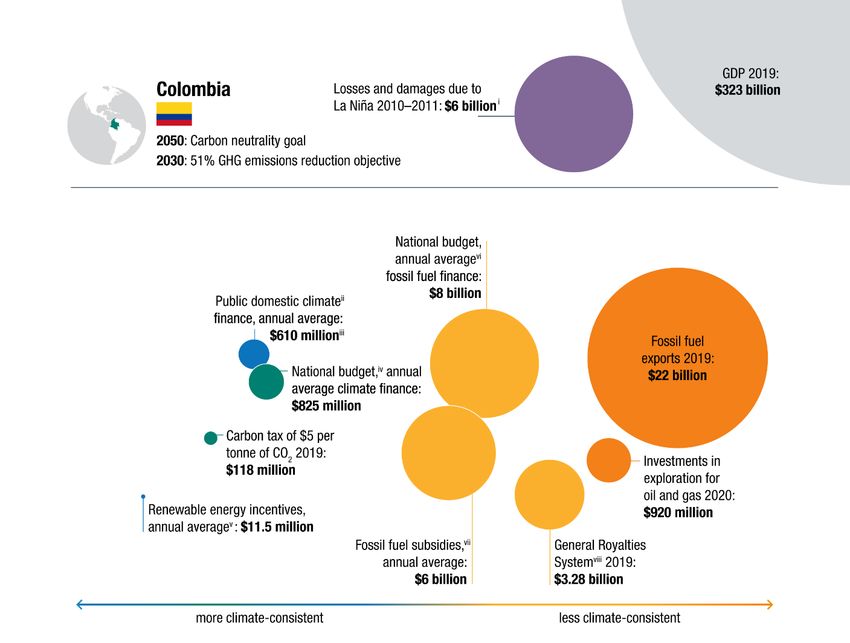

Consistency case study: Colombia March 2021

Figure 2 Consistency of public finance flows with climate objectives in Colombia in

the context of wider finance flows

i

Although there is no direct attribution of losses and damages to climate change, this particular La Niña event

had social and economic consequences to the country that continue to be addressed a decade after and which led

to the creation of the Colombian Adaptation Fund.

ii

This includes the accounting of budgetary measures (39.8% federal budget, 38.5% municipal budget, 4.2%

departmental budget) plus financial resources coming from the General Royalties System and destined to be

climate finance (17.4%). The coverage of the federal budget may therefore overlap with the accounting of climate

finance from the national budget, but this cannot be analysed due to lack of detailed public information.

iii

Average for the period 2011 to 2019. Of the $610 million, there is an annual average of $70 million for

mitigation and $300 million for adaptation; $240 million is cross-cutting. ‘Adaptation’ includes finance by the

Adaptation Fund. However, it does not represent the total amount of financing provided by the Fund ($2.25

billion) because since 2011 a significant amount of the Fund’s resources have been directed to La Niña post-

disaster management.

iv

The national budget is negotiated for the full duration of each government, in this case 2019–2022.

v

For the period 2016 to 2020 (as of November). These incentives are provided in the form of a 50% reduction in

the associated cost of rent for non-conventional renewable energy projects for up to 15 years, an exemption from

paying VAT (with a value of 19%) and a customs duty exemption for imported machinery for projects.

vi

The national budget is negotiated for the full duration of each government, in this case for the period 2019 to

2022. In the budget, a specific amount is allocated to renewable energy, but lack of detailed public information

means this cannot be separated from fossil fuel finance.

vii

Subsidies on petroleum have been annualised for the period 2014 to 2019, while subsidies for electricity and

gas are already accounted on an annual basis. Of the $6 billion, $5.4 billion is for petroleum, $0.6 billion is for

electricity and gas.

viii

This system comprises revenues from fossil fuel exploration and production, resources that are in turn invested

in public projects, including climate finance. The royalties are reported biennially, hence an annual average is

presented for the period 2019 to 2020.

Source: Authors’ own elaboration

Climate-consistency of finance flows: iGST case study series 9Consistency case study: Colombia March 2021 Figure 3 Consistency of private finance flows with climate objectives in Colombia Note: Bank lending loan portfolio correct as of December 2019; bond market issuances correct as of 15 December 2020; insurance sector investment portfolio value correct as of December 2018; listed equity market capitalisation correct as of October 2019; cumulative private equity investments reported in the 2015–2019 period. Source: Authors’ own elaboration Climate-consistency of finance flows: iGST case study series 10

Consistency case study: Colombia March 2021

+ 1. Why collate country actions

supporting Article 2.1c of the

Paris Agreement?

The long-term goal of making finance flows consistent with a pathway towards low GHG

emissions and climate-resilient development is neither defined nor fully articulated under the

UNFCCC process. Nor has there been a place in the negotiations to discuss and develop the

concept of the climate-consistency of finance flows (Bodle and Noens, 2018) or any

requirements for Parties to the Paris Agreement to report on this consistency. 6 Furthermore,

the foundations of the GST do not have highly detailed provisions and, so far, allow ample

flexibility, including in how to take stock of collective progress towards Article 2.1c (Watson

and Roberts, 2019). Developing discussion on how to operationalise Article 2.1c can create

useful lessons and encourage further action, and it may also support a meaningful discussion

at the first of these GSTs in 2023 (UNFCCC, 2015). Despite the lack of clarity of the concept,

commitments to ‘align’ with the Paris Agreement are being made in both public and private

institutions. These emerging initiatives towards the alignment of finance flows with the Paris

Agreement are largely based on guiding statements (MDBs, 2018; Cochran and Pauthier,

2019). Unpacking how to fully operationalise these commitments on Paris alignment remains

work in progress (Carter, 2020). 7

Accountability under the Paris Agreement will fall upon governments. As such, there is a

rationale to focusing on the levers that public actors create for finance flows, both public and

private, by generating incentives and disincentives. Recognising that public flows alone are

not sufficient for a transition to low-emission, climate-resilient pathways, these public levers

could include financial policy and regulation, fiscal policy, public investment and information

instruments (GGBP, 2014; Watson and Schindler, 2017; Whitley et al., 2018) (Table 1).

However, a transformation of the financial system as a whole that is consistent with climate

action will still require additional regulatory, structural and capacity efforts for both public and

private flows.

The Independent Global Stocktake (iGST) (Box 1) can use its independence to work with a

diversity of actors across political and technical challenges. In this case, the challenge relates

to the progression of discussions on the consistency of finance flows with low-emission,

climate-resilient development pathways. This case study of action towards consistency of

finance flows in Colombia includes the concise and high-level early mapping of government-

led policy levers and, where feasible, private initiatives. Building on a framework of

government levers that can help to operationalise consistency (Whitley et al., 2018), this case

study identifies the financial policy and regulation, fiscal policy, public finance and information

instruments relevant to climate action, as well as different initiatives and consistency trends in

private flows that are already present in Colombia. It also highlights future challenges for the

country’s pursuit of consistency. The case study is intended to be a thought-provoker and

conversation starter.

6 It has, however, been suggested that countries could voluntarily choose to do so in their biennial transparency

reports (Whitley et al., 2018).

7 There are, however, a few examples of alignment that could be followed by financial institutions, e.g. the European

Investment Bank’s commitment to align all of its financing activities with the principles and goals of the Paris

Agreement by the end of 2020, and to dedicate 50% of its financing to climate action by 2025, while ensuring that

the other 50% is consistent with and does not undermine the EU’s climate mitigation and adaptation objectives

(EIB, 2020).

Climate-consistency of finance flows: iGST case study series 11Consistency case study: Colombia March 2021

Table 1 Government-led tools to encourage the consistency of finance flows with

climate ambitions

Financial policies Information

Fiscal policy levers Public finance

and regulations instruments

(primarily influence (primarily influence (primarily influence (primarily influence

behaviour through behaviour through behaviour by shifting behaviour through

force of law) price) financial risk) awareness)

• lending • taxes • grants • certification and

requirements • levies • debt labelling

• accounting • royalties • equity • transparency

systems • price support or • guarantees initiatives

• mandates of controls • insurance • corporate strategies

supervisory • public (from public pension • awareness

authorities procurement funds, sovereign wealth campaigns

• standards • budget support funds and public • statistical services

• plans and (including for finance institutions) • scenario analysis and

strategies establishment of stress testing

• disclosure public funds and • standards

requirements finance institutions • plans and strategies

(where mandatory and state-owned • disclosure

and enforced) enterprises) requirements

(where voluntary)

Source: Whitley et al. (2018)

Box 1 What is the iGST and the Finance Working Group?

The Independent Global Stocktake (iGST) is a data and advocacy initiative, led by the

ClimateWorks Foundation, that brings together climate modellers, analysts, campaigners

and advocates to support the Paris Agreement. The iGST is structured into four working

groups (covering adaptation, mitigation, finance and equity) with additional activities

undertaken by an umbrella group of iGST partners. The objective of the iGST is to positively

influence the official GST, by supporting information collection, technical assessment and

political consideration, as well as bolstering national, regional and subnational relevance in

the process.

The Finance Working Group (FWG) of the iGST is an open partnership that brings together

a wide range of expert perspectives from its members from the Global North and South.

Focusing on the finance-related aspects of the Paris Agreement, ‘finance’ as used by the

working group encompasses two core, interrelated topics. It considers both the provision of

support to developing countries to mitigate and adapt to climate change (Article 9), and the

consistency of all finance flows with climate objectives (Article 2.1c).

The ultimate goal of the FWG is to support more ambitious country pledges and domestic

actions by 2025, which will lead to substantial progress towards meeting all three of the long-

term goals of the Paris Agreement. To achieve this goal, the FWG’s long-term objective is to

have direct influence of the UNFCCC GST process, through the production of knowledge,

outreach and support for appropriate data inputs, and to support a benchmarking of the

official GST through the assessment of progress on financing the commitments to the Paris

Agreement. It will also support an active, independent civil society on the issues surrounding

the financing of climate action.

Climate-consistency of finance flows: iGST case study series 12Consistency case study: Colombia March 2021

+ 2. Country framing: interpreting the

consistency of finance flows at

the country level

The Paris Agreement adopts a bottom-up, country-driven approach. It has shifted multilateral

negotiations away from a top-down, target-setting approach, so that countries themselves

define their own pathways to becoming low-emission, climate-resilient economies. For the

operationalisation and pursuit of consistency of finance flows and in the absence of predefined

criteria, this suggests there will be nationally-driven interpretations, but it also necessitates

transparency, whereby each country’s interpretation of ‘consistency’ can be scrutinised to give

it legitimacy. This further allows country progress to be acknowledged in light of common but

differentiated responsibilities and respective capabilities.

This section outlines the relevant country and market contexts within which Colombia will need

to make finance flows consistent with a low-emission, climate-resilient development pathway

(see also Box 2).

Box 2 Colombia at a glance

Colombia is an upper-middle-income economy

(World Bank, 2020a).

Gross domestic product (GDP): $323.8 billion

(World Bank, 2020b)

GDP per capita: $6,432.4 (World Bank, 2020c)

Population: 46 million (77.1% living in urban areas)

Credit rating: BBB– (Fitch Ratings, 2020)i

Poverty: 35.7% of Colombia’s population are in a situation of povertyi and 9.6% are in

extreme monetary povertyii (DANE, 2020a)

As of 31 December 2019, Colombia’s Consolidated General Balance for the national and

territorial levels and the public sector had $381.1 billion (136.3% of GDP) in assets, $424.7

billion (151.9% of GDP) in liabilities and $–43.66 billion (15.6%) in equity (Bohórquez

Ramírez, 2020).

Colombia is a Party to the UNFCCC, the Kyoto Protocol and the Paris Agreement, a Non-

Annex I country under the UNFCCC and a member of the G77/China and the Independent

Association of Latin America and the Caribbean (AILAC) negotiation group.

i As of November 2020. The rating was downgraded from BBB in April 2019 due to ‘risks to fiscal consolidation

and the trajectory of government debt, the weakening of fiscal policy credibility, and increasing risk from

external imbalances (Fitch Ratings 2019).

ii Poverty is defined as an income below the value in money that a given person requires monthly to acquire

basic food, services and minimum goods to live (DANE, 2020c).

iii Extreme monetary poverty is defined as an income below the value in money that a given person requires

monthly to acquire basic food to live with a minimum calorific value of 2,105 for urban inhabitants and 2,079

for rural inhabitants (DANE, 2020c).

Source: Authors’ own elaboration

Climate-consistency of finance flows: iGST case study series 13Consistency case study: Colombia March 2021 2.1 Key economic sectors facing climate-related risks in Colombia In 2010–2011, the phenomenon of La Niña caused losses and damage totalling $6 billion, equivalent to 2.2% of GDP. More than 3.2 million people were affected, 3.5 million hectares (ha) were flooded and 845 main and secondary roads were closed throughout the country (Gobierno de Colombia, 2015). Although it is difficult to attribute specific weather events to climate change, it has been estimated that 88% of disasters in Colombia are related to floods, droughts and mudslides (DNP, 2018), events that, according to climate change scenarios, will most likely increase in frequency and intensity, representing a direct risk to the Colombian economy and its population in the short and long terms. Also, Colombia has a high dependence on fossil fuel exports, creating transition risks. In the past 10 years, 60% of Colombia’s exports have been related to fossil fuels and extractive industry products; in 2019 alone, exports of fossil fuels, particularly oil and coal, and products of the extractive industries represented $22 billion (DANE, 2020b) (equivalent to 6.7% of GDP). Colombia’s electricity production has relatively low emissions due to a large share of hydroelectricity production (76%) (Delgado et al., 2020). However, Colombia also has 38 operational fossil fuel projects, comprising four natural gas terminals, eight oil pipelines, three gas pipelines and 23 coal-fired units (Browning et al., 2020) and is continuing to invest in exploration for oil and gas, including $920 million in 2020 (70% onshore and 30% offshore) (ACP, 2020). Oil and gas reserves are limited to a few years (6.3 and 8.1 years, respectively), but coal reserves have a much longer horizon, being sufficient for the next 180 years (CCADI, 2020a). The largest share (58%) of Colombia’s emissions comes from deforestation and agriculture (Gobierno de Colombia, 2015), followed by energy (38.5%) (Figure 4). Major drivers of deforestation are the expansion of the agricultural frontier and the transformation of forest into pastures for cattle ranching. In recent decades, illicit activities have been part of the driving force behind deforestation, mainly through illegal cropping, mining, logging and land grabbing. Deforestation and some agricultural practices are not only a source of risk, in increasing climate change vulnerability, but could also contribute to climate change adaptation where used efficiently and sustainably. Climate-consistency of finance flows: iGST case study series 14

Consistency case study: Colombia March 2021 Figure 4 Colombia’s GHG emissions by sector, 2016 Source: Our World in Data (https://ourworldindata.org/co2-and-other-greenhouse-gas-emissions). 2.2 Nationally relevant targets for the consistency of finance flows Colombia’s GHG emissions represent 0.41% of global emissions (Ge and Friedrich, 2020). In its 2015 NDC, Colombia included a mitigation objective to reduce its GHG emissions by 20% from the business-as-usual scenario by 2030, which could be increased to 30% emissions reduction, conditional on international support. The 2020 updated version of Colombia’s NDC includes an economy-wide mitigation objective to reduce its GHG emissions by 51% by 2030 (Presidencia de Colombia, 2020a). The NDC also includes 148 specific national, sectorial and territorial mitigation measures 8 owned by governmental ministries, territorial entities and companies – which may help to ensure budgetary provisions for their implementation – and contemplates the elaboration of carbon budgets by 2023 at the latest. It includes a goal to reduce the deforestation rate from 158,894 ha per year to 50,000 ha per year by 2030 (Gobierno de Colombia, 2020), as well as a 40% emissions reduction objective for black carbon by 2030. The updated NDC, which constitutes Colombia’s first Adaptation Communication, includes detailed risk and vulnerability information and maps, as well as specific sectorial and territorial goals to reduce vulnerability and increase adaptive capacity through adaptation planning and governance, ecosystem-based adaptation, risk assessment and management, and resilient infrastructure, and through monitoring and evaluation for households and water, health, energy, trade, industry and tourism, agriculture and transport (MADS, 2020). Through this Adaptation Communication, it is initially estimated that an annual 8 These measures relate to: energy (energy efficiency, fugitive emissions, generation and supply management); cities and livelihoods (waste management, waste water management, sustainable construction); agriculture and rural development (sustainable agriculture, cocoa, rice and coffee production); industry and tourism (energy efficiency in industrial facilities, efficiency in brick kilns, fertilisers, cement production efficiency, logistics efficiency); transportation (electric mobility, modernisation of freight vehicles, development oriented to transportation, train transport); environment (ecosystem conservation and restoration, substitution of wood-burning stoves for efficient cooking stoves, HFC reduction, deforestation reduction); and finance (carbon tax) (Gobierno de Colombia, 2020). Climate-consistency of finance flows: iGST case study series 15

Consistency case study: Colombia March 2021 adaptation investment of 0.2% of GDP (approximately $600 million) is required up to 2030 to cover Colombia’s finance adaptation gap (Gobierno de Colombia, 2020). The government of Colombia estimates the total amount of investment needed in relation to the 2015 NDC to be $2.07 billion by 2030 for mitigation alone (AILAC, 2020). Some mitigation actions under the NDC are already included in the National Development Plan 2018–2022, hence they rely, to a certain extent – at least during the implementation period of the Plan – on the public budget for their completion. Further international cooperation in the form of technical and financial assistance is still required for the fulfilment of the NDC, particularly now that its ambition has been significantly increased, although there is no clarity on the amounts required as the costs of specific measures have not yet been presented. While Colombia’s national Climate Change Law (Congreso de Colombia, 2018a) provides general guidelines to ensure that climate scenarios are integrated into public and private finance planning (ibid.), this has been irregularly implemented, partly because the Law’s regulatory framework is due to be agreed in 2021. The upcoming regulatory framework constitutes a great opportunity to foster a more preventive approach to adaptation, different from that of risk management. It will also enable a more consistent pathway in the use of public and private finance for the implementation of the country’s NDC and its first Adaptation Communication, as well as for future development planning processes that internalise climate scenarios and associated physical, financial and transition risks for both public and private entities. Colombia has a long-term goal to reach carbon neutrality by 2050. A long-term low-emissions strategy for the country is also currently being developed. 2.3 The potential impact of Covid-19 on Colombia’s climate objectives In the second and third quarters of 2020, the economy contracted by 15.8% and 9%, respectively, due to the Covid-19 pandemic (Gobierno de Colombia, 2020). Hence, a 2020–2022 Covid-19 recovery plan is being developed. The plan has five policy elements: job creation, clean growth, support to vulnerable groups, agriculture and peace, and health, with the investment of over $26 billion (around 8% of GDP) and the creation of 1 million direct and indirect jobs. The plan includes health policy measures, plus the acceleration of 27 energy projects for renewable energy and transmission (including nine wind, five solar, three geothermal and one hydropower project, as well as nine transmission lines), the planting of 180 million trees, with incentives for silvopastoral production and agroforestry schemes that have community support, and provisional increased non-conditional payments to vulnerable groups (Presidencia de Colombia, 2020b). In particular, the renewable energy and reforestation goals of this plan are intended to accelerate the country’s climate commitments through the recovery package. However, the plan does not explicitly refer to the climate or biodiversity crises, and it emphasises how the mining and energy sectors are central to regaining productivity. Moreover, since early 2020, Colombia has committed at least $378.59 million to supporting different energy types through new or amended policies, of which at least $374.17 million is destined for unconditional fossil fuels (oil and gas) and $4.42 million for unconditional clean energy (Energy Policy Tracker, 2021). Therefore, a thorough follow up to the implementation of the Covid-19 recovery plan would be necessary to assess the consistency between these investment flows and the climate goals of the country and the Paris Agreement. Climate-consistency of finance flows: iGST case study series 16

Consistency case study: Colombia March 2021

+ 3. Public levers supporting the

consistency of finance flows with

low-emission, climate-resilient

development pathways in

Colombia

3.1 Key actions considered to be consistent with climate objectives

Climate change has gradually become an essential component of the development planning

processes in Colombia – particularly after the adoption of the Paris Agreement – which are

increasingly being guided by the overall objectives of reaching carbon neutrality by mid-

century and enhancing climate resilience in Colombia’s most vulnerable ecosystems, regions

and populations.

The Climate Change National Policy contemplates that Colombia’s NDC 2015, as well as

subsequent NDCs, need to be embedded within each National Development Plan (approved

every four years), with explicit sectoral and budgetary contributions towards their

accomplishment (DNP, 2018). The last three national development plans (for 2010–2014,

2014–2018 and 2018–2022) incrementally feature green growth and climate change. This

illustrates the integration of these issues into the country’s planning processes. The

2018–2022 National Development Plan includes concrete goals to: reduce deforestation by

30% relative to the business-as-usual scenario; double the existing railway infrastructure; and

increase the use of non-conventional renewable energy, to reach 2,500 MW (DNP, 2018),

which would represent growth from less than 1% to 10% of the energy mix (Ministerio de

Minas y Energía, 2020a). The Climate Change Law has also created a more complete

institutional setting within which to manage climate public policy, and has driven initial specific

actions, such as the Carbon Tax, the measurement, reporting and verification (MRV) system

for climate finance (Congreso de Colombia, 2018a) (which will also soon start tracking climate-

misaligned finance), and the future development of an emissions trading scheme.

Table 2 outlines in more detail the government-led actions that the Government of Colombia

is taking and which might be considered relevant to making finance flows consistent with low-

emission, climate-resilient development pathways. It should be noted that plans, policies and

regulations described in the context column in Table 2 are not specifically finance-related, as

per the ODI framework. However, the authors consider that this political framework forms the

basis of more specific actions for consistency of financial flows, therefore they have been

included.

Climate-consistency of finance flows: iGST case study series 17Consistency case study: Colombia March 2021

Table 2 Government-led actions supporting consistency of finance flows in Colombia

Government Context Mitigation-relevant actions Adaptation-relevant actions

lever Quantitative information Qualitative information Quantitative Qualitative information

information

Financial policy and The Energy Plan 2050 (2016) aims Carbon neutrality by 2050 goal Renewable energy The National Adaptation

regulation to diversify the country’s energy auctions were initiated in Plan (2011) was one of

resources and ensure a reliable 2019 as a way to facilitate Colombia’s first policy

NDC 2020, with a mitigation

energy supply through greater use clean energy investment and instruments. It defines for

objective to reduce GHG

of non-conventional renewable enable renewable goals in sectors and territories the

emissions by 51% by 2030

sources of electricity (IEA, 2020). an emerging market for non- main guidelines on

(Presidencia de Colombia,

The Plan can be implemented conventional renewable prioritising actions that

2020a)

through enhanced use of renewable energy. These auctions reduce vulnerability and

energy auctions to ensure greater have already helped including climate change

use of renewable sources of increase the use of non- and variability in their

energy. conventional renewable planning processes. There

energy to 1,500 MW (6% of are 11 territorial adaptation

the energy matrix) plans and sectorial plans.

The Climate Change National

(Ministerio de Minas y The continuous

Policy (2017) has a 12-year

Energía, 2020a). implementation of these

timeframe within which climate

plans is envisaged in the

policy is to be regularly revised and

Climate Change Law

updated. Building upon previous

(Gobierno de Colombia,

policy instruments, it aims to

2011).

influence public and private

developmental decision-making and

mainstream adaptation and NDC 2020, which

mitigation rationales at the territorial represents the first

and sectoral levels (Murillo, 2017). Adaptation

Communication, includes

detailed risks and

The Climate Change Law (Law

vulnerability information as

1931, 2018) was enacted as a way

well as specific sectorial

to establish the general regulatory

goals to reduce vulnerability

guidelines for climate action in the

and increase adaptive

country. It establishes a Financial

capacity (MADS, 2020).

Management Committee (CGFi) to

be in charge of coordinating and

facilitating a dialogue for public and

private climate finance actions and

to ensure the necessary flow of

resources for the implementation of

the Climate Change National Policy

(Congreso de Colombia, 2018a).

Climate-consistency of finance flows: iGST case study series 18Consistency case study: Colombia March 2021

Government Context Mitigation-relevant actions Adaptation-relevant actions

lever Quantitative information Qualitative information Quantitative Qualitative information

information

Fiscal policy The implementation of the Carbon Carbon Tax: Carbon Tax Law 1819,

Tax created a national voluntary - tax of ~$5/tonne of CO2 on adopted in 2016, came into

carbon market by certifying net fossil fuels (except coal) in place force in 2017 (Presidencia

emission reductions achieved since 2017 (started at de Colombia, 2017).

through mitigation projects in $3.9/tonne of CO2)ii

Colombia, mostly in the forest

- cumulative carbon revenue The Ministry of Finance is

sector (MADS, 2017). ~$367 million, as of July 2020 currently working on the

- covers 27% of Colombia’s issuance of green

Revenues generated by the Carbon GHG emissions (DIAN, 2020), sovereign bonds to

Tax are to be transferred to the fund mainly from road transportation diversify its debt

Colombia in Peace, where 70% are management through green

- increases every February, in

directed to the peace process and line with the inflation rate plus investments, which could

30% to environmental action enhance the visibility of its

1% (MADS, 2017).

(Congreso de Colombia, 2018b). green bonds market (CBI,

2020).

Between 2016 and 2020 (as of

It will be important to see whether November), the Ministry of

the Carbon Tax is expanded to

Energy has provided economic

include coal or other GHGs, and

incentives to renewable

how it relates to the upcoming energy projects totalling $46.2

national emissions trading scheme

million (UPME, 2020)iii which

and/or is used for the

represents an average annual

implementation of the International

amount of $11.5 million.

Civil Aviation Organization’s

compensation scheme (CORSIA)

and Article 6-derived markets.

Climate-consistency of finance flows: iGST case study series 19Consistency case study: Colombia March 2021

Government Context Mitigation-relevant actions Adaptation-relevant actions

lever Quantitative information Qualitative information Quantitative Qualitative information

information

Public finance A Climate Finance National As part of the MRV system for Between 2011 and 2019, Decree 4819 for the

Strategy was presented in 2017 climate finance, it has been public domestic finance creation of the Adaptation

with the view to identify economic estimated that between 2011 for adaptation totalled Fund, 2010, which aimed to

and financial instruments that can and 2019, public domestic $2.8 billion, of which address the reconstruction

be used to advance climate action, financeiv destined for climate 39.4% came from the and social and economic

as a general guideline for the work action totalled $5.6 billion, of Colombian Adaptation recovery after the 2010–

of the CGF (CGF 2017). which $0.66 billion was Fund for projects directly 2011 La Niña events

destined for mitigation finance related to adaptation. (Pineda Tellez, 2019).

and $2.3 billion for cross-

cutting finance (mitigation and Over time, this Fund has

Over the same period, the

adaptation) (DNP, 2020). Adaptation Fund allocated increasingly focused its work

a total of $2.25 billion to on mainstreaming an

Average annual public finance address the direct effects approach that involves

for climate action is estimated at of the 2010–2011 La Niña increasing the resilience and

$0.61 billion, equivalent to events in affected areas, reducing the vulnerability of

0.15% of Colombia’s GDP directed to the health, municipalities, communities

(CGF, 2017). v infrastructure (livelihoods, and infrastructure that are

transportation, water and being financed for recovery

sanitation, and education), or reconstruction. The

On the other hand, the national

economic recovery and approach uses ecosystem-

budget 2019–2022 provides

environment sectors based and/or community-

$3.3 billion for the

(Pineda Tellez, 2019). based adaptation, including

environment sector, which can

through several macro-

be considered Paris-aligned

projects directly related to

(1.15% of the total budget), and

structural and social

an additional $9.6 billion (3.39%)

may be related to climate action adaptation.vi

in regard to sustainable

transport, water infrastructure

and sanitation, sustainable

public expenditure and local

development (Congreso de

Colombia, 2019). There is no

clarity over the specific budget

for renewable energy.

Climate-consistency of finance flows: iGST case study series 20Consistency case study: Colombia March 2021

Government Context Mitigation-relevant actions Adaptation-relevant actions

lever Quantitative information Qualitative information Quantitative Qualitative information

information

Information instruments The National Climate Change A regulatory roadmap for the

System (SISCLIMA, 2016; development of a green

constituted by an Inter-ministerial finance taxonomy and

Commission on Climate Change vii), promotion of the adoption of

nine Regional Climate Change environmental, social and

Nodes and local authorities together governance (ESG) criteria

form the institutional axis through by financial companies, to

which climate action and enhance transparency and

development plans are managed disclosure and build

(Murillo, 2017). institutional capacity, was

adopted by

Superintendencia Financiera

The national MRV system for

(2019) (CCADI, 2020b)

climate finance (2017) tracks

climate finance flows, both domestic

and international (DNP, 2020). For Superintendencia Financiera

the time being, the system does not and the Central Bank of

measure alignment with either the Colombia are members of

Climate Change Law or the NDC. the Network for Greening

Private finance was originally the Financial System,

tracked, but there are significant which can contribute to the

data gaps in the tracking. development of guidelines

and regulations for creating

a greener financial system

The financial regulator,

(NGFS, 2019).

Superintendencia Financiera, is

also working on a new taxonomy for

climate finance that may help

reduce information gaps and better

inform decision-making, including

by the private sector.

i

The CGF membership comprises: National Development Department, Ministry of Finance, Ministry of Foreign Affairs, Ministry of Environment and Sustainable Development,

Ministry of Trade, Industry and Tourism, Presidential Cooperation Agency, Hydrology, Meteorology and Environmental Studies Institute, Fund for Financing the Agriculture

Sector, National Development Trustee, Development Trustee, Adaptation Fund, Green Protocol, Foreign Trade Bank of Colombia, the Inter-ministerial Commission on Climate

Change and the Regional Nodes on Climate Change.

ii

It is estimated that the implementation of the 2015 NDC would require a marginal cost of $20 per ton of CO2e by 2030 (Delgado et al., 2020), to align mitigation efforts and

carbon pricing with the carbon neutrality goal. A higher would be required to ensure implementation of the 2020 updated NDC.

iii

These incentives are provided in the form of a 50% reduction in the associated cost of rent for non-conventional renewable energy projects for up to 15 years, an exemption

from VAT (with a value of 19%) and a customs duty exemption for machinery imported for projects.

Climate-consistency of finance flows: iGST case study series 21Consistency case study: Colombia March 2021

iv

This includes the accounting of budgetary measures (39.8% federal budget, 38.5% municipal budget and 4.2% departmental budget) plus financial resources coming from

the General Royalties System and destined to climate finance (17.4%). These estimates are not absolute; rather, a conservative approach that refers to ‘associated’ investment

for mitigation and adaptation to climate change is used. Actions are classified as highly associated or potentially associated to climate change and national policy instruments.

v

To achieve the 2015 NDC, it has been estimated that public funding for mitigation action needed to increase its annual investments by 86%, although specific quantification

of adaptation needs is still required (CGF, 2018). These estimates need to be updated for the 2020 updated NDC.

vi

Overall, however, public adaptation funding is insufficiently aligned with the country’s climate vulnerabilities (i.e. food security has a 35% climate-related risk, but public

adaptation funding for this issue is only 1%) (CGF, 2018).

vii

The Commission membership comprised: Ministry of Environment and Sustainable Development, Ministry of the Interior, Ministry of Finance, Ministry of Agriculture,

Ministry of Mines and Energy, Ministry of Transport, Ministry of Foreign Affairs, Ministry of Livelihoods, Cities and Territories, Ministry of Trade, Industry and Tourism,

National Planning Department, and National Unit for Risk Disaster Management.

Source: Authors’ own elaboration

Climate-consistency of finance flows: iGST case study series 22Consistency case study: Colombia March 2021

3.2 Key actions considered to be inconsistent with climate objectives

In addition to capturing the positive aspects of government-led action on consistency, it is

important to consider the more inconsistent aspects of public action. These can indicate areas

in which progress is required and challenges that are likely to be faced when operationalising

the concept of consistency. In Colombia, there are two major areas that stand out:

deforestation and agriculture, and energy.

3.2.1 Deforestation and agriculture in Colombia

In 1990, 56.4% of Colombia’s land territory was covered by natural forests. In the period

between 1990 and 2014, deforestation, mainly in the Colombian Amazonia (which has 66.7%

of the country’s forest area), reduced forest coverage to 51.6% (IDEAM, 2020a). After the

signing of a peace agreement in 2016, 79% of Colombian Protected Areas experienced

increased deforestation, with a dramatic and highly significant 177% increase in the

deforestation rate (158,894 ha in 2019). Major drivers of deforestation are the expansion of

the agricultural frontier, the transformation of forest into pasture for cattle ranching, and land

grabbing. In recent decades, illicit activities have also been part of the driving force behind

deforestation, mainly in relation to illegal cropping, mining and logging. Another factor in the

exacerbation of deforestation is the exit of the Revolutionary Armed Forces of Colombia

(FARC), which used to control a large part of the country. Agriculture and its expansion often

leads to deforestation and is a source of emissions, but it is also a potential mitigation solution

(Searchinger et al., 2020).

Although in the past couple of years the deforestation rate has started to decline (from

219,973 ha in 2017 to 158,894 ha in 2019) (IDEAM, 2020b), in looking to the future (and

awaiting data for 2020, when the deforestation rate seems to have increased) it will still be

necessary to enhance law enforcement, promote rural land use regulation and ensure

effective conservation of protected areas, together with an integrative, comprehensive

understanding of local communities’ needs, sustainable development and long-term

management (Clerici et al., 2020). Public levers – including public agricultural support, social

protection and access to green finance – play an important role in shifting incentives and

disincentives in agriculture and forestry.

3.2.2 Energy transition in Colombia

Colombia’s energy matrix currently has a high share of hydroelectricity (76% of total electricity

generation) (Calderón et al., 2016). Notwithstanding this fact, an energy transformation of

Colombia’s economy is needed – to achieve the 2020 updated NDC and the carbon neutrality

goal – which must address the following issues:

• The economy’s strong dependence on the exportation and continuous

exploitation of fossil energy. Fossil fuels and products of the extractive industries

made up an average of 60% of national exports over the past 10 years, representing

about 8% of the country’s GDP (DANE, 2020b); 9 90% of Colombia’s coal is exported

and Colombia is the world’s sixth largest coal exporter, although coal mining only

represents about 1.3% of the country’s GDP (Strambo and González Espinosa, 2020).

Colombia also has 38 fossil fuel projects in operation, comprising four natural gas

terminals, eight oil pipelines, three gas pipelines and 23 coal-fired units (Browning et

al., 2020) and is continuing to invest in exploration for oil and gas, including $920

9 Percentages are estimates using official public information from 2010 to 2020.

Climate-consistency of finance flows: iGST case study series 23You can also read