Fertilizers - GPCA Fertilizer Convention

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

September 2019

Mapping fertilizer trends in major producing regions

Oliver Hatfield, VP Business Development, Argus Media Ltd

Market Reporting

Fertilizers

Consulting

Fertilizers

illuminating the markets

illuminating the markets

Copyright © 2019 Argus Media group.

All rights reserved Events

Disclaimer and Notices This presentation (the “Report”) is confidential, made available strictly under licence and has been prepared solely for the internal use of the applicable Argus licensee (a “Client”). Any use or disclosure of this Report and its contents without specific written permission from Argus is strictly prohibited. No duty of care is owed by Argus to any third party and Argus disclaims all liability in relation to any third party who seeks to rely upon or use the Report or any of its contents. The Report, including the Argus trademarks and logo/legal notices, may not be altered. Derivative works of all or part of the Report may not be created without prior written permission. The data, information or opinions contained in this Report are provided on an “as is” basis without any warranty, condition or other representation as to its accuracy, completeness, or suitability for any particular purpose and shall not confer rights or remedies upon the recipients of this presentation or any other person. Data and information contained in the Report come from a variety of sources, some of which are third parties outside Argus’ control and some of which may not have been verified. Argus does not warrant that this Report is in all respects accurate and complete and does not warrant any results obtained or conclusions drawn from the use of this Report. Argus has no obligation to maintain or update this Report. All analysis and opinions, data, projections and forecasts provided may be based on assumptions that are not correct or which change, being dependent upon fundamentals and other factors and events subject to change and uncertainty; future results or values could be materially different from any forecast or estimates described in the Report. Subject to any agreement between Argus and its Client, Argus expressly disclaims any and all liability for any direct, indirect or consequential loss or damage, claims, costs and expenses, whether arising in negligence or otherwise, in connection with access to, use or application of these materials or suffered by any person as a result of relying on any information included in, or omission from, this Report and related materials or otherwise in connection therewith, to the maximum extent permitted by law. The Client’s use of the Report is entirely at the Client’s own risk. This Report does not offer or provide financial, tax or legal advice. Copyright notice Copyright © 2019 Argus Media group. All rights reserved. All intellectual property rights in this presentation and the information herein are the exclusive property of Argus and and/or its licensors and may only be used under licence from Argus. Without limiting the foregoing, you will not copy or reproduce any part of its contents (including, but not limited to, single prices or any other individual items of data) in any form or for any purpose whatsoever without the prior written consent of Argus. Trademark notice ARGUS, the ARGUS logo, ARGUS MEDIA, INTEGER, ARGUS GLOBAL MARKETS, other ARGUS publication titles and ARGUS index names are trademarks of Argus Media Limited. For additional information, including details of our other trademarks, visit argusmedia.com/trademarks. illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.

Over 30 experts globally across 7 offices

3

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.

Analytics key content

Key content New

Published Methodology:

Price forecast -15yr cyclical and reversion forecast updated quarterly

-25yr LRMC forecast updated annually

S&D analysis for major markets Demand Forecasts derived from an Agricultural Model

Assessment of new capacity Project Screening to filter out future capacity

Cost analysis Full Cost curve updated quarterly or annually (depending on product)

Frequency of Updates 4 Quarterly updates + 1 Annual spotlight

Data available on Argus Direct Front End included

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.

Presentation overview

Mapping fertilizer trends in major producing regions

• Recent developments and short to long term market analysis for:

• Potash

• Phosphate

• Nitrogen

• Focusing on regions and countries that move the supply balance

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reserved

Potash Fertilizers Copyright © 2019 Argus Media group. illuminating the markets All rights reserved

• We are still feeling the effects of the upturn in potash • Geography of expansions is focused on Canada, Russia, Belarus and China. prices in 2008! • While there have been some new entrants, generally the supply • New capacity has exceeded new demand since 2009. concentration has remained relatively high. • Creation of spare capacity normally weakens the market. • Oligopoly has meant pricing has been reasonably stable until recently. Fertilizers Copyright © 2019 Argus Media group. illuminating the markets All rights reserved

But we are starting to see the impact of the most recent expansions

Short-run MOP balance Recent potash prices

‘000 t

1,500 MOP balance Forecast Surplus

1,327

1,000 892

503

500

301

216 175

160

5 34

0

-233

-500

-845

-1,000 Deficit

-1,500 -1,433

Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020

• 2018 was a strong demand year. • Robust demand underlined a strong pick up in potash prices in 2018.

• Q1 2019 was tight, but the balance shifted to equilibrium in mid-year. • But sentiment has softened in 2019.

• As we look forwards, we’re moving in to a period of surplus supply. • Our expectations are for weaker market in the short term.

• Key potash suppliers are adjusting capacity, looking for equilibrium.

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reserved

Supply

Key themes in mid-2019

Nutrien and Mosaic curtail MOP

supply as weak demand allows MOP

prices to fall; K+S follows

Bethune continues to face quality

issues, production ramps up,

maintenance planned

SQM continues to focus on lithium

China ramps up pressure in SOP

market

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reserved

MOP capacity forecast to 2024: Includes firm and probable MOP projects

MOP Capacity Forecast

Million t

Bolivia

3.0 2.8 2.8 China + Laos

2.7

Jordan

2.5 Spain

Turkmenisatan

2.0 Ø 2.2

2.0 1.9 2.0 Canada Greenfield

1.8

Belarus Petrikov

Canada Brownfield

1.5 1.4

Russia Greenfield

Russia Brownfield

1.0

Capacity represents Argus’

0.5 assessment of operable

capacity, rather than

0.0 design/nameplate capacity.

2017 2018 2019 2020 2021 2022 2023 2024

• MOP incremental capacity addition run rate in recent years has been • The biggest changes to capacity in 2019 are Belaruskali adding capacity

around 2 million t/y. at Petrikov, and ongoing ramp up of Eurochem new mines.

• For the period between 2019 to 2024 this will increase to 2.4 million t/y. • By 2021, we see brownfield expansions in Canada with Mosaic ramping

• Major recent projects in recent years were Bethune in Canada and two up Esterhazy K3, while K+S plans to increase production at Bethune (2nd

Eurochem projects, which are gradually ramping up. phase). Uralkali is also expanding capacity at Solikamsk 3

• Other small additions have been projects in China, Laos, Turkmenistan, by • By 2023, we should see new capacity from Uralkali Ust-Yayvinksy starting

APC in Jordan and YLB in Bolivia up. Nutrien is also planning substantial new brownfield capacity

expansion.

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedGlobal Capacity Forecast: adjusting for mine closures

MOP Forecast Net Capacity

Million y/t Mine 2018 2019 2020 2024

2.8 2.7

3 2.6

1.9 Sigmundshall -900 0 0 0

2 1.4

1.0 1.1 Ø 1.4 Picadilly -2,000 0 0 0

1

Capacity expansions

0 Boulby -1,040 0 0 0

Closure: Germany (Sigmundshall)

-1 Closure: Canada (Picadilly)

Closure: UK (Boulby) Vilafruns (Sallent) 0 0 -500 0

-2.1

-2 Closure: Spain (Sallent)

Taquari Vassouras 0 0 0 -625

-3 Closure: Brazil (Taquari)

Closure: Russia (Berezniki 2)

-4 Net capacity Berezniki 2 -200 0 -290 -410

-5

2017 2018 2019 2020 2021 2022 2023 2024 Total -4,140 0 -790 -1,035

• Substantial closures will to some extent offset the additional capacity outlined previously.

• Nutrient announced the closure of it 2 million t/y Picadilly mine in Saskatchewan. However, it will have relatively minor

commercial impact.

• European closures have greater commercial impact in Spain, Germany and UK.

• Note that this is based on committed capacity, it doesn’t capture losses of production due to commercial decisions, e.g.

SQM.

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedSignificant ramp up in capacity, mostly in Russia

mn t EuroChem production ‘18-23

5.5 Usolskiy capacity Uralkali Russia 13,000 12,600 13,200 15,400 600

5.0 Volgakaliy capacity EuroChem Russia 0 400 5,300 7,500 4,900

4.5

Belaruskali Belarus 10,800 12,900 14,400 14,400 1,500

4.0

3.5 Turkmenhimya Turkmenistan 0 300 650 1,300 350

3.0 Uzkimyosanoat Uzbekistan 200 600 600 600 0

2.5 FSU nameplate capacity 24,000 26,800 34,150 39,200 7,350

2.0

FSU production 17,112 24,150 29,197 32,510 5,047

1.5

1.0 FSU op. rate 71% 90% 85% 83% -5%

0.5 FSU demand 2,220 2,026 2,199 2,370 173

0.0 FSU S/D Balance 21,780 22,124 26,998 30,140 4,874

2018 2019 2020 2021 2022 2023

• The biggest change in capacity in this region in the next five years is

mn t Regional demand Russian Production Eurochem’s potash investment.

35 Others Belarusian Production • Usolskiy first phase produced 467kt in 1H 2019, FY target of 1.1

30 mt. Design capacity likely by 2021, upgrade possible by 2022.

25 • Usolskiy phase II underway, likely 2023. Capacity total = 4mt.

20

• Volgakaliy more complicated. Assuming 2.3 mt by 2023, phase I;

phase II to follow.

15

• We expect to see other project activity also from Acron and Slavkaliy,

10 which could be new entrants in this timeframe.

5 • FSU regional exportable surplus increasing from 22mn t to 30 mn t by

0 2028.

2010 2015 2020 2025 2030

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedMOP capacity expansion in Canada will magnify the region’s exportable supply surplus

North American MOP balance North America MOP Capacity Expansions/Closures

Million t/y

35 Million t/y

45.9

46

30 Picadilly Bethune

44 43.5

25 Nutrien Various Esterhazy ramp up

42 Jansen Existing NAm capacity

20

40 38.9

15 38.2

Imports (Outside NAm) 38 37.0 36.7

10 33.9 36.1 35.9 36.3

Exports (Outside NAm) 36

5 9.6 11.3 10.5 11.1 10.7 10.8 10.9 11.0 11.1 11.5 11.8

Production 34

0 Apparent Demand

32

-5 -10.0 -11.5 -14.2 -13.6 -13.9 -13.9 -14.5 -14.9 -15.8 30

-10 -18.3

-22.1 28

-15

0

-20 -2

2017 2018 2019 2020 2021 2022 2023 2024 2028 2033

-25

2016 2017 2018 2019 2020 2021 2022 2023 2024 2028 2033

• Canadian potash capacity is predicted to continue to expand, resulting in an increasing exportable surplus.

• Brownfield investment will result in 3 million t/y of capacity being added in the next 5 years.

• The biggest increase is predicted to take place beyond 2024, with the emergence of BHP’s greenfield investment.

• With some modest increase in regional demand, it means that the exportable surplus of potash capacity should increase by

around 50%.

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedGlobal MOP balance

Unprecedented MOP demand growth in 2018 helped absorb capacity additions but from 2019 a supply surplus builds y-o-y until 2024

MOP net balance

Mn t Cumulative net change Inoperable

• Robust demand growth in 2017

8 Net change Capacity closures and 2018, combined with some

Demand growth Capacity expansions

7 closures, led to a significant deficit

To surplus

6 and tightening of the market.

5 • We are already seeing that shift in

4 to reverse in 2H 2019. Demand

3 growth this year is expected to be

2 flat while capacity ramps up at

1 various new/recent projects.

0 • As we move forward, we will see a

-1 gradual and persistent supply

-2 surplus as the ramp up of new

-3

project activity, adjusted for

-4

closures, exceeds incremental

-5

demand growth.

• Will new entrant tonnes make

To deficit

-6

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

pricing more competitive?

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedPhosphate Fertilizers Copyright © 2019 Argus Media group. illuminating the markets All rights reserved

Global phosphates market is becoming increasingly

regionalised

Europe

Canada & dominated by

Latin America North African

dominated by and Russian DAP

US

Africa – Indian

increasingly subcontinent

Brazil still globally targeted by

competitive dominated by

market but OCP and Saudi Arabia

Chinese influence Saudi product

in retreat (east and China

coast)

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedChinese phosphates sector undergoing consolidation

China becomes net DAP exporter in 2007

But Chinese production is facing come challenges

• Zero growth in domestic fertilizer demand by 2020

• Permitting of rock mining tightened

• Ongoing environmental control

• DAP exporters facing increased competition

Capacity additions are slowing due to the chronic DAP oversupply

Market consolidation is happening:

• Kailin-Wengfu merger was confirmed after a year of rumours

• China's 2nd and 3rd largest producers overtaking YTH with 10mn t/yr of DAP/NPK capacity

Likely future outcomes:

• Vertical integration encouraged

• Older, higher cost producers forced out of business

• Fewer participants remaining with higher utilisation

• Longer term capacity decline likely, but weighted against macro demands of China’s economy

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedChina DAP exports continue

‘t Total China DAP exports in

January-April 2017-19

600,000

• Weak domestic Chinese 500,000

demand in 1Q19 400,000 Source: GTT

• Suppliers look to meet

300,000

Indian DAP demand

• China ships 1.3mn t in 200,000

January-June 2019 to India –

100,000

up by 34%

0

2017 2018 2019

January February March April

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedNorth America – horizontal consolidation

Reason: 2005 • US Chem exits market

• Phosphate rock reserves depleting and permitting 2006 • Mosaic closes Green Bay plant

is difficult

• Environmental issues (Phosphogypsum) 2010 • Agrifos switches away from phosphates

• Mosaic acquires CF phosphate assets

2013

• PhosChem disbands

Result:

• Mosaic now owns 70pc of DAP/MAP/MES

• May: OCP agrees supply deal with PCS

capacity 2014

• December: MissPhos ceases production

• Nutrien owns 20pc

2016 • PCS /Agrium merger– Nutrien formed

Implications: 2017 • Mosaic idles Plant City (1.8mn t/yr, mainly DAP)

• Higher concentration

2019

• New export strategy orientation/MWSPC • Nutrien ceases MAP production at Redwater in

Canada, starts to convert unit to AS

• DAP Tampa no longer international benchmark

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedCapacity growth driven by Morocco and Saudi Arabia, timing is important

OCP, Morocco Egypt

DAP/MAP/NPS – JPH 3.4mn t/yr P2O5 Phosacid – NCIC (2019)– 360,000 t/yr P2O5

DAP/MAP/TSP/DCP/MCP – SPH - 1mn t/yr P2O5 Phosacid – Misr (2022)– 500,000 t/yr P2O5

DAP/MAP - PhosBoucraa 330,000 t/yr P2O5

Kazphosphate, Kazakhstan

MAP - Taraz (+110,000 t/yr P2O5, 2018)

Nutrien, US NPK/DCP – Eurochem ( +250,000 t/yr P2O5

Geismar plant to close end-2018

(-200,000 t/yr P2O5)

Kribhco/OCP JV, India

DAP/NPK – 1.2mn t/yr - 2022

Nutrien, Canada

Redwater MAP plant conversion to AS - 2019

(-345,000 t/yr P2O5)

China– Industry restructuring

Argus assumed the closure of small inefficient plants

Ma’aden, Saudi Arabia Equivalent to -0.7mn t P2O5 PhosAcid

DAP/MAP/NPS – Ma’aden 3 - +1.7 mn t/yr P2O5, ~2024

Mosaic, US – Plant City closure, -1mn t PhosAcid :

• Lower operating costs and improve system-wide margins

JPMC, Indonesia

• Reduce CAPEX requirements

China Molybdenum, Brazil Pupuk Kaltim, Bontang (200,000 t/yr P2O5, 2019)

• Serve own distribution business and other India customers

MAP/TSP - Catalao - +200,000 t/yr P2O5, 2020/21 Pupuk Sriwijaya (Pusri), Palembang (200,000 t/yr P2O5, 2020)

with low-cost MWSPC JV

Base Case assumes plant will not restart

Yara, Brazil

MAP/TSP - Galvani, Serra do Salitre (+180,000 t/yr P2O5, 2020/21)

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedNitrogen Fertilizers Copyright © 2019 Argus Media group. illuminating the markets All rights reserved

Global urea capacity forecast, 2018-2033

Argus is tracking 36.0 million t/y of new urea capacity; either at the construction stage or in feasibility

Limited investment potential in Global Capacity expansions

Europe and the Americas. Instead

capital is flowing to the following

regions.

Nigeria: Cheap gas priced at $1.50-

2.00/MMBtu and cheap building costs

are offsetting risk.

India: Government is supplying cheap

capital to offset imports and support

the subsidy domestically.

Russia Central Asia: Cheap gas

$0.50-3.50/MMBtu is providing a

steady stream of projects.

SE Asia: Stranded gas in Brunei and

Australia is seeking monetisation.

Iran and Egypt: Government backed

building to support local economy

Forecast capacity expansions

Possible capacity expansions

Speculative capacity expansions

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedGlobal urea capacity forecast, 2018-2024

mn t/y

7.5

Pro-rated urea capacity forecast

Americas Middle East

• Basis for inclusion in CIS Africa

our firm listing in this SE Asia South Asia

timeframe is projects 5.0

which are financed,

received all required

permits and have

begun construction.

Projects undergoing

feasibility are

2.6

excluded, as are those 2.5

without LT gas supply.

0.0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedDramatic expansion of West African urea supply will expand continent’s exportable supply surplus

• Three new trains in Nigeria will add close to 6 million t/y of capacity. mn t/y

• The Dangote project recently signed a new gas supply contract with Chevron, though 18

still some questions.

Production

16

• Eleme project understood to be on track. 14

12

• Regional demand expected to grow, but exportable surplus set to grow substantially. 10

• The NCIC project is not yet firm, but seems likely to progress. Egypt gas situation is greatly 8

improved.

6

4

• Elsewhere, capacity in Algeria has stabilised, operations at around 90% utilization. Exports 2

of 3.2 million t in 2018 likely will be repeated in 2019. 0

2010 2015 2020 2025 2030

mn t

18

2010 2015 2018 2025 ‘18-25 Exportable

16 surplus

Egypt 5.1 5.9 6.8 7.3 +0.5 Jul- Production

Kima II Egypt 520 14

Algeria 0.0 3.0 3.4 3.4 +0.0 19

12

Nigeria 0.3 0.3 1.7 6.0 +4.3 Jul-

Dangote I Nigeria 1,271 10

21

Libya 0.9 0.9 0.9 0.9 +0.0 8

Jul-

African capacity 6.4 10.2 12.8 17.7 +4.9 Dangote II Nigeria 1,271

22 6

Technical surplus 4.0 7.7 10.1 14.3 +4.2 Jul- 4

Eleme II Nigeria 1,400

22 2

African production 5.8 4.8 11.4 15.6 +4.2 Existing

African op. rate 91% 47% 89% 88% -1% Expansion 0

2010 2015 2020 2025 2030

Possible/Spec. Jul-

African S/D Balance 3.4 2.2 8.7 12.2 +3.5 NCIC Egypt 380

23

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedBarauni has been connected to the Indian gas network

• We added the HURL project at Barauni to our list of firm projects, after progress on gas

supply.

mn t/y

50 Production

• This raises our expectations of firm new Indian urea capacity to 4 projects, adding 5 million Capacity: Bangladesh

t/y. Indian urea capacity would reach 30 million t/y.

40

• Two other projects are considered speculative at Talcher (coal-gasification) and in 30

Bangladesh. 20

• Collectively, firm project activity would reduce the regional urea import requirement from 10

nearly 13 million tonnes in 2015 to just over 5 million t/y. 0

2010

2015

2020

2025

2030

mn t

2010 2015 2018 2025 ‘18-25 50

India 23.0 24.0 24.0 30.4 +6.4 Ramagundam India Mar-20 1,271

40

Pakistan 4.6 6.3 6.3 6.3 +0.0 Matix Fert. India Oct-20 1,271

Bangladesh 3.0 3.0 3.5 3.5 +0.0 Gorakhpur India Mar-22 1,271 30

Afghanistan 0.1 0.1 0.1 0.1 +0.0 Barauni India Dec-22 1,271

Other South Asia 0.0 0.0 0.0 0.0 +0.0 Total firm 5,082 20

S. Asian capacity 30.7 33.4 33.9 40.3 +6.4 Sindri India Jul-23 1,271

Technical surplus -6.5 -9.4 -6.1 -1.3 +4.9 Talcher India Jul-23 1,271 10

S. Asian production 28.3 30.5 30.6 36.7 +6.1 Existing Polash Bangladesh Jul-24 924

Expansion 0

S. Asian op. rate 92% 91% 90% 91% +1% Total speculative 3,465 2010 2015 2020 2025 2030

Speculative

S. Asian S/D Balance -9.2 -12.8 -9.7 -5.3 +4.4 Total: Firm + Speculative 8,547

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedChinese urea output has increased with gas availability

Chinese urea capacity is forecast to stabilise between 65-70 million t/y over the medium term

Chinese urea plant closures Chinese capacity, 2010-33

1. Capacity closure rate is slowing, but for now mn t/y mn t/y

we are still seeing net decrease in capacity. 6 90

5.3

80

2. Operating rates have improved towards 4.5 4.5 70

80%, while higher gas availability means 4 3.8 60

more production over the winter. 50

40 Production

3. Urea production up ~2.0 mn t this year… 2 30 Consumption

20

4. …and we are seeing this increment being Chinese capacity

10

passed into the export market.

0 0

2016 2017 2018 2019 2010 2015 2020 2025 2030

Chinese Capacity Expansions Chinese urea production, 2017-19 Chinese urea production, 2017-19

mn t/m mn t/y mn t

Name Country Start Capacity

10 55 14

2015

Erdos Wulan In. Mongolia Sep-19 1,200 12

Annualised production 54

Runjin Chem Shanxi Nov-19 300 10

Sanning Hubei Nov-19 795 53 2016

8

Mingshengda Shandong H2 2020 795 5

52 6

XLX Jiangxi Jiangxi H2 2020 525 2017

4

Hongtaixing Heilongjiang H2 2020 300 51

2 2018

Linggu Chem Jinagsu H2 2021 1,680 Monthly Chinese production

Zhengyuan Hebei H2 2021 248 0 50 0

Jan- Jul- Jan- Jul- Jan- Jul- Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Total firm 6,368 17 17 18 18 19 19

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedMarket Balance: Five-year Outlook

Cheaper inputs, a weak RMB and capacity make the market look moderately over-supplied in the year

ahead

mn t/y

• The withdrawal of Chinese exports in 2016 8

Net Change

and 2017 contributed to a reduction in Demand

Chinese export delta

the net change surplus, then a deficit in

7

Iran export delta

2018, which brought a tighter market in 6 Closures

that year.

Restarts

5

Capacity expansion

• We had been expecting a tighter 2019, 4

but a weak RMB and weak energy prices 3

mean that Chinese urea exports have 2

tipped the balance towards surplus.

For the period 2020-21, the market looks

1

•

to be shifting to surplus with 5 million t/y 0

of new export oriented capacity -1

exceeding new demand growth, so the -2

market likely to weaken. -3

• For 2023-2024, the rate of new capacity

-4

additions slows, and we can expect a

tighter market. But there’s a risk that some -5

projects move ahead and tip the balance. -6

2016 2017 2018 2019 2020 2021 2022 2023 2024

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reserved… thanks for your attention!

Copyright notice

Copyright © 2019 Argus Media Ltd. All rights reserved. All

intellectual property rights in this presentation and the

information herein are the exclusive property of Argus and

and/or its licensors and may only be used under licence from

Argus. Without limiting the foregoing, by reading this

presentation you agree that you will not copy or reproduce

any part of its contents (including, but not limited to, single

prices or any other individual items of data) in any form or for

any purpose whatsoever without the prior written consent of

Argus.

Trademark notice

ARGUS, ARGUS MEDIA, the ARGUS logo, DEWITT, FMB,

FUNDALYTICS, METAL-PAGES, JIM JORDAN & ASSOCIATES,

JJ&A, ARGUS publication titles and ARGUS index names are

trademarks of Argus Media Limited.

Disclaimer

All data and other information presented (the “Data”) are

provided on an “as is” basis. Argus makes no warranties,

express or implied, as to the accuracy, adequacy, timeliness, or

completeness of the Data or fitness for any particular purpose.

Argus shall not be liable for any loss or damage arising from

any party’s reliance on the Data and disclaims any and all

liability related to or arising out of use of the Data to the full

Fertilizers

extent permissible by law.

Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedAppendix:

Update on Argus fertilizer sector coverage

Fertilizers Copyright © 2019 Argus Media group.

illuminating the markets All rights reservedBuilding on 30+ years of excellence

1982 2011 2012-2016 2018

2012-2013

FMB Consultants Argus acquires FMB Rapid expansion of Acquisition of

Argus acquires JJ&A,

Ltd founded market services and DeWitt expanding related services, global fertilizer Integer Research

conferences team and locations

market coverage

1980 1990 2000 2010 2020

2004 2013 2016-2019

2012

FCC Consultants Fertilizers win top awards from Launches enhanced

Argus acquires FCC

founded Trade Association Business data services,

International Analytics and mobile

tools

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.Over 30 experts globally across 7 offices

31

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.Analytics key content

Key content New

Published Methodology:

Price forecast -15yr cyclical and reversion forecast updated quarterly

-25yr LRMC forecast updated annually

S&D analysis for major markets Demand Forecasts derived from an Agricultural Model

Assessment of new capacity Project Screening to filter out future capacity

Cost analysis Full Cost curve updated quarterly or annually (depending on product)

Frequency of Updates 4 Quarterly updates + 1 Annual spotlight

Data available on Argus Direct Front End included

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.Giving you an expanded portfolio of services

Over 650 price Fertilizer

assessments across

market reports

Market Intelligence Consulting Conferences

Over 200 news alerts each Multi-Client

month Global

Reports

Regional

Reports

Forecast and

Data Services

and Single-

Regional

Events

Regional

Forums

Client Work

Trusted for indexation in Nitrogen Europe

Outlooks WSF

physical contracts Ammonia

Phosphate

NorthAm

Brazil Analytics

EEF

Micronutrients

Africa, Asia, Added Value

Potash

Sub-Saharan

LatAm, FSU, Fertilizer

Sulphur Russia Cost

Africa Europe WSF & NPK

SulAcid Africa Curves

Short-term and long-term NPK Asia

forecast publications and

data sets

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.New in 2019: DEF, TGU, Sulphur, Africa and Asia content illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.

Fertilizer Analytics services

4 Quarterly Reports Interactive Excel Spreadsheets 1 Annual LT Report

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.Analytics key content

Key content New

Published Methodology:

Price forecast -15yr cyclical and reversion forecast updated quarterly

-25yr LRMC forecast updated annually

S&D analysis for major markets Demand Forecasts derived from an Agricultural Model

Assessment of new capacity Project Screening to filter out future capacity

Cost analysis Full Cost curve updated quarterly or annually (depending on product)

Frequency of Updates 4 Quarterly updates + 1 Annual spotlight

Data available on Argus Direct Front End included

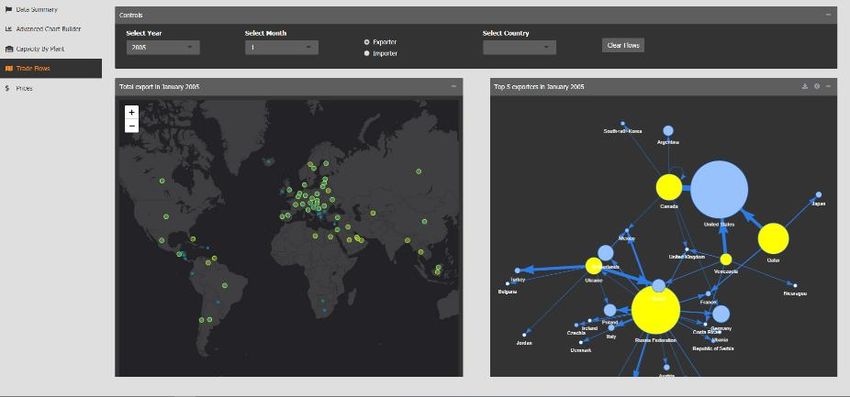

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.Analytics data visualisation dashboard

Argus is continuously seeking to improve

data delivery and user experience. Our team

is developing a new interactive platform for

you to easily access all fundamentals data.

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.Dashboard shows capacity by country, location illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.

Shows prices and trade flows plus advanced chart builder illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.

… and last but not least, Fertilizer Focus magazine

The leading fertilizer industry magazine is

undergoing a revamp:

• Widest and most credible fertilizer industry

circulation

• Best in class articles on the sector

• The most compelling vehicle for advertising

to reach a qualified fertilizer audience

40

illuminating the markets Copyright © 2019 Argus Media group. All rights reserved.You can also read