Demand-Supply Dynamics of Asia's Healthcare Sector - CFA ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

11 January 2018

Market Updates

Demand-Supply Dynamics of Asia’s Healthcare Sector

Asia’s accelerated ageing rates and the rise of lifestyle diseases will likely boost the region’s

healthcare spending outlook in coming decades, while in supply terms, the region’s medical

facilities, equipment and manpower will continue to trail the per capita averages of the 34 OECD

member countries. SGX-listed healthcare plays that derive significant revenues from markets

beyond Singapore have exposure to these robust demand-supply dynamics.

Singapore’s listed healthcare sector, as tracked by the benchmark SGX All-Healthcare Index,

consists of 30 companies and related trusts with a combined market capitalisation of more than

S$34 billion. Seven of the 10 largest constituents of the Index report more than a third of group

revenues to Asia Pacific ex-Singapore, namely Southeast Asia, North Asia and South Asia.

Healthcare stocks posted a mixed performance in 2017, as funds rotated out of defensives into

cyclical plays. However, the tide has turned over the last few weeks, making Healthcare the best-

performing sector on a market capitalisation-weighted basis in the month of December, and

positive momentum continuing into the New Year.

Opportunities and challenges abound within the demand and supply dynamics of Asia’s healthcare services

industry. In terms of demand drivers, Asia’s growing population is ageing. Rising affluence and a surge in

lifestyle diseases are additional key structural drivers. On the supply side, the number of doctors, nurses,

hospitals and medical equipment still trail the per capita averages of the 34 OECD member countries. With

many Asian emerging economies grappling with limited fiscal funding, there is an increasing role for

corporations to engage in these opportunities and challenges.

Investors can participate in the structural Asian healthcare theme through SGX-listed healthcare stocks,

which are rapidly expanding into regional and global markets to meet growing patient needs.

Accelerated Ageing Rates

Asia’s demographics are favourable for the region’s healthcare spending outlook. According to the

International Monetary Fund (IMF), East Asia – which includes China, Hong Kong, Japan, North and South

Korea, Mongolia, Macao and Taiwan – is ageing faster than anywhere else in the world, with its old-age

dependency ratio roughly tripling by 2050.

Japan is the world’s most-aged country, with an old-age dependency ratio of 43.3% at the end of 2015, with

this figure forecast to rise to 70.9% by 2050, the IMF wrote in its Asia-Pacific economic outlook report

published last Spring. For Hong Kong, the end-2015 figure was 20.6%, and is projected to rise to 64.6% by

2050, while the equivalent figures for China are 13.1% and 46.7% respectively, the IMF noted. As for South

Korea, the country will become a “super-aged” society by 2030, with 24.5% of the population over the age of

65, according to projections by the Bank of Korea.

East Asia’s Old-Age Dependency Ratios Set to Surge in Next Three Decades Rise of Lifestyle Diseases In its 2018 Global Health Care Outlook report, Deloitte noted that rapid urbanisation, sedentary lifestyles, changing diets, and rising obesity levels are fuelling a surge in lifestyle diseases – most notably, cancer, heart disease, and diabetes. China and India have the largest number of diabetes sufferers in the world, at around 114 million and 69 million respectively, while globally, the number is expected to rise from the current 415 million to 642 million by 2040, Deloitte noted. According to OECD, cancer is the second leading cause of death after cardiovascular disease in the Asia Pacific region. Increasing Healthcare Expenditure In line with these factors, global healthcare spending is projected to increase at an annual rate of 4.1% between 2017 and 2021, up from just 1.3% between 2012 and 2016, the Deloitte report noted. In Asia, the share of government spending in healthcare is estimated to be on average one-third less than that of the OECD average, other studies showed. As for Singapore, government expenditure on healthcare is expected to accelerate over the next three to five years – rising by at least S$3 billion by 2020 from current levels, Finance Minister Heng Swee Keat said last month. Global Healthcare Spending Forecast to Rise

The rapid emergence of the middle class in Asia could also turn the region into a consumption powerhouse, and have far-reaching implications on healthcare demand. According to OECD estimates, two-thirds of the global middle class – defined as households with daily expenditures of US$10-US$100 per person in 2005 purchasing power parity (PPP) terms – will be residents of the Asia-Pacific region, with China home to the largest share of this demographic. Regional Supply Shortfall In terms of medical technology, equipment and manpower, Asia suffers a shortfall compared with the developed markets. According to OECD data, Asia has 1.2 doctors per 1,000 people, compared to 3.2 for the OECD average, and 2.8 nurses per 1,000 people compared to 8.7 for the OECD average. The number of hospital beds per person for Asia is also almost a third less than the OECD average. Asia has less tomography scanners, MRI units, mammography units and radiation therapy units versus the OECD average. The region’s demand drivers, coupled with the current shortfall in comparative services, supplies and technology, offer opportunities for increased participation by Singapore-listed providers and suppliers in the region’s healthcare sector. Healthcare Sector Benchmark The SGX All Healthcare Index is a free-float, market capitalisation-weighted index that measures the performance of Singapore’s listed healthcare sector. Currently, the five largest components by index weight are Top Glove (15.4%), Parkway Life REIT (10.1%), Haw Par Corp (9.9%), First REIT (9.7%), IHH Healthcare (9.5%). These five stocks make up more than half the index. For calendar year 2017, the SGX All Healthcare Index registered a price gain of 9.5%, compared with the MSCI AC Asia Health Care Index’s 16% gain in Singapore dollar terms. Between January and September last year, institutional investors were net-sellers of Singapore healthcare stocks, as funds rotated out of defensive stocks into cyclical plays. However, the tide turned in the last quarter of 2017, as selected healthcare plays with exposure to recovering consumer sentiment rebounded, making Healthcare the best- performing sector on a market capitalisation-weighted basis for the month of December. SGX All-Healthcare Index vs MSCI AC Asia Health Care Index in 2017 The 10 largest constituents of the SGX All-Healthcare Index comprise three healthcare providers, two medical equipment providers, two pharmaceutical companies, and three healthcare REITs, and have a combined market capitalisation of over S$31 billion. They are: IHH Healthcare, Raffles Medical Group and Talkmed Group, Top Glove and Riverstone Holdings, Haw Par and Tianjin Zhongxin Pharmaceutical, Parkway Life REIT, First REIT and RHT Health Trust.

Expanding Geographical Reach

Seven of the 10 largest constituents of the SGX All-Healthcare Index report more than a third of their group

revenues to Asia Pacific, ex-Singapore. They have operations and assets that span the following geographical

markets: Singapore, Malaysia, Vietnam, Thailand, Cambodia, Brunei, Indonesia, Hong Kong, China, Japan,

South Korea, Bangladesh, India, Turkey, Bulgaria, and Macedonia.

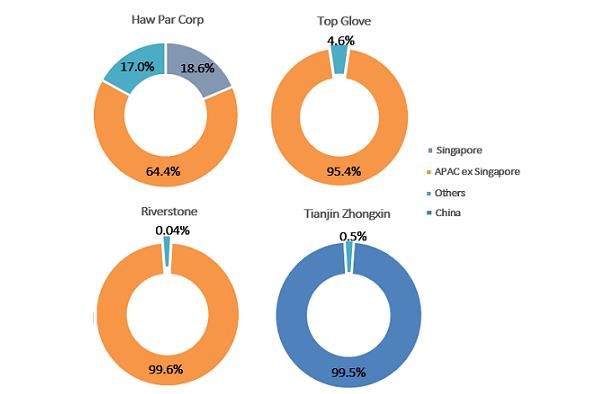

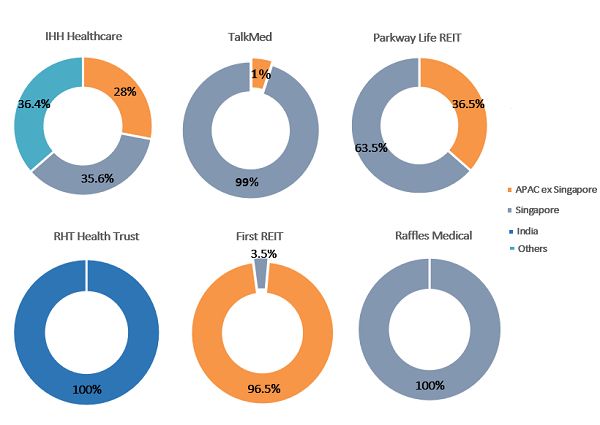

Healthcare Service Providers – Revenue Breakdown by Geography (%)

Notes:

Although Raffles Medical Group derives 100% of group revenue from Singapore, it has recently set

up operations in Hong Kong and Shanghai, and acquired clinics in Vietnam and Cambodia. It now has

a presence in 13 cities in Asia.

IHH Healthcare’s APAC ex-Singapore exposure comprises medical centre and hospital operations in

China, Hong Kong, India, Brunei and Malaysia, while its EMEA exposure comprises Iraq, United Arab

Emirates, Turkey, Bulgaria and Macedonia.

Talkmed’s APAC ex-Singapore exposure comprises medical oncology and stem cell transplant

services in Hong Kong, Vietnam and Indonesia.

Parkway Life REIT’s APAC ex-Singapore exposure primarily comprises hospital, medical centre and

nursing home operations in 14 prefectures in Japan and Malaysia.

First REIT’s APAC ex-Singapore exposure comprises hospital operations in Indonesia and a nursing

facility in South Korea.

Source: Company data and annual reportsHealthcare Equipment and Product Suppliers – Revenue Breakdown by Geography (%)

Source: Company data and annual reports

Note: Healthcare equipment suppliers export their products globally, while their manufacturing and/or sales

offices are located throughout Asia Pacific, USA and/or Europe.

Did You Know?

SGX’s healthcare sector comprises 30 listed healthcare companies and healthcare-related trusts with a

combined market capitalisation of more than S$34 billion. Healthcare Providers form the largest sub-

industry within the sector with 16 companies. The remaining 14 healthcare companies fall under various

sub-industries, including Healthcare Equipment, Pharmaceuticals, and Real Estate asset owners, according to

the Global Industry Classification Standard (GICS).

The 30 constituents of the SGX All-Healthcare Index are detailed below, sorted by market capitalisation. Click

on each stock name to access its profile in SGX StockFacts.

Name SGX Code Weight Market Gics Sub-Industry

(%) Cap

(S$M)

Top Glove Corp BVA 15.3 3,765 Healthcare Equipment & Services

Parkway Life REIT C2PU 10.2 1,791 Real Estate

Haw Par Corp H02 10.0 2,663 Pharmaceutical & Lifescience

First REIT AW9U 9.7 1,100 Real Estate

IHH Healthcare Q0F 9.5 16,067 Healthcare Equipment & Services

Raffles Medical Group BSL 9.1 1,930 Healthcare Equipment & Services

RHT Health Trust RF1U 7.5 666 Healthcare Equipment & Services

Riverstone Hldgs AP4 4.4 786 Healthcare Equipment & Services

Tianjin ZhongXin Pharmaceutical T14 4.2 2,029 Pharmaceutical & Lifescience

Health Management 588 3.8 566 Healthcare Equipment & Services

International

Q&M Dental Group QC7 3.6 525 Healthcare Equipment & Services

Singapore Medical Group 5OT 2.2 258 Healthcare Equipment & Services

TalkMed Group 5G3 2.1 900 Healthcare Equipment & ServicesCordlife Group P8A 1.2 202 Healthcare Equipment & Services

iX Biopharma 42C 1.1 118 Pharmaceutical & Lifescience

ISEC Healthcare 40T 1.0 163 Healthcare Equipment & Services

Singapore O&G 1D8 0.9 207 Healthcare Equipment & Services

Healthway Medical 5NG 0.7 263 Healthcare Equipment & Services

OUE Lippo Healthcare 5WA 0.6 201 Healthcare Equipment & Services

HC Surgical Specialists 1B1 0.6 107 Healthcare Equipment & Services

Techcomp Holdings T43 0.5 77 Healthcare Equipment & Services

Medtecs International Corp 546 0.4 26 Healthcare Equipment & Services

Aoxin Q&M Dental Group 1D4 0.4 76 Healthcare Equipment & Services

QT Vascular 5I0 0.3 28 Healthcare Equipment & Services

AsiaMedic 505 0.3 25 Healthcare Equipment & Services

Camsing Healthcare BAC 0.1 29 Retail

Star Pharmaceutical AYL 0.1 14 Pharmaceutical & Lifescience

UG Healthcare Corp 41A 0.1 38 Healthcare Equipment & Services

Suntar Eco-City BKZ 0.05 13 Pharmaceutical & Lifescience

Pharmesis International BFK 0.03 5 Pharmaceutical & Lifescience

Source: SGX StockFacts, Bloomberg (Data as of 10 January 2018)My Gateway SGX’s investor education portal with market, product and investment information and events. Sign up now at sgx.com/mygateway to receive our investment updates and economic calendar. www.sgx.com This document/material is not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject Singapore Exchange Limited (“SGX”) and/or its affiliates (collectively with SGX, the “SGX Group Companies”) to any registration or licensing requirement. This document/material is not an offer or solicitation to buy or sell, nor financial advice or recommendation for any investment product. This document/material has been published for general circulation only. It does not address the specific investment objectives, financial situation or particular needs of any person. Advice should be sought from a financial adviser regarding the suitability of any investment product before investing or adopting any investment strategies. Use of and/or reliance on this document/material is entirely at the reader’s own risk. Investment products are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not indicative of their future performance. Any forecast, prediction or projection in this document/material is not necessarily indicative of the future or likely performance of the product. Examples (if any) provided are for illustrative purposes only. While each of the SGX Group Companies have taken reasonable care to ensure the accuracy and completeness of the information provided, each of the SGX Group Companies disclaims any and all guarantees, representations and warranties, expressed or implied, in relation to this document/material and shall not be responsible or liable (whether under contract, tort (including negligence) or otherwise) for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of any kind, including without limitation loss of profit, loss of reputation and loss of opportunity) suffered or incurred by any person due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information, or arising from and/or in connection with this document/material. The information in this document/material may have been obtained via third party sources and which have not been independently verified by any SGX Group Company. No SGX Group Company endorses or shall be liable for the content of information provided by third parties (if any). The SGX Group Companies may deal in investment products in the usual course of their business, and may be on the opposite side of any trades. Each of SGX, Singapore Exchange Securities Trading Limited and Singapore Exchange Bond Trading Pte. Ltd. is an exempt financial adviser under the Financial Advisers Act (Cap. 110) of Singapore. The information in this document/material is subject to change without notice. This document/material shall not be reproduced, republished, uploaded, linked, posted, transmitted, adapted, copied, translated, modified, edited or otherwise displayed or distributed in any manner without SGX’s prior written consent. Please note that the general disclaimers and jurisdiction specific disclaimers found on SGX’s website at http://www.sgx.com/wps/portal/sgxweb/footerLinks/tos#panelhead21 are also incorporated into and applicable to this document/material.

You can also read