MONTHLY PROPERTY MARKET & ECONOMIC UPDATE - NEW ZEALAND FEBRUARY 2018 - CORELOGIC

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Monthly Property Market & Economic Update New Zealand February 2018

Contents

About CoreLogic 4

CoreLogic Data and Analytics .................................................................................................................................................................. 4

Legal Disclaimer ............................................................................................................................................................................................. 4

Macro Economic and Demographic Indicators 6

New Zealand Asset Classes ....................................................................................................................................................................... 7

New Zealand Population ............................................................................................................................................................................. 8

Migration ........................................................................................................................................................................................................... 9

Regional Building Consents ....................................................................................................................................................................... 10

Population Growth Compared to Building Consents ...................................................................................................................... 10

Consumer Confidence ................................................................................................................................................................................. 11

Employment .................................................................................................................................................................................................... 12

Interest Rates .................................................................................................................................................................................................. 13

Housing Overview 14

Nationwide Values ......................................................................................................................................................................................... 15

Sales Volumes ................................................................................................................................................................................................. 16

Rent ..................................................................................................................................................................................................................... 17

Market Activity ............................................................................................................................................................................................... 18

Valuations Completed................................................................................................................................................................................... 19

Listings ............................................................................................................................................................................................................... 20

Buyer Classification ....................................................................................................................................................................................... 22

House Price Index .......................................................................................................................................................................................... 23

Main Cities Housing Market Indicators 26

Auckland Market Activity ........................................................................................................................................................................... 28

Auckland Values ............................................................................................................................................................................................. 29

Auckland Suburb Value Change .............................................................................................................................................................. 30

Current Auckland Suburb Values ............................................................................................................................................................ 32

Hamilton Market Activity ............................................................................................................................................................................ 34

Hamilton Values .............................................................................................................................................................................................. 35

Tauranga Market Activity ............................................................................................................................................................................ 36

Tauranga Values ............................................................................................................................................................................................. 37

Wellington Market Activity ......................................................................................................................................................................... 38

Wellington Values .......................................................................................................................................................................................... 39

Christchurch Market Activity ..................................................................................................................................................................... 40

Christchurch Values ...................................................................................................................................................................................... 41

Dunedin Market Activity .............................................................................................................................................................................. 42

Dunedin Values ............................................................................................................................................................................................... 43

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 2

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.

About CoreLogic

CoreLogic is a leading property information, Whilst all reasonable effort is made to ensure

analytics and services provider in the the information in this publication is current,

United States, Australia and New Zealand. CoreLogic does not warrant the accuracy,

CoreLogic helps clients identify and manage currency or completeness of the data and

growth opportunities, improve performance commentary contained in this publication

and mitigate risk, by providing clients with and to the full extent not prohibited by

innovative, technology-based services and law excludes all loss or damage arising in

access to rich data and analytics. connection with the data and commentary

contained in this publication.

Contact

Call us 0800 355 355

Wellington office Auckland office

Level 2, 275 Cuba Street Level 5

PO Box 4072 41 Shortland Street

Wellington 6140 Auckland 1010

Email: reports@corelogic.co.nz

www.corelogic.co.nz

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 3

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.

CoreLogic Data and Analytics

CoreLogic Buyer Classification Suburb scorecard

A unique and flagship product to CoreLogic, Buyer Detailed housing market indicators at suburb level,

Classification determines the type of buyer for every with data either in time series or current snapshot, and

purchase of property based on their current and previous segmented across houses, flats and apartments. The

ownership of NZ property. Created at a record level, this Suburb Scorecard data includes key housing market

can be matched to other datasets or summarised at any metrics such as median prices, median values, transaction

geographic area. volumes, rental statistics and market metrics such as

median selling time.

Our buyer classification is used by financial institutions

and Government agencies at both record and summary

level and overlaid with their own data to assist strategic, To view the latest report online and subscribe to

policy, compliance, risk management and marketing receive it in your inbox on a monthly basis, visit;

decisions.

www.corelogic.co.nz/new-zealand-monthly-

property-market-update

CoreLogic value measures

CoreLogic has a suite of products to measure property

prices. This ranges from simple market measurements If you would like to know more or obtain tailored

such as median or average sales prices through to data, analytics and insights for your business, please

stratified medians, various house price indices, and valuing email us at reports@corelogic.co.nz.

groups of properties using Automated Valuation Models

such as E-valuer. The house price indices are available both

quarterly for completeness and monthly for reactivity.

The Quarterly CoreLogic House Price Index has been

specifically designed to track the value of a portfolio of

properties over time and is relied upon by New Zealand

regulators and industry as the most accurate measurement

of housing market performance. These value measures are

available for long time series and for either standard or

custom geographic areas and property types.

Legal Disclaimer

Copyright Data & Research publications

This publication reproduces materials and content owned Whilst all reasonable effort is made to ensure the

or licenced by RP Data Pty Ltd trading as CoreLogic information in this publication is current, CoreLogic does

Asia Pacific (CoreLogic) and may include data, statistics, not warrant the accuracy, currency or completeness of

estimates, indices, photographs, maps, tools, calculators the Data and commentary contained in this publication

(including their outputs), commentary, reports and other and to the full extent not prohibited by law excludes all

information (CoreLogic Data). loss or damage arising in connection with the Data and

commentary contained in this publication.

© Copyright 2018. CoreLogic and its licensors are the

sole and exclusive owners of all rights, title and interest You acknowledge and agree that CoreLogic does not

(including intellectual property rights) the CoreLogic Data provide any investment, legal, financial or taxation

contained in this publication. All rights reserved. advice as to the suitability of any property and this

publication should not be relied upon in lieu of appropriate

professional advice.

Published date: February 2018

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 4

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 5

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.

Macro Economic and

Demographic Indicators

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 6

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.

New Zealand Asset Classes

Residential Real Estate

$1.07 trillion

($247 billion in home loans)

Commercial/Industrial Real Estate

$201 billion

NZ Listed Stocks

$125 billion

NZ Super and KiwiSaver

$79 billion

The value of residential property continues to grow beyond one trillion dollars, outperforming the

value of other asset classes. Residential mortgages secured against 23% of this value.

Over the last month stocks worldwide experienced somewhat of a market correction with the NZX

dropping 3.6% from its early-January high but they have stabilised in mid-February.

*Source: CoreLogic NZ, Reserve Bank of NZ, NZX, NZ Superfund, Financial Markets Authority

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 7

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.

New Zealand Population

Quarterly Change in National Population

Population growth slowed further in Q4

2017, with the moving average continuing

to trend down.

Almost three-quarters of population

growth is due to net migration, which

was 70,000 for the year to the end of

December 2017. This represents a further

fall from the peak of 72,200 to the end of

June 2017.

After hitting a 20 year low, natural

population growth rebounded in Q4 2017,

but the overall trend is flat.

Population Change Composition

Annual Change in Population

Source: Statistics New Zealand

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 8

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.

Migration

Long Term Migration

The trend of net migration effectively

plateaued for the last three months of

2017 as both arrivals and departures held

firm.

Immigration continues to be a hot topic

for the Government and the declining

trend in net migration is likely to continue.

This may not be as dramatic as previously

expected, due to the need of skilled labour

in an already tight market.

After a few months of net loss to Australia,

the stats veered back into the positives in

the final months of the year. The expected

strength in the Australian economy is

yet to have a significant impact on Kiwi

migrants yet, and while proposed changes

Monthly Net Migration Between New Zealand and Australia to remove the subsidised tertiary fees for

New Zealanders have now been scrapped,

there are still some concerns about the

visa status of New Zealanders in Australia

restricting them from access to certain

Government schemes.

In 2017, Dunedin saw a 23.7% increase

in net migration (from 2016): the largest

increase of all our main centres. Net

migration to Christchurch continues to

slowly decrease, after peaking in the year

to the end of March 2016.

Net Gain Last Year % Change

TOTAL ALL AREAS 70,016 -0.8%

Auckland Region 36,152 6.6%

Hamilton City 1,875 12.3%

Tauranga City 1,052 0.5%

Wellington 3,593 10.9%

Christchurch City 5,403 -4.0%

Dunedin City 1,024 23.7%

Main Urban Area (Other) 5,239 -5.9%

Rural Centres 4,798 8.6%

Not applicable/Not stated 10,880 -23.8%

Source: Statistics New Zealand

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 9

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.

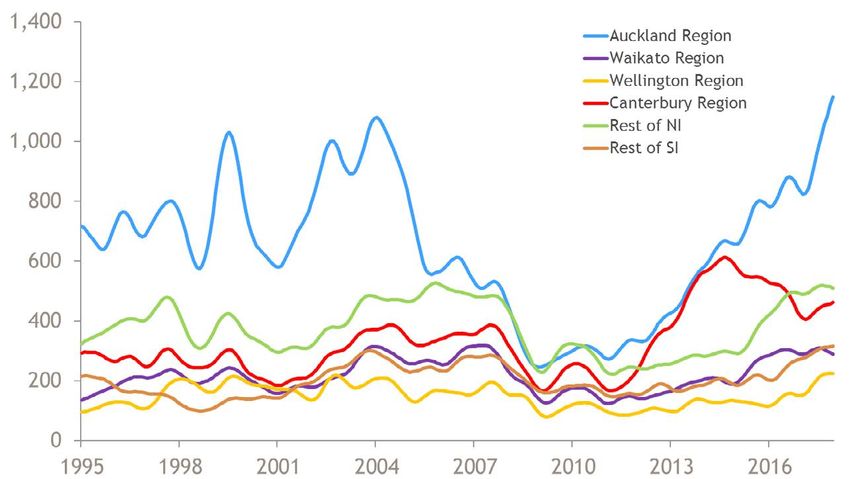

Regional Building Consents

New Dwelling Consents Trend

Building consents issued in Auckland

continues a strong upwards trend but

there are consistent reports of the

construction industry being very close to

capacity.

A recent Government commissioned

‘Stocktake’ report detailed three key

barriers to housing supply: planning,

infrastructure and the development sector.

This foreshadows the Government’s

challenge in implementing KiwiBuild: the

commitment to delivering 100,000 quality

affordable homes in the next ten years,

half of which will be in Auckland.

Elsewhere in NZ consents are now

trending sideways as similar constraints

affect other centres as well.

Population Growth Compared

to Building Consents

Quarterly Population Change and Building Consents Nationwide

With population growth slowing and

building consents continuing to increase,

the gap between the two is reducing.

The gap is calculated by assuming 80%

of dwellings consented translate into an

actual increase in the number of dwellings

(which may be generous given our results

of consent to stock change analysis), and

that each of those dwellings will house

the current average number of people (2.7

people per dwelling).

For example, over the year to December

2017 there were 31,127 dwellings consented

(able to house 67,234 people), and an

increase in population of 97,000, leaving

a difference of almost 30,000 too many

people for dwellings.

Source: Statistics New Zealand

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 10

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Consumer Confidence

ANZ-Roy Morgan Confidence Consumer

Consumer confidence lifted in January

with people remaining happy with their

current financial situation.

Consumer perception of the economic

outlook also lifted, perhaps due to a ‘solid’

start for the Labour-NZ First Government

combining with a relatively stable housing

market and a strong labour market.

The gap in confidence between Australia

and NZ was significantly reduced in

December with the economic outlook in

Australia improving.

Source: ANZ NZ, Roy Morgan

Trans-Tasman Consumer Confidence Index

Source: Westpac NZ, McDermott Miller

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 11

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Employment

Annual Change in Employment, Full Time and Part Time

The rate of part-time employment lifted

however the rate of growth in full-time

employment eased off for the fourth

quarter in a row (albeit only marginally

last quarter). The total number of people

actually employed has continued to rise.

The labour force participation rate eased

slightly to 71.0% in Q4 2017 after peaking

in Q3 2017 at 71.1% and the unemployment

rate dropped further to 4.5% - the lowest

since 2008.

For an employment lead significant

correction in the housing market to occur,

Labour Force Participation Rate there would have to be a turnaround in

employment with people unable to pay

mortgages or rent.

Unemployment Rate

Source: Statistics New Zealand

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 12

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Interest Rates

Mortgage Interest Rates - %

Retail banks are competing strongly for

mortgages, with interest rates again taking

a noticeable dip in January.

The Official Cash Rate (OCR) remained

on hold in February and is projected to

remain below 2.00% until the end of 2019,

which is good news for new borrowers

and those coming off fixed rates.

The new loan-to-value ratio (LVR)

restrictions are now in place. They are only

a minor change from previous restrictions

with the deposit requirement for investors

dropping from 40% to 35% and the share

Projected Official Cash Rate - % of high LVR lending (above 80% LVR) to

owner occupiers increasing from 10% to

15%.

The expected impact on the market is

minimal, although it will contribute to

a small lift in demand from those who

were previously unable to satisfy the LVR

requirements.

Average Two Year Fixed Rates - %

Source: Reserve Bank of New Zealand

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 13

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Housing Overview

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 14

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

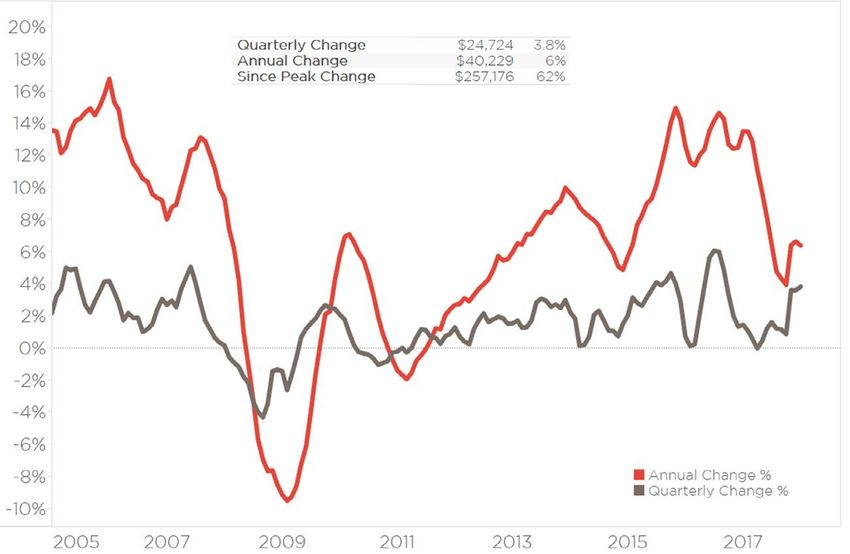

All rights reserved.Nationwide Values

Average Value of Housing Stock - New Zealand

Nationwide value growth moderated

over the summer holiday after a relatively

significant lift in November.

Three month value growth hit 3.8% at

the end of January. This was the fastest

rate for over a year, perhaps due to

post-election jitters calming and buyers

returning to the market - taking advantage

of still-low interest rates.

Annual and Quarterly Change in Value

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 15

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

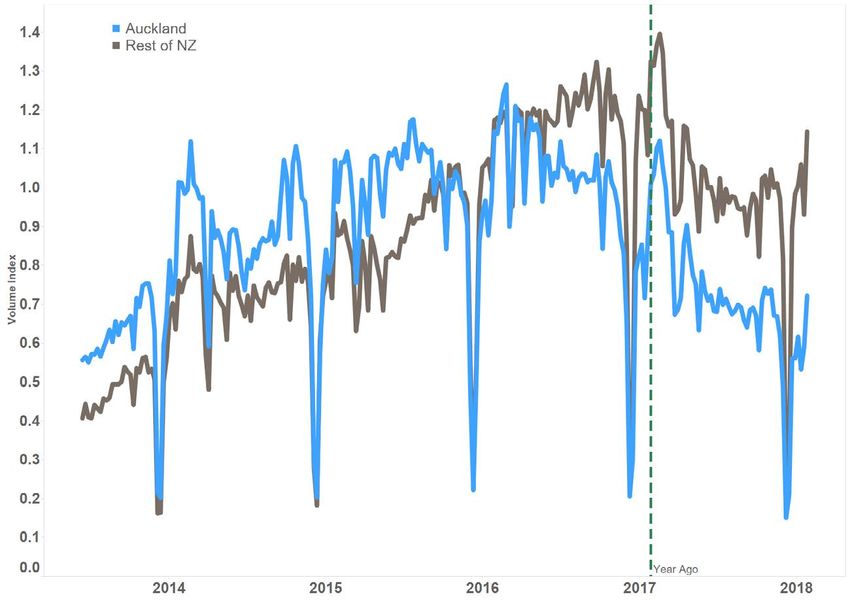

All rights reserved.Sales Volumes

Nationwide Sales Volumes

Sales volumes in December were flat year-

on-year, but January volumes were more

subdued (6% down year-on-year).

Once again sales volumes were very

weak in Auckland. High prices and a re-

balancing of demand/supply have reduced

the fear of missing out, and as a result

the ‘days to sell’ measure has begun to

lengthen.

Christchurch experienced a late-spring

and summer resurgence in sales volumes

with November, December and January all

up on the (admittedly weak) prior year.

Nationwide Annual Change in Sales Volumes

Regional Sales Volumes Year-on-Year

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 16

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Rent

Nationwide Annual Change in Value and Rent

Annual rental growth stabilised at 4.9%

in December and January, illustrating a

similar trend to value growth after both

bottomed out in October 2017.

Gross rental yield continues to hover

along just over 3.0% (as it has done for 18

months+).

Christchurch rent continues to drop,

although the rate of -2.8% is not as great

as the drop witnessed through most of the

second half of 2017.

Meanwhile the growth in median rent in

Dunedin is now trending downwards after

peaking at greater than 10% growth in the

middle of 2017.

Tauranga’s annual rent increase of 12.1%

is slightly misleading because it’s being

compared to an anomaly of a month last

January. Actual annual change in Tauranga

Gross Rental Yield - Nationwide is realistically closer to 7%, which is still

rather high – similar to Wellington (7.6%),

where we’ve seen and heard plenty about

the rental squeeze in the nation’s capital.

Median Weekly Rent Annual Change in Rent Gross Yield

Auckland $511 4.7% 2.1%

Hamilton $365 7.4% 3.5%

Tauranga $436 12.1% 3.2%

Wellington $466 7.6% 3.2%

Christchurch $345 -2.8% 3.6%

Dunedin $340 -5.6% 4.5%

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 17

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

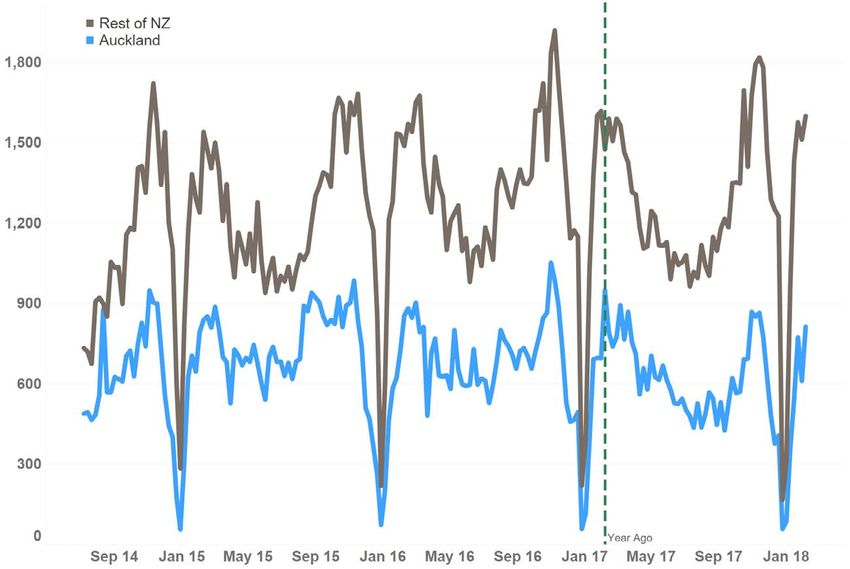

All rights reserved.Market Activity

Market Activity Index

We’re still waiting for the market to

properly swing back into action, after

the prevalence of public holidays in

January and early February impacted

both demand and subsequent activity.

Nonetheless, relative to the same time last

year all major centres are experiencing

reduced activity, with Auckland the

farthest back.

Latest 3 Weeks Year-on-Year Percentage change

Auckland -29%

Hamilton City -6%

Tauranga City -5%

Wellington Region -19%

Christchurch City -19%

Dunedin City -11%

This market activity is based on the number of automated valuations run by bank staff using our systems each week. This

number of valuations correlates very closely to the number of sales that will subsequently occur so this is an extremely

timely measure of buyer demand, more than any measure of sales. We can also track across any geographic area.

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 18

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Valuations completed

Market Activity Year-on-Year

This map shows activity in the latest three

weeks compared to the same three weeks

last year.

New Plymouth has picked up where it

finished last year with a sustained increase

in market activity, 24% up on the same

time last year. Elsewhere there are only

a handful of smaller districts across the

country experiencing a lift in activity.

*Size of bubble represents the level of activity for the period 29 January – 18 February 2018

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 19

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Listings

New Listings

Similar to the demand measure of market

activity, the supply measure of new listings

takes a few weeks to get back to ‘normal’

levels as holiday makers drift back to

work.

The one month change measure is

effectively meaningless because it’s

comparing to Christmas-New Year period

(when listings are scarce). The one year

change however can be informative,

with Wellington listings relatively weak

and not doing much to alleviate already

constrained supply.

New Listings Average last 3 weeks 1 month change 1 year change

New Zealand 2,295 254% -2%

Auckland 732 334% -6%

Waikato 243 169% 4%

Bay of Plenty 156 186% -11%

Wellington 218 330% -12%

Canterbury 361 378% 2%

Otago 101 256% 16%

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 20

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Total Listings

Total listings have begun to trend

upwards again in Auckland, with new

listings starting to lift and ‘days to sell’

lengthening.

The same is true around the rest of the

country but at a reduced rate. Wellington

continues to experience a significant

shortage, only 2% up on the prior year

(which was already a low point for that

time of the year).

Total Listings Latest week 1 month change 1 year change

New Zealand 29,147 4% 9%

Auckland 9,125 5% 23%

Waikato 3,063 4% 15%

Bay Of Plenty 2,092 3% 14%

Wellington 1,571 18% 2%

Canterbury 4,723 7% 8%

Otago 1,097 3% 9%

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 21

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Buyer Classification

Buyer Classification - New Zealand

First home buyers finished 2017 strongly,

accounting for 22.2% of sales in the final

quarter of the year but haven’t started off

2018 quite so well, with 21.7% of sales in

January.

Movers have bounced back from their

Q4 2017 slump, while multiple property

owners remained consistent with 37.5%

of sales. We have previously noted the

reducing share of mortgaged multiple

property owners among this group but

they actually had a stronger month in

January: accounting for almost two-

thirds (66%) of multiple property owners

purchases (up from 62%), perhaps

benefitting from lower interest rates

enabling larger loans.

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 22

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.House Price Index

Average Dwelling Value

Values increased across most of the

country in January, with 3.8% growth

witnessed nationwide in the three months

to the end of January. Auckland values

continued a slight resurgence after

spending most of 2017 in gradual decline.

A similar trend is evident in Tauranga,

however values in Hamilton have remained

flat for almost six months.

Wellington has seen consistent value

growth over the same period after they

stalled briefly in winter last year.

The growth in values in Dunedin has been

more modest but consistent, with 9.3%

growth over the last 12 months.

January 2018

Current Value 3 months 12 months Since 2007 peak

New Zealand $671,531 3.8% 6.4% 62%

Auckland $1,054,974 1.6% 0.7% 93%

Hamilton $544,935 0.3% 2.6% 51%

Tauranga $698,875 1.7% 3.9% 45%

Wellington $634,811 4.0% 9.0% 39%

Christchurch $494,459 0.8% -0.6% 30%

Dunedin $392,512 2.6% 9.3% 37%

Source: CoreLogic NZ QV Monthly House Price Index

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 23

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.House Price Index

Annual Value Change

The greatest growth in values over the last

year has been in the districts of Hawke’s

Bay, Horowhenua and Masterton.

Much of Canterbury has seen little growth

over the last 12 months, with Timaru

and MacKenzie the exceptions. Further

south, the Southland District (main towns

Winton, Te Anau and Riverton) saw the

greatest growth in the year to the end of

January 2018.

*Size of bubble represents the number of properties in the Territorial Authority

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 24

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Three Month Value Change

Three month value change by each of

the Council areas is patchier and shows

a few areas in the top half of the North

Island where values have decreased (blue

dots). These include Thames Coromandel,

Hauraki and Western BOP.

The greatest growth witnessed over this

period in the North Island is in Central

Hawke’s Bay at 8.0%.

Three month growth also remains very

high in the MacKenzie District, however it’s

always best to treat these smaller areas

(smaller dots) with caution due to fewer

sales occurring in these areas.

*Size of bubble represents the number of properties in the Territorial Authority

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 25

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Main Cities Housing

Market Indicators

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 26

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 27

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Auckland Market Activity

Buyer Demand - Auckland

Demand in Auckland has been very weak

so far this year, in part due to the number

of public holidays but this is not the sole

reason. The weakness in demand may be

a sign of further fatigue in the market. The

latest week (up to 18 February) did see a

lift but it’s too early to know if this will be

sustained.

Multiple property owners appear to

have found their new level in Auckland,

consistently accounting for around 40%

of sales. We must note that each quarter

between 25% and 33% of these are making

their purchase without a mortgage,

unaffected by LVRs or serviceability

criteria (and subsequently excluded from

RBNZ reporting).

First home buyers also remain consistently

active at around 23% of the market - we’ve

previously noted this groups’ willingness

to sacrifice location/property type to enter

the property market and this remains true.

Buyer Classification - Auckland

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 28

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Auckland Values

Average Value of Housing Stock - Auckland

Values in Auckland are now up 1.6% over

the last three months, the fastest rate

since December 2016, but with a back

drop of continually reducing volumes, this

growth is unlikely to be sustained.

Papakura continues to experience a

strong recovery in values (up 5.1%) since

August 2017 after seeing a 3.9% drop

after peaking in April 2017. The rest of the

city appears to making a slightly more

restrained recovery after values plateaued

or dropped throughout 2017, with

Waitakere the only area to still be behind

values from a year ago.

Annual and Quarterly Value Change - Auckland

January 2018

Current Value 3 months 12 months Since 2007 peak

Rodney $947,856 1.5% 1.5% 62%

North Shore $1,228,920 2.3% 1.2% 90%

Waitakere $822,871 0.5% -1.6% 94%

Auckland City $1,245,682 1.8% 1.7% 100%

Manukau $904,158 1.2% 0.3% 98%

Papakura $700,283 2.3% 2.4% 95%

Franklin $673,514 1.2% 2.0% 70%

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 29

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Auckland Suburb Value Change

Annual Value Change

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 30

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.The 12 month map of value change in

Auckland details variance across the

city. Parts of Central Auckland and in the

Eastern Suburbs are seeing up to 10%

growth, while out West and South of the

city there are a greater number of suburbs

where values have decreased in the last

year.

Parts of the North Shore are now showing

a bit more sustained growth than

previously witnessed.

*Size of bubble represents the number of

properties in the suburb.

Based on CoreLogic Median E-valuer

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 31

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Current Auckland Suburb Values

Median Value of Housing Stock

20 km

10 km

Slight drops in value have not changed a picture of widespread unaffordability in Auckland.

There are currently still 106 suburbs where the average value of the housing stock is over one million dollars.

*Based on CoreLogic Median E-valuer

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 32

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 33

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Hamilton Market Activity

Buyer Demand - Hamilton

Buyer demand in Hamilton started strong

but hasn’t been sustained and while other

main centres saw a significant lift in the

week ending 18 February, Hamilton did

not.

Multiple Property Owner activity, including

those from Auckland, bottomed out in

Hamilton in the middle of last year but

they are working their way back, with 43%

of sales going to multiple property owners

in January.

Over three quarters of these secured

finance for the purchase. This is interesting

considering the tighter Loan to Value

Ratio limits for investors, and while these

have now been slightly loosened by the

Reserve Bank, it’s too soon for the change

to have had any real effect on sales.

Meanwhile first home buyers had a quieter

month in January

Buyer Classification - Hamilton

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 34

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Hamilton Values

Average Value of Housing Stock - Hamilton

Hamilton values have flattened out since

August 2017 after gradually growing for

most of 2017. Due to the dip in values a

year ago, values are only 2.6% up over the

last year though.

Hamilton South West has continued to

grow recently, however Central & North

West has experienced 4 months of falling

values.

Out East both the Northern and Southern

areas have seemingly plateaued with less

than 0.5% three month growth in each.

Annual and Quarterly Value Change - Hamilton

January 2018

Current Value 3 months 12 months Since 2007 peak

Hamilton Central & North West $494,164 -0.9% 1% 38%

Hamilton North East $692,145 0.5% 2% 54%

Hamilton South East $494,488 0.3% 3% 41%

Hamilton South West $492,551 1.8% 6% 44%

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 35

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Tauranga Market Activity

Buyer Demand - Tauranga

A strong start to the year for market

activity in Tauranga has since been

followed up with the strongest single week

of activity since March 2017, for the week

ending 18 February, suggesting sales for

February could be relatively strong.

Multiple Property owners from Auckland

remain a weakening presence in the

Tauranga market, however other multiple

property owners are holding firm,

including those requiring mortgages.

Buyer Classification - Tauranga

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 36

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Tauranga Values

Average Value of Housing Stock - Tauranga

Values have once again started to grow in

Tauranga (1.7% over the last three months),

although the annual rate of 3.9% remains

near the low point from the last four years.

January saw the average value reach

$698,875, the highest on record.

Annual and Quarterly Value Change - Tauranga

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 37

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Wellington Market Activity

Buyer Demand - Wellington

Market activity in Wellington is following

the typical seasonal pattern - starting

slowly but finally kicking into action

from late January. The upward trend

witnessed since early spring appears to be

continuing.

First home buyers continue to go from

strength to strength in the capital,

accounting for 34% of sales in January

2018. In Lower Hutt they were responsible

for 42% of sales. Access to KiwiSaver

funds and grants are assisting these

buyers, while low interest rates are

helping to keep mortgage repayments

manageable.

Meanwhile movers and to a lesser degree

multiple property owners have kept their

activity in check.

Buyer Classification - Wellington

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 38

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Wellington Values

Average Value of Housing Stock – Wellington

Values in Wellington have continued

an upward trajectory that began in

September last year, increasing 4.0% over

the last three months. The annual rate of

growth however remains below 10% as the

muted period over winter holds it back.

Upper Hutt’s recent exceptional growth

has hit a speed bump, with only 1.1%

growth over the last three months while

Porirua (4.0%) and Wellington (3.5%)

show no signs of slowing down.

Annual and Quarterly Change in Value - Wellington

January 2018

Current Value 3 months 12 months Since 2007 peak

Porirua $548,889 4.0% 13% 44%

Upper Hutt $470,511 1.1% 9% 34%

Lower Hutt $523,344 0.6% 8% 33%

Wellington City $764,560 3.5% 9% 44%

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 39

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Christchurch Market Activity

Buyer Demand - Christchurch

Market activity in Christchurch has

remained muted following a similar end to

2017, although the latest week of activity

(ending 18 February) shows signs of a lift.

Not much changed in terms of the types

of buyers active between Q4 2017 and

January 2018, with movers remaining less

active participants and first home buyers

remaining near their all-time share levels.

While there appeared to be a lift in

multiple property owner activity late last

year in the Garden City, this is almost

wholly attributable to those buyers not

requiring a mortgage. They’re unaffected

by lending criteria and interest rates and

have maintained their activity while all

other buyers have dropped away.

Buyer Classification - Christchurch

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 40

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Christchurch Values

Average Value of Housing Stock - Christchurch

Values remain very subdued in

Christchurch, as growth of only 0.8% over

the last three months means values are

still 0.6% below the same time last year.

This is evident across the City; however

values in the Hills have finally begun to

make some ground back after the average

value dropped to below $650k in October

2017.

Over the longer term, Christchurch

Southwest has seen the greatest growth

since the previous peak at the end of 2007

(39%).

Annual and Quarterly Value Change - Christchurch

January 2018

Current Value 3 months 12 months Since 2007 peak

Banks Peninsula $510,268 -1.0% -1% 6%

Christchurch Central & North $584,136 0.9% -1% 32%

Christchurch East $372,005 0.6% 0% 20%

Christchurch Hills $667,870 2.9% 0% 21%

Christchurch Southwest $471,587 0.4% -1% 39%

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 41

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Dunedin Market Activity

Buyer Demand - Dunedin

2018 market activity has started off

relatively positively for Dunedin, with

gradually increasing volumes leading to a

strong week ending 18 February 2018.

There has been a lift in mortgaged

multiple property owners in Dunedin,

including those from Auckland. This

is a surprise considering the generally

accepted lower level of rental stock in

the student city and the fact that the

policy spotlight is currently on the need

to improve rental quality. Many were

expecting that areas like Dunedin would

become a less attractive investment

option. It may be too early to draw this

connection yet, but it’s certainly one to

keep an eye on.

Buyer Classification - Dunedin

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 42

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.Dunedin Values

Average value of stock – Dunedin

The growth in values in Dunedin has been

modest but consistent, with 2.8% growth

in the last three months and 9.3% growth

over the last 12 months.

Values across the Peninsula and Coastal

areas have been volatile with values

dropping dramatically over winter and

quickly regaining those losses in spring

and now showing signs of stalling again

(although retaining 3.2% growth in the last

three months due to prior growth).

In Taieri, values have again started to rise,

albeit at a slower rate than other parts of

the City.

Annual and quarterly change in value - Dunedin

January 2018

Current Value 3 months 12 months Since 2007 peak

Dunedin Central & North $410,278 3.2% 10% 36%

Dunedin South $373,189 2.0% 9% 31%

Peninsula and Coastal $360,397 3.5% 13% 33%

Taieri $402,502 1.8% 7% 37%

CoreLogic Monthly Property Market & Economic Update New Zealand February 2018 | 43

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication.

All rights reserved.For more information contact us 0800 355 355

© Copyright 2018. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

corelogic.co.nz (including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.You can also read