Financial Management Assessment Uzbekistan: Tashkent Province Water Supply Development Project

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Tashkent Province Water Supply Development Project (RRP UZB 46135)

Supplementary Appendix

Financial Management Assessment

Project Number: 46135-001

August 2016

Uzbekistan: Tashkent Province Water Supply

Development Project

ABBREVIATIONS

ADB = Asian Development Bank

AFS = audited financial statements

APFS = audited project financial statements

EA = executing agency

EIA = environmental impact assessment

FMICRAMP Financial Management, Internal Control and Risk Assessment and

Risk Management Plan

GOU = Government of Uzbekistan

IA = implementing agency

ICB = international competitive bidding

LIBOR = London interbank offered rate

NCB = national competitive bidding

NGO = non-government organization

PAM = project administration manual

PFR = periodic financing request

PFM Project financial management

PSC = project steering committee

QCBS = quality and cost based selection

RRP = report and recommendation of the President to the Board

EA = executing agency

SOE = statement of expenditure

TAC = technical approval committee

TPS = Tashkent Provincial SuvokavaI. CONTENTS

I. INTRODUCTION ................................................................................................... 3

II. BRIEF PROJECT DESCRIPTION ......................................................................... 3

III. COUNTRY AND SECTOR FINANCIAL MANAGEMENT ISSUES ......................... 4

A. Country Level Issues ................................................................................. 4

B. ADB Country Portfolio ................................................................................ 7

II. Source: ADB Uzbekistan Fact Sheet, 31 December 2015 ..................................... 7

A. Water and Sanitation Sector ...................................................................... 7

IV. PROJECT FINANCIAL MANAGEMENT SYSTEM................................................. 8

A. Overview of the executing agency/implementing agency, Financial

Management System and Institutional Context .......................................... 8

1. Budgeting and Funds Flow Arrangements ................................................10

B. Review of UCSA and TPS ........................................................................11

2. UCSA........................................................................................................11

2. Tashkent Provincial Suvokava ..................................................................12

C. Personnel, Accounting Policies and Procedures, Internal and External Audit .......12

V. RISK DESCRIPTION AND RATING – INCLUDING THE FINANCIAL

MANAGEMENT AND INTERNAL CONTROL RISK ASSESSMENT ....................13

A. Inherent Risk.............................................................................................13

B. Control Risk ..............................................................................................15

C. Overall Risk Assessment ..........................................................................17

VI. TPS FINANCIAL ANALYSIS.................................................................................19

VII. SUGGESTED FINANCIAL MANAGEMENT CONVENANTS ................................32

A. Assurances/Covenants .............................................................................32

1. Right of Audit ............................................................................................32

2. Maintenance of Accounting Records .........................................................32

3. Accounting Performance Covenants .........................................................32

4. Governance and Anticorruption .................................................................33

VIII. CONCLUSION......................................................................................................33

ATTACHMENTS ..............................................................................................................34

A. UCSA........................................................................................................34

B. Tashkent Provincial Suvokova ..................................................................38

C. Financial Management Assessment Questionnaire...................................41

D. TPS Auditors Report for YE 2014 .............................................................54

E. UCSA Auditors Report for YE 2013 ..........................................................56

LIST OF TABLES

Table 1: Summary Risk Assessment Mitigation Plan.................................................................. 6

Table 2: ADB Country Portfolio .................................................................................................. 7

Table 3: TPWSDP Costs .......................................................................................................... 20

Table 4: TPS Historical Performance 2013- 2015 .................................................................... 21

Table 5: TPS Tariff Revision 2016............................................................................................ 22

Table 6: TPS Projected Consumption and Demand ................................................................. 23

Table 7: TPS Production Costs per M3 .................................................................................... 24

Table 8: TPS Production Parameters and Costs ...................................................................... 26

Table 9: TPS Projected Performance and Indicators ................................................................ 28

Table 10: TPS Projected Income Statement 2016 – 2027 ........................................................ 29

Table 11: TPS Projected Cash Flow Statement 2016 – 2027 ................................................... 30

Table 12: TPS Actual and Projected Balance Sheets 2013 – 2027 .......................................... 31

Table 13: TPS Projected Water and Sewerage Tariffs 2013 – 2027......................................... 31LIST OF FIGURES

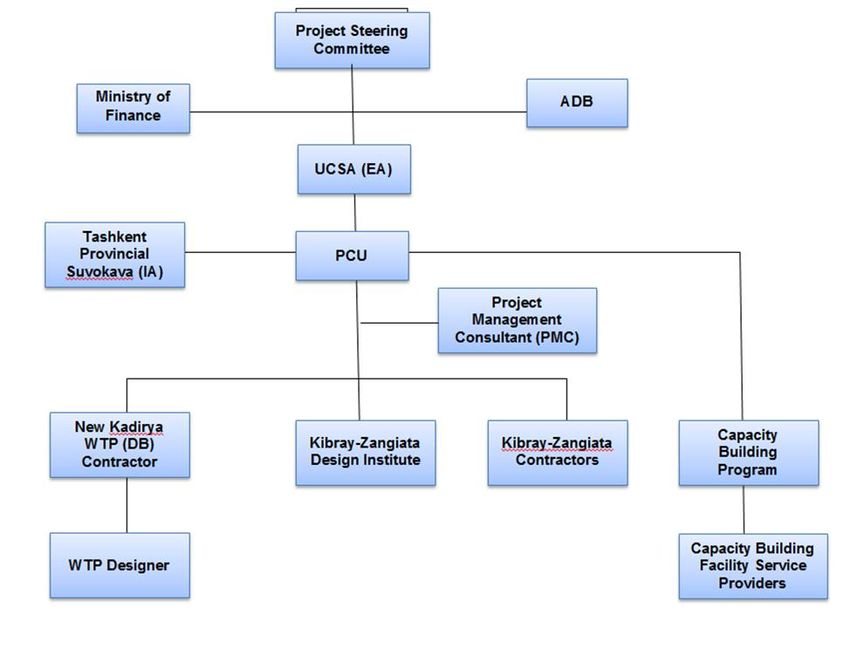

Figure 1: Project Implementation Organisation........................................................................... 9

Figure 2: Proposed Funds Flow ............................................................................................... 10

ATTACHMENT TABLES

Table 1. Summary of Tariffs in Tashkent ProvinceEXECUTIVE SUMMARY 1. This FMA, prepared as part of due diligence for the Tashkent Province Water Supply Development Project (TPWSDP) covers the Uzkommunhizmat or UCSA, the Executing Agency, the agency responsible to overseeing the water and sanitation sector, and the Tashkent Provincial Suvokava (TPS), the proposed Implementing Agency (IA), which is responsible for water and sanitation services in Tashkent Province and the recipient of the project. These two organizations were interviewed as part of the assessment. 2. UCSA has about eight years of experience in implementing ADB-funded projects in the water supply and sanitation sector. UCSA has been submitting audited project financial statements (APFS) of acceptable quality. However, a recent review of the entity financial reports for UCSA has noted that USCA has not been fully implementing the financial reporting arrangements as envisaged in the legal agreements. TPS, the IA, has no experience in the financial management and implementation of a large and complex water sector project. Moreover, TPS was reconstituted only recently in January 2016 by consolidating 19 former district vodokanals as part of the restructuring of the water supply sector following Presidential Decree 306 dated 30 October 2015. In its former role, TPS was only responsible for providing supervision and support to the districts, consequently the entity is only beginning to develop in its role as the operator for all services in the province. TPS in its current constitution as utility operator has not been audited, and the financial capacity assessment as well as financial management assessment is based upon unaudited consolidated information provided by TPS. 3. Overall the assessment of financial management risk for TPS and for the project is Substantial. 4. A comprehensive package of assistance and support to financial management is proposed in the project. The Project Coordination Unit (PCU) in UCSA, dedicated to the implementation of ADB-funded projects, will be staffed with a full-time Financial Management Specialist and Accountant during the five-year project implementation. And, in addition the proposed Project Management Facility (PMF) will include consultant support in the form of an international financial expert for five person-months over the first three years of the project, and 41 person-months for a national finance specialist. TPS will also recruit more financial management staff in its organization dedicated to the financial management of the project, who will be trained by the PCU staff of UCSA and the PMF consultants. The PMF technical assistance will support TPS in developing its financial management capability through training and preparation of a financial manual and provide advice on upgrading the financial management resources and processes required for a modern utility provider. In addition the proposed capacity development program for the project includes training modules and packages covering: financial management, budgeting and reporting, as part of developing an efficient financial management system. Training will also be provided in procurement, internal auditing and for tariff setting, customer relations and management and other associated topics related to financial management in response to an identified need. This support is considered necessary to ensure the sustainable and effective management of project finances and to strengthen TPS financial management capacity. 5. The Government of Uzbekistan has a policy of allowing tariff revisions for water and waste-water every six months, taking into consideration the prevailing costs. Water utilities are allowed to set a tariff to earn a profit margin not exceeding 10% of the production costs including depreciation but excluding administration costs. This policy has been consistently followed in recent years. For example, for Kibray district the domestic water tariff increased by 209% and sewerage by 105% between April 2013 and

2 March 2016, and for Zangiota by 89% for domestic water and 141% for sewerage over the same period. 6. A financial model of TPS has been prepared projecting income and expenditure over the period 2016 to 2027 based on the projected increase in water demand and sewerage production. The model, prepared in nominal prices, shows that modest real increases in tariff during 2016 to 2021 would achieve the target profit margin of 10%. The ADB-financed project will add about UZS600 billion in assets in 2022, which is about 20 times the net fixed assets of UZS30 billion reported in 2016. A tariff increase of 47% in real terms would be necessary in 2022 to support the substantially increased depreciation as a consequence of the 20-fold jump in the asset base, and to meet the debt servicing charges for repayment of the loan principal and interest. Such substantial increases are still allowable within the current policy of the Government that allows full recovery of costs and a profit margin capped at 10%. However, it is to be noted that TPS is likely to embark upon a substantial capital investment program to rehabilitate its existing network across its entire service area for both water supply and wastewater, including expanding service coverage. No cost estimates or investment plans are, as yet available. Financial covenants are proposed in the legal agreements to ensure that TPS remains financially solvent.

I. INTRODUCTION

1. A financial management assessment (FMA) was conducted for all the enterprises

that will be involved in the Tashkent Province Water Supply Development Project

(TPWSDP), Project Number: 46135-004, which is the outcome of TA-8227 UZB Second

Water Supply and Sanitation Investment Program (SWSSIP) implemented during 2015/16.

In particular, the assessment covered the Uzbekistan Communal Services Agency (UCSA),

specifically the Project Coordination Unit (PCU) within UCSA dedicated to the

implementation of ADB-funded projects, which is intended to be the Executing Agency (EA)

for the project, and the Tashkent Provincial Suvokova (TPS) the Implementing Agency (IA).

The FMA included:

(i) an interview with the senior management and the Chief Accountant in each

organisation;

(ii) a review of their accounting and reporting systems and resources, internal

and external auditing, fund disbursement, and information systems, and;

(iii) An analysis of the last three years annual financial statements (income

statement, sources and applications of funds statement, balance sheet), to

determine the key performance indicators and financial ratios.

(iv) Inspection of Audit reports, where available

(v) Update of the FMAs for stakeholders that was prepared in 2013/14 as part of

the earlier project preparation activities for SWSSIP

2. The FMA was undertaken in 2016 by the consultants responsible for the preparation

of the TPWSDP and included a review of documentation for other recent ADB projects in

Uzbekistan, particularly the Djizak Waste Water Project, and the Tashkent Solid Waste

Management Improvement Project, and discussion with key stakeholders. The FMA is based

on ADB’s Guidelines for the Financial Governance and Management of Projects Financed

by the Bank (2002) and Financial Management Guidelines Technical Note, ADB, May 2015.

The instrument used for assessment was ADB’s standard financial management

assessment questionnaire (FMAQ).

3. The FMA assesses the capacity of executing and implementing agencies and

their systems in the areas of planning and budgeting, management and financial

accounting, reporting, auditing, and internal controls. The FMA also includes a review of

proposed disbursement and funds-flow arrangements, and identifies measures for

addressing identified deficiencies in financial management. The results of a financial

analysis of TPS using a financial model to project incomes and expenditure and financial

performance over the period 2016 to 2027 is also included.

II. BRIEF PROJECT DESCRIPTION

4. The TPWSDP will rehabilitate and improve water supply within an existing, outdated

and obsolete regional water supply fed from a 105-km long water transmission main in

Tashkent Province, serving inhabitants in part of two districts of Kibray and Zangiota. The

project will involve: reconstruction of the Kadiyra water treatment plant with the capacity of

105,000m3 per day; construction of a 58.3 km water transmission main, the construction of

eight new and the reconstruction of nine water distribution centers and pumping stations,

27.2 km of distribution mains, 337.8 km of distribution pipes and the reconstruction of village

distribution networks including metered household connections for an estimated 49,255

households. The Project with an estimated cost of $143.83 million will be implemented over

five years 2017 to 2021. The ADB will provide an ADF loan of $120.9 million to fund

approximately 84% of the costs with the government responsible for funding the remainder,

made up of tax and duties.4

5. The project will have two outputs:

(i) Output 1: Kadirya regional water supply system improved and fully

operational. Output 1 will consist of a new potable water treatment plant (WTP)

producing 105,000 m3 of water daily, 58.3-km length of water transmission mains,

eight new and nine rehabilitated pumping station mains, 27.2-km of distribution

main pipes, 337.8-km of distribution pipeworks, and 49,256 household water

supply connections.

6.

(ii) Output 2: Improved financial, operational, and system management of the

TPS for Zangiota and Kibray District branches. Output 2 will consist of

support for the financial, operational and system management of TPS, including

the provision of training for technical and financial management, assistance with

the establishment of customer care units at the Zangiota and Kibray district

branches, installation of household water meters, and implementation of a

computerized financial management system.

7. Executing and Implementing Agencies. The EA is will be a project coordination

unit (PCU) within UCSA, while the IA will be TPS. The proposed project organization

structure is shown in Figure 1.

III. COUNTRY AND SECTOR FINANCIAL MANAGEMENT ISSUES

A. Country Level Issues

8. ADB Country Partnership Strategy.1 ADB’s current CPS 2012 – 2016, prepared in

2011, includes a governance risk assessment at the country and sector levels. This has

identified risks associated with public financial management, procurement, and institutional

accountability; and has proposed relevant mitigation measures. At the country level, public

financial management has improved, but the budget coverage is not fully comprehensive

and development expenditures financed through external loans and grants are not included

in the budget. To mitigate this, the government is implementing a medium-term budgetary

framework that will minimize off-budget expenditures, link overall budgeting to medium-term

policy priorities, and improve the accounting of development spending. At the sector level,

the single treasury account still needs to be rolled out. Tariff policies need to be adopted for

improved cost recovery and sector budgets need to be made more transparent. Improving

the quality of regulation is vital for promoting greater private sector participation at the sector

level. Effective enforcement of the country’s anticorruption laws requires strengthening their

operational procedures and improving internal and external audit policies and capacities.

ADB will support government-led efforts for governance and regulatory improvements, and

procurement reforms, at the sector level. Support for this will be provided through stand-

alone TA, and leveraging investments to strengthen sector institutions and performance.

9. Public financial management. The public financial management system in

Uzbekistan remains largely centralized. It is guided by a Public Financial Management

Reform Program, 2007–2018. The program, however, is yet to be fully implemented. Its key

components include (i) establishing a fully functioning uniform treasury system, (ii) adopting

and implementing a modern, unified budget and accounting system; and (iii) introducing a

medium-term budget framework and program budgeting. Drawing on published documents,

the key achievements of the program to date include the following: (i) greater clarity in the

annual budget calendar has been developed, (ii) appropriation of public expenditure by

parliament is in practice, (iii) expenditure control schemes are operational, (iv) greater

capacity for cash flow forecasts has been developed, (v) a 3-year budget perspective has

1

ADB. 2012. Country Partnership Strategy: Uzbekistan, 2012–2016. Manila.5

been introduced, and (vi) approved and executed budgets are published annually. Viewed

from the perspective of the three sectors - energy, transport, and urban development - the

following challenges remain in the further rolling out of the Public Financial Management

Reform Program to the sector levels: (i) sector planning, budgeting, and financing links

needs to be strengthened through building improved capacity at the central, regional, and

executing agency level to collect and use relevant economic and financial data; (ii) greater

flexibility at the sector and local government levels is needed to manage expenditure

streams; at present, sectoral budget drafting and revisions require complex and time-

consuming negotiations with central authorities; (iii) improved mechanisms and incentives

are needed for rationalizing the operational costs of state-owned enterprises; (iv) improved

cost recovery level tariffs need to be instituted for sustainability at the level of the three

sectors; and (v) greater capacity is needed to speed up processing of contracts and

payments for sector projects and operations.

10. Budgeting. The Law on Budgetary System2 regulates the budgeting process in

Uzbekistan. This law provides the legal basis for the preparation, review, approval and

execution of the state budget. In the case of projects financed jointly with international

financial institutions (IFIs), the PCU within the IA is usually responsible for providing the

forecasted project budget for the subsequent year to the MOF for approval in December for

the next year. Government is taking strong measures to transform accounting standards in

order to make them consistent with international financial reporting accounting standards

(IFRS).3 There is sufficient accounting personnel capacity within the country with knowledge

of the national accounting standards, but they need to be trained in IFRSs, contemporary

financial management techniques and accounting software.

11. Audit. Internal audit in both the private and public sectors is considered poor in

Uzbekistan. Most government ministries and agencies do not have a unit responsible for

internal control and audit. MOF through its CRD unit is responsible for internal audit of public

sector organizations, but both the scope of its work and its human resources are limited.

The external audit system is being developed based on national auditing standards. External

audit is not compulsory for state ministries or agencies. However, Article 1 of the Auditing

Law (2000) states that if a certain international agreement signed by the Republic of

Uzbekistan lays down rules and regulations other than those contained in the legislation of

the Republic of Uzbekistan on audit activity, the former is applicable. Similarly, Article 2 of

the Law on Accounting (2016) also provides that accounting requirements stipulated by an

international treaty will prevail over the national rules. Projects financed by IFIs are subject to

annual audit by an independent external auditor, as long as the loan agreement between the

Government and IFIs stipulates this condition.

12. Risk Assessment Mitigation Plan. The summary RAMP in the table below, taken

from an analysis prepared in 2011 for the ADB CPS, highlights nine major governance risks

for the energy, transport, and urban development sectors in Uzbekistan. It proposes the

following general areas of ADB support to improve governance outcomes and mitigate the

associated key risks: (i) support rollout of public financial management systems at the level

of the three sectors; (ii) improve and build the capacity of sector agencies to strengthen

public financial management, procurement, and transparency systems; (iii) continue support

for the development of manuals, standard operating procedures, and training materials to

build greater efficiency in the procurement processes at the sector level; (iv) provide support,

on demand, to the government’s ongoing anticorruption initiatives; (v) promote the role of the

private sector and public–private partnerships as means to encourage greater openness and

transparency in the three sectors; and (vi) engage in proactive policy dialogue with central

2

Law of the Republic of Uzbekistan No. 158-II on Budgetary System dated 14 December 2000 and amended on

23 May 2005.

3

The recent revision of the Accounting Regulation dated 15 April 2016 has strengthened the accounting

regulatory structure in accordance with recommended international accounting standards.6

and sector agencies to strengthen and promote reforms and improvements to public

financial management, procurement, anticorruption policies, plans, and procedures.

Table 1: Summary Risk Assessment Mitigation Plan

Identified Major Risks Proposed ADB Mitigation Actions

1. Public Financial Management

ADB to continue policy dialogue and support to the

1.1 The rollout and implementation of

Government of Uzbekistan to (i) advance and roll out

the

PFM systems to sector level, and (ii) pilot solution-

Public Financial Management Reform oriented approaches for PFM improvement in priority

Program, sectors through TA and other means.

2007–2018 could be slow and delayed. This will

affect the quality of PFM and the rollout of

PFM reforms to the energy, transport, and

urban development sectors, and to the local

government levels.

1.2 Sector policies and budgeting are not fully ADB to engage in policy dialogue with the government

linked. and sector agencies to (i) support coordination and

This brings the risk of inadequate prioritization of linkages between sector plans, budgets, and

allocation for expenditures and investments in the commitment of public funds; and (ii) support the

three sectors, and delays in project government’s new welfare improvement strategy that will

implementation. provide costing of sector investments that are fully

owned by the government.

1.3 Sector capacities for planning, ADB to provide capacity support for sector staff on

forecasting, and financial management, planning, and results-based

cost benefit analysis in the three sectors are approaches.

insufficient. Sector planning is thus not results-

based, which leads to suboptimal use of resources.

1.4 Sector tariff policies need ADB to engage through sector-specific policy dialogue,

rationalization for TA projects, and training to support the Ministry of

improved cost recovery. Current tariffs are not Finance, treasury, sector agencies, and local agencies to

sufficient to cover operations, maintenance, and enhance capacities, and policies and procedures, for

capital expenditures at the sector level. This affects estimating and implementing cost-recovery tariffs.

the effectiveness, efficiency, and sustainability of

the delivery of services in the three sectors.

1.5 Internal control on revenue and ADB to provide capacity building support to (i) strengthen

expenditure the internal audit units of sector agencies,(ii) promote

management is insufficient at sector levels. expanding the scope of the audit beyond inspections,

Lack of capacity and/or ineffective internal audit and (iii) encourage external auditing in sectors and

units can lead to projects (where needed) to complement internal controls.

diversion of funds to unauthorized uses.

2. Procurement

2.1 Delays in procurement contracts The government has set up high-level tender

registration, on committees, which are expected to be effective in

account of price verification procedures controls. reducing delays associated with price verification. ADB to

This can lead to delays in project implementation, continue policy dialogue with the government for work-

mis- procurement due to increased costs and process enhancements of public

claims from contractors, and open opportunities for p r o c u r e m e n t . ADB-

possible collusion in the three sectors. assisted TA support is ongoing for raising the capacity of

executing agencies on procurement.7

2.2 Limited capacity to manage ADB to (i) continue support for capacity enhancement of

(international) staff of executing agencies in the three sectors on

procurement. Procurement capacity in sector international procurement, (ii) continue support for work-

executing agencies for consultancy services is process enhancement of the procurement system, and (iii)

particularly low because of lack of well- conduct regular procurement needs assessment of sector

established internal rules and procedures and agencies with the engagement of qualified local and

underdeveloped national legislation. international consultants.

3. Anticorruption Arrangements

3.1 Internal and external audit policies and ADB to (i) ensure inclusion of relevant provisions of its

capacities Anticorruption Policy (1998, as amended to date) in

need strengthening to prevent corrupt sector loan and project agreements and bidding

practices arising from lack of transparent documents; (ii) provide technical support on demand to

monitoring and misuse of funds build capacities of sector agencies for internal and external

at the sector level. audits; and (iii) hold regular dialogue with central and sector

agencies on findings of audit reports of ADB- assisted

projects to resolve outstanding issues.

3.2 The approval of the National Plan for ADB to undertake policy dialogue with the government

Fighting on enhancing the effectiveness of the anticorruption

Corruption is still pending, which restricts the framework, including the approval and implementation of the

effectiveness of the institutional framework for National Plan for Fighting Corruption.

anticorruption.

ADB = Asian Development Bank, PFM = public financial management, TA = technical assistance.

Source: ADB. 2011. Uzbekistan: Consolidated Governance Risk Assessment and Risk Mitigation Plan

covering National Level and the Energy, Urban, and Transportation Sectors. Manila. Unpublished.

13. PEFA. A Public Expenditure and Financial Accountability (PEFA) review of the

country’s public sector financial management is recorded as being prepared in 2012 but a

published report is not available through their website.

B. ADB Country Portfolio

14. ADB’s Country Portfolio for Uzbekistan as of 31 December 2015 records 165

projects with a total value of $5,215.8 million, as summarized in Table 2 below. The water

and urban services sector makes up 11% of the total portfolio.

Table 2: ADB Country Portfolio – December 2015

Sector No. ($ million) %

Agriculture, Natural Resources and Rural

Development 28 581.74 11%

Education 21 296.95 6%

Energy 22 1,541.20 30%

Finance 23 629.94 12%

Health 4 41.60 1%

Industry and Trade 3 175.68 3%

Public Sector Management 15 29.73 1%

Transport 28 1,329.85 25%

Water and other Urban Infrastructure and

Services 21 589.12 11%

Total 165 5,215.81 100%

Source: ADB Uzbekistan Fact Sheet, 31 December 2015

Note: Grants and technical assistance include co-financing.

A. Water and Sanitation Sector

15. Uzbekistan’s water supply sector is currently undergoing a major transformation,

notably through nationwide reorganization of its sector institutions and implementation of8

sector-wide management, financial and cost recovery reforms. Driven largely through

Decree 3064, enacted in October 2015, State Unitary Enterprises (provincial Suvokavas)

have been established in each province of the nation, with the responsibility to develop and

implement water supply and sanitation improvements in their respective jurisdictions. In

conjunction with this, previously independent district water and sanitation enterprises

(Suvokavas, (also called vodokanals), have also been restructured and have been absorbed

as district branches into their respective provincial Suvokavas.

16. Decree 306 also stipulates specific measures that are destined to further strengthen

the viability and sustainability of provincial Suvokavas. Firstly, it mandates implementation of

over 40 definitive sector improvement actions, outlining the respective implementation

mechanisms, completion dates and responsible agencies5. Secondly, it requires the

establishment of two high-level committees: one to ensure the recruitment of qualified

management personnel for Suvokavas6, and the other to monitor the timely servicing of

water sector loans of international financial institutions7. Under the leadership of MOF and

UCSA, significant sector reforms are already being achieved: Suvokova charters have been

formulated, State registrations completed, business plans prepared, tariffs harmonized,

asset inventories conducted, and skilled professional and support personnel recruited.

IV. PROJECT FINANCIAL MANAGEMENT SYSTEM

A. Overview of the Executing and Implementing Agency, Financial

Management System, and Institutional Context

17. It is proposed that UCSA, through its PCU dedicated for ADB-funded projects, will be

the Executing Agency (EA) for the project responsible for overall implementation and

coordination. A project steering committee, chaired by the Minister of Finance and

comprising of representatives of MoF, UCSA, Ministry of Environment, Ministry of Health,

Tashkent Province, and other relevant stakeholders, such as Agriculture and water

resources, Foreign economic relations, Investment and trade, will provide overall guidance

on TPWSDP implementation. A separate unit within the PCU will be formed for the

implementation of the project as an adjunct to the existing PCU in UCSA that is dedicated to

the implementation of ADB-funded projects. The PCU will have seven staff covering the

professional disciplines of water supply engineering, water treatment plant engineering,

environment, social safeguards, financial management etc. and support staff.

18. The Tashkent Province Suvokova (TPS) is designated as the Implementing Agency

(IA) with a special unit placed in the Strategic Development Department of TPS. The IA will

be supported by the staff of the PCU, the Project Management Facility (PMF) consultants,

and in addition receive specific capacity development technical assistance through the

proposed capacity development program of the project. TPS will recruit additional

accounting staff for the IA that will be dedicated for the financial management of the project.

The proposed implementation arrangements are shown in Figure 1.

4

Decree 306 ‘On measures to implement the main directions of development of the organizations of water

supply and sanitation’ enacted by the Cabinet of Ministers on 30 October 2015.

5

These actions relate to improvements in water supply system management, physical infrastructure provision,

tariff and accounting system policy, Suvokova staffing capacity, information and communication technologies,

consumer connections, and consumer awareness.

6

‘Committee for attestation and appointment of managerial personnel of SUE Suvokova and its city and district

branches’, chaired by the Deputy Prime Minister of the Republic of Uzbekistan.

7

‘Inter-agency Commission for monitoring of timely servicing of loans received from international financial

institutions under the guarantee of Republic of Uzbekistan for the development and modernization of water

supply and sanitation systems’, chaired by the Deputy Prime Minister of the Republic of Uzbekistan.9 Figure 1: Project Implementation Organisation

10

1. Budgeting and Funds Flow Arrangements

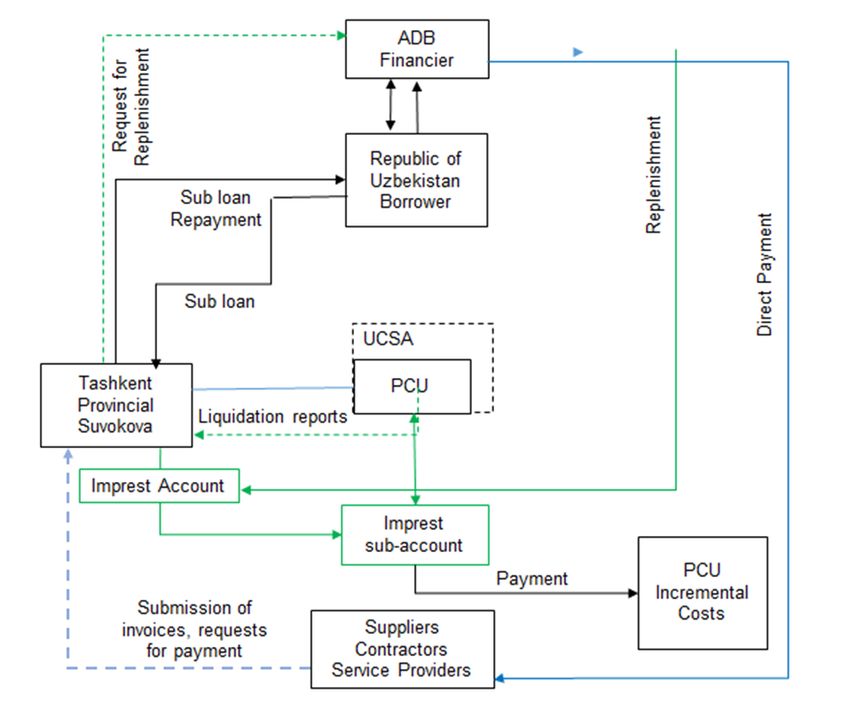

19. The proposed funds flow is shown below in Figure 2.

Figure 2: Proposed Funds Flow

20. Funds Flow Mechanism: The proposed Funds Flow arrangements for the Project

are indicated in Figure 2 above. The IA will be responsible for preparing withdrawal

applications which will require the approval of the PCU before the funds are disbursed. ADB

will make payments directly to suppliers and contractors, subject to a minimum claim size of

$100,000 equivalent. An imprest account will be established in a bank acceptable to ADB,

and a sub-account will be provided to the PCU for financing the incremental recurrent costs

of the PCU (staff salaries and office operating costs).8 The IA will be responsible for project

financial accounting and reporting. The borrower will be responsible for implementing the

project according to the loan agreement and other agreements. On its part, ADB will monitor

the project and review its progress to ensure that the loan proceeds are spent as agreed

8

In a change from the funds flow procedure for earlier projects implemented by UCSA under the earlier tranches

of SWSSIP, UCSA will not be directly involved in the channelling of funds from ADB to contractors and

suppliers and for receiving loan debt servicing repayments from the IAs for transmission to MOF. Loan funds

will be paid from ADB directly to the contractor/ service provider on the authorisation of the PCU and similarly

the repayment of loan funds from TPS will pass to the Tashkent Provincial Administration and onto MOF.

However, UCSA will continue to provide supervision and will need to approve all payments being made, to

supplement the weak financial management capacity of TPS.11

upon. When a loan becomes effective, a loan account will be opened in ADB’s books in the

name of the borrower and the loan amount is credited to that account. All disbursements

under the loan will be carried out in accordance with ADB’s Loan Disbursement Handbook

(2015, as amended from time to time).

B. Review of UCSA and TPS

2. UCSA

21. UCSA is the premier agency in Uzbekistan in the water sector. Currently, It

supervises several other agencies, including an engineering company, the interregional

trunk mains (IRTMs), two project coordination units (PCUs), and the agency

Uzcommunukotashkilotchi (UCTK), and formerly project implementation units in different

provinces. UCSA prepares standalone accounts for itself, and the IRTMs and UCTK, and the

engineering company. UCSA has eight years’ experience in the implementation of projects

in the water supply and sanitation sector funded by ADB, World Bank and other IFIs,

including projects under the first and second water supply and sanitation investment

program, having been set up in 2008. A recent restructuring of the PCU arrangements

within UCSA now limits it to having only two PCUs, one for ADB projects and another for WB

funded projects. Previously there were several PCUs within UCSA dedicated for individual

projects. This means that UCSA no longer can set up new separate PCUs dedicated to the

implementation of a particular project and it is proposed that for TPWSDP a new separate

sub-unit or department with be setup within the existing PCU dedicated for ADB-funded

projects.

22. UCSA, through its PCUs, has the capability and experience for financial

management for the implementation of the project. However, a recent assessment of the

audit process for the consolidated entity and project financial statements relating to the

disbursement of funds from earlier MFF tranches has highlighted some substantial

deficiencies, as noted below.

a. The reporting currency used in the consolidated project financial statements was in

US dollars, whereas in accordance with the Cash-based International Public Sector

Accounting Standards (IPSAS) the reporting currency should be the local currency

Uzbek Sums (UZS).

b. In accordance with the subsidiary loan agreements, ADB loans are on-lent by the

Ministry of Finance (MOF) to UCSA, on a back-to-back basis, on the same terms

and conditions as received from ADB. UCSA is responsible for the interest rate and

exchange rate risks. For the first tranche, UCSA was to on-lend the loan to

beneficiary Suvokavas and IRTMs, with the same terms as regards exchange rate

and interest rate risks, but charge a premium of 0.20% per annum. For the

remaining tranches, UCSA was to on-lend the proceeds without any premium.

Because of the way the funds flow and on-lending arrangements have been

structured under the MFF, the legal agreements for the first three tranches include a

requirement for UCSA to prepare entity level financial statements to capture all the

financial flows. For the fourth tranche, the legal agreements require the Suvokavas

to submit entity financial statements.

c. In the past, UCSA has submitted the standalone financial statements of UCSA as

the entity financial statements required under the legal agreements. However, these

statements did not disclose any of the other activities, such as those of the IRTMs,

PPMU or the engineering company, or the ADB supported projects.

d. In fact, UCSA has not incorporated the financial transactions arising from the ADB

supported projects for the last six years. The assets being created under the

project, together with the liabilities that have accrued in UCSA to the MOF against12

the ADB loans have not been accounted for in the books of UCSA. The

consolidated project financial statements (prepared in US dollars) are not intended

to serve this purpose. They are special purpose financial statements prepared on a

cash basis, and serve merely to report cash inflows and outflows. This issue has

been brought to the attention of UCSA and MoF by ADB and is in the process of

being resolved: the MOF has agreed to get UCSA's accounts revised to incorporate

the obligations arising from the ADB loans.

e. In the financial accounts of UCSA the ADB loan should be reported as a loan from

GoU and on the assets side it should have a corresponding entry for a loan to the

loan recipients – the IRTM, and provincial Suvokavas. In turn, in their books, the

loan should be reported as a liability to UCSA, while on the assets side of the

balance sheet it should be matched by “assets under construction” or assets in

operation created by the project expenditure. The accounting needs to capture both

ADB funding and funding by the government (whether by way of exemption of

taxes, or otherwise).

23. These issues are still in the process of being resolved and recently ADB has

supported the engagement of additional financial management services to assist UCSA in

addressing the issues and rectifying the deficiencies. The successful completion of this

work should ensure that UCSA can adequately perform its financial management function to

the satisfaction of ADB.

2. Tashkent Provincial Suvokava

24. Presidential Decree No. 306, dated 30 October 2015 provided for the consolidation of

district and city Suvokavas in each province into a provincial Suvokava, renamed as a State

Unitary Enterprise Suvokova. The existing entities became branches of the Suvokova.

Under the order the Tashkent Provincial Suvokova absorbed the assets and liabilities of the

19 city and district branches and assumed the responsibility for managing the WSS services

in Tashkent province. TPS is also responsible for the repayment of loans comprising both

principal and interest to ADB, and absorbing the foreign exchange risk.

25. TPS has no experience of implementing internationally-funded projects, and the

scale, complexity and rigor of managing the implementation of the TPWSDP will tax its

existing resources and systems. Furthermore, TPS has only recently been reorganised from

1 January 2016 to take over the responsibility for managing the delivery of water supply and

sewerage services in the province as a utility operator, and is still in the process of transition

to this new role. The IA that it is proposed will be set up in the Strategic Development

Department of TPS will be a new organisation. Support to the IA will be provided by PCU

staff and the PMF, complemented by the capacity building program that is proposed under

the project for TPS. In addition TPS plan to recruit extra staff for financial management of the

project.

26. Details of the FMA for UCSA’s PCU and TPS are included in an appendix to this

report.

C. Personnel, Accounting Policies and Procedures, Internal and External

Audit

27. Personnel: Technical assistance personnel arrangements and positions within the

PCU and the PMF to support the IA will be as is proposed by the design consultants report,

and agreed by ADB and the government. It is proposed that a comprehensive capacity

development program will be provided to TPS, including support to FM and procurement, to

strengthen its capacity to manage WSS after the completion of the investment project.13

28. Accounting Process: TPS is using the Russian accounting software, 1C, and will

upgrade to Version 8 by the end of 2016, so that all its branches accounting and reporting is

online. The former branches of TPS were not fully computerized.

29. Accounting Policies and Financial Reporting: Accounting processes will follow the

Law on Accounting (2016) and adopt Uzbekistan National Accounting Standards, GoU

procedures and where applicable appropriate International Financial Reporting Standards

(IFRS) will be applied for project financial reporting for ADB funds. The accrual basis of

accounting will be adopted.

30. Internal and External Audit: Internal audit is not undertaken within TPS and

external audit by an independent external auditor is scheduled to be done annually. The

Project accounts will be subjected to an annual external audit by an approved external

auditor and the audit report provided to ADB. TPS will provide the auditors with the annual

project financial statements in a timely manner within t hr ee months after t h e f in an c ia l

year-end to ensure that annual audits can be completed within the covenanted time period.

31. Information Management. A modern information management system suitable for a

large water supply utilities operation will be introduced to TPS with the support of the

capacity building program funded under the project.

V. RISK DESCRIPTION AND RATING – INCLUDING THE FINANCIAL

MANAGEMENT AND INTERNAL CONTROL RISK ASSESSMENT

32. A Financial Management Internal Control and Risk Management Assessment was

conducted for the project, and the proposed IA. The risk-assessment approach is based

largely on the International Standard on Auditing 400 Risk Assessment and Internal

Control. The following risk assessments are based on the IA existing structure, staffing,

resources and procedures. It includes recommendations for risk mitigation measures. The

level of risk is assessed according to four levels:

High - H likely to occur, will have high impact if occurs

Substantial - S unlikely to occur, will have high impact if occurs

Moderate - M likely to occur, will have low impact if occurs

Low - L not likely to occur, will have low impact if occurs

A. Inherent Risk

33. Inherent Risk is the susceptibility of the project financial management system to

factors arising from the environment in which it operates, such as country rules and

regulations and the entity working environment (assuming the absence of any counter

checks or internal controls).14

Risk

Risk Description Impact Likelihood assessment Mitigation Measures

INHERENT RISK

1. Country- Specific Risks H Likely H (i) This is an exogenous risk beyond

(i) Vulnerability of the control of the project. The impact

macroeconomic stability of this risk will need to be dynamically

and the fiscal position from monitored, and mitigations will require

external shocks, particularly country level intervention.

the weaker economy in

Russia, a major trading (ii) The project will be required to

partner. repay the ADB loan at the official

(ii) The divergence between exchange rate, and is protected from

the official and market market-based exchange rates.

exchange rate which has

repercussions for domestic

inflation and project costs,

and exchange rate risk for

debt servicing.

Weak Public Financial H Less Likely S TPS and project financial management

Management, lack of will be ring-fenced from the larger

transparency and public financial management. A clear

accountability and lack of organizational and implementation

internal audit processes, structure for TPS, PCU and the project

accountability for ADB funds will be prepared with specific terms of

and recording of liabilities reference for the staff and the design

and assets. and supervision consultants.

Capacity development support will

mitigate the impact.

2. Entity- Specific Risks H Likely S Government is addressing issues of

TPS is a newly formed entity residual liability and outstanding

with expanded responsibility accounts receivable through a

for the delivery of WSS rationalization of historical debt and

services in Tashkent recovery of arrears.

province, having taken over The proposed PCU and PMF staff will

the debts and liabilities of the provide support and guidance,

former district Suvokavas. Its complimented by the proposed

cash flow position and capacity development.

financial sustainability are

threatened.

Current tariffs will need H Likely H Government as recently updated the

significant revision to cover tariff review and setting process to

operations, maintenance, allow for tariff adjustment twice a year

and capital expenditures at in response to changes in costs and

the sector level. This affects recognizes the need for support etc.

the effectiveness, efficiency, Project management will support

and sustainability of the necessary tariff increases necessary

delivery of WSS services for cost recovery to ensure financial

and TPS capacity for viability, taking account of tariff

repayment of the ADB loan. affordability of the population,

especially the poorer segment

Financial management H Likely H TPS has plans to upgrade and

capability and resources are modernize the accounting and

limited affecting reporting systems from branch level to

transparency and the center.

accountability risks and Project will provide assistance to

reporting and monitoring. financial management through the

PCU and PMF staff and the proposed

capacity development program and the

preparation of an accounting financial

manual.15

Risk

Risk Description Impact Likelihood assessment Mitigation Measures

3. Project- Specific Risks H Less S TPS will be fully supported by UCSA

The relatively complex and Likely for all aspects of project

large scale of the proposed implementation, with additional TA

WS development project to support from ADB. Comprehensive

be implemented by an support for project implementation

organization with no track- through adequate staffing of the PCU

record and experience in and PMF consultants coupled with a

managing the comprehensive capacity development

implementation of such a program.

project. Operator training will be embedded into

the design and build contract for the

construction and operation of the

Kadiyra WTP.

It is recommended that an associated

corporate development support

program be pursued for TPS, possibly

supported by a piggy-back TA or grant

Management and skill H Less Likely S UCSA

fundingwill provide

from other overall

donors.supervision

capacity issues in financial and guidance to TPS at every stage of

management and weak project implementation.

administrative capacity to Targeted capacity building and training

implement reform and will be provided to the IA (TPS) to

modernization of financial address low levels of skills and

management, billing competency in financial management.

systems, tariff collection etc.

A project financial manual will be

prepared

Rehabilitation of the HQ and branch

offices and update of facilities

(electricity reliability, internet, essential

equipment) is proposed under the

Overall Inherent Risk S project.

B. Control Risk

34. Control Risk is the risk that the Project’s accounting and internal control framework

are inadequate to ensure project funds are used economically and efficiently and for the

purpose intended, and that the use of funds is properly reported.

Risk Mitigation Measures or Risk

Risk Description Impact Likelihood Assessment Management Plan

CONTROL RISK

1. Implementing Entity H Likely H The project implementation

TPS’s governance and arrangements have been designed to

capacity for financial address TPS’s shortcomings in

management, planning, implementing a large and complex

budgeting, reporting, and project through assigning key staff

verification is limited from the PCU and PMF to work

compounded by their recent closely with TPS.

promotion to be responsible

for delivery and management

of WSS services in Tashkent

province through 19 branch

offices, from their previous

administrative and supportive

function.16

Risk Mitigation Measures or Risk

Risk Description Impact Likelihood Assessment Management Plan

2. Funds Flow L Less likely L UCSA will continue to be fully

The proposed funds flow involved in project financial

mechanism with less accounting. Except for smaller value

involvement of UCSA is a payments up to $100,000 equivalent,

departure from the previous ADB’s direct payment and

practice. commitment letter procedures will be

used to pay contractors and

suppliers, ensuring timely payments.

The government will exempt taxes

and duties for the project.

Governance issues concerning funds

release and timely disbursement will

3. Staffing be addressed by the TA.

H Likely H A comprehensive package of support

TPS's financial management will be provided by the Project to TPS

staff have a relatively low staff through the proposed capacity-

level of skills and resources, building program, including those at

especially at district level, district branch level, through reform to

with limited opportunity for in- financial management, development

service training. of financial manual, computerized

accounting and billing systems and

training and human resource capacity

development.

TPS will recruit additional accounting

staff dedicated for the management of

4. Accounting Policies and M Likely M project

TPS finances the accounting

is upgrading

Procedures system to the latest 1-C accounting

The accounting systems software with its own resources.

used in TPS are not Reform of the budgeting, financial

standardized, with many management and reporting systems

branch offices use a manual will be addressed by the project and

excel-based system, which is computerized accounting systems

not conducive to the efficient and billing systems expanded to the

and effective management of district level, supported by ongoing

the entity, especially with training and follow up support through

respect to budgeting, a capacity building program.

accountability for the source

and application of all funds.

They do not have a

standardized accounting

manual

5. Internal Audit M Likely H Provision for additional support for

In line with government internal audit may be considered for

procedures, TPS does not the recruitment of an external audit

have an internal audit firm to function as internal auditor to

capability, which is a provide a continuous internal audit

limitation to internal control process. However, this requires

and accountability. further discussion with the

Lack of capacity and/or government before adoption.

ineffective internal audit

units can lead to

diversion of funds to

unauthorized uses.17

Risk Mitigation Measures or Risk

Risk Description Impact Likelihood Assessment Management Plan

6. External Audit H Likely H Project accounts/annual project

TPS as a State Unitary financial statements will be audited by

Enterprise is subject to an independent auditor as required by

annual audit, although audit the legal agreements, following

reports have not highlighted International Standards on Auditing.

any significant issues, and The TOR of the approved external

suggests underlying issues of auditor will highlight the need to

financial viability are not address these issues.

being fully acknowledged Issues raised in the audit report to be

and addressed. addressed and rectified promptly by

UCSA and TPS .

7. Reporting and Monitoring H Less S With adoption of an upgraded 1C

Financial reporting of income Likely version 8 accounting software, the

and expenditure is not degree of automation will be

produced automatically, increased.

requires manual extraction,

and cannot be easily verified

for completeness and

accuracy by management.

8. Safeguard of assets. L Less likely L Project financial reporting will include

Records of fixed assets on a full accounting for assets created

current and regular basis are under the project.

maintained, however it will

be necessary to ensure

proper addition to the assets

register of assets created by

the expenditure of the

project.

8. Information Systems H Likely S The modernization of TPS financial

TPS does not have a fully management will introduce a

computerized and up to date computerized accounting and

financial management Financial Information System at all

system or accounting levels with support to develop the

software that allow the capacity of accounting staff to use

automatic production of a upgraded computerized accounting

comprehensive set of systems, standardized across the

financial statements. District branch offices.

branch staff are not all The Russian IC accounting software

competent to manage the will be updated standardized and

accounting program (IC) installed in all branch offices.

proposed to be adopted.

The storage and back up of Financial records will be coupled with

records are not secure and physical records for management and

robust. preparation of annual performance

assessments of the delivery of WSS

services for planning and

management.

Overall Control Risk S Support will be provided to facilitate

the secure storage and retrieval

system for records.

C. Overall Risk Assessment

35. Risk Analysis. The inherent risk was assessed as Substantial due to country-level

risks. Control risk was assessed as Substantial, mainly because a regular internal audit is

not conducted by the CRU under MOF for TPS; TPS was only constituted in its present form

in December 2015 by consolidating existing smaller vodokanals, and is still consolidating itsYou can also read