Deutsche Bank Global Auto Industry Conference - January 13, 2015

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Deutsche Bank Global Auto Industry Conference January 13, 2015

Safe Harbor This presentation contains what the Company believes are forward-looking statements related to future financial results and business operations for Cooper Tire & Rubber Company. Actual results may differ materially from current management forecasts and projections as a result of factors over which the Company may have limited or no control. Information on certain of these risk factors and additional information on forward-looking statements are included in the Company’s reports on file with the Securities and Exchange Commission and set forth at the end of this presentation. 244844-64 - CTB investor day - 15Apr14 - V17 (Roy script).pptx Draft—for discussion only 1 1

Our Value Proposition

To be our

customers' best

service/value supplier

Great Great Great

Products Price Service

244844-64 - CTB investor day - 15Apr14 - V17 (Roy script).pptx Draft—for discussion only 2

Winning Formula for Operational Excellence

Vision Globally competitive cost structure on every tire we produce

1 2 3 44

Cost Product Portfolio

Global Sourcing Automation

Effectiveness Management

Optimize production Reduce total Invest in U.S. plant Reduce

across global production cost per automation manufacturing

footprint tire • Reduce labor cost complexity

Strategic • Material • Decrease variation

Near-sourcing • Conversion and scrap Improve cost

Focus strategy • Scrap • Improve quality competitiveness

Areas • Distribution

Product family

consolidation

5

All cost initiatives pursued while maintaining and elevating

quality, safety and sustainability

244844-64 - CTB investor day - 15Apr14 - V17 (Roy script).pptx Draft—for discussion only 3

Americas Tire Operations Business Overview

• 4th largest manufacturer • Established in 2007 • Max-Trac Tire Co., Inc.

in North America1 dba Mickey Thompson

• One manufacturing Performance Tires &

• Three tire manufacturing facility near Wheels; wholly-owned

facilities (Findlay, Tupelo Guadalajara with our Cooper subsidiary

and Texarkana) JV partner • Acquired in 2003

• Premium brand,

• ~4,900 employees • ~1,100 total performance positioning

employees including • ~75 employees

JV partner

Cooper Cooper CS5 Cooper Deegan 38

Discoverer AT3 Ultra Touring Classic

1. Based on production capacity. Source: Tire Business 2013 Global Tire Report

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 4 4

Americas 2013 Unit Sales Breakdown

Replacement Focus Diversified Product Mix Principally Branded

Replacement Market

99%

Light

20% Truck House Private

Passenger 74% 69% 31%

brands label

1% TBR

3% Winter

1%

2% Specialty

OE Market

increasing exposure to the fastest growing and most attractive

segments with a strong portfolio of house brands

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 5 5

Winning Formula for Americas Tire Operations

Diversify and grow in the most attractive segments

Vision to be our customers' best service/value supplier

1 2 3 4

Become an Grow in Leverage

Mix and margin

established OE Commercial footprint to grow

enhancement

supplier Vehicles in Latin America

Continue product launch Grow OE segment Recover and grow Expand Mexico

successes Roadmaster share manufacturing

No more than 10% of

Strategic Focus on growth of the

Cooper brand

business Grow in OE segment Continue success in

Mexico and Central

Focus Enter car dealer Enter fleet replacement America

Convert capacity to grow replacement channel channel

Areas more premium units Leverage footprint to

Further advance grow in the rest of Latin

Grow in underpenetrated Cooper technology America

channels

Deemphasize wholesale

private-label business

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 6 6

1 Mix & margin enhancement

We Have Been Successfully Shifting Our Mix Toward

Premium Segments…

Cooper PCR / SUV mix Several Drivers of Premium Mix Shift

% of Cooper volume • Increasing pace of branded new product

development with focus on premium

segments

• Accelerating capacity conversion to

Premium segments

(Winter, UHP, H, V, support premium unit growth

and SUV)

• Growing our branded PCR and SUV share

in underpenetrated channels

• Continuing Mickey Thompson growth in the

T & below specialty segment

• Raising brand awareness through targeted

2009 2011 2013 Next level advertising spend

(by 2017)

Operating profits for “premium segments" 5 to 15 times

higher than T & below rated tires

1. Winter, UHP, V-rated, H-rated and SUV

Source: Cooper internal data

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 7 7

2 Become an established OE supplier

Cooper Pursuing Becoming an Established OE Supplier in

North America

OE Growing Twice as Fast as We Have a Strong Rationale for

Replacement Market1 in North America2 Entering the OE Business Now

Million units

OE is a faster-growing segment and

500 market conditions for OE profitability

have improved

CAGR

2.6%

368 '13-17

We have the right technology and

333

23% OE 4% products

21%

250 OE generates pull for replacement market,

increases penetration in car dealership

channels

79% 77% Replacement 2%

Also enhances brand awareness

0 Ultimately, it compels us to always get better!

2013 2017E

We expect to maintain focus on the replacement segment

while pursuing OE business.

1. Includes PCR and LT. 2. United States, Canada, and Mexico.

Source: LMC Automotive

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 8 8

3 Grow in Commercial Vehicles

We Are Increasing Our TBR Market Share in North

America...

Focused on Recuperating

Roadmaster Share… … and Growth in Fleet and OE

TBR unit sales Significant growth opportunity for

-46%

Cooper, and currently building in-

+33% CAGR house expertise and capabilities:

• National Accounts Program

• 24/7 Fleet Emergency Service

• Fleet Engineer team

Success in fleets also a pull-through

2008 2010 2012 2013

in OE segment

Supply issue resolved Increased investments in sales and

marketing

Began delivering Roadmaster products in Q1 2014

Winning back positions with key customers

Our TBR margins ~2–3 times higher than PCR/LT margins

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 9 94 Leverage footprint to grow in Latin America

...And Growing in Mexico, Brazil and Latin America by

Leveraging Mexico LCC Manufacturing

Leveraging Strong Asset in Mexico… ...To Grow in Latin America

Low cost, near-sourced manufacturing facility Colombia 2017F

(Millions)

• Lower labor and distribution cost

Population 48

• Faster response to market demand changes Replacement

7

tire demand1

Mexico 2017F

Reduced duties for major Latin American (Millions)

markets Population 128

Replacement

27

Opportunity to raise capacity by 50% to tire demand1

accelerate LT and PCR production

Brazil 2017F

(Millions)

Chile 2017F Population 206

Cooper tire (Millions) Replacement

47

manufacturing Population 18 tire demand1

facility near Replacement

5

Guadalajara tire demand1

1. Annual replacement unit demand for PCR, LT and TBR

Source: LMC Automotive

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 10 10International Tire Operations Business Overview

Cooper Tire Asia Cooper Tire Europe

~1,100 employees ~1,400 employees

Established operations in 2006 Acquired operations in 1997

One manufacturing facility in China: Two manufacturing facilities in Europe:

Kunshan (CKT) Melksham (U.K.) and Krusevac (Serbia)

Asia Technical Center opened in 2008, European Technical Center opened in 2007

moved to new facility in 2014

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 11 11Winning Formula for International Tire Operations

Vision Achieve profitable, sustainable growth in our International segment sales

1 2 3 4

Profitable Leverage our

PCR / TBR Penetrate

growth in sourcing for growth

growth in China China OE market

Western Europe in Eastern Europe

Increase pace of new Expand our OE Clarify and strengthen Improve service

product launches to position in China product offering to through local sourcing

meet customer needs customers

Strategic Generate consumer Improve manufacturing

Improve PCR/TBR pull via increased Improve Cooper brand cost competitiveness

Focus distribution channels brand recognition awareness and growth

Areas Grow in high potential

Grow profitably in key Eastern European

markets (U.K., countries and Russia

Germany)

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 12 12CCT Ownership Decision

Independent

valuation firm

determined the fair

market value of the

joint venture

Cooper Buys CCT Cooper Sells CCT

• Well-built asset with a great track • Cooper maintains supply via offtake

record rights for at least three years

• Likely to continue to look at other • Several options available, e.g.

growth opportunities, e.g. M&A acquisitions, brown or greenfield

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 13 132 Penetrate China OE market

OE Presence is Vital to Win in China

In China, OE Accounts for ~40%

of total PCR and LT demand Growth in OE is Vital to Win in China

Million units OE segment for PCR and LT make up ~40% of

500 market demand in China and growing rapidly

at ~11% per year

12% 375 Consumers have a strong sense of brand in

China and OE fittings drive consumer pull for

40% 11% replacement tires

250 235 • High preference for OE brand in first and

second replacements

43%

OE presence also important to raise brand

60% 13%

awareness and consideration

57%

0

2013 2017E

OE Replacement

Note: Figures include demand for PCR and Light Truck

Source: LMC Automotive

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 14 143 Profitable growth in Western Europe

We Are Focused on Growing our Solid Position in the U.K.

and Capturing Profitable Growth in Germany

United Kingdom

Total replacement

demand (M units) • Cooper one of the top 5 players

60 with well established brands and

1%

distribution footprint

40 33 35 • Melksham production facility to

serve local demand

20 • Profitable niche and premium

strategy (e.g. UHP, motorcycle,

0 racing tires)

2013 2017F

United

Germany Kingdom Germany

Total replacement

demand (M units) • Largest market in Europe

100

• Increased market share in 2013

3% with strong growth in W,Y,Z rated

64

58 PCR and SUV segments

50 • Leveraging new product

successes to grow Cooper brand

0

awareness

2013 2017F

Note: Figures include demand for PCR, light truck and TBR

Source: LMC Automotive

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 15 154 Leverage our sourcing for growth in Eastern Europe

Plans to Expand Presence in High Potential Countries in

Eastern Europe

Eastern Europe (including Russia)

Total demand (units)

200

6%

163

150 129

100

Estonia

Russia 50

Latvia

Lithuania 0

Belarus 2013 2017F

Poland

Czech

Ukraine • Fastest growing markets in Europe

Rep. Slovakia

Hungary Romania

• Leverage manufacturing presence in Serbia

Serbia

Bulgaria

– LCC cost advantage

– Duty free into both EU & Russia

• Plans to increase sales force and resources

in Eastern Europe

Note: Figures include OE and replacement demand for PCR, light truck and TBR

Source: LMC Automotive

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 16 16Financial Update

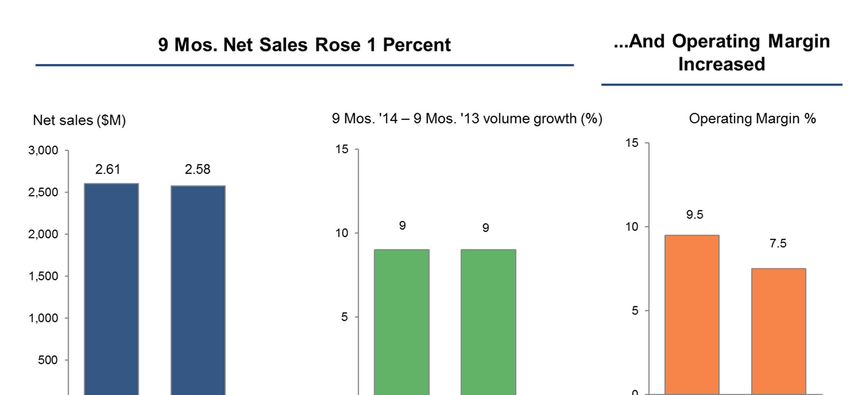

9 Months 2014 Results*

*9 months 2013 includes the impact of labor actions at Cooper’s Chinese joint venture, the impact of inefficiencies related to an ERP installation, and costs related to a then-pending merger which was

Subsequently terminated. YOY comparisons are not necessarily representative of the business under normal circumstances.

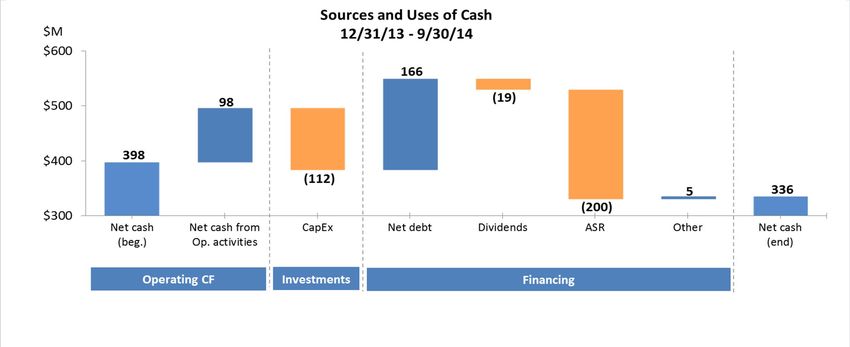

244844-64 - CTB investor day - 15Apr14 - V17 (Roy script).pptx Draft—for discussion only 18 18A Strong Balance Sheet Gives us Financial Flexibility

Healthy Balance Sheet... ...With Ample Financing Flexibility

Cash and cash equivalents ($M)

600 +15%

398

400 346

$200M

200 Asset backed revolving

credit facility

0

Q4 ’07 Q4 ’13

Debt/Enterprise value1

40

38 $175M

Accounts receivable

-22 securitization program

20 16

0

2008 2013

1. Debt is short-term debt, current portion of long-term debt and long-term debt

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 19 19We Carefully Consider How to Best Allocate Capital to High

Shareholder Return Opportunities

Different Alternatives for In the Last Five Years,

Using Excess Cash We Efficiently Deployed Capital

Fund maintenance projects

Pursue high ROIC projects ROIC1 ROIC weighted average

• E.g. U.S. plant automation, product mix change in last five years = 16%

30

Expand capacity to support growth 20

• Within current plant footprint ...

• ... or beyond, e.g., Serbia 10 22

16 16 14

11

8

Maintain strong balance sheet including 0

pension funding

-14

-10

Return capital to shareholders:

• Regular dividends (set based on ability to -20

maintain through recessions)

2007 2008 2009 2010 2011 2012 2013

• Buybacks or special dividend

1. Return on Invested Capital, including non-controlling equity

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 20 20We Expect to Further Grow Cash to Fund the Business and Other Uses DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 21

We Have Set Bold Aspirations for the Future

Long-term

$5-6B 10+%

operating

net sales

margin

8-10%

operating margin on a

consistent basis

2013

$3.4B 7%

operating

net sales

margin

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 22 22Risks

It is possible that actual results may differ materially from projections or expectations due to a variety of factors, including but not limited to:

• volatility in raw material and energy prices, including those of rubber, steel, petroleum based products and natural gas and the unavailability of such raw materials or energy sources;

• the failure of the Company’s suppliers to timely deliver products in accordance with contract specifications;

• changes in economic and business conditions in the world;

• failure to implement information technologies or related systems, including failure by the Company to successfully implement an ERP system;

• increased competitive activity including actions by larger competitors or lower-cost producers;

• the failure to achieve expected sales levels;

• changes in the Company’s customer relationships, including loss of particular business for competitive or other reasons;

• the ultimate outcome of litigation brought against the Company, including stockholders lawsuits relating to the Apollo merger as well as products liability claims, in each case which

could result in commitment of significant resources and time to defend and possible material damages against the Company or other unfavorable outcomes;

• changes to tariffs or the imposition of new tariffs or trade restrictions;

• changes in pension expense and/or funding resulting from investment performance of the Company’s pension plan assets and changes in discount rate, salary increase rate, and

expected return on plan assets assumptions, or changes to related accounting regulations;

• government regulatory and legislative initiatives including environmental and healthcare matters;

• volatility in the capital and financial markets or changes to the credit markets and/or access to those markets;

• changes in interest or foreign exchange rates;

• an adverse change in the Company’s credit ratings, which could increase borrowing costs and/or hamper access to the credit markets;

• the risks associated with doing business outside of the United States;

• the failure to develop technologies, processes or products needed to support consumer demand;

• technology advancements;

• the inability to recover the costs to develop and test new products or processes;

• a disruption in, or failure of, the Company’s information technology systems, including those related to cyber security, could adversely affect the Company’s business operations and

financial performance;

• the impact of labor problems, including labor disruptions at the Company, its joint venture, or at one or more of its large customers or suppliers;

• failure to attract or retain key personnel;

• consolidation among the Company’s competitors or customers;

• inaccurate assumptions used in developing the Company’s strategic plan or operating plans or the inability or failure to successfully implement such plans;

• failure to successfully integrate acquisitions into operations or their related financings may impact liquidity and capital resources;

• changes in the Company’s relationship with its joint-venture partner or suppliers, including any changes with respect to CCT’s production of Cooper-branded products;

• the inability to obtain and maintain price increases to offset higher production or material costs;

• inability to adequately protect the Company’s intellectual property rights; and

• inability to use deferred tax assets;.

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 23 23Available Information

You can find Cooper Tire on the web at coopertire.com. Our company webcasts earnings calls and

presentations from certain events that we participate in or host on the investor relations portion of our

website (http://coopertire.com/investors.aspx). In addition, we also make available a variety of other

information for investors on the site. Our goal is to maintain the investor relations portion of the

website as a portal through which investors can easily find or navigate to pertinent information about

Cooper Tire, including:

• Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any

amendments to those reports, as soon as reasonably practicable after we electronically file that material

or furnish it to the Securities and Exchange Commission (“SEC”);

• Information on our business strategies, financial results and selected key performance indicators;

• Announcements of our participation at investor conferences and other events;

• Press releases on quarterly earnings, product and service announcements and legal developments;

• Corporate governance information; and,

• Other news and announcements that we may post from time to time that investors may find relevant.

The content of our website is not intended to be incorporated by reference into this presentation or in

any report or document we file with or furnish to the SEC, and any references to our website are

intended to be inactive textual references only.

DB Leverage conf Oct 2014 (3).pptx Draft—for discussion only 24 24You can also read