Emerging Vehicle Technologies - Finity Personal Lines Pricing and Portfolio Management Seminar 11 April 2013 - Finity Consulting

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Emerging Vehicle Technologies Finity Personal Lines Pricing and Portfolio Management Seminar 11 April 2013 © 2013 Finity Consulting Pty Limited

Presentation Outline

Emerging vehicle safety technologies

Re-format

• What are they?

• Potential impact

• Current market practice

• How long before these are widespread

Telematics

• Background and short history

• Benefits, challenges and business case

• Potential early adopters

Emerging Vehicle (Safety) Technologies

Forward Collision

Lane change warning

Tire-pressure avoidance Rollover prevention /

(blind-spot

monitoring technology (with mitigation

detection)

automatic braking)

Lane-departure Adaptive headlights

warning and Drowsy driver alert (cornering Smart headlights

prevention headlights)

Electronic stability Emergency response

control systems

3

Forward Collision Avoidance Technology

(FCAT)

4

Volvo Collision Avoidance with Emergency

Braking System

5

Forward Collision Avoidance Technology

(FCAT)

Currently Available

• Higher end manufacturers

• Volvo, Audi, Subaru, Lexus, Mercedes & Infiniti

• Standard or optional

• Effective operation at higher speed: Volvo (50-

70 km/h), Mercedes 200km/h

• Pedestrian Detection

Under Development • Backup collision intervention

• Collision avoidance using vehicle to vehicle

communication

6

Lane Change (Blind Spot) Warning 7

Lane Departure Warning & Prevention 8

Lane Change / Lane Departure Warning

and Prevention

Currently Available

• Higher end / European manufacturers

• Mercedes-Benz, Audi, BMW, HSV, Volkswagen,

Volvo, Porsche, Range Rover

• Standard or optional (majority)

• Intersection assistance

• Vehicle to vehicle communication technology

Under Development

9

Adaptive (Cornering) Headlights 10

Adaptive (Cornering) Headlights

Currently Available

• Higher end manufacturers

• Audi, Mercedes-Benz, BMW, Lexus, Acura,

Infiniti, Volkswagen, Citroen

• Mostly optional

• Adaptive brake lights

• Single-source fibre-optic lights

Under Development • Laser based headlights

• Infrared headlights (night vision)

• Self-levelling system (keeping lights on road when

driving over a bump)

11Some Studies show Technologies may

Reduce Accidents

Research

Technology Research Impact Research Source

Basis

Volvo XC60 vs.

Collision 20-30% lower IIHS Status Report, US Insurance

other mid-size

Avoidance PD claims cost 2011 claims data

luxury SUV

10-14% lower

Collision Vehicles where IIHS Status Report, US Insurance

PD claim

Avoidance FCAT is optional 2012 claims data

frequency

Centre for

Simulation 30 – 50% of all

Collision Automotive Safety NSW crash

based on injury injuries may be

Avoidance Research (Uni records

crash data prevented

Adelaide), 2012

Vehicles where

Adaptive adaptive 5-10% lower PD IIHS Status Report, US Insurance

headlights headlights are frequency 2012 claims data

optional

12Effectiveness influenced by driver

response

May generate false alarms

Less reliable on lower quality roads, poor weather or night

time

May be switched off

Risk compensation: Driver complacency or increase risk-taking

1320% Premium Reductions for FCAT?

"This is set to be reflected in our Insurance Australia Group -

pricing, and we would estimate including NRMA, SGIO and CGU -

that the cost of an insurance and Allianz support City Safety

premium for this vehicle will up with a 20 per cent reduction on

to 20 per cent cheaper than it insurance premiums.

would be if it didn't have the Volvo Australia spokesman Oliver Peagam

technology.“

(NRMA's research director Robert McDonald )

The benefits of Subaru’s EyeSight™ driver

assist system have been acknowledged

with a 20 per cent premium reduction on

Comprehensive Motor Insurance by

Allianz Australia.

http://subaru.com.au/news/eyesight-improves-20-cent-allianz

14Premium Relativity: FCAT vs. No FCAT

1.2

Premium Relativity (Premium model/Base)

1

0.8

0.6

0.4

0.2

0

GIO AAMI IAG Allianz

Volvo XC70 vs XC90 Subaru Liberty 2.5i Premium vs 2.5i Subaru Outback 2.5i Premium vs 2.5i

15Optional FCAT – Audi A6 16

Optional Lane Change / Departure – Volvo XC60 17

Vehicle Book Comparison

Glasses Redbook JATO

Explicit data fields

Features and Options Features and Options (flagged as standard,

Data structure

codes codes optional or not

available)

Yes, including separate

fields for features

Collision Avoidance No No (tighten seat belt,

warning light, brake

assist etc.)

Lane Change Warning Yes Yes No

Lane Departure

Yes No Yes

Warning

Adaptive Headlights No No Yes

18New ‘premium’ safety technologies quickly

become a standard feature of cars

Progression of Technology Implementation

100%

90%

Proportion of New Vehicles With Technology as Standard

80%

70%

60%

50%

40%

30%

20%

10%

0%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Year of Manufacture

Airbags ABS Brake Assist Electronic Stability Control

19Forward

Collision

Warning

Automatic Blind Spot

Parking Monitor

2013 Holden

VF SS-V

Series

Commodore

Rear Lane

Traffic Departure

Alert Warning

21Vehicle to Vehicle communication

Exchange • Vehicle velocity

info with • Acceleration

nearby • Position

vehicles

• Heading

• Activate collision

Enhance avoidance

current • Intersection assistance

technologies • Lane change warning /

mitigation

Enables • Crash-less car

future

technologies • Self-drive car

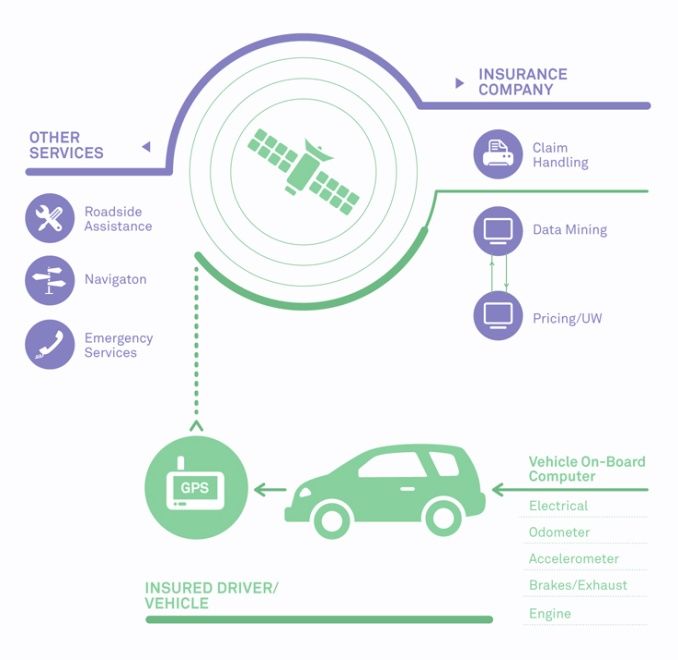

22Telematics

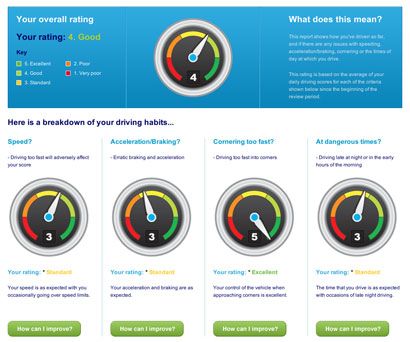

What is Telematics?

The basic infrastructure behind an insurance telematics system

24A (very) Short History

No. products

growing : AA, Co-

1st Generation UBI Real PAYD Op, State Farm, First Australian

products, patented Insurethebox comp motor

by Progressive telematics product?

1998 2000 2002 2004 2006 2008 2010 2012

2013

‘Pay-per-km’ style

products grow in 2nd Generation UBI products.

popularity US /

Europe / South Progressive launches Snapshot

25 Africa (now ~1m policies)What’s in the box?

GPS

Accelerometer

Gyroscope

Modem

Sim Card

Depends on the technology solution – doesn’t all have to be in the

box – can utilise mobile phone, on-board computerKey Rating Factors / Enabler

Accelerometer Acceleration / Braking

Gyroscope Cornering Speed

Distance Driven

GPS Speed (by road type)

Time of Day

27Benefits of Telematics

Lower Claims Cost Base

- Selection

- Driver behaviour

Retention & Cross-Selling

- Price positioning

- Customer engagement

Claims Handling & Fraud

- Location, time of day

- Fault determination

Ancillary

- Roadside assistance

- Petrol prices, parking

- Targeted marketingAustralia is Different

US and UK comprehensive policies cover both

bodily injury and property damage

Market issues especially in UK

Aggregators

Prohibitively high premiums for young

drivers

21 year old driver in London:

Ford Focus 2006 – from £2,650 (£2,200

with a box)

Holden Commodore GTX – from £6,500

“Gender Directive” in EU

29Segmentation Benefit Source: Market Finesse Source: Progressive

Pricing Dynamics 32

Pricing Dynamics 33

Some Key Drivers

“Lift” from additional factors

Decrease in cost from improvement in driver behaviour

Discount Required to Install Telematics

Portfolio mix – “selection” Device

Over 20%

Quantum of discounts / loadings

Required Discount

16% - 20%

Premium size

11% - 15%

Cost of device and infrastructure

6% - 10%

Potential market size

1% - 5%

0% 10% 20% 30% 40% 50%

34 Source: ProgressiveChallenges

Product Design

Privacy and Data Ownership

Pricing

Technology and Infrastructure

Analytical Capabilities

35Progressive were one of the trailblazers of

insurance telematics in the early 2000’s -

available in 42 states across the US

6-week monitoring period – no ongoing

monitoring

Utilises OBDII port - Device installed by

the user, delivered in post

No GPS. Not based on location or

speed - Rating on acceleration /

braking, distance, time of day

Premiums only adjusted downward,

maximum 30% discount.

36Smartbox

Collaborative product with a panel of

underwriters – CoverBox provides the

technology

Assessed every 90 days, initial

discount of 25%

Device installed by technician

Online ‘dashboard’ to view behaviour

– updated daily

60% policyholders log on 3 or more

time a week

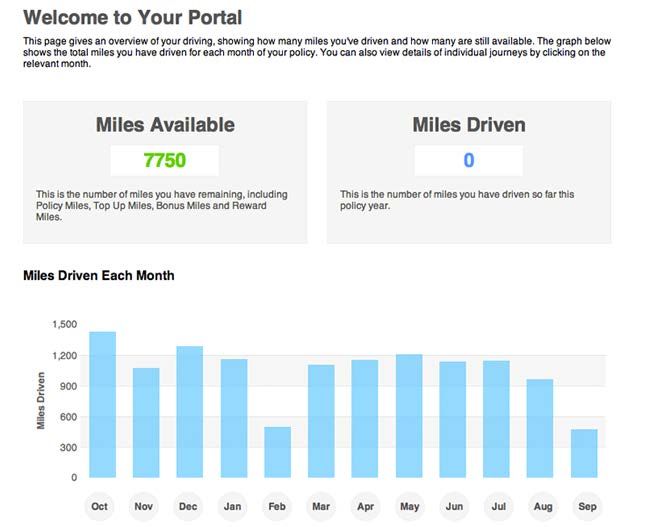

37“The UK’s Leading Telematics Insurer” –

Insurethebox website

Device installed by a technician –

behind the dashboard

No installation cost – they will come

to you

Gives away free miles rather than $

discounts

Claims 95% receive a discount on

renewal – average discount £601

Online ‘portal’ to view driving

statistics

38Potential Early Adopters

Coles

The South Africans

Motor clubs

Allianz

39Price Positioning in NSW

Coles is significantly more expensive for younger drivers and

40 parts of western SydneyThe South Africans

Hollard – “Pay-as-you-Drive”

~R60 (A$6) per month for device – provides distance and

behaviour summary statistics for the user

Real Insurance in Oz

Woolworths Insurance

Outsurance – “Safe_Driver@Out”

Behaviour monitored through out the year and considered

at next renewal

Maximum of 20% discount based on the experience

YOUI in OzMotor Clubs Different financial imperatives to big listed Seeking to maximise reach Need to remain relevant to young driver segment Good alignment with road safety advocacy position Offer range of aligned services eg roadside assistance, petrol pricing

Telematics technology in over 80,000

vehicles across 9 countries – primarily

Europe

A global telematics strategy – personal

and commercial lines

Allianz has a dedicated Telematics

division to explore global opportunities

Italy (2012)

Self-installed, OBDII

technology

Roadside assistance

~7% market share in the Australian

marketConclusions

Big changes afoot

Australian insurers slow to move

Coming

quicker than Some challenges involved

Pricing new

you might technologies Game changers?

think? Clearly

Telematics surmountable

Potentially large impact on

product design and pricing

Bigger incumbents will be slow

to moveDistribution & Use Reliances & Limitations

This presentation has been prepared for the Finity Consulting Finity wishes it to be understood that the information presented at

Personal Lines Pricing & Portfolio Management Seminar, held on 11 the seminar is of a general nature and does not constitute actuarial

April 2013. It is not intended, nor necessarily suitable, for any other advice or investment advice. While Finity has taken reasonable

purpose. care in compiling the information presented, Finity does not warrant

that the information provided is relevant to a particular reader’s

Third parties should recognise that the furnishing of this presentation situation, specific objectives or needs.

is not a substitute for their own due diligence and should place no

reliance on this presentation or the data contained herein which Finity does not have any responsibility to any attendee at the

would result in the creation of any duty or liability by Finity to the conference or to any other party arising from the content of this

third party. presentation. Before acting on any information provided by Finity in

this presentation, readers should consider their own circumstances

and their need for advice on the subject – Finity would be pleased to

assist.Contact

Nelson Henwood

Principal

Tel: +61 2 8252 3460

Mobile: +61 0438 656 341

www.finity.com.au

46You can also read