Digital currencies and the future of the monetary system

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Digital currencies and the future of the monetary system

Remarks by Agustín Carstens 1

General Manager, Bank for International Settlements

Hoover Institution policy seminar

Basel 27 January 2021

Introduction

It is a great pleasure to be here today. Thank you to John Taylor and John Cochrane for the invitation. It is

an honour to speak to this select group of Hoover Institution affiliates, Stanford faculty and Stanford

students – who are surely the policymakers, entrepreneurs and innovators of tomorrow.

In my remarks today, I will address the digitisation of money. 2 Does the economy need digital

currencies? Digital money itself is not new. Commercial bank money has been digital for decades, and we

already use digital means of payment on a daily basis. Central banks already provide wholesale digital

money to banks.

In today’s lecture, though, I would like to discuss new forms of digital currencies or “digital cash”

that have been in the news lately, including central bank digital currencies, or CBDCs. If we need digital

currencies of these new kinds, who should issue them, and how should they be designed? What are the

implications of digital currencies for the monetary system? These are weighty issues that are much on the

minds of central bankers, scholars and the general public. Today I hope to clarify the concepts and sketch

a path for the way forward.

1. Do we need new digital currencies? If so, who should issue them?

Let’s start with whether the economy needs digital currencies, and from whom.

It is stating the obvious that our economy is in the middle of a technological revolution. 3 A

combination of new digital technologies and greater online activity allows huge volumes of data to be

1

I would like to thank Raphael Auer, Jon Frost, Leonardo Gambacorta and Hyun Song Shin for support in preparing this speech,

and Morten Bech, Sarah Bell, Stijn Claessens, Emma Claggett and Tara Rice for providing comments. I thank Giulio Cornelli for

research assistance.

2

“Digitisation” refers to the process of changing information from analogue to digital form. In the context of money, this refers

to creating a digital representation of money, or moving it to digital form. “Digitalisation”, meanwhile, refers to the use of digital

technologies to change a business model and provide new revenue and value-producing opportunities, or the process of moving

to a digital business. See Gartner, Gartner Glossary, 2021, accessed 15 January 2021.

3

F Caselli, “Technological revolutions”, American Economic Review, vol 89, no 1, 1999 defines a technological revolution simply as

“the introduction of a new type of machines” that are “more productive than machines of the pre-existing type”. T Kuhn, The

structure of scientific revolutions, University of Chicago Press, 1962 discusses the related notion of scientific revolutions, when, in

the accumulation of new knowledge, anomalies lead to a sudden “paradigm shift” or change in beliefs. K Schwab, “The fourth

1/17

collected, managed and telecommunicated. This has dramatically lowered the costs of many tasks. 4 It has

resulted in powerful, hyper-scalable applications that have disrupted entire industries – everything from

taxis to print media. New players have entered the digital economy to provide these services. While

advances in information technology and communications have been under way for many decades, the

past decade has ushered in truly far-reaching changes. The Covid-19 pandemic may have further

accelerated the pace of digital change. 5

The technological revolution has also reached the financial system – and even the design of

money itself. Just to name one example, on primary foreign exchange (FX) venues, market-makers can

now access real-time prices at five-millisecond time intervals. Project Rio, a new application for monitoring

fast-paced markets developed at the BIS Innovation Hub, allows the entire market order book to be

monitored every 100 milliseconds, or 36,000 times every hour. 6

The first point of entry into finance is the market for payment services, which are foundational to

all economic activity. 7 Payments are attractive for digital disrupters because they are relatively less capital-

intensive than other financial services, and the information they generate is highly valuable for cross-

selling. Perhaps it is no surprise that we’ve seen a burst of digital innovation in payments, including new

digital payment offerings by fintech startups, big techs and incumbents. 8

Many payment innovations build on improvements to underlying infrastructures that have been

many years in the making. For instance, harnessing technological progress, central banks around the world

have instituted real-time gross settlement (RTGS) systems over the past decades. Meanwhile, operating

hours of these systems have continued to lengthen around the globe, and in several countries are already

operating almost 24/7. Also on the retail side, innovation is rampant, and a growing number of economies

– 51 by our last count – have fast retail payment systems, which allow 24/7 instant settlement of payments

between households and businesses (Graph 1). These include systems like the Unified Payment Interface

(UPI) in India, CoDi in Mexico, PIX in Brazil and the FedNow proposal in the US. Together, these innovations

have shown that the existing system can adapt, providing good examples of how innovation in public-

private partnerships is working.

industrial revolution: what it means, how to respond”, Foreign Affairs, December 2015 discusses the unique features of the fourth

industrial revolution, which involves “a fusion of technologies that is blurring the lines between the physical, digital, and biological

spheres”.

4

For an overview, see A Goldfarb and C Tucker, “Digital economics”, Journal of Economic Literature, vol 57, no 1, 2019.

5

To name just one example, the pandemic has led to a surge in e-commerce, particularly in countries with stricter lockdown

measures and where e-commerce was previously less developed. See V Alfonso, C Boar, J Frost, L Gambacorta and J Liu,

“E-commerce in the pandemic and beyond”, BIS Bulletin, no 36, 2021.

6

Project Rio is being developed in the BIS Innovation Hub’s Switzerland Centre, together with the Swiss National Bank. See BIS,

“BIS Innovation Hub sets out annual work programme and launches Innovation Network”, press release, 22 January 2021; and

A Carstens, “Central bank innovation – from Switzerland to the world”, speech at the founding ceremony of the BIS Innovation

Hub Swiss Centre, Zurich, 8 October 2019.

7

See BIS, “Central banks and payments in the digital era”, Annual Economic Report 2020, June 2020, Chapter III.

8

See M Bech and J Hancock, “Innovations in payments”, BIS Quarterly Review, March 2020.

2/17

Diffusion of retail fast payment systems1

Number of countries Graph 1

1

The dotted part of the lines corresponds to projected implementation.

Source: BIS, “Central banks and payments in the digital era”, Annual Economic Report 2020, June 2020, Chapter III.

Yet no one is compelled to choose the path of the existing monetary system. In addition to

improvements to existing systems, many attempts to innovate in less traditional fields have been

unleashed. One example is digital currencies – which could transcend both traditional account-based

money and physical cash. As already mentioned, account-based money has been digital for decades, as

electronic deposits on a digital ledger. Yet there have been calls and attempts to digitise all money,

including cash. 9 In my view, fully replacing either bank accounts or cash is neither desirable nor realistic,

but let us discuss what a further digitisation of money could look like.

Narayana Kocherlakota – one of the world’s leading monetary theorists, former president of the

Federal Reserve Bank of Minneapolis and a former Stanford professor – argued in a famous 1998 paper

that “money is memory”. By substituting for an otherwise complex web of bilateral IOUs, money is a

substitute for a publicly available and freely accessible device that records who owes what to whom. 10

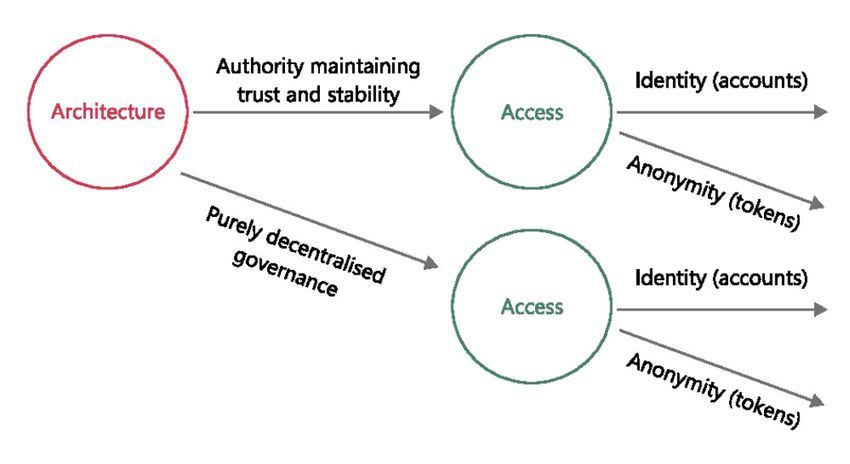

The idea that money is the economy’s memory leads us to two forks in the road for the design

of digital money (Graph 2). At these junctions, decisions about architecture and access need to be taken.

First, it needs to be ensured that the memory is always and everywhere correct. In payments parlance, this

means ensuring the integrity and safety of the payment system, as well as the finality of payments. How

to do this relates to the role of a central intermediary versus a decentralised governance system. And

second, rules to guide who has access to this information, and under what circumstances, need to be

determined, with appropriate safeguards in place to protect privacy. In other words, we need to establish

both proper identification and privacy in the payment system. Let me discuss these in turn.

9

For instance, see K Rogoff, “The case against cash”, Project Syndicate, 5 September 2016; and K Rogoff, “Will Covid make countries

drop cash and adopt digital currencies?”, The Guardian, 6 August 2020.

10

See N Kocherlakota, “Money is memory”, Journal of Economic Theory, vol 81, issue 2, 1998.

3/17

Two forks in the road for digital currencies Graph 2

Source: Adapted from R Auer and R Böhme, “The technology of retail central bank digital currency”, BIS Quarterly Review, March 2020, pp 85–

100.

If societies want digital money, the first fork in the road is the choice of operational architecture.

Should the payment system rely on a trusted central authority (such as the central bank) to ensure integrity

and finality? Or could it be based on a decentralised governance system, where the validity of a payment

depends on achieving consensus among network participants on what counts as valid payments?

This is the concept behind Bitcoin. Satoshi Nakamoto’s protocol envisions a decentralised

consensus, with no need for a central intermediary. Yet in practice, it is clear that Bitcoin is more of a

speculative asset than money. One contact recently told me that like Bitcoin is “Tesla without the cars” –

observers are fascinated by it, but the actual value backing is lacking. Perhaps the Bitcoin network should

be seen more like a community of online gamers, who exchange real money for items that only exist in

cyber space. Bitcoin poses as its own unit of account, but fluctuations in value mean it is unrealistic to set

prices in bitcoin. This also undermines its usefulness as a means of exchange, and makes it a poor store of

value. The structure of the Bitcoin market is decidedly concentrated and opaque, and there is research

evidence on price manipulation. 11

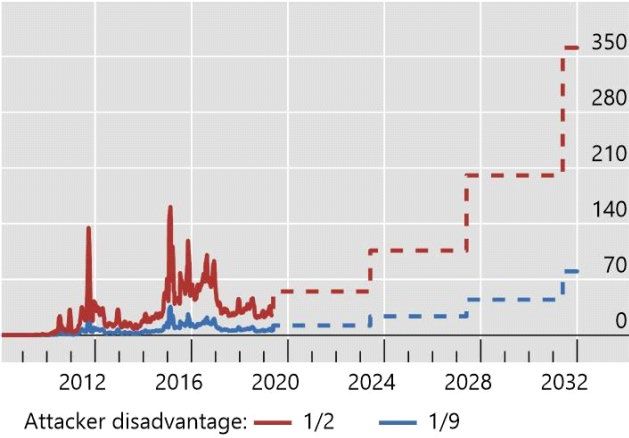

Above all, investors must be cognisant that Bitcoin may well break down altogether. 12 Scarcity

and cryptography alone do not suffice to guarantee exchange. Bitcoin needs a hugely energy-intensive

protocol, called “proof of work”, to safely process transactions. Currently, so-called miners sustain the

system’s security, and are rewarded with newly minted coins. A sad side effect is that the system uses more

electricity than all of Switzerland. In the future, as Bitcoin approaches its maximum supply of 21 million

coins, the “seigniorage” to miners will decline. As a result, wait times will increase (Graph 3, left-hand panel)

11

See J Griffin and A Shams, “Is Bitcoin really untethered?”, The Journal of Finance, vol 74, no 4, 2020.

12

On the outlook for Bitcoin, see R Auer,: “Beyond the doomsday economics of ‘proof-of-work’ in cryptocurrencies”, BIS Working

Papers, no 765, January 2019.

4/17

and the system will be increasingly vulnerable to the “majority attacks” that are already plaguing smaller

cryptocurrencies (right-hand panel). 13

Bitcoin is increasingly vulnerable; others already have been “majority attacked” Graph 3

Substantially longer waiting time results when block A timeline of cryptocurrency majority attacks since 2017

reward declines1

Hours

Attack Electronuem

Reorg Bitcoin Cash

Reorg Bitcoin Gold

Attack ETH Classic

Attack ETH Classic

Attack ETH Classic

Attack Monacoin

Attack ZenCash

Attack Vertcoin

Attack Vertcoin

Attack Vertcoin

Attack Vertcoin

Attack Karbo

Attack Verge

Attack Vertcoin

Attack Pigeoncoin

Reorg Bitcoin Gold

Attack Litecoin cash

Attack AurumCoin

Attack Bitcoin Private

Attack Verge

Attack Bitcoin Gold

Attack ETH Classic

2017 2018 2019 2020

1

The lines show the implied waiting time (number of block confirmations before merchants can safely assume that a payment is irreversible)

required to make an economic attack unprofitable: the attacker rents mining equipment on a short-term basis and executes a change-of-

history attack. The dashed pattern indicates predicted values (see Auer (2019) for calculations).

Sources: R Auer, “Beyond the doomsday economics of ‘proof-of-work’ in cryptocurrencies”, BIS Working Papers, no 765, January 2019;

S Shanaev, A Shuraeva, M Vasenin and M Kuznetsov, “Cryptocurrency value and 51% attacks: evidence from event studies”, The Journal of

Alternative Investments, Winter, 2020; blocksdecoded.com; bravenewcoin.com; btcmanager.com; coinbase.com; Coindesk.com; deribit.com;

github.com; medium.com.

What then of so-called stablecoins – cryptocurrencies that seek to stabilise their value against

sovereign fiat currencies or another safe asset? Facebook’s Libra – recently renamed Diem – was initially

marketed as a “simple currency for billions”. It would import credibility by being pegged to a basket of

stable currencies like the US dollar and euro. More recent incarnations of Diem would be denominated in

individual sovereign currencies, looking more like so-called e-money or other digital payment services.

This is certainly more credible than Bitcoin. But there are still serious governance concerns if a private

entity issues its own currency and is responsible for maintaining its asset backing. Historical examples

show us that there may be strong incentives to deviate from an appropriate asset backing, such as pressure

to invest in riskier assets to achieve higher returns. 14 Overall, private stablecoins cannot serve as the basis

for a sound monetary system. There may yet be meaningful specific use cases for stablecoins. But to remain

credible, they need to be heavily regulated and supervised. They need to build on the foundations and

trust provided by existing central banks, and thus to be part of the existing financial system. 15

13

See A Carstens, “Money in the digital age: what role for central banks?”, speech, 6 February 2018; and BIS, “Cryptocurrencies:

looking beyond the hype”, Annual Economic Report 2018, 2018, Chapter V.

14

For one such example, see J Frost, H S Shin and P Wierts, “An early stablecoin? The Bank of Amsterdam and the governance of

money”, BIS Working Papers, no 905, November 2020.

15

See Libra Association, White Paper v 2.0, 16 April 2020; D Arner, R Auer and J Frost, “Stablecoins: risks, potential and regulation”,

Bank of Spain Financial Stability Review, no 39, 2020.

5/17

I side here with Milton Friedman, who argued, “Something like a moderately stable monetary

framework seems an essential prerequisite for the effective operation of a private market economy. It is

dubious that the market can by itself provide such a framework. Hence, the function of providing one is

an essential governmental function on a par with the provision of a stable legal framework.” 16 This idea

remains as relevant as ever in the digital age.

So, clearly, if digital money is to exist, the central bank must play a pivotal role, guaranteeing the

stability of value, ensuring the elasticity of the aggregate supply of such money, and overseeing the overall

security of the system. Such a system must not fail and cannot tolerate any serious mistakes.

The second fork in the road is the question of how access should be arranged. There are many

nuances, but the main choice is whether access should be around verification of identity as in bank

accounts (sometimes called “account-based access”) or around validity of the object being traded as with

physical cash, for instance with cryptography (“token-based access”). 17 In other words, is it “I am, therefore

I own” or “I know, therefore I own” (Graph 4)?

16

M Friedman, A program for monetary stability, Fordham University Press, 1960.

17

Importantly, this definition of token versus accounts must not be confused with the one used in the field of computer science.

Here the distinction between accounts and tokens is the identification requirements: “In a token-based system, the thing that

must be identified for the payee to be satisfied with the validity of the payment is the ‘thing’ being transferred – ‘is this thing

counterfeit or legitimate?’ In an account-based system, however, the identification is of the customer – ‘Is this person who she

says she is? Does she really have an account with us?’” (C Kahn, “How are payment accounts special? Payments innovation”

symposium, Federal Reserve Bank of Chicago, 2016).

6/17

Account-based access compared with token-based access Graph 4

In an account-based CBDC (left-hand side), ownership is tied to an identity, and transactions are authorised via identification. In a CBDC based

on digital tokens (right-hand side), claims are honoured based solely on demonstrated knowledge, such as a digital signature.

Source: R Auer and R Böhme, “The technology of retail central bank digital currency”, BIS Quarterly Review, March 2020, pp 85–100.

Again, this harks back to the notion of money as the memory of society’s economic interactions

and the need for identification in it. Just as our memories are tied to experiences we have in specific

relationships, money does not exist in a vacuum that is separate from economic relationships. Economic

transactions weave a web of long-term relationships between suppliers, intermediaries and customers, as

well as between borrowers and lenders. Such a web of trading creates – and rests on – a reservoir of

relationship-specific capital that sustains financial relationships. 18 This capital is built up with the

identification of all counterparties, as well as some degree of traceability of the underlying transactions.

Historical examples show that identification has been critical to allow commerce to flourish. For

instance, in 18th century Europe merchants used so-called bills of exchange to solve the lack of trust

between physically remote lenders and borrowers. Instead of extending loans directly to borrowers in

distant cities, merchants could make arrangements with others whom they personally knew, creating a

web connecting far-flung parties together. Another example are the Maghreb traders of the 11th century.

As Avner Greif – also of Stanford – famously showed, it was identity and traceability that allowed these

traders to sustain trade, even over long distances and in the presence of great uncertainty. 19

This is even more the case today: your virtual ID is key to government benefits like pensions and

cash transfers. Some form of identification is crucial for the safety of the payment system, preventing fraud,

and supporting anti-money laundering and combating the financing of terrorism (AML/CFT). There are

trade-offs between access and traceability. Socially, there are many benefits to having more information,

for example to prevent money laundering or tax evasion. Good identification can help here, giving law

enforcement authorities new tools to fulfil their mandate.

So overall, my sense is that a purely anonymous system will not work. And the vast majority of

users would accept for basic information to be kept with a trusted institution – be that their bank or public

18

This is also true in today’s credit or trade finance relationships, but the roots go back much further. See I Schnabel and H S Shin,

“Liquidity and contagion: the crisis of 1763”, Journal of the European Economic Association, vol 2, no 6, 2004.

19

See A Greif, “Reputation and coalitions in medieval trade: evidence on the Maghribi traders”, The Journal of Economic History,

vol 49, no 4, 1989.

7/17

authorities. The idea of complete anonymity is hence a chimera. Users have to leave a trace and share

information today with financial intermediaries. This makes it easier for them to work online and prevent

losses. To recount one recent anecdote, the user who lost his hard drive with $220 million of bitcoin would

have probably liked to have a backup. 20

So if we take the path I have laid out just now, where do we end up? I argue that we end up with

central bank digital currencies with some element of identification – that is, with primarily account-based

access.

Today we have the possibility to produce a technologically superior representation of central

bank money. This can combine novel digital technologies with the tried and true characteristics of central

banks – such as trust, transparency, legal backing and finality – that others would need to either rely on or

create for themselves from the ground up.

2. Designing CBDCs for the benefit of societies

Let me turn now to CBDC design.

There are two types of central bank digital currencies. The first is in the wholesale realm, for

payments between financial institutions and large commercial parties. In the last few years, there has been

a lot of activity around both private and central bank-issued wholesale digital currencies. 21 These efforts

could introduce efficiency gains, for instance by allowing faster settlement and delivery versus payment. 22

Yet they may not be all that disruptive. Again, digital central bank money for wholesale purposes already

exists, in the form of central bank reserves. Notably, privately issued wholesale digital currencies, also

called utility tokens or wholesale stablecoins, are not separate currencies per se. They still depend on

central banks for the finality of clearing and settlement. Like the stablecoins I discussed before, they still

have an “umbilical cord” connecting them to the existing financial system.

The second type of digital currency is in the retail space, and it is here where the real disruption

lies. Retail digital currencies could be used in daily transactions by households and businesses, and

depending on their design, they could upend our existing financial system.

The BIS has surveyed central banks around the world on their engagement with CBDCs. In a new

BIS Paper, out today, 23 we see that a full 86% of 65 respondent central banks are now doing some kind of

research or experimentation (Graph 5, left-hand panel). Some are working primarily on the wholesale side,

and some primarily on retail, but the largest number are looking into both (centre panel). Increasingly, we

see central banks moving beyond research towards actual pilots (right-hand panel). Since 2020, there has

been a live CBDC, with the Sand Dollar project in the Bahamas. The People’s Bank of China is performing

20

See N Popper, “Lost passwords lock millionaires out of their Bitcoin fortunes”, New York Times, 12 January 2021.

21

For instance, on private digital tokens, see Committee on Payments and Market Infrastructures, Wholesale digital tokens,

December 2019. For various models for wholesale CBDCs, see Bank of Canada, Monetary Authority of Singapore, Bank of England

and HSBC, Cross-border interbank payments and settlements: emerging opportunities for digital transformation, 15 November

2018.

22

See eg BIS, Project Helvetia: settling tokenised assets in central bank money, December 2020.

23

See C Boar and T Wehrli, “Ready, steady, go? Results of the third BIS survey on central bank digital currency”, BIS Papers, no 114,

January 2020.

8/17

large-scale pilots across China. And the Boston Fed is working with the MIT Digital Currency Initiative on

retail CBDC research that will be open source, for all to review. 24

Central bank engagement on CBDCs is rising

Share of respondents Graph 5

Engagement in CBDC work Focus of work1 Type of work in addition to research1

1

Share of respondents conducting work on CBDC.

Source: C Boar and A Wehrli, “Ready, steady, go? Results of the third BIS survey on central bank digital currency “, BIS Papers, no 114,

January 2021.

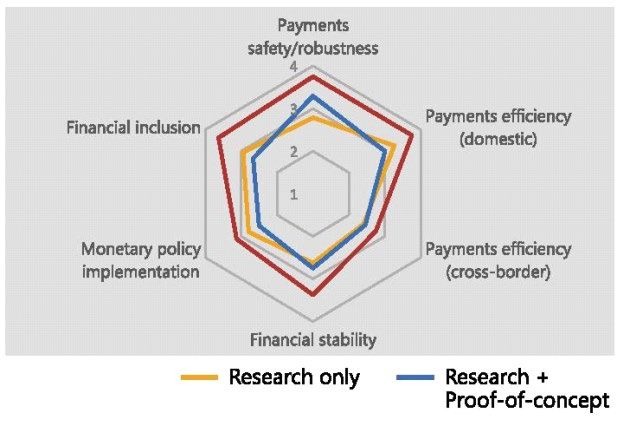

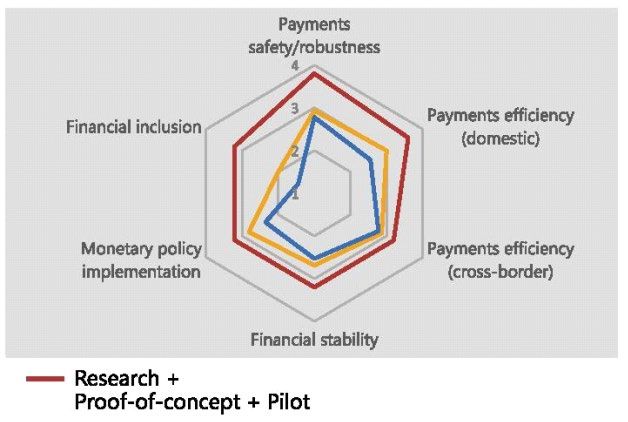

The motivations for central banks engaging in CBDC work vary across central banks, and across

retail versus wholesale projects (Graph 6). But it is striking that in both cases, and particularly for those

central banks that have moved beyond research toward proofs of concept or pilots, safety and robustness

are highlighted as being a key requirement. In the context of declining cash use and a lack of universal

access to the banking system, many central banks see CBDC as a means to ensure that the public maintains

access to a safe, publicly issued payment option to complement cash. Notably, central banks see

opportunities in digital technologies, not least to enhance payments efficiency and promote financial

inclusion. Thus, the question here is not so much “Do we need digital currencies?” but “Can central banks

grasp the opportunity for what could be a technologically superior representation of central bank

money?”.

24

See Federal Reserve Bank of Boston, “The Federal Reserve Bank of Boston announces collaboration with MIT to research digital

currency”, press release, 13 August 2020.

9/17

Main motivations of CBDC work by stage

Average importance Graph 6

Retail CBDC Wholesale CBDC

(1) = “Not so important”; (2) = “Somewhat important”; (3) = “Important”; (4) = “Very important”.

Source: C Boar and A Wehrli, “Ready, steady, go? Results of the third BIS survey on central bank digital currency “, BIS Papers, no 114, January

2021.

The work on CBDCs does not imply replacing private sector initiatives. Of course, we need to take

advantage of private sector innovation, and in many research projects and pilots the private sector is a key

partner. The CBDC work shows that while disruptive innovation can be a threat, it can also be an

opportunity. Thus, even with CBDC, central banks are sticking to what money has always been: a social

convention that involves a role both for the private sector and for the central bank or other public

authorities. In this sense, money is an instance of a public-private partnership.

Thus, CBDCs can and must also be designed to preserve the two-tiered financial system, as a

public-private partnership. In terms of involvement by the private sector, we should not think only about

models where the central bank provides retail services directly (such as the FedAccounts idea). 25 From a

user perspective, a successful retail CBDC would need to provide a resilient and inclusive digital

complement to physical cash – but that does not preclude an important role for the private sector.

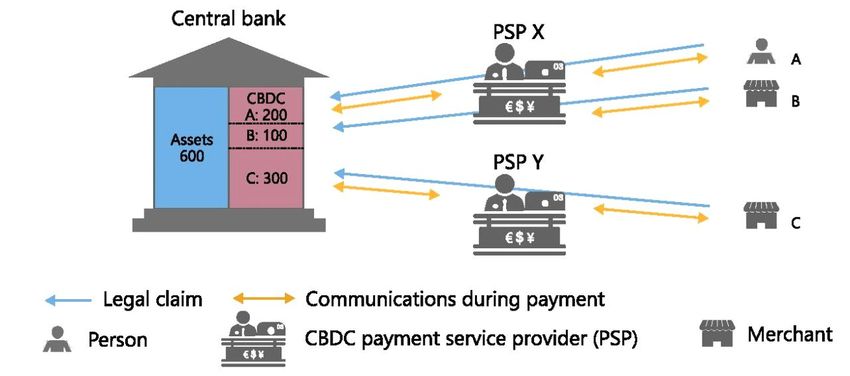

Research at the BIS scopes out how two-tier “Hybrid” and “Intermediated” CBDC architectures

can involve the private sector as the default operator of payments, with the central bank optionally

operating a back-up infrastructure to provide additional resilience (Graph 7). Users could pay with a CBDC

just as today, with a debit card, online banking tool or smartphone-based app, all operated by a bank or

other private sector payment provider. However, instead of these intermediaries booking transactions on

their own balance sheets as is the case today, they would simply update the record of who owns which

CBDC balance. The CBDC itself would be a cash-like claim on the central bank. In this way, the central bank

avoids the operational tasks of opening accounts and administering payments for users, as private sector

intermediaries would continue to perform retail payment services. The benefit is that there are no balance

sheet concerns with private sector intermediaries. Further, these architectures also allow the central bank

to operate backup systems in case the private sector runs into technical outages.

25

See M Ricks, J Crawford and L Menand, “FedAccounts: digital dollars”, George Washington Law Review, 2018.

10/17Hybrid CBDC architectures allow for public-private partnership in payments Graph 7

Sources: R Auer and R Böhme, “The technology of retail central bank digital currency”, BIS Quarterly Review, March 2020, pp 85–100; R Auer

and R Böhme, “Central bank digital currency: the quest for minimally invasive technology”, BIS Working Papers, forthcoming.

A system that in many ways resembles today’s system could run successfully on distributed ledger

technology (DLT), as a BIS working paper that we are releasing today shows. 26 This paper finds that despite

all the limitations with Bitcoin and other permissionless cryptocurrencies, greater economic promise lies

with the “permissioned” variant of DLT. In permissioned DLT, a known network of validators replaces the

traditional model with one central validator. The BIS Innovation Hub has already demonstrated that this

works in a lab environment, in a proof of concept that involved the settlement of tokenised assets in central

bank money using a DLT-based software. 27 Going beyond the lab environment, the working paper shows

26F

that the technology may have economic potential primarily in niche markets. It shows that while the

permissioned version of DLT holds more promise than the permissionless one, a trusted central

intermediary fares even better. DLT hence can improve upon the traditional model of centralised exchange

only where trust in, and enforcement of, the rule of law is limited.

In addition to the governance of the system itself, the governance rule of how participants can

access it also warrants attention. What about the role of identification, and of the transaction data that

digital currencies will generate? Here, we need to compare different governance rules and analyse the role

of the public and the private sector in guarding data. Of course, the danger of data breaches or abuse by

public authorities warrants a careful approach. But there are designs where some level of individual privacy

can be preserved – a CBDC does not have to entail an Orwellian Big Brother, where the central bank sees

each and every transaction.

Private sector intermediaries have a role to play in this, too, as settlement agents in a competitive

payment system. In particular, private intermediaries could (temporarily) record and guard users’ data. Yet

decisions on data privacy are very important. This is not just a technical issue, but an important policy issue

that transcends the financial sphere. Central banks will need to listen to societies in this respect. Moreover,

public sector supervision and clear frameworks for the governance of data will still be needed. If multiple

26

See R Auer, C Monnet and H S Shin, “Permissioned distributed ledgers and the governance of money”, BIS Working Papers,

no 924, January 2021.

27

See BIS (2020), op cit.

11/17parties are involved in collecting, transferring and storing data, it must be ensured that one institution is

ultimately responsible to the user. If this is done successfully, such a system could help maintain privacy

while allowing access to law enforcement under clearly defined rules, much like today’s system. Moreover,

it could put competitive pressure on today’s intermediaries, pushing for more efficiency, lower costs and

better service in payment markets. 28

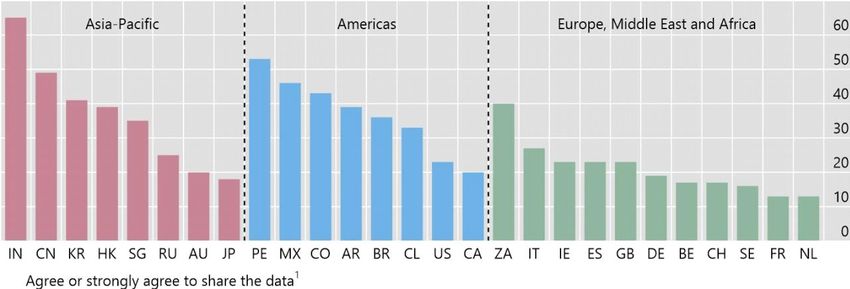

Again, different jurisdictions may pursue different avenues. This relates in part to different

preferences regarding data privacy across different societies. In China and India, for instance, users are

much more comfortable with their data being securely shared (Graph 8). And in China, the approach of

the People’s Bank of China in its CBDC, the e-CNY, is to periodically record all user data from private

intermediaries. In Europe and the United States, users report in surveys being more worried about their

privacy. For these cases, there are also technical designs that allow the central bank to be shielded from

knowing identities, or even from having access to retail transaction data, recognising that it may not want

this information. 29

28

For one take on these points, see J Cochrane, “The digital euro is a threat to banks and governments. And that’s OK”, Il Sole 24

Ore, 23 December 2020.

29

This approach has been hinted at by Jay Powell, who noted the data privacy and information security issues associated with the

central bank keeping a running record of all payments data. See J Powell, “Letter to Congressman French Hill”, 19 November

2019.

12/17Preferences regarding privacy vary across countries

In per cent Graph 8

1

The question in the survey reads, “I would be comfortable with my main bank securely sharing my financial data with other organisations if

it meant that I received better offers from other financial intermediaries”; for Belgium, the figure covers Belgium and Luxembourg.

Source: S Chen, S Doerr, J Frost, L Gambacorta and H S Shin, “The fintech gender gap”, BIS Working Papers, forthcoming; EY, Global FinTech

Adoption Index 2019, June 2019.

Above all, the discussion of identification in CBDC needs to be considered in the wider context

of digital ID. The use of personal data is necessary to improve the provision of financial services. Financial

inclusion is about overcoming inequality, in particular by reducing information asymmetries. CBDCs can

be the entry point for financial services, but they need to be linked to an ID. By offering the unbanked

access to a digital ID, authentication can help to support inclusion in the long term and to formalise the

informal economy. While this appears to create trade-offs, as citizens also value their privacy and enjoy

the anonymity of cash, there can be long-term gains from overcoming this.

Again, this seems to be the direction in which central banks are moving. As central banks report

being more likely to issue CBDCs in the medium term (Graph 9, left-hand and centre panel), CBDCs tied

to an identity scheme (“primarily account-based CBDCs”) are also relatively more common (right-hand

panel). These can serve as the basis for well functioning payments with good law enforcement. 30 The idea

that CBDCs will be like $100 bills floating around is a mischaracterisation of what CBDC would look like in

practice. My own view is that CBDCs without identity (purely token-based CBDCs) will not fly. First, they

would open up big concerns around money laundering, the financing of terrorism and tax evasion. Second,

they may undermine efforts to enhance financial inclusion, which are based on good identification and

building up an information trail for access to other financial services. Third, they could have destabilising

cross-border effects, allowing large and sudden shifts of funds between economies. For these reasons, we

need some form of identity in digital payments.

30

See R Auer, G Cornelli and J Frost, “Rise of the central bank digital currencies: drivers, approaches and technologies”, BIS Working

Papers, no 880, 2020. The authors also document that that all central banks that are developing CBDCs have also promised to

keep cash around. So, also in the digital era, central banks will continue to offer a fully anonymous means of payment – cash.

13/17Likelihood of CBDC issuance is increasing, with account-based access preferred Graph 9

Responses on likelihood of retail Responses on likelihood of wholesale Relatively more central banks are

CBDC issuance in the medium term1 CBDC issuance in the medium term1 leaning toward account-based access

Share of respondents, in per cent Share of respondents, in per cent Number of retail CBDC projects

1

Medium term: 1–6 years. “Likely” combines “very likely” and “somewhat likely”. “Unlikely” combines “very unlikely” and “somewhat

unlikely”. 2 Includes models with token-based access for small transactions.

Sources: C Boar and A Wehrli, “Ready, steady, go? Results of the third BIS survey on central bank digital currency “, BIS Papers, no 114, 2021;

R Auer, G Cornelli and J Frost, “Rise of the central bank digital currencies: drivers, technologies and approaches”, BIS Working Paper, no 880,

August 2020.

3. Implications for the monetary system

Let me move now to the implications for the monetary system.

If they are properly designed and widely adopted, CBDCs could become a complementary means

of payment that addresses specific use cases and market failures. They could act as a catalyst for continued

innovation and competition in payments, finance and commerce at large.

But if that happens, how will it affect national financial systems beyond payments? And what are

the international repercussions of CBDC issuance?

Let me discuss these considerations through the lens of the core principles for CBDC issuance, as

laid out in a recent report of the BIS, the Board of Governors of the Federal Reserve System and six other

major central banks. This report laid out a Hippocratic Oath for CBDC design, the premise to “first, do no

harm”. 31

First and foremost, this oath implies that a precondition for CBDC issuance is that its design will

not disintermediate commercial banks, nor lead to heightened volatility of their funding sources. Central

banks do not dismiss these risks. But there are tools to address digital runs and the potential for

disintermediation, like caps on the size of CBDC holdings, or variable interest rates that discourage very

large holdings by users. 32 If depositors did temporarily move funds from bank deposits to CBDCs during

31

See Group of Central Banks, “Central bank digital currencies: foundational principles and core features”, joint report no 1, October

2020.

32

See U Bindseil, “Tiered CBDC and the financial system”, ECB Working Paper no 2351, 2020.

14/17financial turmoil, central banks could also quickly re-channel liquidity back to commercial banks, much as

they do now with open market operations. Structurally, I do not anticipate the central bank becoming a

major player in intermediating savings in the economy. While such risks do need to be managed, CBDCs

do not need to threaten the stability of bank funding or lending to the real economy. 33

Second, as long as CBDC is supplied in response to transactional demand for it, this oath means

that the impact on monetary policy and its transmission will be limited. Naturally, the monetary policy

implications have received ample attention. In theory, retail CBDCs could be interest-bearing, influencing

monetary policy transmission and, in today’s context, for some advanced economies, allowing for more

negative policy rates. However, one has to keep in mind that since CBDC would complement cash rather

than replace it, and since another policy objective is to limit the central bank’s systemic footprint, these

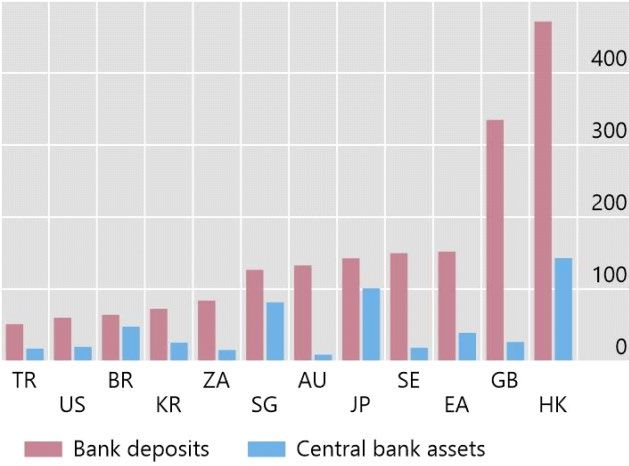

monetary policy effects might be contained in practice. Much as cash holdings and even total central bank

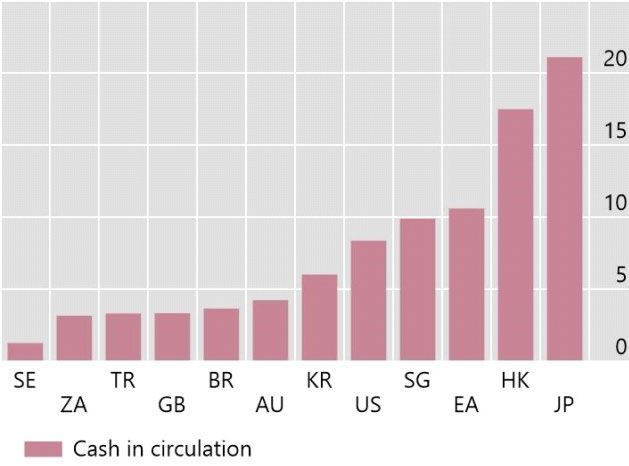

assets are currently moderate in relation to bank deposits (Graph 10), I expect that CBDC holdings will not

become very large. This could also mean that the central bank toolkit will remain largely unaffected.

CBDCs can be designed to have a limited systemic footprint – like cash today

As a percentage of GDP Graph 10

Cash holdings are moderate…1 …and consumers’ sight deposits vastly exceed central

bank balance sheet sizes1,2

1

Data for 2018. 2

Closest alternative where data is not available.

Source: R Auer and R Böhme, “Central bank digital currency: the quest for minimally invasive technology”, BIS Working Paper, forthcoming.

Third is the international aspect and the threat of international currency competition. 34 Payment

system design is a domestic choice, but it has important international implications. Wherever there are

macroeconomic or institutional reasons for dollarisation today, foreign CBDC issuance may aggravate this

threat, by making it even easier for users to adopt a foreign (digital) alternative. Some have argued that

33

See D Andolfatto, “Assessing the impact of central bank digital currency on private banks”, The Economic Journal,

September 2020.

34

This relates to the broader debate on the denationalisation of money and digital currency areas. For the classic appeal to allow

international competition between currencies, see F Hayek, The Denationalization of Money, Institute of Economic Affairs, 1976.

For a rebuttal, see M Friedman and A Schwartz, “Has government any role in money?” in A Schwartz (ed), Money in Historical

Perspective, University of Chicago Press, 1987. For the discussion of digital currency areas, see M Brunnermeier, H James and J-P

Landau, “The digitalization of money”, NBER Working Paper no 26300, 2019.

15/17an e-CNY or digital euro could even challenge the dominance of the US dollar as a global reserve

currency. 35 But here, I doubt that CBDCs alone will tip the balance – especially if they are account-based.

Indeed, the main reasons why a reserve currency is attractive are related to the macroeconomy. The dollar

is the world’s premier reserve currency because it has a stable value (low inflation), a large supply of safe

assets and the credibility of the US economic and legal system. Investors can also easily access the US’s

deep and efficient capital markets, without worrying about capital controls. These factors are likely to

remain the primary drivers of global reserve currency status.

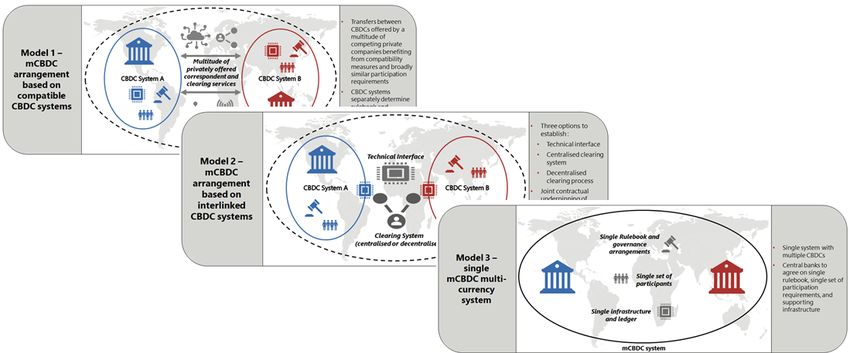

Yet beyond currency competition, there are opportunities from CBDCs to enhance the efficiency

of cross-border payments. Multi-CBDC arrangements (Graph 11) could tackle frictions in today’s

correspondent banking system, such as differences in opening hours, varying communication standards

and a lack of clarity around exchange rates or fees. 36

Potential models for multi-CBDC arrangements Graph 11

Source: R Auer, P Haene and H Holden, “Multi-CBDC arrangements and the future of cross-border payments”, forthcoming.

Conclusion

Let me conclude. Sound money is central to our market economy, and it is central banks that are uniquely

placed to provide this. If digital currencies are needed, central banks should be the ones to issue them. If

35

For an argument in this direction, see A Kumar and E Rosenbach, “Could China’s digital currency unseat the dollar?”, Foreign

Affairs, May 2020. For a more nuanced take, see M Chorzempa, “China, the United States, and central bank digital currencies:

how important is it to be first?”, China Economic Journal, 2021.

36

See R Auer, P Haene and H Holden, “Multi-CBDC arrangements and the future of cross-border payments”, BIS Papers,

forthcoming for an examination of the potential of CBDC in cross-border payments, as well as Committee on Payments and

Market Infrastructures, Enhancing cross-border payments: building blocks of a global roadmap, July 2020 for a discussion of how

these could feature in global efforts to improve cross-border payments. M Ferrari, M Mehl and L Stracca, “Central bank digital

currency in an open economy”, ECB Working Paper no 2488, 2020, and International Monetary Fund, “Digital money across

borders: macro-financial implications”, IMF Policy Papers, no 2020/050, 2020 analyse the international ramifications of the

digitisation of money.

16/17they do, CBDCs could also play a catalytic role in innovation, spurring competition and efficiency in

payments.

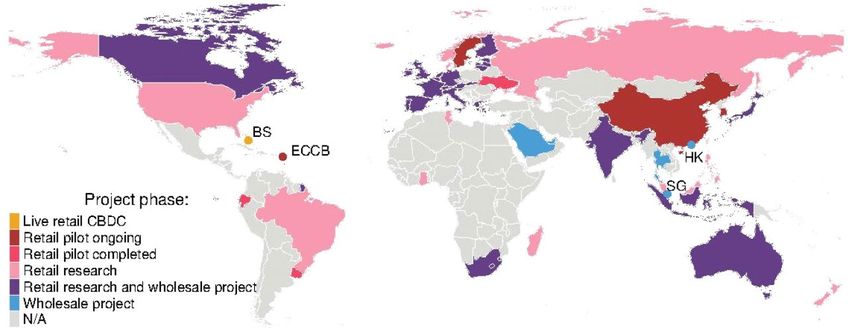

In this light, even as they fight the fires related to the Covid-19 pandemic, central banks around

the world have stepped up their CBDC design efforts (Graph 12). This should not be seen primarily as a

reaction to the emergence of cryptocurrencies or the announcement of corporate stablecoin projects.

Rather, they are proactively researching a new form of money and how it could improve retail payments

in the digital area, in line with central bank mandates.

CBDCs research and pilots around the globe Graph 12

BS = The Bahamas; ECCB = Eastern Caribbean Central Bank; HK = Hong Kong SAR; SG = Singapore.

The use of this map does not constitute, and should not be construed as constituting, an expression of a position by the BIS regarding the

legal status of, or sovereignty of, any territory or its authorities, to the delimitation of international frontiers and boundaries and/or to the

name and designation of any territory, city or area.

Source: R Auer, G Cornelli and J Frost, “Rise of the central bank digital currencies: drivers, approaches and technologies”, BIS Working Paper,

no 880, August 2020.

However, developing CBDC comes with a host of technological, legal and economic issues that

warrant careful examination before issuance. Central banks – the guardians of stability – will proceed

carefully, methodically and in line with their mandates. Issuing a CBDC is a national choice. Wherever

issued, CBDCs will be an additional payment option that coexists with private sector electronic payment

systems and cash. Careful design – such as the architecture defining the roles of the central bank and

private intermediaries – would ensure that they preserve the two-tiered financial system, and that

monetary policy implementation and financial stability will not be jeopardised.

In all this, the need for international coordination cannot be overstated. It is up to individual

jurisdictions to decide whether they issue CBDCs or not. But if they do, issues such as “digital dollarisation“

and the potential role of CBDCs in enhancing cross-border payments need to be addressed in multilateral

forums. The BIS is supporting this international discussion, ensuring that central banks can continue

learning from one another and can cooperate on key issues in design. In this way, central banks can work

together to support digital money ready for the economy of the future.

17/17You can also read