Depreciating rupee: Managing currency risk

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Depreciating rupee: Managing currency risk

Indian rupee in 2013 so far…

After remaining within the range of 50−55 during most of 2012, the Indian rupee continued to trade in the

same range until May 2013. One of the first major events that took place during that period was gold prices

crashing globally to close to 15% within a span of two trading sessions in April 2013. This sudden crash

triggered a surge in import of gold by India on account of the huge domestic demand. Data announced on May

13 indicated that the deficit witnessed on 13 April had increased by 72% over that announced on 13 March, on

cheap gold imports surge. Silver and gold imports were up by 138% to US$7.5 billion, as compared to last year,

and this continued to put pressure on the current account deficit. To add to the worry, S&P confirmed India’s

rating at BBB, with the negative outlook highlighting the uncertainty of the Government’s ability to support

investment growth. May 2013 saw the rupee losing over 5% against the US$ and crossing the INR56/US$ mark

after a year.

In mid June 2013, the US Federal Reserve’s Federal Open Market Committee (FOMC) hinted that it is likely to

begin tapering the country’s quantitative easing program in 2013 and wind it up altogether by mid 2014 if the

US economy witnesses the economic recovery expected. This was enough reason for global investors to pull out

money from most emerging markets and FII sold over US$6 billion in Indian debts and equities, putting further

pressure on Current Account Deficit (CAD) financing. Despite the Government’s measures to curb gold imports,

CAD hit a record high of US$87.7 billion (or 4.8% of India’s GDP) in fiscal year 2012/2013 (from US$78.2 billion

a year earlier) on increasing imports of oil and gold. For the second consecutive month, the rupee lost by more

than 5% in June 2013 and touched a psychological barrier of INR60/US$ for the first time, even after the RBI’s

intervention.

With currency market becoming extremely volatile, July 2013 can be considered the “RBI intervention month”

due to the RBI shifting its entire focus on managing the volatility in the country’s currency market. The market

continues to debate whether this was the right move. The RBI began squeezing short-term INR liquidity in the

market to curb speculative trading in the currency market and raised the Marginal Standing Facility and Bank

Rates by 200 bps to 10.25%. It also put a market-wide cap of INR75000 crores that banks can borrow daily

from it. A week after that, the RBI further tightened the liquidity of the rupee by reducing the overall limit for

borrowing from it to 0.5% of individual bank deposits. The RBI also made mandatory for banks to maintain 99%

(against 70%) of their daily cash reserve ratio (CRR) requirements with it. As a result of these measures, short-

term rupee interest rates shot up to over 200 bps and 10Y benchmark bonds yields up to 90 bps. However, this

had limited results with the rupee moderately appreciating from INR60/US$ to INR59/US$. In its widely

anticipated monetary policy initiated on 13 July, the RBI maintained all its policy rates unchanged. However,

with no further measures being taken by it and the continued pressure on CAD saw the rupee losing yet again,

although moderately. (All these measures helped the rupee lose only 1.73% on 13 July.)

The first few trading sessions on 13 August saw the rupee losing further ground, breaking a new psychological

barrier — INR61/US$ — and making it the worst performing Asian currency against the US$ at a loss of 13% in

2013.

Depreciating rupee: Managing currency risk 2What’s next for the Indian rupee…

It seems definite that the rupee will continue to be under pressure in the short term due to the volatility of the

currency market.

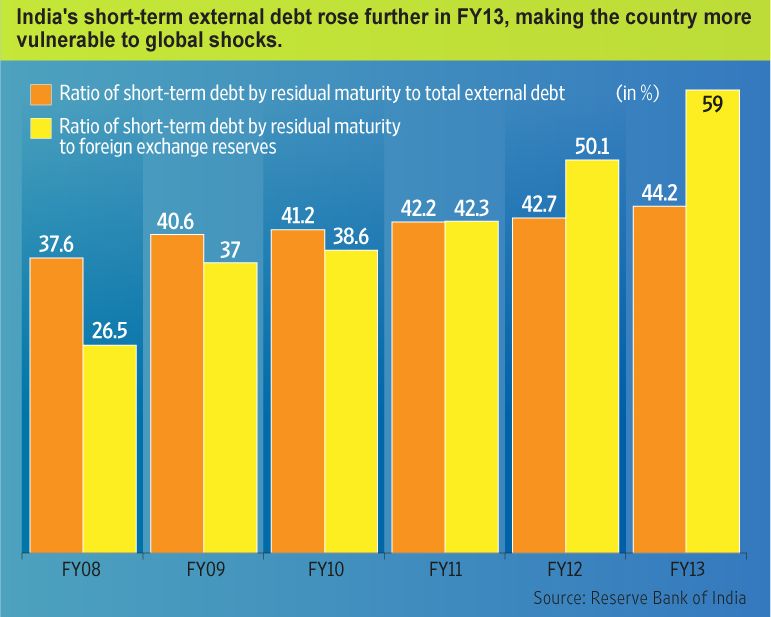

As of 2 August 2013, India’s forex reserves stood at US$280 billion — a three-year low after depletion of more

than US$16 billion since 13 May due to the RBI’s intervention at various levels to support the rupee. India’s

short-term debt, which will mature in March 2014, amounts to US$172 billion. The current account deficit

amounts to nearly 5% of the country’s GDP and much of its increased CAD has been funded by debt flows. It is

important to note that India’s short-term debt, which will mature in March 2014, constitutes nearly 60% of its

forex reserves. Theoretically this means that if India’s capital flows were to dry up due to some unforeseen

events and NRIs stopped renewing their deposits in the country, 60% of its forex reserves might need to be

deployed to pay back foreign borrowings due within a year. This will definitely restrict the RBI’s ability to

intervene in the forex market to prevent the rupee from depreciating further and put additional pressure on the

currency market.

Apart from meeting its debt-repayment obligation of US$172 billion by 31 March 2014, India needs another

US$90 billion of net capital flows to meet its current account deficit, which has been projected at 4.7 % of its

GDP by the Prime Minister’s Economic Advisory Council (PMEAC) for the 2013−14 fiscal.

As can be seen from the markets (as on 6 August 2013), the 1M US$/INR Fx Forward is trading at 62.23 (at an

all-time high premium of 52 paise) and the 1Y US$/INR Fx Forward is trading at 66.61 (at an all-time high

premium of 490 paise) over an all-time high spot of 61.70. This is a clear indication of the pressure building on

further weakening of the rupee.

Events to watch out for…

India clearly needs to attract more capital inflows to widen its CAD. The Government has already issued various

directives to curb import of gold. It has taken decisions on easing its FDI policy, issuing NRI bonds, global

events, e.g., the final print on “QE tapering.” In addition to this, every macro-economic data announcement

includes GDP-related data, CAD/trade deficit numbers and industrial output, Inflation has the potential to

adversely affect the performance of India’s equity market. Any data that is below expectations can trigger

losses in the equity market and put the rupee under further pressure.

Depreciating rupee: Managing currency risk 3Risk management

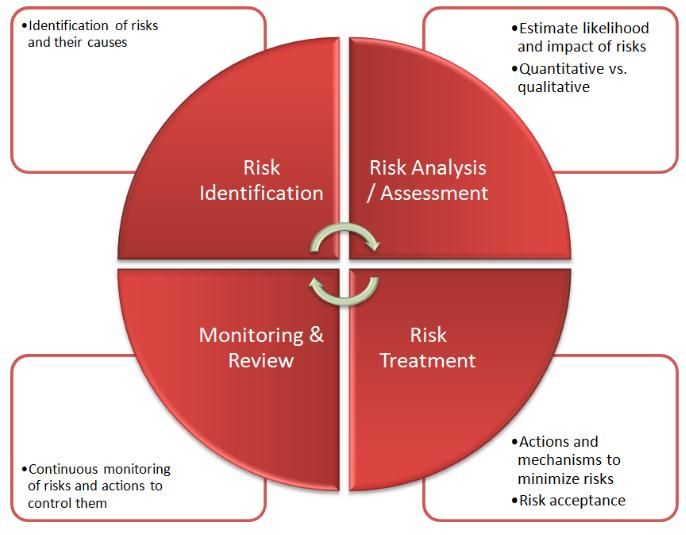

Risk management includes identification, assessment and prioritization of risks, followed by coordinated and

economical application of resources to minimize, monitor and control the probability and/or impact of

unfortunate events or maximize realization of opportunities. The following details the various stages involved:

Identification of risk

Financial markets are dynamic and efficient but unpredictable. It is extremely difficult to predict them, which

can result in risk for an organization. Considering the volatility witnessed in today’s currency market, it is

critical for management to first identify the risks faced by their organizations. Management of currency risk

must start with identification of economic exposure each company faces in its business.

For instance, an IT company, which is a natural IT exporter to US and European clients, will have a natural

exchange rate risk on US$ and €/£ vis-à-vis the rupee, since finally, what matters is its INR balance sheet.

Similarly an oil importer, whose typically billings are conducted in US$, will have exposure to the US$ against its

INR books in India. This looks fairly academic on paper, but it is extremely critical for management to

understand its organization’s business profiling, chain of operations and supply dependencies, and accordingly

identify its economic exposure to currency risk. It is pertinent to understand the nature of transactions

conducted by organisations, which lead to currency risk. To elaborate, in the case of foreign currency

borrowings/ECB, most companies look only at their exchange rate risk, but given that servicing of such loans is

dependent on interest rates, they should also focus on their interest-rate and currency risks.

Interest rate and currency risks, which are interlinked mathematically, are dependent on various factors.

Announcement of key macro-economic data in different currencies can adversely affect organizations’ interest

exchange rates. Some key data figures that typically affect interest and exchange rates include GDP-related and

inflation data, factory and industrial output, unemployment-related data and monetary policy announcements.

All such events need to be closely followed by management, since these can be a source of risk.

Depreciating rupee: Managing currency risk 4Measurement and control of risk

Having identified the risks, it is equally critical to measure them correctly. The simplest measure includes

quantifying the Net Open Position in different currencies. Most organizations are unable to exhaustively

quantify their exposure across various currencies. This requires a detailed understanding of a business, areas of

operations and how accounting of all transactions is executed. The CFO of an organisation should ensure that all

exposures are specifically accounted for and well represented in its treasury and integrated systems. Unless an

organization measures its currency positions correctly, it is impossible for further action to be taken by it. What

is of paramount importance in this procedure is the speed and transparency of information flow between the

organization’s finance, business and treasury functions.

Once risks are correctly measured, the next step is to determine how they should be manages. In common

parlance, the tool to manage risk is called “hedging.” Which instruments/products should be used for hedging

risks? It is extremely important to understand underlying risks that every derivative product carries. Just as

there are no free lunches, there are no “high rewards with low risks.” There are various derivative products

available for hedging currency risks, right from the simplest “Fx Spot/Forward to Fx Options” to complex

structured products. Every product has its own leveraging effect and costs associated with it. It is up to

management to understand, define its priorities, i.e., whether the ultimate objective is making P/L out of

currency fluctuations or real hedging and mitigate the risk of losing money. Markets work on “greed” and “fear”

and it is extremely important to find the right path through this without losing one’s focus on one’s real

objectives. The suitability and appropriateness of every product needs to be studied in light of organizational

goals before entering “new” business.

Control of risk, in a nutshell, refers to defining the risk appetite of an organization. At how much is an

organization willing to set its loss limit? Different levels of risks limits can be structured to ensure that no

individual can exceed its authority. Value at Risk Rigorous VaR & Stop Loss limits need to set and more

importantly, tracked and adhered to, regularly. Limits must be set on an organization’s exposure to different

currencies to restrict its operations to selected countries. CFOs should ensure a clear distinction between an

organization’s trading and hedging position, and ensure that while hedging trades, all supporting

documentation is in place to prove the hedge effectiveness of their organizations. It needs to be ensured that

the positions of all derivatives are mark-to-marketed (MTM) on a regular basis to obtain a fair/market value of

financial instruments. This can help management take an informed decision on what is the impact of derivative

trades on an organization’s bottom line. The RBI has already issued detailed guidelines for dealing in the foreign

exchange market, which should be complied with.

Broad risk categories and common tools

It is important to understand three broad categories of risk:

Credit risk: Credit risk relates to loss due to a debtor's non-payment of a loan or other line of credit —

either the principal or interest (coupon) or both.

Market and liquidity risk: Market risk is defined as risk of losses on on-balance sheet and off-balance sheet

positions arising from movements in market prices. Liquidity risk is the risk an organization faces when it

cannot meet its payment obligations as and when they fall due. The broad categories of such risk include

interest rate risk, currency risk, commodity risk and equity risk.

Operational risk: Operational risk is the risk of incurring an economic loss due to inadequate or failed

internal processes or external events, whether such events are deliberate, accidental or natural

occurrences. Management of operational risk is underpinned by an analysis of the cause-event-effect

chain.

Depreciating rupee: Managing currency risk 5Some important and widely used risk management tools:

Value at Risk (VaR): VaR measures the maximum loss that an organization can suffer at a particular level

of confidence for a specific holding period. This tool provides a broad idea to its management on the risks

that the organization is running in its books. This is a common market risk tool.

Potential Future Exposure (PFE): Potential Future Exposure (PFE) is defined as the maximum expected

credit exposure over a specified period of time, calculated at a level of confidence. This is also a common

credit risk tool.

This is a multi-layered limit structure on respective currencies, interest rates, stop loss limits, etc.

Asset and liability gapping: Limits are set on gapping for management of ALM/liquidity mismatches.

Closing remarks…

The global crisis during 2008 has taught us that there is a likely convergence between the sub-categories of

risks mentioned earlier, especially credit and market/liquidity risk. Globalization of Indian markets has made

them vulnerable to any global event. Markets are volatile, will continue to be unpredictable and surprise us with

un-anticipated events. These dynamics call for sophisticated risk management frameworks, solutions and

processes to manage risks with an enterprise-wide view rather than in the traditional way of managing risks in

silo. In this volatile scenario, organizations should not only be reactive but need to be proactive as well. They

should have the best risk-management practices in place to stay ahead of the market. A strong risk-

management framework in an organization is a role model for regulators, customers, and most importantly,

shareholders, reassures them that it is resilient to future shocks and is making a whole-hearted effort to ensure

that its bottom line is predictable within an acceptable range. This also contributes to the organization’s

competitiveness by enabling enhanced management insight in the business, allowing it to take advantage of

future opportunities when others will keep playing the “catching game.”

One earlier said, “No risks – no reward,” but now it is time to say, “Better managed risks – better rewards.”

This article is produced by Financial Services Risk Management Team of EY

Depreciating rupee: Managing currency risk 6Our offices

Ahmedabad Kolkata

2nd floor, Shivalik Ishaan 22, Camac Street

Near. C.N Vidhyalaya 3rd Floor, Block C”

Ambawadi, Kolkata – 700 016

Ahmedabad – 380 015 Tel: + 91 33 6615 3400

Tel: + 91 79 6608 3800 Fax: + 91 33 2281 7750

Fax: + 91 79 6608 3900

Mumbai

Bengaluru 14th Floor, The Ruby

12th & 13th floor 29 Senapati Bapat Marg

“U B City” Canberra Block Dadar (west)

No.24, Vittal Mallya Road Mumbai – 400 028

Bengaluru – 560 001 Tel + 91 22 6192 0000

Tel: + 91 80 4027 5000 Fax + 91 22 6192 1000

+ 91 80 6727 5000

Fax: + 91 80 2210 6000 (12th floor)

Fax: + 91 80 2224 0695 (13th floor) 5th Floor Block B-2,

Nirlon Knowledge Park

1st Floor, Prestige Emerald Off. Western Express Highway

No.4, Madras Bank Road Goregaon (E)

Lavelle Road Junction Mumbai – 400 063

Bengaluru-560 001 India Tel: + 91 22 6192 0000

Tel: +91 80 6727 5000 Fax: + 91 22 6192 3000

Fax: +91 80 2222 4112

Chandigarh NCR

1st Floor Golf View Corporate

SCO: 166-167 Tower – B

Sector 9-C, Madhya Marg Near DLF Golf Course,

Chandigarh – 160 009 Sector 42

Tel: + 91 172 671 7800 Gurgaon – 122 002

Fax: + 91 172 671 7888 Tel: + 91 124 464 4000

Fax: + 91 124 464 4050

Chennai

Tidel Park, 6th floor, HT House

6th & 7th Floor 18-20 Kasturba Gandhi Marg

A Block (Module 601,701-702) New Delhi – 110 001

No.4, Rajiv Gandhi Salai Tel: + 91 11 4363 3000

Taramani Fax: + 91 11 4363 3200

Chennai – 600 113

Tel: + 91 44 6654 8100

4th & 5th Floor, Plot No 2B,

Fax: + 91 44 2254 0120

Tower 2, Sector 126,

Noida – 201 304

Hyderabad

Gautam Budh Nagar, U.P. India

Oval Office

Tel: + 91 120 671 7000

18, iLabs Centre,

Fax: + 91 120 671 7171

Hitech City, Madhapur,

Hyderabad – 500 081

Tel: + 91 40 6736 2000 Pune

Fax: + 91 40 6736 2200 C—401, 4th floor

Panchshil Tech Park

Kochi Yerwada (Near Don Bosco School)

9th Floor “ABAD Nucleus” Pune – 411 006

NH-49, Maradu PO, Tel: + 91 20 6603 6000

Kochi – 682 304 Fax: + 91 20 6601 5900

Tel: + 91 484 304 4000

Fax: + 91 484 270 5393Ernst & Young LLP EY | Assurance | Tax | Transactions | Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in. Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata - 700016 © 2013 Ernst & Young LLP. Published in India. All Rights Reserved. This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

You can also read