Findings from 2020 research on attitudes and experiences in the domestic and SME electricity and gas markets in Ireland

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Findings from 2020 research on attitudes and

experiences in the domestic and SME

electricity and gas markets in Ireland

Prepared by Behaviour & Attitudes Ltd and The Research Perspective Ltd

On behalf of the CRU

Behaviour & Attitudes - Milltown House, Mount St Annes,

Milltown, Dublin 6 / +353 1 205 7500

i

Contents

Contents ............................................................................................................................................ ii

1. Executive Summary .................................................................................................................... 1

2. Key Findings ............................................................................................................................... 6

3. Research background ............................................................................................................... 11

4. Market background .................................................................................................................. 12

5. Purpose of the research ........................................................................................................... 12

6. Data Collection Methodology ................................................................................................... 14

7. Representative Sample............................................................................................................. 15

8. Market Satisfaction Profile ....................................................................................................... 16

9. Bill Delivery, Clarity and Understanding ................................................................................... 21

10. Response to the bill ............................................................................................................. 24

11. Clarity of bill estimated or actual status .............................................................................. 26

12. Bill delivery and rating – SME electricity and gas markets ................................................... 27

13. Domestic arrears ................................................................................................................. 29

14. Competition and consumer understanding of market structures ........................................ 33

15. Understanding and comparing offers .................................................................................. 36

16. Market Structure and Understanding .................................................................................. 37

17. Switching and Engagement.................................................................................................. 39

18. Drivers for switching amongst electricity and gas markets .................................................. 46

19. Drivers for not switching ..................................................................................................... 48

20. Overall experience of the switching process ........................................................................ 50

21. Dual Fuel ............................................................................................................................. 54

22. Assessment of the sales process .......................................................................................... 57

23. Awareness of the CRU and Complaint Handling .................................................................. 60

24. Vulnerable and Priority Customers ...................................................................................... 63

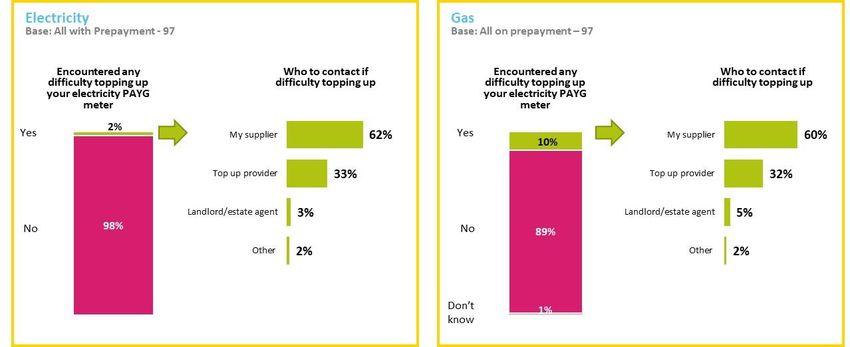

25. Prepayment ......................................................................................................................... 67

26. Smart Metering and Renewable Energy .............................................................................. 69

27. Impact of Covid-19 .............................................................................................................. 79

28. Conclusion ........................................................................................................................... 85

ii

1. Executive Summary

CRU defined its’ mission, vision and values for 2019-2021, together with four Strategic

Priorities to support the core activities of the Commission and to ensure the public interest is

protected. The Strategic Priorities relate to the delivery of sustainable low-carbon solutions

within well regulated markets and networks, to ensure compliance and accountability, to

develop effective communications to support customers and to maintain a high-performing

organisation to support the delivery of the work of the Commission. All of these in

combination seek to ensure public interest is served.

The annual survey into attitudes and experiences in the domestic and SME electricity and gas

markets was commissioned in the context of these and past strategic priorities. The survey is

used by CRU as one source of information to determine if the public interest imperative is

being met through monitoring the degree to which residential and business customers are

satisfied with their suppliers, the services offered and the functioning of the market in terms

of choice and competition. The survey gives CRU an insight into customer experiences and

attitudes within the energy market and both supports the market monitoring activities of CRU

and is used to inform policy discussion, decision, and development.

This research has been in place since 2011 and this report provides insight to the changes

which have occurred for different time windows since then. The 2020 research was conducted

by Behaviour & Attitudes and The Research Perspective under the direction of the CRU. This

survey is designed to ensure continuous annual measurement of customer experience and

attitudes in the residential and SME electricity and gas markets. Its design ensures

comparability with previous measurements undertaken since 2011 is maintained. Whilst

maintaining comparability is central, it also extends to update certain metrics to take account

of changes in the market and associated attitudes over time. This year presented a particular

challenge because the established methodology of face to face interviewing could not take

place, because of the restrictions associated with the Covid-19 pandemic. Therefore, the data

collection approach changed to comprise a combination of telephone and online panel

interviews. The research in the residential market is based on a nationally representative

sample of households, conducted using a Computer Based Telephone Interview (CATI)

approach and the Acumen Online Panel, to reach over 1,000 respondents, in each of the

electricity and gas markets. The total number of residential customers interviewed was 2,000.

1

The scope of the research includes the residential and SME electricity and gas markets. As

with previous years measurements, in the case of the residential market, the report is based

on the feedback of a sample of customers who use electricity or gas in their domestic

premises, including those with night saver meters. For both SME electricity and gas markets,

the focus of the research is on enterprises with low to medium consumption, typically meter

point categories DG5 and DG6, with 250 or fewer employees. The SME research was

unaffected by Covid-19 in terms of the data collection methodology, where a Computer Based

Telephone Interview (CATI) approach was used to get responses from 400 SME’s in the

electricity market and 250 in the gas market. Further details are provided in the Section –

Data Collection Methodology.

From a strategic perspective, the survey provides evidence of success for CRU in terms of its

vision and strategic initiatives. With the CRU focus on developing effective communications

to support customers and the regulatory process, there is clear evidence of increased

empowerment in the customer base, with a greater number of customers showing willingness

to leverage available technologies to compare offers. More domestic customers found it easy

to compare offers from electricity (47%) and gas (46%) suppliers. While this score still offers

much scope for improvement, this increased customer confidence is evidenced in enhanced

capability and sophistication when comparing offers. Less customers indicate that they

automatically continue with their current supplier when the contract has expired and there

has been a substantial increase in the numbers who report they look around to see if there is

a better offer available from a different supplier, to whom they can switch. Specifically when

comparing offers, customers report an increasing focus on comparing the unit cost of

electricity/gas, as opposed to just the overall bill amount, which increased from 48% in 2019

to 62% in 2020 for the electricity market. In addition, customers indicate an increased

appetite for more and varied information sources to aid in price comparison, to support

switching, with notable increase in those who report they used supplier websites and

comparison websites to support their research to switch.

Consumers are more willing to explore available options as they approach the end of their

contract, and to be proactive in searching for suitable switching options, as opposed to waiting

to be approached by a supplier. In particular, in the electricity market, the proportion of

contacts who opted to initiate contact to explore options for switching increased from 13% to

22%, and this in combination with the increased use of supplier and comparison websites

points to a more engaged customer base.

2

The increase in confidence is supported by the more informed customer base as evidenced by

the survey, where understanding of the relative roles of CRU, Networks and the suppliers is

continuing to improve. There is increasing understanding of the role of suppliers, particularly

in relation to billing and payment, where there was an increase of 23% among those who

understood that billing payment was not the responsibility of ESB Networks, rather that of

their supplier.

The key outcome from effective communication and empowerment centres on switching

levels. Switching has not yet become a routine or even firmly established behaviour with 44%

of electricity customers and 43% of gas customers indicating they have never switched

supplier. However, there is hope that increased empowerment and customer knowledge may

promote switching behaviour moving forward. The primary dependency for switching is

market awareness and credible alternatives. It is interesting to note that spontaneous

awareness of suppliers has followed a downward trajectory since 2017 and noteworthy

declines are recorded in 2020. Market awareness and knowledge of alternatives is a key

dependency for switching and therefore an area for action from a strategic perspective

remains to leverage increased engagement to improve market awareness to ensure a strong

and dynamic market. This may also include seeking to extend customer engagement beyond

price comparison to include product and service offerings, which will cause consumers to

investigate and explore market options further.

The strategic initiative related to the development of sustainable low carbon solutions

appears to be supported by consumers who are citing an increased acknowledgment of the

role of more environmentally friendly generation in decisions related to switching supplier.

There were increases in the proportion of respondents who agreed they would consider

switching if the prices were the same, but the electricity/gas product was from more

environmentally friendly generation sources. The emphasis on the importance of renewable

energy and Green Sources Product in influencing decision making about suppliers has been

confirmed by consumers where 89% of electricity customers feel it is important to ensure

that our energy is produced from renewable sources (for example wind, solar, hydro). This

represented an increase of 22% from 2019. In addition, 59% agree that a supplier’s ability to

provide ‘Green Source Products’ (energy from renewable sources) influenced their decision

making when choosing a supplier, representing an increase of 6% from 2019.

On the Smart Meters front, the work of CRU appears to be paying dividends, as the numbers

of consumers interested in getting a smart meter to monitor daily usage increased while

3

customer willingness to share their energy information with suppliers to avail of new offers

and services increased to 83% from 63% in 2019. Finally, notwithstanding the uncertain times

ahead in terms of financial security, there has been an increase of 14% from 2019 in the

proportion of customers who indicated they had undertaken significant energy efficiency

improvements (external insulation, heating installation of a high efficiency boiler etc.) in their

homes.

Overall customers indicate a decline in total satisfaction across electricity providers at 80% in

2020, which is a decline of 8% from 2019, and satisfaction with gas suppliers declined from

89% to 82%. It should be noted that at least part of this decline is due to the change in

measurement methodology, while another part may be attributable to a more discerning

assessment by customers given their reported increased levels of engagement and

involvement.

In the context of the SME sector, there is some evidence of engagement and empowerment

but not to the extent apparent in the residential sector, but both sectors exhibited similar

outcomes in terms of the constraint of reduced market awareness. Overall satisfaction with

electricity suppliers for SME’s remains steady at 82% and satisfaction with gas supplier has

also remained stable with 2019 levels at 85%.

While SME’s show increased capability in comparing offers, the momentum of previous

improvement is less evident and there is an increased tendency to automatically continue

with the supplier knowing the default tariff will be charged, which went from 3% to 16%.

Evidence of outcomes from the CRU strategic initiatives, which should lead to motivation to

optimise tariffs, explore viable market options and proactively decide on actions at contract

end, are more muted in the SME sector.

The SME market seems more dependent on energy suppliers taking the lead in outbound

contact, but reduced supplier-initiated contact seems to have resulted in reduced switching.

A total of 33% of SME’s reported that they have never switched electricity supplier (+5% from

2019) and 48% have never switched gas supplier (+14% from 2019). Similarly, there is a

reported decline in switching of 8% amongst electricity and gas SME customers, with current

levels of switching in the past 12 months at 17% and 14% respectively. The decline in

switching may be attributable to reported declines in outward contact by suppliers, which

decreased by 23% for electricity and 8% in gas, as reported by the respondents.

4

The strategic initiative related to the development of sustainable low carbon solutions

appears to be less compelling for SME’s who cite a reduced percentage importance (-7% from

2019) that our energy is produced from renewable sources (for example wind, solar, hydro)

but more (+6% from 2019) believe that a suppliers ability to provide ‘Green Source Products’

(energy from renewable sources) influence their decision when choosing a supplier. In

addition, there is evidence of more commitment to investment in energy efficiency

improvements.

Although significant external events such as Covid-19 is likely to cause business considerations

other than energy costs and considerations to have taken precedence (temporarily), there is

still evidence of an appetite for understanding costs and becoming more informed through

technologies such as smart meters, where 83% of respondents indicated an interest in viewing

daily electricity usage.

5

2. Key Findings

The key findings from the residential research include:

Context Setting: Market share and satisfaction

• The declines in market share experienced by Electric Ireland & Bord Gáis since 2016

have now settled & both providers continue to hold the lions share of the electricity

& gas market respectively. Note, market share is based on data provided from CRU.

• Energia’s share of the electricity and gas markets continues to gradually increase & it

now accounts at 11% of the electricity & 9% of the gas market.

• Spontaneous awareness of electricity & gas suppliers has been on a downward

trajectory since 2017.

• Satisfaction with energy providers remains high, but declines in satisfaction are

evident.

o 80% overall electricity supplier satisfaction (88% in 2019)

o 82% overall gas supplier satisfaction (89% in 2019)

Billing

• Within the electricity & gas market there has been a decline in those who pay when

they receive the bill, with electricity experiencing an increase in direct debits & gas

seeing an increase in those on a level pay plan.

• Bill understanding has improved on the already high levels recorded in 2019,with

more customers now claiming to read at least some part of their bill.

• Ease of identifying if the bill is an actual reading or estimate has also increased, as has

the proportion of customers claiming to have submitted their own meter reading in

the past 12 months.

• Prepayment customers also appear to have a greater awareness of billing as there has

been a noticeable increase in awareness of statements being delivered at least 3 times

per year.

Priority and Special Services register

• Awareness of the Priority Services register among electricity customers has fallen back

on 2019 levels to 30% from 39%, which is in line with previous years.

6

• Awareness of the Special Services register is similar across electricity & gas

consumers, at 22% and 23% respectively (28% electricity & 22% gas awareness in

2019).

• Incidence of registering for Priority Services & Special Services register remains low -

mainly due to consumers not knowing it was possible to register.

Offers

• Ease of comparing offers has improved slightly on 2019 levels. Nevertheless, just over

half of all electricity & gas customers still find it difficult to compare offers.

• Usage of online comparison websites continues to increase YoY.

• 47% electricity easy to compare offers

• 46% gas easy to compare offers

Switching

• Switching levels remain similar to 2019 as 16% of electricity & 16% of gas customers

have switched in the past 12 months (with wanting to save money being the main

driver).

• As in 2019 typical behaviour by both electricity & gas customers is to automatically

continue with their supplier but there has been an increase in those looking around

to see if better offers are available.

• Across electricity & gas there has been an uplift in the proportion of customers

initiating the switch, predominantly through the use of supplier websites &

comparison sites (note there has been a decline in contact from suppliers).

• Among those who have switched the ease of switching has been gradually improving

since 2016 (easy to switch now stands at 97% electricity & 91% gas).

7

Smart Metering

• Interest in Smart Meters has increased on 2019 levels, as 7 in 10 electricity & 4 in 5

gas customers claim they would be interested in a Smart Meter (mainly for cost saving

purposes).

• Electricity customers willingness to share their energy information with suppliers to

avail of new offers and services and interest in a Time in Use tariff have also increased

on 2019 and now stands at 83% and 79% respectively.

Tariffs and Green Energy

• Interest in daily energy usage has also increased, as has the importance of renewable

energy & influence of green sourced products.

• Environmental benefits are cited as being an important reason for getting a smart

meter (26% electricity / 43% gas).

• Supplier offering gas at the same price but was more environmentally friendly was

given as a reason to switch by over 40%.

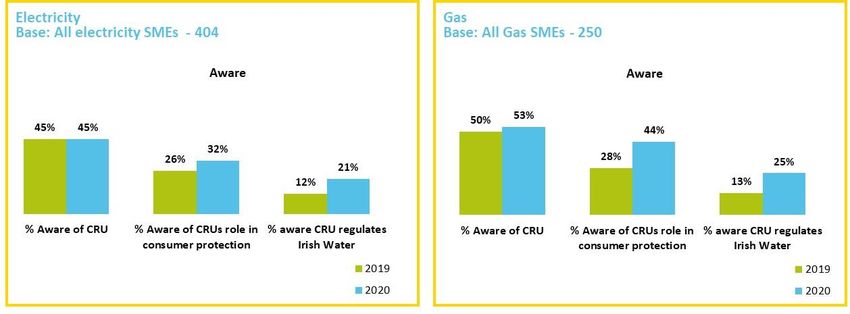

CRU Awareness

• Awareness of the CRU & its role in consumer protection has slipped slightly amongst

electricity customers but remained steady amongst gas customers.

o 25% of electricity aware of CRU.

o 32% of gas aware of CRU.

• Awareness of CRU regulation of Irish Water remains low (9% electricity / 7% gas).

Covid-19

• 12% of electricity & 15% of gas customers claim household ability to pay bills has been

impacted by Covid-19.

• A total of 2 in 5 of all energy users are concerned about increased energy usage and

impact on bills.

8The key findings from the SME research include:

Context setting: Market share

• Energia continues to increase its electricity market share (to 36%), while Electric

Ireland declines (31%). Note, market share is based on data provided from CRU

• Bord Gais & SSE Airtricity remain relatively stable in both markets, while Flogas’ share

of the gas market continues a gradual downward trend.

• Overall Satisfaction - Overall satisfaction for the electricity and gas markets remains

high at 82% and 85% respectively.

• While Electric Ireland scored the highest satisfaction level in electricity (85%), Bord

Gais is the only electricity supplier to show an increase (+4% to 84%) from 2019 levels.

• Flogas and Electric Ireland share the highest satisfaction level in gas (87%), Bord Gais

and Electric Ireland increased on 2019 levels.

Competition

• Spontaneous awareness of electricity & gas providers has decreased compared with

2019 scores.

• Understanding of offers has improved across electricity & gas, as has ease of

comparing offers:

o 56% of electricity SME (41% in 2019) claim it is easy to compare offers.

o 63% of gas SME (57% in 2019) claim it is easy to compare offers.

Covid-19

• Over 1 in 3 electricity & gas SMEs claim their organisations ability to pay energy bills

has been impacted by Covid-19.

• 1 in 4 electricity SMEs and 2 in 5 gas SMEs were aware of the Supply Suspension

Scheme and less than 1 in 10 SMEs claimed to have availed of the scheme.

Switching

• Switching of electricity & gas among SMEs has declined on 2019 levels:

o 17% of electricity SME (25% in 2019)

o 14% of gas SME (22% in 2019)

• The level of contact from competitors has continued to decline, as has the proportion

of SMEs who were approached with a tailored offer.

• Overall, the ease of switching remains high, with 9 in 10 ratings it as easy to switch.

9• The impact of switching remains high but there has been a decline in those claiming

that their bill was reduced by the amount expected.

Billing

• Bill understanding remains on par with the high levels recorded in 2019, for both

electricity and gas.

• Understanding of particular bill elements remains high, albeit a slight slippage across

both electricity & gas is evident.

• Understanding of PSO levy (electricity) and SPC (gas) continue to be the most unclear

elements of the bill.

Smart metering

• Interest in viewing daily usage is high:

o 83% of electricity SME

o 88% of gas SME

103. Research background

The fieldwork for each survey was conducted during May-June 2020 (initial interviewing 9-

27th March paused due to Covid-19 restrictions).

The research was undertaken by Behaviour and Attitudes in conjunction with The Research

Perspective.

This research pays particular focus to the:

• Measurement of the domestic retail electricity and gas market in 2020, with

comparable scope to previous research.

• Measurement of the business electricity and gas markets in 2020 with comparable

scope to previous research. The business element included both small and medium-

sized enterprises (SME), defined as those with 250 employees or fewer.

The methodology used for the domestic retail electricity and gas market measurements has

been kept as comparable as possible to provide comparisons with the trended data from

2013-2019. However, due to health restrictions imposed following the outbreak of Covid-19

in Ireland during March 2020, main survey data collection for the residential study was

conducted utilizing a combined CATI telephone and online approach using B&A's online panel,

Acumen.ie. In previous years all main survey residential interviewing was conducted via face

to face interviewing using CAPI machines, in the respondent's own home. As in previous years

there have been changes to question inclusion, order, sequence and format, which is likely to

have had an impact on comparability - where this has arisen, attention has been drawn to it

in the report.

As in 2019 part of the 2020 measurement included a shorter online study element (n=82

electricity and n=43 gas). The objective of this online element was to ensure a broader reach

of vulnerable customers in both the electricity and gas markets. Advertising placement

seeking participation in the online study was included on Instagram and Facebook sites, which

targeted interest groups related to the definition of vulnerable. B&A’s online survey panel

(acumenpanel.ie) was also utilised. In order to qualify for the online survey, respondents

needed to define themselves as having a disability.

The Computer Assisted Telephone Interviewing (CATI) methodology used for the business

research is directly comparable to the methodology used for the business electricity and gas

market measurement in 2019 and prior measurements. Respondents were decision makers

for electricity/gas supply related decisions within the organisation and included both private

11sector and public sector, government organisations and sole traders. Residential and SME

market share data was provided by CRU and a corrective weighting was applied to the data at

data analysis stage to ensure representivity.

Comparisons between the four measurements are presented with the following caveats:

• The two domestic markets are at somewhat different stages of development in terms

of the level of competition and the regulatory framework: prices in the domestic

electricity market have been deregulated for longer than prices in the domestic gas

market;

• The two SME markets are structurally different with electricity universally used by

SME’s, in comparison natural gas which is used by a minority of SME’s.

4. Market background

Price deregulation of the electricity and gas markets occurred between 2005 and 2014 which

allowed suppliers to enter and compete in the market. Since 2005, competition has continued

to develop in all aspects of the market.

The Single Electricity Market (SEM) is the wholesale electricity market for the island of Ireland

and it went live in 2007, with the goals of providing for the least cost source of electricity

generation to meet customer demand across the island of Ireland and maximising long-term

sustainability and reliability.

At present there are a total of 19 suppliers across the different segments of the gas and

electricity markets, serving the domestic and business communities.

5. Purpose of the research

The purpose of this research is:

• To determine the level, quality and benefits of competition in the domestic and

business electricity and natural gas markets as perceived by customers within these

markets;

• To determine the level of switching occurring, drivers or inhibitors impacting the level

of switching and other measures of engagement in the four markets, such as

consumer’s understanding of and ability to compare offers;

• To measure issues such as bill clarity, sales process, the complaints process and

protection of vulnerable customers;

• To assess other issues related to the transition from ex ante to ex post regulation as

they arise;

• To inform CRU generally about consumer behaviour and attitudes as they emerge

within the markets.

12• To examine the impact of Covid-19 on utility usage and consumers ability to pay utility

bills, as well as consumer awareness of various measures put in place to assist

consumers during the pandemic.

The research included the following specific areas:

1. General awareness of and satisfaction with competition and supply companies

providing services in each market;

2. Experience of switching within each market including switching rates, reasons for

switching or not switching and perceived understanding and ability to compare offers;

3. Level of engagement by customers with suppliers as demonstrated by investigation

of alternative tariff packages, changing to alternative tariff packages, changes in

payment methods and changes in billing frequency;

4. Assessment of the sales process and advertising from electricity and gas supply

businesses;

5. Knowledge of pricing, understanding of billing, and interest in and experience of

prepayment;

6. Payment arrears;

7. Understand of the role of supplier;

8. Interest in dual fuel offers (purchasing electricity and natural gas from a single

supplier);

9. Awareness and use of complaint handling procedures and experience of those

procedures;

10. Awareness of the availability of registration as vulnerable customers (defined by a

range of criteria including those who rely on electricity supply for the operation of

medical equipment in the home, the elderly and the disabled).

11. Impact of Covid-19 on utility usage, ability to pay utility bills and awareness of

measures in place to assist consumers during the pandemic.

This report is a summary of the findings of the research and is designed to cover the issues

assessed at a high level. The full research will be released by the CRU in a set of stand-alone

PowerPoint presentations, one covering the domestic electricity and gas markets and a

second report covering the business electricity and gas markets.

136. Data Collection Methodology

The data collection methodology followed best practise methods and processes executed

under internationally recognised quality standards (ESOMAR).

The methodology used for the domestic retail electricity and gas market measurements has

been kept as comparable as possible to provide comparisons with the trended data from

2013-2019. However, due to health restrictions imposed following the outbreak of Covid-19

in Ireland during March 2020, main survey data collection for the residential study was

conducted utilizing a combined CATI telephone and online approach using B&A's online panel,

Acumen.ie. In previous years all main survey residential interviewing was conducted via face

to face interviewing using CAPI machines, in the respondent's own home.

As in previous years, the SME surveys used a Computer Assisted Telephone Interviewing

(CATI) based methodology and were also conducted by Behaviour and Attitudes. Telephone

interviewing is particularly appropriate for business respondents because calls can be easily

scheduled for times when the respondent is available, and it is also flexible enough to allow

rescheduling at short notice at the respondent’s request.

The organisations contacted for interview for the electricity and gas business surveys were

selected at random from validated lists of businesses and public sector organisations with up

to 250 employees. The respondents of the SME electricity survey were distributed across the

Republic of Ireland, while the respondents of the SME gas survey were distributed across the

areas served by the national natural gas network. These populations of potential respondents

included the full range of business categories.

The number of responses achieved with each survey, as shown in figure 1 matched the

number of responses included in previous measurements. The sample sizes were selected to

ensure that the results are statistically robust and reliable.

14Figure A: Number of Respondents in the four market surveys

Sample Size Electricity Natural gas

Domestic 1,020 1,008

SME business 404 250

Research services have been provided annually to CRU by B&A and The Research Perspective since 2011,

with the exception of the 2017 measurement. Services were initially provided by The Research

Perspective and subsequently by a combined team within Behaviour and Attitudes and The Research

Perspective.

7. Representative Sample

As in previous years ensuring a representative sample was fundamental. For the domestic

electricity survey strict interlocking quota controls were placed on both the CATI telephone

and online samples, calculated on age and class targets within gender. Overall, demographic

quota controls were based upon the latest Census / Central Statistics Office population

estimates. For the domestic gas survey, a similar approach was used with respondents being

restricted to those living within areas served by the natural gas supply network and

demographic quotas set in line with previous surveys. At data analysis stage the CATI

telephone and online samples were merged together and a corrective weight was applied to

ensure full representivity of the sample. In the case of the business surveys, the population

from which respondents were randomly drawn was checked to ensure representation across

sub-sectors and other demographic dimensions, both during the survey and upon completion

of the survey.

Post-fieldwork, the respondent sets were validated to ensure a representative sample across

other market specific dimensions such as use of different electricity suppliers or payment

methods. This validated respondent data set was determined to be representative at a

household/business level and representative of the distribution of market share by supplier

in Quarter 4, 2019.

158. Market Satisfaction Profile

Satisfaction with the service provided by suppliers

Respondents were asked to rate their overall satisfaction with the service provided by their

electricity or gas supplier. The focus of this question on respondent’s overall satisfaction is

likely to include assessment across all facets of the supplier-customer relationship, such as

price, tariff, offer etc. In terms of the satisfaction metric, customers continue to express high

levels of satisfaction with their own supplier, albeit satisfaction has declined on 2019 levels. It

should be assumed that at least part of this decline is due to the change in methodology.

Overall satisfaction amongst the online vulnerable customer survey sample is at 72%, while

satisfaction amongst the vulnerable online survey gas sample is at 81%.

16Figure 1: Overall satisfaction with Domestic electricity (left) and gas (right) suppliers

Despite the overall decline on satisfaction levels versus 2019, a high level of customer

assessment is still enjoyed by all suppliers within the electricity and gas markets. Looking

specifically at the electricity market, Electric Ireland and Prepay Power customers now report

the highest level of satisfaction at 82%, albeit Electric Ireland’s customer satisfaction levels

have declined -9%pts since 2019. SSE Airtricity customers report the most significant drop in

satisfaction, dropping -13%pts, followed by Energia (-10%pts), but satisfaction remains high

at 79% and 73% respectively. Prepay Power is the only electricity provider experiencing an

increase in satisfaction this wave moving to 82% from 70% in 2019.

In the gas market, overall satisfaction has also declined vs 2019, falling from a satisfaction rate

of 89% to 82%, with all providers reporting a drop in satisfaction this wave. Energia has

experienced the most significant drop in satisfaction, falling -9%pts. SSE Airtricity now scores

the highest level of satisfaction at 85%, followed by Electric Ireland at 84%.

17Figure 2: Satisfaction amongst domestic customers with the service provided by current

supplier of electricity (left) and gas (right)

Among businesses, overall level of satisfaction with electricity suppliers remains high at 82%,

showing remarkable stability in satisfaction with electricity providers since 2016. With regards

to the SME gas market, overall satisfaction with gas suppliers also remains relatively

unchanged since 2016, at 85%.

18Figure 3: Satisfaction amongst SME business customers with the service provided by

current supplier of electricity (left) and gas (right).

Looking specifically at providers within the electricity SME market, satisfaction with service

has remained relatively stable across suppliers, with the exception of Bord Gais which has

seen an improvement. Looking at the gas SME market however satisfaction with Energia has

fallen back (albeit still high at 78%), while Electric Ireland satisfaction has improved +6%pts.

Satisfaction with Flogas is showing a gradually declining trend.

19Figure 4: Satisfaction amongst SME business customers with the service by current supplier

of gas (left) and electricity (right).

209. Bill Delivery, Clarity and Understanding

The bill is the primary communication to every customer from their electricity or gas supplier,

and as such it is an important channel for understanding energy consumption and associated

pricing.

Some 59% of electricity customers now pay their bills via direct debit, up from 53% in 2019

(higher among Energia and SSE Airtricity), while the incidence of those on level payment plan

and those who use a prepayment meter has remained steady. The increase in direct debits

has reduced the proportion who pay when they receive the bill, which is now at 1 in 5 (down

from 3 in 10).

Within the gas market the incidence of those who pay their bills via direct debit has remained

stable at 3 in 5 (higher among SSE Airtrcity and Energia). As with the electricity market there

has been a decrease in the proportion who pay when they receive the bill (-6%pts), as more

customers are now on a fixed payment plan (+6%pts). As in 2019, 15% use a prepayment credit

meter. Payment methods used by the vulnerable electricity sample are similar to the market,

while the vulnerable gas sample indicates a larger proportion of vulnerable gas customers are

on prepayment (23%).

21Figure 5: Payment methods used by domestic electricity (left) and gas (right) customers

An interesting finding from the surveys is that the incidence of customers receiving their

electricity and gas bills via email continues its upward momentum since 2012 (note answer

code change 2019) , but may be accelerated by the change in data collection methodology, -

Energia and SSE Airtricity customers continue to have the highest proportion receiving their

bill online and the 18-35 age group continue to have the highest percentage of email/online

billing recipients.

22Figure 6: Method of receiving bill among domestic electricity (left) and gas (right) customers

2310. Response to the bill

The vast majority of electricity and gas customers open their bill and read at least some part

of it, with the main focus being on the total bill amount, followed by bill payment date. Only

1 in 3 electricity customers and half of gas customers claim to look at the actual price, as

opposed to the total amount.

Figure 7: Typical Bill Behaviour in electricity (left) and gas (right) customers

Bill understanding has improved upon the already high levels recorded in 2019 across both

electricity and gas. Bill understanding is also high amongst the online sample. On the

electricity side, Energia & Electric Ireland customers claim highest level of agreement with

understanding how the total amount of the bill is calculated and how much energy they have

used, while gas customers with Electric Ireland and SSE Airtricity claim the highest level of

understanding. Those who receive their bill online vs via post report a higher level of

understanding of bill elements across both electricity and gas (the 2019 survey found that post

recipients had a higher understanding of the bill).

24Figure 8: Rating the bill in electricity (left) and gas (right) customers

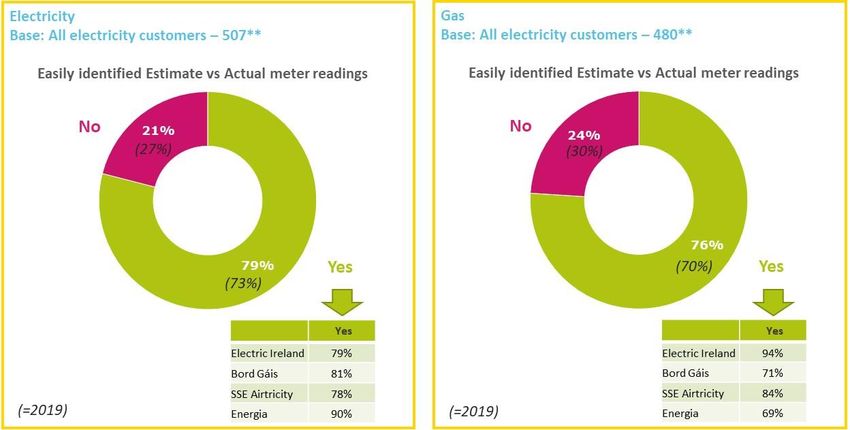

2511. Clarity of bill estimated or actual status

Consumers were asked if they could easily identify if a bill was based on estimated or an actual

reading. In both the electricity and gas markets the incidence of customers who can easily

identify if their bill is an actual reading or an estimate has increased on the already high levels

reported in 2019 and now stands at almost 4 in 5. Energia electricity customers and gas

customers of Electric Ireland seem to evaluate their bill more positively than customers of

other suppliers, in terms of this metric.

Figure 9: Incidence of submitting own meter reading in electricity (left) and gas (right) customers

When it comes to actually submitting their own meter reading, circa 50% of electricity and gas

customers have submitted their own meter reading in the past 12 months, an increase on

2019 levels. As in 2019 this is higher among Energia customers & SSE Airtricity across both

electricity and gas.

26Figure 10: Incidence of submitting own meter reading in electricity (left) and gas (right)

customers

12. Bill delivery and rating – SME electricity and gas markets

Businesses were also asked how frequently they receive their bills. Electricity SME’s continued

to be predominantly billed for their electricity usage on a bi monthly basis, while 2 in 5 are

billed monthly. There has however been an increase in the proportion of gas SMEs who are

now billed on a bi monthly basis, with bi monthly billing now accounting for half of all bill

frequency.

27Figure 11: Bill frequency mong electricity SMEs (left) and all gas (right) SMEs

Bill understanding overall remains on par with the high levels recorded in 2019, across both

electricity and gas. The proportion of gas SME’s who claim that the bill helps them to

understand the tariff they are on and to identify all of its components has continued to

improve. It should be noted that changes in the wording/coding associated with this question

are likely to have had an impact on the 2019 and 2020 scores, which are substantially higher

than the scores recorded in previous years.

28Figure 12: Bill understanding and impact in electricity (left) and gas (right) SMEs

13. Domestic arrears

The incidence of those claiming to always pay their bill on time and in full remains high across

both the electricity and gas markets, albeit there has been a slight decline amongst electricity

customers attributable to an increase in those reporting they are in arrears (albeit marginal).

Further research has shown that respondents tend to reflect a somewhat liberal

interpretation of what constitutes arrears and perhaps there is evidence of some reluctance

to disclose such sensitive information. Consequently, it is likely that the data under represents

the degree of arrears, as reported by the suppliers.

29Figure 13: Bill payment record and arrears by electricity (left) and gas (right) customers

Similarly, nearly all SME’s claim to pay their bill on time and in full. As with consumers there

may also be a ‘broad’ interpretation of what constitutes arrears and also some reluctance to

disclose such sensitive information.

30Figure 14: Bill payment record and arrears by electricity (left) and gas (right) SME business

customers

Awareness of the options available to customers in the event of bill payment issues was also

covered in this research. The survey found that the incidence of electricity and gas customers

who are aware of the potential to make a payment arrangement with their supplier in the

event of payment issue has increased over the past year and now stands at 49% and 48%

respectively. Awareness is higher among the online sample.

31Figure 15: Awareness of availability payment plan arrangements by electricity (left) and

gas (right) customers

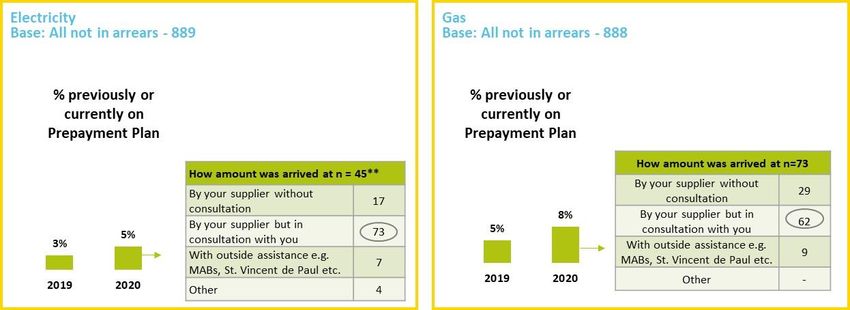

There has been a slight increase in the proportion of electricity & gas customers who claim to

have been previously/currently on a prepayment plan; rising from 3% to 5% in the electricity

market and 5% to 8% in the gas market (albeit not significant).

The most significant change to this measure is how the repayment amount is now defined,

with the majority of customers now claiming that the repayment amount was defined by the

supplier but in consultation with the customer. The 2019 research found that the repayment

amount was typically defined by the supplier without consultation across both electricity and

gas (note small base).

32Figure 16: Prevalence of prepayment plans among electricity (left) and gas (right)

consumers

14. Competition and consumer understanding of market

structures

Both original incumbents in the energy market remain strongly present in consumer minds,

but spontaneous awareness for these suppliers has continued a downward trajectory since

2017, with Bord Gais experiencing the biggest decline amongst electricity providers (-21%pts)

and Electric Ireland experiencing the biggest decline amongst gas providers (-17%pts) versus

the 2019 survey results.

33Figure 17: Awareness of electricity and gas competitors in amongst electricity (left) and gas

(right) consumers

Within the SME electricity market unprompted awareness of electricity providers has fallen

back to resemble 2017 levels, with market Electric Ireland continuing to achieve the highest

top of mind awareness, despite awareness declining -14% pts. Energia now achieves second

highest top of mind awareness at 50%. Bord Gais experienced the most significant decline

within the electricity market (-23%pts).

Looking at the SME gas market, Bord Gais Energy continues to receive highest unprompted

awareness of all gas suppliers at 77%, followed by Electric Ireland and Energia at 31% each.

Electric Ireland experienced the biggest decline (-13% pts).

34Figure 18: Awareness of electricity and gas competitors amongst electricity (left) and gas

(right) SME business customers

3515. Understanding and comparing offers

The level of consumer ability to understand market offers is an important dynamic in a

competitive market. Consumers were asked about the ease of comparing offers, to which 53%

of electricity customers claimed that they find it difficult to compare offers. Prepay Power and

Energia customers claim the highest level of ease. In order to understand the channels used

for comparison, the survey investigated the usage of price comparison websites to compare

offers, and results showed that 34% of all adults claimed to have used a price comparison

website to compare electricity offers – up significantly over the past number of years.

When we examine gas consumers, 54% of gas customers find comparing offers difficult. SSE

Airtricity customers claim the highest level of ease when comparing offers. In addition, a total

of 42% gas customers have used a comparison website to compare offers – indicating a rising

trend. Albeit, the rate of the increase has likely been impacted by the change in methodology.

Figure 19: Ability to compare and understand offers from electricity and gas suppliers in

electricity (left) and gas (right) customers

36Within the SME market, understanding of offers on the market has improved amongst

electricity and gas SMEs, with 2 in 5 electricity and almost half of gas SMEs claiming they have

a good understanding of offers. Ease of comparing offers has also improved, with circa 2 in 5

SME’s claiming it is easy to compare offers.

Figure 20: Ability to compare and understand offers from electricity and gas suppliers in

electricity (left) and gas (right) SMEs

16. Market Structure and Understanding

Market structures and differentiation of the roles of Suppliers and Networks companies is

typically a a challenge for electricity and gas customers. However, the 2020 results show that

awareness of ESB Networks and Gas Networks role in repairing power failures/gas leaks &

maintaining the grid has increased on 2019 levels. There is also increased clarity on who is

responsible for billing and payment. Respective roles related to meter reading and setting

energy prices continues to cause confusion however across both electricity and gas

customers.

37Figure 21: Customer understanding of the roles of energy supplier and Networks in

electricity (left) and gas (right) customers

Within the SME market, awareness of ESB Networks role in repairing power failures and

maintaining the grid remains steady, with 2 in 5 electricity customers believing CRU is

responsible for setting energy prices. Among gas customers Gas Networks role of repairing

gas leaks, maintaining the gas networks and meter reading also remains stable, while a total

of 1 in 4 gas SME’s believe CRU is responsible for setting energy prices.

38Figure 22: Understanding of the roles of energy supplier and Networks in electricity (left)

and gas (right) SMEs, 2019 vs 2020

17. Switching and Engagement

Levels of switching, the ease of doing so and the positive outcome of switching energy

providers is a key focus of this research. This research follows the same structure as in

previous studies across the four markets. The research includes an assessment of the level of

switching, experience of switching and reasons for the decision to switch, or not to switch.

The research also includes an assessment of the sales process and sales techniques used by

electricity and gas suppliers in the domestic market.

Domestic and SME electricity and gas markets

As in 2019 typical behaviour by both electricity and gas customers is to automatically continue

on with their supplier when the initial 12 month contract has expired, however there has been

an increase in the proportion of both electricity and gas customers who now look around to

see if there are better offers available.

39Figure 23: How consumers typically react when initial 12 month contract expires amongst

electricity (left) and gas (right) consumers.

Among SMEs the typical behaviour is similar to electricity and gas residential customers. There

has however been an increase in the proportion of electricity SMEs who automatically

continue with the supplier knowing the default tariff will be charged. The proportion of gas

SMEs who continue with the supplier irrespective of the tariff has also increased vs 2019.

40Figure 24: How SMEs typically react when initial 12-month contract expires

When it comes to switching energy supplier, over half of electricity and gas consumers have

switched supplier at least once in the past (56% electricity and 57% gas). Among those who

have switched, consumers report similar levels of switching within the last 12 months across

both gas and electricity. Among the online gas and electricity samples, the incidence of last 12

months switching is in line with the population, thus there is no evidence to suggest that

switching is an issue for more vulnerable customers. Electricity switching peaks among the

36-45 age group, while gas switchers rates are higher amongst those aged 46+. Little variation

across social class or region.

41Figure 25: Switching past - 12 months in electricity (left) and gas (right) customers Within the SME market 67% of electricity SMEs and 52% of gas SMEs have switched energy provider at least once in the past. The incidence of those SME’s who have switched electricity supplier within the last 12 months has declined on 2019 levels however. The reported rate of gas switching within the past 12 months has also declined on previous levels. SMEs with

Figure 26: Switching past - 12 months in electricity (left) and gas (right) SMES

Among residential customers who switched in the previous 12 months, 20% of electricity

customers and 15% of gas customers believe that there were no conditions associated with

their switch.

43Figure 27: Understanding of offer – among electricity (left) and gas (right) switchers

(customers)

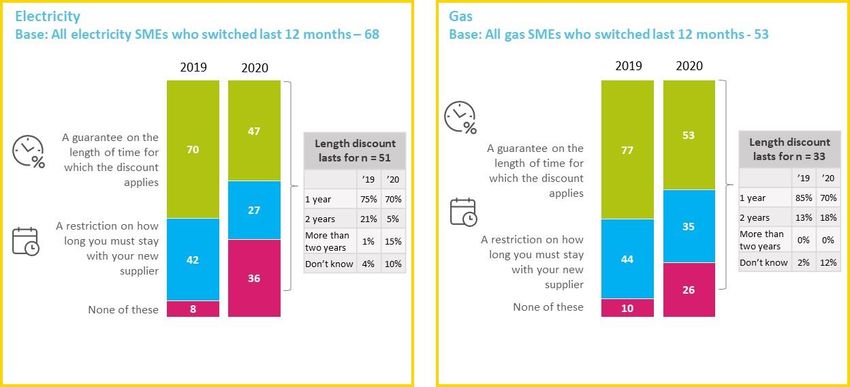

The proportion of SME customers who believe there is a guarantee on the term of the discount

they received has declined on 2019 levels and now stands at 47% for the SME’s who switched

electricity supplier and 53% for those who switched gas supplier.

44Figure 28: Understanding of offer – among electricity (left) and gas (right) switchers (SME)

Amongst consumers it is clamed that s website with a calculator & price comparison websites

would have the biggest impact on consumers likelihood to switch. The claimed impact of these

tools on consumer switching levels has increased significantly on 2019 levels. These high

percentages demonstrate consumers limited awareness of current offer comparison

websites.

45Figure 29: Impact of information sources on switching likelihood in electricity (left) and gas

(right) customers

18. Drivers for switching amongst electricity and gas markets

Respondents were asked to give their reasons for switching electricity and gas supplier in

order to understand the factors influencing switching in the market. Motivation to save money

was the main reason given by both electricity and gas customers as the reason for switching

within the last 12 months.

46Figure 30: Reasons for switching during last 12 months amongst electricity (left) and gas

(right) customer switchers

Amongst SMEs the quest for a reduction in cost was also the main motivation behind changing

supplier for both electricity and gas switchers, with previous supplier announcing a price hike

being referenced by almost half of all electricity SME switchers. To receive a reduction in the

total cost of electricity was also a main motivator for electricity SME last 12 month switchers.

47Figure 31: Reasons for switching during last 12 months amongst electricity (left) and gas

(right) SME switchers

19. Drivers for not switching

Domestic electricity and gas consumers who had not switched in the previous 12 months were

asked why they had not switched their energy supplier. Amongst these customers the options

selected most frequently were ‘not saving sufficient amount of money by switching’ and ‘I like

the service that I receive from my current supplier’ pointing to these as the two main reasons

given for not switching gas or electricity provider in the last 12 months.

48Figure 32: Reasons for not switching during last 12 months among electricity (left) and gas

(right) customers

Similarly, among SME non switchers, ‘satisfaction with current provider’ was the main reason

given for not switching, among both electricity and gas SMEs.

49Figure 33: Reasons for not switching during last 12 months among electricity (left) and gas

(right) SMEs

20. Overall experience of the switching process

Across electricity and gas switching there has been an uplift in the proportion of customers

initiating the switch, predominantly through the use of supplier websites and price

comparison sites. Electricity has also seen an increase in the proportion of switches conducted

via phone where the customers initiated the contact.

50Figure 34: Contact method used to switch by electricity (left) and gas (right) customer

switchers

With regards to the actual process of switching energy providers, a positive experience of the

switching process is reported by both electricity and gas switchers and has been gradually

improving since 2016, especially in relation to electricity customers. The majority of online

sample respondents who has switched in the last 12 months claim it was easy to do so (note

extremely small base).

51Figure 35: Experience of switching process by electricity (left) and gas (right) customer

switchers

Positive impact of the switching process is also evident across both electricity and gas SME

switchers, however there has been a decline in those claiming that their business bill has

reduced by the amount they expected. Some slippage in respondents level of understanding

of the terms and conditions is also evident across both electricity and gas respondents, but

remains high.

52Figure 36: Experience of switching process by electricity (left) and gas (right) SME switchers

Residential electricity customers were also asked what factors would encourage them to

switch energy provider. Greater discounts for chosen payment methods was identified as the

factor that would have the biggest impact on both electricity and gas consumer switching. It

is interesting to note that time of use tariffs is increasing in terms of its potential impact in

considering changing electricity supplier.

53Figure 37: Influencing switching in electricity (left) and gas (right) customers

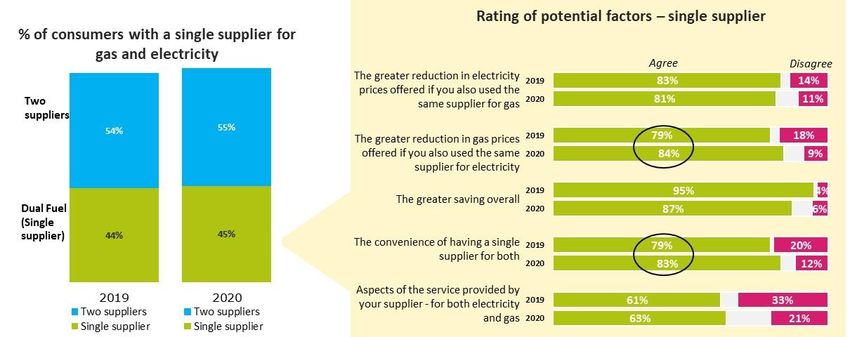

21. Dual Fuel

The use of a single supplier to provide both gas and electricity to their home or business is an

option that is available to customers and businesses based in areas catered for by the Natural

gas pipeline. Dual fuel offers from suppliers typically include additional discounts and offers

in order to incentive customers to have their gas and electricity with one supplier. SME

customers were asked about the uptake of Dual fuel contacts. Among SME’s, a total of 2% of

all electricity SME’s use natural gas in their business (7% in 2019), and 45% of these claim to

be on dual fuel contracts. Among all electricity SME’s with gas and all gas SMEs, 45% indicate

they are dual fuel customers (44% in 2019).

54You can also read