Ganesh Polytex Limited Dark Horse Dhamaka - Stock pick for July 2010

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Ganesh Polytex Limited Dark Horse Dhamaka – Stock pick for July 2010

Best Buying Price

Consortium advocates a two-phase buying strategy:

1st Phase : Buy at the recommended price range Rs 47.5-52.5 [60% of investment]

2nd Phase : Add if the price falls down to Rs 40-44 [40% of investment]

Recommended average buy price – Rs. 46.8

Expect at least 8-10 times returns in the next 3 years time frame!!

2

Table of Contents

The Theme – Page# 4

Overview – Ganesh Polytex Limited – Page# 7

Ganesh Polytex – Waste Recycler – Page# 11

Ganesh Polytex – Products & Applications – Page# 16

Ganesh Polytex – Expansion Plans – Page# 23

Forward Revenue estimate & Financial Statements – Page# 27

The Management – Page# 32

Shareholding Pattern – Page# 34

Buying Strategy - Page# 36

Investment Rationale - Page# 38

Challenges/Risks Involved – Page# 40

3

The Theme

4

From the research desk of Consortium Securities

Non Bio-Degradable waste, especially the PET bottles pose serious threats to our

environment. Considering the humongous growth in consumption, there successful

recycling is extremely important. The use of Plastic products has been a major cause of

concern since long. We have seen people, organizations clamoring about reducing the

usage of Plastic products.

These days as we move across streets, parks, etc, we see many PET bottles littered around

giving not just a bad look but also posing serious threats to our environment.

PET is one of the fastest growing segments in plastics providing a hygienic, durable and

user friendly packaging solution for all kind of bottled drinks, beverages, liquor,

pharmaceuticals, chemicals, and other liquid products.

As the consumption of PET is growing, so as the quantum of its waste is increasing at rapid

pace. PET bottle waste being Non-Biodegradable, its recycling is inevitable else piling of it

will be the biggest threat to the environment.

5

From the research desk of Consortium Securities

We see a huge opportunity in the huge challenge that the nation and the world faces and we

are happy to announce Ganesh Polytex Ltd as the Dark horse Dhamaka pick for the month of

July 2010 , which directly plays a role in solving the problem of managing huge quantum of PET

bottles waste.

Ganesh Polytex Ltd is a waste management company & is one of The largest PET Waste

Recycler in India.

Company Business model is interesting as it transforms post-consumer pet bottle waste (which

is otherwise hazardous for environment being non bio-degradable in nature) back again into

environmental friendly, hygienic, and comfortable fibers which are more economical in

comparison to virgin fibers.

The company has charted out aggressive capex plans for the next three years. We expect the

company’s impressive business module coupled with aggressive expansion plans to translate

into healthy growth with increased profitability in the near future.

Harveer S. Kalra

Consortium Securities Pvt Ltd

6

Overview – Ganesh Polytex Ltd

7

The Company

Ganesh Polytex Ltd (GPL). was incorporated as a Public Limited company in the year 1988. At

Present Company is the largest PET waste recycling company with prominent presence in recycled

Polyester Staple Fiber (RPSF) and largest to recycle PET bottle waste in the country, with forward

integration to manufacture RPFY.

The company is having two production units:

o One at Raipur, Rania, Kanpur Dehat (U.P) which is on the main highway- Kanpur Jhansi Road.

o Second unit, where the company has done major expansions, is located at Rudrapur

(Uttarakhand). This unit is entitled for exemption from Central Excise and Income Tax for a

period of 10 years.

The company went into diversification in the year 1994 to produce Regenerated Polyester Staple

Fiber in India. This was the first venture of its type in India to produce PSF from polyester waste &

bottle flakes.

In the year 2006, the second unit at Rudrapur (Uttarakhand) was set up with a production capacity

of 6000 MT per annum which was subsequently increased by installing three more lines. The total

aggregate capacity of the Kanpur & Rudrapur plant is 4800 MT per month or 57600 MT per

annum.

8

Milestones Achieved

Year Achievements

1987-88 Incorporation and commencement of business

1989 Creation of Dyeing and Doubling facilities for 360 TPA

1991 First public issue of 2.10 lakh shares and Capacity expansion

Dyeing 1080 MT

1992-93 Creation of Texturising capacity – 216 spindles

1993-94 Rights issue of 34.50 lakh shares

1994-95 Expansion of Dyeing capacity to 1150 TPA.

1996-07 Expansion of Dyeing capacity to 1800 TPA and recycled PSF to

10800 TPA. Equity Capital expanded to Rs.9.37 crore

2007-08 Set up Rudrapur Unit for recycled PSF with an capacity of 21600 TPA and Expanded

dyeing capacity to 2400 TPA.

2008-09 Expanded Capacity of Kanpur Unit for RPSF to 18000 TPA.

Equity Capital expanded to Rs.9.87 Crores

9Ganesh Polytex Limited (As on July 21st 2010)

CMP = Rs 52.00 (Jul 21st 2010) – The stock is in PE = 6.15

Incepted GoingEdServ

in 2001, forward, the revenue

is World's is expected to

first 4th generation

the consolidation phase facing stiff resistance at education

increase companydue

multi-fold thatto

uses

thetechnology to efficiently

major capacity expansion.

Rs 52.5 At synchronize

present themanpower

companydemandcommands and supply

very lowin number

multiple on

and skills

account of right

low from development

visibility. However, to deployment.

it should be able to

52 week’s high/low = Rs 56.5/8.05 –The stock

EdServ's business is web enabled

command a very high multiple once and is run through a

the investors

recently made a new 52 week high. As it is in the secured partner-driven center network in Integrated

strong bullish phase it can continue to make new understand the business model.

Learning Model through its EdCenter brand.

highs.

Peak share price = Rs 56.5 (19th July ‘2010) –

When the stock reaches its life time high it goes

EdServ’s is India’s

Shareholdings only

: No Ofcompany to Share

shares [% have seamlessly

Holding ]

integrated education and placement

Total Foreign: 0.3lakhs [0.3%] end-to-end in

into a strong bullish phase in the absence of any partner based web network.

resistance. At CMP Ganesh Polytex is very close Total Institutions: 0.1 lakh [0.1%]

to its life time peak of 56.5. Total Non Promoter Corporate Holding 25.1lacs

EdServ focuses on the bottom of the pyramid, the Real

[20.3%]

Trading volume = Min 1.37 lacs shares (approx) India, the hugely

Total recession-proof

Promoters market

0.586 crore having the

[47.6%]

per day –These are early days for a company continuous

Total need

Publicof&affordable education

others 39.2lacs and a career

[31.8%]

which is soon going to create a huge impact in growth pathOutstanding

Total and guidance. The company

Shares also[100

1.23crore rolled

%]out

the Waste Recycling sector. The stock is liquid EdCampus, Ed-Cademy, and EdCenters with EdClass

This shall help investors to get in and out of stock during the year that offer learning, jobs, metrics, and

Debt/Equity = 2 [Mar’10]

easily. live lectures, online in-campus.

ROCE = 14.2% [Mar’10]

EPS = Rs 8.45 – The company is expected to end ROE = 17.6% [Mar’10]

the FY 11 with a net profit of Rs 13 crore on the EdServ hasRatio

Current launched

= 1.0in[Mar’10]

the year 2009, World's first 4th

equity base of Rs 13 crore, culminating into an Generation

Deliverededucation

Volume per model

daythat has a definite

= Approx 58% job

EPS of Rs 10 fitment for every aspirant who wishes to seek a career

BSE Code 514167

as a fresher.

10Ganesh Polytex – Waste Recycler

11PET Waste Recycling company

Ganesh Polytex Ltd is the largest PET waste recycling

company with prominent presence in recycled Polyester

Staple Fiber (RPSF) and largest to recycle PET bottle waste

in the country, with forward integration to manufacture

RPFY.

Ganesh Polytex is market leader in this segment of

manufacturing of Recycled polyester staple fiber (RPSF) &

has been in the field of Recycled PSF for over 15 years.

Besides procuring the Waste from vendors, the company

has set up its own procurement centers in different cities to

insulate itself from raw material shortage as well as price

fluctuations.

Finished product finds application for spinning of yarn,

stuffing in toys and other life style products like pillows,

quilts, mattresses and furniture, non-woven carpets and

fabrics, medical & packaging textile, geo textile, fur fabrics,

construction and paper industry and other technical textile.

12Raw Material

The major raw material required for Recycled PSF is post- consumer PET bottle waste.

PET is one of the fastest growing segments in plastics providing a hygienic, durable and user

friendly packaging solution for all kind of bottled drinks, beverages, pharmaceuticals, liquor,

chemicals, and other liquid products.

As the consumption of PET is growing, so as the quantum of its waste is increasing.

PET bottle waste is non bio-degradable in nature (takes thousands of years in decomposing) and

hence, poses a serious threat to soil, water sources and forests and thus harmful for human being

and other living creatures. Therefore, its recycling is inevitable else piling of it will be the biggest

threat to the environment.

13Increase in consumption of PET bottles

Region PET Resin Capacity Demand

Global 17.5 million tonnes 14.0 million tonnes

India 0.80 million tonnes 0.40 million tones and the rest is being exported due

to price advantage

With life style changes and higher disposable income, demand of PET bottles is set to grow at

much faster pace as the per capita PET consumption in India is 0.22 kg. as compared to the world

average of 2.1 kg. in 2008.

As per industry estimates, about 65% of PET bottles consumption is available for recycling. That

means, indigenous availability of PET bottle waste would be 3.0 lakh tone during 2010, which is

much more than the overall requirement of entire domestic recycling capacity (aggregate installed

capacity of about 1.75 lakh ton per annum during 2010) in the country.

The consumption of PET bottles is expected to grow to 0.60 million tonne by 2012, availability of

waste will also increase correspondingly.

The present installed capacity of Recycled PSF in India is about 1.63 lakh tonne, Ganesh Polytex

Ltd has a capacity of 57600 MT per annum & is at the first position in the sector.

14Collection of Raw Material

Availability of Raw material is almost free of cost, but the critical issue is collection of waste and

transportation / processing cost.

Ganesh Polytex Ltd. is in this line of business since last 15 years and has a well-streamlined

network of its collection centers (operating on franchisee module) of PET waste spread all over the

Country at strategic locations.

It has also developed a network of traders over the periods who exclusively supply the material to

the Company.

Further there is huge possibility of imports of PET bottle waste from foreign countries and this

avenue is still to be tapped by the Company as imported bottles are little bit costly due to

transportation factor. In case of need, the company may plan to set up a raw material processing

/washing unit in near future at Europe or USA, where abundant quantity of raw material is

available.

Company also uses other types of polyester waste viz. Waste undrawn fiber, POY/ PFY waste,

polyester film waste etc., which is also available in small quantities.

15Ganesh Polytex – Products and Applications

16Products & Applications

Ganesh Polytex Products Category

Recycled Polyester Staple Fibre (RPSF) Dyed Texturised / Twisted Filament Yarn

Raw Material Used

Post Consumer PET bottle Waste and POY/FDY and Grey Texturised Yarn

other kind of industrial Waste of Polyester

Application/ End use

Textile Sector : Spun Yarn; Hosiery Yarn etc. Fabrics, Saree, Dress Material,

Industrial Sector – Filter Fabrics; Geo textile; Upholstery and furnishing fabrics,

Non-woven carpets and Fabrics; Medical and Sewing Threads, Cords etc.

packaging textile etc.

17Recycled Polyester Staple Fibre (RPSF)

Ganesh Polytex (GPL) product includes low-end basic segment to mid and high-end premium

segment.

Recycled PSF replaces 100% virgin PSF in textile sector due to its most distinctive advantage of

cost-effectiveness and it replaces Foam, Cotton, P.P. fiber etc. in other industrial sectors due to

its durability, comforts and hygienic characteristics besides cost-effectiveness.

Polyester has now become common man’s fabrics in terms of prices, durability and comforts in

comparison to cotton and other fibres.

With growth in the economy and growing middle class, the per capita consumption of polyester

fabric is also set to increase both for clothing and non-clothing applications. In fact, with growing

per capita income consumption of non-clothing fabric will grow at much faster rate than clothing

fabric.

As Recycled Polyester Fibre is suitable both for clothing and non-clothing applications, its

demand is improving both in textile and industrial sector. This bodes well for GPL as it has strong

presence in both the sectors

18Market demand & Industry Scenario

Major User Industry Of Recycled PSF

Non-woven/technical

Yarn spinning Stuffing

textile

19Non-woven/Technical Textile

Textile for non-clothing applications is classified in non-woven and technical textiles, which are

growing roughly at twice rate of textiles for clothing applications and now account for major chunk

in total textile production.

The large Indian population of over one billion with nearly 48% in the age group of 18-35 and 250

million strong middle class which has high purchasing power and living standards presents a

potential huge market for non-woven products & with the Indian economy poised for a rapid

growth of more than 8% during the next five years, non-woven production and consumption is

expected to see rapid growth.

Areas of non-woven applications like infrastructure, automotive textiles, carpets, interlinings and

wading, furnishings and beddings, agricultural textiles, medical textiles, sports textiles etc are

already seeing a lot of activity and are bound to grow at rapid rate in order to catch up with the

developed world.

The market size of technical/non-woven textile in India grew from Rs.31,000 crore during 2003-04

to Rs.44,000 Crore during 2007-08. Further, as per an internal document prepared by the textile

ministry, it is estimated that the technical textile market would grow to Rs.78,060 Cr. by 2014–15

with an annual growth rate of 14%.

20Yarn Spinning

Recycled PSF is used in yarn spinning in replacement of virgin grade PSF, which is about 15%

costlier that recycled PSF.

Recycled PSF can be used 100% in coarse counts of yarn (up to 30 count – which account for

almost 40% of the total yarn consumption in India), and for fine counts (above 30, which are

mostly used in apparels & wearing cloths), it is blended with virgin grade PSF.

Due to cost & sale price equation as well as growing demand for non-apparels fabric, use of virgin

grade PSF is being replaced by Recycled PSF.

This has opened up a large window for Recycled PSF in spinning sector because present domestic

market size of coarse denier spun yarn is about 4.00 lakh tonne per annum.

21Stuffing

With improvement in life style and urbanization coupled

with increasing disposable income, use of home furnishing

products like quilts, comforters, mattresses, pillows,

furniture etc. is increasing and growth in their market size is

in double digit.

Traditionally these products were stuffed with cotton,

foam, coir etc. with increasing prices and decreasing

availability, cotton is almost out for such uses.

Recycled PSF is now being preferred over other traditional

products like foam and coir because of its inherent qualities

like hygiene, wash-ability, light-weight and user friendly

characteristics.

Likewise there is phenomenal growth in market of soft toys,

where there is no substitute of Recycled PSF in stuffing.

Estimated market size of all these products in India is over

Rs.15,000 crore.

22Ganesh Polytex – Expansion plans

23Ganesh – Leading all the way

Rank Company In this Sector (RPSF) Place Present Capacity

MTPA

1. Ganesh Polytex Ltd Kanpur & 57600

Rudrapur

2. Reliance Industries Ltd Hazira 42000

3. Shiva Tex Fab (P) Ltd Ludhiana 18000

4. Rishiraj Filaments Ltd - 12000

5. Allainz Fibres Gujrat 6000

6. Arora Fibres Ltd Silvassa 6000

7. Himalaya Fibres Baddi (H.P) 6000

8. K.K.Fibres Baddi (H.P) 6000

9. Capital Fibres (P) Ltd - 600

10. Nirmal Fibres Gajraula (U.P) 3600

TOTAL 1,63,200 MTPA

24Economies of Scale

Ganesh Polytex Ltd. has the largest capacity in the industry, which has enabled the company to

optimize per unit cost of production and ward off the competition due to economics of scale.

Since the product is replacement of downstream virgin PET product market, it has ever increasing

demand from both - the replacement market and growing uses from consumer market.

PET recycling has drawn the attention of many big business houses including Reliance Industry.

Company would not be affected by the presence of large players like Reliance because of enough

wide market and multiple uses.

Rather their presence is beneficial for the development of down stream consumption of recycled

PET and products .

Ganesh Polytex Ltd is having the largest product range in the industry on the one hand and source

of raw material (PET bottle waste) is open market which can’t be influenced.

25Expansion Plans

GANESH POLYTEX LTD is encouraged to expand its production to match with the demand and

diversify into forward integration for value added products. Company has a ambitious growth

plans which includes enhancing the recycling capacity to over 100,000 TPA in stages over the next

2 years.

Aggressive Capex Plans Over The Next Three Years.

Ganesh Polytex has charted out expansion plan with a capital outlay of Rs.850millions over

the next three years. The company shall invest Rs.250millions for ramping up of Recycled PSF

capacities by 14,400 MT/pa. The project shall be operational in FY11.

The company has expanded additional capacity of Recycled Polyester Staple Fiber (RPSF) by

18,000 TPA at Rudapur with an estimated cost of Rs.250mn.

The company has also firmed up plans to set up a facility for manufacturing Recycled Partially

Oriented Yarn (POY) as a part of forward integration for value added product. The plant will

have a capacity of 18000MT/pa and shall entail an investment of Rs.350 millions. The new

facility shall be operational in FY12.

26Forward Revenue Estimates & Financial Statements

27Revenue Forecast

FINANCIAL MATRIX 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

Actual Projections

Net Sales (Cr) 51.94 62.67 105.42 135.37 190 234 400

Other Income (Cr) 0.2 0.33 0.38 0.08 0 0 0

EBDITA (Cr) 5.77 7.01 12.35 17.1 26 35 75

EBDITA Margin (%) 11.1 11.18 11.71 12.63 14 15 17

CAGR Growth (%) 28.25% 35%

Depreciation (Cr) 1.4 1.81 3.6 5.66 7 10 17

PAT (Cr) 1.46 1.89 3.75 4.35 9 13 30

PAT margin(%) 2.81 3.01 3.55 3.21 4.50 5.50 6.25

Cash Generation (Cr) 2.86 3.7 7.35 10.01 16 23 47

Equity Share Capital (Cr) 9.37 9.37 9.86 9.86 12.32 13.38 19

Net worth (Cr) 14.2 15.99 20.2 23.98 31 48 108

Total Borrowing (Cr) 14.19 27.91 46.6 61.35 82 68 82

Gross Block (Cr) 32.45 47.29 66.97 85.83 111 116 175

Debt Equity Ratio 0.36 0.78 1.11 1.29 1.37 0.66 0.51

EPS (Rs) 1.57 2.03 3.62 4.35 8.01 8.78 15

Book Value (Rs) 15.16 17.07 20.5 24.33 31.7 35.86 54

RONW(%) 9.92 11.5 16.33 16.26 25.29 24.46 27.36

28Income Statement (Last 5 Years)

The Company’s sales and net

profits have grown at healthy

compounded annual growth rate

(CAGR) of 28% and 30%

respectively in the past four

years.

The Revenue and Profitability

grew exponentially from Rs 52

crore to Rs 199 crore and Rs 1.47

crore to Rs 9 crore respectively.

Its EBIDTA improved to Rs. 24.30

crore in FY09-10 from Rs. 4.77

crore in FY06 on the back of

improved product mix.

Growth plans are likely to propel

CAGR of 35-40% in its top and

bottom lines during next five

years.

29Quarterly Results

The company has been

recording a sequential

growth in revenue and net

profit for the last 4

quarters.

The company has been

able to scale up it’s NPM by

almost 90% from 3% to

5.70%.

In the last 4 quarters itself,

the company has recorded

a growth of 142% in it’s net

profit from Rs 1.28 crore to

Rs 3.11 crore.

GPL has recently upgraded

it’s facility by 18,000 TPA.

The revenue from the new

facility shall start coming in

from Q1 of FY 11.

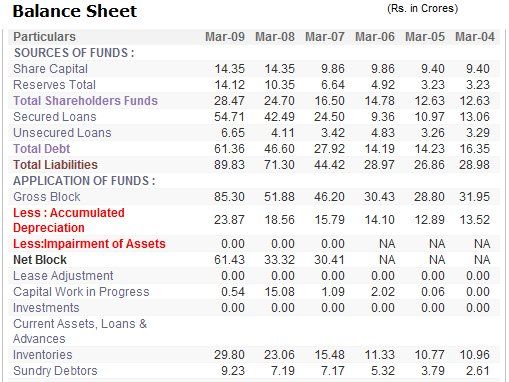

30Balance Sheet

For the last 5 years the Gross Block of the company has witnessed continuous expansion from Rs 28 crore to Rs

85 crore. The company has been expanding its capacity on a consistent basis enabling the company report

higher sales and profitability.

As per the projected estimates, the company intends to bring down its Debt/Equity ratio to almost 0.5 in the

next two years, while it will still continue with capacity expansion through internal accruals and limited equity

dilution.

31Management

32Men at the Helm

Mr. Shyam S. Sharma – Chairman & MD – A textile engineer.

Served the Birla group for 25 years in various senior positions and

promoted the said company in the year 1987. He is well versed with

the fiber and textile technology with an experience of more than 45

years.

Mr. V. D. Khandelwal – Executive Vice President – A Post

Graduate in Commerce and having experience of more than 36 years

in trading of different types of textile yarns. He is one of the Promoter

Director and looks after the affairs of the company since inception.

Mr. Sharad Sharma – Joint Managing Director – A Commerce

graduate with more than 17 years in marketing of yarns and fiber. He

is engaged with the company since 1992.

Mr. Rajesh Sharma – Executive Director – A Commerce

Graduate with rich experience spanning over 20 years in plant

administration. Looks after the administration of the company’s

Rudrapur unit.

33Shareholding Pattern

34Shareholding – Promoters & Non Promoters

At the end of Mar’ 10 the Promoter holding stands at 47.55%, which is reasonable and the increase in

stake further reflects the confidence of the management in the prospects of the company.

The Promoter’s have been increasing their stake consistently for the last 5 quarters.

The total Paid-up Equity Share Capital of the Company has been enhanced from Rs. 9,85,50,000/- to Rs.

12,32,00,000/-because of allotment of 24.65 Lakhs Equity Shares to the Promoters and Others,

consequent upon the exercise of conversion option of warrants

35Buying Strategy

36Best Price to Buy

In the last 11 months, the stock has already appreciated by around 400%, while for last 4 months it’s

been consolidating.

As evident from the chart the stock’s been witnessing higher lows, however it’s been facing a strong

resistance at around Rs 52.5. We expect the stock to consolidate for some more time and would

therefore suggest a buying price range of Rs 47.5 to Rs 52.5

37Investment Rationale

38Investment Rationale

The company is the leader in its area of operations and recently surpassed the annual production

capacity of Reliance Industries Ltd.

The investors lack the understanding of the Business Model of the company. Once the investors

realize the true potential and the main area of operation i.e. Waste Recycling, the stock will

command very high multiples.

The company is contemplating a change in the name of the company to reflect the true

operations. A change in name will lead to better visibility and a change in perception, which will

result in Re-rating.

The company has chalked out an aggressive expansion for the next two years, which will not only

increase the profitability and sales but also result in margin expansion.

Based on the Projected income and sales, the company is available at low valuations thereby

ensuring safety of margin.

39Challenges / Risks involved

40Challenges / Risks involved

Following are some of the key risks that could derail our estimates and expectations –

A change in the manufacturing technology of PET bottles may affect the company’s ability to

recycle the waste

Availability of Raw material is almost free of cost, but the critical issue is collection of waste and

transportation / processing cost.

The increasing number of players are now making a shift from conventional yarn manufacturing

techniques to Re-cycling PET bottles for manufacturing yarn. This may hurt company’s waste

collection dominance and it’s ability to procure raw material at cheaper rates.

41Powered by the JV between: Consortium Securities & HBJ Capital

About Consortium Securities & HBJ Capital

Consortium Securities HBJ Capital

Consortium Securities is a decade old financial HBJ Capital Services Pvt Ltd is a NextGen

services firm with a vision to simplify the complex Financial services provider with equity research

world of the financial markets. The company as its core competence. HBJ Capital was

provides a wide range of services nationwide to a founded in 2005 by a group of 6 consisting of Ex-

substantial and diversified client base that Infoscions, IIM and IIT graduates. While they

includes retail clients, HNI’s, corporates and were all from different academic backgrounds

financial institutions. Consortium’s services and industries, they were having something in

include: Portfolio Management, Broking & common - passion towards Equity markets and

Advisory- Equity, Commodity and Foreign Investment research. Today, HBJ Capital with its

Exchange and Corporate Financial Services. The business headquartered at Bangalore, operates

company has outlets in over 100 cities across 14 end to end research services in public and

states. Well regarded for its leadership and path private equity with more than 70 associates. HBJ

breaking approach to investing, Consortium was Capital provides services across 3 broad

recognized as one of the leading brokers in India domains - Independent Equity Research (Retail),

in 2007 and 2008. Corporate consulting and Institutional Services.

43Disclaimer

The information and opinions in this report have been prepared by Consortium Securities Pvt Ltd (Consortium Securities) and are subject to change

without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be

altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior

written consent of Consortium Securities. While we would endeavour to update the information herein on reasonable basis, Consortium Securities, its

subsidiaries and associated companies, their directors and employees (“Consortium Securities and affiliates”) are under no obligation to update or

keep the information current. Also, there may be regulatory, compliance, or other reasons that may prevent Consortium Securities from doing so.

Nonrated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable

regulations and/or Consortium Securities policies, in circumstances where Consortium Securities is acting in an advisory capacity to this company, or

in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made

nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and may not be used or

considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to

all the customers simultaneously, not all customers may receive this report at the same time. Consortium Securities will not treat recipients as

customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that

any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report

may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and

needs of specific recipient. This may not be taken in substitution for the exercise of independent judgement by any recipient. The recipient should

independently evaluate the investment risks. The value and return of investment may vary because of changes in interest rates, foreign exchange

rates or any other reason. Consortium Securities and affiliates accept no liabilities for any loss or damage of any kind arising out of the use of this

report. Past performance is not necessarily a guide to future performance. Actual results may differ materially from those set forth in projections.

Forward-looking statements are not predictions and may be subject to change without notice.

Consortium Securities and affiliates, including the analysts who have issued this report, may, on the date of this report and from time to time, have

long or short positions in, and buy or sell the securities of the companies mentioned herein or engage in any other transaction involving such securities

and earn brokerage or compensation or act as advisor or have other potential conflict of interest with respect to company/ies mentioned herein or

inconsistent with any recommendation and related information and opinions. Consortium Securities and affiliates may seek to provide or have

engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction to the companies referred to

in this report, as on the date of this report or in the past. Consortium Securities may have issued other reports that are inconsistent with and reach

different conclusion from the information presented in this report. Consortium Securities and affiliates may act upon or make use of information

contained in the report prior to the publication thereof.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state,

country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject

Consortium Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may

not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to

inform themselves of and to observe such restriction. This publication is not to be disseminated in the United States in any form or so ever.

Consortium Securities Inc accepts responsibility for its contents accordingly, though its accuracy and completeness cannot be guaranteed. Any person

receiving this report and wishing to effect a transaction in any security discussed herein must do so through Consortium Securities.

44Thank You!

You can also read