Epoch's Quarterly Capital Markets Outlook

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Epoch’s Quarterly

Capital Markets Outlook

WILLIAM W. PRIEST, CFA KEVIN HEBNER, PhD RICK VANDALE, CFA

Executive Chairman Managing Director, Global Managing Director, Global and

and Co-CIO Investment Strategist U.S. Portfolio Management

Thursday, June 24, 2021 | The webinar replay will be available on our website: www.eipny.com

The information contained in this presentation is distributed for informational purposes only and should not be considered investment advice or a recommendation of any particular

security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. The information contained in this

presentation is accurate as of the date submitted, but is subject to change. Any performance information referenced in this presentation represents past performance and is not

indicative of future returns. Any projections, targets, or estimates in this presentation are forward looking statements and are based on Epoch’s research, analysis, and assumptions

made by Epoch. There can be no assurances that such projections, targets, or estimates will occur and the actual results may be materially different. Other events which were not

taken into account in formulating such projections, targets, or estimates may occur and may significantly affect the returns or performance of any accounts and/or funds managed

by Epoch. To the extent this presentation contains information about specific companies or securities including whether they are profitable or not, they are being provided as a

means of illustrating our investment thesis. Past references to specific companies or securities are not a complete list of securities selected for clients and not all securities selected

for clients in the past year were profitable.

The Reopening Trade: Time to Favor Quality Growth?

Consumer: Key driver of economy well into 2022

• $2 tn savings: Pent-up demand

• Booming labor market: Rebound will take 2+ years

Shape of recovery: Does transitory mean 3 Qs or 3 years?

• Labor market: Supplementary jobless benefits expire by Labor Day for 10+ mn

• Commodities: Lumber prices won’t normalize until 2023+

• Semiconductors: Major headwind for IP recovery, especially autos

• Housing: Strong fundamentals, soaring prices

Key developments in H2: Good news already priced in?

• “Infrastructure”: Base-case is $3.0 tn with $1.5 tn in tax offsets, over 10 years, via reconciliation

• Employment & wage growth: Strong and, so far, no signs of accelerating wages

• Corporate earnings: Solid outlook, but revisions may soon peak

Five major risks: Beyond the inflation obsession

• COVID: Major risk in many EMs

• Inflation: Risks are highest in decades

• Taper tantrum: Does tapering mean hikes are imminent?

• DC policies: Corporate tax hikes, antitrust (Lina Khan, FTC)

• Valuations: Currently fair, conditional on low interest rates

2The Long Road Back to “Normal”: High Frequency, Micro Data

Open Table reservations (% chg from 2019) TSA # travelers (mn, 7dma)

Almost back to “normal”; Currently 12% below 2019 mean

NYC & LA are lagging,

Miami is booming

Google mobility: Retail & recreation activity Apple: U.S. mobility tracker

Transit almost back to pre-COVID;

3% below baseline (1/2020)

Baseline 1/2020

Source: Bloomberg, Open Table, TSA, Google, Apple 3Shape of Recovery: From Demand- to Supply-constrained

There has never been a V-shaped recovery:

# of months to return to peak employment

Every recovery since WWII: Same basic shape

• Months to return to pre-recession peak employment

o 2008: 75 mths

o 2001: 53 mths

o 1990: 37 mths

• We’re only 15 mths into this recovery!

Where did all the sawmills go?

Lumber prices: 3+ years to normalize

Source: Bloomberg, BLS

Source: Bloomberg, CME 4Celebrate Reopening: But Don’t Lose Sight of the Forever Virus

Nowhere near herd immunity

Vaccination rates are anything but uniform

• 14 U.S. states have full vaccination rates < 40%

Delta variant

• Won’t be last mutation of genetically unstable virus

Above global average Below global average

Source (all three charts): Our World in Data

5Will the Inflation Genie Escape?

"The least responsible economic policy in 40 years." Larry Summers, Harvard

Tempting FAIT: Three elements of America’s risky experiment

1. MMT/fiscal stimulus: To ensure “broad-based & inclusive” full employment

• What is upper limit on fiscal policy? Only limiting principle is inflation

2. Reopening + $2 tn consumer savings: “Roaring Twenties” redux?

• From demand- to supply-constrained

3. Monetary policy: Dual mandate reinterpreted, more tolerant of running hot

• FAIT: Flexible Average Inflation Targeting

• Jobs vs inflation

MMT: First ignored, then ridiculed and finally accepted

Old view: Economy typically operates near full employment

• So fiscal stimulus is dangerous: Will crowd out private sector and spur inflation

New view: Economy almost always operates well below full employment

• Fiscal stimulus is necessary: Inflation a remote risk, less costly than persistent unemployment

Why now? The dog didn’t bark

• No inflation in spite of massive fiscal stimulus, ZIRP, and multiple rounds of QE

“When it comes to the economy we’re building, rising wages aren’t a bug; they’re a feature.”

— President Biden

6Fed Overestimating its Abilities to Fine-tune Economy

Market suggests 40% chance CPI

will exceed 3% over next 5 years

“Keeping emergency settings after the emergency

has passed carries bigger risks for the Fed than

missing its inflation target by a few decimal points.”

— Stanley Druckenmiller

Inflation soared from late-1960s, was

walloped by Volcker, has been stable since

Three distinct inflation regimes since 1960

Source: Bloomberg, Minneapolis Fed

“We have the tools and the experience

to gently guide inflation back to target.”

— Lael Brainard, Fed Governor

Source: Bloomberg, NBER 7How Likely is a Repeat of The Great Inflation?

Shock therapy: Only way to slay inflation

The Great Inflation: Five key features

once expectations become unanchored

1. Complacency: Following long period of

Key events during Great Inflation of 1965-82 benign inflation (1953-65)

2. Accelerated govt spending (from 1964)

3. Fed prioritized jobs vs inflation (until ‘79)

4. Two OPEC supply shocks (9% of PCE)

5. Took many years: Multiple policy errors

The early-50s: A better historical analogy

GDP growth soared as Korean War

spending led to transitory burst of inflation

Source: Bloomberg, NBER, Minneapolis Fed

“In a rapidly changing world the opportunities

for making mistakes are legion.”

— Arthur Burns, Fed chair, 1970-78

Source: Bloomberg, NBER, Minneapolis Fed 8Investors Took a Beating During Great Inflation of 1965-1982

FIN likely to benefit from higher S-T inflation;

underperformers include TECH, HLTH & CONS A little inflation: +’ve cyclical signal

• But too much inflation is negative,

Correlation between 2Y inflation

signals end of cycle & recession

breakeven and equity sectors

Eight inflationary periods since 1925

• Average real return: -7%

o Non-inflationary periods: +10%

Equity markets typically tumble when

L-T inflation expectations rise

CORR with 5Y5Y inflation swap

Source: Bloomberg, Epoch Investment Partners

“For those who are quick to dismiss inflation, it is

worth remembering that it is a destructive force

… a genie that should be kept in the bottle.”

— Aswath Damodaran, NYU

Source: Bloomberg, Epoch Investment Partners 9Inflationary Pressures: Likely Transitory, but Risks Are Large

Four signals to watch

1. 5Y5Y: Currently 2.2% vs 2YBE of 2.7%

2. Wages: Compositional effects, focus on ECI and Atlanta Fed

3. Rents: Big weight in CPI & PCE, house prices booming

4. Bottlenecks: Semis, lumber, autos,… (relative price changes inflation)

• How long is transitory, 3Qs or 3Ys?

Two structural risks: Inflation is a policy choice

MMT: Keep pushing the envelope. The endgame for MMT is inflation.

• Divided govt is best insurance against inflation: 50 Senators not enough

Fed: Prioritizing jobs over price stability

• FRB has six members: Powell’s term ends in Feb, the two Vice Chairs before then

"There are slippery slopes, and once you start a process of accelerating inflation there

are precious few examples of where inflation has been brought back down without very

substantial economic disruption and without enormous disruption to financial markets.”

— Larry Summers, Harvard

10The Fed’s Next Policy Action: A Taper Tantrum is Unlikely This Time

Tapering to be announced in Q3 Tapering doesn’t mean hikes are imminent

Commencing in Q4,

initially with MBS

10Y yield: Round trip in 2013-14 Equities performed well despite the tantrum

Tantrum

Source for all charts: Bloomberg, FRB, NBER

11A Second Likely Policy Action: Higher Corporate Taxes

Proposed corporate tax: From 21% to 28%

Tax hike to 28%: Mild headwind for EPS

• Hit to SPX EPS of 5% to 8% in 2022

o Higher in tech & healthcare

• Consensus: 25% is more likely than 28%

Global minimum tax

• US corporate profits booked in tax havens

o 5% of foreign profits in 1965, 60% today

• Will mainly affect 45 companies

o Mostly in tech & healthcare

Source: U.S. Treasury Department

Corporate tax share: Shrinking Corp tax receipts, select countries (% GDP)

Source: Bloomberg Source: U.S. Treasury Department, "The Made in America Tax Plan"

12Value vs Growth: SVX Usually Outperforms Early Cycle

Twenty-five-year perspective Performance during pandemic: Three phases

Value typically performs with real yields Both SVX & SGX trading close to fair value

Correlation: 80%

SGX’s earnings & CF growth

has been much stronger

Source for all charts: Bloomberg, Epoch Investment Partners, NBER

13Equity Market: Fairly-Valued, Conditional on Bond Yields

SPX: EPS with consensus forecasts

Earnings growth Consensus

• Strong rebound: Already priced in? 2019-21: 11% (annualized)

2022: 12%

2023: 6%

Valuations

• Neutral-ish: Assuming lower for longer rates

Speculative excesses abound

• Reflecting excessive liquidity, “free” money

If interest rates stay near current range, equity markets appear fairly-valued

Source (all 3 charts): Bloomberg, Epoch Investment Partners, NBER

14America’s Risky Economic Experiment: Investment Conclusions

1. Strongest GDP Growth Since 1984: Consumer-driven

• Supportive policy: But both fiscal & monetary impulses have peaked

• Reopening + massive savings: Strongest rebound in service sectors

2. Market Risks

• COVID: The forever virus, especially EMs

• Inflation: Likely transitory, but watch for wage-price spiral

• Taper tantrum: Tapering imminent hikes

• DC policies: Corporate tax hikes, antitrust

• Valuations: Fair, provided rates stay low & FCF meets high expectations

3. Portfolio Positioning as Re-opening Trade Matures

• Quality growth: Sustainable FCF growth

• Capital allocation: Especially important as CF recovers

• Global Champions: Winner-takes-most economy

4. What is Your Business Strategy for the Digital Age?

• We remain focused upon firms with resilient business models and strong FCF growth

o We look for a demonstrated ability to allocate that CF effectively between return of capital

options and reinvestment/acquisition opportunities

• It is imperative that companies successfully implement a business strategy for the Digital Age

o Especially favors companies in tech, healthcare, and communication sectors

15The COVID-19 Crisis Created a Historic Opportunity

Opportunity to buy companies in the U.S. Small Cap universe at very

reasonable prices.

R2000 (Small Cap) vs. R1000 (Large Cap)

Performance as of September 30, 2020

20%

15%

10%

5%

0%

-5%

-10%

QTD YTD 1 Year 3 Year 5 Year 10 Year

◼ Russell 2000 4.9 -8.7 0.4 1.8 8.0 9.9

◼ Russell 1000 9.5 6.4 16.0 12.4 14.1 13.8

Small Cap underperform Large Cap across all time periods depicted.

Source: Epoch Investment Partners; Frank Russell Company ("Russell").

16Small Caps Outperforming Large Caps Since Vaccine Breakthrough

R2000 (Small Cap) vs. R1000 (Large Cap)

Performance as of June 18, 2021

60.0

49.8

50.0

40.0

31.4

30.0 27.7

20.0

13.7 12.7

10.0 5.9 5.2

1.0

0.0

4Q 2020 1Q 2021 2Q 2021 9/30/2020-6/18/2021

R2000 R1000

Source: Epoch Investment Partners; Frank Russell Company ("Russell").

17Window of Opportunity Remains Open for Small Caps

Historically, small caps have been one of the best performing asset classes following a

sharp decline in the market.

25 Worst Rolling Quarter Small Cap Returns Since 1926

50%

37.8%

40%

30%

20.8%

20% 15.2%

12.5% 10.7%

6.9% 8.2% 5.8%

10%

0%

-10%

-20%

-30% -23.6%

-40% -34.6%

-50%

Trailing Quarter 1 Year Return 3 Year Return 5 Year Return 10 Year Return

Large Cap Small Cap

Period ending March 31, 2020 QTD Return

Russell 2000 Index (small cap) -30.6

Russell 1000 Index (large cap) -20.2

Source: Ibbotson Associates

18Window of Opportunity Remains Open for Small Caps

Historically, small caps have performed better in higher GDP environments.

Small cap sales, earnings, and cash flows are levered to better economic U.S. growth and when

U.S. GDP grows quickly, especially well above 2%, small caps tend to perform much better.

Russell 2000 Returns During Different GDP Environments

Average Return Median Return

Real GDP Range # Instances

(Current year) (Current Year)

0 – 2% 7 2.4% -1.6%

2 – 4% 18 13.0% 16.3%

> 4% 9 12.7% 21.3%

US Real GDP Growth 2020 2021(E) 2022 (E)

-3.5 6.4 3.5

Source: eVestment – https://www.macrotrends.net/countries/USA/united-states/gdp-growth-rate

19Window of Opportunity Remains Open for Small Caps

Small cap fundamentals look superior to large caps

Expected Sales Growth Expected Earnings Growth

14.0 120

13.0

101.8

12.0

10.8 100

10.0

80

8.0 7.3

6.4

60 53.0

6.0

4.0 40

31.5

2.0

20

8.7

0.0

2021E 2022E

0

2021E 2022E

R2000 (Small Caps) S&P 500 (Large Caps) R2000 (Small Caps) S&P 500 (Large Caps)

Source: Epoch Investment Partners; FactSet

20Window of Opportunity Remains Open for Small Caps

Small cap relative valuations remain near all time lows

R2 ex. Biopharma / SP5, Relative P/E

180% 180%

170% 170%

160% 160%

150% 150%

140% 140%

130% 130%

120% 120%

110% 110%

100% 100%

90% 90%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

NTM FY2

Source: Fury Research Partners, FactSet.

21Window of Opportunity Remains Open for Small Caps

Small cap flows could prove favorable

Small-Cap Flow s

In millions of dollars

10000

-30000

-70000

-110000

-150000

Dec-03 Jun-05 Dec-06 Jun-08 Dec-09 Jun-11 Dec-12 Jun-14 Dec-15 Jun-17 Dec-18 Jun-20

The Nasdaq 100’s market capitalization is $14.8 trillion versus $1.2 trillion for the S&P Small-Cap 600.

Source: EPFR; Jefferies

22What's Driving the Rally in Small Caps?

To date lower quality companies have led the rally in small cap equities accentuated by the

wild speculation in "Meme" stocks.

S&P SmallCap S&P SmallCap S&P 600 SmallCap Low Quality versus High

600 Quality – 600 Quality - Quality Index

Highest Quintile Lowest Quintile

160

Index (USD) Index (USD)

150

YTD 11.5% 39.5%

140

130

120

110

100

S&P SmallCap 600 Quality

S&P SmallCap 600 Quality - Lowest Quintile Index (USD)

Source: S&P Dow Jones Indices LLC. As of June 18, 2021

23What's Driving the Rally in Small Caps?

Beware the "Meme" stocks

Definition:

A meme stock is a stock that has seen an increase in volume and stock price, not because of the

company’s performance, but rather because of hype on social media and online forums. For this reason,

these stocks often become overvalued, seeing drastic price increases in just a short amount of time.

YTD Return ROE 5-Year Avg

GameStop Corp 1,252.7% -22.1%

AMC 2,357.7% -97.8%

500%

424% R2V Total Return

400%

300%

200%

100%

100%

28.8% 31.5%

7.1% 8.6%

0%

Meme Stocks Other Stocks Index

YTD QTD

Source: FRP, FactSet; as of 6/9/21; Meme stocks are AMC, BBBY, CLNE, EXPR, GME, GEO, and WKHS.

24Advocating a High-Quality Approach

High and low FCF Yield and ROE quintiles indexed to 100 (last 35 years)

CAGR 1986-2020 (35 Years) CAGR 1986-2020 (35 Years)

HIGH FCF YIELD (Q1) RUSSELL 2000 15.1% HIGH ROE (Q1) RUSSELL 2000 11.5%

LOW FCF YIELD (Q5) RUSSELL 2000 -0.7% LOW ROE (Q5) RUSSELL 2000 0.4%

RUSSELL 2000 VALUE 10.2% RUSSELL 2000 VALUE 10.2%

RUSSELL 2000 9.7% RUSSELL 2000 9.7%

16,000 5,000

13,554 4,566

14,000 4,500

4,000

12,000

3,500

10,000 2,969

3,000

2,553

8,000 2,500

2,000

6,000

1,500

4,000 2,969

1,000

2,000 2,553 500

100

100 117

78

- -

High ROE (Q1) Russell 2000 Value

High FCF Yield (Q1) Russell 2000V

Russell 2000 Low ROE (Q5)

Russell 2000 Low FCF Yield (Q5)

As of December 31, 2020

Source: Russell, Jeffries, Epoch Investment Partners

25Advocating a High-Quality Approach

High quality small caps are as cheap as they ever have been.

R2 Relative Median P/E (High Quality vs. Low Quality)

120% 120%

100% 100%

80% 80%

60% 60%

40% 40%

20% 20%

0% 0%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

NTM FY2

Source: Fury Research Partners, FactSet.

26Advocating a High-Quality Approach

Quality lags off bear market bottoms and then recovers

R2 High Quality / R2, Relative Index, Monthly

1.05

1.00

0.95

0.90

0.85

-8

-6

-4

-2

0

-24

-22

-20

-18

-16

-14

-12

-10

+2

+4

+6

+8

+10

+12

+14

+16

+18

+20

+22

+24

+26

+28

+30

+32

+34

+36

Months Before/After Market Trough (0 = Trough Month)

Feb-03 Feb-09 Mar-20

Source: Fury Research Partners, FactSet.

27Advocating a High-Quality Approach

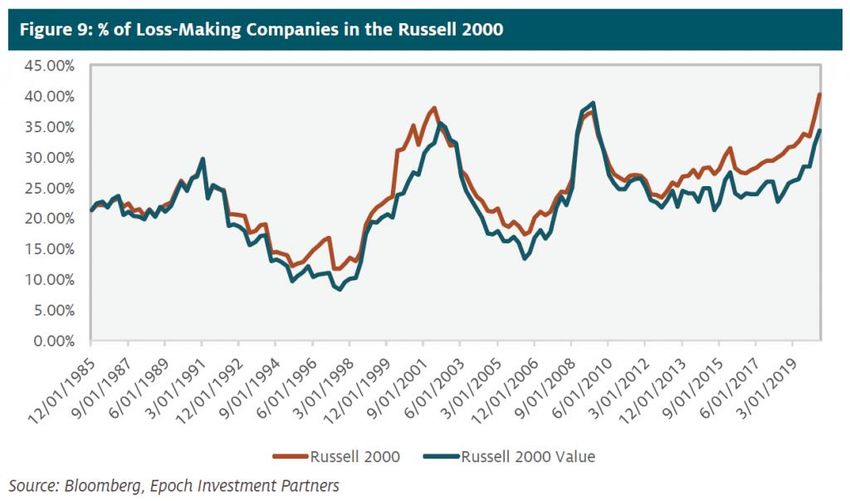

Passive solutions lead to large exposures in loss-making companies

28The Small Cap Opportunity from Our Perspective

▪ Small Caps had underperformed Large Caps for almost a decade.

▪ The onset of the pandemic accelerated this trend, providing an attractive

opportunity.

▪ While Small Caps have outperformed Large Caps since 3Q 2020, the

window on the Small Cap opportunity has not closed in our opinion.

▪ We advocate taking a high-quality approach to Small Cap investing based on

superior fundamentals and historical precedent.

▪ We also advocate an active versus passive approach due to the index's large

exposure to loss-making companies.

29Epoch Thought Leadership

RECENT PUBLICATIONS AND WHITE PAPERS

Podcast – Actively Speaking Moore’s Law & the Race for the

Our latest releases: Rest of the Chessboard

Jun. 16, 2021 The Cambrian explosion of breakthroughs in AI,

Will the Inflation Genie Escape autonomous driving, 5G, and cloud computing will

drive double-digit growth in semiconductor

May 27, 2021

revenues for the foreseeable future. Superstar

Money 3.0: Central Bank Digital Currencies

firms have come to dominate all subsectors of the

(CBDC)

increasingly concentrated semiconductor industry.

America’s Risky Experiment: Will the The Epoch Core Model:

Inflation Genie Escape? Our Proprietary Stock Model

Inflation risks are at a four-decade high due to More than just our proprietary stock selection

today’s combination of a generous Treasury, an model, the Epoch Core Model (ECM) is a

overly tolerant Fed, and a reopening economy. rules-based expression of Epoch’s free cash

Investors should brace themselves for more flow investment philosophy. Learn about its

inflation scares, which will likely remain a key driver components and how it’s being used to

of equity markets well into 2022. enhance the firm’s investment processes

across strategies.

Money 3.0: Central Bank Digital Winning at Active Management

Currencies (CBDC) Authored by three Epoch portfolio managers,

During the past two years, CBDC has progressed the book examines the issues facing the

from a bold speculative concept to a seeming investment management industry and

inevitability and core feature of our financial explores the essential roles of culture,

ecosystem. This paper explores the implications for philosophy and technology.

monetary policy, the FinTech and payments sectors,

and the potential disintermediation of significant

swaths of the commercial banking system.

30You can also read