Fed signals eventual shift from easy-money pandemic policies - USD Interest Rates Update

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

USD Interest Rates Update

June 2021

Fed signals eventual shift from

easy-money pandemic policies

AUB Group

Treasury Sales Team

Interest Rate Risk Management Solutions

1

Executive summary

Background

Federal Open Market Committee’s April 27-28 policy meeting minutes were released on 19th May 2021. Given below are the key takeaways

from same;

▪ There was less unanimity about the timeline for considering a tapering in asset purchases. “A number” of meeting participants suggested “it

might be appropriate at some point in upcoming meetings to begin discussing a plan” for tapering -- a shift from March, when there was no

such suggestion.

▪ Federal Reserve officials had a discussion about financial stability in the wake of the run-up in asset prices and the Archegos affair. “A couple

of participants remarked that, should investor risk appetite fall, an associated drop in asset prices coupled with high business and financial

leverage could have adverse implications for the real economy.”

▪ The discussion around the outlook for growth and inflation evolved from March, with participants assessing that “risks to the outlook were no

longer as elevated as in previous months.” And “some participants mentioned upside risks around the inflation outlook that could arise if

temporary factors influencing inflation turned out to be more persistent than expected.” There was a discussion about signs of a shortage of

labor, which were later confirmed by the April jobs report. “Some participants noted that the step-up in demand for labor had started to put

some upward pressure on wages.”

▪ The minutes also showed participants discussing the merits of standing repo facilities for both domestic and foreign institutions, noting that

the benefits outweighed the costs.

Interest rate strategy

In the midst of a heightened uncertainty, we keep seeing selective opportunities in the current market environment:

❑ hedge medium to long-term risk via Interest Rate Swap to take advantage of the current low rate environment: with Fed rates close to zero

this provides a very good entry point for clients looking to hedge their long term floating rate exposures;

❑ along the same lines, forward-starting IRS seem to offer decent value given the relatively flat yield curve;

❑ alternative hedging strategy structured via options (like Interest Rate Collar).

2

Interest Rate Markets

3

April Fed meeting update

Fed holds target for benchmark rate unchanged at 0 to 0.25%

▪ The FOMC left rates unchanged, maintained its bond-buying pace and

didn’t provide any new guidance for when those policies might change.

▪ Powell also said it’s not time to begin talking about tapering the Fed’s

bond-buying program. He reiterated that the central bank was still

planning on communicating such a decision “well in advance,”

but noted throughout the press conference that they still see the

economy as far from the “substantial further progress” marker they’ve

made a pre-condition for such a move, repeating that it will still be

“some time” before it’s met.

Economic assessment pointed toward improving economy

▪ During his press conference, Powell read a lengthy statement in

response to a question about whether the Fed was worried that

inflation might get out of control. It was a forceful display of

confidence that Fed officials are absolutely not worried about that

happening.

▪ Marking a clear improvement since the pandemic took hold more than

a year ago, the Fed said that “risks to the economic outlook remain,”

softening previous language that referred to the virus posing

“considerable risks.” The statement also noted that sectors hit hardest

by the Covid-19 pandemic had “shown improvement.”

Market reaction

▪ The dollar remained lower on the day, and most Treasury yields

dropped after the FOMC decision, with traders likely most focused on

the idea that it’s not yet time to taper and that policy makers will be

looking past higher inflation.

Data source: Bloomberg

4

A look at current interest rates environment

Fed officials signal open to taper talk at ‘upcoming meetings’

▪ Some Federal Reserve officials were open to a debate at “upcoming

meetings” on scaling back their massive bond purchases, a record of

their April gathering showed, potentially putting taper talk on the table

as early as next month.

▪ The U.S. labor market posted strong gains in March, the most recent

month for which Fed officials had data at the April meeting. Policy

makers have since said they’d need to see continued strength to

indicate that the economy was on its way to meeting the Fed’s test to

scale back bond buying.

▪ Fed officials reiterated that they need to see progress in actual data

and not just forecasts in order for the recovery to meet that test,

according to the minutes.

▪ While a number of them noted that the economy was making “rapid

progress” toward the central bank’s goals, that was before a

disappointing April jobs report that also revised down the March

figures.

▪ The Fed’s massive asset-purchase program is designed to support the

economy though the pandemic by lowering borrowing costs on

everything from auto loans to houses. While there are signs the

recovery is still uneven, some officials have argued that a hot property

market is reason enough for the central bank to consider curbing its

purchases of MBS.

▪ Fears of higher inflation have unsettled some investors in recent weeks

amid rising commodity prices, while Fed critics argue that its ultra-easy

policies, combined with massive U.S. fiscal stimulus, risk overheating

the economy.

▪ In their comments about inflation, Fed officials said that a jump in

demand along with some bottlenecks in supply would likely push

inflation measures above 2% in the near term.

Data source: Bloomberg

5

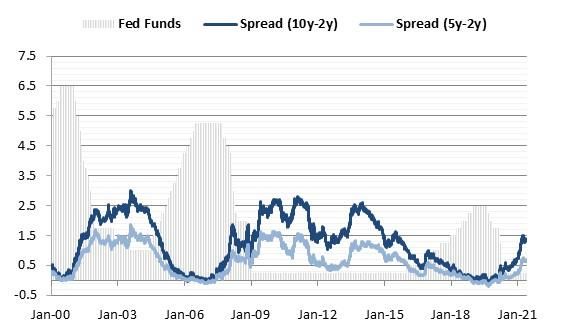

Historical perspective

10y swap rate did not move much post April Fed Meeting

▪ For Jan’21 to end of March’21, we saw rates moving up rapidly – 10y

US Swap rates nearly doubled -- moved from 92bps to 180bps. But

since then the rates have either remained subdued or moved a bit

lower.

▪ Markets are predicting the Federal Reserve and Bank of England will

both starting raising interest rates at about the same time. U.S. policy

makers will get there first, according to many leading strategists.

▪ Interest-rate swaps are pricing in about 16 basis points of hikes from

both the Fed and BOE by the end of next year, with the spread

between Fed funds and sterling contracts pretty much flat.

Interest rates monitor: statistics (January 2000 – May 2021)

10yr IRS 5yr IRS 2yr IRS

Historical

Average 3.554 2.971 2.327

Max 7.871 7.795 7.666

Min 0.506 0.243 0.179

Current 1.5933 0.9114 0.2500

From Average -1.961 -2.059 -2.077

From Max -6.278 -6.884 -7.416

D

From Min 1.087 0.668 0.071

6m $Libor 3m $Libor

Historical

Average 2.094 1.958

Max 7.109 6.869

Min 0.179 0.147

Current 0.1788 0.1470

From Average -1.915 -1.811

From Max -6.930 -6.722

D

From Min 0.000 0.000

Data source: Bloomberg

6

Market forecast

All forecast updated as of 21 May 2021 Data source: Bloomberg

7

Main Economic Indicators

8

Economic activity: Consumers and Business

U.S. recovery gains steam as spending fuels 6.4% GDP growth

▪ U.S. economic growth accelerated in the first quarter as a rush of

consumer spending helped bring total output to the cusp of its pre-

pandemic level, foreshadowing further impressive gains in coming

months.

▪ Gross domestic product expanded at a 6.4% annualized rate following a

softer 4.3% pace in the fourth quarter, the Commerce Department’s

preliminary estimate showed. Personal consumption, the biggest part

of the economy, surged an annualized 10.7%, the second-fastest since

the 1960s.

▪ Rising vaccinations, faster job growth and two rounds of federal

stimulus payments combined to supercharge household spending. As

government restrictions on activity are widely lifted, consumer

demand is seen broadening and driving outlays for long-downtrodden

services such as travel and leisure.

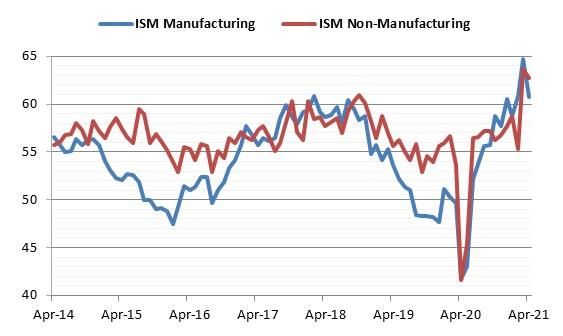

Service-sector vigor persists despite modest slide

▪ A retracement in the April ISM services index follows a surge to an all-

time high in the prior month. The record reading in March not only

reflected the sector’s rapid reopening, but also a rebound from the

winter freeze. With those tailwinds absent from the April tally, a

modest reversal is not surprising.

▪ The level of the headline index still reflects a booming recovery in

services and reinforces our projections for the sector to emerge as a

key driving force behind economic growth over the next couple of

quarters.

▪ Lengthening delivery times highlight that supply shortages are not only

affecting the manufacturing sector, but “supply chain is challenged at

every level” in the service sector as well.

Data source: Bloomberg

9

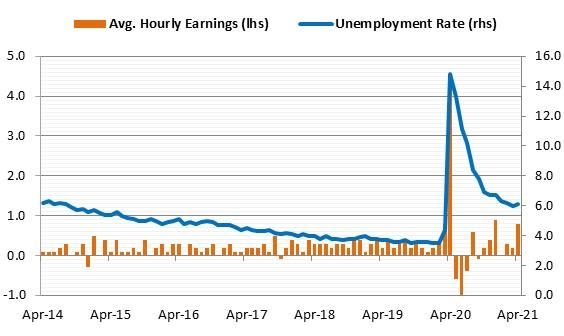

Labor market

U.S. job growth disappoints in challenge to economic recovery

▪ U.S. job growth significantly undershot forecasts in April, suggesting

that difficulty attracting workers is slowing momentum in the labor

market and challenging the economic recovery.

▪ Payrolls rose 266,000 from a month earlier, that represented one of

the largest downside misses on record. Economists in a Bloomberg

survey projected a 1 million hiring surge in April.

▪ The unemployment rate edged up to 6.1%, though the labor-force

participation rate also increased.

▪ The report stunned investors as Treasury yields plunged and the dollar

turned sharply lower. U.S. stocks rose on expectations that monetary

policy will remain conducive to economic growth for a sustained

period. The eurodollar market pushed back its pricing for a Federal

Reserve rate increase to mid-2023.

Data source: Bloomberg

10Inflation outlook

U.S. consumer prices jump most since 2009, outpacing estimates

▪ U.S. consumer prices climbed in April by the most since 2009, topping

forecasts and intensifying the already-heated debate about how long

inflationary pressures will last.

▪ The consumer price index increased 0.8% from the prior month,

reflecting gains in nearly every major category and a sign burgeoning

demand is giving companies latitude to pass on higher costs. Excluding

the volatile food and energy components, the so-called core CPI rose

0.9% from March, the most since 1982.

▪ The gain in the overall CPI was twice as much as the highest projection

in a Bloomberg survey of economists. Similar to last monthly jobs

report, forecasters are struggling to get a handle on the rapidly

reopening economy.

▪ The report showed sharp increases in prices for motor vehicles,

transportation services and hotel stays as businesses hardest-hit by the

pandemic reopen more broadly and vaccinated Americans resume

social activities and travel.

▪ Treasury yields rose and bond-market gauges of future price pressures

jumped to multiyear highs after the report, while short-end interest

rate pricing showed increased odds for a Federal Reserve hike as early

as late-2022. The dollar rose with yields, while U.S. stocks fell.

▪ The annual CPI figure surged to 4.2%, the most since 2008 though a

figure distorted by the comparison to the pandemic-depressed index in

April 2020. This phenomenon -- known as the base effect -- will skew

the May figure as well, likely muddling the ongoing inflation debate.

▪ At the same time, annualized inflation over the past three and six

months has shown a clear acceleration.

Data source: Bloomberg

11Asset prices and the wealth effect

Is the equity market slump in horizon ?

▪ The Dow Jones, the S&P 500 and the Nasdaq have been extremely

volatile in the last three weeks, reacting to news about President

Biden's proposed capital gains tax, Treasury Secretary, Yellen’s

comments on inflation, Elon Musk's tweets about bitcoin, and weekly

unemployment reports. Investors have been on a rollercoaster ride,

wondering whether the dreaded stock market slump is on the horizon.

▪ Earnings per share (EPS) for 90% of the S&P 500 companies increased

by 46% year on year (YOY), rather than the expected 20%. 68%

outperformed the consensus by one standard deviation. Financials and

consumer discretionary both experienced 135% and 187% EPS growth,

respectively. Despite the strong performance, the broader markets are

down from a month ago. That is because markets had already

anticipated earnings growth and the fear of rising inflation. Daily data – Base = 100 on 1 January 2013

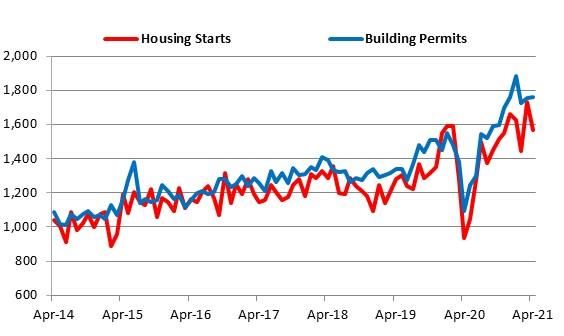

U.S. housing starts trail estimate, hinting at supply chain woes

▪ U.S. housing starts fell by more than forecast in April, suggesting that

supply-chain constraints and rising materials costs continue to hold

builders back.

▪ Construction has been held back in recent months by supply chain

constraints as well as higher materials costs, particularly for lumber.

That said, strong demand for residential real estate, fueled by low

borrowing costs, is expected to bolster the housing market in the

coming months.

▪ Backlogs continued to mount as the number of homes authorized for

construction but not yet started rose 5% from the prior month, the

data showed. Applications to build, a gauge of future construction,

rose 0.3% to an annualized 1.76 million, exceeding the pace of starts.

Data source: Bloomberg

12Beyond the headlines…

Fed acknowledged that the run up in asset prices is heating up, A number of participants proposed to initiate the discussion on

and should the investor risk appetite fall and with the amount tapering sooner rather than later, this is shift from march

of leverage involved, the risk to real economy would be high. meeting where the wait and watch approach was mentioned.

Fed officials reiterated that they need to see progress in actual Fed officials said that a jump in demand along with some

data and not just forecasts in order for them to start thinking of bottlenecks in supply would likely push inflation measures

taking any tapering action. above 2% in the near term

U.S. job growth significantly undershot forecasts in April, Rising vaccinations, faster job growth and two rounds of federal

suggesting that difficulty attracting workers is slowing stimulus payments combined to supercharge household

momentum in the labor market. spending.

Labor market concerns, risk associated with sharp fall in asset We acknowledge that there is a possibility of things moving

prices and the lack of consistent positive economic data may back to track much sooner post vaccinations, and thereby

not allow Fed to move the rates in near future. leaving room for a potential hike sooner rather than 2023.

What is your view?

13Interest Rate Hedging

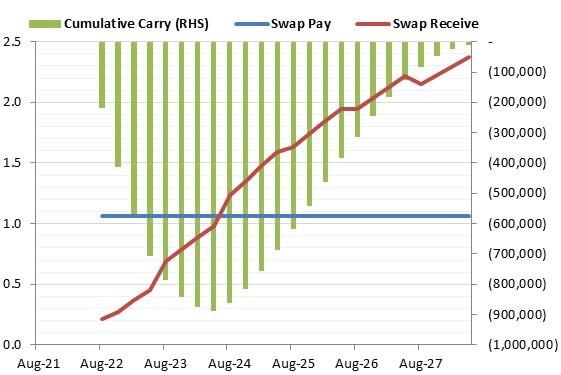

14Hedging – Vanilla Interest Rate Swap

Description Indicative Terms*

Initial Notional of USD 100mn,

▪ An IRS is a highly liquid and very wide-spread derivative instrument Notional

Equally amortizing over the tenor

used as the basic tool to hedge interest rate risk.

▪ It is an agreement between two parties to exchange periodic Start Date Spot

interest payments based on a fixed interest rate against payments

Tenor (alternatives) 5 years 7 years 10 years

based on a floating interest rate (e.g.: 3m $Libor), calculated on a

notional amount and for a specified tenor.

Fixed rate paid 0.57% 0.83% 1.14%

▪ If coupled with a floating rate loan, the IRS eliminates the exposure

to rising interest rate payments by creating a “synthetic” fixed Floating rate received 3m $Libor, quarterly reset

interest rate loan.

Payments Quarterly, act/360

Main features / drawbacks

✓ Absolute certainty over future cash flows, supporting budgeting

and planning exercise and easy accounting treatment (hedge

accounting – no impact on P&L under certain assumptions).

✓ Flexibility over the loan amount (also with an amortizing profile)

and tenor to be hedged, allowing for partial notional and shorter

tenor than the full one.

✓ Can be structured in a fully Islamic format.

The borrower cannot benefit if Libor drops as they have locked in a

fixed rate through the IRS.

Should Libor rise less than current market expectations (forward

rates), the overall cumulative carry would be negative.

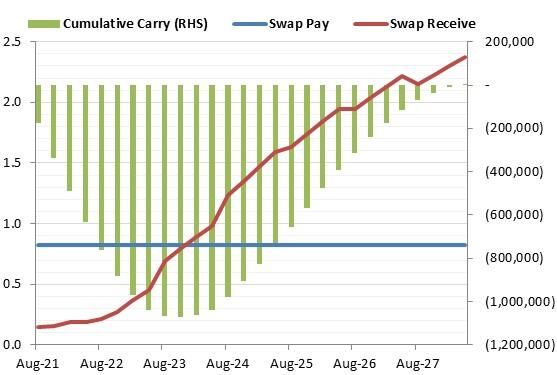

*The levels shown are mid-market levels and do not include any credit and liquidity related charges 15Hedging – Forward-start Interest Rate Swap

Description Indicative Terms*

Initial Notional of USD 100mn,

▪ While an IRS allows borrowers to eliminate their risk and avoid Notional

Equally amortizing over the tenor

unwanted fluctuations in their interest payments, client can

further reduce fixed rate to be paid by using a forward-start IRS – Start Date 1 year 2 years

due to current shape of rates forward curve.

Tenor (alternatives) 4 years 6 years 3 years 5 years

▪ For example, in a 1yr forward-start IRS the deal is concluded

(hence, the rate is fixed) on the Trade Date, but the exchange of

Fixed rate paid 0.78% 1.07% 1.13% 1.40%

flows starts in one year (Start Date).

▪ Hence, between Trade Date and Start Date – if the borrower hold a Floating rate received 3m $Libor, quarterly reset

view that rates will go further down before rising up in future –

then they can still benefit from the low Libor. Payments Quarterly, act/360

Main features / drawbacks (compared to a vanilla IRS)

✓ Client can benefit from short term rates remaining low for 1y or 2y

and at the same time can be hedged for any rise in rates

thereafter.

The client achieves a slight negative carry initially. The initial

difference between the floating rate received and the fixed rate

paid is negative – this is offset by later positive cash-flows.

Client in unhedged for the period between Trade Date and Start

Date of the forward IRS.

*The levels shown are mid-market levels and do not include any credit and liquidity related charges 16Hedging – Interest Rate Collar

Description Indicative Terms*

Notional Equally amortizing over the tenor

▪ An Interest Rate Collar is an option on a reference interest rate

that would give the buyer a best case and worst case rate. Start Date Spot

▪ As a hedging tool, it works to protect a floating rate borrower

(Collar buyer) should the reference interest rate (e.g.: 3m $Libor) Tenor (alternatives) 5 years 7 years

rise above a certain threshold (Cap Strike) but should the reference

interest rate (e.g. 3m $Libor) fall below a certain level (Floor Strike) Cap Strike (alternatives) 2.00% 2.50%

client has a minimum rate to pay.

Floor Strike (alternatives) 0.30% 0.40%

▪ An Interest Rate Collar combines buying a Cap and selling a Floor,

the sale of the floor allows the borrower to reduce the cost of the Underlying Index 3m $Libor, quarterly reset

hedge while still allowing him to benefit from lower Interest Rates

up to a certain level. Payments Quarterly, act/360

Main features / drawbacks (compared to a vanilla IRS)

✓ Full protection above the Cap Strike, with the possibility to benefit

should Libor fall up to the floor level.

✓ Worst-case scenario and Best-case scenario is known at inception.

✓ Current market environment (flat to negative yield curve) allows

Collar levels to be attractive

✓ No cash flow if markets remain between the cap and floor

If Markets fall below floor, client will pay the floor which at the

time will be above market levels, yet still it is lower than the

current vanilla swap.

*The levels shown are mid-market levels and do not include any credit and liquidity related charges 17Disclaimer and contact details

Bahrain Treasury Sales

Sameh Baqer Ali Ghuloom

+973 17585823 +973 17585829

Sameh.Baqer@ahliunited.com Ali.Ghuloom@ahliunited.com

Talal Alhaiky Sami Rafia

+973 1758 5824 +973 17585822

Talal.AlHaiky@ahliunited.com Sami.Rafia@ahliunited.com

Sidharth Dubey

+973 17567105

Sidharth.Dubey@ahliunited.com

DISCLAIMER

This document has been prepared and issued by Ahli United Bank B.S.C. (“AUB”) which is regulated by the Central Bank of Bahrain.

All recipients of this document should note that it is being furnished to them solely for information purposes and may not be reproduced or redistributed

to any other person without the permission of AUB.

Although information has been obtained from and is based upon sources believed to be reliable, AUB does not warrant its accuracy and it may be

incomplete or condensed.

All opinions and estimates constitute AUB’s judgment at the date of publication and are subject to change without notice.

AUB does not advise as to the suitability or otherwise of this information and provides the information to recipients exclusively on the basis that they

have sufficient knowledge, experience and / or professional financial, legal, tax and other advice to make an independent assessment thereof.

18You can also read