Corporate Overview beyond pioneering

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Corporate Overview beyond pioneering

Who We Are

Bruining 1 st

Erkelens

• Five (5) unique cultivars have been

5

standardized and commercially accepted

as raw material for the production of

Active Pharmaceutical Ingredients (“API”);

• Standardized placebo is also available for

clinical and scientific trials;

Standardized Cultivars

DROge (= ‘dry’) • Patients, researchers, and

18

pharmaceutical partners in over a dozen

countries and jurisdictions count on

Bedrocan’s products;

• Governments, corporates, and research

CANnabis

institutions (NGOs, CROs, etc.) favor the

Jurisdictions served Bedrocan product suite

• Established 1984

30

• Preferred provider to the Office of

Medicinal Cannabis (“OMC”) in the

Netherlands since 2003, ten (10) years

prior to the establishment of the MMPR in

Canada

Years experience

2

Facts and Figures

Operating Statistics Select Financial Statistics*

40 G ro w R o o m s

w o rld w id e

62%Kgs Sold CAGR 2013-2017

53%Revenue CAGR 2013-2017

18 80% Production Capacity CAGR

Ju risd ictio n s

w h e re B e d ro can

p ro d u cts are

10

availab le

Years Fiscal Growth

* O r g a n ic C A G R s d e fin e d a s w ith o u t M & A a c tiv ity

3Once upon a time…

4Corporate Timeline

Start – Program – Start – Expansion – GMP – Expansion

Founding of Dutch Health Official start Start USA team Good Capital –

Bedrocan as an Minister starts under the Dutch and start new manufacturing BI prepares for

agricultural medicinal medicinal production practice (GMP) global expansion

company cannabis cannabis facility in Czech and opening and large equity

program program Republic new Dutch infusion

facility

1984 1999 2003 2015 2017 2018

1992 2002 2014 2016 2017

Seeds – License – Canada – Australia – Outside

First production Bedrocan is New facility Start Bedrocan Investment –

of cannabis awarded 1 s t under Canada Brazil and plans Bedrocan

seeds license to grow Health and for Australia accepts its first

medicinal opening new become reality funds from an

cannabis Dutch facility outside investor

5Global Market for Cannabis and Market Environment

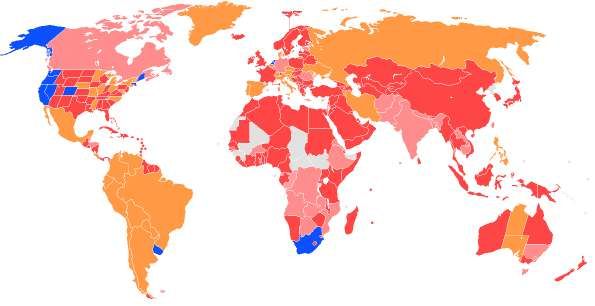

Current Regulation Legality of Possession of Small Amounts of Cannabis

• As of the date of this publication, medical use of cannabis is legal in

Canada, Israel, Belgium*, Austria* Netherlands, Czech Republic,

Denmark (4-year pilot project), Estonia, Spain, Greece, Portugal,

Croatia, Mexico, Chile, Uruguay, Poland, Finland, Norway,

Macedonia, Germany, Jamaica, Australia, Italy, Colombia, Slovakia,

Lesotho and Switzerland;

• Cannabis is classified as a Schedule IV drug in the UN Single

Convention on Narcotic Drugs (the “Convention”); the Convention,

however, allows independent nation states the choice of establishing

cannabis for medical and scientific purposes. L e g a l o r E s s e n tia lly L e g a l Ille g a l

Ille g a l b u t d e c r im in a liz e d N o in fo r m a tio n

* O n ly w ith p r e s c r ip tio n o f s p e c ia lis t d o c to r

Ille g a l b u t u n e n fo r c e d

Regulatory Outlook

Exemptions for Medical Use

• The US does not show a sign of uniform legislation on the near term,

although states are increasingly moving toward recreational use and

robust medical use programs. The preponderance of states have

legalized cannabis in some capacity, and only a single digit few still

enforce misdemeanor possession laws on the books;

• In Canada, legislation allowing for national adult use is set to take

effect on October 17, 2018, with nationwide dispensaries and other

distribution outlets set to open to an eager adult use population;

• Experience in the US and Canada suggests that, once in place,

medical cannabis laws are difficult to repeal, which may be due to a

multitude of factors such as acceptance by the population at large,

M e d ic a l U s e L a w s in P la c e

increased tax revenues, lower healthcare spending, and other social

S o u r c e s : U N O D C , D E A , F r o n tie r F in a n c ia ls G lo b a l L e g a l C a n n a b is R e p o r t.

and economic considerations. 6The Dutch Model – The Office of Medicinal Cannabis (“OMC”)

• Established 2000;

• Part of the Dutch Health Ministry;

• Responsible for production, distribution

(export) and quality;

• Mandator of Bedrocan Nederland (Dutch

licensee of Bedrocan International);

• Monopoly on trade of all raw cannabis

(similar to production of poppies);

• www.cannabisbureau.nl (EN pages too).

7Regulatory and Commercial Landscape

United States Canada Netherlands Europe

N in e (9 ) s ta te s h a v e p a s s e d fe d e ra l le g is la tio n fo r

S c h e d u le 1 N a rc o tic in th e C S A ; S c h e d u le 2 N a rc o tic in th e C S A G o v e rn m e n t a s c o u n te rp a rty c re a te s p a rtn e rs h ip &

Federal Regulation / A d v e rs e E x e c u tiv e b ra n c h & e n fo rc e m e n t p o lic y ;

M e d ic a l u s e le g a liz e d s in c e 2 0 0 2 / re c re a tio n a l u s e

le g itim a c y ;

m e d ic a l c a n n a b is c o n s u m p tio n (B I h a s lo n g

s ta n d in g re la tio n s h ip s w ith e a c h ju ris d ic tio n );

Enforcement Policy a llo w e d fro m O c to b e r 1 7 2 0 1 8

N o n -c o m p lia n t w ith U N tre a tie s

S c a le & in te rs ta te c o m m e rc e p ro h ib ite d G o v ’t to G o v ’t (“G 2 G ”) s u p p ly c h a in ; P u b lic / P riv a te p a rtn e rs h ip s

F u ll d e p o s ito ry , w ire , tre a s u ry s e rv ic e s b y m u ltip le F u ll d e p o s ito ry , w ire , tre a s u ry s e rv ic e s b y m u ltip le F u ll d e p o s ito ry , w ire , tre a s u ry s e rv ic e s b y m u ltip le

Access to Banking / L im ite d a n d in c o n g ru e n t a c c e s s (o fte n a t g lo b a l in v e s tm e n t a n d m e rc h a n t b a n k s ;

R e v o lv in g , p ro je c t fin a n c e , a n d re a l e s ta te fa c ilitie s

g lo b a l in v e s tm e n t a n d m e rc h a n t b a n k s ;

R e v o lv in g , p ro je c t fin a n c e , a n d re a l e s ta te fa c ilitie s

g lo b a l in v e s tm e n t a n d m e rc h a n t b a n k s ;

R e v o lv in g , p ro je c t fin a n c e , a n d re a l e s ta te fa c ilitie s

Depository Services c o n s id e ra b le p re m ia ) b e tw e e n / a m o n g th e s ta te s

a v a ila b le a t c o m m e rc ia l ra te s ; a v a ila b le a t c o m m e rc ia l ra te s ; a v a ila b le a t c o m m e rc ia l ra te s ;

N o a d v e rs e ta x N o a d v e rs e ta x N o a d v e rs e ta x

Tax Considerations § 2 8 0 E D e d u c tio n L im ita tio n

A c c e s s to a g ric u ltu ra l, b io te c h , a n d p h a rm a A c c e s s to a g ric u ltu ra l, b io te c h , a n d p h a rm a A c c e s s to a g ric u ltu ra l, b io te c h , a n d p h a rm a

s u b s id ie s a n d g ra n ts s u b s id ie s a n d g ra n ts s u b s id ie s a n d g ra n ts

+ 1 1 8 L ic e n s e s Is s u e d – fre e m a rk e t p o lic y ; P re fe rre d p ro v id e r to O M C fo r fifte e n (1 5 ) y e a rs ; L im ite d lic e n s in g

D is p a ra te lic e n s in g re g im e s b e tw e e n / a m o n g

s tric t re g u la tio n s to p ro h ib it d iv e rs io n a n d to P u b lic te n d e r d is b u rs e d e v e ry 3 -5 y e a rs ;

Licensing s ta te s g u a ra n te e m in im u m q u a lity ; S e p a ra te te n d e rs fo r m e d ic a l & re c re a tio n a l u s e to In d o o r C u ltiv a tio n ; 3 + y e a r h is to ry o f C O A s ;

N o s tric t s e p a ra tio n m e d ic a l/re c re a tio n a l b e ra tifie d in 2 0 1 9 C h e m ic a l p ro file s s im ila r to B I C u ltiv a rs ;

Quality and “C o m p a s s io n a te U s e ” N o n -p h a rm a c e u tic a l re g u la tio n (A C M P R ) S tric t S ta n d a rd iz a tio n to G A C P a n d G M P

S tric t s ta n d a rd iz a tio n a s m e d ic a l c a n n a b is v ie w e d

standardization (n o s ta n d a rd iz a tio n re g u la tio n ) F o r m e d ic in a l a n d re c re a tio n a l u s e (N o n -c o n fo rm in g c ro p s d e s tro y e d )

a s a p h a rm a c e u tic a l p ro d u c t in E U ;

Requirements G A C P a n d G M P s ta n d a rd iz a tio n

Total Addressable 3 3 0 m illio n * 3 7 m illio n 1 7 m illio n 7 5 0 m illio n

Market (Population)

Total Addressable $ 5 0 -5 5 b illio n (1) $ 4 .3 – 7 .5 b illio n (2) $ 1 .5 – 3 .0 b illio n (3) $ 1 0 0 -1 2 5 b illio n (4)

Market ($)

(1 ) M a r i ju a n a B u s i n e s s D a i l y E s t i m a t e d D e m a n d , l e g a l a n d b l a c k m a r k e t .

(2 ) B N N B lo o m b e r g ; C a n a d a ’s le g a l c a n n a b is m a r k e t b y t h e n u m b e r s

(3 ) O p e n S o c ie t y F o u n d a t io n e s t im a t e s > $ 4 0 0 m illio n in t a x r e c e ip t s b y D u t c h A u t h o r it ie s in 2 0 1 3 f r o m c o f f e e - s h o p s ..

(4 ) In d u s t r y e s t im a t e s b a s e d o n p o p u la t io n , g e o g r a p h y , a n d p r o p r ie t a r y m a r k e t r e s e a r c h .

8Views on European Cannabis Market

European cannabis market Select Forecast

• Europe is destined to become the world’s largest medical cannabis

market because the Continent will require fully registered cannabis

medicines in its market, and will hold those medicines to

pharmaceutical and GMP standards throughout.

• Driven in large part by pharmacies and physicians, European

cannabis agencies will enforce Good Manufacturing Practices

(“GMP”) and public healthcare coverage policies that will ensure high

standards from the cannabis industries. Only companies that are

able to meet and maintain these high standards, will survive in the

European cannabis industry.

• Recreational cannabis is very unlikely to become widely regulated in

Europe as it is in the US and Canada, as the compassionate use

systems of the Western Hemisphere are unlikely to cross the ocean

to Europe.

Unique position

Bedrocan is likely to become the key-cultivator because:

• Nearly three decades of experience in cultivating top-quality medical

cannabis in the most scrutinized government-to-government

supply chain on the planet;

• Assisted governments around the world in understanding the Dutch

Framework of cannabis regulation, and seeks to export regulatory

influence and commercial discipline in every new market it enters;

• Acquired GMP certification for its whole cultivation process.

930 years in business

10Global presence (Office or facility)

N e th e rla n d s

1984 C ze c h R e p

2014

*C a n a d a

USA

2014

2015

*B ra zil

2016

A u s tra lia

2016

B e d ro c a n c u rre n t p re s e n c e

11

*Jurisdiction subject to moratorium between Canopy and BedrocanExportation to the world

*B ra z il

*C a n a d a

N e th e rla n d s

Ita ly

P o la n d

Is ra e l

D e n m a rk

F in la n d

A u s tria

G e rm a n y

M a c e d o n ia

N o rw a y

Sw eden

C ze c h R e p

U n ite d K in g d o m

S w itz e rla n d

A u s tra lia

M a lta

B e d ro c a n c u rre n t p re s e n c e

12

*Jurisdiction subject to moratorium between Canopy and BedrocanCorporate Partnerships

Pharma Research Organizations

Governments Academic

13Professional Team and Industry Advisors

Legal Financial

Consulting Other

14Questions?

15Corporate

Overview

Tjalling Erkelens Mauricio Agudelo, JD CFA

Founder, Chairman, and CEO Chief Financial Officer

t.erkelenes@bedrocan.com m.agudelo@bedrocan.com

16You can also read