DEALERSHIP OF PART 2: THE FUTURE - By Glenn Mercer Commissioned by NADA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DEALERSHIP By Glenn Mercer

Commissioned by NADA

OF

TOMORROW PART 2: THE FUTURE

OUR BIAS: FORECASTS OVERSHOOT

IN THE LAST 25 YEARS AUTOMOTIVE PUNDITS* HAVE PREDICTED THAT BY NOW:

CARS WILL BE BUILT-TO-ORDER... BUT INVENTORIES STAY AT 60 DAYS

PUBLIC CHAINS WILL SWEEP THE BOARD… BUT THEY ARE STUCK AT 9% M/S

EQUILIBRIUM

DEALERSHIPS WILL BECOME MULTI-BRANDED… NOT AT ALL

RATHER THAN

OEMs

EXTRAPOLATION

WILL CONSOLIDATE DOWN TO 5-6… BUT INSTEAD THEY PROLIFERATE

WE’LL HIT “PEAK DRIVING”… AND IT DOES PAUSE, THEN RESUMES GROWTH

ELECTRIC VEHICLES WILL DOMINATE… CURRENTLY AT 0.6% M/S

MILLENNIALS WON’T BUY CARS… UNTIL THEY’RE THE BIGGEST SEGMENT

…

* Including me!

THE 4 HORSEMEN OF THE APOCALYPSE

THE 4 HORSEMEN OF THE CARPOCALPYSE

Electric Vehicles (EVs): Autonomous Vehicles (AVs): Mobility Services (MS): The Connected Car (CC):

FORECAST: Penetration by FORECAST: By 2025 ~100% of FORECAST: Highly uncertain. FORECAST: Already well

2025 of ~5% (PHEV+BEV) new cars have high levels of IMPACT: As configured today under way, as relatively cheap

TODAY ~1% ADAS; 50% with partial (taxi’s, limo’s), modest head- and easy to do. 50% TODAY?

IMPACT: Minimal: dealers can autonomy (TODAY 1% @ L2); wind to sales (TODAY 1% OF 100% by 2025.

handle EV as easily as and 10% capable of often VMT). But if AVs and MS are IMPACT: Impact modestly

gasoline, diesel, more. driving in this mode. linked up (“robotaxis”), we favorable, as CC is tied more

IMPACT: Probably positive: enter a world of “eternal closely to the dealership).

AVs likely to boost VMT and rental.” Implications highly

may very well boost new sales unclear. Lower sales but

(e.g. elderly or disabled), likely higher VMT. Unclear who will

age faster. But slow to do the maintenance!

penetrate total parc.

A FACT: MONEY IS POURING IN

THE 4 HORSEMEN OF THE CARPOCALPYSE

Electric Vehicles (EVs): Autonomous Vehicles (AVs): Mobility Services (MS): The Connected Car (CC):

FORECAST: Penetration by FORECAST: By 2025 ~100% of FORECAST: Highly uncertain. FORECAST: Already well

2025 of ~5% (PHEV+BEV) new cars have high levels of IMPACT: As configured today under way, as relatively cheap

TODAY ~1% ADAS; 50% with partial (taxi’s, limo’s), modest head- and easy to do. 50% TODAY?

IMPACT: Minimal: dealers can autonomy (TODAY 1% @ L2); wind to sales (TODAY 1% OF 100% by 2025.

handle EV as easily as and 10% capable of often VMT). But if AVs and MS are IMPACT: Impact modestly

gasoline, diesel, more. driving in this mode. linked up (“robotaxis”), we favorable, as CC is tied more

IMPACT: Probably positive: enter a world of “eternal closely to the dealership).

AVs likely to boost VMT and rental.” Implications highly

may very well boost new sales unclear. Lower sales but

(e.g. elderly or disabled), likely higher VMT. Unclear who will

age faster. But slow to do the maintenance!

penetrate total parc.

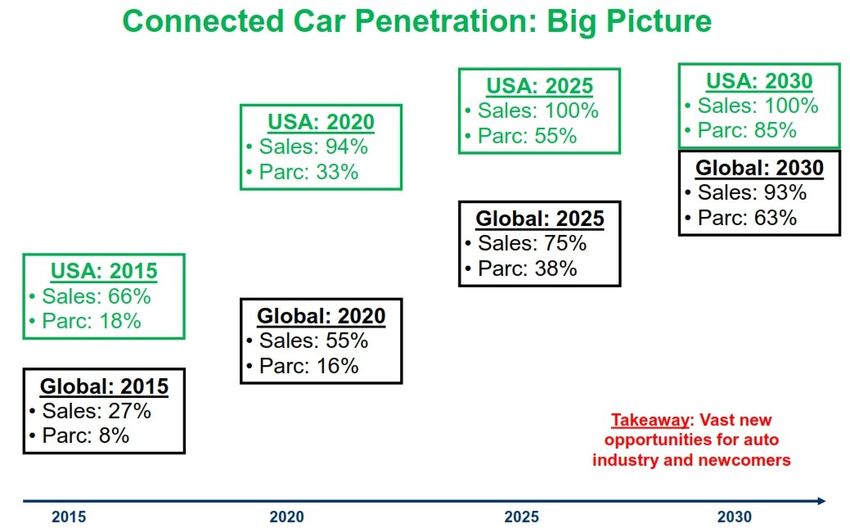

CONNECTED CAR: “INEVITABLE”

CORE ISSUE: VAST AMOUNTS OF

DATA GENERATED, BUT HOW

MUCH IS IT WORTH?

(Is it already in the phone?)

THE 4 HORSEMEN OF THE CARPOCALPYSE

Electric Vehicles (EVs): Autonomous Vehicles (AVs): Mobility Services (MS): The Connected Car (CC):

FORECAST: Penetration by FORECAST: By 2025 ~100% of FORECAST: Highly uncertain. FORECAST: Already well

2025 of ~5% (PHEV+BEV) new cars have high levels of IMPACT: As configured today under way, as relatively cheap

TODAY ~1% ADAS; 50% with partial (taxi’s, limo’s), modest head- and easy to do. 50% TODAY?

IMPACT: Minimal: dealers can autonomy (TODAY 1% @ L2); wind to sales (TODAY 1% OF 100% by 2025.

handle EV as easily as and 10% capable of often VMT). But if AVs and MS are IMPACT: Impact modestly

gasoline, diesel, more. driving in this mode. linked up (“robotaxis”), we favorable, as CC is tied more

IMPACT: Probably positive: enter a world of “eternal closely to the dealership).

AVs likely to boost VMT and rental.” Implications highly

may very well boost new sales unclear. Lower sales but

(e.g. elderly or disabled), likely higher VMT. Unclear who will

age faster. But slow to do the maintenance!

penetrate total parc.

CURRENT “SCRAMBLED” VIEW OF EVS

THE COMBINATION OF LOW VOLUMES, FAST GROWTH, AND (AS WE

SHALL SEE) PERVASIVE STATE INTERVENTION ALONG WITH RAPIDLY

SHIFTING ECONOMICS MAKES FOR WIDELY DIVERGENT

CORE ISSUE: RECENT

IRRESISTABLE

FORECASTS SUPPLY FORCE (GOV’T

REGULATION) MEETS

(EXAMPLES ARE USA PEV MARKETIMMOVABLE

2025 SHAREDEMAND

PREDICTIONS):

OBJECT

(CONSUMER PREFERENCES)

1 MILLION; 5%; 800,000; 1.5 MILLION; 10%; 1.5%; 6%; 10%; 2-3%

SOURCES (SCRAMBLED): WORLD ENERGY COUNCIL, EPA/NHTSA,

NAVIGANT, BLOOMBERG, THE EV TECHNOLOGY CENTER,

GOVERNMENT OF THE UK, JATO DYNAMIS, IEA, UBS

SUPPLY “PUSH” BROADLY SPEAKING, THERE ARE 3 SUPPLY “PUSH” FACTORS: 1. GOV’T ACTION: KEY: political will is driving China hard 2. GOV’T ACTION: KEY: policies everywhere attack emissions 3. TESLA AND DIESEL EFFECTS: KEY: Tesla shook every OEM vis-à-vis EVs in the same way Prius shook them regarding hybrids KEY: “Dieselgate” has accelerated German OEM move into EV

SUPPLY PUSH: ARE INCENTIVES SUSTAINABLE?

DEMAND “PULL” SUMMARY BROADLY SPEAKING, THERE ARE 3 DEMAND “PULL” FACTORS: 1. ECONOMICS: KEY: more or less competitive with ICE 2. OFFERINGS: KEY: expanding and offering 3. PERFORMANCE: KEY: car and network improving … YET (US) CONSUMER VIEWS REMAIN DECIDEDLY MIXED: DEPENDING ON SURVEY SOURCE, INTEREST IN EVS IS EITHER NOT GROWING OR ACTUALLY FALLING

RESULT: EV FORECAST STRONG SUPPLY PUSH IMPELS OEMs TO PRODUCE EVs… … BUT WEAK DEMAND PULL MAKES THEM HARD TO SELL RESULT FOR NOW IS THAT EVERY BEV LOSES MONEY* FALLING COSTS OF BATTERIES (PLUS RISING COST OF ICE EMISSIONS TECH) IMPLY REACHING OEM ICE/EV BREAK-EVEN IN THE FUTURE: EUROPE BEFORE 2020 (DUE TO HIGH FUEL TAXES, SMALL CARS) CHINA BEFORE 2025 (DUE TO GOVERNMENT ACTIONS) USA AFTER 2025 (DUE TO CHEAP FUEL, HEAVY VEHICLES) …WITH PROFITS IN EACH CASE SOME 3-5 YEARS THEREAFTER * NB: low-end Chinese EVs may be profitable now; recall that consumer TCO does not directly tie to OEM profits, thanks to incentive payments; and luxury OEMs will turn profitable in EVs faster than will volume producers.

TBC FORECAST 2025

Region Ʃ Vehicles Mild H HEV PHEV + BEV = “EV” ICE

W Europe 15 mm 25% 7 5 10 15 53

USA 15 3 5 4 2 6 86

China 35 5 2 6 20 26 67

IMPACT ON DEALERS:

Japan 5 2 30 1. 3 Must learn

2 to sell EVs,

5 or risk63

being seen as anti-environment!

ROW 33 3 4 1 2 3 90

2. Recognize that lifetime service

Total 103 7 5 4 revenue

7 will be11lower 75TECHNOLOGY OUTLOOK: “4 HORSEMEN”

Electric Vehicles (EVs): Autonomous Vehicles (AVs): Mobility Services (MS): The Connected Car (CC):

FORECAST: Penetration by FORECAST: By 2025 ~100% of FORECAST: Highly uncertain. FORECAST: Already well

2025 of ~5% (PHEV+BEV) new cars have high levels of IMPACT: As configured today under way, as relatively cheap

TODAY ~1% ADAS; 50% with partial (taxi’s, limo’s), modest head- and easy to do. 50% TODAY?

IMPACT: Minimal: dealers can autonomy (TODAY 1% @ L2); wind to sales (TODAY 1% OF 100% by 2025.

handle EV as easily as and 10% capable of often VMT). But if AVs and MS are IMPACT: Impact modestly

gasoline, diesel, more. driving in this mode. linked up (“robotaxis”), we favorable, as CC is tied more

IMPACT: Probably positive: enter a world of “eternal closely to the dealership).

AVs likely to boost VMT and rental.” Implications highly

may very well boost new sales unclear. Lower sales but

(e.g. elderly or disabled), likely higher VMT. Unclear who will

age faster. But slow to do the maintenance!

penetrate total parc.PEAK AV HYPE? A patent application published by the USPTO 9/2018 suggests that Walmart has at least considered the possibility of a self-driving shopping cart. The application depicts a Roomba-esque motorized device attached to the underside of a shopping cart. Customers use their smartphone or other mobile device to summon the cart; from there, it is controlled by a centralized computer, and navigates the store using its sensors.

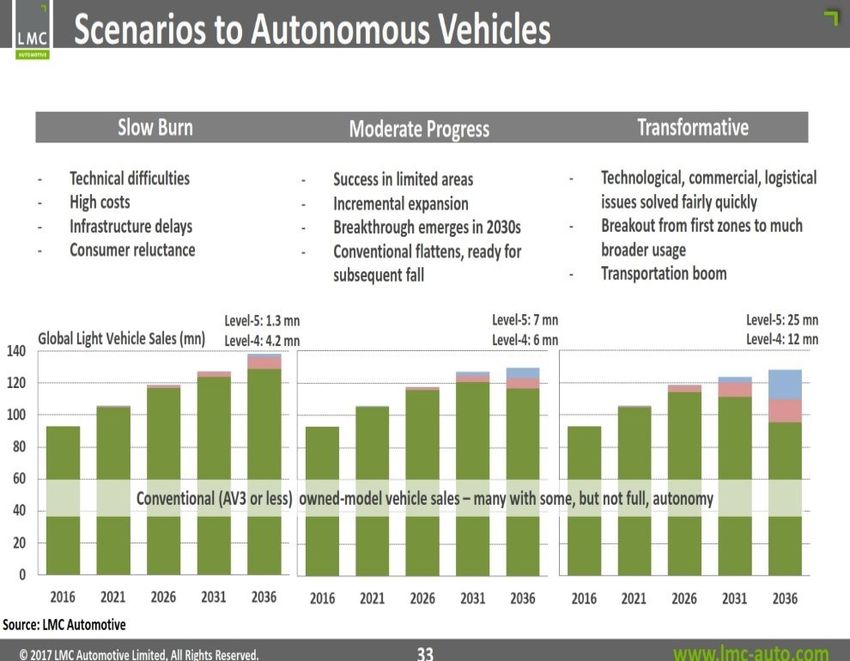

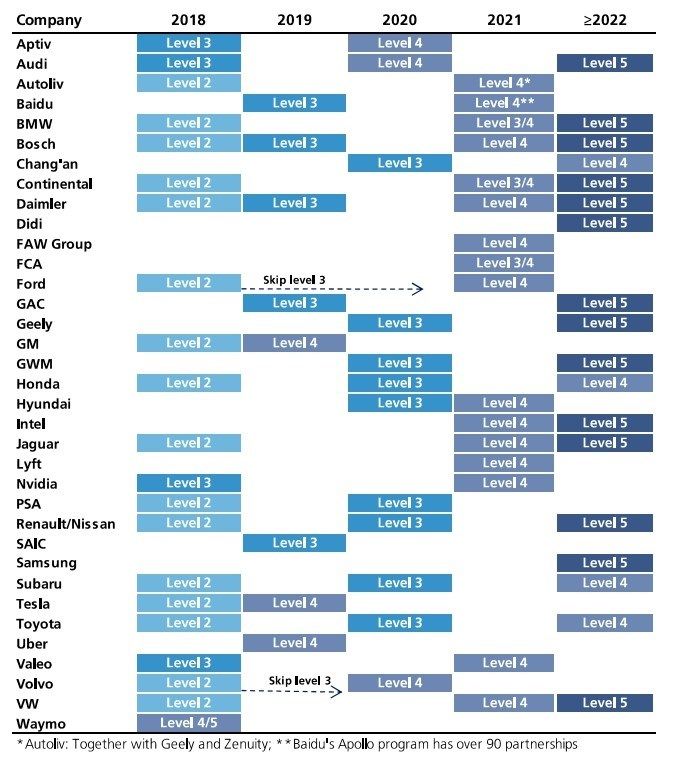

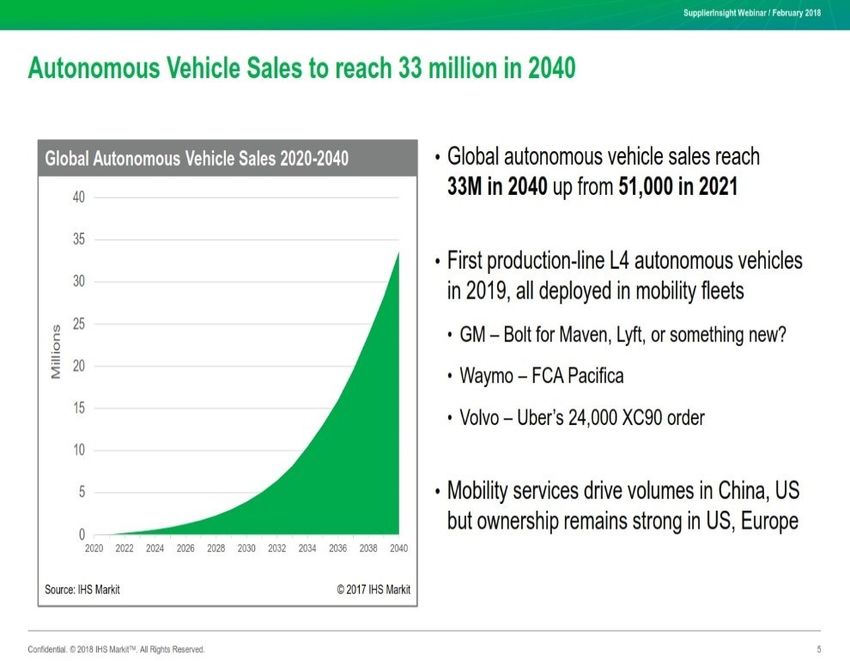

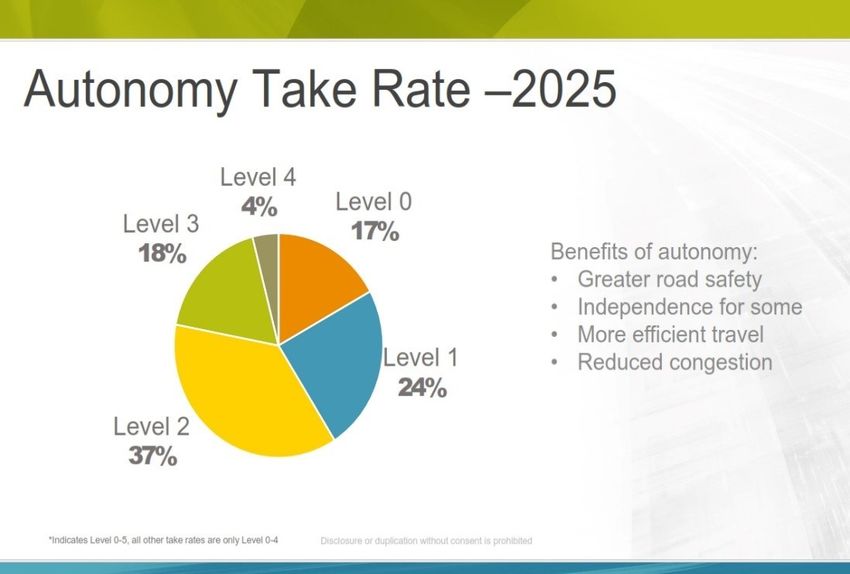

AUTONOMOUS VEHICLES INEVITABLE: THE DEBATE IS ONLY ABOUT SPEED OF PENETRATION THERE ARE HUGE DEFINITIONAL ISSUES! “AUTONOMOUS,” “SEMI- AUTONOMOUS,” “SELF-DRIVING,” “DRIVERLESS,” “ROBOCARS,” ETC. THE IMPACT ON DEALERS MAY BE POSITIVE: SALES: CAN GROW, AS THE ELDERLY AND DISABLED “GET BACK ON THE ROAD” SERVICE: COULD GROW, AS THESE VEHICLES ARE USED FOR MANY MORE MILES THERE IS ALMOST NO WAY TO PREDICT ALL THE EFFECTS OF AVs DECREASE TRAFFIC (SHARED ROBOTAXIS) OR INCREASE (ABANDON THE BUS)? REDUCE PARKING LOTS DOWNTOWN… BUT HAVE FOUR “RUSH HOURS?” HARMLESS SOCIAL EFFECTS (SEX IN THE CAR!) OR HARMFUL (DELIVER AN IED)?

AVS: FORECAST CONFUSION

CONFUSION ALSO DUE TO “LEVEL” ISSUE

REGIONAL VARIATIONS ALSO SIGNIFICANT

UNINTENDED EFFECTS WILL BE MANY!

My boss fired me, so for revenge I told

his AV to drive itself to North Korea!

Pyongyang A SOURCE OF CONFUSION: 2 PATHS, 1 END?

35

DEGREE OF AUTOMATION

AUTONOMY THE GOAL

30

25

20

AUTONOMY

15

WAYMO, UBER, A RESULT

GM/CRUISE?

10

MOST

5

OEMs

TIME

0AND FINALLY…

TECHNOLOGY OUTLOOK: “4 HORSEMEN”

Electric Vehicles (EVs): Autonomous Vehicles (AVs): Mobility Services (MS): The Connected Car (CC):

FORECAST: Penetration by FORECAST: By 2025 ~100% of FORECAST: Highly uncertain. FORECAST: Already well

2025 of ~5% (PHEV+BEV) new cars have high levels of IMPACT: As configured today under way, as relatively cheap

TODAY ~1% ADAS; 50% with partial (taxi’s, limo’s), modest head- and easy to do. 50% TODAY?

IMPACT: Minimal: dealers can autonomy (TODAY 1% @ L2); wind to sales (TODAY 1% OF 100% by 2025.

handle EV as easily as and 10% capable of often VMT). But if AVs and MS are IMPACT: Impact modestly

gasoline, diesel, more. driving in this mode. linked up (“robotaxis”), we favorable, as CC is tied more

IMPACT: Probably positive: enter a world of “eternal closely to the dealership).

AVs likely to boost VMT and rental.” Implications highly

may very well boost new sales unclear. Lower sales but

(e.g. elderly or disabled), likely higher VMT. Unclear who will

age faster. But slow to do the maintenance!

penetrate total parc.MOBILITY SERVICES: SOMETHING NEW?

The auto industry has been living

with “mobility services” for a long

time (Hertz was founded in 1918):

is this latest wave of innovations

fundamentally different?MOBILITY SERVICES

HIGHLY CONTROVERSIAL: HIGH ACTIVITY, LOW/NO (USA) PROFITS

IN CURRENT CONFIGURATION, A SMALL DRAG ON NEW-CAR SALES

(NB: IN THE USA MS+TAXI+LIMO = ONLY 1% VMT)

IF AV IS LINKED TO MS, THEN DRIVERS MAY GIVE UP CAR OWNERSHIP

IN FAVOR OF “ETERNAL RENTAL” OR “ROBOTAXIS” – AS A RESULT

SALES MIGHT FALL, ALTHOUGH SERVICE WILL LIKELY RISE

THIS ALREADY MAKES ECONOMIC SENSE IN LONDON AND NEW

YORK* -- THE QUESTION IS HOW FAR WILL IT SPREAD, HOW FAST?

THE REAL THREAT IS TRUE SHARING: IF RIDERS GO TOGETHER IN

ROBOTAXIS, NOW SALES START TO FALL.

* BUT NOTE THAT ~50% OF FAMILIES IN NYC AND LONDON STILL OWN A CARARITHMETIC OF MS - 1 1. ASSUME 10 PEOPLE DRIVE 1,000 KM/YEAR/PERSON, IN 10 CARS THAT COVER 1,000 KM/YEAR, AND WEAR OUT IN 5,000 KM; FOR 10 YEARS. TOTAL KM ARE 100,000, THUS 20 CARS SOLD (EACH LASTS 5,000 KM) AVERAGE CAR REPLACED EVERY 5 YEARS (5,000/1,000=5) 2. NOW ASSUME “ROBOTAXIS” THAT MAKE TRAVEL EASIER: 10 PEOPLE DRIVE 1,250 KM/YEAR/PERSON, IN CARS THAT LAST 5,000 KM, FOR 10 YEARS. BUT WE ONLY NEED 4 CARS AT ONCE (HIGHER UTILIZATION). TOTAL KM ARE = 125,000, THUS 25 CARS SOLD (EACH LASTS 5,000 KM) AVERAGE CAR REPLACED EVERY 4 YEARS (5,000/1,250=4) 3. “ROBOTAXIS” DO NOTHING TO REDUCE TRAVEL, AND PROBABLY INCREASE IT, SO IF CARS LAST SAME NUMBER OF KM EACH, WE SELL MORE CARS, AND MORE QUICKLY.

ARITHMETIC OF MS - 2

1. ASSUME 10 PEOPLE DRIVE 1,000 KM/YEAR/PERSON, IN 10 CARS THAT

COVER 1,000 KM/YEAR, AND WEAR OUT IN 5,000 KM; FOR 10 YEARS.

TOTAL KM ARE 100,000, THUS 20 CARS SOLD (EACH LASTS 5,000 KM)

2. NOW ASSUME “ROBOTAXIS” THAT MAKE TRAVEL EASIER: 10WILL

KEY QUESTION: PEOPLE

MOVE 1,250 KM/YEAR/PERSON, IN CARS THAT LAST

PEOPLE 5,000 TO

DECIDE KM,SHARE

FOR 10

YEARS. BUT WE ONLY NEED 4 CARS AT ONCE (HIGHER UTILIZATION).

RIDES?*

TOTAL KM ARE = 125,000, THUS 25 CARS SOLD (EACH LASTS 5,000 KM)

3. NOW ASSUME EVERY TRIP IS SHARED BY ON AVERAGE 2 PEOPLE: WE

SELL ONLY 12.5 CARS IN 10 YEARS

10 PEOPLE MOVE 1,250 KM ANNUALLY, BUT WITH 2 PEOPLE/CAR TOTAL KM

IN 10 YEARS ARE 62,500, CARS LAST 5,000 KM, WE SELL ONLY 12.5 CARS.

* China data point: 80% of Didi rides are 1 person; USA data point: carpool trips are ~4% of all trips.MS: ON THE OTHER HAND…

CARLOS GHOSN: “MANY THINK [MS] ARE SUBSTITUTION. NO, IT'S ADDITION. THE

TRADITIONAL BUSINESS OF BUILDING, SELLING, AND OWNING CARS CONTINUES.“

1. MS ARE NOT (YET) OFFERING ANYTHING TRULY NEW. JUST A FORM OF TAXI.

OEMS ARE INVESTING IN THEM JUST TO SECURE FLEET CONTRACTS

2. “CARS ARE IDLE 95% OF THE TIME” MISLEADS. THERE MUST BE IDLE CAPACITY

MOST OF THE TIME IF WETo

ALLborrow

TRAVELfrom Duke

AT ONCE professor

SOME Dan(RUSH

OF THE TIME Ariely,

HOUR)

3. mobility

“IT’S KM, NOT CARS!” REPLACEservices areKM/YEAR)

A CAR (25K like teenage

WITHsex: “Everyone

A TAXI (125K) AND IT

WEARS OUT FASTERtalks about

(3 YEARS it, nobody

VS 12), AND YOUreally knows

SELL AS MANYhow

CARSto do it,

ANYWAY!

4. MS SO FAR RARELY MAKESeveryone

MONEYthinks

(MAYBEeveryone else

IN BEIJING, is doing

WHERE it, soTO

IT’S HARD

everyone

GET A CAR), IN PART BECAUSE claimsWITH

MS COMPETES theySUBSIDIZED

are doing MASS

it.” TRANSIT.

5. MS VALUES EFFICIENCY EXCESSIVELY VERSUS EFFECTIVENESS: OWNING YOUR

VEHICLE CREATES VALUE MS CAN’T (E.G. INSTANT AVAILABILITY, CUSTOMIZA-

TION, STORAGE, FLEXIBILITY, CHAINED TRIPS, EXPENSE CONTROL, ETC.)MS SUPPLY: HOW TO MAKE MONEY?

Q42017: -$1.1 billion

Q12018: “only” -$0.6 billion

(after cutting driver pay by

$250 mm and R&D by the

same)

Source: Len ShermanMS DEMAND: HOW ROBUST IS IT?

So where are Uber or

Lyft?TECHNOLOGY OUTLOOK: “4 HORSEMEN”

NEUTRAL POSITIVE UNCLEAR/NEGATIVE NEUTRAL

Electric Vehicles (EVs): Autonomous Vehicles (AVs): Mobility Services (MS): The Connected Car (CC):

FORECAST: Penetration by FORECAST: By 2025 ~100% of FORECAST: Highly uncertain. FORECAST: Already well

2025 of ~5% (PHEV+BEV) new cars have high levels of IMPACT: As configured today under way, as relatively cheap

TODAY ~1% ADAS; 50% with partial (taxi’s, limo’s), modest head- and easy to do. 50% TODAY?

IMPACT: Minimal: dealers can autonomy (TODAY 1% @ L2); wind to sales (TODAY 1% OF 100% by 2025.

handle EV as easily as and 10% capable of often VMT). But if AVs and MS are IMPACT: Impact modestly

gasoline, diesel, more. driving in this mode. linked up (“robotaxis”), we favorable, as CC is tied more

CONFIDENCE: HIGH IMPACT: Probably positive: enter a world of “eternal closely to the dealership).

AVs likely to boost VMT and rental.” Implications highly CONFIDENCE: HIGH

may very

Two well boost

roads tonew sales unclear. Lower sales but

Supply pushing

Revising the same

(e.g. elderly end? likely

or disabled), higher VMT. Unclear

demand?who will

do the maintenance! “Done deal”

upwards age faster. But slow to

penetrate total parc. CONFIDENCE: LOW

CONFIDENCE: HIGHCLOSING THOUGHTS FROM A DEALER PERSPECTIVE: 1. CONNECTED CAR IS A “DONE DEAL” NOW, AND GENERALLY POSITIVE 2. EVs ARE REAL, SOON, SLIGHT NEGATIVE; THE DEBATE IS OVER SPEED 3. AVs WILL BE REAL, SOMEDAY, LIKELY POSITIVE; SAME DEBATE 4. MS MAY BE REAL; SHARED ROBOTAXIS COULD BE A MAJOR THREAT; THE DEBATE IS HOW ECONOMICS AND HUMAN BEHAVIOR WILL INTERACT

THANK YOU! For comments and questions: gmercer2@gmail.com

You can also read